Canfor Corporation CIBC Marketing June 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Canfor Corporation

CIBC Marketing

June 2020

1

CIBC Marketing

Alan Nicholl Pat Elliott

CFO and Executive VP, SVP, Finance and Sustainability

Finance and Canfor Pulp

The presentation and answers to questions today contain forward-looking

statements which involve known and unknown risks, uncertainties and other

factors that may cause actual results to be materially different from any future

results, performance or achievements expressed or implied by such statements.

Factors that could have a material impact on any future oriented statements

made herein include, but are not limited to: general economic, market and

business conditions, product selling prices, raw material and operating costs,

foreign exchange rates, interest rates, changes in law and public policy, the

outcome of trade disputes, and opportunities available to or pursued by the

Company.

For further details on these factors and our assumptions and applicable risks

and uncertainties, please refer to Canfor Corporation’s Annual Report for the

year ended December 31, 2019 available at www.canfor.com or www.sedar.com.

2

Lumber

Supply & Demand

3

LUMBER MARKETS – US Supply and Demand

2020 – US Softwood Lumber Supply & Demand

U.S. Lumber Supply U.S. Lumber Demand

2020

Supply (Bfbm) 2018 Est. 2019 Est. 2020 Fct. Segments (Bfbm) 2018 Est. 2019 Est.

Fct.

U.S. PRODUCTION 34.9 35.1 34.2 New Home1 15.8 16.2 14.8

Imports – Canada 13.6 13.2 11.1 Repair & Remodeling 17.5 17.5 19

Imports – EU & Other 1.4 1.5 1.6 Industrial 12.0 12.1 9.7

U.S. Exports (minus) 1.7 1.4 1.1 Non-Residential 2.5 2.6 2.3

Total Supply 48.2 48.4 45.8 Total Demand 47.8 48.4 45.8

Source: WWPA, Statistics Canada, FEA, Canfor 4

4

US Housing Starts

• Q2 housing starts continue to track 25-30% below Q4 2019 levels

• Moderate improvement continues in Q3 and returning back to 2019 levels in Q4 2020

• Single family starts to hold a higher percentage of total starts post COVID-19, supported by suburbanization

• Lack of existing homes for sale and declining new home premium will improve starts

Analysts’ Forecast – April 2020

1,600

1,400 1,320 Housing Starts 2020 2021

1,290 (SAAR)

1,250

1,174 1,200

1,200 1,150

1,112

1,004 RBC 1.16 1.25

1,000 925

780

NAHB 1.08 1.33

800

CIBC 1.22 1.37

600

Fannie Mae 1.17 1.26

400

MBA 1.20 1.38

200

FEA 1.06 1.32

-

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Industry Average 1.15 1.32

Single Family Multifamily

Source: U.S. Census Bureau, Canfor, CIBC, APA 5

R&R Spending – US Housing Stock Currently Oldest In History

• High sales of existing homes in 2019 supports high potential for R&R in 2020

• Currently experiencing increased levels of home center demand; home improvement spending was up 6.5% YoY in April

• Homeowner equity trending at high levels, allowing homeowners to access these funds for large scale improvements

Share of Homes Built by Year Homeowner Equity

21,000

19,000

4% 17,000

16% 2010 >

15,000

38% 2000 - 2009

13,000

15% 1990 - 1999

11,000

1980 - 1989

14% 13%

1970 - 1979 9,000

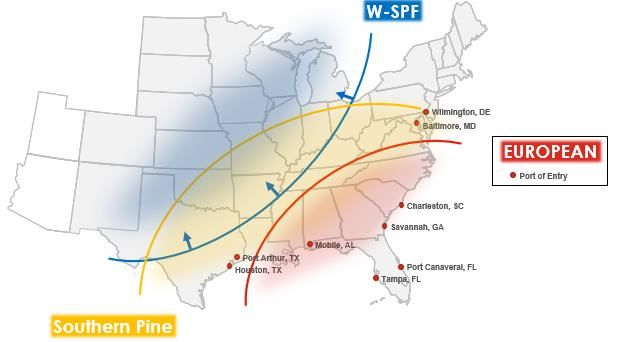

W-SPF Declines While US South and EU Imports Gain Market Share

• As W-SPF production declines, diversified species and global

operations allow us to support our US customers

• Softwood imports from EU will remain heavily dependent on housing

starts

• German, Austrian, and Swedish manufacturers hold largest share of

EU imports in North America

• We expect an annual increase of 28% pushing US imports of EU

lumber to 1.3 BBF

US Import Volume from EU (BBF)

