Economic activity and social change in the UK, real-time indicators: 7 April 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Statistical bulletin

Economic activity and social change in the

UK, real-time indicators: 7 April 2022

Early experimental data and analysis on economic activity and social change in the UK.

These faster indicators are created using rapid response surveys, novel data sources,

and experimental methods.

Contact: Release date: Next release:

Emelia D’Silva-Parker 7 April 2022 14 April 2022

faster.indicators@ons.gov.uk

+44 1633 455120

Notice

7 April 2022

This publication of retail footfall data will be the last release for the foreseeable future. The associated charts and

commentary in previous bulletins will remain available. We apologise for any inconvenience this may cause.

Page 1 of 20

Table of contents

1. Main points

2. Latest indicators at a glance

3. Consumer behaviour

4. Business and workforce

5. Transport

6. Data

7. Glossary

8. Measuring the data

9. Strengths and limitations

10. Related Links

Page 2 of 20

1 . Main points

Both UK spending on credit and debit cards, and OpenTable UK seated diners, increased by 6 percentage

points in the latest week; meanwhile, visits to retail stores and recreation areas were 15% below pre-

coronavirus (COVID-19) levels and 1% lower than the previous week according to Google Mobility data.

Section 3.

In the latest week, there were increases in 16 of the 28 online job advert categories, with the largest

weekly increase in “travel and tourism” (11%). Section 4.

In March 2022, the seasonally adjusted number of new Value Added Tax (VAT) reporters was 12% lower

than the previous month and 18% lower than reported in March 2021. Section 4.

The top two concerns reported by businesses continued to be input price inflation (23%) and energy prices

(20%); concerns about energy prices saw the largest rise of all concerns, from 15% in late February 2022

to 20% in late March 2022 (final results from Wave 53 of the Business Insights and Conditions Survey

(BICS)).

While the volume of all ship visits and road traffic showed week-on-week decreases of 10% and 4

percentage points, respectively, daily UK flights increased by 19% in the latest week, to the highest level

compared with the pre-coronavirus equivalent week. Section 5.

The System Average Price (SAP) of gas increased by 17% in the week to 3 April 2022, with the level now

58% of that on 10 March 2022, when prices peaked in the rolling seven-day series; the SAP is 444%

higher compared with the same period last year (week ending 4 April 2021).

Results presented in this bulletin are experimental and may be subject to revision. Data sources used to compile

these indicators are regularly reviewed to ensure representativity and relevance, which may mean indicators

change at short notice.

2 . Latest indicators at a glance

Notes:

1. The break in the available shipping data (from 14 to 19 June 2021) is when the data collection system

changed.

2. OpenTable seated diners weekly comparisons were previously made with the seven-day period to each

Monday. From the previous week’s release (31 March 2022) the weekly comparison period has changed to

the seven-day period to each Sunday.

3. Adzuna online job adverts in the previous period are compared from 21 March 2022 to 25 March 2022.

Caution is advised when comparing these data as this is not the Friday-to-Friday comparison period

historically used.

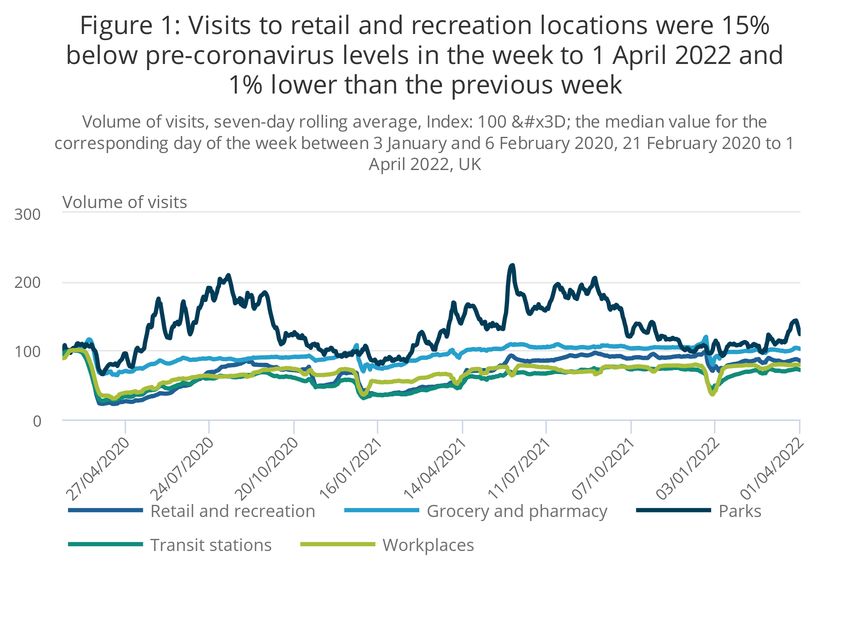

3 . Consumer behaviour

Consumer activity across the UK showed a mixed picture in the most recent week, with a 6 percentage point

