DELTA VARIANT INTERRUPTS RECOVERY - U.S. Economic Outlook SEPTEMBER 2021 - Morning Consult

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DELTA VARIANT

INTERRUPTS

RECOVERY

U.S. Economic Outlook

SEPTEMBER 2021

Copyright © 2021 Morning Consult. All Rights Reserved.

ABOUT THIS REPORT

Morning Consult’s monthly U.S Economic Outlook report

provides an integrated assessment of the strength of U.S.

consumers, workers and households.

Businesses and investors rely on this report to understand

emerging trends in consumer demand, employment and

personal finances.

The report draws on Morning Consult Economic Intelligence,

a high-frequency, global economic dataset, reflecting over 11,000

daily economic surveys across the 15 largest global economies.

2

TABLE OF CONTENTS

U.S. Economic Outlook: September 2021 4

Consumer Confidence 7

Employment 16

Spending and Spending Intentions 27

Price Expectations 36

Personal Finances, Consumer Credit and Housing 40

Methodology 52

3

D E L T A V A R I A N T I N T E R R U P T S R E C OV E R Y : U . S . E C ON OMI C OU T L OOK

U.S. ECONOMIC OUTLOOK:

SEPTEMBER 2021

SUMMARY

In August, a resurgent pandemic further undermined the U.S. economic recovery, as the Delta variant drove cases and

hospitalizations up to levels not seen since January. Consumer sentiment fell sharply as hopes of nearing an end to the

pandemic were dashed. While layoffs and unemployment remained stable in August, real consumer spending likely fell

for the second consecutive month. Should lagging confidence derail the anticipated switch from consumer goods to

service sector spending this fall, rosy forecasts for second half U.S. real GDP will likely need to be downwardly revised.

Consumer confidence and spending: Morning Consult’s Index of Consumer Sentiment has fallen sharply since the beginning of

1 July and is now at its lowest level since February 2021, as the 7-day moving average of new COVID cases reaches levels not seen

since winter. Retail sales likely contracted in August for the second consecutive month, but emerging trends in the data indicate that

spending will turn the corner in September. The U.S. wasn't alone in terms of deteriorating confidence. Large exporting economies like

Brazil and Germany experienced the two largest decreases in confidence in August, draining momentum from the global recovery.

Employment: The increase in COVID-19 cases pushed the U.S. jobs recovery into a holding pattern. Pay and income losses stalled

2 in August, which is better than Q3 2020 when increasing case counts led to additional layoffs. Morning Consult's unemployment rate

remained essentially unchanged last month. Looking ahead, employed workers remain relatively optimistic about keeping their jobs

for the next month, and they grew increasingly open to looking for new positions.

Personal finances: A growing share of consumers struggled to pay their bills in July leading to a 3-percentage point increase in

3 missed housing payments. These deferred liabilities are artificially inflating American's savings accounts: Once homeowners and

renters make their housing payments, their savings will decrease, likely resulting in increased financial vulnerability.

5

ECONOMIC INDICATORS DASHBOARD

CURRENT PERIOD PRIOR PERIOD CHANGE I M PA C T

Consumer Confidence

ICS 91.6 94.1 -2.5 pts N E G AT I V E

Employment

Lost pay/income 12.5% 12.1% 0.4% N E G AT I V E

Unemployment rate 14.1% 14.0% 0.1% N E G AT I V E

Labor force participation rate 53.6% 53.9% -0.3% N E G AT I V E

Employment to population ratio 46.0% 46.3% -0.3% N E G AT I V E

Personal Finances

Fell short of paying bills 16.5% 13.7% 2.4% N E G AT I V E

Financial vulnerability (unable

to pay basic expenses for a full 21.4% 21.9% -0.5% POSITIVE

month using just savings)

6

D E L T A V A R I A N T I N T E R R U P T S R E C OV E R Y : U . S . E C ON OMI C OU T L OOK CONSUMER CONFIDENCE

C ON S U ME R C ON F I D E N C E

Consumer confidence falls further in August

Morning Consult Daily U.S. Index of Consumer Sentiment

120

March 11, 2020: Dec. 27, 2020: Jan. 20, 2021:

115 WHO declares President Trump signs President

COVID-19 a pandemic second coronavirus Joe Biden’s July 7, 2021:

relief package into law inauguration Consumer

110 confidence begins to

March 13, 2020:

March 9, White House declares national fall amid COVID

105 2020: surge

emergency over coronavirus pandemic

Dow Jones

100 Industrial Nov. 3, 2020:

Average sees March 27, 2020: Election day

95 its worst drop President Donald Trump signs

since 2008 CARES Act into law

90

85

March 6, 2021:

80 Senate passes

Sept. 15, 2020: $1.9 trillion

75 Average daily COVID-19 economic relief bill

cases begin rising again

70

0

1

0

0

1

1

0

0

20

20

1

0

0

1

0

0

1

1

0

1

-2

-2

-2

-2

-2

-2

-2

-2

-2

l-2

l-2

2

2

2

2

2

2

2

n-

n-

n-

n-

g-

p-

-

-

g-

r

r

ar

ar

ay

ay

b

b

ct

ov

ec

Ju

Ju

Ap

Ap

Ja

Ju

Ja

Ju

Au

Se

Au

Fe

Fe

O

M

M

N

D

M

M

Source: Morning Consult Economic Intelligence

8

C ON S U ME R C ON F I D E N C E

Delta variant surge continues to drive decline in sentiment

• Morning Consult’s Index of Consumer Sentiment

New cases, 7-day moving average (LHS) ICS, 5-day average (RHS) (ICS) continued to fall in August as the Delta variant

surge saps confidence across the U.S.

300,000 105

• The index has fallen sharply since the beginning of

250,000 100 July and is now at its lowest level since February

2021, as the 7-day moving average of new COVID

200,000 95 cases reaches levels not seen since winter.

150,000 90 • Amid the surge, U.S. adults are increasingly

unwillingly to take part in many activities that could

put them at risk. According to an Aug 19-22 survey,

100,000 85

62% of adults said they were comfortable dining in a

restaurant, down from 71% at the beginning of July.

50,000 80

• With optimistic economic projections dependent on

0 75 consumption shifting from goods to services this fall,

plummeting sentiment will likely lead to downward

1

1

1

0

0

20

20

1

0

1

1

1

1

-2

-2

-2

-2

-2

l-2

2

2

2

2

2

n-

n-

g-

p-

-

-

g-

r

ar

ay

b

ct

ov

ec

Ju

revisions to real U.S. GDP forecasts.

Ap

Ja

Ju

Au

Se

Au

Fe

O

M

N

D

M

Source: Morning Consult Economic Intelligence, Our World in Data, Johns Hopkins University CSSE COVID-19 Data

9

C ON S U ME R C ON F I D E N C E

Consumers most worried about future business conditions and inflation

• The recent decline in consumer sentiment has Change in ICS and each of its components (July 1-Aug 23)

primarily been driven by a deterioration in views

toward future business conditions. Business Business Personal Personal

Conditions: 12 Conditions: 5 Finances: Finances: 12

Month Year Current Buying Current Month

• Since the beginning of July, 12-month expectations Expectations Expectations Conditions Conditions Expectations

for future business conditions have fallen 12.7%,

while 5-year expectations have fallen 11.5%. This

compares to only 5.6% and 4.9% for current and

12-month expectations for personal finances.

