Beware of the High Yield ETF Trap 9 - March 2018

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Beware of the High Yield ETF Trap

9 – March 2018

Global interest rates are at record lows. The lowest the world has seen. The US Federal Reserve however, is gearing

up to raise interest rates by 3 or 4 times this year. Don’t be fooled. Even with these rate hikes, interest rates will still be

historically low. Australian rates on the other hand, will remain near historical lows for years, with inflation unlikely to

hit 2% until the end of 2019 at least.

That’s quite a conundrum for yield hungry investors who will have no other choice but to look else where for returns in

excess of the measly couple of percent they can get on their bank deposits. Retirees in particular have done it tough.

A large bulk of their savings are in interest bearing assets. You can understand why they feel hard done by. With

interest rates so low, retirees take on more risk by chasing higher returns. Rather than doing proper research and

searching for quality investments, some retirees have pursued a less desirable alternative: High Yielding ETFs. The

low interest rate world has led to a new breed of investments devised to solve the yield problem. These instruments

attempt to give yield hungry investors the high yield they’re so desperately seeking. But it all comes at a hefty cost.

These investments are called High Yield Exchange Traded Funds.

Firstly what are High Yielding ETFs?

They are exchange traded funds listed on the ASX. Billed as simple to use and cost-effective instrument, these

securities allow investors to implement an equity income investment strategy over a portfolio of 20 blue-chip Australian

shares. The ETF peddlers highlight their ‘attractive income’ as their key quality. And they’re right. These High Yielding

ETFs are capable of earning quarterly income (including franking credits) that exceeds the dividend yield of its

underlying share portfolio over the medium term. For this article we’ll used the Betashares Equity Yield Mazimiser

Fund (YMAX) or the BetaShares Australian Dividend Harvester Fund (HVST) as an example.

YMAX has a 12 month distribution yield of 8.5% which grossed up is 10.30% and has 49.8%

franking.

That yield is exceptionally high and very attractive but here’s the catch. What the ETF peddlers don’t tell you is that all

that is gained on the distribution yield is given back in capital losses. The Harvester uses a 'dividend harvest' strategy.

What that means is that it buys shares that are about to payout a high dividend, such as a bank or infrastructure

company. The sad truth is when buying pre dividend shares are usually higher. When selling ex dividend, shares will

have already fallen by the dividend amount. This results in a capital fall every time it is done. You can see it in the

funds performance. Both the YMAX and HVST are carrying huge capital losses since inception. This makes the

attractive distribution claim a little bit of a con. At inception, 29 October 2014, the HVST Fund NAV was $24.86. Today

it is trading at a NAV of $16.00. That’s a 36% loss since inception. The fund lost 17.90% in the year to the 31 January

whilst it paid out a distribution yield of 11.40%. So in effect the fund actually lost you 6.50%. The fund seems to have a

hedging strategy in place to minimize downside volatility. However the hedging doesn’t seem to be working with the

fund still amassing huge losses.

However the fund does have some appeal to retirees. It pays its high dividend monthly and straight into your bank

account at the middle of every month. Therefore living off dividends makes it very easy. But the only drawback is the

harvesting strategy in a bull market. Using the dividend harvesting technique results in less upside when markets are

going up. But what we’ve also noticed, is that the HVST fund also fell during downturns in the ASX 200. That makes

us somewhat question the firm’s risk management strategy.

Don’t fall in the trap

The bottom line is that the HVST fund is a dividend trap, it delivers income at the expense of capital growth. The fund

basically pays you back part of your capital with every distribution, until they’ll be nothing left. Whilst the fund

publishes its distribution as 11.40%, it’s really -6.50%. As mentioned above, one of the reasons for the capital loss is

buying cum dividend shares at their high and selling ex dividend shares at their low. We think a buy and hold equity

strategy will reap far better rewards. Look for real yield over fake yield and have absolute certainty over the capital

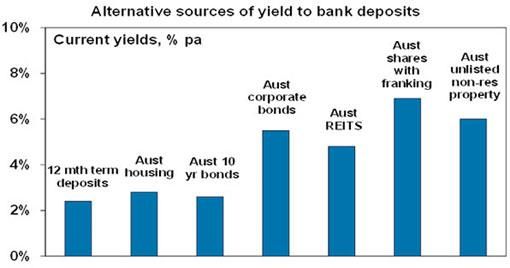

value of the investment. The table below shows yields on a range of Australian investments.