increase in both credit and debit card purchases and OpenTable seated diners. Meanwhile Pret A Manger

transactions fell at most locations in part because of adverse weather conditions. Springboard’s retail footfall

decreased by 8% from the previous week, while Google Mobility data show a slight decrease (1%) in retail and

recreation visits, and were 15% below pre-coronavirus (COVID-19) levels.

Page 3 of 20Mobility

Google Mobility data provide an indicator of changes in the volume of visits to different location types compared

with a pre-coronavirus baseline.

Visits are calculated based on publicly available anonymised data from Google users in the UK who have opted

into Location History for their Google account, so are based on a subset of users. Full details of Google’s methods

used to compile the data are available.

We have transformed the publicly available anonymised data into an indexed seven-day moving average to

smooth the weekday and weekend.

We have used data for the following location types:

Page 4 of 20Grocery and pharmacy: grocery stores, supermarkets, farmers’ markets, specialty food shops and

pharmacies

Parks: parks, public beaches, marinas, public gardens and other public open spaces

Transit stations: public transport hubs such as train, light rail, tram and bus stations

Retail and recreation: restaurants, cafes, shopping centres, theme parks, museums, libraries, theatres and

cinemas

Workplaces: places of work

Figure 1: Visits to retail and recreation locations were 15% below pre-coronavirus levels in the week to 1

April 2022 and 1% lower than the previous week

Volume of visits, seven-day rolling average, Index: 100 = the median value for the corresponding day of the week between 3

January and 6 February 2020, 21 February 2020 to 1 April 2022, UK

Source: Google LLC "Google COVID-19 Community Mobility Reports" https://www.google.com/covid19/mobility/ Accessed: 5

April 2022.

Notes:

1. These data have not been seasonally adjusted. Users should consider seasonal events, such as the

weather and holiday periods, that may impact movements in the data.

Visits to retail and recreation locations have not yet returned to pre-coronavirus levels and remain below pre-

Omicron variant levels. There has been a slow upward trend in visits to workspaces since the low of April 2020,

but these are still 21% below pre-coronavirus levels. Visits to transit stations have been the slowest to recover

and are still 28% below pre-coronavirus levels.

Visits to each location type in the week to 1 April 2022 compared with the previous week:

Page 5 of 20parks decreased by 12%

no change in transit stations

grocery and pharmacy increased by 1%

retail and recreation decreased by 1%

workplaces increased by 1%

The full data time series can be found in our accompanying Visits to location types using Google Mobility dataset.

These are experimental indicators, which we are working to develop further. However, further geographical

breakdowns of the Google Mobility data are available.