-4.9%

-5.6%

• This disparity suggests that pessimism is still being -6.7%

driven more by outward fears, rather than negative

impacts to household balance sheets.

• Consumers are also worried about rising prices,

-11.5%

with views toward current buying conditions falling

-12.7%

6.7% over the last two months. However, the bulk

of this decline occurred in July, indicating inflation

fears moderated in August.

Source: Morning Consult Economic Intelligence

10C ON S U ME R C ON F I D E N C E

Sentiment stabilizing somewhat among highest earners

• As of Aug. 23, sentiment among the highest

Morning Consult U.S. Index of Consumer Sentiment

income segment – households earning above

By annual household income

$100,000 – has stabilized as the stock market

Rolling 30-day % change

hit record highs. This group is also typically

Adults Less than $50,000 $50,000 - $100,000 Over $100,000 somewhat shielded from high rates of wage

15% income loss.

10%

5% • Despite this respite among high income adults,

consumer sentiment continues to fall overall,

0%

with the last reading for the 30-day change for

-5%

all adults still at -3.9% as of August 23.

-10% Sentiment among those earning less than

-15% $50,000 had the worst 30-day decline at 4.6%.

-20%

-25% • Cooling sentiment likely weighed further on

-30% spending in August, following a 0.14%

contraction in real personal consumption

-35%

expenditures in July. Changes in Morning

Fe 0

20

Fe 1

21

Ju 0

Ju 1

Au 0

Au 1

M 0

N 0

M 1

M 0

Ap 0

M 1

Ap 1

Se 0

20

D 0

Ja 0

21

l-2

l-2

2

-2

2

2

-2

2

-2

2

-2

-2

2

2

-2

-2

Consult’s ICS remain highly correlated with

g-

p-

g-

n-

n-

n-

n-

r-

r-

b-

b-

ov

ec

ct

ay

ay

ar

ar

Ju

Ju

Ja

O

changes in real consumer spending.

Source: Morning Consult Economic Intelligence

11C ON S U ME R C ON F I D E N C E

Consumers’ views of their finances deteriorate across the country

Morning Consult Personal Finances: Current Conditions Index

% change since Jan 2020

-30% -20% -10% 0% 10%

FEBRUARY 2020 APRIL 2020 OCTOBER 2020

JANUARY 2021 MAY 2021 AUGUST 2021

Source: Morning Consult Economic Intelligence. *August 2021 data reflects the 30-day rolling average from July 27 to August 25, 2021.

12C ON S U ME R C ON F I D E N C E

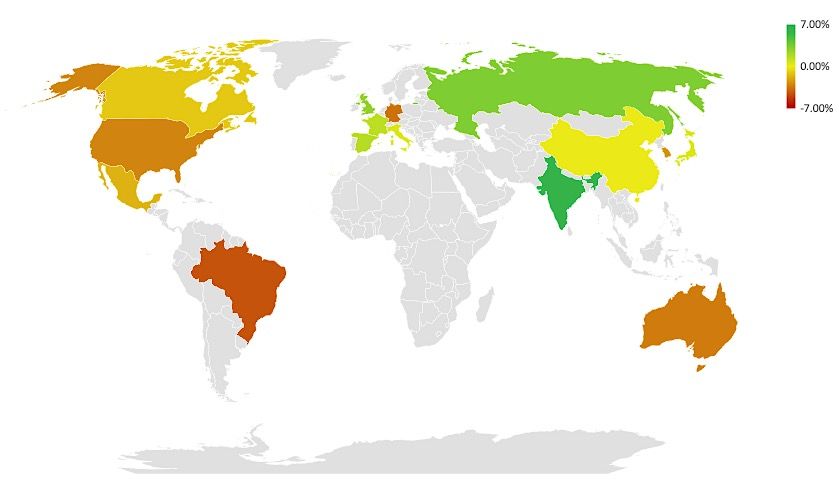

Drop in U.S. sentiment ranks 4th among major economies in August

Morning Consult Index of Consumer Sentiment

Monthly % change

• Among the 15 largest global economies, the

U.S. decline in consumer sentiment in August

was the fourth largest.

• Brazil, Germany, and Australia all saw worse

outcomes than the U.S. in August, with each

economy struggling with COVID-19

resurgences of their own.

• India saw the greatest increase in sentiment,

where an improving public health situation

saw sentiment rise 6.1%. Russia, the U.K.,

and Spain followed India, which saw

sentiment rise 3.3%, 2.8%, and 1.7%,

respectively, in August.

Source: Morning Consult Economic Intelligence, data for August reflects August 1-25, 2021.

13C ON S U ME R C ON F I D E N C E

Vaccines provide key ingredient of consumer recovery

% Change in ICS from Jan 1 to Aug 25, 2021, vs. % of population fully vaccinated

• Higher vaccination rates are strongly 30%

positively correlated with an increase in United Kingdom

consumer confidence since the beginning of

% change in ICS from Jan 1 to Aug 10, 2021

25% Italy Spain

2021.

• While a myriad of factors goes into consumer 20%

Correlation

sentiment readings, vaccinations lay the France = 68.9%

South Korea

foundation for improved public health 15%

outcomes, consumer confidence, spending Japan Canada

and economic activity more broadly. Russia China

10%

• Developing economies that lack the same Mexico

access to vaccinations as Western, 5% Germany

developed countries will continue facing India

additional barriers to stimulating their 0% Australia

economies. United States

-5% Brazil

-10%

0% 10% 20% 30% 40% 50% 60% 70% 80%

% of population fully vaccinated

*Size of bubbles reflect 2020 GDP in USD. Source: Morning Consult Economic Intelligence, Our World in Data, World Bank

14C ON S U ME R C ON F I D E N C E

The U.S. and less-vaccinated developing economies lagging in sentiment rebound

Morning Consult Daily Index of Consumer Sentiment, % Change From

Beginning of Pandemic

10% • With the already sluggish

rebound in consumer sentiment

5% France

China dropping off in recent months,

Japan the U.S. now ranks last among

0%

Australia the 15 largest economies

Russia tracked by Morning Consult in

-5% UK terms of confidence relative to

Canada

-10% Mexico pre-COVID levels.

Germany

-15% India • With sentiment 18.9% below

Brazil January 2020 levels in August,

-20% U.S. the U.S. recovery now ranks

below major developing

-25% economies, which lack the same

access to vaccines or fiscal

-30% firepower available in the U.S.

