AGRIFOOD ATLAS Facts and figures about the corporations that control what we eat 2017 - Bund für Umwelt und Naturschutz Deutschland

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

AGRIFOOD ATLAS Facts and figures about the corporations that control what we eat 2017

IMPRINT The AGRIFOOD ATLAS is jointly published by Heinrich Böll Foundation, Berlin, Germany Rosa Luxemburg Foundation, Berlin, Germany Friends of the Earth Europe, Brussels, Belgium Chief executive editors: Christine Chemnitz, Heinrich Böll Foundation Benjamin Luig, Rosa Luxemburg Foundation Mute Schimpf, Friends of the Earth Europe Executive Editors of the German edition: Christian Rehmer, Reinhild Benning, Marita Wiggerthale Managing editor: Dietmar Bartz Art director: Ellen Stockmar English Editors: Paul Mundy, Oliver Mundy Proofreader: Maria Lanman Contributors: Christophe Alliot, Dietmar Bartz, Stanka Becheva, Reinhild Benning, Christine Chemnitz, Jennifer Clapp, Olivier de Schutter, Stephen Greenberg, Roman Herre, Saskia Hirtz, Nina Holland, Emile Frison, Benjamin Luig, Sylvian Ly, Elise Mills, Heike Moldenhauer, Sophia Murphy, Christine Pohl, Christian Rehmer, Shefali Sharma, Christoph Then, Jim Thomas, Jan Urhahn, Katrin Wenz, John Wilkinson Editorial responsibility (V. i. S. d. P.): Annette Maennel, Heinrich Böll Foundation This publication is written in international English. First English edition, October 2017 Produced by HDMH sprl, Brussels, Belgium This material is licensed under Creative Commons “Attribution-ShareAlike 4.0 Unported“ (CC BY-SA 4.0). For the licence agreement, see http://creativecommons.org/licenses/by-sa/4.0/legalcode, and a summary (not a substitute) at http://creativecommons.org/licenses/by-sa/4.0/deed.en. Cover-Copyright: image-background © Julien Eichinger/fotolia.com image-foreground © shironosov/istockphoto.com FOR ORDERS AND DOWNLOADS Heinrich-Böll-Stiftung, Schumannstraße 8, 10117 Berlin, Germany, www.boell.de/agrifood-atlas Rosa-Luxemburg-Stiftung, Franz-Mehring-Platz 1, 10243 Berlin, Germany, www.rosalux.org/agrifood-atlas Friends of the Earth Europe, Rue d’Edimbourg 26, 1050 Brussels, Belgium www.foeeurope.org/agrifood_atlas

AGRIFOOD ATLAS

Facts and figures about the corporations that control what we eat

2017TABLE OF CONTENTS

02 IMPRINT 18 FERTILIZERS

CHEMICALS FOR THE SOIL

06 INTRODUCTION Synthetic fertilizers increase agriculture’s

productivity, but do not improve soil quality.

Manufacturers want to sell more – despite the

high energy and environmental costs.

20 SEED AND PESTICIDES

FROM SEVEN TO FOUR –

GROWING BY SHRINKING

Mergers galore: Bayer wants to buy

08 INDEX Monsanto and become the world’s largest

THE CORPORATIONS MENTIONED producer of seeds and agrochemicals.

IN THE AGRIFOOD ATLAS All top rivaling companies are pairing up.

10 HISTORY 22 ANIMAL GENETICS

SUPERSIZE ME IN THE BEGINNING WAS

Whether protectionism or deregulation THE PATENT

– the agrifood industry keeps growing. Genetically modified livestock are prone

Mergers are making firms bigger all the to disease and are difficult to market.

way along the value chain. But many labs are developing methods to

further industrialize animal production.

12 MERGERS

ONE GROUP TO RULE THEM ALL 24 CROP GENETICS

A single private equity firm, 3G Capital JUGGLING GENES

from Brazil, controls some of the world’s In the coming years, seed companies plan

biggest food and beverage corporations. to use genome editing to produce crops

The company’s aggressive takeover with new characteristics – and market

strategy is just the tip of the iceberg. them without having to state that they are

“genetically modified”.

14 PLANTATIONS

MODERN-DAY LANDOWNERS 26 COMMODITIES

New corporations have emerged that buy or AGRICULTURAL TRADERS’

lease vast areas of farmland in developing SECOND HARVEST

countries. They grow monocultures to feed Four Western corporations dominate

the industrialized agriculture. the global trade of agricultural products.

Now a Chinese firm has joined them.

16 AGRICULTURAL TECHNOLOGY

DIGITAL MANOEUVRES – 28 MANUFACTURERS

WHEN TRACTORS GO ONLINE BRANDS DOMINATING MARKETS

Precision farming promises to revolutionize Fifty manufacturers account for 50 percent

farm management. But it will only benefit of global food sales in the industry. The

large landholdings and capital-intensive big companies are growing fastest and are

agro enterprises. rapidly increasing their market share.

4 AGRIFOOD ATLAS 201730 RETAILING 42 WORLD TRADE

EXPANDING AISLES IN CONTROL, NOT UNDER CONTROL

Food shoppers in the developed world let International trade deals reflect the

the cash registers ring at the likes of interests of the industry. Agrifood

Wal-Mart, Lidl, Carrefour and Tesco. The corporations want to keep a grip on

supermarket revolution is now expanding the steering wheel.

throughout the developing world.

44 EU LOBBYING

32 FEEDING THE WORLD BIG BUSINESS IN BRUSSELS

CHEMICAL SPRAYS, BUT HUNGER STAYS The crowds of industry lobbyists trying to

Industry says it can feed the world. But total infl uence European Union policy often

food production is not the issue; access to find they are pushing at an open door. They

food is. The key solution is to fight poverty. combine legitimate lobbying with underhand

methods such as hiring government

34 MEAT insiders and publishing quasi-scientifi c

HERD INSTINCT studies. The EU must recognize such tactics

They are largely unknown to the public, but for what they are.

they dominate the world’s meat supplies.

Much of the beef, pork and chicken we eat is 46 CHINA

controlled by just a handful of big firms. PUBLIC AND PRIVATE COMPANIES

ARE REACHING OUT

36 ALTERNATIVES The world’s new economic powerhouse

LOOKING FOR A NEW WAY is located in China. Its land investments in

Agroecology is a successful concept which Africa and Latin America have attracted

promotes farming methods that are headlines, but Southeast Asia is where it is

attuned to local ecosystems. It is already making its influence most felt.

used for growing rice worldwide.

48 RULES

38 CAPITAL MARKETS MARKET POWER AND HUMAN RIGHTS

INVESTORS CARE ABOUT GROWTH – Again and again, corporations fail to

NOT ABOUT THE GROWERS respect human rights. Voluntary measures

Speculators are increasingly placing are not enough: we need binding rules.

their bets on agriculture. Capital flows into

stock exchanges are exacerbating price 50 RESISTANCE

fluctuations in agricultural commodities PROTESTS, BOYCOTTS

– to the benefit of funds and banks. AND RESISTANCE

In many countries, people are resisting

40 WORKING CONDITIONS agrarian and trade policies that boost

PILE IT HIGH, SELL IT CHEAP the power of the multinationals. Individual

Labels on supermarket packaging trumpet companies also come in for criticism.

all kinds of concerns for people

and nature. But most have little impact

on the miserable conditions 52 AUTHORS AND SOURCES

endured by farm and plantation workers. FOR DATA AND GRAPHICS

AGRIFOOD ATLAS 2017 5INTRODUCTION

T

he contrast could hardly be greater.