2.5

2

1.5

1

0.5

0

7

EU Markets: Post COVID-19

• Initial production cuts throughout Northern Europe began in early April in response to COVID-19 related demand declines

• UK demand remains the largest intra-Europe outlet for European SPF production

• UK residential property transactions fell sharply in April, indications of sharp rebound in May supported by re-opening

• UK demand will dictate level of increased EU shipments to US

UK Residential Property Transactions

160,000

140,000

Property Transactions (SAAR)

120,000

100,000

80,000

60,000

40,000

20,000

0

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

Sep

May

May

May

May

May

May

May

May

May

May

May

May

May

May

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

Jan

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Zoopla 8

EU Beetle Kill: Production & Trade Outlook

• EU softwood lumber production is poised to remain level over 2020 and 2021 as investments currently under way will not provide additional production in the

near term

• We expect EU exports of logs to continue increasing despite COVID-19 as EU producers work to harvest beetle kill timber; reaching ~10 million m3 in 2021

• With fewer foreign workers in Russia and disrupted trade lanes due to COVID-19, we expect Russian log exports to China to remain below average for Q3

EU Softwood Lumber Production

60

48 48 49

50 46 47

45

Production Volume (BBF)

42 43 43

41 42 41 41

38

40

30

20

10

0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Austria Czechia Finland France

Germany Latvia Poland Romania

Sweden United Kingdom Other

Source: FEA, Eurostat 9

China: Markets & Supply

Markets:

• Chinese index for new export orders continues below growth levels, we expect consumption to remain low

• Recent announcements around increased infrastructure spending may improve demand in Q3

• Chinese exporters are pivoting capacity to meet domestic demand but they have run into difficulties, this is slowing consumption

Supply:

• Russian government has banned Chinese workers to control COVD-19, this has resulted in Chinese run lumber mills shutting

• Opportunities for additional supply from Canada and EU will improve with decline in shipments ex Russia

• Recent special issue exemptions from the Chinese government on US SYP log imports will push up SYP log imports

Source: FEA, IHS Markit 10Commodity Lumber Prices (US$/Mfbm)

2017 BC Forest Fires 2018 Severe Winter Curtailment Curtailment Curtailment

1.2 M ha. (July - Sept) Railcar shortage Announcements Announcements Announcements

650

600

550

500

450

400

350

300

250

JanFeb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

2017 2018 2019 2020

WSPF 2x4 2&Btr 310 375 359 407 388 368 403 395 419 446 484 457 493 523 524 552 634 609 564 468 414 323 337 320 335 406 371 328 312 360 356 340 373 361 385 385 396 433 367 317 361 378

SYP E 2x6 #2 332 361 380 401 368 343 342 360 392 422 414 411 391 415 399 411 521 552 477 383 354 307 336 341 318 349 326 314 283 265 320 314 340 306 305 283 305 301 317 301 447 482

Current pricing (June 26, 2020)

20.26% CVD • WSPF 2x4: $432

Duty (April – Aug 2017) 7.28% ADD 20.52% CVD / ADD • SYP 2x6: $480

Rate (July – Dec 2017) (Jan 2018 – Oct 2020)

