CONCEPT REPORT The South African energy landscape

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CONCEPT REPORT

The South African energy landscape

This report has been commissioned by the ERLN via the Isandla Institute and compiled by Dirk de Vos. The views and opinions

expressed in this report are those of the author and do not necessarily reflect those of the ERLN or the Isandla Institute.

ERLN is an initiative of

Contents

Concept Report – the South African energy landscape....................................................1

Introduction........................................................................................................................3

Policy making & solving our electricity conundrum...........................................................4

Why we are where we are.................................................................................................5

Eskom at a glance.............................................................................................................5

Staffing..............................................................................................................................6

Prices................................................................................................................................7

Sales.................................................................................................................................7

Renewables.......................................................................................................................7

Cogeneration.....................................................................................................................7

Gas....................................................................................................................................8

South Africa’s electricity intensity & increasing energy efficiency (EE).............................8

The economic cost of load shedding...............................................................................13

The distribution sector and local government..................................................................14

Local government’s revenue model and the role of electricity.........................................15

The problem of data........................................................................................................18

Smart-meters and smart grids – a key consideration for municipalities in unlocking

the economic opportunities at sub-national level............................................................19

The future........................................................................................................................22

ERLN is an initiative of Produced for ERLN by www.erln.org.za

2 info@erln.org.za

Introduction

This ERLN concept note has been compiled as an input to the ERLN event titled, “Local and sub-national

renewable energy and energy efficiency: Challenges and opportunities for economic development”.

The event sets out to explore the question: “Can we stimulate renewable energy (RE) and energy

efficiency (EE) markets in a manner that is developmental and equitable whilst being sustainable for

municipalities?”

The just-released Bloomberg New Energy Outlook of 20151 highlights five shifts that will disrupt the

global electricity system going forward. These can be summarised as:

1. Solar, solar everywhere. The further decline in the cost of photovoltaic technology will drive a

$3.7 trillion surge in investment in solar, both large-scale and small-scale.

2. Power to the people. Some $2.2 trillion of this will go on rooftop and other local PV systems,

handing consumers and businesses the ability to generate their own electricity, to store it using

batteries and – in parts of the developing world – to access power for the first time.

3. Demand undershoots. The march of energy efficient technologies in areas such as lighting and

air conditioning will help to limit growth in global power demand to 1.8% per year, down from 3%

per year in 1990-2012. In OECD countries, power demand will be lower in 2040 than in 2014.

4. Gas flares only briefly. Natural gas will not be the “transition fuel” to wean the world off coal.

North American shale will change the gas market, but coal-to-gas switching will be mainly a US

story. Many developing nations will opt for a twin-track of coal and renewables.

5. Climate peril. Despite investment of $8 trillion in renewables, there will be enough legacy fossil-

fuel plants and enough investment in new coal-fired capacity in developing countries to ensure

global CO2 emissions rise all the way to 2029, and will still be 13% above 2014 levels in 2040.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

3 info@erln.org.za

Aside perhaps from the gas power dynamic (although here SA’s trajectory may have elements similar

to the US depending on how this unfolds) these all have direct implications for municipalities and new

economic opportunities.

This report outlines the overall energy landscape in South Africa and explores some of the conundrums

and challenges we face.

Policy making & solving our electricity conundrum

At a national level, official energy policy remains the 1998 White Paper setting out a progressive vision

for our electricity sector, with a substantial restructuring of our electricity sector separating generation,

transmission and distribution, the extensive use of markets to regulate price, promoting energy

efficiency and environmental sustainability. Extracts from the 1998 White Paper (page 43) include:

“To ensure the success of the electricity supply industry as a whole, various developments will have

to be considered by government over time, namely:

• giving customers the right to choose their electricity supplier;

• introducing competition into the industry, especially the generation sector;

• permitting open, non-discriminatory access to the transmission system; and

• encouraging private sector participation in the industry.”

On industry finances, the White Paper reads as follows (p46):

“The entire industry (generation, transmission and distribution) must move to cost-reflective

tariffs with separate, transparent funding for electrification and other municipal services.”

ERLN is an initiative of Produced for ERLN by www.erln.org.za

4 info@erln.org.za

This has not been comprehensively followed. We have to work with what we have. In this context, there

are challenges in how to engage with energy:

• Energy is subject to many pressures and claims - decision making is not straightforward and is

subject to a wide range of interests;

• At this stage, there are no clear “win-wins”;

• There many players in the field with strong statutory, economic and/or other interests. These

range from Eskom, Nersa (the regulator), industry, mining, the Intensive Energy User’s Group

(IEUG), agriculture, the different spheres of government, residential customers, Independent

Power Producers and others. These have established positions. As such, any policy

intervention will be subject to extensive scrutiny;

• As far as government is concerned, there needs be clarity in roles and interests in order to bring

certainty and predicatibility, as well unlock economic potential;

• Solutions will need to evolve from these players (from the existing ecosystem); and

• Economics and politics will continue to challenge evidence-based policy;

In terms of regional/sub-national economic development, a central challenge to unlocking the economic

potential lies in the challenge facing local government:

• Electricity sales by municipalities are an important source of their income;

• Municipalities as the most direct link to consumers/users of electricity are in the best position to

implement policies and strategies that will make South Africa energy efficient and energy secure; and

• Efforts to achieve energy efficiency and local generation will potentially reduce municipal income.

Conversely, the benefits of efficiency and local generation of renewable energy (economic growth

and therefore increased tax receipts) accrue only indirectly to municipalities.

Why we are where we are

Eskom ought to be understood in its historical context. It was first established to provide cheap electricity

to the mining sector. In late Apartheid years, Eskom, like Sasol had a role in securing South Africa’s

energy security in an increasingly hostile world. However, it is important to understand that Eskom

has never been a particularly efficient utility. Perhaps part of the reason why the 1998 White Paper

on Energy Policy was not implemented was that the apparent low prices and exemplary electrification

performance created the impression that Eskom was highly efficient and in no need of reform.