The list of the world’s largest 500

companies by turnover contains a

„ The fight for market share

is achieved at the expense

of the weakest links in the chain:

huge number of firms engaged in farmers, and workers.

agriculture and food: firms that have

carved up big chunks of the sector among

themselves. At the same time, the sector protection does not necessarily depend on

is the basis of the livelihoods for many the size of a company. But in many

millions of farmers and farm workers who parts of the agrifood sector, individual

are among the poorest people in the world. corporations have gained so much market

sway that they have the ability to shape

The trend continues towards a further markets and policies. Conflicts usually

concentration of power. In the developing involve unequal power relations: between

world, the growth of the middle class agricultural, food and trade corporations

is changing tastes and diets. Demand for on the one hand, and farmers and farm

processed foods is sure to rise. The workers on the other. The gap between

declared aim of agriculture, chemicals their shares of revenues yawns ever wider.

and food corporations is to grab as Across the globe, inequality is increasing.

big a slice of the cake as possible, but

A

they have now been joined by banks, grifood corporations are driving

insurance companies and the information industrialization along the entire

technology industry. global value chain, from farm to

plate. Their purchasing and sales policies

Takeovers and mergers like Monsanto promote a form of agriculture that

by Bayer, Kraft with Heinz and Dow with revolves around productivity. The fight

DuPont are just the tip of the iceberg. for market share is achieved at the expense

A spate of corporate marriages is of the weakest links in the chain: farmers,

concentrating control at each link in the and workers. The price pressure exerted

value chain, from field to fork. The by supermarkets and food firms is a

biggest players are growing the fastest major cause of poor working conditions

and are pushing through their own and poverty further back in the chain.

interests and approaches. It also promotes the onward march of

industrial agriculture and its associated

When does big become too big? That is effects on the environment and climate.

not an easy question to answer. The loss of soil fertility and biodiversity,

Attention to ecological and social values marine pollution and the emission of

such as human rights, labour rights, greenhouse gases: all these are partly due

as well as climate and environmental to the spread of industrial farming.

6 AGRIFOOD ATLAS 2017Despite all this, a reorientation is still not

in sight – except in a few promising cases.

On the contrary, attempts to make binding

„ A growing number of

people are changing

their buying habits to recreate

rules on human rights, working conditions diversity in the value chain.

and the environment are routinely tor-

pedoed. A major reason lies in the power

relations described in this atlas. To push the value chain. But the current debate over

for the necessary political changes, we first new permits for glyphosate has shown

need to understand the business models that political institutions and the interests

and growth strategies of the corporations. of the industry are closely interwoven.

C A

itizens must be able to influence growing number of people are

food politics. But around the world, organizing themselves and

we see democratic freedoms being are changing their buying habits

restricted. In many of the countries in to recreate diversity in the value chain.

which our organizations are active, civil But that is not enough to end hunger

society is increasingly being discouraged, and poverty or to protect the environment.

censored and intimidated. Two trends The withdrawal of government from

coincide in the agrifood sector: ever-fewer economic intervention is a major cause of

corporations are taking control of an the colossal environmental and climate

ever-bigger market share and are gaining damage and the global injustice that

influence in many parts of the world. we see today. It is high time for a socially

At the same time, the opportunities for and politically oriented regulation

civil society and social movements of the agrifood industry. We hope that

to oppose such developments are being this atlas will stimulate a broad-based

restricted. social debate on this vital topic.

The megafusions that have been announced

in the seed and agrochemicals sector –

between Bayer and Monsanto, Dow

and DuPont and Syngenta and ChemChina

– must serve as a wake-up call. Politicians Barbara Unmüßig

and competition authorities must Heinrich Böll Foundation

come to grips with mergers that have social

Dagmar Enkelmann

and environmental effects in fields that are

Rosa Luxemburg Foundation

already concentrated in a few hands. They

must push ahead with competition law Jagoda Munic

reforms to prevent further concentration in Friends of the Earth Europe

AGRIFOOD ATLAS 2017 7INDEX

THE CORPORATIONS MENTIONED UNITED KINGDOM

IN THE AGRIFOOD ATLAS • Associated British • SABMiller 10/11,

Foods 28/29 12/13, 28/29

• BG 10/11 • Sainsbury 30/31

• CNH 16/17 • Shell, Royal Dutch

UNITED STATES • Compass Group Shell 10/11, 14/15

• 3G Capital 12/13, 28/29 • Intellia Therapeutics 48/49 • Tesco 10/11, 30/31,

• AB InBev 10/11, 12/13 24/25 CANADA • Envigo 22/23 48/49

• ADM cf. Archer Daniel • Intrexon 22/23 • Agrium 18/19 • Genus 22/23 • Unilever 10/11,

Midland • IT-DNA 24/25 • AquaBounty 22/23 • Hume Brophy 44/45 12/13, 28/29, 40/41,

• AGCO 16/17 • John Deere 10/11, 16/17, • Canpotex 18/19 • Oxitec 22/23 42/43, 44/45

• Allergan 10/11 24/25, 38/39 • Nutrien 18/19

• Alta Genetics 22/23 • Kellogg’s 40/41 • Potash 18/19

• Amazon 10/11 • Koch Foods 34/35 IRELAND

• Anheuser-Bush 12/13, • Kraft, Heinz, Kraft Heinz • Fyffe 50/51

28/29 10/11, 12/13, 28/29, • Actavis 10/11

• Anthem 10/11 40/41

• Archer Daniel Midland • Kroger 10/11, 30/31,

14/15, 18/19, 26/27, 48/49

FRANCE

28/29, 38/39 • Life Technologies 24/25

• Auchan 30/31,

• AT&T 10/11 • Mars 28/29

48/49

• Autodesk 24/25 • McDonald’s 10/11, 48/49

• Bigard Group 34/35

• BAT 10/11 • Microsoft 10/11, 24/25

• Carrefour 30/31,

• Berkshire Hathaway • Mondelez 12/13, 28/29

48/49

12/13, 28/29 • Monsanto 10/11, 12/13,

• Castel 12/13

• BlackRock 38/39 16/17, 20/21, 24/25, MEXICO

• Cellectis 24/25

• Bunge 18/19, 26/27, 34/35, 38/39, 42/43, • Industrias

• Danone 28/29

38/39 44/45 Bachoco 34/35

• Finatis 48/49

• Burger King 12/13 • Morgan Stanley 38/39

• Grimaud 22/23

• Cargill 10/11, 14/15, • Mosaic 18/19

• Groupe Doux

18/19, 26/27, 34/35, • Neogen 22/23

34/35

38/39, 42/43 • OSI 34/35

• ITM (Intermarché)