Source: Random Length Publications, Inc., Canfor

11Operations

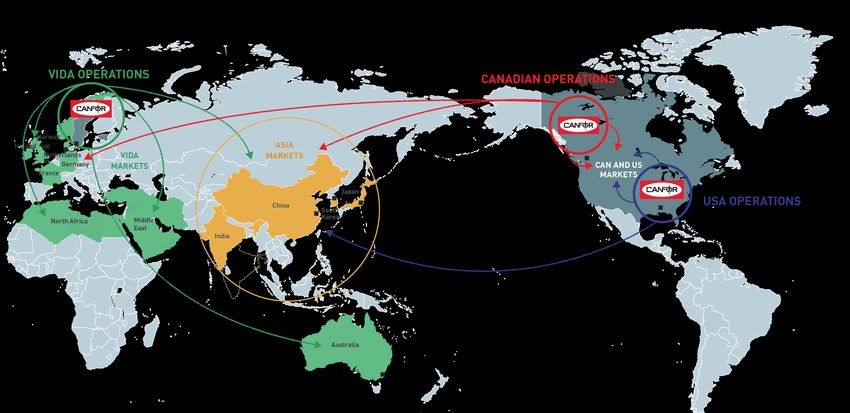

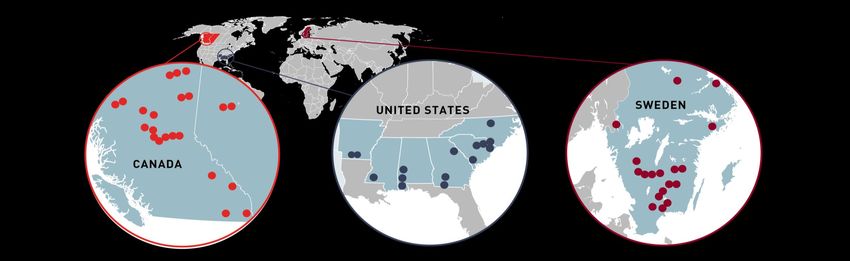

12Canfor

Operations

Lumber Regional Lumber Capacity Other Operations

4%

• 34 Sawmills with annual operating capacity of 6,700 MMfbm • 9 value-added facilities (packing, housing, energy) – Sweden

• 10 Western Canada - 3,200 MMfbm • 3 Pellet Plants – BC

22%

• 12 US South - 2,000 MMfbm • 2 Glulam Plants – US South

• 12 Sweden - 1,500 MMfbm* • Finger Joint Plant – US South

43%

• Green Energy Plant – BC

• Trucking Fleet – US South

Pulp and Paper

• 4 Mills in British Columbia

• 1.1 million tonnes of Northern Softwood Kraft

31%

• 230k tonnes BCTMP

• 140k tonnes Kraft Paper BC US South Europe Alberta

*Lumber capacity includes planned acquisition of Bergs Timber

13Western Canada

• Significant action taken over the past 18 months in response to challenging market conditions and elevated log costs in British Columbia

• Approx. 2.2 billion board feet of permanent industry rationalization to-date

• Estimated ~1.0 billion board feet of additional rationalization required to balance demand with long-term fibre supply

• Industry wide production curtailments in response to COVID-19 have reduced production by approx. 600 million board feet to-date in Western Canada

• Company has taken a number of short and long term measures to mitigate fibre cost escalation and support improved market pricing

• Anticipating modest reduction in log costs in 2020 reflecting impact of rationalization and lower market pricing in 2019

• Sales realizations anticipated to benefit from a ~15% reduction of duty rates effective October 2020

$100 Lumber Price vs. BCTS Bidding $1,000

2019 MPS

$90 Update $900

CVD / ADD Cash Deposit Rates

Lumber Price ($Cdn/Mfbm)

$80 $800

Company Current Rate New Rate* Change % Change

Bid Price ($/m3)

2020 MPS

$70 2018 MPS $700

Update

Update Canfor 20.5% 4.6% -15.9% -77.4%

$60 $600

West Fraser 23.6% 9.1% -14.5% -61.5%

$50 $500 Resolute 17.9% 15.8% -2.1% -11.5%

$40 $400 Tolko 22.1% 8.2% -13.9% -62.8%

$30 $300 J.D. Irving 9.4% 4.3% -5.1% -53.9%

$20 $200 All Others 20.2% 8.2% -12.0% -59.4%

*Preliminary rate effective October 2020

BCTS Avg Bid ($/m3) 2x4 RL 2&Btr ($/Mfbm)

14US South

• Currently benefitting from unprecedented demand

from home centers and lumber treaters

• Total lumber capacity of 2.0 billion board feet with full

run-rate achieved in 2021

• Over 300% growth since 2013, including 2019

acquisition of Elliott Lumber Company (210 MMfbm)

• 300 MMfbm organic program (US$125 million) to be

completed in 2020

• Strong fibre supply region, high performing

operations Fulton Planer mill; CDK;

infrastructure

( Completed 2019)

• Focus on high-value products and market

diversification supporting sales realizations and

strong operating margins

Camden – Full Mill Upgrade

(Finishing 2020)