What I should look for when buying shares for dividend yield?

There’s an old adage, “if it sounds too good to be true, it probably is”. It’s a phrase that indicates pessimism but it’s

one that can save investors from getting caught in yield traps. When an investment is yielding +10% there’s good

reason to be concerned because in some cases the yield will come at a cost. A yield trap means buying a company

that promises to pay a high dividend but don't have the cash flow to support the payments. The aim is to look at higher

quality companies that pay a sustainable and consistent dividend yield that is attractive. Grossed up yields of around

6%-9% that are sustainable. Anything above that and it gets risky. Here are some rules to picking good dividend

stocks:

o Sustainability is a primary consideration in estimating dividend yields.

o Avoid companies that borrow to pay dividends. It’s not sustainable and will eventually lead to a

dividend cut.

o The quickest way to see whether a dividend is sustainable is to use the “payout ratio” — The

relationship between the company’s annual dividend payout per share and the company’s annual

earnings per share.

o A low payout ratio means the dividend is more sustainable and the company is reinvesting for growth.

o A payout ratio +70% is worth further investigation.

o A payout ratio of 100% is usually a good sign that the company has a looming growth challenge and

its dividend is ripe for a cut.

o A bank with higher levels of capital, a lower payout ratio and no sign of bad or doubtful debts is not

under pressure to cut dividends.

o Newly listed companies generally have lower payout ratios because they want to reinvest more of

their earnings in order to keep growing.

o Keep an eye out for dividend cover. It is the inverse of the payout ratio. It’s he ratio of company's net

income over the dividend paid to shareholders. EPS divided by the DPS. It indicates how sustainable

a dividend is. Dividend Cover of less than 1.5 may indicates the danger of a dividend cut while more

than 2 is viewed as healthy.

o Debt to Equity ratio is below 2.00 but preferably below 1.50. Below 1.00 is excellent.

ASX Code Company Price Gross Yield Payout Ratio Dividend Cover Debt to Equity Dividend Growth Risk of a Cut

GMA GenworthMortgage $3.13 13.50% 85.6 1.168 10% 9.70% High

TCL Transurban Group $12.67 6.71% 290.4 0.344 305% 8.90% Medium

RIO Rio Tinto $71.54 7.00% 55.6 1.799 34% -4.30% Low

MQG Macquarie Group $99.50 5.90% 71.1 1.406 408% 4.10% Low

NAB National Aust Bank $29.38 9.60% 83.8 1.19 394% 0.00% Low

As you can see from the above table GMA has the highest Grossing Yield. But it is a dividend trap. GMA has fallen in

share price by 30% over the last three months alone more than offsetting this dividend yield. It’s payout ratio is close

to 90% and is at risk of a cut. TCL is also at risk of a dividend cut, it is funding its payments by debt. If interest rates

rise, its dividend may not be sustainable. Dividend cover is 0.34. RIO and MQG both have fairly sustainable dividends.

Dividend cover is above 1.00, payout ratio is above 60 but below 100 and the yield isnt too high. NAB and MQG have

a high debt to equity ratio. Naturally, banks have relatively high levels of debt compared with other large companies

because taking deposits is their core business.

Here are two low risk high yielding alternatives

Our solution to attaining a reasonable and sustainable yield is to look at fixed interest cash and floating rate bond

products. Bond yields are the simplest real form of yield around. Like a loan, a bond pays interest periodically and

repays the principal at a stated time, known as maturity. A bond’s price always moves in the opposite direction of its

yield and interest rates.