• Caribou Biosciences • PepsiCo 10/11, 12/13,

30/31

24/25 28/29, 40/41

• Lactalis 28/29

• CF Industries 18/19 • Perdue Foods 34/35

• Leclerc 30/31

• Charter 10/11 • Pfizer 10/11

ECUADOR • Sodexo 48/49

• Cibus Biotech 24/25 • Pilgrim‘s Pride 10/11

• Palmar 40/41

• Cigna 10/11 • Popeyes 12/13

• Reybanpac 40/41

• Citibank 38/39 • RBI 12/13 GHANA

• Climate 16/17 • Recombinetics 22/23 • Fan Milk 28/29

• Coca-Cola 10/11, 12/13, • Reynolds 10/11

28/29, 40/41, 44/45 • Sangamo BioSciences

• Costco 10/11, 12/13, 24/25

30/31 • See‘s Candies 12/13

• Dairy Queen 12/13 • Smithfield 10/11, 28/29,

• Dell 10/11 34/35 BRAZIL

• DirecTV 10/11 • Swift 10/11 • 3G Capital 12/13, 28/29

• Dow, Dow Chemical 10/11,• Target 30/31, 48/49 • Amaggi 14/15

20/21, 24/25, 44/45 • The Pampered Chef • AmBev 12/13

• DuPont 10/11, 16/17, 12/13 • Biosev 14/15

20/21, 24/25, 34/35 • Tim Hortons 12/13 • BRF 10/11, 34/35

• Editas Medicine 24/25 • Time Warner Cable 10/11 • Copersucar 14/15

• EMC 10/11 • Trans Ova Genetics 22/23 • Cosan 14/15

• FMC 20/21 • Twist Bioscience 24/25 ARGENTINA • Frangosul 34/35

• Gen 9 24/25 • Tyson Foods 28/29, • El Tejar 14/15 • Granol 14/15

• General Mills 28/29 34/35, 38/39 • InBev 12/13

• GenScript 24/25 • Verizon 10/11 • JBS 10/11, 28/29, 34/35

• Goldman Sachs 26/27, • ViaGen 22/23 • Marfrig 34/35

38/39 • Wal-Mart 10/11, 12/13, • Petrobras 14/15

• Heinz cf. Kraft 30/31, 48/49 • Raizen 14/15

• Hershey 12/13 • Wintergreen Research • Santelisa 14/15

• Hormel 34/35 16/17 • Vanguarda Agro 14/15

• IBM 10/11 • Wyeth 10/11

• Intel 24/25 • Zoetis 22/23

8 AGRIFOOD ATLAS 2017CHINA

• ChemChina 10/11, 20/21

• China Asean Resources 46/47

• China Minzhong Food 46/47

• COFCO 10/11, 26/27

• First Pacific 46/47

• IR Reources 46/47

NORWAY • Jiusan 14/15

• Yara 18/19 • New Hope 34/35

RUSSIA • Shandong Chenxi Group

• PhosAgro 18/19 14/15

• RIF 26/27 • Shanghui Group 34/35

SWEDEN/ • Uralkali 18/19 • Shuanghui Development

DENMARK 34/35

• Arla Foods 28/29 • Sinofert 18/19

• Smithfield cf. WH Group

• Wen‘s Food 34/35

UKRAINE • WH Group, Smithfield 10/11,

• Kernel Group 14/15 28/29, 34/35

• Yunnan Power Biological

Group 46/47

• Yurun Group 34/35

ITALY • ZTE 46/47

• CNH 16/17

ISRAEL JAPAN

• Fiat 16/17

• Adama 20/21 • Kubota

• ICL 18/19 16/17

• Nipponham

34/35

SWITZERLAND

• CRISPR Therapeutics SAUDI ARABIA INDIA

24/25 • Acolid 34/35 • Mahindra 16/17

• Glencore 26/27

• Tata 28/29

• Nestlé 10/11, 12/13, THAILAND

• UPL 20/21

28/29, 42/43, 44/45, • CP Group 34/35

48/49, 50/51

• Syngenta 10/11,

20/21, 24/25, 38/39, NETHERLANDS

44/45 • ABN Amro 10/11

MALAYSIA

• CNH 16/17

• Sime Darby 14/15

• CRV 22/23

• Hendrix Genetics

22/23 SINGAPORE

• Koepon 22/23 • Noble 10/11 INDONESIA

• Louis Dreyfus 14/15, • Olam 26/27 • Sinar Mas 14/15

18/19, 26/27, 38/39 • Wilmar 14/15

• Nidera 10/11 GERMANY

• RFS 10/11 • Aldi 30/31, 34/35

• Royal Dutch Shell, • BASF 16/17, 20/21,

Shell 10/11, 14/15 24/25, 44/45

• Topigs Norsvin 22/23 • Bayer 10/11, 16/17,

• Unilever 10/11, 12/13, 20/21, 24/25, 34/35,

28/29, 40/41, 42/43, 44/45

SOUTH AFRICA 44/45 • Claas 16/17

• Shoprite 30/31 • Vion Food 34/35 • Deutsche Bank 38/39

• Edeka 30/31, 34/35, AUSTRALIA

40/41, 48/49 • Nufarm 20/21

• JAB Holding 28/29

• K+S 18/19

• Metro 30/31

• Netto 34/35

BELGIUM • Ostfriesische Tee

• AB InBev, Anheuser-Busch Gesellschaft 28/29

InBev, InBev, Interbrew • Rewe 30/31, 34/35

10/11, 12/13 • Schwarz (Lidl, Kaufland)

30/31, 34/35, 40/41

• Teekanne 28/29

• Tönnies 34/35

• Westfleisch 34/35

AGRIFOOD ATLAS 2017 9HISTORY

SUPERSIZE ME

Whether protectionism or deregulation opment of new food preservation and transformation tech-

– the agrifood industry keeps growing. nologies to produce food and drink for urban consumption.

Mergers are making firms bigger all the In the 1930s, the development of hybridization made cross-

ing crop varieties or breeding lines possible. This led to the

way along the value chain.

emergence of companies that produced seeds and animal

breeding stock. Each of these industries had its own technol-

T

he global agrifood system can trace its origins back to ogies or marketing characteristics that created barriers to

the last quarter of the 19th century in Britain, which entry for new firms. Food retailing remained local and fami-

was then the world’s dominant commercial power. ly-based until the 1950s in the USA and the 1960s in Europe,

The first large agricultural corporations with a global reach when self-service supermarket chains emerged.

emerged for a range of reasons, both technological and With the rise in protectionism and the decline of trade in

institutional. Farm work was mechanized; agrochemicals the first half of the 20th century, big firms in the USA and Eu-

were invented and marketed; trains, ships and ports revo- rope turned themselves into transnational corporations by

lutionized transport; and new technologies improved the investing in other countries, rather than just exporting their

preservation and storage of food. Free trade removed tariff products there. Oligopolies, in which a few actors determine

barriers, and futures markets overcame capital shortages what happens, emerged at various stages along the value

by selling crops even before the seed had been put in the chain.

ground. This process accelerated with the US-led reconstruction

From the point of view of farm production, these corpo- programmes in Europe after the Second World War, and

rations could be roughly divided into upstream and down- was reinforced by the emergence of new types of products:

stream firms. Upstream firms supplied farm machinery and fast food, snacks and drinks. The upstream machinery and

chemicals to large estates in Europe and big commercial agrochemicals firms, along with the newly created seed in-

family farms in the Americas. Downstream firms focused dustry, paved the way for the industrialization of agriculture

either on trading and primary processing, or on the devel- in Europe. Food aid and the Green Revolution, with its reli-

ance on seed, fertilizers, pesticides and machinery, enabled

these firms to spread in Asia and Latin America.

Post-war economic growth and rising incomes led to a

WHERE CORPORATIONS WORK

shift in diets. Food options expanded. According to Engel’s

Major areas of activity in the agrifood industry,

schematic diagram law, as income rises the proportion of income spent on food

falls. Companies responded to this potential loss of turnover

Finance Investment Insurance Information

by launching new, more expensive, products and by inten-

sifying their marketing. The family grocer gave way to su-

permarkets, and giant retailers exerted their influence both

Machinery Land Water backwards along the agrifood chain to processors and farm-

Seed Pesticides Fertilizer ers, and forwards with consumers. Health and fitness con-

cerns created demand for fresh products such as vegetables,

Breeding lines Veterinary Feed fruit and fish, which came to be organized under the direct

control of the retailers.

