Global Offshore Wind Market Report 2018 - David S. Ottesen, Director Wind - NORWEP

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global Offshore Wind Market Report

2018

David S. Ottesen, Director Wind

We are not giving up on oil & gas

…

but ..

….utilising our expertise from

offshore and shipping to add

value in the offshore wind

industry!

150 of ca. 250 Norwegian Energy Partners´ partners are interested in offshore wind

Agenda

• Global offshore wind: a summary

• Market forecasts

• Expenditure and levelised cost of energy

• Europe

• Historical contracting and supply chain

• UK

• Germany

• Asia

• Market forecasts

• Expenditure and levelised cost of energy

• North America

• Market forecasts

• Expenditure and levelised cost of energy

• Emerging markets

• Priority Projects

• Floating Wind

The market

Global forecast

Global Forecast to 2022

10 50

Installed capacity:

Cumulative installed capacity

Annual installed capacity (GW)

Source: BVG Associates

8 15.0% 40

Global

6 30 Installed capacity by end of 2022: 46.4GW

(GW)

Major markets: China, Germany and the UK

4 20

2 10 Europe

Installed capacity by end of 2022: 33.9GW

0 0 Major markets: Germany and the UK

'18 '19 '20 '21 '22

Europe Asia Asia

North America Cumulative Installed capacity by end of 2022: 11.3GW

Major markets: China, Japan and Taiwan

• Globally there will be almost 16GW installed capacity at

the end of 2017 North America

Installed capacity by end of 2022: 1.2GW

• Offshore wind has grown to be a multi-national Major markets: The US (east coast)

industry over a fifteen-year period.

• Nearly all offshore wind development has occurred in

Europe, with deployment starting in Asia in recent

years.

© BVG Associates 2017

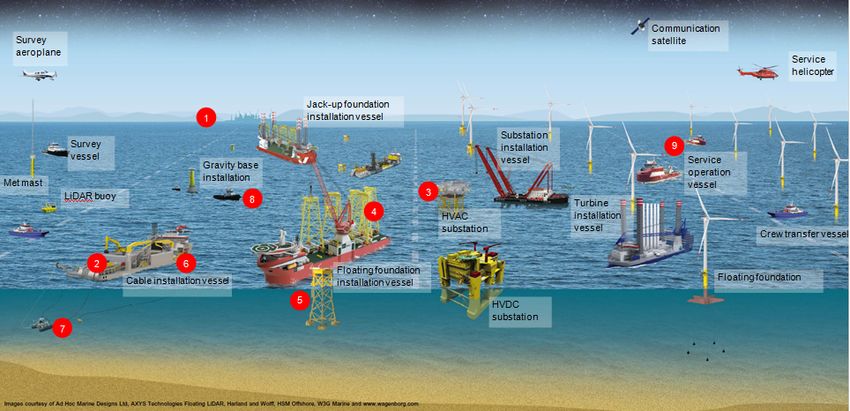

Technology, Supply Chain and Expenditure

Global Forecast to 2022

30,000

Source: BVG Associates • The rated power of turbines has increased over a 15-

25,000 year period, from 2MW to 8MW.

Expenditure (€million)

20,000

• Monopile foundations will continue to be widely used.

15,000 Jacket and gravity base foundations will be used in

rocky soil conditions or deeper waters.

10,000

5,000 • In 2017, the first large-scale floating foundation

project was installed in the UK.

0

'18 '19 '20 '21 '22

• 66kV array cables were first installed on a project in

Project development Turbine

2017 meaning capacity of a string can be increased

Foundation Array cable

and electrical losses can be reduced.

Transmission Turbine installation

Foundation installation Array cable installation • Higher voltage transmission will be used for larger

Transmission installation OMS projects further from shore, or where 'clusters' feed

into central HVDC transmission systems.

• Global annual expenditure for offshore wind in 2022 will be • Move towards 'third generation' jack-up installation

approximately €25,7 billion vessels to perform lifts in higher wind speeds.

• Expenditure between 2018 and 2022 will be about €108,3 • SOVs and drones will become more widely used for

billion larger projects located further from shore.