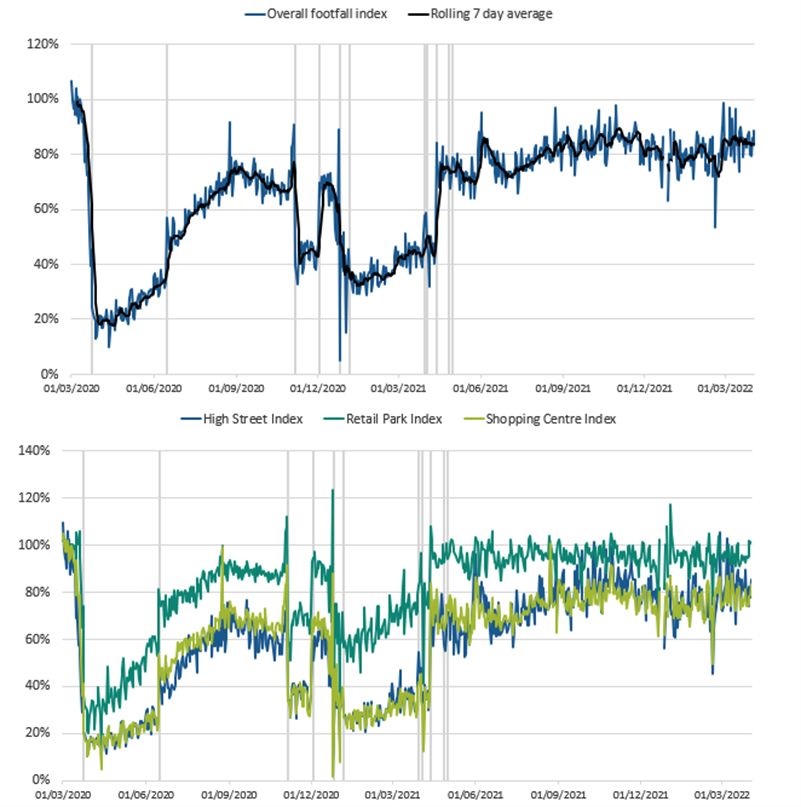

National retail footfall

National retail footfall figures are supplied by Springboard, a provider of data on customer activity. They measure

the following for overall UK retail footfall, as well as by high street, retail park and shopping centre categories:

Page 6 of 20daily retail footfall as a percentage of its level on the same day of the equivalent week of 2019; for

example, Saturday 2 April 2022 is compared with Saturday 30 March 2019

total weekly retail footfall as a percentage of its level in the equivalent week of 2019

the percentage change in weekly footfall compared with the previous week; for example, Week 13 of 2022

is compared with Week 12 of 2022

Springboard’s weekly data are defined over a seven-day period running from Sunday to Saturday. Week 13 of

2022 therefore refers to the period Sunday 27 March to Saturday 2 April 2022.

Because of data offsets between 2021 and previous years, footfall data from Springboard for the following days

have been omitted: 22 to 23 December 2021, 25 to 26 December 2021, 29 December 2021 and 1 January 2022.

Users should note that all quoted figures have been rounded to the nearest integer.

Page 7 of 20Figure 2: Overall weekly retail footfall in the UK decreased by 9% in the latest week and was 84% of the

level seen in the equivalent week of 2019

Volume of daily retail footfall, percentage compared with the equivalent day of the equivalent week of 2019, 1 March 2020 to 2

April 2022, UK

Source: Springboard, Department for Business, Energy and Industrial Strategy

Notes:

1. The vertical lines indicate notable events and coronavirus restriction changes.

2. Users should note that week-on-week changes in retail footfall volumes are outlined as percentages, rather

than as percentage point changes. Percentage change figures quoted in the commentary will therefore not

necessarily match the percentage point changes observed in the chart.

The volume of overall weekly retail footfall in the UK in the week to 2 April 2022:

Page 8 of 20in high streets decreased by 13% from the previous week and was 81% of the level seen in the equivalent

week of 2019

in shopping centres decreased by 6% from the previous week and was 79% of the level seen in the

equivalent week of 2019

in retail parks decreased by 2% from the previous week and was 98% of the level seen in the equivalent

week of 2019

Figure 3: The South West had the highest weekly levels of retail footfall in the week to 2 April 2022,

compared with the equivalent week of 2019, at 90%

Volume of daily retail footfall, percentage of the level recorded on the same day of the equivalent week of 2019, seven-day

rolling average, UK countries and English regions, 1 March 2020 to 2 April 2022

Source: Springboard, Department for Business, Energy and Industrial Strategy

Retail footfall saw week-on-week percentage decreases in all of the 10 UK countries and English regions in the

week to 2 April 2022. The largest of these were in the East of England, East Midlands, Northern Ireland, and the

North and Yorkshire, all falling by 10% over the week.

In the same period, relative to the levels seen in the equivalent week of 2019, retail footfall was strongest in the

South West of England and Greater London, at 90% and 86%, respectively. In contrast, retail footfall was

weakest in East Midlands and the East of England, at 81% and 83% of the levels seen in the equivalent week of

2019, respectively.