In the 1980s, the transnational crop companies increas-

Agricultural

ingly became global players with interests around the

production

world. In developing countries, liberalization dismantled

Energy state controls over commodity markets and tariff barriers,

production Commodity trading leading to a rapid expansion of global trade in foodstuffs.

and transport

Chemicals Big retailers began organizing new supply chains to source

fresh produce from developing countries. They also expand-

Food production ed in the larger countries in the developing world to serve

and processing the needs of the new middle classes there.

A handful of global corporations now organizes the

world’s agriculture and food-consumption patterns. They

Wholesale, retail Gastronomy are remarkably long-lived: many of today’s leaders were

AGRIFOOD ATLAS 2017

Consumption

It’s a long way from field to plate.

Information: weather, markets, farm management Farmers are the most

vulnerable link in the chain

10 AGRIFOOD ATLAS 2017THE BIGGEST MERGERS OF THE LAST DECADE

Timeline, by sector and transaction value in billion US dollars (controlled for inflation, base year 2016),

publicly traded companies only, includes announcements

agrochemicals,

food, drinks,

132 130 tobacco

finance, oil,

Verizon 117 Dow/ pharmaceuticals,

112 (Share purchase,

DuPont technology

technology)

(Agrochemicals)

AB InBev/ 100

ABN Amro/ SABMiller

RFS (Drinks)

(Finance) Heinz/ 85

79 Kraft

75 (Food) AT&T/

70 71

Charter/ 67 Time 66

Pfizer/ Time Warner

57 Wyeth Warner (Technology)

Royal Actavis/ Bayer/

(Pharmaceuticals) Cable

Dutch 47 49 Allergan 47 Monsanto

(Technology) (Pharmaceuticals) (Agrochemicals)

InBev/ Shell/

BG Dell/

AGRIFOOD ATLAS 2017 / AM ARCHIVES

Anheuser-Busch AT&T/

(Drinks) (Oil) Anthem/ EMC BAT/

Cigna DirecTV (Technology) Reynolds

(Finance) (Technology)

(Tobacco)

2007 2008 2009 2013 2015 2016

Mergers in the agrifood

founders of the modern agrifood system, such as Cargill industry are just as big as in other

(grain trader), John Deere (farm machinery), Unilever (pro- sectors of the economy

cessed food, and plantation production in the past), Nestlé

(dairy and chocolate), McDonald’s (fast food), Coca-Cola

(fizzy drinks). Two developments – the shift towards finance the wider world. They must begin to address issues such

capital and the impact of biotechnologies – have led to a as hunger, climate change, waste, sustainability, health

wave of mergers and acquisitions since the 1980s, changing and disease, as well as social justice. These concerns have

the face of the sector. been highlighted by social movements, international con-

In the last 20 years, much of the action has shifted to the ventions and civil society organizations. These organiza-

developing world and to Asia, especially China, which has tions and institutions are now exerting more pressure than

become the leading market for commodities. New global ever on the global corporations, demanding changes in the

players are emerging. Two Brazilian firms are now world production approaches, marketing methods and purchas-

leaders in the meat sector. BRF (formely Brasil Foods) has ing practices, which the latter have used over the last 150

expanded in Argentina, the Middle East and Thailand. JBS years.

has snapped up Swift, Pilgrim’s Pride and part of Smithfield

Foods, three of the largest US meat producers. Chinese state-

owned companies are also getting in on the act. ChemChi-

AGRIFOOD ATLAS 2017 / FILE

THE BIGGEST AGRO AND FOOD CORPORATIONS

na is acquiring Syngenta, a Swiss agrochemicals and seeds

Headquarters of companies with the highest turnover, 2015

business. COFCO, the China National Cereals, Oils and Food-

stuffs Corporation, has bought two commodity traders: industry trade

Singapore-based Noble and the Dutch firm Nidera. Mean-

3 Costco

while, global trade is once again leaning towards protec- 5 Tesco

2 Cargill Welwyn Garden

tionism. City

At the same time, the digital revolution and biotechnol- Issaquah

4 Kroger Brussels

Minnetonka Purchase Vevey 5 Anheuser-Busch InBev

ogy are redefining the sector and result in the emergence of Cincinnati

Atlanta 2 PepsiCo

new external players. Big data and intelligent vehicles are Bentonville 1 Nestlé

4 Coca-Cola

making farm production and food retailing attractive for

the likes of IBM, Microsoft and Amazon. 1 Wal-Mart

Despite their all-embracing power, the food majors have

so far paid little attention to the impact of their actions on São Paulo

3 JBS

Only one of the top five agrifood trade

and industrial firms comes from the developing Industry: only turnover with agricutural products and foods; Trade: including non-food

world: a meat producer from Brazil

AGRIFOOD ATLAS 2017 11MERGERS

ONE GROUP TO RULE THEM ALL

A single private equity firm, 3G Capital In 2010, 3G acquired Burger King, along with its out-

from Brazil, controls some of the world’s standing debt, for US$4 billion. Around one-third of Burger

biggest food and beverage corporations. King was owned by another private equity consortium and

around two-thirds were floated to the public. Part of the

The company’s aggressive takeover

new business model was a “refranchising initiative”: before

strategy is just the tip of the iceberg. 2010, out of more than 13,000 restaurants, 1,344 were still

company-owned. By 2013, only 52 were.

L

arge-scale takeovers in the food and beverage indus- In 2013, 3G Capital joined forces with Warren Buffett’s

try are nothing new. Mirroring trends in other sectors, Berkshire Hathaway and bought the food giant Heinz. Two

in the late 1980s and the 1990s corporations such as years later, in 2015, Heinz acquired Kraft Foods Group for

Nestlé and Kraft diversified their control over brands by US$62 billion to form Kraft Heinz, the world’s fifth-largest

making acquisitions in various markets. Since the end of food and beverage company, with revenues of US$6.6 billion

the 1990s, financial investors began exerting a strong influ- in 2016. The motives for this merger are symptomatic for the

ence on mergers and acquisitions in the food and beverage whole wave of mergers in recent years: while Heinz had a

sector. Firms were urged to focus on their core brands and strong global foothold with 61 percent of its sales outside

industries, and to make vertical and horizontal acquisitions North America, Kraft Foods generated 98 percent of its sales

within the same subsector. in North America. At the time of the merger, Kraft had a very

Profit maximization, rather than expansion, became the good credit rating, which made it easy for 3G and Berkshire

key objective. Instead of accumulating capital to expand to refinance its debt. The management announced cost sav-

a firm’s operations, financial investors demanded that it ings arising from synergies and rationalisation of logistic

channel its cash flow into dividend payouts and share buy- structures, which amounted to US$1.5 billion per year for

backs, giving financial investors (and not the firm itself) the the first three years. This rationalization resulted in the loss

flexibility to diversify their investments. Both institutional of around 5,000 jobs. In the USA and Canada, one-fifth of 41

investors and leading market analysts now wanted acquisi- processing plants were closed.

tions to be “leveraged” – to be based on debt. Since the early Two years later, in February 2017, 3G attempted, through

2000s, all major acquisitions in the food and beverage sec- Kraft Heinz, a takeover of its much larger rival Unilever for

tor have been justified using the pretext of increasing short- US$143 billion. The offer was rejected. In 2016, Mondelez, a

term shareholder value. snack-and-confectionery maker spun off from Kraft in 2012,

One of the most prominent private equity firms that has failed to take over Hershey, a US chocolate maker. These fail-

fundamentally restructured a number of corporations is 3G ures have increased the likelihood of Mondelez being reab-

Capital. Founded in 2004 by Jorge Paulo Lemann and part- sorbed into Kraft Heinz.