© BVG Associates 2017

The Supply Chain

The Cost

Levelised Cost of Energy (LCOE)

XX Box header

180

Source: BVG Associates

160

140

LCOE (€/MWh)

120

100

80

60

40

20

0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Offshore wind NNG (UK) EA1 (UK) Horns Rev 3 (DK)

Borssele 1&2 (NL) Vesterhav (DK) Kriegers Flak (DK) Borssele 3&4 (NL)

Triton Knoll (UK) Hornsea 2 (UK) Moray Firth (UK)

© BVG Associates 2017

LCOE Continued

Where cost reduction has come from

© BVG Associates 2017

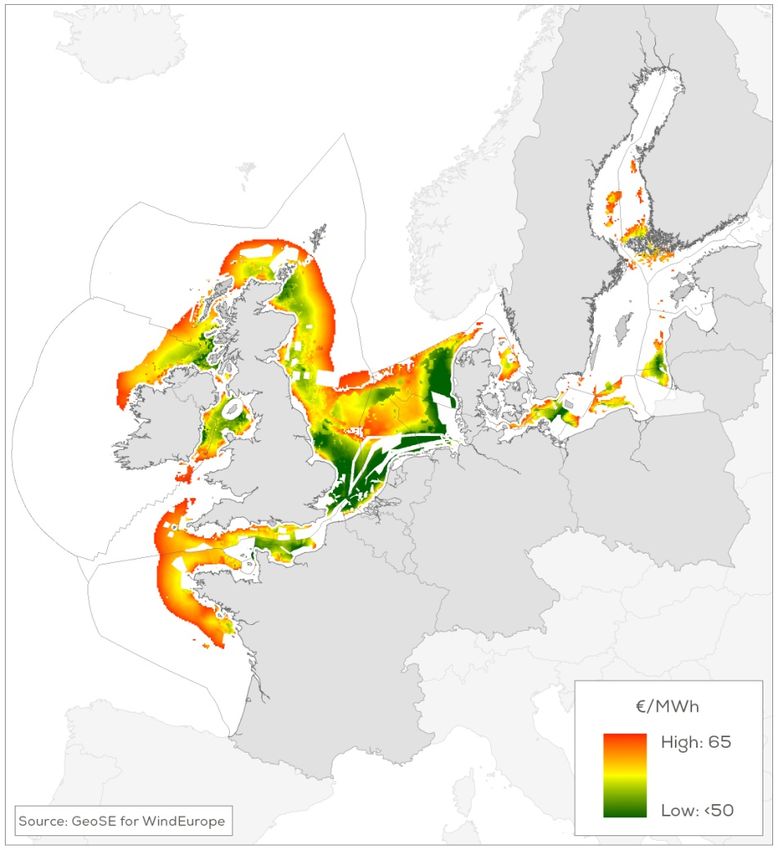

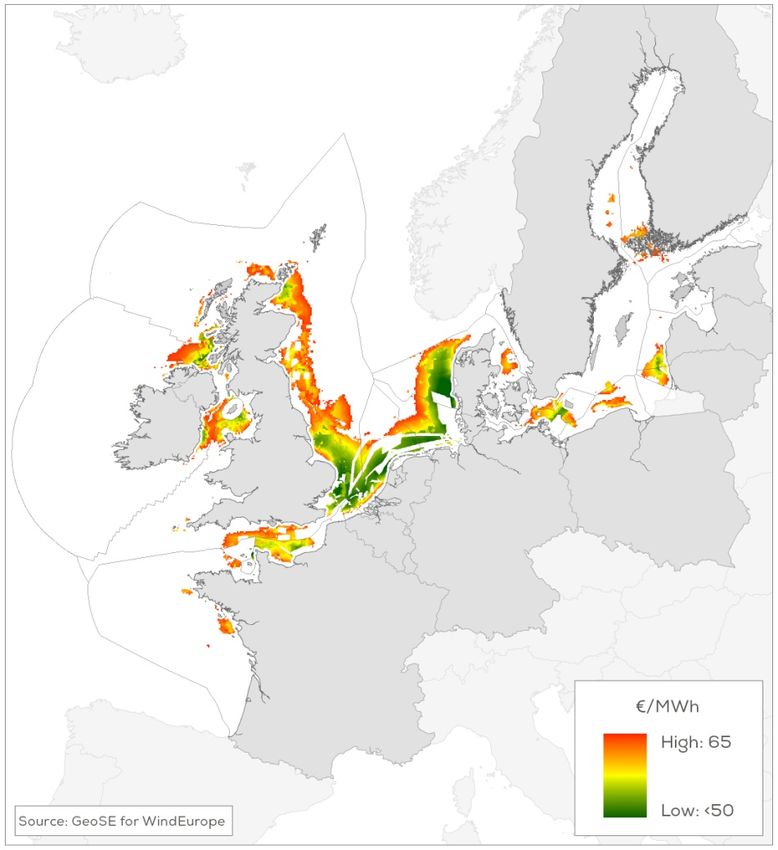

Economically attractive potential

Baseline and upside potential up to €65/MWh.

Baseline: 2,600TWh/year (600GW) Upside 6,000TWh/year (1,350GW)

© BVG Associates 2017The European Market

Europe leads globally

European Forecast to 2022

5,000 50

Cumulative installed capacity

Annual installed capacity (MW)

Source: BVG Associates 4.7%

4,000 40

3,000 30

(GW)

2,000 20

1,000 10

0 0

'18 '19 '20 '21 '22

BE DK FR

DE NL UK

Other Europe Cumulative

• Europe will have almost 16GW installed capacity at

the end of 2017

• In comparison, rest of world had just under 2GW

installed at end 2017

• By end of 2022, anticipated to reach about 33.9GW

• Main markets after 2020: UK, Germany, Netherlands

and France

© BVG Associates 2017European trends

Expenditure and levelised cost of energy

• Key driver in cost of energy reductions is

competition through auction schemes.

• Increasing the size of the turbine means that there

are fewer associated components to install and

maintain, which decreases cost. Focus on LCOE is

driving the use of larger turbines (8MW to 10MW).

• European sites are relatively benign: the North Sea

is fairly shallow, wind speeds are high, super-storms

are very rare. Small waves rather than the swell

waves.