A closer look shows that Eskom’s ability to undertake its electrification programme was as a result of other

factors such as very low coal prices, exemption from taxation and dividends, financing subsidies and by

the fact that consumers had largely amortised the loans required to fund the generation over-capacity built

in the 1970s and 1980s. Eskom’s poor performance then was the subject of the De Villiers Commission set

up in 19842 . Eskom did not invest in any new capacity from the 1980s and so a falling debt (via amortising

older plant) was the most significant contributor to its ability to deliver cheap electricity through the 1990s

and first decade of the 21st century. For two decades, Eskom’s electricity prices have been very low by

international standards but critically, also below its own long-run marginal costs leading to an economy with

excessive electricity consumption patterns - something that exacerbates the current shortage of capacity.

Eskom at a glance

Eskom has a total Generating Capacity: 41,194MW3. In the world of electricity utilities, Eskom is an

extreme outlier. By generating capacity, it is the 5th or 6th biggest electricity utility4 in the world5 but

operates in an economy that is only the 29th biggest by GDP6.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

5 info@erln.org.za

Eskom’s revenues for its 2014 financial year amounted to R139.5 billion which means that by

revenues, Eskom is South Africa’s fourth or fifth biggest company7. If only South African revenues were

the measuring criteria, it would move higher up.8

Eskom is responsible for 95% of all electricity consumed in South Africa9. Other than the Koeberg

nuclear power station and a small contribution from hydro, 95% of Eskom’s electricity has been

generated from coal-fired power stations. An overview of Eskom’s Coal Fired Generators (as set out in

Eskom ‘s presentation to Parliament 29 July 2014) is set out below. The capacity of coal fired Power

Stations is as follows:

Nominal Capacity Age in 2014

Station Location

(MW) (design life 30 years)

Arnot Middleburg, MP 2 232 38

Camden Ermelo 1 480 42

Duhva Witbank 3 450 34

Grootvlei Balfour 1 090 44

Hendrina MP 1 865 43

Kendal Witbank 3 840 25

Komati Middelburg MP 791 52

Kriel Bethal 2 850 34

Lethabo Viljoensdrif 3 558 28

Majuba Volksrust 3 843 17

Matimba Lephalale 3 690 27

Matla Bethal 3 450 34

Tutuka Standerton 3 510 28

Recently, the performance of Eskom’s plant has fallen dramatically. Although poor maintenance is a

factor in all this, the age of Eskom’s generating plant is also a factor. The fall-off in plant availability

is now rather deep. In 2010 plant availability stood at 85%, but by 2014 it had fallen to 75%10. This

is important, Eskom’s own reserve margin requirement (the margin required to prevent unplanned

outages is at 15-20% of generating capacity11.

The under-investment is not only in the generating capacity. The South African Grid is also in trouble.

It is estimated that as much as R163 billion will be needed to get the South African grid to Grid

Code Standard. As South Africa cannot rely on other utilities in neighbouring countries to kick start

a national black-out, our grid ought to be extremely robust. It is not only the robustness of the grid

which is important. If the grid is going to be able to evacuate new generating capacity, it will need to be

strengthened12.

Staffing

Eskom’s staff complement in 2013, stood at 46 000 – 47,000 employees13. Of these, about 15 000

are involved in Eskom’s own distribution/retail activities. On the face of it, Eskom seems over-staffed.

Depending on available plant or full (theoretical) capacity, Eskom employs more than 1 person per KW

capacity. By way of comparison, Iberdrola, a Spanish utility with a capacity of 45GW, a little bigger than

Eskom’s 41GW employs 30,678 people or 1 employee per 1.4KW while Duke Energy, the US’s largest

electricity utility with 57GW of capacity, employs just 27,948 people or 1 employee per 2kW14. Poor

ERLN is an initiative of Produced for ERLN by www.erln.org.za

6 info@erln.org.za

productivity is less of a problem if employers are paid less than Eskom’s peers but this is not the case,

the average salary per Eskom employee stands at more than R600,000/annum.

Prices

For the present, South Africa’s electricity price is still amongst the cheapest in the world15. For industrial

users, it is amongst the cheapest anywhere in the world16. According to 2014 figures, Eskom’s average

selling price was 71c/kwh17 but this tariff is likely to go up dramatically. The average cost of running

the Ankerlig Open Cycle Gas Turbines is R3/kwh and Nersa calculated in 2012 that Medupi will, on a

stand-alone basis need to have a tariff of 97c/kWh, a figure which has since increased. Once Medupi

and Kusile come on line, they will represent between 20-25% of Eskom’s total generating capacity. At

present, Eskom’s estimation of revenue shortfall in MYDP3 period18 is R225 billion (Eskom presentation

to Parliament 29 July 2014).

Sales

The table below sets out Eskom’s sales of electricity.

2013/14 2012/13 2011/12 2010/11 2009/10 2008/09 2007/08 2006/07

Total sold, GWh 217 903 216 561 224 785 224 446 218 591 214 850 224 366 218 120

Growth/

0.6 (3.7) 0.2 2.7 1.7 (4.2) 2.9 4.9

(reduction)

Eskom does not disclose the sectors to which it sold its electricity but using a 2004 Treasury study, the

splits across the different sectors are as follows:

Category Percentage of Total

Domestic 17.9%

Agriculture 2.7%

Mining 17.6%

Manufacturing 39.8%

Commercial 11%

Transport 2.9%

General 8%

Renewables

Moves to bring in Independent Power Producers commenced in 2011 in renewables – under the

Renewable Energy Independent Power Producer programme (REIPPP). This was as a consequence

of our commitments to the Conference of the Parties (COP) processes under the Kyoto Protocol.

The renewables programme operates via an Independent Power Programme (IPP) office run from

the Department of Energy. Every renewable plant supplies its power to Eskom in terms of a Power

Purchase Agreement that is guaranteed by the state. Already, via four bidding rounds, 5 243 MW has

been procured amounting to investments totalling R200 billion. Another 1 084 MW will be added shortly

as an extension to the fourth bidding round and an expedited fifth round may add another 1 800 MW

of renewable energy. The Department of Energy has sought to secure an additional 6 300 MW of

renewable energy.