ners, 3G is headquartered in New York and has offices in Rio

de Janeiro and São Paulo. Before founding 3G, Lemann and

his partners laid the foundation of their wealth through in- Snack producers – high-growth companies

vestments and acquisitions that resulted in the formation of in 2016 – became expensive buys

the Brazilian beer giant, Ambev. while slow-growth retailers were cheaper

AGRIFOOD ATLAS 2017 / IMAP

INVESTORS’ ACTIVITIES, CLOSELY EXAMINED

Mergers and acquisitions activity Deals by financial and Public food and beverages companies by earnings multiples,

in the United States, number of transactions strategic buyers, 2016, selected product groups

in the food & beverages sector in percent

Earnings multiples*

20x snacks

financial

305

potentially

overrvalued

300 investors 18x

283

261 268

249 16x beverages

239

29.7

210 14x

undervalued

70.3 12x alcoholic beverages

potentially

10x distributors

strategic

investors 8x

2016

* Earnings (before interest, tax, depreciation and amortization) multiples define the

2009 2010 2011 2012 2013 2014 2015 2016 assumed value of a company by financial investors in relation to annual income

12 AGRIFOOD ATLAS 2017AN INVESTOR’S AGRIFOOD PORTFOLIO

Warren Buffett’s Berkshire Hathaway Inc. food-related holdings as of June 30, 2017,

percent of shares and value in million US Dollars

Coca-Cola 9.4 %

18,024

retail chemicals

food and beverages restaurants

543

Restaurant Brands Int. 3.6 %

320*

Costco 1.0 %

The Pampered Chef 100 %

720

410*

See’s Candies 100 % Monsanto 1.8 %

Kraft Heinz 26.7 %

964

25,400

4,100* 110

Wal-Mart 0.05 %

AGRIFOOD ATLAS 2017 / CNBC

Dairy Queen 100 %

23

* diamonds: total sales or revenues of other food-related

Mondelez 0.04 %

firms owned by Berkshire Hathaway, 2014–16

Warren Buffett is the world’s largest

3G has followed a similarly aggressive strategy in the private investor and a key player

beverage sector. Through successive mergers in 2004 and in acquiring and merging companies

2008, Ambev together with Interbrew from Belgium and

Anheuser-Busch from the USA formed AB Inbev, the largest

brewing company in the world. In 2015, AB InBev took over ally, including Budweiser, Corona, Stella Artois, Becks and

SABMiller. The resulting company has 25 percent of global Jupiler. The SABMiller takeover is the likely end of AB InBev’s

beer sales and 45 percent of the sector’s profit. merger activity in beer because of the risk of being blocked

Again, a key motivation has been to drastically cut oper- by antitrust regulators. Options may include diversifying

ating costs by creating a global giant. AB Inbev plans to cut into other alcoholic beverages (e.g. wine through Castel in

5,500 jobs in this process. Together, AB Inbev and SABMiller France) or into soft drinks (e.g., PepsiCo or Coca-Cola).

control seven of the ten most important beer brands glob- However, 3G’s aggressive takeover strategy is just the

tip of the iceberg. Almost all large food companies have

launched their own venture capital arms in recent years,

After failing to acquire Unilever, the world’s investing in smaller, upcoming brands. Aggressive take-

largest consumer goods company, in 2017, overs, pushed by venture capital, have become the status

3G is said to be looking for other targets quo. AGRIFOOD ATLAS 2017 / MEDIA REPORTS

HUNGRY, THIRSTY, GREEDY

Mergers and aquisitions led or accompanied by 3G Capital and its partners including Berkshire Hathaway

2004 AmBev 2008 InBev purchased

merged with 2015 AB InBev world’s largest

Anheuser-Bush to form

Interbrew to merged with SABMiller beer company

AB InBev

form InBev

2014 Tim Hortons purchased

world’s third-largest

2010 Burger King and merged with Burger King 2017 Popeyes

fast food restaurants

purchased to form Restaurant Brands added to RBI

operator

International (RBI)

2015 Kraft purchased

world’s fifth-largest

2013 Heinz purchased and merged with Heinz

food processor

to form Kraft Heinz

AGRIFOOD ATLAS 2017 13PLANTATIONS

MODERN-DAY LANDOWNERS

New corporations have emerged that buy or more profitable downstream activities. The traditional ap-

lease vast areas of farmland in developing proach of producing on plantations seemed less lucrative.

countries. They grow monocultures to feed Since the end of the 20th century, there has been a dra-

matic increase in the area used to cultivate oil palm, maize,

the industrialized agriculture.

sugarcane and soybeans. These four crops are used not only

as food, but also as animal feed, biofuel and industrial feed-

F

rom the start of the colonial era in the 16th century, stock, earning them the moniker “flex crops”.

globalization was driven by European powers in their The production of oil palm is closely linked to rapid de-

search for cheap labour and slaves. Trading compa- velopment in Southeast Asia. Agricultural concerns from

nies established plantations to produce food and industrial Malaysia, Singapore and Indonesia dominate the market.

raw materials for the rapidly growing cities of Europe. This They both supply raw materials to Western industries and

changed in the second half of the 20th century. As Asian and cater to the enormous demand in their home countries.

African countries gained their independence in the 1950s The Malaysian state-owned company Sime Darby was

and 1960s, Western corporations reduced their activities created through the nationalization of British colonial com-

there. Many pulled out of direct primary production in the panies. It first expanded to Indonesia and Papua New Guin-

1980s, but maintained control of the sector through con- ea and is now also active in Liberia and Cameroon. Sime Dar-

tract farming, as in the case of banana cultivation in Central by controls nearly a million hectares around the world. The

America or tea growing in India. They focused instead on Singaporean firm Wilmar is the world’s leading producer

of cooking oil. Robert Kuok, billionaire and majority share-

holder, is often called the “King of Cooking Oil”. His com-

pany cultivates over 200,000 hectares worldwide, mostly in

BEFORE AND AFTER

Malaysia and Indonesia, and controls parts of the processing

Land use changes as a result of international investment

1,004 deals made between 2000 and 2016 in the Land Matrix Register, industry. Another major player is the Widjaja family. It con-

Figures in percent trols the Indonesian company Sinar Mas, which owns over

100,000 hectares.

Land use before acquisition The sugarcane sector is structured in a similar way. In

Brazil, seven joint ventures between Brazilian capital and

10 Western commodity corporations control 50 percent of the

5

arable

sugar mills. The Brazilian side belongs mostly to associations

forests of family enterprises whose wealth is based on the owner-

27 shrubs, pasture ship of vast tracts of land.

58 marginal land The Copersucar corporation, which in 2014 created a

joint venture with the US agricultural giant Cargill, owns

47 sugar mills and controls another 50 through contracts.