• Developers with large pipelines of operational

projects are able to implement learning from early

projects to reduce costs on later projects.

• With the use of large turbines, CAPEX potentially

increases, but operational expenditure (OPEX)

decreases

• No wind farms outside Germany will use HVDC grid

connections before 2022.

© BVG Associates 2017Procurement strategies

Multi contracting vs EPCI

Multi contracting

• Developer typically awards main contracts.

• Some packages can be split or combined depending on a developer’s needs, preferences or

capabilities.

• Multi-contracting is often preferred by large utilities, particularly if the project is funded from their

balance sheet.

© BVG Associates 2017Procurement strategies

Multi contracting vs EPCI

EPCI

• EPCI contracting usually involves three main

packages. The turbine package is typically kept

separate. The other two packages vary in scope

according to the strengths of the bidders.

• Contract values can exceed £1 billion, which is a

major risk for all but the largest and most experienced

contractors.

• The interfaces between the non-turbine packages are

not difficult for the developer to manage.

• Independent developers and less experienced

utilities prefer this approach.

© BVG Associates 2017The UK market

UK focus – the largest European market

2,000 20

Cumulative installed capacity

5.7%

Annual installed capacity (MW)

Source: BVG Associates

1,500 15

(GW)

1,000 10

500 5

0 0

'18 '19 '20 '21 '22

Year of first turbine installation

Annual Cumulative

• At the end of 2017, the UK will have around 7.0GW

of installed capacity.

• This is likely to reach 13.6GW by the end of 2022

• CAGR between 2018 and 2022 of 5.7%.

• Between 2019 and 2022, the annual installed

capacity is likely to be between 400MW and

1,700MW.