Cogeneration

Beyond renewables, the IPP programme has recently issued a request for bids under the cogeneration

independent power producer (IPP) procurement programme and the deadline for 1 600MW of

ERLN is an initiative of Produced for ERLN by www.erln.org.za

7 info@erln.org.za

Baseload Coal IPP bids (spread over different bids of no larger than 600MW each) are expected in

August 2015. Of interest is that the baseload coal IPPs will need to bid in their projects with a tariff of

less than 82c/kWh.

Gas

In May 2015 the Department of Energy issued a request for information (RFI) for gas-fired electricity

generation and this will help with the development of a 3 126 MW Gas to Power Procurement

Programme.

South Africa’s electricity intensity & increasing energy

efficiency (EE)

South Africa’s economy is one of the most electricity intensive (kWh required to produce a unit of

GDP). Despite the movement towards a bigger services sector, inherently less energy intensive than

mining or manufacturing, our economy’s energy intensity has grown. Figures show that South Africa’s

energy (and with it electricity), intensity doubled over the period 1990 to 200719. In large part this was

due to increases in energy intensive manufacturing activities in the 1990s, particularly in the area of

aluminium smelting (the non-ferrous metals sector).

Our economy is also characterised by a small number of industrial concerns consuming almost half

of our electricity. Most of them are members of The Energy Intensive Users Group (EIUG)20. Its 31

members account for 44% of all electricity consumed in South Africa but, collectively, they also have

a collective annual turnover of R741 billion, more than 20% of South Africa’s GDP and employ nearly

600 000 South Africans.

Almost half the EIUG’s members are in mining and a third are manufacturing concerns. Of importance

here is that across the EIUG’s membership, a significant component of their annual expenditure, nearly

20%, is made up of electricity. This would indicate that they are both heavily dependent on electricity

ERLN is an initiative of Produced for ERLN by www.erln.org.za

8 info@erln.org.za

but are also very exposed to increases in the price of electricity. It would be a mistake to understate the

importance of most of the EIUG membership. The EIUG membership represents much of what South

Africa exports to the rest of the world. These exports finance our dependence on imports of industrial

equipment, a necessary input if this economy is to grow21. Moreover, many of them form an important

base upon which the economy rests.

Another way of looking at things is to compare South Africa to its peers. The table below lists the 25th –

37th biggest economies in the world in US dollar terms, South Africa, being the 35th biggest. It then sets

out population size and electricity production:

Country GDP Population GDP/ Capita Electricity Electricity Electricity

(Nominal in millions World Bank Production Intensity Intensity per

in US US dollars TWh ratio (Elec Population)

Dollars) Nominal BP Statistical prod/ GDP) (Elec prod/

World World Bank Review of Pop ratio)

Bank 2013 World Energy

2013

Nigeria $522 638 178.9 $3 010 24 827 47 139

Poland $517 543 38.5 $13 342 164 800 318 4 280

Norway $512 580 5.1 $100 819 134 200 261 26 313

Belgium $508 116 11.1 $45 387 85 100 168 7 666

Venezuela $438 284 28.9 $14 415 131 700 300 4 557

Austria $415 844 8.5 $49 074 67 700 163 7 964

Thailand $387 252 64.4 $5 779 164 800 426 2 559

UAE $383 799 9.0 $41 692 111 300 290 12 366

Colombia $378 148 47.7 $7 829 62 200 165 1 303

Iran $368 904 77.6 $4 763 263 400 714 3 394

South

$350 630 52.9 $6 618 256 100 730 4 841

Africa

Denmark $330 814 5.6 $58 930 30 402 92 5 428

Malaysia $312 435 30.4 $10 514 131 600 421 4 328

South Africa is an outlier being the most electricity intense economy.

One of the more interesting documents submitted by Eskom in support of a 16% year-on-year tariff

increase was a report produced by Deloitte entitled “The Economic Impact of Electricity Price Increases

on Various Sectors of the South African Economy”22. In it, the work of University of Pretoria academics

Roula Inglesi-Lotz and Professor Blignaut studying price elasticity of demand by different sectors of the

economy is extensively cited. One of the important findings by these academics is that as electricity

prices declined from the 1980s, South Africa’s electricity intensity has increased dramatically. So while

in 1990 South Africa had roughly the same electricity intensity as the OECD (a group of developed

industrialised countries), by 2006 it had almost doubled. These academics were also able to show that

when South Africa experienced its last big electricity price increases in the early 1980s when Eskom’s

build programme was at its height, the price elasticity of electricity demand in South Africa was

significantly negative. We are likely already in this position once again.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

9 info@erln.org.zaThis has important implications for the procurement of generating capacity. At present, our current

planning is set out in the Integrated Resource Plan of 2010 (IRP2010). It provides the basis for the

procurement of new generating capacity. In general terms, it projects that economic growth requires

a growth of generating capacity. But some of the assumptions are based on a price compact to which

Eskom committed itself in 1991 which brought prices of electricity progressively lower23. The compact

was broken in 2006 and from then, prices have increased significantly as seen from the table below:

Comparison of approached tariff increases with rate of inflation

Average approved Average yearly

Year

tariff increase % inflation %

2008 27.5 11.5

2009 31.3 7.1

2010 24.8 4.3

2011 25.8 5.0

2012 16.0 5.7

2013 8.0 5.7

2014 8.0 6.1

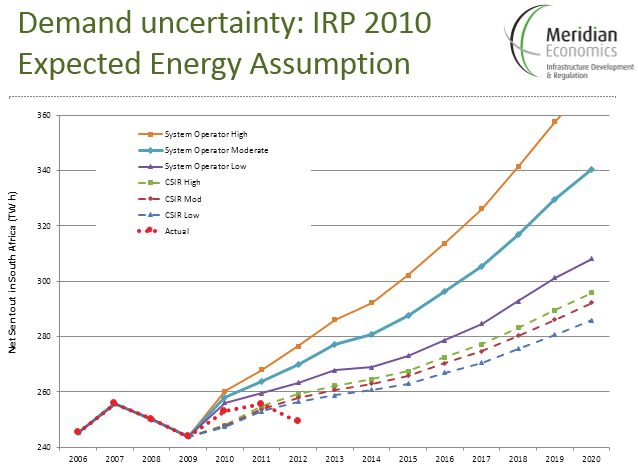

The five years since the publication of the IRP2010 has shown that assumptions around electricity

demand are incorrect. Given the economy’s extreme electricity intensity, this is not surprising. South