-35%

-40%

9 9 9 0 0 0 0 0 0 0 0 0 0 0 0 0 1 1 1 1 1 1 1 1

t-1 v -1 c -1 n-2 b-2 r-2 r-2 y -2 n-2 l-2 g -2 p -2 t-2 t-2 v -2 c -2 n-2 b-2 r-2 r-2 y -2 n-2 l-2 g -2

O c No De J a Fe Ma Ap Ma J u J u Au Se O c O c No De J a Fe Ma Ap Ma J u J u Au

Source: Morning Consult Economic Intelligence

15D E L T A V A R I A N T I N T E R R U P T S R E C OV E R Y : U . S . E C ON OMI C OU T L OOK

EMPLOYMENTE MP L OY ME N T

Weekly pay losses ticked slightly higher across all income groups in late August

Share of U.S. adults who lost pay or income in the prior week

• While the Delta variant drove a decrease in U.S. By annual household income

confidence, it has yet to drive a significant increase

in pay or income losses. For the week ending Aug. Adults Less than $50,000 $50,000 - $100,000 Over $100,000

21, 12.5% of U.S. adults reported a loss in pay or 30%

income, close to the same level observed over the

past several months. 25%

• Unlike the second wave of COVID-19 cases from

Oct. – Dec. 2020, the most recent increase in 20%

cases has not disproportionately affected low-

income workers, indicating that recent employment 15%

gains by low-income workers are more resilient to

increases in cases. 10%

• Given the number of workers forced to find

jobs with new employers or in new industries, 5%

elevated levels of pay and income losses are likely

to persist for longer than they would typically. 0%

Au 0

Au 1

Ju 0

Ja 1

Fe 1

Ju 1

Se 0

O 0

D 0

Ja 0

21

M 20

N 20

M 21

M 1

Ap 1

Ju 0

Ju 1

2

-2

-2

-2

l-2

l-2

2

2

2

2

2

2

-2

-2

r-

-

r-

b-

n-

n-

n-

n-

g-

p-

g-

ar

ay

ay

ct

ov

ec

Ap

Source: Morning Consult Economic Intelligence; weekly surveys of a representative sample of 20,000 U.S. adults on average

17E MP L OY ME N T

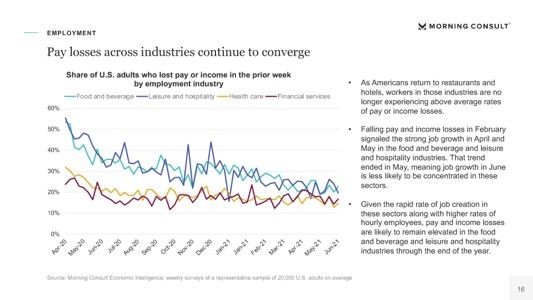

Despite rising cases, weekly lost pay for hospitality jobs remains stable so far

Share of U.S. adults who lost pay or income in the prior week

By employment industry • The share of restaurant and hotel

workers reporting lost pay has stabilized

Food and beverage Leisure and hospitality Health care Financial services

at a level only slightly above the share of

60% workers in sectors less-impacted by the

pandemic.

50%

• The food and beverage and leisure and

hospitality industries tend to experience

40% higher worker turnover even without the

added impact of COVID-19, so pay

30% losses are likely to remain elevated

through the end of the year, especially

given the rapid rate of job creation in

20%

these sectors.

10% • The spread of the Delta variant over the

past several weeks has not yet resulted

0% in a sizable uptick in job losses, as was

seen during earlier case surges—though

Au 0

Au 1

20

21

21

21

Se 0

20

D 0

0

21

0

1

0

N 0

M 1

21

1

-2

-2

-2

r-2

-2

-2 this may change if rising cases lead to

l-2

l-2

2

-2

-2

b-

n-

n-

n-

n-

g-

p-

g-

ay

ay

r

ar

ct

ov

ec

Ju

Ju

Ap

Ap

Ju

Ja

Ja

Ju

Fe

O

dwindled demand and business

M

M

restrictions.

Source: Morning Consult Economic Intelligence; weekly surveys of a representative sample of 20,000 U.S. adults on average

18E MP L OY ME N T

Hispanic adults reported a sharp increase in income losses in late August

Share of U.S. adults who lost pay or income in the prior week

By ethnicity • Minority workers reported a sharp

increase in income losses in late

Black Hispanic Other White

August, with 19% of Hispanic adults

40% and 16% of Black adults reporting lost

pay or income. For both groups, these

35% increases represented the highest level

of pay losses since since May.

30%

25% • Pay losses among white workers

remained relatively low, though the rate

20% of decline has slowed compared with

earlier in the year.

15%

• For many minority workers employed in

10% services industries, the continuing

impact of COVID-19 and the spread of

5%

the Delta variant are likely to slow

0% recovery and keep pay losses elevated

for these groups.

Au 0

Au 1

20

21

21

21

Se 0

20

D 0

0

21

0

1

0

N 0

M 1

21

1

-2

-2

-2

r-2

-2

-2

l-2

l-2

2

-2

-2

b-

n-

n-

n-

n-

g-

p-

g-

ay

ay

r

ar

ct

ov

ec

Ju

Ju

Ap

Ap

Ju

Ja

Ja

Ju

Fe

O

M

M

Source: Morning Consult Economic Intelligence; weekly surveys of a representative sample of 20,000 U.S. adults on average

19E MP L OY ME N T

Unemployment creeps higher in August

U.S. (4-week moving average)

Note differences in scales

Unemployment Rate Employment to Population Ratio Labor Force Participation Rate

18% 48% 56%

47%

16% 55%

46%

14% 54%

45%

12% 44% 53%

1 0/3 0

1 0/2 2 0

1 2/2 2 0

/2 1

/2 1

4 /1 0 1

/2 1

/2 1

/2 1

8 /1 4 1

/2 1

1 0/3 0

1 0/2 2 0

1 2/2 2 0

/2 1

/2 1

4 /1 0 1

/2 1

/2 1

/2 1

/2 1

/2 1

2 /2 7 1

5 /2 2 1

7 /2 4 1

4 /20

1 2/5 0

6 /20

4 /20

1 2/5 0

6 /20

2 /2 7 1

5 /2 2 1

7 /2 4 1

1 0/3 0

1 0/2 2 0

1 2/2 2 0

/2 1

3 /2 0 1

4 /1 0 1

/2 1

6 /1 2 1

/2 1

/2 1

/2 1

2 /2 7 1

5 /2 2 1

7 /2 4 1

4 /20

1 2/5 0

6 /20

2

2

2

4 /2

4 /2

2

2

2

/2

/2

/2

/2

/2

2

2

2

4 /2

/2

/2

/2

/2

2 /6 /

5 /1 /

7 /3 /

2 /6 /

5 /1 /

7 /3 /

/

/

/

/

2 /6 /

5 /1 /

7 /3 /

/

/

9 /1 2

1 /1 6

3 /2 0

6 /1 2

9 /1 2

1 /1 6

3 /2 0

6 /1 2

8 /1 4

9 /1 2

1 /1 6

8 /1 4

1 1/1

1 1/1

1 1/1

• Labor force participation fell again, hitting a new series low in August, while unemployment ticked higher to 14.1%. Fewer adults were

willing and able to work in August, and a smaller share of the shrinking labor force had a job last month. The combination of these two factors

drove down the employment-to-population ratio to 46.0%, wiping away the gains accumulated so far this year.

• Seasonal factors, workforce decline worsen unemployment outlook. The BLS typically applies a slight negative adjustment to the

unemployment rate in August, diminishing the likelihood of seasonal effects contributing to the June-August upward trend in joblessness.

Furthermore, the late-August decline in unemployment was driven by labor force exits, not job creation.

