ECONOMY INSTA PT 2021 EXCLUSIVE - JUNE 2020 - JANUARY 2021 - Insights

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INSTA PT 2021 EXCLUSIVE ECONOMY JUNE 2020 – JANUARY 2021

INSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

www.insightsonindia.com 1 InsightsIAS

INSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

Table of Contents

Schemes / Government Initiatives .............................................................. 5

1. FACELESS TAX SCHEME ............................................................................................... 5

2. NEW INDUSTRIAL DEVELOPMENT SCHEME FOR JAMMU & KASHMIR (J&K IDS, 2021) . 5

3. INSOLVENCY AND BANKRUPTCY CODE (IBC) ................................................................ 5

4. SECTION 32A OF INSOLVENCY AND BANKRUPTCY CODE (IBC) ..................................... 6

5. PRE-PACKS UNDER INSOLVENCY REGIME .................................................................... 6

6. ATMANIRBHAR BHARAT ROJGAR YOJANA (ABRY) ........................................................ 7

7. CODE ON WAGES ACT ................................................................................................. 8

8. MAKE IN INDIA POLICY ................................................................................................ 8

9. DAKPAY....................................................................................................................... 9

10. PRODUCTION-LINKED INCENTIVE (PLI) SCHEME ....................................................... 9

11. ATAL BEEMIT (BIMIT) VYAKTI KALYAN YOJANA ....................................................... 10

12. AGRICULTURE INFRASTRUCTURE FUND ................................................................. 10

13. NATIONAL SMALL SAVINGS FUND (NSSF) ............................................................... 11

14. COUNTRY OF ORIGIN IN GEM PLATFORM .............................................................. 11

15. ESSENTIAL COMMODITIES (AMENDMENT) BILL, 2020............................................ 12

16. MERCHANDISE EXPORTS FROM INDIA SCHEME (MEIS) .......................................... 13

Indian Economy and Issues relating to planning, mobilization of resources,

growth, development and employment .................................................... 14

1. K-SHAPED ECONOMIC RECOVERY.............................................................................. 14

2. CORE SECTOR ........................................................................................................... 15

3. OVERHEATING OF AN ECONOMY .............................................................................. 15

4. TECHNICAL RECESSION ............................................................................................. 15

5. BORROWING BY STATES ............................................................................................ 15

6. FISCAL DEFICIT .......................................................................................................... 16

7. FISCAL POLICY ........................................................................................................... 18

8. COUNTER-CYCLICAL FISCAL POLICY ........................................................................... 18

9. FISCAL PRUDENCE ..................................................................................................... 19

10. ADJUSTED GROSS REVENUE (AGR) ......................................................................... 19

11. GROSS VALUE ADDED (GVA) .................................................................................. 19

12. GROSS DOMESTIC CAPITAL FORMATION (GDCF) .................................................... 20

13. MONETISATION OF ASSETS .................................................................................... 20

14. TRENDS IN THE ECONOMY .................................................................................... 20

Banking Sector / Financial Sector .............................................................. 26

1. BAD BANK ................................................................................................................. 26

2. LIMITED LIABILITY PARTNERSHIP (LLP) ....................................................................... 26

3. HC UPHOLDS ARREST PROVISION IN CGST ACT FOR TAX EVASION ............................. 27

4. LOTTERY, GAMBLING AND BETTING TAXABLE UNDER GST ACT: SC ............................ 27

5. GST: PHYSICAL VERIFICATION OF PREMISES IS NOW MANDATORY ............................ 28

6. GST COMPENSATION ................................................................................................ 28

7. OFF-BUDGET BORROWING ....................................................................................... 28

8. SECURED OVERNIGHT FINANCING RATE (SOFR) ........................................................ 29

9. ASSET UNDER MANAGEMENT (AUM) ........................................................................ 29

www.insightsonindia.com 2 InsightsIAS

INSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

10. BUSINESSES WITH MONTHLY TURNOVER OF OVER ₹50 LAKH TO PAY AT LEAST 1%

GST LIABILITY IN CASH ...................................................................................................... 29

11. ZERO COUPON BONDS .......................................................................................... 30

12. NEGATIVE YIELD BONDS ........................................................................................ 30

13. ADDITIONAL TIER-1 BONDS ................................................................................... 31

14. DEVELOPMENT FINANCE INSTITUTION (DFI) .......................................................... 32

15. PONZI SCHEME ...................................................................................................... 33

16. NON-BANKING FINANCIAL COMPANIES- MICROFINANCE INSTITUTIONS (NBFC-

MFIS).. ............................................................................................................................. 33

17. PRIVATE SECTOR BANKS REFORMS ........................................................................ 34

18. TARGETED LONG TERM REPO OPERATION (TLTRO) ................................................ 34

19. OPEN MARKET OPERATIONS (OMO) ...................................................................... 35

20. OPERATION TWIST ................................................................................................ 35

21. GOVERNMENT SECURITY (G-SEC) .......................................................................... 36

22. CESS ...................................................................................................................... 37

23. CREDIT DEFAULT SWAP ......................................................................................... 37

24. PARTICIPATORY NOTES .......................................................................................... 37

25. SIN GOODS AND SIN TAX ....................................................................................... 38

26. CONTINGENCY FUND (CF) OF THE CENTRAL BANK ................................................. 38

27. PRIORITY SECTOR LENDING (PSL) ........................................................................... 39

28. PAYMENTS INFRASTRUCTURE DEVELOPMENT FUND (PIDF) ................................... 39

29. RIGHTS ISSUE ........................................................................................................ 40

30. BANKING REGULATION (AMENDMENT) BILL, 2020 ................................................ 40

31. COOPERATIVE BANKS UNDER RBI .......................................................................... 41

32. DOMESTIC SYSTEMICALLY IMPORTANT INSURERS (D-SIIS) ..................................... 41

33. LEVERAGE RATIO FOR BANKS................................................................................. 42

External Sector .......................................................................................... 43