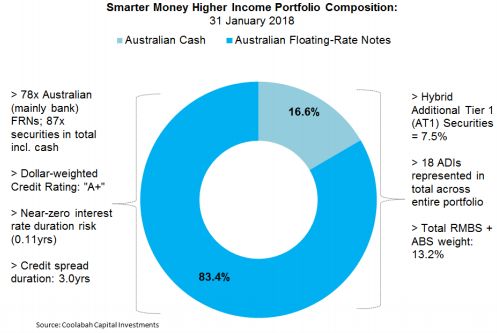

At the lowest risk side is Strategy Money Investments.The Fund manager is a is a leading independent, active fixed-

income manager established in 2011 by Christopher Joye, Darren Harvey and their team of portfolio managers and

analysts. They manage all of Smarter Money’s funds via Coolabah Capital Investments. The fund is called the

Smarter Money Higher Income Fund and is a low duration, short-term fixed-interest investment solution that targets

returns that outperform the RBA’s cash rate by 1.5%-3.0% per annum after all fees, over rolling 12 month periods.

That means the total return is somwhere betwseen 4.0%-5.50%. Smarter Money Higher Income invests in a portfolio

of Australian deposits, Australian investment-grade bonds (mainly issued by banks) and hybrids issued by banks and

companies. SMHI does not invest in fixed-rate bonds, equities or overseas bonds. Bonds are low duration. Investors

should be aware that higher duration funds are riskier because longer maturity bonds are more sensitive to rate

changes. They are however useful during a softening interest rate cyclce.

Since inception, September 2014, the gross return has been 4.7% p.a, including interest income and movements in

the price of the bond portfolio after all fund fees. The annualised volatility estimate of 0.57% p.a. Just to highlight, a

standard deviation of 0% to less than 0.50% is very low. You cant go wrong with the Smarter Money Higher Income

Fund. It pays up to 5.50% in yield without the risk of losing your capital.

The second alternative is a bank hybrid.

Hybrid securities issued by banks are listed on ASX but they are not the same as investing in the bank's ordinary

shares. Banks will issue hybrids to raise money that can count as regulatory capital under the prudential standards.

Capital notes and convertible preference shares are very similar in that they pay regular interest payments, called

distributions or dividends. On a fixed date, around 8-10 years in the future, you should receive ordinary shares in the

bank that issued the hybrid or the $100 facevalue in cash. We think the CBA Perls X (CBAPG) issue is an attractive

investment opportunity yielding the BBSW rate plus a margin in the indicative range of 3.40% to 3.60% per annum.

That equates to somewhere between 5.22%-5.42% per year. That’s a fair price for a a hybrid investment. However

investors are exposed to an equity like component and losses can occur. This means they should not be viewed as

traditional fixed-income products, nor should they be considered a substitute for low-risk investments such as term

deposits. An investment in CBAPG should only be considered by investors with a medium to high investment risk

tolerance. The securities are scheduled to begin trading on a deferred settlement basis on April 9.

The bottom line is, don’t blow up your capital chasing high yield securities such as ETFs. In order to find the right opportunities, focus on a sustainable yield rather than a high yield. Focus on quality. Whether you’re investing on your own or with a money manager, you might want to consider bonds and hybrids. As we see bond yields rise, it could signal the beginning of the end of the dividend equity run. Be picky in regard to high-dividend flyers as many are borrowing cash to pay their dividends. Don’t get caught in the trap.

Platinum’s next frontier - China

This week the UWJ team attended Platinum Asset Management’s annual adviser luncheon. Whilst legendary founder

and CEO Kerr Neilson stepped down from the top job last month, he still has considerable input on the company’s

vision and framework. Nielson hands the reins over Andrew Clifford, Platinum's chief investment officer, who will

succeed Mr Neilson from July 1 this year.

It’s all about China

Platinum’s luncheon was a packed house held at Melbourne’s Sofitel Hotel. What was striking was that the entire

presentation was based on one thematic. China. The first speaker was portfolio manager Dr Joseph Lai. Think back a

couple of years ago. Remember that 60 minutes report on China’s Ghost cities back in 2013? Here’s the link if you

missed it. To recap, China built massive cities. Brand new skyscrapers, apartment blocks, roads, bridges and shops.

Everything needed for a modern, urban lifestyle. Everything except one major thing. People. These cities were empty.