© BVG Associates 2017UK background

Regulations Capex & Opex

• The Crown Estate has leased sites for offshore wind • Expenditure across all supply chain activities in

sites in UK territorial waters and in the UK exclusive 2022 will be about €6,600 million.

economic zone. In Scotland, management was

passed to Crown Estate Scotland in April 2017. • Expenditure between 2018 and 2022 will be about

€30,000 million.

• Offshore wind projects in England and Wales are

defined as nationally significant infrastructure • Around 60% of expenditure between 2018 and 2022

projects and are examined by the Planning will be spent on DEVEX and CAPEX. Around 40%

Inspectorate. In Scotland, Marine Scotland will be spent on OPEX.

examines applications.

• The support mechanism for new projects that have Main players

not reached FID is through CfDs. CfDs last 15 years • Orsted (formerly DONG)

and are awarded through allocation rounds • Statoil

• Vattenfall

• Offshore Transmission Owners (OFTOs) are • Scottish Power Renewables

granted licences to own and operate offshore • SSE

transmission assets • INNOGY

• Siemens Gamesa

• Developers typically take up an option to build the • MHI Vestas

transmission assets and sell on within 18 months of • Seajacks

wind farm commissioning. • MPI Offshore

© BVG Associates 2017The German market

Germany focus

Annual installed capacity (MW)

1,800 12.0

Cumulative installed capacity

Source: BVG Associates

1,200 8.0

(GW)

-21.6%

600 4.0

0 0.0

'18 '19 '20 '21 '22

Year of first turbine installation

Annual Cumulative

• At the end of 2017, Germany will have around

5.4GW of installed capacity.

• This is likely to reach 9.4GW by the end of 2022.

• Between 2019 and 2022, the annual installed

capacity is likely to be between 200W and 1,200MW.

• Around 75% of capacity will be located in the North

Sea. Remaining 25% will be located in the Baltic

Sea.

© BVG Associates 2017Germany background

Regulations Capex & Opex

• The German market regulation changed with the • Expenditure across all supply chain activities in

introduction of the WindSeeG (Offshore Wind Act) 2022 will be about €3,500 million.

which became law on 1 January 2017.

• Expenditure between 2018 and 2022 will be about

• The WindSeeG introduces a centralised planning €18,000 million.

approach, which involves an Area Development

Plan and a new CfD support mechanism. • Around 60% of expenditure between 2018 and 2022

will be spent on DEVEX and CAPEX. Around 40%

• A transitional mechanism provides support to will be spent on OPEX.

projects anticipated to be commissioned between

2021 and 2025.

Main players

• Offshore grid connections are constructed, owned • Orsted (formerly DONG Energy)

and operated by transmission system operators • WPD

(TSOs) TenneT (North Sea) and 50Hertz • EnBW

Transmission (Baltic). • Northland Power

• E.ON

• Under WindSeeG, this process is incorporated into • HypoVereinsbank

the Area Development Plan which outlines the • Global Infrastructure

location and construction schedule of future • ABB

transmission assets, currently out to 2025. • Engie Fabricom

© BVG Associates 2017The Asian Market

Asian Forecast

Asian Forecast to 2022

3,000 12

Cumulative installed capacity

Annual installed capacity (MW)

Source: BVG Associates and

Renewable Energy Solutions 34.4%

2,000 8

(GW)

1,000 4

0 0

'18 '19 '20 '21 '22

CN JP TW

Other Asia Cumulative

• Asia had almost 1.7 GW installed capacity at the end

of 2016

• By end of 2022, anticipated to reach about 11.3GW

• Main markets after 2020: China, Japan and Taiwan

© BVG Associates 2017Asian trends

Expenditure and levelised cost of energy Historical contracting

• In Asia, governments are committing to decarbonise • In general, multicontracting is preferred by

their energy systems. At this early stage of market developers, to gain experience, developers tend to

growth, LCOE reduction is less of a focus than it is contract a greater number of individual contracts

in Europe.

• A significant degree of government involvement in

• The region is faced with difficult weather conditions projects is coupled with support from major local

(typhoons and sea bed earthquakes in parts of conglomerates

China and Taiwan), river delta sea bed sediments

(China), and deep water (Japan and South Korea • The contracting approach for Asian operating

market is still emerging

• China, Japan and South Korea have track-records

with wind turbine production and corresponding Main players

supply chain.