Africa has grown (very modestly) but as the chart below shows, it has actually reduced the amount of

electricity it uses.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

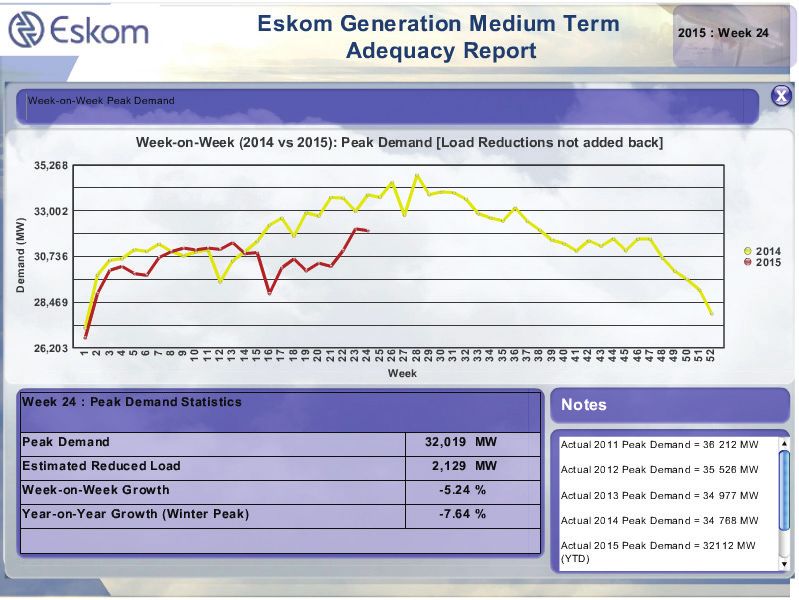

10 info@erln.org.zaMore recent figures from Eskom show that South Africans are using progressively less electricity, even

at peak times24:

Energy efficiency will increasingly become an integral part of our economy. The graphic below shows

how in response to increased electricity prices, the output from a unit of electricity has increased. This

trend is set to continue:

Considerably more work on energy efficiency has been done elsewhere than here. While a number of

energy efficiency measures are in place, very little has been done about its implementation25. Where

incentives such as section 12L of the Income Tax Act exist they are limited in their ambit26.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

11 info@erln.org.zaEnergy efficiency, research from the International Energy Agency (IEA) suggests, is routinely and

significantly undervalued. Their research shows that under existing policies of their member countries

(the OECD), two-thirds of the economically viable energy efficiency potential available to 2035 will

remain unrealised27.

The problem is that energy not used, and costs not incurred, are hard to measure hence the

description of energy efficiency as the “hidden fuel”. Nevertheless, the benefits of energy efficiency are

huge28. Amongst the IEA member countries, energy use avoided in 2010 was bigger than the demand

met by any other single energy supply including oil, coal or gas. To demonstrate the effectiveness of

these measures, the research also showed that the total amount invested in energy efficiency across

those countries as of 2011 was an estimated $300 billion, which equalled their aggregate investments

in non-renewable conventional energy sources.

There are other benefits, energy efficiency can provide health benefits and improve industrial

productivity by lowering the costs of energy in the supply chain. Greater energy efficiency can improve

national budgets by lowering the cost of energy used in the government’s infrastructure which could be

directed to say, increasing access to electricity for low-income populations. The report also dealt with

the rebound effect where efficiency gains are lost when people respond by buying more energy. This is

not a bad thing as people improve their well-being with the same amount of energy. Some developed

countries such as the USA has seen a divergence between energy consumption and economic growth

since the 1970’s29. This is also happening on a global level30.

We need to understand the scope for greater efficiencies in our economy. If South Africa is to grow,

it will need to delink economic growth from greater electricity consumption. Energy efficiency and

the revenue models of municipalities must be changed. Energy efficiency programmes run by

municipalities run contrary to their revenue models.

Nevertheless, there is now evidence that South Africa is becoming less electricity intense as seen from

the chart below:

ERLN is an initiative of Produced for ERLN by www.erln.org.za

12 info@erln.org.zaWe need a more thorough understanding of demand elasticity for electricity across and within various

sectors. Very little research exists. We need to understand to what extent our balance of payments

or our ability to fund imports of capital equipment depends on certain electricity price levels in the

important mining and parts of the manufacturing (ferro-chrome processing) sectors. In doing so, we

need to identify those sectors that look the most vulnerable to increases in price and to what extent can

these industries become less energy intensive31.

All the above is very important to understand as South Africa embarks on a build programme. How

much generating capacity does South Africa need at different price points? Beginning to understand

this is key to breaking the generation long cycle of over investment and under investment. It will also

help answer what type of generating capacity we ought to consider.

The economic cost of load shedding

Most reliable observers say that load shedding will remain with us for at least another five years. It

obliges us to answer the question of the economic cost of unserved electricity to the South African

economy. It can be a tricky question to address. Different businesses will have vastly different costs.

Some businesses can manage a work-around, while others are less able to do so.

The calculations currently used by the revised Integrated Resource Plan 2010 (2013) provide one basis

and was the basis of a study published by the CSIR on the financial benefits of the renewable power

projects that have already been commissioned32. Even at the very high tariffs (compared to subsequent

renewable projects under construction, the paper calculated that South Africa’s net benefit amounted to

R800 million. Demonstrating that the renewable projects under consideration had delivered 2.2 terawatt

hours to the grid, they could derive the savings on diesel not burnt but then went on to show that the

2.2 terawatt hours avoided 120 hours of unserved electricity. Avoiding unserved energy amounted to

a “benefit” of R1.6 billion. How is this derived? The number comes from a worksheet for the current

revised Integrated Resource Plan33 found on the Department of Energy’s website34.