Raízen is another joint venture formed by the Cosan cor-

Production target at acquisition

poration with the mineral-oil company Shell; Biosev is a

partnership between Santelisa with Louis Dreyfus Compa-

23 21 agrofuels ny, one of Cargill’s competitors. Sugarcane plantations are

food expanding worldwide, but nowhere as fast as in Brazil. The

livestock cultivated area doubled between 2005 and 2013 from five to

9 other agricultural ten million hectares.

products (non-food)

9 In contrast to oil palm and sugarcane, large soybean

38 not specified

producers focus mainly on production, not processing. The

Argentinean grain-and-meat producer El Tejar controls

700,000 hectares in Brazil, Argentina, Paraguay, Bolivia

Land use after acquisition

and Uruguay through leases and contract farming. Amaggi

oilseeds owns 200,000 hectares of land on which soy is grown. Blairo

17

cereals Maggi, the head of the company, is the former governor of

AGRIFOOD ATLAS 2017 / LAND MATRIX

3 sugarcane the Brazilian state of Mato Grosso and the current Minister

3 44 trees

3 of Agriculture of Brazil.

beverage and

10 spice crops

roots and tubers

20

other Shifting land use to livestock and

industrial crops increases the risk of

regional and national food insecurity

14 AGRIFOOD ATLAS 2017AGRIFOOD ATLAS 2017 / LAND MATRIX

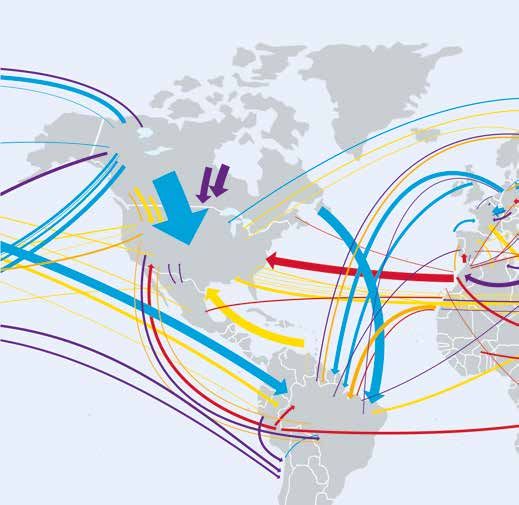

GRABBING ACRES

The 20 largest countries of origin and destination for land acquisition by international investors, noted in the Land

Matrix register, area in million ha

origin and destination countries for investments tax haven

Russia

Ukraine

2.4

2.4

1.3

0.6 1.8

Netherlands

Canada United Kingdom 0.5

0.5 0.4 Kazakhstan 1.0

3.3 0.6 0.5

Jersey Cambodia

0.5 China

USA France South Korea

Cyprus 0.7

Morocco Luxembourg 1.4 Laos Papua

0.7 New Guinea

Saudi-

0.7 1.1

Sudan Arabia 1.3 0.4 2.3

British Sierra Leone Hong Kong

0.5 Ethiopia India

Virgin Islands 0.6

South Sudan 1.0

Liberia

0.3 Ghana 0.7 3.7 Indonesia

0.6

Brazil 0.8 Rep. Congo Malaysia 3.0

1.6

Madagascar

2.0 0.7 Singapore

0.6

Paraguay

Zambia Mozambique

0.5

0.5

0.5

0.8 0.4 South Africa

Argentina 1.1

Comparison: 3.1 2.6 1.1

Belgium Rwanda Jamaica

Land acquisitions to produce for the world

Various corporations compete to control the production market are booming in Eastern Europe,

of feed and biodiesel from oilseeds. These include Brazilian South America, Southeast Asia and Africa

corporations such as the state-owned Petrobras and private-

ly held Vanguarda Agro and Granol, Western commodity

traders such as Archer Daniels Midland and Cargill, as well These firms contribute to the economic growth of

as importers such as the state-controlled Jiusan and the pri- emerging countries. They control vast areas of farmland;

vate Shandong Chenxi Group from China, the leading im- many have been criticized for grabbing land. They bene-

porting country. fit from cheap labour and new technology. Many holdings

The main maize-growing areas present a mixed picture. are in family ownership, while others are listed on the stock

In the Midwest of the United States, ethanol production exchange, and a few are state owned. By and large they act

from maize has increased steadily over the last 20 years. To- discreetly and opaquely. The workforce of sugarcane and

day maize is grown on 40 million hectares in the USA, main- oil palm plantations face colonial-style working conditions:

ly by family farms that use modern technology to cultivate they are paid piece-wages, and safety standards are low.

large areas. States play a central role in promoting the flex crop in-

But US producers are increasingly facing competition dustry. Politicians decide to sell or lease state-owned land

from Eastern Europe, mainly from Ukraine, Russia and and whether to finance transport infrastructure. Produc-

Kazakhstan. Ukraine is the third-largest wheat producer tion and processing plants are often subsidized. Quotas for

worldwide. The Kiev-based Kernel Group is a large and fast bio-fuels push up demand, sales and earnings of these crops.

growing producer and exporter of grain and sunflower oil Plantation corporations are modern, financially strong

from Ukraine and Russia. In 2017, it became Ukraine‘s larg- actors that are transforming agriculture into agro-indus-

est land user with a land bank of 700.000 hectares, a quarter try. We can no longer see them as mere relicts of colonial-

of the country‘s 2.8 million hectares of agricultural land. ism.

AGRIFOOD ATLAS 2017 15AGRICULTURAL TECHNOLOGY

DIGITAL MANOEUVRES –

WHEN TRACTORS GO ONLINE

Precision farming promises to revolutionize have bought up smaller competitors and maintained their

farm management. But it will only benefit brands. The global market is dominated by three players.

large landholdings and capital-intensive The US corporation Deere & Company is the market leader;

it is known for its biggest brand, John Deere. CNH Industri-

agro enterprises.

al belongs to the Fiat group; its twelve brands include Case,

New Holland, Steyr, Magirus and Iveco. The third-largest

T

he market for agricultural machinery and technology player is the US company AGCO, with Gleaner, Deutz-Fahr,

is huge. With a worldwide turnover of $US 137 bil- Fendt and Massey Ferguson. These three corporations share

lion, 2013 was the best year ever for the sector. Since more than 50 percent of the global market. Deere alone had

then, the sales of tractors, balers, milking machines, feed- a turnover of $US 29 billion in 2015: higher than the com-

ing equipment and other technical gear have been falling. bined seed and pesticide sales of Monsanto and Bayer.

In 2015 the turnover dropped to $US 112 billion. A further Market consolidation is not the only trend in the farm

decline is expected in 2016. An immediate recovery is un- equipment sector. The digitalization of agricultural pro-

certain. duction is still at an early stage, but is developing quickly.

There are several reasons for the recession. Low prices for Sensors measure milk production, livestock movements

agricultural products around the world depress investment. and feed rations. Quality assessments are performed online

The European and North American markets are saturated. during milking instead of afterwards in a laboratory. In crop

The number of farms is decreasing, especially in animal pro- farming, digitalization (known as “precision farming”) op-

duction. The area used for farming is shrinking and fewer timizes operations, saving money and resources and maxi-

subsidies are being paid out. mizing yields.

China and India remain the most attractive markets. Chi- Tractors are steered by GPS; apps provide data about soil

nese agriculture is regulated by the government. State poli- quality to planters via wireless networks, and calculate op-

cies have boosted the percentage of work done by machines timal sowing patterns and planting distances. Drones could

in the past 15 years from 34 percent in 2005 to 61 percent take over the spraying of pesticides. Information technology

in 2014. India’s market is not yet as advanced. The industry enables digital “farm management systems” to access data-

hopes that the government will modify its agricultural poli- bases and combine soil-quality data with weather forecasts.

cies to encourage equipment sales. Producers plan to sell half Control over this technology is concentrated in the hands of

of all tractors worldwide in these two countries by 2020. Asia a few corporations.

will then account for over 40 percent of the global market. Digitalization is opening up new markets for agrotech

A few large corporations share the equipment market companies. New joint ventures and acquisitions already

amongst themselves. Instead of growing organically, they point towards this trend. AGCO and the pesticide producer

DuPont announced in 2014 that they would work together

on data transmission. In the same year, CNH and Monsan-

to’s “Climate Corporation” division signed a contract to

TOP 6 AGROTECH CORPORATIONS

develop precision planting technologies. Deere and the

Headquarters of the leading enterprises in 2016

Climate Corporation have agreed to give Deere’s farm man-

publicly traded private or family enterprise agement system permission to access the large datasets of

the Climate Corporation. AGCO and the chemical company

5 Claas BASF have also formed a partnership to develop their own

1 Deere 4 Kubota farm management system.

Amsterdam

London

Harsewinkel

CNH introduced self-driving tractors in 2016. Sensors

Moline

Duluth Osaka guide the vehicle, making a driver’s cab unnecessary. They

2 CNH are among the first “agricultural robots”: machines that

Mumbai

plough, sow, spray, prune, milk, shear and harvest. The US

3 AGCO consulting firm Wintergreen Research estimates that the

AGRIFOOD ATLAS 2017 / AM ARCHIVES

global market for these technologies will grow from $US

6 Mahindra 1.7 billion in 2016 to $US 27 billion in 2023. However, Win-

Some dominant producers sell

equipment under their own brand names.