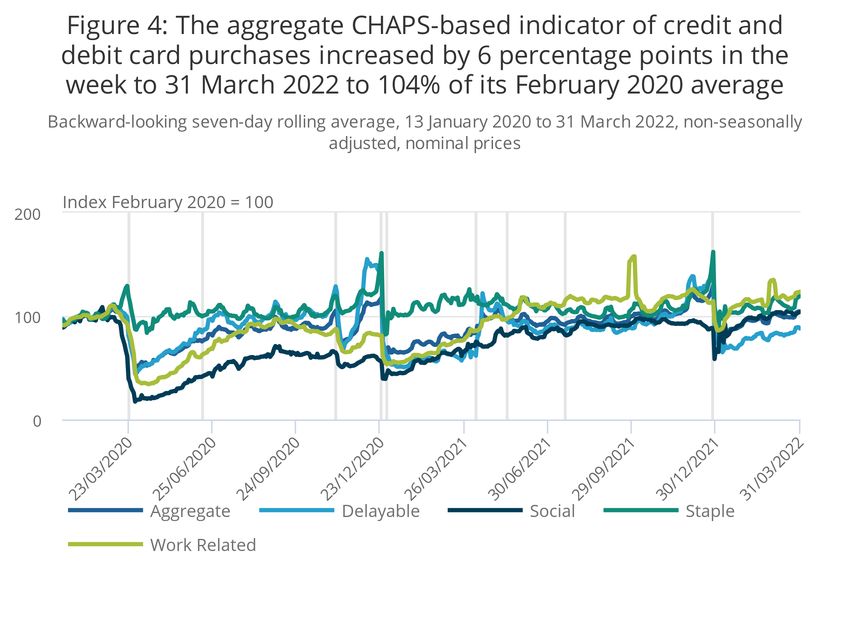

UK spending on debit and credit cards: daily CHAPS-based indicator

These data series are experimental faster indicators for estimating UK spending on credit and debit cards. They

track the daily CHAPS payments made by credit and debit card payment processors to around 100 major UK

retail corporates. These payments are the proceeds of recent credit and debit card transactions made by

customers at their stores, both via physical and via online platforms.More information on the indicator is provided

in the accompanying CHAPS methodology article.

Companies are allocated to one of four categories based on their primary business:

Page 9 of 20Page 10 of 20

“staples” refers to companies that sell essential goods that households need to purchase, such as food and

utilities

“work-related” refers to companies providing public transport or selling petrol

“delayable” refers to companies selling goods whose purchase could be delayed, such as clothing or

furnishings

“social” refers to spending on travel and eating out

Figure 4: The aggregate CHAPS-based indicator of credit and debit card purchases increased by 6

percentage points in the week to 31 March 2022 to 104% of its February 2020 average

Backward-looking seven-day rolling average, 13 January 2020 to 31 March 2022, non-seasonally adjusted, nominal prices

Source: Office for National Statistics and Bank of England calculations

Notes:

1. Users should note the daily payment data is the sum of card transactions processed up to the previous

working day, so there is a slight time lag when compared with real-life events on the chart.

2. The vertical lines indicate notable events and coronavirus (COVID-19) restriction changes.

3. Percentage point difference is derived from current week and previous week index before rounding.

Figure 4 shows changes in the value of CHAPS payments received by large UK corporates from their credit and

debit card processors, “merchant acquirers”.

In the week to 31 March 2022, the aggregate CHAPS-based indicator of credit and debit card purchases

increased by 6 percentage points from the previous week, to 104% of its February 2020 average level.

Page 11 of 20The spending categories recorded the following changes in the latest week:

“social” increased by 3 percentage points

“delayable” increased by 4 percentage points

“work-related” increased by 5 percentage points

“staple” increased by 12 percentage points, this may in part be due to seasonality

“Work-related”, “staple” and “social” spending were above their February 2020 average levels at 123%, 119% and

104%, respectively. “Delayable” spending meanwhile was below its February 2020 average level at 88%.

UK spending on debit and credit cards: Monthly CHAPS-based indicator

The monthly CHAPS-based indicator of aggregate credit and debit card spending was at 101% of its February

2020 average level in March 2022. This is 5 percentage points higher than in January 2022 (96%) and 20

percentage points higher than March 2021 (81%).

The monthly data time series is available in the accompanying CHAPS dataset and includes methodological notes

that users should bear in mind. The monthly CHAPS index is calculated by the Office for National Statistics

(ONS), rather than being an additional series that is produced and validated by the Bank of England.