The basis for the cost of unserved electricity is derived from surveys done by Eskom at its largest

customers. These suggested that the cost of unserved electricity was 150 times larger than the cost of

supplying electricity. Using the average tariff at the time, the cost of unserved electricity was deemed

to be R75/kwh. The CSIR updated this to R87/kwh based on the average selling tariff at the time. The

Department of Public Enterprises, in its own calculations, uses a figure of R100/kwh35.

It ought to be remembered that the original Eskom survey was not undertaken to calculate the actual

cost to the economy of unserved electricity, its purpose was to determine the size of the reserve margin

that Eskom ought to maintain (i.e. the size of mostly idle capacity). Intuitively, it does not make sense.

If it were a reliable measure then any increase in the tariff would result in an increase in the costs of

loadshedding to the economy. Very little research has been done on the impact of loadshedding and

many numbers are mere speculation36.

More work needs to be done. The economy is not only represented by a sample of Eskom’s largest

customers. The services sector, which does not use much electricity, would have a far greater cost

where electricity is a small but essential part of the services business concerned. Being unable to have a

hot shower or eat a hot meal at home is a horrible inconvenience but probably does not generate much

of a cost to the economy. Deriving a figure for the costs of load shedding to our economy would be a

very difficult task. Many of the costs are not direct costs but would include issues like investor sentiment

and confidence in the future of the country, social stability issues, opportunity costs and so on.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

13 info@erln.org.zaPerhaps better numbers could be derived from undertaking a sectoral analysis or undertaking a study

on a regional or local level. Expanding the requirements of local government’s mandated Integrated

Development Plans to include issues around electricity and the costs of loadshedding to local

economies could one way to achieve this.

The distribution sector and local government

There are over 170 licensed electricity distributors in South Africa. Eskom serves 48% of customers in

the country and municipalities serve 52%. The current position in the electricity distribution industry is

the result of its historical development. Before 1994, municipalities distributed electricity in historically

white areas, while Eskom covered historically black townships and some of the former so-called

homelands. The table below sets out the position.

Estimated number of Customers Estimated Sales Per Category MWh

Category

Eskom Municipalities Total Eskom Municipalities Total

Domestic 3 376 276 3 470 054 6 846 330 7 965 000 26 109 593 34 074 593

Agriculture 78 433 20 621 99 054 4 358 000 784 918 5 142 918

Mining 1 180 823 2 003 33 372 000 26 774 133 33 639 741

Manufacturing 2 988 40 964 43 952 53 715 000 22 234 526 75 949 526

Commercial 43 880 199 332 243 212 6 936 000 14 135 177 21 071 177

Transport 511 1 642 2 153 3 182 000 2 383 011 5 565 011

General 1 771 34 334 36 105 1 429 628 13 916 728 15 346 356

Total* 3 505 039 3 767 770 7 272 809 110 957 628 79 831 694 190 789 322

*An increase of 13% to each category would be a reasonably accurate update to 2015

The municipalities do not only have residential customers, they also service industrial/manufacturing,

commercial and even mining companies but Eskom itself, measured on capacity, distributes

significantly more electricity to customers directly than all the municipalities put together. Twelve of

the largest municipalities account for about 80% of electricity distributed by all municipalities. The

remainder are small and mostly uneconomic.

We have come to see dependence of local government on electricity (and more particularly the

surpluses it generates) puts local government in a bind. We saw this with the collapse of a programme

to rationalise distribution into a number of Regional Electricity Distributors (REDs) in 200937. There are

several reasons why the REDs initiative was not successful but the unresolved financial implications on

local government’s finances was amongst the primary reasons.

To a very large extent, the question of what to do in place of having REDs has not been adequately

resolved and this is becoming a critical issue. Nersa, which in terms of the Electricity Regulation Act

undertakes audits of distributors, shows up a progressive deterioration of plant amongst many of the

distributors, particularly the smaller municipalities. The audits verify whether the planned network

maintenance and inspections are conducted as planned and assessments are conducted on electrical

assets in substations, mini-substations, pole mounted transformers, switching stations of secondary

substations and overhead lines to gain an understanding of the condition of the electrical network.

The poor state of many local networks has been known for a long time. More recently, the amount

of money owed to Eskom by certain municipalities has brought the matter of failing small local

municipalities back into focus.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

14 info@erln.org.zaOther than the abandoned REDs initiative. There was a plan to turn this around called the “approach to

distribution asset management (ADAM), a comprehensive, multi-year initiative targeted at addressing

maintenance, refurbishment and strengthening shortcomings. Other initiatives included a master plan

for standardisation and centralised purchasing of equipment for upgrades.

Given the financial benefit of being able to distribute electricity, one suggestion has been to allow

local distributors in small municipalities to retain their electricity businesses and to provide them with

intensive and sustained support. To do this, however, it would be necessary to develop ring-fenced,

corporatised, effectively regulated and well-managed utilities, with adequate investment in physical and

human capital. If this were to occur, large corporatised municipal distribution companies could play a

much larger role in future.