1. BILATERAL INVESTMENT TREATY ............................................................................... 43

2. INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS (IAIS) .......................... 43

3. INTERNATIONAL FINANCIAL SERVICES CENTRES AUTHORITY (IFSCA) ......................... 43

4. INTERNATIONAL FINANCIAL SERVICES CENTRES (IFSC) .............................................. 44

5. SPECIAL ECONOMIC ZONES (SEZS) IN INDIA .............................................................. 44

6. CURRENT ACCOUNT SURPLUS ................................................................................... 45

7. LINE OF CREDIT (LOC)................................................................................................ 46

8. FOREIGN CONTRIBUTION (REGULATION) ACT, 2020 .................................................. 46

9. CURRENCY SWAP ARRANGEMENT............................................................................. 46

10. FOREX RESERVES ................................................................................................... 47

11. SPECIAL DRAWING RIGHT (SDR)............................................................................. 47

12. INTERNATIONAL COMPARISON PROGRAM ............................................................ 48

13. CAPITAL ADEQUACY RATIO (CAR) .......................................................................... 48

14. BASEL GUIDELINES ................................................................................................ 48

15. WASHINGTON CONSENSUS ................................................................................... 49

16. ANTI-DUMPING DUTY ............................................................................................ 49

Infrastructure: Energy, Ports, Roads, Airports, Railways etc. ..................... 50

1. NATIONAL INFRASTRUCTURE PIPELINE (NIP) ............................................................. 50

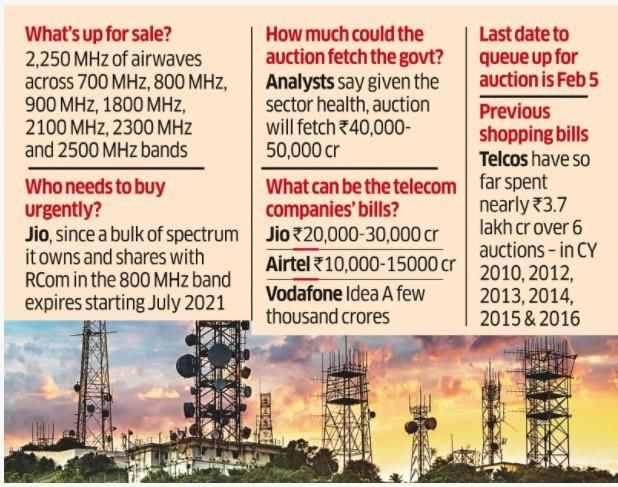

2. SPECTRUM AUCTIONS ............................................................................................... 50

www.insightsonindia.com 3 InsightsIAS

INSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

3. RENEWABLE ENERGY PARK ....................................................................................... 51

4. NATIONAL INVESTMENT AND INFRASTRUCTURE FUND (NIIF) .................................... 51

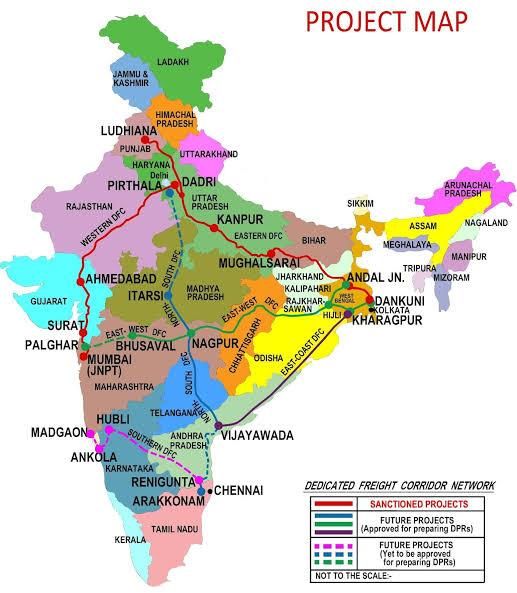

5. DEDICATED FREIGHT CORRIDOR................................................................................ 52

6. CENTRAL ELECTRICITY REGULATORY COMMISSION (CERC) ........................................ 52

7. GUJARAT MARITIME CLUSTER ................................................................................... 52

8. NATURAL GAS MARKETING REFORMS ....................................................................... 53

9. INDIA’S FIRST SEAPLANE PROJECT ............................................................................. 53

10. BOT, HAM AND EPC PROJECTS............................................................................... 54

11. COAL GASIFICATION AND LIQUEFACTION .............................................................. 54

Reports / Ranking / Committees / Awards / Events .................................. 56

1. INDIA INNOVATION INDEX ........................................................................................ 56

2. FIFTEENTH FINANCE COMMISSION ........................................................................... 56

3. KAMATH PANEL REPORT ........................................................................................... 57

4. PURCHASING MANAGER’S INDEX (PMI) ..................................................................... 57

5. CONSUMER PRICE INDEX FOR INDUSTRIAL WORKERS (CPI-IW).................................. 58

6. STATE OF FOOD SECURITY AND NUTRITION IN THE WORLD 2020 (SOFI 2020) ........... 58

Departments / Agencies............................................................................ 59

1. NATIONAL COMPANY LAW APPELLATE TRIBUNAL ..................................................... 59

2. INDIAN BANKS’ ASSOCIATION (IBA) ........................................................................... 59

3. INSURANCE OMBUDSMAN ........................................................................................ 59

4. INDIA ENERGY MODELING FORUM............................................................................ 60

5. DEPUTY GOVERNORS OF RBI ..................................................................................... 61

6. INFRASTRUCTURE INVESTMENT TRUSTS (INVITS) ...................................................... 61

Miscellaneous ........................................................................................... 63

1. NON-PRICE COMPETITION ........................................................................................ 63

2. DATA LOCALISATION NORMS .................................................................................... 63

3. NOBEL PRIZE IN ECONOMICS .................................................................................... 63

4. TRADEMARK ............................................................................................................. 64

www.insightsonindia.com 4 InsightsIAS

INSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

Schemes / Government Initiatives

1. Faceless tax scheme

In the Union Budget 2019, the Finance Minister proposed the introduction of a scheme of faceless

e-assessment.

