Amarin Corporation PLC (AMRN) - Q4 2019 - Seeking Alpha

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Amarin Corporation PLC (AMRN)

Q4 2019

Amarin Corporation PLC (AMRN) | 2 CONTENTS Disclaimer 3 Stock Performance & Financials 4 Stock Information 4 Financial Statement 4 Company Fundamentals 5 Thesis 5 Updates & Catalysts 7 Closing Remarks 7

Amarin Corporation PLC (AMRN) | 3 Disclaimer The intention of this report is to provide insight, not investment advice. While the information provided in this report is intended to be factual, there is no guarantee and prospect investors are encouraged to do their own fact-checking and research before investing in a company. One must also consider one's own financial standings, risk tolerance, portfolio diversification, etc. before making a decision to buy shares in a company. Many of my reports detail biotechnology companies with little or no revenue. These stocks are, therefore, speculative and volatile. Even when prospects seem promising, there is no predicting the future. Losses incurred may be significant.

Amarin Corporation PLC (AMRN) | 4

Stock Performance & Financials

Stock Information 5.8

5.2

Outstanding Shares: 358,906,887

Price per share: $24.02

4

Market capitalization: $8.62B

Cash & cash equivalents (as of Sept. 30): $673M

Debt: NA

Enterprise value: ~$8B 1.6

Cash burn per quarter: $5M-$10M (figures to decrease) 2011E 2012E 2013E 2014E

Estimated cash runway: Beyond 2022

RETAIL DINING

Accumulated deficit: $1,418,245,000

CULTURE UNDEVELOPED

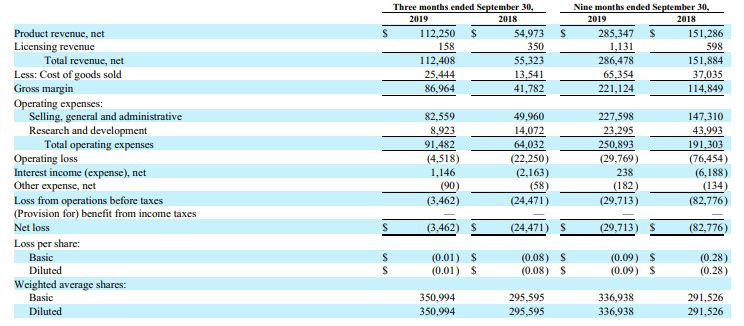

Financial StatementAmarin Corporation PLC (AMRN) | 5

Company Fundamentals

Thesis PRICE TARGET

Vascepa, icosapent ethyl, is currently FDA-approved for patients with severe

hypertriglyceridemia (TG >500 mg/dL). Amarin began marketing Vascepa for

this indication in January 2013. Two years later, Amarin began marketing

$35

Conservative estimates have Vascepa

Vascepa for patients with persistently high triglyceride levels (> 200 mg/dL) securing near $3B in peak annual

despite statin therapy. revenue. Additionally, Vascepa appears

to be safe from “copycats” for, at least,

Vascepa saw humble, but consistent growth for this limited indication: seven years following label expansion.

Assuming management is able to secure

a healthy label and executes on sale

fronts, there is no reason to believe

Amarin will not be valued well over $10B.

My price target may or may not change

following sNDA approval (when we get

an idea of how large the label is in terms

of the population Vascepa can be

prescribed to).

Figure 1: Vascepa revenues beginning to plateau (Source: Seeking Alpha)

At the same time and in hopes of securing a much larger indication, the

company began a cardiovascular outcome study named REDUCE-IT. The

Revenue

study assessed over 8,000 individuals with high cardiovascular event risk Estimates

despite statin therapy – mainly, these individuals had persistently elevated (in millions)

triglyceride levels (the average TG level in REDUCE-IT ended up being ~216).