Others have several brands

16 AGRIFOOD ATLAS 2017HEAVY MACHINERY IN A LIGHT MARKET

Declines in food prices and turnover in agrotechnology

Global world market shares of agrotech by region

Agrotech development compared with the previous year in percent and countries, average 2012–14 in percent

25 325 EU USA Russia China Brazil EU

Nafta * 17

China 26

20 300 6

South America

India 6

15 275 CIS **

8 22

other

* USA, Canada, Mexico 15

10 250 ** Mainly Russia

5 225

0 200 2012 2013 2014 2015

-5 175

-10 150

AGRIFOOD ATLAS 2017 / AMIS, VDMA

Price indices for cereals and edible oils of UN Food

and Agriculture Organization (2002/04 =100)

-15 125

index for cereals index for oils

-20 100

2012 2013 2014 2015 2016

The recession in the sector is expected to last

tergreen expects the price of the equipment to fall once it is until 2018. But these corporations refrain from

produced on a large scale. talking about a crisis so as not to appear weak

While a boom in the sector will generate employment

in equipment production, servicing and software, it will

reduce the number of jobs in animal production and in la- AGCO expects consortia to form around Deere and Claas,

bour-intensive aspects of crop farming. The developers aim a German tractor-maker. The ETC Group, a non-governmen-

to reduce labour costs and drudgery, and enable farmers to tal organization based in the USA, anticipates a takeover of

become independent of working hours. Image-recognition the seed and pesticide industry by agrotech corporations

techniques are advancing quickly, allowing computers to due to their financial power. This would increase their con-

detect if fruit and vegetables are ripe for harvest and which trol over farms and our food even further.

ones to pick. Manufacturers promise that unlike human

workers, their machines can work day and night without

errors. For cost reasons, humans can only pass through a

AGRIFOOD ATLAS 2017 / AG WEB

MAKING MACHINES FOR FARM AND FIELD

field once or twice to harvest it; machines can do so contin-

Turnover of the largest corporations, by size,

uously. in billion US dollars, 2014

Hopes exist that the digitalization of agriculture can help

combat climate change. Sensors could calculate soil carbon 35

stocks and farmers could earn money by selling the stocks

30 agrotech

on the emission offsets market. That would pave the way for other

larger-scale industrial agriculture but it would leave the en- 25

vironmental problems unsolved. Such techniques could be

used only by large, capital-intensive farming enterprises in 20

the developed world. Farms not only have to expand but will

also have to digitalize to remain profitable. The notion “up 15

or out” will change to “digitalize or out”. Structural changes

10

in agriculture will continue to make workers redundant.

5

Some experts speculate that producers 0

will buy up competitors to stay Deere CHN AGCO Kubota Claas Mahindra

competitive with the market leader, Deere

AGRIFOOD ATLAS 2017 17FERTILIZERS

CHEMICALS FOR THE SOIL

Synthetic fertilizers increase agriculture’s groups and fertilizer corporations co-founded the Global Al-

productivity, but do not improve soil quality. liance for Climate-Smart Agriculture. The aim of this alliance

Manufacturers want to sell more – despite the is to increase productivity by using fertilizers, pesticides and

improved seed. It also wants to include carbon sequestration

high energy and environmental costs.

in soils in international emissions trading.

However, measuring the carbon stock is difficult. And

S

oil fertility is of central importance to farmers. They the prospect of making money with sequestration would

fertilize their fields to replenish the nutrients re- give farmers the wrong incentives. It might promote un-

moved through the harvest. The three main nutrients, sustainable cultivation methods and land speculation that

nitrogen, phosphorus and potassium, are found in manure, would threaten fundamental goods: food security, soil fer-

chicken droppings, crop residues and other materials of tility and biological diversity.

animal or vegetable origin. Mineral fertilizers also contain The production of artificial fertilizers is extremely energy

them, but their sources are different: phosphorus and potas- intensive, which means that their prices are tied to gas and

sium are mined from rock. Synthetic nitrogen is produced oil prices. Synthetic nitrogen is produced mainly in North

through a chemical process. America, India, China, Russia, the Middle East, Australia and

The invention of mineral fertilizers made possible the Indonesia. Eighty percent of the potassium comes from Can-

industrialization of agriculture first in Europe and North ada, Israel, Russia, Belarus and Germany. Rock phosphate is

America, then in developing countries. The Green Revolu- extracted in opencast mines: more than 75 percent of the

tion introduced Western agricultural practices to other re- world’s reserves are located in Morocco and in the Moroc-

gions. A billion-dollar fertilizer business has emerged. The can-occupied Western Sahara.

industry proudly points to rising yields but ignores the nega- Since 1961, the consumption of artificial fertilizers has

tive impacts on soils, climate and environment. increased sixfold, and in 2013, world sales totalled US$ 175

Corporations are trying to turn the international de- billion. Manufacturers, especially of phosphate and potash,

bate surrounding “climate-smart agriculture” (CSA) to their dominate certain geographic markets or sectors and act as

advantage. The Food and Agriculture Organization of the monopolists. The biggest players are Agrium in Canada,

United Nations (FAO) introduced this concept in 2010. Its Yara in Norway and the Mosaic Company in the USA. They

idea was to link agriculture, food security and climate pro- operate their own mines and factories; together they ac-

tection. Selected practices adapted to local climate, and soil count for 21 percent of the global fertilizer market.

conditions were supposed to make smallholder farms more For the period 2015–20, FAO expects artificial fertilizer

productive and boost humus formation. The idea is to adapt deliveries to rise from 246 to 273 million tonnes. The latter

agriculture to climate change and promote carbon seques- includes 171 million tonnes of nitrogen fertilizer and about

tration in soils, especially in developing countries. 50 million each of phosphate and potash. The industry ex-

But the original idea changed quickly. In 2014, FAO, pects uneven growth in this period. Africa is expected to

the World Bank and several governments, as well as lobby have the strongest annual growth rate, at 3.6 percent, fol-

lowed by Latin America, South Asia, and the successor states

of the Soviet Union.

China’s demand for fertilizer is plateauing. In 2015, the

AGRIFOOD ATLAS 2017 / SOIL ATLAS

THE FERTILIZER TOP 10

government decided to limit the country’s fertilizer use to

Headquarters of firms with the biggest turnover, 2015

one percent a year. By 2020/21, markets in 50 percent of

publicly listed state-owned private the global market – China, North America, Western Europe

and Australia – will be saturated, with sales growing weakly

1 Agrium 2 Yara 8 PhosAgro or shrinking. But if these regions import more feed and food,

4 Potash 9 Uralkali for example from Brazil, they will be outsourcing agricultur-

Calgary Oslo Moscow Beresniki

Saskatoon Kassel al production as well as fertilizer usage.