• The faceless assessment of tax will 'honour honest income tax payers in the country'.

• All income tax appeals, ranging from e-allocation of appeals, to e-communication of notices,

e-verification, e-enquiry and e-hearing will take place online.

• It is an attempt to remove individual tax officials’ discretion and potential harassment for

income tax payers.

• The scheme allows for appropriate cases where a certain hearing is necessary, so then after

following protocols, a hearing is given.

• The main objective is to remove physical interaction as much as possible.

• The National e-Assessment Center in Delhi will be governing authority for all communication

with taxpayers under the faceless assessment scheme.

2. New Industrial Development Scheme for Jammu & Kashmir (J&K IDS,

2021)

Government of India has formulated New Industrial Development Scheme for Jammu & Kashmir

(J&K IDS, 2021) for the development of Industries in the UT of Jammu & Kashmir.

About the scheme:

J&K IDS, 2021 is a Central Sector Scheme. The scheme aims to take industrial development to the

block level in UT of J&K, which is first time in any Industrial Incentive Scheme of the Government

of India.

• The financial outlay of the proposed scheme is Rs.28400 crore for the scheme period 2020-21

to 2036-37.

• Scheme while encouraging new investment, also nurtures the existing industries in J&K by

providing them working capital support at the rate of 5% for 5 years.

Objective:

Main purpose of the scheme is to generate employment which directly leads to the socio-

economic development of the region.

• It aims at development of Manufacturing as well as Service Sector Units in J&K.

Key Features of the Scheme:

• Scheme is made attractive for both smaller and larger units.

• It attempts for a more sustained and balanced industrial growth in the entire UT.

• Scheme has been simplified on the lines of ease of doing business by bringing one major

incentive- GST Linked Incentive- that will ensure less compliance burden without

compromising on transparency.

• It is not a reimbursement or refund of GST but gross GST is used to measure eligibility for

industrial incentive to offset the disadvantages that the UT of J&K face.

3. Insolvency and Bankruptcy Code (IBC)

What is insolvency and bankruptcy?

Insolvency is a situation where individuals or companies are unable to repay their outstanding

debt.

Bankruptcy is a situation whereby a court of competent jurisdiction has declared a person or

other entity insolvent, having passed appropriate orders to resolve it and protect the rights of the

creditors. It is a legal declaration of one’s inability to pay off debts.

www.insightsonindia.com 5 InsightsIAS

INSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

About the IBC:

The Insolvency and Bankruptcy Code, 2016 (IBC) is the bankruptcy law of India which seeks to

consolidate the existing framework by creating a single law for insolvency and bankruptcy.

Insolvency Resolution: The Code outlines separate insolvency resolution processes for

individuals, companies and partnership firms.

For companies, the process will have to be completed in 180 days, which may be extended by 90

days, if a majority of the creditors agree. For start-ups (other than partnership firms), small

companies and other companies (with asset less than Rs. 1 crore), resolution process would be

completed within 90 days of initiation of request which may be extended by 45 days.

The Insolvency and Bankruptcy Code (Amendment) Act, 2019 has increased the mandatory

upper Time limit of 330 days including time spent in legal process to complete resolution process.

Insolvency regulator: The Code establishes the Insolvency and Bankruptcy Board of India, to

oversee the insolvency proceedings in the country and regulate the entities registered under it.

The Board will have 10 members, including representatives from the Ministries of Finance and

Law, and the Reserve Bank of India.

Insolvency professionals: The insolvency process will be managed by licensed professionals.

These professionals will also control the assets of the debtor during the insolvency process.

Bankruptcy and Insolvency Adjudicator: The Code proposes two separate tribunals to oversee

the process of insolvency resolution, for individuals and companies: (i) the National Company Law

Tribunal for Companies and Limited Liability Partnership firms; and (ii) the Debt Recovery

Tribunal for individuals and partnerships.

4. Section 32A of Insolvency and Bankruptcy Code (IBC)

SC has upheld section 32A of Insolvency and Bankruptcy Code (IBC).

What is Section 32A?

• Section 32A provides that Corporate Debtor shall not be prosecuted for an offence committed

prior to commencement of Corporate Insolvency Resolution Process (CIRP) once Resolution

Plan has been approved by Adjudicating Authority (AA).

• The section further provides that no action shall be taken against property of Corporate

Debtor covered under such a Resolution Plan.

What did the Supreme Court say in its judgment?

In its judgment, the apex court, while upholding the validity of Section 32 A of IBC, said

• It was important for the IBC to attract bidders who would offer reasonable and fair value for

the corporate debtor to ensure the timely completion of corporate insolvency resolution

process (CIRP).

• Such bidders must also be granted protection from any misdeeds of the past since they had

nothing to do with it.

• Such protection must also extend to the assets of a corporate debtor, which form a crucial

attraction for potential bidders and helps them in assessing and placing a fair bid for the

company, which, in turn, will help banks clean up their books of bad loans.

5. Pre-packs under Insolvency regime

The Ministry of Corporate Affairs (MCA) has set up a committee to look into the possibility of

including what are called “pre-packs” under the current insolvency regime to offer faster

insolvency resolution under the Insolvency and Bankruptcy Code (IBC).

www.insightsonindia.com 6 InsightsIAS

INSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

So, what is a pre-pack?

Also called as a pre-packaged insolvency, It is an agreement for the resolution of the debt of a

distressed company.

• It is done through an agreement between secured creditors and investors instead of a public

bidding process.

• The process needs to be completed within 90 days so that all stakeholders retain faith in the

system.

Benefits of a pre-pack:

1. Faster: This process would likely be completed much faster than the traditional Corporate

Insolvency Resolution Process (CIRP) which requires that the creditors of the distressed

company allow for an open auction for qualified investors to bid for the distressed company.

2. It would act as an important alternative resolution mechanism to the CIRP and would help

lower the burden on the National Company Law Tribunal (NCLT).