Almost like ghost cities. Everyone thought China was crazy and labelled it a huge housing bubble. Fast forward to

today and Ordos Kangbashi, China's largest ghost city, is now full. It’s a thriving metropolis that is occupied by more

than two million people. It’s a remarkable achievement that no one imagined possible. Lai says more than 20 million

people have now moved into these ghost cities as the middle class migrate from farms and villages into these urban

cities. In doing so, they’re actively buying up land and property. In-fact some cities have introduced a lottery system for

the sale of new houses as demand is overtaking supply. The lottery guarantees transparent and fair distribution of

homes. These ghost cities made headlines for nearly a decade with many sitting empty for years. Economists and

analysts saw this as a sign that they country was almost certainly headed for a massive property crash. They were

wrong. This was merely China’s style of urban expansion required for a giant population and giant economy.

It doesn’t stop there though, China’s good fortunes are spreading throughout the economy. The country is no longer

just a manufacturing economy. It’s a country teeming with entrepreneurs and innovators who are driving a tech

revolution. Over the past 20 years, Shenzhen has been transformed into a booming Silicon Valley. The country is

adopting tech on a massive scale. And if you think about it, it makes sense. For a start, China is massive. Lai says the

country produces 4 million technological engineers every year. The talent pool is huge. Which means its ability to

produce new tech companies and disrupt is more than anywhere else in the world. Here’s an interesting fact: 15

Chinese startups had reached unicorn status last year. Effectively 30% of the world’s billion-dollar companies were

created in China in 2017. What we are witnessing is a tech revolution and it’s only just starting. China is re-shaping

itself as a tech innovator and its long-term strategy is to lead the world in technologies such as machine learning,

blockchain, EV and energy.

To highlight this even further the Platinum team used mobile payments as an example. They visited a small town

called Chengda. What they found was that a movie theatre did not accept cash only payments via smartphone. Alipay

(Ali Baba) and WeChat (Tencent) Pay rank as the top payment options. Mobile payments have made massive inroads

as a medium of payment in Chinese cities. So much so that convenience stores, shopping malls, fine dining and even

vegetable markets have switched to mobile payments. It’s fast becoming a completely cashless society. China’s

mobile payment sector topped 29.5 trillion yuan in the third quarter of 2017. That completely dwarfs mobile payments

in the US. And the opportunities don’t end there. Think insurance. The insurance market is still in its infancy however

its adoption of cutting edge tech is first class. A company called Ping An with a market capitalisation of US$200bn

uses disruptive tech for its claims. For example a customer can use the Ping An smartphone app to lodge a claim on

the spot and submit a photo of the accident. The company then assesses the damage using artificial intelligence and

within minutes an assessment is delivered followed by the payment if applicable. In comparison, this process in

Australia is a costly and lengthy procedure that can take weeks if not months to complete.

Platinum’s next speaker was Portfolio Manager Clay Smolinski and for him it’s all about electric vehicles (EVs). Forget

the US. China is vying to become the world’s first all-electric vehicle ecosystem. In an effort to reduce pollution and

smog which is choking some of China's biggest cities, the country has decided to make a change. Air pollution is responsible for as many as one million excess deaths per year in China. For China to clean its air quality it will need systemic change and that’s going to come from its auto industry. Motor vehicles are the largest source of pollution so it makes sense to transform to an all-electric society. Chinese automakers churned out 680,000 all-electric cars, busses and trucks in 2017, more than the rest of the world combined. And China's output is growing faster than the rest of the world's. As more and more EV’s are churned out, the prices will continue to fall. The running cost of an electric car is $2.30 per 100kms compared to $12-$14 in a petrol car. That’s 80% cheaper. It’s also cheaper to service. An EV has 35 moving parts whereas most combustion engines have +200 moving parts. But the big best part is that EV’s are 50% cleaner for the environment than their petrol counterparts. And that’s huge. Sure there are teething problems such as the time it takes to recharge an EV battery and the maximum 300km range a car can travel before running out of energy. But these teething problems will be ironed out as EVs become more widely accepted. Innovation is bringing down the cost of batteries and that’s the key. The sticking point however is regulation. Within the four years every auto manufacturer will need to manufacture at least 5-10% of their fleet as electric vehicles or simply will not meet global omission standards. If the cars they produce don’t sell, they’ll need to drop prices dramatically to sell them until the 5% is reached. That’s great news for consumers. Smolinski points out, that investors can benefit not from just buying Chinese auto makers but also from battery manufacturers and from the mining companies that supply them. LG Chem supplies batteries globally and is about to open Europe’s largest factory for building lithium-ion batteries for use in electric cars. The facility will be able to supply as many as 100,000 EV batteries per year beginning next year. Inside each battery are similar compounds of either Cobalt, Nickel and Copper. Over the next five years demand for these three products is tipped to skyrocket. Platinum’s exposure to this area is via Glencore. The miner is the number 1 producer of Cobalt and number 3 producer of Nickel and Copper.

