COVID-19 Government Stimulus Programs - AARON REILLY, MBA, CPA, LPA PARTNER, REILLY BACK LLP

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

COVID-19 Government Stimulus Programs A A R O N R E I L LY, M B A , CPA , L PA PA R T N E R , R E I L LY B ACK L L P

Agenda • Tax Deadline Changes • 10% Wage Subsidy • Canada Emergency Wage Subsidy (CEWS) • Canada Emergency Small Business (CEBA) Loan • Canada Emergency Response Benefit (CERB) • BDC/EDC Business Loan Program • Canada Emergency Commercial Rent Assistance (CECRA) • Other COVID related considerations

Tax Deadline Changes

• Personal tax returns:

• Deadlines have passed – June 1st for non-self employed individuals, and June 15th for self-employed

(T2125) individuals – however the CRA has announced that any returns filed by September 1, 2020 will

not be assessed a late filing penalty

• Why the June 1 deadline if payment is due September 1? It could impact payment amounts for

programs like the Canada Child Benefit or the GST/HST credit. Any balances owing are due on

September 1, 2020.

• Corporate income tax returns:

• Return filing: if return was due after May 30, new deadline is September 1

• Amounts owing: Part I tax due after March 18 can be paid by September 1 without penalty, however

no extensions in Part IV tax (ie. tax on dividend income)

• HST

• Return filing: deadlines are unchanged.

• Amounts owing: any amount that became owing from March 27 onward can be paid by June 30

without penalty

• Trust and Charity Return deadlines have also been extended – consult your accountant.10% Wage Subsidy - Overview • How much? 10% of remuneration between March 18 and June 19, up to $1,375 per employee and $25,000 per employer. • How to claim? Reduce source deduction remittances for income tax (not CPP or EI) by eligible amounts. • Eligible entities: Individuals (excluding trusts), corporations (must be a Canadian Controlled Private Corporation or CCPC), non-profit organizations, registered charities, and partnerships who had a payroll account as of March 15, 2020. • Eligible employees: employed in Canada other than individuals who weren’t paid for 2 weeks or more during the eligible period. Non-arm’s length employees are limited based on average pay from Jan. 1 – Mar 15. • Eligible remuneration: Salary and wages. Excluded: severance, stock options, personal use of corporate vehicle.

10% Wage Subsidy – Important notes

• What if I missed reducing my source deductions for the subsidy?

• When filing payroll return at the end of the year, the CRA will allow you to

calculate how much you should have claimed and refund the difference.

• What do I need to report to CRA?

• CRA has yet to release the document – but a self-identification form will need to

be submitted indicating if you did or did not claim the 10% subsidy.

• Is this taxable?

• Yes, all government related COVID-19 stimulus programs are taxable.Canada Emergency Wage Subsidy (CEWS) • A 75% wage subsidy, up to $847/week per employee. • Eligible entities: Individuals (including trusts), taxable corporations, non-profit organizations, registered charities, and partnerships who had a payroll account as of March 15, 2020. • Eligible employees: employed in Canada other than individuals who weren’t paid for 2 weeks or more during the eligible period. Non- arm’s length employees are limited based on average pay from Jan. 1 – Mar 15. • Eligible remuneration: Salary and wages. Excluded: severance, stock options, personal use of corporate vehicle.

CEWS – Periods covered and Revenue drop

Period Revenue drop required* Salary period

March 15% March 15 to April 11

April 30% April 12 to May 9

May 30% May 10 to June 6

• Two benchmark options exist for measuring revenue drop:

• 1) Comparing year over year (ie. March 2020 vs. March 2019)

• 2) Comparing to first two months of 2020 (ie. March 2020 vs. average of Jan/Feb 2020)

• Government has officially extended CEWS to August 29 and is currently

reviewing revenue thresholds and requirements for these periods. Legislation

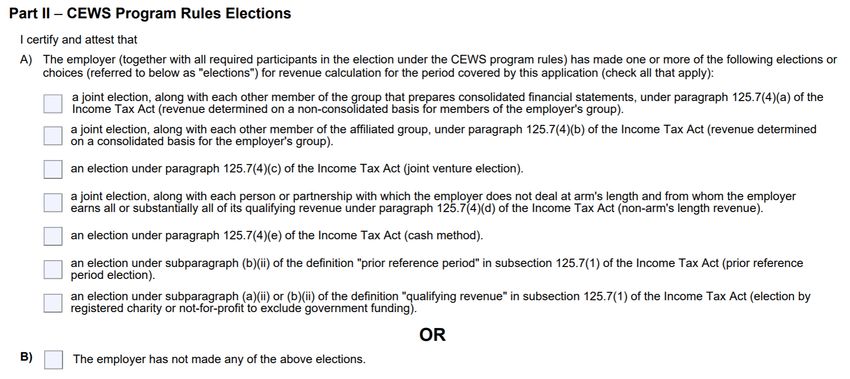

regarding this has yet to be passed by Parliament as of June 16, 2020.CEWS – Other important notes • Can use either cash or accrual method for accounting, as long as application is consistent throughout the application. • Qualifying for one CEWS period will automatically qualify you for the subsequent period. • Any benefit received from CEWS should be reduced by the 10% wage subsidy or the EI work share program. • Specific rules exist around revenue measurement for large groups of companies and charities/not-for-profit organizations – consult your accountant! • When applying to use cash method of revenue measurement, or using a different benchmark – an election must be made on your on your application or RC661 if being filed by your accountant. • Deadline to submit is September 30, 2020.