• China Three Gorges Corp.

• The balance of plant and logistics supply chains are • China Longyuan (China Guodian Group)

generally less developed than in Europe • CGN Group

• SPIC

• In general, the projects are smaller than in Europe, • China Huaneng Group

reducing the economies of scale. • CNOOC

• Goldwind

• Legislation and governmental support mechanisms • Dongfang Electric Corporation

for offshore wind are less stable • Jiangsu Hangtong Ship Heavy Industry

• Ming Yang

• ZPMC

© BVG Associates 2017The North American Market

North America

North America Forecast to 2022

1,000 157.5% 2

Cumulative installed capacity

Annual installed capacity (MW) Source: BVG Associates and

Renewable Resources International

750 1.5

(GW)

500 1

250 0.5 Report: Northeast could add 8 GW of installed offshore wind capacity by 2030

The Northeastern US could add up to 8 gigawatts of installed offshore wind capacity by 2030,

0 0 according to reports from Massachusetts, Rhode Island and New York. "Offshore wind is gaining

'18 '19 '20 '21 '22 momentum as a significant new source of renewable energy in markets across the Northeast,

and these reports demonstrate that this regional resource will create thousands of new American

US Other North America Cumulative energy jobs in the process," said Alicia Barton, president and CEO of the New York State Energy

Research Development Authority.

• North America has 30MW installed capacity at the end of

2017

• By end of 2022, anticipated to reach about 1,2 GW,

almost exclusively in the US

• Main markets after 2020: US (east coast)

© BVG Associates 2017North American trends

Expenditure and levelised cost of energy Historical contracting

• Early interest is in the US north east in the states of • Experienced European are likely to multicontract

New York, Maryland and Massachusetts with mature, global suppliers, which may collaborate

with North American to localise, transfer knowledge

• The supply chain is inexperienced and for and minimise costs.

installation, the US Jones Act means that either a

local vessel and crew must be used, or the vessel • EPCI contracting is likely to be preferred by less

operations are very restricted experienced US developers, including Deepwater

• There are also uncertainties in planned financial Wind and US Wind .

support levels and in building requirements

Main players

• In the US, early projects are generally positioned

further from shore than early projects built in • Orsted (formerly DONG Energy)

Europe, • Dominion Energy

• Massachusetts Clean Energy Centre

• Projects in development have lower total capacities • Deepwater Wind

than projects in Europe. • Statoil

• Avangrid Renewables

• Many projects built along the west coast of the US • US Wind

and Canada after 2025 will be in deep waters that • Bluewater Shipping

will require floating structures. • GE

© BVG Associates 2017Emerging markets

Rest of Europe

Estonia

Estonia has a target within its National Renewable Energy Action Plan to install up to 500MW of offshore wind

capacity by 2018, although as of yet it has no offshore wind installed capacity so reaching this target is unlikely.

Finland

There are three demonstration projects operating in Finland, with a total capacity of 32MW. In 2017, the 42MW

Tahkoluoto offshore wind farm was commissioned. The wind farm uses technology designed specifically for icy

weather conditions.

Ireland

In 2014, the Irish government published its Offshore Renewable Energy Development Plan setting targets for

offshore wind development for 2030. Following the plan, Ireland would install a minimum of 800MW of capacity,

with medium and high scenarios of 2.3GW and 4.5GW also envisioned by 2030. In June 2016, Ireland signed a

letter of intent alongside other EU nations to facilitate cost-effective deployment of offshore renewable energy,

although no binding commitments were made.

Norway

To date, Norway has 2MW of offshore wind capacity installed at the Hywind floating demonstrator project.

In 2016, the Power for Change. Energy policy by 2030 white paper written by the Standing Committee on Energy

and the Environment called for the Norwegian Government to provide a subsidy scheme for offshore wind

demonstration projects and other marine renewable energy technologies by the end of 2017.