Platinum could have kept talking for hours on end about the merits of their investment strategy but it’s plainly clear their sole focus is on China. China’s fortunes have improved dramatically over the last decade driven by a tech revolution that we think is still in its infancy. Which-ever way you look at it, China is fast becoming the global leader in tech. It’s already grown four of the world’s largest tech stocks Baidu, Alibaba, Tencent and JD.com. Pretty soon the BATs will soon rival the FANG s of the world. They’re not far behind in market capitlisation. With that in mind, we think the Platinum International Brands managed fund is a great way to play the China thematic and to gain exposure to the fastest growing major economy in the world.

3 Stocks from the herd – CSL, TLS, SGR

In this section we provide readers with three stocks that have attracted the interest of the broking community or

the ‘herd’. Broker recommendations tend to be biased and highly optimistic. We try and breakdown these barriers

and give our own honest opinion. It is important to keep in mind that technical analysis is only one part of the

investment process and any recommendations do not give consideration to the underlying fundamentals of each

business.

CSL – $163.48 – Delivered a robust profit result last month. It posted a NPAT rise of 35% to US$1.086bn which was a

huge beat on an expected US$901m. It also upgraded guidance. Revenue was up 11% to $4.147bn, EBIT was up

31% to $1.476bn and EPS rose 32% to $2.40. CSL also upped its dividend by 23% to $0.79. Here are some dot

points:

Immunoglobulin sales up 13% on trailing period

Exceptionally strong demand for Idelvion® (rFIX-FP)

Specialty Products sales up 19% on trailing period

Seasonal influenza vaccine sales up 43% – strong QIV growth

Holly Springs cell culture facility – output up four fold

FLUAD® approved in the UK

NOT BAD

CSL

StockOmeter CSL Ltd $163.48

DEEP

VALUE 62 BUY PE FY0 35.92x Dividend 1.17% 52 Week High $165.84 Short term 46%

62

PE FY1 35.42x Gross yield 1.67% 52 Week Low $119.01 Long term 77%

ROE FY0 46.67% Franking 0% Price 1M % +16.36% RSI 72

ROE FY1 44.60% Debt / Equity 125.65% Price 1Y % +33.46% PEG Ratio 1.96

NO GOOD GOOD EPS FY0 2.99c EPS FY1 3.61c EPS Grow th +20.82% Market Cap $73.94bn

Intrinsic Value $89.56 Current Ratio 2.84

Broker View: Credit Suisse (OUTPERFORM $170.00) – The broker has a positive view on the stock following what

was a robust first half result. It says CSL’s Seqirus product is well placed to compete for market share due to the shift

towards higher margin products. A break even result in FY18 is dependent on the level of flu vaccine returns.

Unconventional View: We agree with Credit Suisse. CSL is the stock that keeps on giving. The earnings beat has

driven a 15% share price rise with shares trading at around $163 up from $142 mid-February. CSL’s profit guidance is

now forecast to hit US$1.5bn-US$1.6bn. Whilst the doubters have asked time and time again whether an expensive

CSL can deliver growth? Yes it can. It truly is the market darling and sits at the top of this reporting season’s winners

list. There should always be a space for CSL in your portfolio, especially this year. CSL is one that you can buy with

your eyes closed. Its lofty premium is justified by its growth in earnings year after year. CSL’s ROE sits on a whopping

46% driven by its commitment to investing in R&D and production. CSL has a market leading position and has a

number of upside catalysts that allow it to continue growing. We think it is well positioned to continue to grow into

fiscal 2019. As long as CSL can grow earnings, its share price will tick higher.