Source: Morning Consult Economic Intelligence

20E MP L OY ME N T

Unemployment dropped for higher earners in August, stagnated for those earning

under $100,000

U.S. unemployment rate by annual household income (4-week moving average)

Note differences in scales

Under $50,000 $50,000 - $100,000 Over $100,000

26% 10% 7%

24%

9% 6%

22%

8% 5%

20%

18% 7% 4%

1 0/3 0

1 0/2 2 0

1 2/2 2 0

/2 1

3 /2 0 1

4 /1 0 1

/2 1

6 /1 2 1

/2 1

/2 1

/2 1

2 /2 7 1

5 /2 2 1

7 /2 4 1

4 /20

1 2/5 0

6 /20

1 0/3 0

1 0/2 2 0

1 2/2 2 0

/2 1

/2 1

4 /1 0 1

/2 1

/2 1

/2 1

8 /1 4 1

/2 1

4 /20

1 2/5 0

6 /20

2 /2 7 1

5 /2 2 1

7 /2 4 1

2

2

2

4 /2

/2

/2

/2

/2

1 0/3 0

1 0/2 2 0

1 2/2 2 0

/2 1

/2 1

4 /1 0 1

/2 1

/2 1

/2 1

/2 1

/2 1

2 /2 7 1

5 /2 2 1

7 /2 4 1

4 /20

1 2/5 0

6 /20

4 /2

2

2

2

/2

/2

/2

2 /6 /

5 /1 /

7 /3 /

2

2

2

/

/

4 /2

/2

/2

2 /6 /

5 /1 /

7 /3 /

/

/

9 /1 2

1 /1 6

8 /1 4

9 /1 2

1 /1 6

3 /2 0

6 /1 2

2 /6 /

5 /1 /

7 /3 /

/

/

1 1/1

9 /1 2

1 /1 6

3 /2 0

6 /1 2

8 /1 4

1 1/1

1 1/1

• Unemployment remained elevated for those earning less than $100,000 per year

• Joblessness for high-income earners (i.e., annual incomes over $100,000) fell slightly to 4.2%, tying the lowest level since April

Source: Morning Consult Economic Intelligence

21E MP L OY ME N T

Fewer part-time workers want to find full-time jobs

Even if none are exactly correct, what is the main reason

Would you like to work more than 35 hours per week?

why you do not want to work more than 35 hours per week?

Yes Don't Know No

100%

90%

8%

9%

80% 30%

70%

60% 16%

50%

40%

17% 19%

30%

20%

Family/personal obligations

10% Other

0% Health/medical limitations

Retired/Social Security limit on earnings

20

Fe 1

21

M 1

1

0

1

Au 0

Au 1

M 0

N 0

M 1

Se 0

20

D 0

0

21

School/training

2

-2

l-2

l-2

2

-2

2

2

-2

-2

2

-2

-2

g-

p-

g-

n-

n-

n-

b-

r-

r-

ov

ec

ct

ar

ay

ay

Ju

Ju

Ap

Ap

Ju

Ja

Ju

Child care obligations

O

• In August, 46% of U.S. adults that worked fewer than 35 hours per week said they would like to work more hours,

down from 60% in April 2020 and 57% as recently as in January of this year.

• Family or personal reasons other than child care was the most frequently cited reason for not wanting to work more

hours (30%); followed by ”other” reasons and health or medical limitations.

Source: Morning Consult Economic Intelligence; monthly surveys of an average of 566 U.S. adults that worked fewer than

35 hours per week, and 218 who did not want to work more than 35 hours per week in August 22E MP L OY ME N T

Hispanic unemployment increased in August, even as labor force participation fell

U.S. unemployment rates by race or ethnicity U.S. labor force participation by race or ethnicity

(4-week moving average) (4-week moving average)

Black Hispanic Other race or ethnicity White Black Hispanic Other race or ethnicity White

24% 72%

22% 68%

20%

64%

18%

60%

16%

56%

14%

12% 52%

10% 48%

21

21

21

21

21

21

4/20

4/20

6/20

4/20

4/20

6/20

/ 20

/ 20

/ 20

/ 21

/ 21

/ 21

/ 21

/ 21

/ 21

/ 21

/ 21

/ 20

/ 20

/ 20

/ 21

/ 21

/ 21

/ 21

/ 21

/ 21

/ 21

/ 21

2/6/

5/1/

7/3/

2/6/

5/1/

7/3/

9/12

10/ 3

12/ 5

1/16

2/27

3/20

4/10

5/22

6/12

7/24

8/14

9/12

10/ 3

12/ 5

1/16

2/27

3/20

4/10

5/22

6/12

7/24

8/14

10/ 2

11/ 1

12/ 2

10/ 2

11/ 1

12/ 2

• The slight increase in unemployment was largely driven by Hispanic workers; Black and white unemployment remained flat.

• Labor force participation declined for Hispanic adults, remained flat for white adults, and increased slightly among Black adults since July.

Source: Morning Consult Economic Intelligence

23E MP L OY ME N T

Interest in job-switching remains elevated, with active applicants and openness to

new positions both reaching their highest levels of 2021

U.S. workers (4-week moving average)

Note differences in scales

Actively applying for new positions Open to new positions, not applying Not open to new positions

18% 33% 55%

54%

32%

53%

31% 52%

16%

30% 51%

50%

29%

49%

14% 28% 48%

1 0/3 0

1 0/2 2 0

1 2/2 2 0

/2 1

/2 1

4 /1 0 1

/2 1

/2 1

/2 1

/2 1

/2 1

1 0/3 0

1 0/2 2 0

1 2/2 2 0

/2 1

/2 1

4 /1 0 1

/2 1

/2 1

/2 1

8 /1 4 1

/2 1

2 /2 7 1

5 /2 2 1

7 /2 4 1

4 /20

1 2/5 0

6 /20

2 /2 7 1

5 /2 2 1

7 /2 4 1

4 /20

1 2/5 0

6 /20

1 0/3 0

1 0/2 2 0

1 2/2 2 0

/2 1

3 /2 0 1

4 /1 0 1

/2 1

6 /1 2 1

/2 1

/2 1

/2 1

2 /2 7 1

5 /2 2 1

7 /2 4 1

4 /20

1 2/5 0

6 /20

2

2

2

4 /2

2

2

2

4 /2

/2

/2

/2

/2

/2

2

2

2

4 /2

/2

/2

/2

/2

2 /6 /

5 /1 /

7 /3 /

2 /6 /

5 /1 /

7 /3 /

/

/

/

/

2 /6 /

5 /1 /

7 /3 /

/

/

9 /1 2

1 /1 6

3 /2 0

6 /1 2

8 /1 4

9 /1 2

1 /1 6

3 /2 0

6 /1 2

9 /1 2

1 /1 6

8 /1 4

1 1/1

1 1/1

1 1/1

• About 17% of currently employed workers were actively applying for new positions in late July, and an

even higher share of the active workforce (32%) were open to switching roles.

• The number of workers not open to new positions fell to 51% in July, down from 54% in April.