Local government’s revenue model and the role of electricity

Municipalities themselves use electricity as a tax to cross subsidise their other activities. In the large

metro’s, electricity sales make up as much as a third of total revenues38:

35 34%

32%

30% 30%

30 28% 28%

27%

26%

24% 24%

25

20

15

10

5

0

07/08 08/09 07/08 08/09 07/08 08/09 07/08 08/09 07/08 08/09

Johannesburg Cape Town Tshwane eThekwini Nelson

Mandela Bay

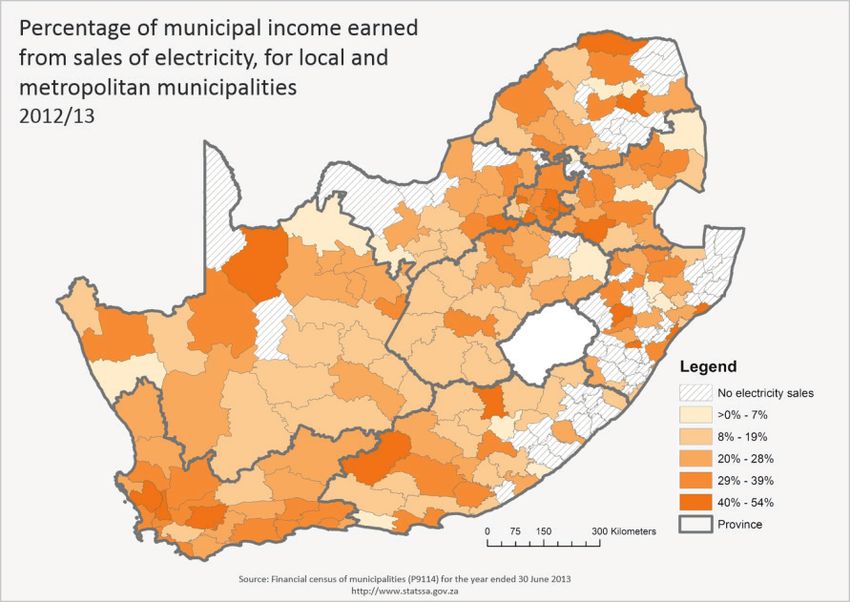

The amount of income earned by municipalities does, however, vary greatly. The figure below is from a

June 2015 STATSSA report39.

While electricity was as cheap as it has been, the local government has used the supply of electricity in

a manner somewhat similar to an income tax. As seen from the tables above, the operational surpluses

that electricity sales generate contribute as much as 15% of total municipal income (and in some cases

ERLN is an initiative of Produced for ERLN by www.erln.org.za

15 info@erln.org.zamuch higher). It is the only local government service for which it charges consumers that makes any

significant contribution to the general budget. Without the contribution of electricity “surpluses”, local

government budgets would be significantly affected.

As electricity becomes more expensive, the ability to subject its supply to a surcharge or tax becomes

more difficult. It also puts local government, as least as far as its revenue model is concerned, on the

wrong side of important efforts to reduce exposure to load shedding, get behind energy efficiency, deal

with the introduction of embedded generation, undertake demand response efforts and commence with

the development of local procurement. If the retention of surpluses from electricity remains an important

source of funding for local government, none of these initiatives will succeed and local government will

remain exposed to the necessary changes that will have to happen in our national electricity system.

As shown above, local government has a far greater exposure to residential consumers than Eskom

itself. While the residential sector represents only about 17-18% of total electricity consumption, it is

characterised by peaks in the early morning and the early part of the evening. During these peak times,

the residential sector makes up 35% of Eskom’s generating capacity40.

Electricity Consumption Peak Demand

2% 2%

4% 4%

10% 10%

Industry

Mining

Residential 35%

14%

49% 17%

Agriculture

Transport

Commerce

18%

35%

As one would expect, these peaks become more pronounced in winter.

Eskom report to Parliament (p 25).

In terms of demand, there is the need for more than one full power station between daytime

consumption and the evening peak in winter.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

16 info@erln.org.zaResidential pricing has become rather complicated. As one would predict in a progressive tax

system, local government uses inclining block tariffs (IBT) in terms of which the more electricity that is

consumed, the more one pays per kwh. This has important consequences. One study41 showed that

since the introduction of IBT, a municipality in Gauteng has lost R53 million and now owes Eskom R200

million while a Free State municipality lost R75 million.

Poorer customers using less than 350kwh per month are supplied electricity at below what it costs

to provide it. This does not take into account illegal connections and the free allocation of 50kWh/

month. That being said, poor customers are already stretched beyond breaking point42. The poorest

households already spend 47.7% of household income on food and 32% on housing, water, electricity,

gas and other fuels. While the national government provides some support to municipalities to fund

free electricity, a good part of it is done through cross-subsidisation. The graph below43 (using ERC-

UCT44 data) shows the impact of this for higher use customers:

Real Electricity Cost 2006/7 - 2013/14 (June 2013 Rands)

R800

R700

R600

R500

Electricity Cost

R400

R300

R200

R100

R0

2006/7 2007/8 2008/9 2009/10 2010/11 2011/12 2012/13 2013/14

Low (150kWh) R71.28 R70.28 R71.45 R74.03 R76.95 R77.53 R77.88 R80.91

Medium (350kWh) R178.19 R175.69 R178.62 R185.08 R216.91 R230.54 R239.71 R247.22

High (450kWh) R320.74 R316.25 R369.81 R478.23 R555.92 R608.47 R628.66 R643.47

Source: ERC - UCT

As an aside, many poor households are charged using the highest tariffs. If a single electricity

connection is shared between several households as is often the case in informal settlements, then

that single connection would be charged on the highest tariff, losing out on the 50kwh free electricity

allocation.

The cross-subsidy only works when there are sufficient high consumption users in the system. One

calculation shows that it is only those residential customers that consume over 600kWh per month

that generate surpluses45.The commercial sector generates significant surpluses but high voltage

(HV) industrial customers mostly have a neutral impact. If the type of customers that provide the cross

ERLN is an initiative of Produced for ERLN by www.erln.org.za

17 info@erln.org.zasubsidy are no longer in part of the system, it doesn’t work. Cross-subsidies in electricity tariffs are

inevitable in a country such as South Africa but these should be levied transparently. Local government

should make the effort to establish and publicise the average level of cross-subsidy between customer

categories so that customers are made aware of it.

Cheap electricity has become woven into our public finances. Cheap electricity has been used to fund

other things. It is also embedded into the social welfare system. When electricity was cheap, it was

easy to fund low-income users via a basic free allocation and the inclining black tariffs. When these

assumptions change, as they must do, what are the implications? We have already seen the results of

this with over-indebted municipalities.