3. In the case of pre-packs, the incumbent management retains control of the company until a

final agreement is reached. This is necessary because Transfer of control from the

incumbent management to an insolvency professional as is the case in the CIRP leads to

disruptions in the business and loss of some high-quality human resources and asset value.

4. Also, a financially distressed company can continue its operations during the period leading

to a formal default, and even thereafter, without the resultant reputational risks, business

disruptions, or value erosion.

What are some of the drawbacks of pre-pack?

Reduced transparency compared to the CIRP as financial creditors would reach an agreement

with a potential investor privately and not through an open bidding process.

• This could lead to stakeholders such as operational creditors raising issues of fair treatment

when financial creditors reach agreements to reduce the liabilities of the distressed

company.

Unlike in the case of a full-fledged CIRP which allows for price discovery, in the case of a pre-pack

the NCLT would only be able to evaluate a resolution plan based on submissions by the creditors

and the investor.

Do we need pre-packs?

Yes. It is because slow progress in the resolution of distressed companies has been one of the

key issues raised by creditors regarding the CIRP under the IBC.

6. Atmanirbhar Bharat Rojgar Yojana (ABRY)

Atmanirbhar Bharat Rojgar Yojana (ABRY) aims to boost employment in formal sector and

incentivize creation of new employment opportunities during the Covid recovery phase under

Atmanirbhar Bharat Package 3.0.

About the Atmanirbhar Bharat Rojgar Yojana (ABRY):

• Under this, Government of India will provide subsidy for two years in respect of new

employees engaged on or after 1st October, 2020 and up to 30th June, 2021.

• Government will pay both 12% employees’ contribution and 12% employers’ contribution i.e.

24% of wages towards EPF in respect of new employees in establishments employing upto

1000 employees for two years.

• Government will pay only employees’ share of EPF contribution i.e. 12% of wages in respect

of new employees in establishments employing more than 1000 employee for two years.

Eligibility:

www.insightsonindia.com 7 InsightsIAS

INSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

• An employee drawing monthly wage of less than Rs. 15000/- who was not working in any

establishment registered with the Employees’ Provident Fund Organisation (EPFO) before 1st

October, 2020 and did not have a Universal Account Number or EPF Member account number

prior to 1st October 2020 will be eligible for the benefit.

• Any EPF member possessing Universal Account Number (UAN) drawing monthly wage of less

than Rs 15000 who made exit from employment during Covid pandemic from March 1, 2020,

to September 30, 2020, and did not join employment in any EPF covered establishment up to

September 30 will also be eligible to avail benefit.

7. Code on Wages Act

• Representatives of industry bodies, had requested the Labour Ministry to hold back

implementation of new definition of wages, which would increase social security deductions

and reduce the take-home pay of workers.

• The new definition of wages is part of the Code on Wages, 2019 passed by Parliament. The

new definition would result in a major cut in take-home salaries and also place a burden on

employers.

About the Code on Wages Act:

The code will amalgamate the Payment of Wages Act, 1936, the Minimum Wages Act, 1948, the

Payment of Bonus Act, 1965, and the Equal Remuneration Act, 1976.

• The wage code universalises the provisions of minimum wages and timely payment of

wages to all employees, irrespective of the sector and wage ceiling.

• It ensures the “right to sustenance” for every worker and intends to increase the legislative

protection of minimum wage from existing about 40% to 100% workforce.

• It also introduces the concept of statutory floor wage which will be computed based on

minimum living conditions and extended qualitative living conditions across the country for all

workers.

• While fixing the minimum rate of wages, the central government shall divide the concerned

geographical area into three categories – metropolitan area, non-metropolitan area and the

rural area.

• Wages include salary, allowance, or any other component expressed in monetary terms. This

does not include bonus payable to employees or any travelling allowance, among others.

• The minimum wages decided by the central or state governments must be higher than the

floor wage.

• Payment of wages: Wages will be paid in (i) coins, (ii) currency notes, (iii) by cheque, (iv) by

crediting to the bank account, or (v) through electronic mode. The wage period will be fixed

by the employer as either: (i) daily, (ii) weekly, (iii) fortnightly, or (iv) monthly.

8. Make in India policy

The Ministry of Railways had written to the Department for Promotion of Industry & Internal

Trade (DPIIT) seeking exemption for procuring certain medical items manufactured outside

India, particularly medicines used in the treatment of COVID-19 and cancer.

What's the issue?

In the existing ‘Make in India’ policy, there is no window available to procure such items from the

suppliers who may not meet the Local Content Criteria required for Class-I and Class-II Local

Supplier category.

1. Class-I is a local supplier or service provider whose goods, services or works offered for

procurement have local content equal to or more than 50%.

2. Class-II is a supplier or service provider whose goods, services or works offered for

procurement have local content of more than 20% but less than 50%.

www.insightsonindia.com 8 InsightsIAS

INSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

Only these two categories of suppliers shall be eligible to bid in the procurement of all goods,

services or works and with estimated value of purchases of less than ₹200 crore.

About 'Make in India' Policy:

On September 25, 2014, the Indian government announced the ‘Make in India’ initiative to

encourage manufacturing in India and galvanize the economy with dedicated investments in

manufacturing and services.

Targets:

1. To increase the manufacturing sector’s growth rate to 12-14% per annum in order to increase

the sector’s share in the economy.

2. To create 100 million additional manufacturing jobs in the economy by 2022.

3. To ensure that the manufacturing sector’s contribution to GDP is increased to 25% by 2022

(revised to 2025) from the current 15-16%.

Outcomes so far:

1. Foreign direct investment (FDI) has increased from $16 billion in 2013-14 to $36 billion in

2015-16 but it has not increased further and is not contributing to Indian industrialisation.

2. FDIs in the manufacturing sector are becoming weaker than before. It has come down to $7

billion in 2017-18 as compared to $9.6 billion in 2014-15.

3. FDIs in the service sector is $23.5 billion, more than three times that of the manufacturing

sector.