Source: Morning Consult Economic Intelligence

24E MP L OY ME N T

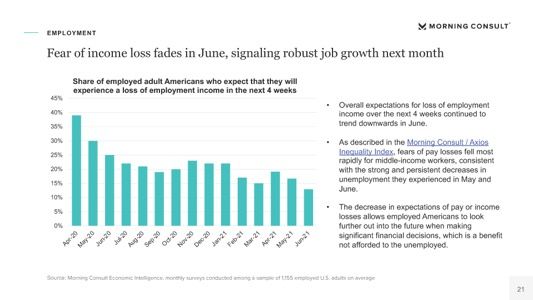

Fear of income loss ticks down in August, hits pandemic series low

Share of employed adult Americans who expect that they will

experience a loss of employment income in the next 4 weeks

30.0%

• Overall expectations for loss of employment

25.0% income over the next 4 weeks remained

stable in August, ticking downwards to a

20.0% new, modestly lower series low.

15.0% • As described in the Morning Consult / Axios

Inequality Index, fears of pay losses

10.0% remained relatively lower compared to last

fall and winter when the last COVID-19

5.0% surge drove fears higher.

0.0%

0

1

0

21

21

20

20

0

0

21

1

0

M 1

21

1

-2

r-2

-2

-2

l-2

l-2

2

-2

-2

b-

n-

n-

n-

g-

p-

g-

ay

ar

ct

ov

ec

Ju

Ju

Ap

Ju

Ja

Ju

Au

Se

Au

Fe

O

M

N

D

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a sample of 1,155 employed U.S. adults on average

25D E L T A V A R I A N T I N T E R R U P T S R E C OV E R Y : U . S . E C ON OMI C OU T L OOK

SPENDING AND SPENDING

INTENTIONSSPENDING

U.S. adults allocated about 36% of monthly household expenditures to housing

in July, and about 14% went towards grocery purchases

Nominal average monthly spending per category in July 2021, all adults

Housing $70 $56

$83

Grocery

$85

Utilities

$90

Cars

$100

Health insurance

$100

Telecom $1,149

Car insurance $103

Total = $3,182

Gas $117

Education

$118 $88 from

Apparel

June

Restaurant $133

Furniture

Healthcare $147

Hotels $154 $433

Airfare $197

Public transportation

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults. Average spend level estimated as the weighted average

spending level, calculated by multiplying the midpoint for each spending bucket by the share of respondents selecting that respective bucket—then summing all products.

27SPENDING

Housing and vacation spending increased in July, while health

care costs declined

Percent change in spending from June – July 2021, all adults

• Rent and mortgage payments

increased 5.6% on average for

8%

U.S. households in July, driving up 7%

total spending $61 for the month. 6%

• Health insurance and out-of- 4% 4%

3%

pocket medical care spending 2% 2%

declined in July, despite rising 1% 1% 1% 1%

COVID-19 cases and related 0%

hospitalizations over the month. 0% 0%

-1%

• Discretionary categories— -2%

including airfare, hotels,

restaurants, and apparel—all

s

l

l

ry

re

n

e

as

m

s

e

re

t

ng

s

re

n

ho

re

an

tie

ar

el

tio

nc

io

nc

ce

ca

co

it u

rfa

G

si

pa

co

ot

at

increased, a sign that many

ur

C

ra

tili

ra

ta

ou

le

ro

lth

rn

Ai

H

uc

Ap

ta

Al

r

su

U

su

Te

G

po

Fu

H

ea

es

Ed

consumers are taking summer

in

in

ns

H

R

lth

ar

tra

C

ea

vacations despite COVID-19

ic

H

bl

Pu

concerns.

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults. Average spend level estimated as the weighted average

spending level, calculated by multiplying the midpoint for each spending bucket by the share of respondents selecting that respective bucket—then summing all products.

28SPENDING

U.S. households slightly pared back grocery spending for a

second straight month in July

Monthly spending on groceries, U.S. adults

• Average monthly grocery spending fell in

$460 July, but it remains higher than it was at the

start of the year.

$450

$450

$446 • One reason for lower spending on food to

$440 be consumed at home may be due to U.S.

$437 adults spending less time at home; vacation-

$436

$430 $433 related spending picked up in July,

$428 indicating that many households reallocated

$420 budgets (and made fewer grocery trips) to

$416 account for fewer meals consumed at home.

$410

• While additional restrictions on indoor dining

$400 are likely to harm restaurant spending, they

also have the potential to discourage future

$390 grocery foot traffic.

1/1/21 2/1/21 3/1/21 4/1/21 5/1/21 6/1/21 7/1/21

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults. Average spend level estimated as the weighted average

spending level, calculated by multiplying the midpoint for each spending bucket by the share of respondents selecting that respective bucket—then summing all products.

29SPENDING

Trips to the grocery store fell steadily since peaking in May, while online

orders for groceries remained stuck at their lowest level of the year

Average monthly visits to grocery stores per adult Average monthly online grocery orders per adult

6.3 2.5

6.2 2.4

6.2

6.1 2.0 2.2 2.1 2.2

6.0 1.9 1.9 1.9

5.9 6.0 1.5

5.8 5.9 5.9

5.8 5.8

5.7 1.0

5.6

5.6

5.5 0.5

5.4

5.3 0.0

1/1/21 2/1/21 3/1/21 4/1/21 5/1/21 6/1/21 7/1/21 1/1/21 2/1/21 3/1/21 4/1/21 5/1/21 6/1/21 7/1/21

US households shopped for groceries less frequently in July as the Delta variant led to increased concern about visiting public places for

some, and while others diverted spending towards restaurants or carry-out.

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults. Average monthly visits level estimated as the weighted

average visit level, calculated by multiplying the midpoint for each visit bucket by the share of respondents selecting that respective bucket—then summing all products.

30SPENDING

Visits to restaurants and carry-out orders stayed flat from June to July as

comfort with dining out dipped slightly amidst rising COVID-19 case count

Monthly visits to restaurants and share of respondents claiming

to be “very comfortable” with dining out, U.S. adults Monthly carry-out/delivery orders, U.S. adults

Restaurant visits (LHS) Indoor dining (RHS) 3.8

3.5 Outdoor dining (RHS) 60%

3.7

3.0 3.6

3.7

3.1 50%

2.8 2.8 2.8 2.9 3.5

2.5 2.7

40%

3.4

2.0 2.2

3.3 3.4

30%

1.5 3.3 3.3 3.3 3.3

3.2

20%

1.0 3.1 3.2

3.0

0.5 10%

2.9

0.0 0% 2.8

Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21

• Despite a decline in consumer’s comfort with dining out, U.S. adults did not overwhelmingly substitute carry-out meals for in-person dining

last month; consumers visited restaurants slightly more in July than June and did not change their frequency of to-go orders.

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults. Average monthly visit level estimated as the weighted

average visit level, calculated by multiplying the midpoint for each visit bucket by the share of respondents selecting that respective bucket—then summing all products.

31SPENDING

Travel plans increased across all income brackets as COVID-19 restrictions

were loosened in late spring of this year

• 47% of adults had vacation plans as of

Share of adults planning to purchase a trip or

vacation in the next 12 months, by income July, only slightly below the peak of

48% a month earlier and up from 38%

Less than $50,000 $50,000-$100,000 More than $100,000 Adults in January, reflecting pent-up demand

90%

created by the lack of travel during the

80% pandemic: Only 22% of adults reported

70% taking trips since July 2020, whereas

nearly half are planning to travel over

60%

the next year.