4 . Business and workforce

The total volume of online job adverts on 1 April 2022 was broadly unchanged from the previous week, though

there were increases in 16 of the 28 online job advert categories. The largest of these was an 11% increase in

“travel and tourism”.

Small business sales recorded by Xero were up by 4 percentage points from January 2020, while small business

jobs decreased by 4 percentage points. The seasonally adjusted number of new Value Added Tax (VAT)

reporters decreased by 12% in March 2022 compared with the previous month.

Self-isolation rates in the workforce by sector and for working age population

by country

Data from the Coronavirus (COVID-19) Infection Survey (CIS) were used to provide modelled estimates of the

proportion of the workforce self-isolating because of coronavirus, by work sector; and the proportion of the

working age population self-isolating because of coronavirus, by country.

The percentage of people self-isolating because of coronavirus remained stable in the week ending 26 March

2022. This follows an increase in self-isolation across all work sectors except the “food production, agriculture

and farming” work sector in the two weeks ending 19 March 2022.

Figure 5: The percentage of the working-age population self-isolating because of

coronavirus increased in England in the week ending 26 March 2022

Estimated percentage of the working-age population (aged 17 to 69 years) self-isolating because of

coronavirus (COVID-19) from 6 February to 26 March 2022, UK countries

Notes:

Page 12 of 201. All results are provisional and subject to revision.

2. These statistics refer to self-reported self-isolation occurring in working-age adults (aged 17 to 69 years),

regardless of employment status, living in private households.

3. During the period shown, self-isolation requirements were frequently updated with different changes taking

place at different times across the UK countries.

Download the data

.xlsx

Figure 6: The sectors with the highest percentage of the workforce in self-isolation on 26

March 2022 were “health care” and “teaching and education”, both at 3.8%

Estimated percentage of the workforce self-isolating because of coronavirus (COVID-19), by work sector, 30

January 2022 to 26 March 2022, UK

Notes:

1. All results are provisional and subject to revision.

2. These statistics refer to self-reported self-isolation in working adults (aged 16 years and over) living in

private households.

3. In the “health care” work sector, there is a 95% confidence interval from 3.0% to 4.7%.

4. In the “teaching and education” work sector, there is a 95% confidence interval from 3.0% to 4.7%.

Download the data

.xlsx

More information on how these estimates were calculated is available in Coronavirus (COVID-19) Infection

Survey estimates of the UK workforce in self-isolation by sector, published on 14 February 2022.

A breakdown of the CIS data is available in our accompanying estimates of the UK workforce in self-isolation

dataset.

Online job adverts by category

These figures are experimental estimates of online job adverts provided by Adzuna, an online job search engine,

by category and by UK country and English region. The number of job adverts over time is an indicator of the

demand for labour. The Adzuna categories used do not correspond to Standard Industrial Classification (SIC)

categories, so these values are not directly comparable with the Office for National Statistics’ (ONS) Vacancy

Survey.

Figure 7: The total volume of online job adverts on 1 April 2022 increased by 1% from the

previous week, and was 137% of its February 2020 pre-coronavirus average level

Volume of online job adverts by category, index: 100 = February 2020 average, 4 January 2019 to 1 April 2022,

non-seasonally adjusted

Notes:

Page 13 of 201. Further category breakdowns are included in the Online job advert estimates dataset and more details on

the methodology can be found in Using Adzuna data to derive an indicator of weekly vacancies.

2. Users should note that week-on-week changes in online job advert volumes are outlined as percentages,

rather than as percentage point changes. Percentage change figures quoted in the commentary will

therefore not necessarily match the percentage point changes observed in the charts and accompanying

dataset.

3. Because of data collection issues, recent comparisons have alternated between Friday-to-Friday and

Monday-to-Monday comparisons. Caution is advised when comparing data between 4 and 25 March 2022

for this reason. We have now reverted back to the usual Friday comparisons.

Download the data

.xlsx

Of the 28 categories, 16 saw an increase in the number of online job adverts on Friday 1 April 2022. The largest

increase was in “travel and tourism” (11%), followed by “energy, oil and gas” and “catering and hospitality”, which

both increased by 9%. The number of online job adverts remained unchanged in five categories, and decreased

in seven categories, the largest decrease being in the “charity and voluntary” category, where it fell by 9%.

The categories with the highest level of online job adverts when compared with their February 2020 pre-

coronavirus average levels were “HR and recruitment” at 252%, followed by “transport, logistics and warehouse”

at 248%.