4. India’s share in the global exports of manufactured products remains around 2% which is far

less than 18% share of China.

9. DakPay

It is a new digital payment application launched by the Department of Posts and the India Post

Payments Bank (IPPB).

● DakPay is a suite of digital financial and assisted banking services provided through the postal

network to cater to the financial needs of various sections of society, particularly those living

in rural areas.

● The services include free-of-cost money receipts and transfers at doorsteps, and scanned QR

codes, to make payments for a range of utility and banking services.

10. Production-linked incentive (PLI) scheme

The Central government has unveiled a production-linked incentive (PLI) scheme to encourage

domestic manufacturing investments in 10 more sectors.

The 10 sectors include:

Food processing, telecom, electronics, textiles, speciality steel,

automobiles and auto components, solar photo-voltaic modules

and white goods, such as air conditioners and LEDs.

About the PLI scheme:

To make India a manufacturing hub, the government had

announced the PLI scheme for mobile phones, pharma

products, and medical equipment sectors.

● Notified on April 1, 2020 as a part of the National Policy on

Electronics.

● It proposes a financial incentive to boost domestic

manufacturing and attract large investments in the

electronics value chain.

www.insightsonindia.com 9 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

What the scheme seeks to achieve?

1. Make domestic manufacturing competitive and efficient.

2. Create economies of scale.

3. Make India part of global supply chain.

4. Attract investment in core manufacturing and cutting edge tech.

5. Competitive manufacturing would in turn lift exports.

Key features of the scheme:

● The scheme shall extend an incentive of 4% to 6% on incremental sales (over base year) of

goods manufactured in India and covered under target segments, to eligible companies, for a

period of five (5) years with financial year (FY) 2019-20 considered as the base year for

calculation of incentives.

● The Scheme will be implemented through a Nodal Agency which shall act as a Project

Management Agency (PMA) and be responsible for providing secretarial, managerial and

implementation support and carrying out other responsibilities as assigned by MeitY from

time to time.

What kind of investments will be considered?

All electronic manufacturing companies which are either Indian or have a registered unit in India

will be eligible to apply for the scheme.

These companies can either create a new unit or seek incentives for their existing units from one

or more locations in India.

● However, all investment done by companies on land and buildings for the project will not be

considered for any incentives or determine eligibility of the scheme.

11. Atal Beemit (Bimit) Vyakti Kalyan Yojana

Launched by the Employee’s State Insurance (ESI) in 2018.

Aim: It aims to financially support those who lost their jobs or rendered jobless for whatsoever

reasons due to changing employment pattern.

Eligibility criteria for availing the relief were relaxed in August 2020, as under:

1. The payment of relief has been enhanced to 50% of average of wages from earlier 25% of

average wages payable upto maximum 90 days of unemployment.

2. Instead of the relief becoming payable 90 days after unemployment, it shall become due for

payment after 30 days.

3. The Insured Person should have been insurable employment for a minimum period of 2 years

before his/her unemployment and should have contributed for not less than 78 days in the

contribution period immediately preceding to unemployment and minimum 78 days in one of

the remaining 3 contribution periods in 02 years prior to unemployment.

12. Agriculture Infrastructure Fund

It is a new pan India Central Sector Scheme.

• The scheme shall provide a medium - long term debt financing facility for investment in

viable projects for post-harvest management Infrastructure and community farming assets

through interest subvention and financial support.

• The duration of the Scheme shall be from FY2020 to FY2029 (10 years).

Eligibility:

Under the scheme, Rs. One Lakh Crore will be provided by banks and financial institutions as

loans to Primary Agricultural Credit Societies (PACS), Marketing Cooperative Societies, FPOs,

SHGs, Farmers, Joint Liability Groups (JLG), Multipurpose Cooperative Societies, Startups etc.

Interest subvention:

www.insightsonindia.com 10 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

All loans under this financing facility will have interest subvention of 3% per annum up to a limit

of Rs. 2 crore. This subvention will be available for a maximum period of seven years.

Credit guarantee:

• Credit guarantee coverage will be available for eligible borrowers from this financing facility

under Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) scheme for a

loan up to Rs. 2 crore.

• In case of FPOs the credit guarantee may be availed from the facility created under FPO

promotion scheme of Department of Agriculture, Cooperation & Farmers Welfare (DACFW).

Management of the fund:

• It will be managed and monitored through an online Management Information System (MIS)

platform.

• The National, State and District level Monitoring Committees will be set up to ensure real-

time monitoring and effective feed-back.

13. National Small Savings Fund (NSSF)

• A “National Small Savings Fund” (NSSF) in the Public Account of India has been established

with effect from 1.4.1999.

• All small savings collections are credited to this Fund.

• Similarly, all withdrawals under small savings schemes by the depositors are made out of the

accumulations in this Fund.

• The balance in the Fund is invested in Central and State Government Securities.

• The investment pattern is as per norms decided from time to time by the Government of

India.

• The Fund is administered by the Government of India, Ministry of Finance (Department of

Economic Affairs) under National Small Savings Fund (Custody and Investment) Rules, 2001,

framed by the President under Article 283(1) of the Constitution.

• The objective of NSSF is to de-link small savings transactions from the Consolidated Fund of

India and ensure their operation in a transparent and self-sustaining manner.

• Since NSSF operates in the public account, its transactions do not impact the fiscal deficit of

the Centre directly.

• As an instrument in the public account, the balances under NSSF are direct liabilities and

constitute a part of the outstanding liabilities of the Centre.

• The NSSF flows affect the cash position of the Central Government.

14. Country of Origin in GeM platform

Government e-Marketplace (GeM) has brought in certain changes to promote ‘Make in India’

and ‘Aatmanirbhar Bharat’.

1. It is now mandatory for sellers to enter the Country of Origin while registering all new

products on GeM.

2. ‘Make in India’ filter has now been enabled on the portal. Buyers can choose to buy only

those products that meet the minimum 50% local content criteria.