50%

• Higher-income households are almost

40% twice as likely than those earning less

30% than $50,000 to plan on taking a

vacation; 74% of those earning over

20%

$100,000 had travel plans in July

10% compared with only 38% of households

0% earning less than $50,000.

1/1/21 2/1/21 3/1/21 4/1/21 5/1/21 6/1/21 7/1/21

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 1,000 U.S. adults

32SPENDING

Adults grow less willing to travel domestically in July and August,

foreshadowing future drop in air travel volumes

U.S. adults’ opinion on domestic travel vs. TSA throughput

• The Delta variant and breakthrough

Share of respondents saying they are less likely to travel within the U.S. in the next 6

months due to pandemic (LHS) cases prompted a growing share of

70% TSA throughput (RHS, millions) 2.5 adults in early July to say they’re less

likely to travel within the U.S. in the

60% next six months, reversing a trend since

2

50% early January.

1.5 • Americans' willingness to fly remains a

40%

leading indicator of TSA throughput 2-3

30%

1 weeks into the future, indicating that air

20% travel is likely to continue to fall

0.5 throughout September.

10%

• A decrease in travel should provide

0% 0

0 0 0 0 0 0 0 0 0 1 1 1 1 1 1 1

Americans with additional income to

ar-2 pr-2 ay-2 un-2 ul-2 ug-2 ep-2 ov -2 ec -2 an-2 eb-2 ar-2 pr-2 ay-2 ul-2 ug-2

M A M J J A S N D J F M A M J A spend elsewhere or strengthen their

finances.

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults; TSA data.

33S P E N D I N G I N T E N T I ON S

Millennials and Gen Z consumers increasingly looking to buy a home

Share of respondents who intend on purchasing a house or apartment in the next 12 months

By generation

Baby Boomers (1946-1964) GenXers (1965-1980) Millennials (1981-1996) GenZers (1997-2012)

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 1,000 U.S. adults

34D E L T A V A R I A N T I N T E R R U P T S R E C OV E R Y : U . S . E C ON OMI C OU T L OOK PRICE EXPECTATIONS

P R I C E E X P E C T A T I ON S

Fewer consumers expecting price increases for homes and vacations

Percentage point increase from June to July in the share of consumers who said they

expect prices to rise over the next 12 months in the following categories: • A larger share of consumers

expected higher prices in July than

June across the majority of spending

A house or apartment -2.9% categories tracked by Morning

Trips and vacations -1.6% Consult (8 of 11).

Energy and utility bills -0.3%

• However, after months of increases,

Food and groceries 0.2% several categories saw the share of

Home improvements 0.2% consumers expecting price

Home appliances 0.6%

increases fall in July.

Furniture 1.2% • Price expectations fell for homes,

Electronics 1.7% vacations and utilities, with the share

A used vehicle

of consumers expecting price

2.0%

increases over the next 12 months in

Motorcycles 2.2% each of these segments decreasing

A new vehicle 2.4% 2.9%, 1.6% and 0.3%, respectively.

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 1,000 U.S. adults

36P R I C E E X P E C T A T I ON S

Consumer price expectations tracking higher CPI inflation in 2021

Net share of consumers who expect prices to rise over the next 12 months minus

• Despite the modest decline in some categories

share that expect declines, averaged across 11 price categories;

in July, the net share of consumers expecting and CPI inflation, year-over-year

prices to increase in the next 12 months

remains considerably higher compared to the Net share of consumers expecting price increases (LHS) CPI Inflaiton, y-o-y (RHS)

beginning of the year. 45% 6%

40%

• During his Jackson Hole speech, Federal 5%

Reserve Chair Powell reiterated his view that 35%

inflation is likely temporary. He emphasized

30% 4%

inflation was still concentrated in pandemic-hit

sectors and highlighted consumers’ relatively 25%

3%

stable inflation expectations. 20%

• Morning Consult’s data shows that the rate of 15% 2%

growth in price expectations began to slow in 10%

May, supporting Powell’s view that inflation 1%

expectations remain well anchored. 5%

0% 0%

Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 1,000 U.S. adults.

37P R I C E E X P E C T A T I ON S

Conservatives much more likely to be “very concerned” about inflation

• Inflation concerns are prevalent across

political ideologies, but respondents who How concerned are you about inflation (July 2021)? By political ideology

consider themselves conservatives are

more likely to be very concerned about Not concerned at all Not too concerned Somewhat concerned Very concerned

inflation risks.

• 67.1% of conservatives said they were “very Conservative 5.5% 26.5% 67.1%

concerned” about inflation, compared with

40.5% of moderates and 38.7% of liberals.

• The political divide is likely drive by the fact

Moderate 14.0% 43.2% 40.5%

that U.S. conservatives tend to view

themselves as fiscally conservative and

believe the federal government should limit

its spending. Additionally, inflation tends to

be more financially harmful for retirees and Liberal 6.7% 50.6% 38.7%

wealthier investors, a larger share of whom

tend to be conservative.

Source: Poll conducted from July 29 to August 8, 2021, among a representative sample of 1,000 U.S. adults

38D E L T A V A R I A N T I N T E R R U P T S R E C OV E R Y : U . S . E C ON OMI C OU T L OOK

PERSONAL FINANCES, CONSUMER

CREDIT AND HOUSINGP E R S ON A L F I N A N C E S

The share of households with money left over after paying expenses

dwindled to its lowest level since January

After you paid your recurring expenses last month, did you have any

money left over that you could save or add to your savings?

Of those responding “No, our expenses were more than our

No, our expenses were more than our income income,” 80% earned less than $50,000 per year

No, our expenses roughly equaled our income with nothing left over

Over $100,000

Yes, we had some money left over 4%

16% 14% 13% 12% 14% 14% 16%

$50,000-

25% $100,000

25% 26% 26% 25%

28% 26% 16%

Under

61% 63% 61% $50,000

56% 61% 60% 57% 80%

Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults 40P E R S ON A L F I N A N C E S

Financial vulnerability remains stable in August

Share of adults lacking savings to pay basic expenses for a full month • The share of Americans lacking savings to

30% cover their basic expenses for a full

July 31, 2020:

June 31, 2021: month fell in August to 21.4%, down from

$600 per week federal

More than 20 states terminate 21.9% in July.

25%

unemployment benefits expire

federal unemployment benefits

• Following a modest decline, improving

20%

financial vulnerability was one of the few

metrics that saw improvement in August

15% as concerns over the COVID-19 surge

take their toll on the economy.

10%

• There is no evidence yet of financial

5% vulnerability increasing due to the

expiration of federal unemployment

benefits. However, recent history

0%

suggests it could take a few months

0

1

0

1

20

20

0

0

21

20

21

21

1

21

1

-2

r-2

-2

l-2

l-2

-2

-2

-2

before financial vulnerability increases.

g-

p-

g-

n-

n-

n-

b-

ay

ar

ov

ec

ct

Ju

Ju

Ap

Au

Se

Au

Ju

Ja

Ju

Fe

O

M

N

D

M

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a representative sample of 2,200 U.S. adults 41P E R S ON A L F I N A N C E S

Unemployment payments trending lower as expanded benefits expire

• Average weekly unemployment insurance benefits fell to $471 in mid August, down from $571 in mid July. Payments remain

above the series low of $437 in Dec. 2020, indicating there remains additional room for payments to decrease in the coming months.