The latest five weeks of data for the regional breakdown of Adzuna online job adverts are now available, which

include a revision to the entire regional backseries following a methods update. This is available within our

accompanying online job advertisements dataset.

Page 14 of 20Value Added Tax returns

New reporters

The new reporters index measures the number of firms sending Value Added Tax (VAT) returns for the first time,

which is related to the number of firm creations.

Figure 8: The seasonally adjusted number of new VAT reporters in March 2022 was 20,920; this was 12%

lower than February 2022 (23,820)

Number of new firm reporters, January 2015 to March 2022, seasonally adjusted and non-seasonally adjusted, UK

Source: Her Majesty’s Revenue and Customs (HMRC)

In the services industry, there were 16,250 new VAT reporters in March 2022, a 13% decrease from the 18,740

reported in February 2022. This latest figure is 27% lower than reported in March 2021.

The number of new reporters in the production industries increased by 9% compared with the previous month,

while the number of new reporters in construction industries fell by 7% over the same period. The number of new

VAT reporters in the production and construction industries were 110% and 126% of their March 2021 levels,

respectively.

The figures explained in this section refer to seasonally adjusted data. Non-seasonally adjusted data are

available in our accompanying Value Added Tax dataset.

Page 15 of 20Business turnover estimates

Turnover diffusion indices are an aggregate measure used to track whether most firms are reporting an increase

or decrease in turnover in their VAT returns. They are calculated as the percentage of firms with increasing

turnover minus the percentage with decreasing turnover.

The heatmap in Figure 9 is a visual way of showing the VAT diffusion indices based on the standard deviation

from their historical 2008 to 2019 average. Larger deviations are more darkly coloured, with red representing a

negative change, while teal represents a positive change when compared with the previous period.

Figure 9: A net 5% of firms reported increased month-on-month turnover in February 2022

Heatmap of business turnover estimates, UK, diffusion index standard deviation from the mean, up to February

2022, new reporters, UK, up to March 2022

Notes:

1. Agri - Agriculture, forestry and fishing, All - All industries, SA - Seasonally adjusted.

2. More information is available in the methodology article

Download the data

.xlsx

The all-industry turnover estimate for February 2022 shows that in the past month, more firms had reported

increasing rather than decreasing turnover (net 5%).

A net 10% of firms in the production industry reported increasing turnover in February 2022, the highest net figure

since February 2021 (13%).

A net 6% and 4% of firms in the services and agricultural industries, respectively, reported increasing turnover in

February 2022. In the construction industry, a net 1% of firms reported increasing turnover in the last month.

The figures explained in this section refer to seasonally adjusted data. Non-seasonally adjusted data are

available in our accompanying Value Added Tax dataset.

5 . Transport

The transport indicators showed a mixed picture, with 10% decreases in both all ships and cargo ships, as well

as a 4 percentage point decrease in road traffic. In comparison UK daily flights increase by 19% in the week to 3

April 2022, coinciding with the start of Easter holiday period.

Page 16 of 20UK flight data

These data are daily flight figures from the European Organisation for the Safety of Air Navigation

(EUROCONTROL). Daily flight numbers for the UK alongside other countries are available in EUROCONTROL's

dashboard. EUROCONTROL is a pan-European, civil-military organisation dedicated to supporting European

aviation. Its Aviation Intelligence and Performance Review Unit provides independent collection and validation of

air navigation services performance-related data and intelligence gathering.

The flights data include international arrivals and departures to and from the UK (including Crown dependencies)

and domestic UK flights but exclude overflights (flights that pass over UK territory). They capture all flight

movements that operate under Instrument Flight Rules (IFR), where the pilot uses instruments in the flight deck

to control, guide and adjust the plane. This includes commercial flights carrying passengers and cargo as well as

non-commercial flights such as private and military flights.

Data from EUROCONTROL do not include information on the volume of passengers or cargo carried on UK

flights. Especially in the context of the coronavirus (COVID-19) pandemic, flights might not be operating at full

capacity and therefore trends in passengers and cargo will differ from trends in flights presented here.