GeM is a state-of-the-art national public procurement platform of Ministry of Commerce and

Industries, that has used technology to remove entry barriers for bonafide sellers and has created

a vibrant e-marketplace with a wide range of goods and services.

GeM facilities:

1. Listing of products for individual, prescribed categories of Goods/ Services of common use.

2. Look, estimate, compare and buying facility on dynamic pricing basis.

3. Market place buying of majority of common User Items.

www.insightsonindia.com 11 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

4. Buying Goods and Services online, as and when required.

5. Transparency and ease of buying.

6. Useful for low value buying and also for bulk buying at competitive price using Reverse

Auction/ e-bidding.

7. Continuous vendor rating system.

8. Return policy.

Who can buy/purchase through GeM?

All Central government and State Government Ministries/Departments including its

attached/subordinate offices, Central and State autonomous bodies, Central and State Public

Sector Units and local bodies etc. are authorized to make procurement through GeM portal.

Who can sell on GeM?

The “Seller(s)” on GeM will be the OEMs (Original Equipment Manufacturers) and/or their

authorized channel partner(s)/ resellers (having any general authorization / dealership of the

OEM to sell their product in open market) and e- Marketplaces.

15. Essential Commodities (Amendment) Bill, 2020

Parliament passed the Essential Commodities (Amendment) Bill, 2020.

• The Essential Commodities (Amendment) Bill 2020 has provisions to remove commodities like

cereals, pulses, oilseeds, edible oils, onion and potatoes from the list of essential

commodities.

• The EC (Amendment) Bill 2020 aims to remove fears of private investors of excessive

regulatory interference in their business operations.

• In situations such as war, famine, extraordinary price rise and natural calamity, such

agricultural foodstuff can be regulated.

Essential Commodities Act (ECA):

www.insightsonindia.com 12 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

• The Essential Commodities Act (ECA) is an act of the Parliament of India that was established

to ensure the delivery of certain commodities or products, the supply of which, if obstructed

due to hoarding or black marketing, would affect the normal life of the people.

• The ECA was enacted in 1955 and has since been used by the Government to regulate the

production, supply, and distribution of a whole host of commodities that it declares ‘essential’

to make them available to consumers at fair prices.

• Additionally, the government can also fix the minimum support price (MSP) of any packaged

product that it declares an “essential commodity”.

• The list of items under the Act includes drugs, fertilizers, pulses, and edible oils, as well as

petroleum and petroleum products.

Powers of Central Government under the Essential Commodities Act, 1955:

● The central government can designate certain commodities as essential commodities.

● The central government may regulate or prohibit the production, supply, distribution, trade,

and commerce of such essential commodities.

16. Merchandise Exports from India Scheme (MEIS)

A limit has been imposed on total rewards under the Merchandise Exports from India Scheme

(MEIS).

A scheme designed to provide rewards to exporters to offset infrastructural inefficiencies and

associated costs. The Duty Credit Scrips and goods imported/ domestically procured against them

shall be freely transferable. The Duty Credit Scrips can be used for:

• Payment of Basic Customs Duty and Additional Customs Duty specified under sections 3(1),

3(3) and 3(5) of the Customs Tariff Act, 1975 for import of inputs or goods, including capital

goods, except items listed in Appendix 3A.

• Payment of Central excise duties on domestic procurement of inputs or goods,

• Payment of Basic Customs Duty and Additional Customs Duty specified under Sections 3(1),

3(3) and 3(5) of the Customs Tariff Act, 1975.

Merchandise Exports from India Scheme (MEIS) under Foreign Trade Policy of India (FTP 2015-20)

is one of the two schemes introduced in Foreign Trade Policy of India 2015-20, as a part of Exports

from India Scheme (The other scheme is Service Exports from India Scheme (SEIS)).

• The rewards are given by way of duty credit scrips to exporters.

• The MEIS is notified by the DGFT (Directorate General of Foreign Trade) and

implemented by the Ministry of Commerce and Industry.

Objective of the scheme:

To offset infrastructural inefficiencies and associated costs involved in export of goods/products,

which are produced/manufactured in India, especially those having high export intensity,

employment potential and thereby enhancing India’s export competitiveness.

MEIS replaced the following five other similar incentive schemes present in the earlier Foreign

Trade Policy 2009-14:

1. Focus Product Scheme (FPS).

2. Focus Market Scheme (FMS).

3. Market Linked Focus Product Scheme (MLFPS).

4. Infrastructure incentive scheme.

5. Vishesh Krishi Gramin Upaj Yojna (VKGUY).

www.insightsonindia.com 13 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

Indian Economy and Issues relating to planning, mobilization of

resources, growth, development and employment

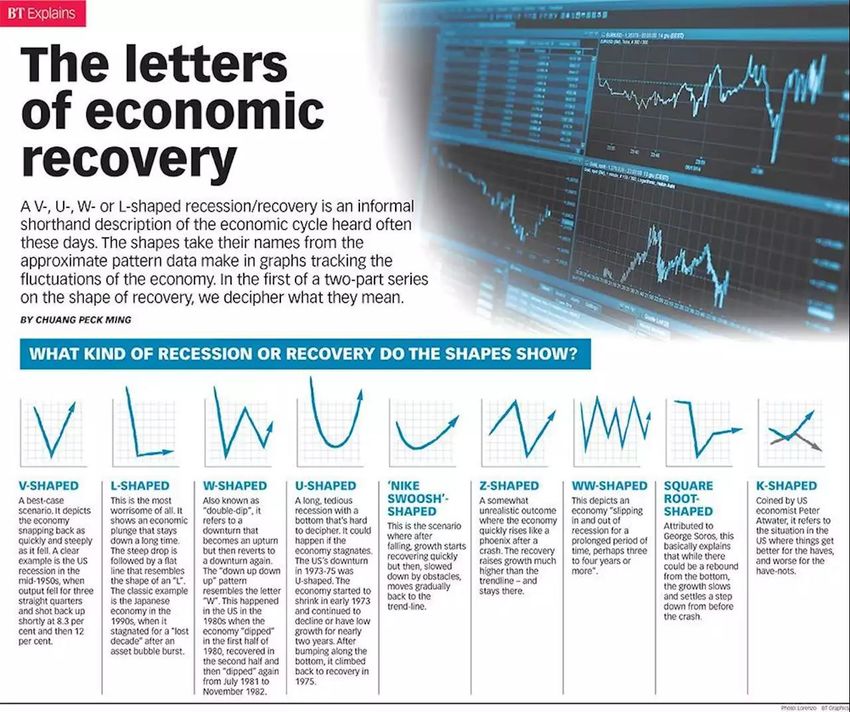

1. K-shaped Economic Recovery

A K-shaped recovery happens when different sections of an economy recover at starkly different

rates.