• Expiring expanded unemployment payments paired with increasing cases elevates risks for Americans’ finances. Similar to

last year, Americans will become more financially dependent on wage income than government subsidies at a time when the

increase in cases calls into question the employment recovery.

Average weekly unemployment insurance payment ($)

June 2021:

Dec-Jan 2021:

July 31, 2020: March 11, 2021: Over 20 states begin

700 Federal benefits

$600 enhanced Federal benefits terminating federal

extended, but delay

benefits expire extended to unemployment benefits

September: $300 complicates state

600 September

6-week extension implementation

500 $471.03

400

300

200

100

0

Apr-20 Ma y-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Ma r-21 Apr-21 Ma y-21 Jun-21 Jul-21 Aug-21

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a sample of 2,200 U.S. adults on average 42P E R S ON A L F I N A N C E S

Largest Child Tax Credit payments sent to parents on the higher end

of the eligible income range

• Parents earning over $100,000 are

more likely to have more children,

Child Tax Credit payment amount received in July, by annual income entitling them to multiple payments.

• Higher income, married parents

received larger payments on average as

a result of the credit, suggesting that

these groups may have extra cash to

spend through the end of the year as

$604 $568 payments continue to be distributed.

$543 $523

$436

• The payments are likely to boost

spending among parents as inflation

continues to raise prices on household

expenses and summer travel and back

Over $100,000 $50,000-$100,000 Under $50,000 Married parents Single to school shopping apply added strain to

parent/guardian monthly budgets.

Source: Poll conducted from August 3-7, 2021, among 355 adults that reported having received a Child Tax Credit payment in July 2021, with a margin of error of +/-5%. Average

payment size estimated by taking the weighted average of the midpoints of each dollar value range. 43C ON S U ME R C R E D I T

Middle-income earners reported increasing credit card debt in July, while few earning

over $100,000 reported rising balances

Share of respondents reporting an increase in unpaid credit card debt • Fewer high-earning adults saw an increase

By annual household income

in credit card debt last month, with only

Adults Under $50,000 $50,000-$100,000 Over $100,000 14% of those earning more than $100,000

35% reporting higher balances in July—the

30% second straight monthly drop.

25% • Among adults earning between $50,000

20% and $100,000, 23% increased debt levels

in July, the second highest level this year.

15%

10% • While lower credit card debt can be a

positive indicator for household financial

5% stability, a continued softening in debt-

0% fueled spending can also be a sign of

diminished consumer confidence and

1

1

1

20

20

1

1

1

1

-2

-2

-2

-2

l-2

2

2

flagging demand, potentially harkening a

n-

n-

-

-

r

ar

ay

b

ov

ec

Ju

Ap

Ja

Ju

Fe

M

N

D

M

slower pace of economic recovery.

Source: Morning Consult Economic Intelligence, monthly surveys conducted among a sample of 677 adults with outstanding credit card debt on average 44H OU S I N G

After trending downward for much of the year, missed housing payments

increased from June to July

Did any of the following happen to your household last month?

Forbearance

Jun-21 Jul-21

Missed payments

Forgiveness

10%

9% 8%

7%

6% 6%

My household did not pay in full the Our landlord or bank allowed us to Our landlord or bank allowed us to

rent or mortgage last month even not pay in full the rent or mortgage not pay in full the rent or mortgage

though we didn't receive permission last month, and we will not have to last month, but we will have to repay

from our bank or landlord. repay this money in the future. this money in the future.

Source: Morning Consult Economic Intelligence, monthly surveys conducted among an average monthly sample of 1,447 homeowners with mortgage and rent payments

45H OU S I N G

About 1 in 5 Gen-Z renters or homeowners sought permission to delay

housing payments in July

Did any of the following happen to your household last month?

Our landlord or bank allowed us to not pay in full the rent or mortgage last month, but

we will have to repay this money in the future.

By generation

Jun-21 Jul-21

21%

16%

14% 14%

5% 5%

2% 4%

GenZers (1997-2012) Millennials (1981-1996) GenXers (1965-1980) Baby Boomers (1946-1964)

Source: Morning Consult Economic Intelligence, monthly surveys conducted among an average monthly sample of 1,447 homeowners with mortgage and rent payments 46H OU S I N G

Almost 70% of households currently in forbearance expect to start repaying

deferred housing costs by September 1

When will your household have to start repaying the rent/mortgage payments

that you haven't paid, but still owe your landlord or bank?

39%

29%

18%

14%

8/1/21 9/1/21 October 2021 or later I don't know

Source: Morning Consult Economic Intelligence, survey conducted August 3-7, 2021, among a sample of 144 U.S. adults in forbearance

47H OU S I N G

Evictions increased in July and are likely to climb higher throughout 2021

Share of households that reported having received an eviction notice

• The share of households receiving

eviction notices grew from 5.4% in

June to 6.9% in July as the CDC’s

7.7% nationwide eviction moratorium

6.9% expired on July 31.

6.4%

6.1%

5.5% 5.4% • The expired moratorium was quickly

5.0% replaced on August 3 by a similar

measure set to expire in October,

offering protection against eviction for

about 80% of the population.

• In late August, the Supreme Court

overturned the new rule, paving the

Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 way for evictions to resume this

month.

Source: Source: Morning Consult Economic Intelligence, monthly surveys conducted among an average monthly sample of 1,447 homeowners with mortgage and rent payments 48REPORT AUTHORS

John Leer Kayla Bruun Jesse Wheeler

C H I E F E C ON OMI S T E C ON OMI C A N A L Y S T E C ON OMI C A N A L Y S T

LEARN MORE FOLLOW US MEDIA AND SPEAKING

INQUIRIES

MorningConsult.com @MorningConsult press@morningconsult.com

49A B O U T M O R N I N G C O N S U LT

Morning Consult is a global enterprise technology company

delivering intelligent data to power leaders’ decisions. The

company’s proprietary AI technology, including both

machine-learning and natural language processing solutions,

pairs with leading, high-frequency datasets and access to

more than 100 million people globally, to optimize decision

making. Morning Consult’s proven approach gives users a

leading advantage for more effective decision making at an

unparalleled speed and scale.

50GET THE LATEST ECONOMIC ANALYSIS CLICK HERE TO SIGN UP

C OV I D S U R GE T H R E A T E N S R E C OV E R Y : U . S . E C ON OMI C OU T L OOK METHODOLOGY

ECONOMIC MC E I D A T A I N T E L L I GE N C E C A P A B I L I T I E S

INTELLIGENCE Economic Intelligence collects over 15,000 daily responses on

key global macro economic indicators including:

§ Personal § Employment § Pricing Effect

Data Intelligence Finances Type § Supply

On Key Economic Indicators § Buying § Labor Market Expectations

Conditions Sizing § Demand

Morning Consult’s SaaS platform that tracks key § Business § Future Price Expectations

Conditions Increases § Ability to Pay

economic indicators, including consumer sentiment,

§ Employment § GDP

spending, labor conditions, and more. Status expectations

Key Use Cases

T R A C K GL OB A L MON I T OR L A B OR & T R A C K I N F L A T I ON U N D E R S T A N D H OU S I N G

C ON S U ME R C ON F I D E N C E E MP L OY ME N T C ON D I T I ON S E X P E C T A T I ON S MA R K E T

Track global consumer confidence to Compare labor market conditions across Tracking consumer inflation expectations Tracking supply and demand of housing,

better understand and forecast consumer and within countries to identify job and the impact that has on consumer including buying and renting and ability

spending. seekers with appropriate skill sets. spending and buying habits. to make payments.