© BVG Associates 2017Emerging markets

Rest of the world

Australia

Before 2015, the Government did not support development of an offshore wind industry. The current

Australian Government is more favourable towards an offshore wind industry and in 2015, Australia's Clean

Energy Innovation Fund was established to provide AUD $1 billion to support offshore technologies

(including offshore wind) from demonstration to commercial-scale deployment

Canada

Currently, Canada has no installed offshore wind capacity. In 2016 the government of Ontario, where the

majority of Canadian projects are planned to be located, announced it is to keep a moratorium on offshore

wind projects until potential environmental impacts are fully understood

India

In 2015, the Indian Ministry of New and Renewable Energy (MNRE) announced a National Offshore Wind

Energy Policy, allowing areas within India's exclusive economic zone (EEZ) for offshore wind farm

development.

Vietnam

Vietnam has almost 100MW of capacity installed in the Bac Lieu offshore wind farm, installed in phases

between 2013 and 2015. A further 100MW is currently under construction at the first phase of the Khai

Long project, with the potential for an additional 200MW to be development at the site

© BVG Associates 2017Floating Wind

© BVG Associates 2015Why floating?

Wind speed Water depth

© BVG Associates 2015Why floating

Project Project

development and development and

management management

2% 2%

Operations and

maintenance

Turbine

38%

26%

Turbine

33% Operations and

maintenance

38%

Installation and

commissioning

24%

Balance of plant

26%

Balance of plant

24%

Installation and

commissioning

9%

Fixed Floating (but cost of energy +20%)

© BVG Associates 2015Floating is already large market à Close to 400 MW

of Demos and 7 GW of Large Scale Projects

Current MW Current Floating Wind Farms (Announced) under Development

Installed: 20MW Demo Projects Large Scale

12 MW > 2 GW in

US

Hawaii and CA

France, 100-150 MW France, 3.5 GW with

Europe UK, 80 MW commercial tenders

Portugal, 25 MW starting to be prepared

TBD (Target 8GW by 2030,

Japan Up to 100 MW

with mostly floating)

Taiwan/Korea Up to 30 MW 1.5 GW

Source: Principle Power>300 MW of Demos and approx. 7 GW of Large Projects in Dev worldwide

5

Source: Principle PowerFloating Wind“first mover advantage”

30% Norwegian content in Hywind Scotland

- Engineering of substructure, tower and

associated systems

- Procurement services

- Substructure transport

- Assembly preparation of turbines,

substructure and generators

- Towage, anchoring and operations

- Static and dynamic cables and

accessories

- Security, verification and guarantee

compliancePriority Projects

© BVG Associates 2017Norwegian Offshore Wind Industry

45 12%

NOK/bn

40 • Norwegian Market share from 5% today to

35

10% in 2030 10%

• International revenue tripling the next ten

30

years. 8%

25 • Revenue close to 50 billion NOK in 2030

6%

20

15 4%

10

2%

5

0 0%

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Total/ 10/largest/Norwegian/co´s Other Market/ ShareThe strength of the Norwegian supply industry Large complex projects Marine operations Offshore environment and material selection Offshore operation and maintenance Technology and risk assessment HSE&Q culture Experienced resources available

Offshore Wind Market information provided by Norwegian Energy Partners • Priority Projects – March • Global Market Review – August • Industry Report – included industry overview and opportunity mapping– August

International Offshore Wind activities 2018 • Scottish Renewable Offshore Wind Conference – Glasgow 29 - 31 January • Offshore Wind Summit 8th. March in Oslo • Danmark cooperation meeting – 1st. Quarter. • Taiwan/China Late March early April • FOWT – Marseille – 25-26 April • International Partnering Forum Princeton New Jersey – 3 – 6 April • Global Offshore Wind – Manchester – 19-20 June • Wind Energy Hamburg – 25-28 September • China Offshore Wind Summit 2018 - August • AWEA Offshore Wind – Washington 16-17 Oct • Offshore Energy – October - Amsterdam

Tremendous opportunities Limited only by our ability to exploit them! David S. Ottesen – Director Wind david@norwep.com

You can also read