• Households at the top of the pyramid are likely to have seen their in- comes largely protected,

and savings rates forced up during the lockdown, increasing ‘fuel in the tank’ to drive future

consumption.

• Meanwhile, households at the bottom are likely to have witnessed permanent hits to jobs and

incomes.

What are the macro implications of a K-shaped recovery?

• Upper-income households have benefitted from higher savings for two quarters.

• Households at the bottom have experienced a permanent loss of income in the forms of jobs

and wage cuts; this will be a recurring drag on demand, if the labour market does not heal

faster.

www.insightsonindia.com 14 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

• To the extent that COVID has triggered an effective income transfer from the poor to the rich,

this will be demand-impeding because the poor have a higher marginal propensity to

consume (i.e. they tend to spend (instead of saving) a much higher proportion of their

income.

2. Core Sector

• The eight core sector industries include coal, crude oil, natural gas, refinery products,

fertiliser, steel, cement and electricity

• The eight core industries comprise nearly 40% of the weight of items included in the Index of

Industrial Production (IIP).

• The eight Core Industries in decreasing order of their weightage: Refinery Products>

Electricity> Steel> Coal> Crude Oil> Natural Gas> Cement> Fertilizers.

3. Overheating of an economy

• Overheating of an economy occurs when its productive capacity is unable to keep pace with

growing aggregate demand.

• It is generally characterised by a below-average rate of economic growth, where growth is

occurring at an unsustainable rate.

• Boom periods are often characterised by overheating in the economy.

• An economy is said to be overheated when inflation increases due to prolonged good growth

rate and the producers produce in excess thereby creating excess production capacity.

• The main reason behind overheating is insufficient supply allocation because of excess

spending by the people due to increase in consumer wealth.

Effects:

• Overheating is generally preceded by lower than average economic growth.

• Demand pull inflation occurs as suppliers try to capitalize on the excess demand which

cannot be met via existing production constraints.

• These higher prices tend to reduce aggregate demand and exports (since goods and services

become more expensive abroad) leading to reduced consumption.

• Central banks often simultaneously tighten monetary policy in response to increased

inflationary pressures, reducing investment expenditure, which in tandem with decreased

consumption, can lead to economic recession.

4. Technical recession

Recently, the Reserve Bank of India (RBI) said the country had entered into a technical recession

in the first half of 2020-21.

What is a technical recession?

It refers to the sequential decline in GDP for the past two quarters. This presents economic

contraction since the GDP measures the value of all goods and services produced in a country

during a specific period of time, in other words, the total expenditure in the economy.

● Typically, recessions last for a few quarters. If they continue for years, they are referred to

as “depressions”. But a depression is quite rare; the last one was during the 1930s in the US.

5. Borrowing by States

Borrowing by the Government of India and Borrowing by States are defined under Article 292 and

293 of Constitution of India respectively.

Article 293 of Constitution of India "Borrowing by States":

www.insightsonindia.com 15 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

1. Subject to the provisions of this article, the executive power of a State extends to borrowing

within the territory of India upon the security of the Consolidated Fund of the State within

such limits, if any, as may from time to time be fixed by the Legislature of such State by law

and to the giving of guarantees within such limits, if any, as may be so fixed.

2. The Government of India may, subject to such conditions as may be laid down by or under

any law made by Parliament, make loans to any State or, so long as any limits fixed under

Article292 are not exceeded, give guarantees in respect of loans raised by any State, and any

sums required for the purpose of making such loans shall be charged on the Consolidated

Fund of India.

3. A State may not without the consent of the Government of India raise any loan if there is still

outstanding any part of a loan which has been made to the State by the Government of India

or by its predecessor Government, or in respect of which a guarantee has been given by the

Government of India or by its predecessor Government.

Why states need centre's permission while borrowing? Is it mandatory for all states?

Article 293(3) of the Constitution requires states to obtain the Centre’s consent in order to

borrow in case the state is indebted to the Centre over a previous loan.

● This consent can also be granted subject to certain conditions by virtue of Article 293(4).

● In practice, the Centre has been exercising this power in accordance with the

recommendations of the Finance Commission.

Every single state is currently indebted to the Centre and thus, all of them require the Centre’s

consent in order to borrow.

Does the Centre have unfettered power to impose conditions under this provision?

Neither does the provision itself offer any guidance on this, nor is there any judicial precedent

that one could rely on.

● Interestingly, even though this question formed part of the terms of reference of the 15th

Finance Commission, it was not addressed in its interim report.

So, when can the centre impose conditions?

The Centre can impose conditions only when it gives consent for state borrowing, and it can only

give such consent when the state is indebted to the Centre.

6. Fiscal deficit

The Union Government’s fiscal deficit widened to ₹9.53 lakh crore, or close to 120% of the annual

budget estimate, at the end of October 2020.

Reasons behind this:

● The deficit widened mainly due to poor revenue realisation.

● The lockdown had significantly impacted business activities and in turn contributed to

sluggish revenue realisation.

What is the fiscal deficit?

It is the difference between the Revenue Receipts plus Non-debt Capital Receipts (NDCR) and

the total expenditure.

● In other words, fiscal deficit is “reflective of the total borrowing requirements of

Government”.