CEWS – Audit risks and words of warning • Repayment of amounts received and 25% penalty for non-compliance, and an additional 200% penalty for fraudulent claims. • Collection risk: program is administered through payroll account – thus similar to unremitted source deductions, there exists potential for section 227.1 of the Income Tax Act to apply – which expands the CRA’s ability to target corporate directors when efforts to collect against the corporation are futile. • Income suppression in an effort to qualify for CEWS could raise questions as to whether HST has been filed correctly. • When auditing for CEWS, it could provide CRA the opportunity to look into employee status (ie. contractor vs. employee) • Keep your records in a safe place – and if you made a mistake you can amend your application before any penalties/interest come into play.

Canada Emergency Business Account (CEBA) Loan • $40,000 loan with 0% interest until December 31, 2022, with $10,000 forgiven (and taxed) if $30,000 is repaid by December 31, 2022. • Eligibility requirements: registered business as of March 1, 2020, with 2019 payroll between $20,000 and $1,500,000. • Restrictions on use: funds can only be used for non-deferrable operating expenses including: payroll, rent, utilities, insurance, property tax and regularly scheduled debt service, and may not be used to fund any payments or expenses such as prepayment/refinancing of existing indebtedness, payments of dividends, distributions and increases in management compensation.

Canada Emergency Business Account (CEBA) Loan • What if my payroll is below $20,000? • You will also qualify if you have non-deferrable expenses between $40,000 and $1,500,000 • What if am paid with dividends? (no payroll) • You can qualify based on the same criteria above. • CRA will audit these programs – and accounting records showing clear use of funds for non-deferrable expenses should be kept.

Canada Emergency Response Benefit (CERB) • $500 per week for up to 16 weeks for employees that have lost income or out of work due to COVID • Eligibility requirements: minimum 2019 income of $5,000 or the past 12 months prior to application, however must have not had more than $1,000 of income in month prior to application • Definition of income: tips earned while working; non-eligible dividends; honoraria (e.g. nominal amounts paid to emergency service volunteers); and royalties (e.g. paid to artists) received. Pensions, student loans and bursaries are not included. • Fully taxable, with no income withheld at source, thus taxpayer’s must plan for eventual tax plan if drawing on this • Applications accepted up to December 2, 2020, and Federal Government has announced an extension of an additional 8 weeks beyond July • CRA will be reviewing employer payroll records against CERB claims, and any amounts received in error must be repaid prior to December 31 to avoid penalties.

BDC/EDC Loan Program • The Business Development Bank of Canada and Export Development Canada is working with financial institutions to guarantee and co- lend for amounts up to $6.25M for small and medium size entities. • A full loan application process and due diligence will still need to occur similar to a traditional business loan, and there must be a clear ability to pay loans back post COVID. • Cashflow projections and a management business plan for COVID and post-COVID must be presented as a part of the application.

Canada Emergency Commercial Rent Assistance (CECRA) • Property owners will reduce rent by at least 75 % for the months of April and May (retroactive), and June, for their small business tenants. CECRA will cover 50 % of the rent, with the tenant paying up to 25 % and the property owner forgiving at least 25 %. • How to apply? • A request must be made to landlord to start process – and landlord must submit an application. Program is voluntary and landlord participation is not mandatory. • Landlord will receive a loan equal to 50% of gross rent from tenant – with remaining 25% of still coming from tenant. Loan will be forgiven on December 31, 2020 assuming landlord has met all criteria.

Other COVID related accounting considerations • CRA has indicated employer reimbursements of up to $500 for personal-use computer equipment will not be a taxable benefit for employees. • Home office expenses – can they be written off because of COVID? CRA is currently reviewing these rules and will likely allow write-off for period in which restrictions in place. Best advice is to keep your records for next tax season as we await clarification on how these rules will work. If you are able to get a signed T2200 Conditions of Employment from employer for 2020 indicating home office expense eligibility, this is likely a good start.

Other programs not discussed but available • Canada Emergency Student Benefit (CESB) • Canada Student Service Grant (CSSG) • Increase to Canada Child Benefit by $300/child • Reduced minimum RRIF withdrawal by 25% for 2020 • Work Sharing Program extended from 38 weeks to 76 weeks • WSIB Premiums deferred for up to 6 months for certain employers • Employer Health Tax (EHT) exemption raised from $490k to $1M for 2020

Questions?

If I can be of any assistance, please feel free to contact me:

Aaron Reilly

e-mail: aaron@reillybackllp.com

phone: 905-477-4262You can also read