On the chart, CSL does look a little ritzy following the recent upside break out and could be hitting resistance. Those

wanting to buy might want to wait for an upside break out before buying. The stock has run hard, so we’re just being

mindful. All in all, the fundamentals are good and the chart is in a solid uptrend. CSL ticks all the right boxes.

Telstra (TLS) – $3.39 – Delivered a welcomed earnings beat last month followed by the payment of its dividend. The

result was driven by an increase in its subscriber numbers and lowered fixed costs. The result however did contain a

costly write-down. Underlying NPAT came in at $1.976bn which was up 10.3% and above an expected $1.946bn. This

excluded an impairment charge for Ooyala (its disastrous US-based intelligent video business) of $273m as it wrote

down the business to zero. NPAT was $1.703bn. Telstra also reaffirmed it expectation for its total payout for the year

to come in at 22c a share fully franked, including ordinary and special dividends. It also reconfirmed 2018 FY guidance

with income of $27.6bn- $29.5bn and EBITDA of $10.1bn-$10.6bn. Telstra added 454,000 NCN connections and has

maintained a 51% market share. About 57,000 retail bundled customers were added during the half, with one third of

these bundles including an entertainment component.

NOT BAD

TLS

StockOmeter Telstra Corporation Ltd $3.39

DEEP

VALUE 44 BUY PE FY0 10.58x Dividend 6.78% 52 Week High $4.72 Short term 57%

44

PE FY1 11.88x Gross yield 9.69% 52 Week Low $3.26 Long term 1%

ROE FY0 25.59% Franking 100% Price 1M % -2.44% RSI 49

ROE FY1 23.82% Debt / Equity 118.86% Price 1Y % -26.67% PEG Ratio NaN

NO GOOD GOOD EPS FY0 0.32c EPS FY1 0.30c EPS Grow th -6.71% Market Cap $40.32bn

Intrinsic Value $4.35 Current Ratio 0.86

Broker View: Morgan Stanley (UNDERWEIGHT $3.40) – The broker has a bearish view on the stock despite the

recent results. It says Telstra needs to act soon because it is facing rising competition in key core markets particularly

mobiles. An idea could be to enter the energy market. Juniors such as Vocus (VOC) and Amaysim (AYS) have

already acquired energy retailing businesses to offset weaker sales. To fill in its post-NBN gap in core earnings of

around $1 billion to $2 billion, Telstra may have to spend capital of up $10-20 billion.

Unconventional View: We disagree with Morgan Stanley. We were bearish on Telstra but after its recent results

we’re a lot more confident going forward. The telco increased its subscriber numbers, lowered fixed costs, reduced the

NBN impact and posted a solid profit result. But the highlight of the results was the accelerating pace that Telstra ismaking on 5G. Change is on the way. The telco is stuck in a sentiment hole having cut its dividend following growth

concerns. This caused a massive 50% fall in its share price.

However we think markets have over-reacted and the risk is now to the upside. The market is watching and waiting for

Telstra to up its game and we think 5G is the answer. It is ramping up preparations for the rollout of 5G, it has already

showcased a range of applications and staged a live demonstration of 3.1Gbps download speeds. Telstra delivered a

world first 5G data call on 26Ghz spectrum and delivered Internet of Things (IoT) capability on its mobile network with

Cat M1 and Narrowband IoT. Without getting too technical, Telstra’s 5G network will run faster than the NBN. In-fact

real world tests show speeds 60 times faster than those offered by the NBN. With an explosion in mobile data traffic

and connected devices, it means demand for a new generation of wireless infrastructure has never been higher and

will continue to grow. This is why 5G promises to beat its predecessor by offering faster speeds and lower latency.

Verizon and Ericsson recently tested a 5G network on a moving target, a car being driven around a racetrack and

were able to record a 6.4gb/s connection. To put this into perspective, the NBN is capable of delivering speeds up to

100mb/s, which means the 5G network is more than 60 times faster. Even though Telstra’s rollout of 5G is a little while

off, it is game changer and will quickly propel the telco back into box seat.

On the chart, TLS still looks horrible. So buying Telstra now is really taking a leap of faith and believing that 5G will

pay off. The stock is still in a downtrend and needs to break $3.60-$3.80 before a new short term uptrend is

confirmed. The RSI is at 46 which is showing the stock as oversold.