Figure 10: The seven-day average number of UK daily flights was 4,588 in the week to 3 April 2022, the

highest level since the beginning of the coronavirus pandemic

Number of daily flights, non-seasonally adjusted, seven-day moving average, 2 January 2019 to 3 April 2022, UK

Source: European Organisation for the Safety of Air Navigation (EUROCONTROL)

The seven-day average number of UK daily flights increased for the ninth consecutive week in the week to 3 April

2022 and was 85% of the level seen in the equivalent week of 2019. Caution should be used when interpreting

this figure though as the latest period includes the beginning of the 2022 Easter Holidays, while the 2019

comparison does not.

The full data time series available for UK flights can be found in our accompanying UK daily flights dataset, which

contains daily flight numbers and the rolling seven-day averages.

Page 17 of 206 . Data

Advance potential redundancies

Dataset | Released 7 April 2022

Weekly dataset showing the number of potential redundancies and employers proposing redundancies,

submitted to Insolvency Service via HR1 forms.

Traffic camera activity

Dataset | Released 7 April 2022

Experimental daily traffic camera counts data for busyness indices covering the UK.

System Average Price (SAP) of gas

Dataset | Released 7 April 2022

Daily and rolling average System Average Price (SAP) of gas traded in the UK.

Weekly shipping indicators

Dataset | Released 7 April 2022

Experimental weekly and daily ship visits dataset covering UK ports.

Transactions at Pret A Manger

Dataset | Released 7 April 2022

Weekly transactional data from approximately 400 Pret A Manger stores around the UK.

Value Added Tax (VAT)

Dataset | Released 7 April 2022

Value Added Tax (VAT) turnover and expenditure diffusion indexes and new VAT reporters using data from

HM Revenue and Customs (HMRC) VAT returns.

Users should note that this section lists a selection of the data available with this publication. For the full list of

available datasets please see the accompanying dataset page.

7 . Glossary

Faster indicator

A faster indicator provides insights into economic activity using close-to-real-time big data, administrative data

sources, rapid response surveys or Experimental Statistics, which represent useful economic and social

concepts.

Diffusion index

The diffusion index tracks the growth in turnover and expenditure of firms. It is constructed to lie between

negative 1 and 1. For example, if 65% of firms have increasing turnover, 30% have decreasing turnover and 5%

turnover remains unchanged, then the diffusion index is 0.35.

New reporter

A new reporter is defined as a firm with a Value Added Tax (VAT) reference (that is, firm identification number),

which has not previously reported its VAT returns. New reporters are published within one month of the end of

the reporting period. The new reporting behaviour measure is classified by the month the data were received by

HM Revenue and Customs (HMRC), known as the receipt date; this is not necessarily the same as the reference

period (the period for which the VAT return is made).

Page 18 of 208 . Measuring the data

Information on the methodology used to produce the indicators in this bulletin is available in the Economic activity

and social change in the UK, real-time indicators methodology.

9 . Strengths and limitations

These statistics have been produced to provide timely indicators of the effect of developing world events on the

UK economy and society, using close-to-real-time big data, administrative data sources, rapid response surveys

or Experimental Statistics.

The data presented in this bulletin are reviewed and refreshed on a regular basis. Indicators are swapped in and

out of the publication based on their suitability and availability.

UK coronavirus (COVID-19) restrictions

A full overview of coronavirus restrictions for each of the four UK constituent countries can be found:

England

Scotland

Wales

Northern Ireland

These restrictions should be considered when interpreting the data featured throughout this bulletin.

Seasonality

Seasonal fluctuations are likely to be present in many of these indicators so caution must be applied when

interpreting changes in series that are not seasonally adjusted.

10 . Related Links

Coronavirus (COVID-19) latest data and analysis

Webpage | Updated as and when data become available

Latest data on the coronavirus in the UK and its effect on the economy and society.

Coronavirus and the social impacts on Great Britain

Bulletin | Released 1 April 2022

Latest indicators from the Opinions and Lifestyle Survey.

Deaths registered weekly in England and Wales, provisional

Bulletin | Released 5 April 2022

Provisional counts of deaths registered in England and Wales, including deaths involving COVID-19, in the

latest weeks for which data are available.

Coronavirus (COVID-19) Infection Survey, UK

Bulletin | Released 1 April 2022

Initial data from the COVID-19 Infection Survey (delivered in partnership with IQVIA, the University of Oxford

and Lighthouse laboratories).

Page 19 of 20Page 20 of 20

You can also read