$2,500

Between 2012 and 2018, Amarin’s stock struggled to gain momentum as $2,000

Vascepa revenue was far insufficient to offset dilution and battles between $1,500

Amarin, the FDA (over who Amarin could market to), and other companies $1,000 $2,100

$1,600

(concerning patents) ensued. $500 $986

$410 $650

$0

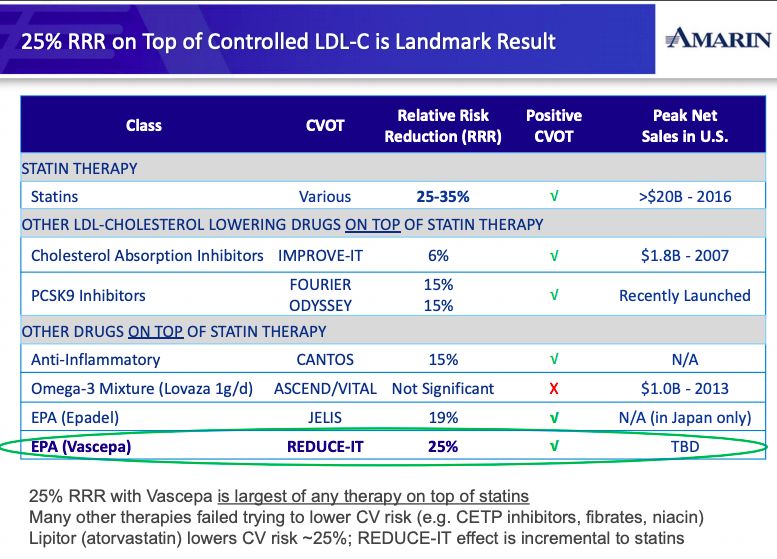

2019 2020 2021 2022 2023Amarin Corporation PLC (AMRN) | 6 Figure 2: FDA-approval & marketization optimism spoiled by reality Everything changed in late September 2018 when Amarin revealed that the REDUCE-IT study results were a massive success. Amarin’s share price soared from $3 to over $20 in a matter of days. The data showed that Vascepa, in patients on statin therapy with residual risk, reduced cardiovascular events by 25% with an extreme degree of statistical significance (p=0.00000001). At that moment, Vascepa joined drug classes like statins and PCSK9 inhibitors. Figure 3: Vascepa joins some blockbuster classes (Source: Amarin Corporation) As news of REDUCE-IT became increasingly available, Vascepa prescriptions and revenue shot up: Figure 4: REDUCE-IT data injects life into Vascepa revenues (Source: Seeking Alpha) Despite glowing and growing recommendations from the medical community (e.g. ADA, NLA, ICER), concerns over an active placebo influencing the study’s results hung over Amarin like a black cloud.

Amarin Corporation PLC (AMRN) | 7 Subsequent news of an Advisory Committee and sNDA delay saw shares bleeding into the low teens. Updates & Catalysts The Advisory Committee summoned itself on November 14 and to the delight of Amarin bulls, the Advisory Committee voted 16 to 0 in favor of the cardiovascular benefit claim of Vascepa. It is believed that while Amarin’s choice of placebo (mineral oil) may not have been inert, the data is far too significant to not attribute the end result to Vascepa. This news saw shares of Amarin reaching 52-week highs. Moving forward, Amarin will present EVAPORATE data very shortly. This will provide insight into the drug’s mechanism of action. I don’t expect this event to be of great significance. The PDUFA goal date is set for December 28, 2019. Amarin hopes to secure the largest label possible. Another issue of contention is how large a label the FDA will permit. A label only inclusive of patients with TG levels exceeding 200 mg/dL would be a bearish outcome. A label inclusive of patients with TG levels exceeding 135 mg/dL would be a bullish outcome. In the event of the former, my price target of $35/share would still likely be appropriate. In event of the latter, my price target may need adjusting – probably in the range of $45-$55 (supporting, essentially, $4-$5B estimate in peak annual revenue). It is my belief, based on my research, that the label will be favorable for Amarin (TG levels of 135 to 200 included). Glancing at the data, cardiovascular reduction benefit seems nearly independent of triglyceride level. Closing Remarks There is no way around it, REDUCE-IT is a landmark study in cardiology that is bound to change the treatment landscape as we know it. For much of the next 7-10 years, Amarin will dominate the landscape with the only drug of its kind firmly in its hands. Furthermore, as we have already seen with rising revenues pre-label expansion, Amarin has a good grip on the market already and one can expect revenues to explode even further upon sNDA approval. Amarin will quickly become a profitable company and will surely procure hundreds of millions of dollars in cash. Based upon REDUCE-IT data, one can expect a label that is favorable to Amarin. Some risks include sNDA delay, new safety concerns over Vascepa, competition, litigation, revenue misses, dilution, and market headwinds. A full assessment of risk in an Amarin investment can be viewed within the company’s latest annual filing.

You can also read