15Customer Channels – Aligned for the Future

SPF CUSTOMER CHANNELS

WHOLESALE DISTRIBUTION • SPF customer channels heavily aligned with key pro-dealer

accounts able to respond to housing demand

PRO DEALER

• Strong alignment with Home Centers continues as we support

programs with Euro supply

HOME

• Key industrial accounts allow for diversification (e.g. Universal

CENTER Forest Products)

OFFSHORE

• Continued exposure to offshore markets allowing for global

INDUSTRIAL

diversification

SYP CUSTOMER CHANNELS

• Continued growth with Home Center accounts has allowed SYP to

WHOLESALE DISTRIBUTION capture a key DIY demand segment

HOME CENTER

• High value products aligned with key treater accounts continue to

provide return and increased exposure to R&R sector

• Focus on the pro-dealer segment provides diversified demand

TREATER INDUSTRIAL

channel aligned well with housing starts

• Strategic accounts in offshore markets aid in diversification and

exposure to more high value accounts

OFFSHORE

PRO DEALER

16Diversified Customers and Markets

• Currently experiencing strong R&R and Home Center demand in North

America (segment represents approx. 20% of WSPF production)

• Notwithstanding solid R&R activity, overall lumber demand anticipated to

decline moderately in 2020 as a result of reduced US housing construction

activity

• Company’s high-value product mix and diversification efforts supporting sales

realizations despite market uncertainty

• Steady takeaway in key offshore markets supporting pricing in North America

• Shipments to China approx. 20% of WSPF production with ability to

increase based on current demand

Canfor WSPF Sales by Country -2007 Canfor WSPF Sales by Country - 2019

USA Canada China Japan Other USA Canada China Japan Other

17Canfor High Value Product Diversification

Products that unlock incremental value with stabilized pricing

J grade & Square Edge Dimension

Appearance Boards, Pattern, Fascia, Clear

Visual appearance is primary purchase variable

SYP Long Length 22’/24’/26’

Application SPF & Spruce Metric Sizes

Matching sizes to end-user requirements

MSR Dimension

Lamina Blanks

Strength SYP Glulam Beams

Leverage fibre strength to match demand

18VIDA

• Vida’s 9 sawmills currently operating at full capacity (annualized rate of 1.2 billion board feet)

• Production primarily focused on structural timber, majority of which is exported to markets other than North

America

• Vida’s largest market is the UK, comprising approx. 30-35% of volume

• Other key markets include Asia, Australia, North Africa and the Middle East

• Geographic and product diversification contributing to more steady pricing despite current global economic

challenges

• Access to significant supply of high quality spruce and pine fibre in close proximity to sawmills

• Fibre costs tightly correlated to market pricing supporting more stable earnings

VIDA Sales by Country - 2019

• Canfor and VIDA are well positioned to capitalize on joint global market opportunities with significantly enhanced

market and geographic diversification; currently on track to achieve targeted synergies

• Recently announced acquisition of 3 sawmills from Bergs Timber (expected to close in Q3 2020)

• Purchase price of ~C$43 million, plus working capital

• Current production of 215 million board feet; targeting 300 million board feet capacity with modest capital

investment

• Strong strategic alignment with Vida’s existing sawmills

UK Other Europe Sweden USA Asia/Australia Other

• Proforma European lumber capacity of 1.5 billion board feet

19VIDA Acquisition Enhancing Market & Product Diversification

SALES OFFICES

20Liquidity Update - Canfor

Available Liquidity Scheduled Maturities*

(Canfor Excl. Canfor Pulp) (Canfor Excl. Vida and Canfor Pulp)

$700 $600

$600 $500

$500

$400

($ millions)

($ millions)

$400

$300

$300

$200

$200

$100 $100

$- $-

2015 2016 2017 2018 2019 Q1 2020 2020 2021 2022 2023 2024 Beyond

Operating Loan Facility Cash Term Debt Operating Loan Facility Revolver (Undrawn)

Canfor (excluding Canfor Pulp) had available liquidity of approximately $400 million at end of Q1 2020

A number of initiatives underway to preserve balance sheet strength in light of COVID-19 uncertainty:

$20 million reduction of planned capital expenditures (excluding Canfor Pulp). Currently anticipating lumber segment capital spend of $90 million in 2020, of which

approximately $25 million relates to European operations (total lumber segment capital spend reduced by approximately $110 million from 2019)

Accelerated filing of tax returns supporting early receipt of tax refunds (~$115 million anticipated by end of 2020)

Significant focus on reducing working capital, with liquidity in the second quarter benefiting from a seasonal unwind of inventory

Suspension of all non-essential overhead, disciplined cash management and government programs supporting liquidity

$200M revolving credit facility undrawn and set to expire mid 2021; no scheduled debt maturities until late 2023

Solid earnings supporting Vida’s planned acquisition; Vida anticipated to retain strong liquidity position through balance of 2020; operating lines renewed annually

The Company remains in full compliance with all covenants relating to operating loan facilities and long-term debt and expects to remain so for the foreseeable future

*US dollar denominated term debt translated at an assumed CAD to USD foreign exchange rate of $1.30

21Canfor Pulp

22Pulp Market Outlook

Supply Demand

• Softwood capacity projected to drop in 2020 after conversions to • Global tissue demand up 3.3% in Q1 2020 reflecting increased “At

dissolving pulp at Stora Enso Enocell in Sweden and Arauco Home” demand, offset in part by lower “Away From Home” usage

Valdivia in Chile

• Global tissue demand estimated to growth at ~3% 2020 - 2024

• COVID-19 providing some challenges with respect to sawmill

• Global Printing & Writing Paper decline accelerating due to COVID

residual fibre availability, major maintenance and project schedules

(down 12% for Q1 2020) with Western Europe seeing significant

• PPPC projects Softwood Market Pulp Capacity in 2024 to be weakness (down 15% for Q1 2020)

400,000 tonnes lower than 2019

• PPPC projects a 4.3% decrease in global demand for Market Pulp in

• PPPC forecasts global pulp demand/capacity balance for softwood 2020 and 5.6% decrease in Softwood demand

market pulp at 89% in 2020, rebounding to 92% in 2021 and

• PPPC estimates Chemical Market Pulp Demand to rebound by 4.4%

gradually increasing to 94% to 2024

in 2021 and increase by an average of 1.5% annually between 2022-

• Capacity increase through 2024 will concentrate on Hardwood 2024

market pulp in South America leading to hardwood pulp

demand/capacity balance in the 87% to 90% range

232008-2020 Global Market Pulp Demand

China is the largest consumer of pulp

Europe Asia N.America Other

40,000

35,000

30,000

Million Tonnes

25,000

20,000

15,000

10,000

5,000

0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: PPPC 24Liquidity Update – Canfor Pulp

Available Liquidity Scheduled Maturities

Canfor Pulp Canfor Pulp

$200 $120

$100

$160

$80

($ millions)

($ millions)

$120

$60

$80

$40

$40

$20

$- $-

2015 2016 2017 2018 2019 Q1 2020 2020 2021 2022 2023 2024 Beyond

Operating Loan Facility Cash Term Loan Operating Loan Facility

Canfor Pulp had available liquidity of approximately $100 million at end of Q1 2020

Significantly reduced capital spend in 2020 supporting balance sheet strength with planned capital expenditures reduced by $15 million in response to COVID-19

Suspension of all non-essential overhead, disciplined cash management and payment deferral programs supporting liquidity

Suspension of quarterly dividend for the foreseeable future recognizing the unprecedented challenges facing the global economy and the Company’s cash preservation efforts

Previously announced $40 million cost reduction initiative underway, with full benefits achieved by end of 2021

$50 million term debt matures in late 2022, with available operating line providing adequate liquidity for the foreseeable future

The Company remains in full compliance with all covenants relating to operating loan facilities and long-term debt and expects to remain so for the foreseeable future

25Canfor / Canfor Pulp – Value Proposition

High Quality Products Sustainable, High-Quality Well Capitalized Top Performing Balance Sheet

& Customers Fibre Supply Mills Pulp, Lumber Business Liquidity

26Investor Contacts

Pat Elliott Alan Nicholl

SVP, Finance and Sustainability CFO and Executive Vice President, Finance and Canfor Pulp

patrick.elliott@canfor.com 604-661-5441 alan.nicholl@canfor.com 604-661-5370

27You can also read