Available in 15 countries

USA CHINA JAPAN GERMANY UK FRANCE INDIA ITALY BRAZIL CANADA S KOREA RUSSIA AUSTRALIA SPAIN MEXICOC ON S U ME R C ON F I D E N C E

We use responses to five daily survey questions to measure consumer sentiment.

Index of Cons. Index of Cons. Index of Current

Sentiment Expectations Conditions

(ICS) (ICE) (ICC)

❏ Better Now + % Pos. + % Pos.

Current Conditions: Would you say that you (and your family living

❏ Same - % Neg. - % Neg.

there) are better off or worse off financially than you were a year

❏ Worse

ago? + 100 + 100

❏ Don’t Know/No Opinion

Personal

Finances ❏ Will Be Better Off

12-Month Expectations: Now looking ahead — do you think that a + % Pos. + % Pos.

❏ Same - % Neg. - % Neg.

year from now you (and your family living there) will be better off

❏ Will Be Worse Off

financially, or worse off, or just about the same as now? + 100 + 100

❏ Don’t Know/No Opinion

❏ Good Times + % Pos. + % Pos.

12-Month Expectations: Now turning to business conditions in the

❏ Neither Good/Bad - % Neg. - % Neg.

country as a whole — do you think that during the next twelve

❏ Bad Times

months we’ll have good times financially, or bad times, or what? + 100 + 100

Business ❏ Don’t Know/No Opinion

Conditions 5-Year Expectations: Looking ahead, which would you say is more

❏ Good Times + % Pos. + % Pos.

likely — that in the country as a whole we’ll have continuous good - % Neg. - % Neg.

❏ Unem./Depression

times during the next 5 years or so, or that we will have periods of

❏ Don’t Know/No Opinion + 100 + 100

widespread unemployment or depression, or what?

Current Buying Conditions: Thinking about the big things people buy ❏ Good Time + % Pos. + % Pos.

Buying for their homes — such as furniture, a refrigerator, stove, television, ❏ Neither Good/Bad - % Neg. - % Neg.

Conditions and things like that. Generally speaking, do you think now is a good ❏ Bad Time

or bad time for people to buy major household items? ❏ Don’t Know/No Opinion + 100 + 100

avg. avg. avg.

ICS ICE ICC

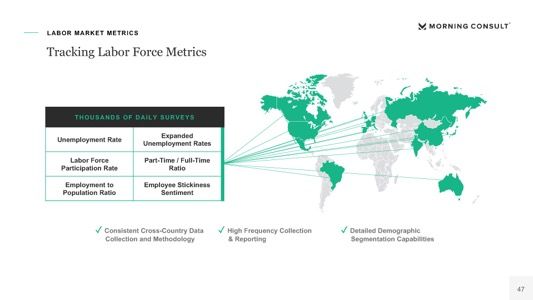

54L A B OR MA R K E T ME T R I C S

Tracking Labor Force Metrics

THOUSANDS OF DAILY SURVEYS

Expanded

Unemployment Rate

Unemployment Rates

Labor Force Part-Time / Full-Time

Participation Rate Ratio

Employment to Employee Stickiness

Population Ratio Sentiment

✓ Consistent Cross-Country Data ✓ High Frequency Collection ✓ Detailed Demographic

Collection and Methodology & Reporting Segmentation Capabilities

55L A B OR MA R K E T ME T R I C S

Morning Consult’s labor force calculations are simplified and standardized

versions of those used by the Bureau of Labor Statistics, OECD and International

Labour Organization.

EM PL O YED Working

UNEM PL O YED Not working, but looking for work and not disabled

I N T HE L ABO R F O RCE Employed + Unemployed

Has a job, but is open to leaving current job or is actively

W I L L I NG TO SW I T CH JO BS

applying for new jobs

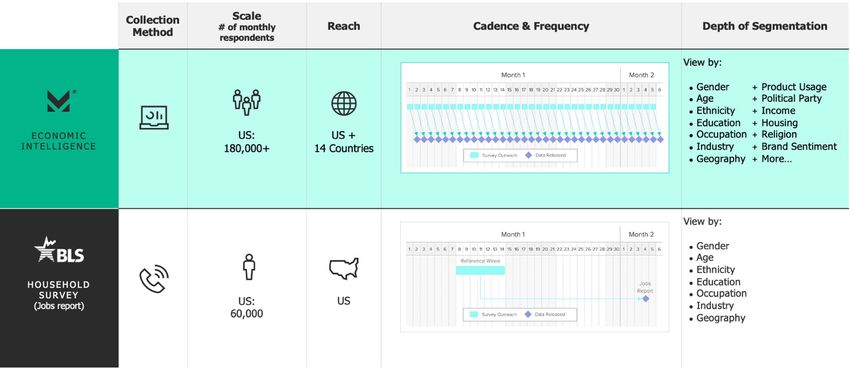

56S U R V E Y C OMP A R I S ON

Morning Consult’s labor market data provides enhanced scale, frequency, and

depth not captured in BLS data.

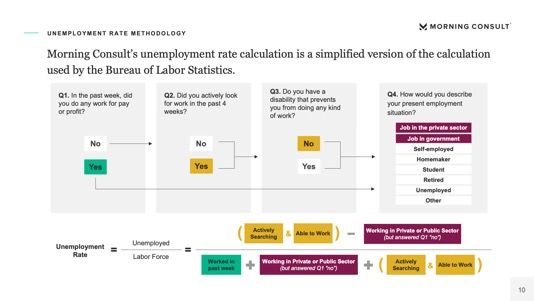

57U N E MP L OY ME N T R A T E ME T H OD OL OGY

Morning Consult’s unemployment rate calculation is a simplified version of the

calculation used by the Bureau of Labor Statistics.

Q3. Do you have a Q4. How would you describe

Q1. In the past week, did Q2. Did you actively look

disability that prevents

you do any work for pay for work in the past 4 your present employment

you from doing any kind

or profit? weeks? situation?

of work?

Job in the private sector

Job in government

No No No

Self-employed

Homemaker

Yes Yes Yes Student

Retired

Unemployed

Other

( Actively

Searching & Able to Work ) Working in Private or Public Sector

(but answered Q1 “no”)

Unemployed

Unemployment

Rate

= =

Labor Force

Worked in

past week

Working in Private or Public Sector

(but answered Q1 “no”) ( Actively

Searching & Able to Work )

58I N T E L L I G E N T DATA ,

INTELLIGENT DECISIONS

© 2021 Morning Consult, All Rights Reserved.You can also read