Poorer or indigent households are in no position to pay more for their electricity consumption and

already in large parts of those areas enjoying an electricity connection for the first time, electricity

theft is becoming a bigger problem46. We should understand that electricity subsidies are becoming

unsustainable. We need to quantify these at different electricity cost levels and move them to the social

welfare budget. This has important consequences for our national budgeting processes. Our welfare

budget has already grown substantially and there is a limit to how much further it can grow

The problem of data

There is very little data about patterns of electricity consumption and such data that does exist,

exists in isolation and is not collated or combined. As such, it cannot be analysed to produce any

valuable insights on a suburb-by-suburb scale. We can produce a macro picture but not with sufficient

granularity.

The disciplines of ETL (Extract, Transform and Load) have not been implemented to any great degree.

We need to get to the point where disparate data from several heterogeneous sources is transformed

and stored in a common format that renders it usable by analysis tools.

For example, municipalities have SCADA systems (a supervisory control and data acquisition) on main

transformers or injection points, but very few are metered. Very little data exists in real time. Far better

informed decisions could be made if data about electricity consumption could be collected on a sub-

station level, even before time-of-use metering is rolled out.

When Eskom provided a reliable, abundant and cheap source of electricity, it was not important to

understand electricity consumption by consumers. Electricity utilities around the world are undergoing

fundamental change47. Far more expensive electricity will drive changes to the traditional municipal

electricity revenue models48 in ways that are not yet clear to us49. Questions of how to maintain the grid

will become important policy issues50

Change will be difficult at an institutional level within electricity departments but to help everyone

understand what is at stake, better information will make the arguments for change clearer.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

18 info@erln.org.zaSmart-meters and smart grids – a key consideration for

municipalities in unlocking the economic opportunities at

sub-national level

Most local governments are on Eskom’s Megaflex package. This means that local government is

subject to different time of-use-tariffs but residential consumers are not.

As electricity becomes more expensive, the response will be to conserve electricity but this is likely

to make the difference between daytime usage and the peaks even greater. Those consumers who

provide most of the cross subsidy (or the biggest contribution to the surpluses from electricity sales) are

getting to the point where alternatives such as PV installations reach “socket parity”. These customers

don’t leave the system entirely but remain grid tied – using municipal-supplied electricity at peak times

alone. In this way, instead of being net contributors or “surplus generators”, they will also be supplied

at a loss. One study showed that the revenue impact of embedded generation can be as much as 60%

of a municipality’s electricity gross profits51. If this were to happen, the ability to cross-subsidise poor

households, something already under pressure, would no longer exist.

At the same time, municipalities must encourage electricity savings, particularly during peak times and

maintain a financially sustainable electricity supply to consumers, without cutting out cross-subsidies.

Local government, as an electricity distributor, charge residential customers using a flat rate. The cost

of supply to a local authority during winter might look something as follows:

ERLN is an initiative of Produced for ERLN by www.erln.org.za

19 info@erln.org.zaDifference between Eskom Peak Pricing and fixed Inclined Block Tariff means no incentive to save

electricity during peak times. Increasing electricity prices mean consumers save more electricity but

savings are mostly during off-peak times. This makes peaks more intense. During winter peaks, even

some high tariff residential customers are supplied at a “loss” described in the graphic below:

If local government/electricity distributors can encourage changes in residential customer behaviour

change by moving to time-of-use pricing – (i.e. charging customers different rates for different times

of the day), then municipal profitability increases even as less electricity is consumed. Customers are

incentivised to reduce peak-time demand when rates are higher and defer usage for cheaper time slots

instead. In essence, the cost of inefficient electricity usage shifts to the customer.

The graphic below shows the stylised position (spreadsheets generating graphics available) for high

tariff users in the winter months and how, with time-of-use metering, this would change. Importantly, it

also shows the position once changes in consumption habits are made. It is possible that under certain

tariff structures the consumer might be able to reduce the electricity bill.

The graphic below shows the position from the distributor’s/local government’s point of view. While

the consumer has reduced his/her bill, the gross profit margin and the cumulated net profit amount

increases.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

20 info@erln.org.zaThere are very few win/win opportunities in our electricity sector. Time-of-use metering is one of these.

The implementation of smart-metering programmes is something that requires special attention

though. In this regard, we need to be sure to avoid single supplier lock-in. In this regard, standard

specifications for Smart Meters are crucial before going down this road. Future-proofing metering

solutions is best achieved by securing “optionality”, not vendor lock-in.

Any time-of-use metering programme must thus be guided by the requirement that the programme

needs to produce a given ROI within a set period. Over-complicating the meters or insisting on “Smart

Meters” could increase costs with marginal return. For example, simple time-of-use meters have 80%

of the functionality of fully-fledged smart meters for less than 20% of the cost.

Options could include:

• An incremental implementation path where “learning” takes place within electricity departments

should be undertaken.

• Maintaining control of the protocol to communicate to the time of use meters fitted/deployed.

• Other aspects than must be controlled include:

o the management platform.

o the ERP applications.

o the access network (for security and liability) and the on-boarding process for meter

manufacturers.

o the manufacturing of the meters can be done locally provided that the local authority

concerns provides a certification process to approve meters, management platforms and

access networks.

ERLN is an initiative of Produced for ERLN by www.erln.org.za

21 info@erln.org.zaThe future

With the rapidly declining price of renewable energy (RE) – especially wind and solar PV – along with

the massive increases in energy efficiency across all products (from lighting, to cars, to fridges and

industrial machinery) the future landscape for energy is changing.

Michael Leibrech in his keynote address to the 2015 Bloomberg New Energy Future52 conference

notes that a shift is taking place in the power system value chain – a shift from an old world dominated

by energy extraction and generation to a future where the key rests with responses to demand and

managing distribution. It is also a shift from a centralised view of energy to a far more localised and

distributed approach to managing and delivering energy. The challenges for municipalities in this space

are only going to grow – as are the economic potentials and opportunities.

How we respond now will be critical to unlocking that value, build our energy security and contribute

productively to our economic development.