Plymouth

Deerfield

Tel Aviv

Peking Multinational agricultural trading groups such as Arch-

3 Mosaic

10 K+S 6 Sinofert er Daniels Midland, Bunge, Cargill and Louis Dreyfus Com-

7 ICL pany have reduced their investments because of the low

growth prospects. At the same time, the big players are

5 CF Industries

buying up their competitors. The Canadian PotashCorp,

world’s #4, holds shares of Sinofert (#6) from China and ICL

In 2018, a new leader will dominate the fertilizer

ICL and K+S: only fertilizer sales top 10 when the merger between Agrium and Potash

is completed and its name is changed to Nutrien

18 AGRIFOOD ATLAS 2017AGRIFOOD ATLAS 2017 / ICIS, FAO

BY LAND AND BY SEA

World transport routes of artificial fertilizers, flows over 300,000 tonnes, 2013

potassium Sales by region in millions of tonnes, 2014

phosphate

nitrogen-phosphate

compounds

nitrogen 22.3 15.4 3.9 1.8 67.6

sulphur

11.8 3.8 1.5 1.4 23.4

11.5 4.1 0.6 0.4 15.2

Americas Europe Africa Oceania Asia

Nitrogen-phosphate compound fertilizers separated into nitrogen and phosphate, without sulphur-containing fertilizers

Potassium and phosphate deposits, as well as

(#7) from Israel. Norwegian Yara, the world‘s second largest the natural gas used to produce nitrogen fertilizer, are

fertilizer producer, has acquired holdings in Brazil and the unevenly distributed. That steers international trade

USA. Yara also plans to expand its business in Africa by pro-

moting large-scale, industrial agriculture and participating

in public–private partnerships such as the New Alliance for heavy metals are leached out of the heaps. For cost reasons,

Food Security and Nutrition in Africa. K+S refuses to bring the tailings back into the mine. Howev-

The four largest companies control more than half of the er, regional politicians have celebrated a minor success: K+S

production in all major producer countries except China. says it will reduce the discharges by half by 2027.

In North America, three big companies dominate the pot-

ash sector: Agrium (the world’s number one), Mosaic and

PotashCorp. They work together in a cartel and distribute

INTENSIVE FARMING

their products through a joint company, Canpotex. Some

Fertilizer use by country, kilograms per hectare

countries such as Hungary and Norway have only one ferti- arable land, 2013

202

lizer company. Indonesia

In Germany, nitrogen usage has increased by two-and-

China

a-half times and the usage of agricultural lime by half since

1961. Germany is dependent on imports: 66 percent of its

140

nitrogen and 94 percent of its phosphate come from abroad.

Domestic potassium is abundant. K+S is one of the world‘s

largest manufacturers. Fertilizers account for half of this

firm’s turnover of € 3.8 billion. Good for K+S, bad for the en-

557 USA

vironment. The firm discharges effluent into the river Werra

204

615

or injects it into the ground. Salt that cannot be sold is piled

AGRIFOOD ATLAS 2017 / WELTBANK

into large heaps. The groundwater is contaminated, and India

Germany

158 Egypt

In many parts of world, the overuse

of fertilizers acidifies soils and pollutes

groundwater, lakes and rivers

AGRIFOOD ATLAS 2017 19SEED AND PESTICIDES

FROM SEVEN TO FOUR –

GROWING BY SHRINKING

Mergers galore: Bayer wants to buy figure, US$ 43 billion, for Syngenta. Along with Syngenta’s

Monsanto and become the world’s largest pesticide and seed production, ChemChina, already a pro-

producer of seeds and agrochemicals. ducer of non-patented chemicals, will gain an enormous

amount of knowledge on genetic engineering despite re-

All top rivaling companies are pairing up.

sistance by many Chinese about using this technology in

farming, and doubts over whether the Chinese government

S

even companies currently dominate the global pro- will support the introduction of genetically modified plants.

duction of pesticides and seeds, a key sector in agri- Whether Syngenta’s new owners will list parts of the compa-

culture. But this oligopoly will shrink if the EU and ny on the stock exchange is unclear.

US competition authorities give their green light. The two Bayer is financing the takeover of Monsanto with US$

US corporations DuPont and Dow Chemical have merged, 57 billion of loans. Its board argues that the enormous po-

ChemChina has bought the Swiss company Syngenta, and tential of global agricultural markets justifies the price, and

the German chemical giant Bayer is going to take over the taking on so much debt. It expects the global turnover of

US company Monsanto. Three newly-formed conglomerates seed and pesticides to increase from US$ 85 billion in 2015

would dominate more than 60 percent of the market for to US$ 120 billion in 2025. For comparison: in 2015 Bayer

commercial seed and agricultural chemicals. They would and Monsanto had a turnover of US$ 25.5 billion and a prof-

manage the supply of almost all the genetically modified it of US$ 5 billion.

plants on this market. They would also own the majority Bayer AG, the world’s tenth largest chemicals manu-

of patent applications for intellectual property rights for facturer, has expanded into seeds by acquiring other com-

plants at the European Patent Office. panies. It has joined the league of large multinational seed

The new Bayer-Monsanto would be the world’s largest corporations, following in the footsteps of other chemicals

agricultural corporation, holding one-third of the global companies. Five of the world‘s seven largest seed producers

market for commercial seed and a quarter of the market come originally from the chemical industry: Monsanto, Du-

for pesticides. Bayer has agreed to buy Monsanto for US$ Pont, Syngenta, Dow and Bayer.

66 billion. Bayer-Monsanto and DuPont-Dow will remain No other company has swallowed more competitors in

on the stock market, and will continue to be accountable to the seed sector than Monsanto. This corporation began buy-

their shareholders. The management of DuPont-Dow plans ing up seed producers around the world in the 1990s and now

to split the new group into three listed companies, one of dominates a quarter of the world’s commercial seed market.

them an independently operating agrochemicals compa- It owns rights to most of the genetically modified plants, but

ny. ChemChina, a state-owned firm that is China’s biggest also sells many conventional seeds, in particular vegetables.

chemicals producer, has also agreed to pay an eleven-digit Monsanto’s presence is difficult to detect because the com-

panies it controls often keep their original name; Monsanto’s

logo rarely appears on a seed package in Europe.

The narrowing of the oligopoly from six or seven to

AGRIFOOD ATLAS 2017 / AGROPAGES

TOP 10 IN AGROCHEMICALS

three members will bring Bayer-Monsanto, DuPont-Dow

Headquarters of the firms with the biggest turnover, 2015

and ChemChina-Syngenta closer to their objective of dom-

publicly listed state-owned inating seed and pesticide markets and dictating products,

prices and quality standards. All three groups are pursuing

the strategy of ousting other suppliers and eliminating com-

4 Dow Chemical 2 Bayer

7 Adama (ChemChina) petitors, if necessary through acquisitions.

8 FMC

Philadelphia

Leverkusen Ludwigshafen Thirty national antitrust authorities worldwide are ana-

Midland Basel

St. Louis Wilmington Beijing lysing these mega mergers. The European Commission has

Tel Aviv ruled that DuPont must sell off some of its pesticides as well

Mumbai

6 DuPont 3 BASF as its research and development branch. To squeeze past the

1 Syngenta regulators Bayer is forced to sell off its South African busi-

ness in genetically modified cotton, as well as its Liberty Link

5 Monsanto 10 UPL

crops and chemicals.

Melbourne

9 Nufarm The influence of transnational corporations can

be difficult to detect. They often sell their products under

the brand names of the companies they buy up

20 AGRIFOOD ATLAS 2017You can also read