The Star Entertainment Group (SGR) - $5.46 – Delivered what was a mixed profit result. NPAT came in at $120m

up 12.4% with trading in Sydney coming in softer than expected in the early parts of this year. Results were also

impacted by low actual International VIP Rebate business win rate and significant items from USPP debt restructuring

costs. Here are some dot points:

Strong revenue beat in VIP.

In-line domestic revenue growth of +5.7% YoY driven by QLD (+8.7% YoY vs. NSW +4% YoY) but was offset

by higher than expected operating expenditure from the higher volumes, G/Coast opening costs, resumption

of bonus payments and wage inflation and higher VIP commissions due to increased revenue share

arrangements.

Net operating cash flow up 12.3% to $287.1m.

Outlook: No financial guidance was provided, consistent with prior management practice.NOT BAD

SGR

StockOmeter Star Entertainm ent

Group Ltd $5.46

DEEP

VALUE 48 BUY PE FY0 29.12x Dividend 2.93% 52 Week High $6.40 Short term 67%

48

PE FY1 18.79x Gross yield 4.19% 52 Week Low $4.88 Long term 56%

ROE FY0 8.63% Franking 100% Price 1M % -9.60% RSI 37

ROE FY1 7.20% Debt / Equity 31.90% Price 1Y % +7.91% PEG Ratio 7.51

NO GOOD GOOD EPS FY0 0.28c EPS FY1 0.24c EPS Grow th -12.16% Market Cap $4.51bn

Intrinsic Value $5.51 Current Ratio 0.73

Broker View: Macquarie (OUTPERFORM $5.46) – The broker has reviewed its forecasts for the casino operator and

has upgraded its operating earnings estimates for FY18-20 after taking into account the Sovereign Resort expansion

completion in FY20.

Unconventional View: We agree with Macquarie. Whilst the result was a touch on the disappointing side the reason

it was softer than expected was an overall weakness in trading conditions for the sector. Star realises gambling at

tables in private VIP rooms was down from last year and trading in Sydney was softer. An abnormally low win rate of

1.06% was recorded, much lower than the 1.35% expected. As a result the company is aggressively trying to turn this

around. Weaker conditions were also due to different timings of the Chinese Lunar New Year which fell earlier in

2017. The highlight was the company’s Queensland properties which posted pleasing results. Star will officially open

its new hotel at the Star Gold Coast later this month ahead of the Commonwealth Games. The new 17-storey hotel

features 57 rooms is currently undertaking a $345 million refurbishment of The Star Gold Coast in Broadbeach. The

casino is also undergoing a $220m facelift of its Sovereign VIP facility in Sydney with the refurbishment tipped to open

before Crown’s Barangaroo opening in 2021. Its capital

Sydney – commence Sovereign Resort upgrade preparations, progress lobby and Porte Cochere

redevelopment

Gold Coast – complete current phase of Gold Coast expansion and leverage Commonwealth Games to

successfully launch expanded and improved property

Queen’s Wharf Brisbane – complete demolition, commence excavation, fine tune property plans

Progress JV developments with Chow Tai Fook and Far East Consortium in Sydney (The Ritz-Carlton Hotel)

and the Gold Coast (Masterplan)

Whilst this result was on the softer side, we think Star will have a better second half. FY2018 priorities remain focused

on improving earnings across the group, sustaining domestic growth through capital development program and

delivering on the next stage of its capital program. Although no guidance was given, we think Star will be a huge

beneficiary from the Commonwealth Games and its results next half will surprise on the upside. On the chart, SGR is

sitting near its uptrend support line. The recent pullback has put SGR at an attractive valuation. With the RSI at 42 the

stock is oversold.Wattle Partners Pty Ltd Unit 10, 3 Bromham Place Richmond Victoria 3121 Australia T + 61 3 8414 2909 www.wattlepartners.com.au General advice disclosure Any recommendations given in this document is General Advice only. We have not considered clients’ personal or individual circumstances. All clients and readers should seek professional advice before acting on any recommendation. You should also obtain a copy of and consider the Product Disclosure Statements for any product discussed before making any decision.

You can also read