POWER SYSTEM VALUE CHAIN

Old World

Extraction Generation Transmission Distribution Demand

$$$

$$$

Age of Plenty

Extraction Generation Transmission Distribution Demand

ERLN is an initiative of Produced for ERLN by www.erln.org.za

22 info@erln.org.zaEndnotes

1 http://www.bloomberg.com/company/new-energy-outlook/

2 http://www.gsb.uct.ac.za/files/BusinessDay_newspaper_article.pdf

3 http://www.eskom.co.za/OurCompany/CompanyInformation/Pages/Company_Information_1.aspx

4 http://www.power-technology.com/features/featurethe-top-10-biggest-power-companies-

of-2014-4385942/

5 http://www.power-technology.com/features/featurethe-top-10-biggest-power-companies-

of-2014-4385942/

6 http://en.wikipedia.org/wiki/List_of_countries_by_GDP_%28PPP%29

7 http://www.eskom.co.za/news/Pages/IR2014.aspx

8 http://businesstech.co.za/news/general/36163/biggest-companies-in-south-africa/

9 http://www.eskom.co.za/OurCompany/CompanyInformation/Pages/Company_Information_1.aspx

10 http://www.bdlive.co.za/business/energy/2014/09/01/power-crisis-too-big-for-medupi-says-

eskom

11 http://www.gsb.uct.ac.za/files/AEFPowerShortages-Nice08.pdf

12 http://m.engineeringnews.co.za/article/eskom-warns-on-ipp-connections-as-it-defers-some-

transmission-capex-2014-10-10/rep_id:3182

13 http://www.eskom.co.za/OurCompany/CompanyInformation/Pages/Company_Information_1.aspx

14 http://www.power-technology.com/features/featurethe-top-10-biggest-power-companies-

of-2014-4385942/

15 http://cleantechnica.com/2013/09/30/average-electricity-prices-around-world/

16 http://www.sajs.co.za/sites/default/files/publications/pdf/Thopil_Review%20Article.pdf

17 http://www.nersa.org.za/Admin/Document/Editor/file/Consultations/Electricity/Presentations/

Eskom%20-%202.pdf (page 16)

18 http://www.sapvia.co.za/wp-content/uploads/2013/04/NERSA-final-presentation-on-MYPD3-

determination.pptx 2013-2018

19 https://ideas.repec.org/p/rza/wpaper/204.html

20 http://www.eiug.org.za/about/

21 http://www.tradesecrets.co.za/pdf/sec3-1.pdf

ERLN is an initiative of Produced for ERLN by www.erln.org.za

23 info@erln.org.za22 http://www.eskom.co.za/CustomerCare/MYPD3/Documents/Economic_Impact_of_Electrcity_

Price_Increases_Document1.pdf

23 http://www.treasury.gov.za/publications/other/epir/Electricity.pdf

24 http://www.eskom.co.za/Whatweredoing/SupplyStatus/SupplyStatus/AdeqRep2015w24.swf

25 http://proceedings.eceee.org/visabstrakt.php?event=3&doc=2-506-13

26 http://www.sanedi.org.za/sanedi-road-show/

27 http://www.iea.org/newsroomandevents/pressreleases/2014/september/name-125300-en.html

28 http://www.iea.org/Textbase/npsum/MultipleBenefits2014SUM.pdf

29 http://thinkprogress.org/climate/2014/01/29/3220341/energy-economic-growth/

30 http://www.washingtonpost.com/blogs/wonkblog/wp/2014/01/17/can-we-sever-the-link-

between-energy-and-growth/

31 http://www.egi-sa.org.za/wp-content/uploads/2013/05/smartelectricityplanningreport-060520132.

pdf Page 29-32.

32 http://www.csir.co.za/docs/Financial%20benefits%20of%20Wind%20and%20PV%20in%20

2014-%20CSIR%20-%2021Jan2014_FINAL.pdf

33 http://www.doe-irp.co.za/content/IRP2010_updatea.pdf

34 http://www.doe-irp.co.za/factsheets/S1_Cost_of_Unserved_Energy.pdf

35 http://www.enca.com/money/eskom-blackouts-cost-sa-much-r80bn

36 http://www.rdm.co.za/business/2015/02/11/how-load-shedding-hurts-the-economy

37 http://www.dailymaverick.co.za/article/2010-11-23-sa-electricity-distribution-industry-

government-goes-back-to-the-drawing-board#.VW2LYUbVHIU

38 http://proceedings.eceee.org/papers/proceedings2013/2-506-13_Covary.

pdf?returnurl=http%3A%2F%2Fproceedings.eceee.org%2Fvisabstrakt.

php%3Fevent%3D3%26doc%3D2-506-13

39 http://www.statssa.gov.za/?p=4772

40 http://www.90x2030.org.za/oid%5Cdownloads%5CFinal%20smart%20electricity%20

planning%20report%206%20May%202013.pdf Extracted from (p27)

41 http://www.ee.co.za/wp-content/uploads/2014/11/AMEU-Convention-2014-p32-40.pdf

42 http://www.ee.co.za/article/south-africa-electricity-pricing-paralysing-poor.html

ERLN is an initiative of Produced for ERLN by www.erln.org.za

24 info@erln.org.za43 http://www.ee.co.za/article/south-africa-electricity-pricing-paralysing-poor.html

44 http://www.erc.uct.ac.za/

45 http://www.ee.co.za/wp-content/uploads/2014/11/AMEU-Convention-2014-p32-40.pdf

46 http://www.ee.co.za/article/eskoms-energy-revenue-loss-management.html.

47 http://www.utilitydive.com/news/how-new-york-is-reinventing-the-electric-utility/262727/

48 http://www.bloomberg.com/news/articles/2015-06-23/the-way-humans-get-electricity-is-about-

to-change-forever

49 http://www.ilsr.org/report-energy-democracy/

50 http://www.nationaljournal.com/policy/insiders/energy/should-consumers-bear-the-cost-to-

upgrade-the-grid-20140317

51 http://www.ee.co.za/wp-content/uploads/2014/11/AMEU-Convention-2014-p51-55.pdf

52 https://vimeo.com/125066482

ERLN is an initiative of Produced for ERLN by www.erln.org.za

25 info@erln.org.zaYou can also read