Impact of high fiscal deficit:

In the economy, there is a limited pool of investible savings. These savings are used by financial

institutions like banks to lend to private businesses (both big and small) and the governments

(Centre and state).

www.insightsonindia.com 16 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

● If the fiscal deficit ratio is too high, it implies that there is a lesser amount of money left in

the market for private entrepreneurs and businesses to borrow.

● Lesser amount of this money, in turn, leads to higher rates of interest charged on such

lending.

● A high fiscal deficit and higher interest rates would also mean that the efforts of the Reserve

Bank of India to reduce interest rates are undone.

What is the acceptable level of fiscal deficit for a developing economy?

For a developing economy, where private enterprises may be weak and governments may be in a

better state to invest, fiscal deficit could be higher than in a developed economy.

● Here, governments also have to invest in both social and physical infrastructure upfront

without having adequate avenues for raising revenues.

● In India, the FRBM Act suggests bringing the fiscal deficit down to about 3 percent of the

GDP is the ideal target. Unfortunately, successive governments have not been able to

achieve this target.

What is an escape clause?

The "escape clause" allows the government to breach its fiscal deficit target by 0.5 percentage

points at times of severe stress in the economy, including periods of structural change and those

when growth falls sharply.

What is government borrowing?

Borrowing is a loan taken by the government and falls under capital receipts in the Budget

document.

Usually, Government borrows through issue of government securities called G-secs and Treasury

Bills.

How does increased government

borrowing affect govt finances?

Bulk of government's fiscal deficit

comes from its interest obligation

on past debt.

● If the government resorts to

larger borrowings, more than

what it has projected, then its

interest costs also go up

risking higher fiscal deficit.

That hurts government's

finances.

● Larger borrowing programme

means that the public debt

will go up and especially at a

time when the GDP growth is subdues, it will lead to a higher debt-to-GDP ratio.

Fiscal Consolidation:

Fiscal Consolidation refers to the policies undertaken by Governments (national and sub-

national levels) to reduce their deficits and accumulation of debt stock.

FISCAL CONSOLIDATION is a process where government's FISCAL health is getting improved and is

indicated by reduced FISCAL deficit. Improved tax revenue realization and better aligned

expenditure are the components of FISCAL CONSOLIDATION as the FISCAL deficit reaches at a

manageable level.

www.insightsonindia.com 17 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

7. Fiscal Policy

• Fiscal policy is the guiding force that helps the government decide how much money it should

spend to support the economic activity, and how much revenue it must earn from the system,

to keep the wheels of the economy running smoothly.

• Through the fiscal policy, the government of a country controls the flow of tax revenues and

public expenditure to navigate the economy.

• If the government receives more revenue than it spends, it runs a surplus, while if it spends

more than the tax and non-tax receipts, it runs a deficit.

Main objectives of Fiscal Policy in India:

• Economic growth: Fiscal policy helps maintain the economy’s growth rate so that certain

economic goals can be achieved.

• Price stability: It controls the price level of the country so that when the inflation is too high,

prices can be regulated.

• Full employment: It aims to achieve full employment, or near full employment, as a tool to

recover from low economic activity.

What is the difference between fiscal policy and monetary policy?

• The Reserve Bank of India (RBI) is vested with the responsibility of conducting monetary

policy. This responsibility is explicitly mandated under the Reserve Bank of India Act, 1934.

• The primary objective of monetary policy is to maintain price stability while keeping in mind

the objective of growth.

• In May 2016, the Reserve Bank of India (RBI) Act, 1934 was amended to provide a statutory

basis for the implementation of the flexible inflation targeting framework.

• The amended RBI Act also provides for the inflation target to be set by the Government of

India, in consultation with the Reserve Bank, once in every five years.

• RBI primarily factors in retail inflation while making its bi-monthly monetary policy.

On the other hand, under the fiscal policy, the government deals with taxation and spending by

the Centre.

Importance of Fiscal Policy in India:

• In a country like India, fiscal policy plays a key role in elevating the rate of capital formation

both in the public and private sectors.

• Through taxation, the fiscal policy helps mobilise considerable amount of resources for

financing its numerous projects.

• Fiscal policy also helps in providing stimulus to elevate the savings rate.

• The fiscal policy gives adequate incentives to the private sector to expand its activities.

• Fiscal policy aims to minimise the imbalance in the dispersal of income and wealth.

8. Counter-cyclical fiscal policy

While counter-cyclical fiscal policy is necessary to smooth out economic cycles, it becomes

critical during an economic crisis.

Relevance of Counter-cyclical Fiscal Policy:

Indian Kings used to build palaces during famines and droughts to provide employment and

improve the economic fortunes of the private sector. Economic theory, in effect, makes the same

recommendation: in a recessionary year, Government must spend more than during expansionary

times. Such counter-cyclical fiscal policy stabilizes the business cycle by being contractionary

(reduce spending/increase taxes) in good times and expansionary (increase spending/reduce

taxes) in bad times. On the other hand, a pro-cyclical fiscal policy is the one wherein fiscal policy

www.insightsonindia.com 18 InsightsIASINSTA PT 2021 EXCLUSIVE (ECONOMY)

NOTES

reinforces the business cycle by being expansionary during good times and contractionary

during recessions.

9. Fiscal prudence

• In simple words, fiscal prudence is Spending within budget.

• For any economy to mature, fiscal prudence is critical. If the government continues to spend

way more than its revenues, it will either have to print more currency or borrow from the

market to meet the shortfall. Printing currency will fuel inflation and, at times, hyper-inflation.

• In a bid to avoid these scenarios and mandate fiscal prudence, the Government of India

passed the Fiscal Responsibility and Budget Management (FRBM) Act in 2003. Its objective

was to institutionalise fiscal prudence and reduce the country’s fiscal deficit in such a manner

that it gradually moves towards balancing the Budget.

10. Adjusted gross revenue (AGR)

The Supreme Court has allowed telecom companies 10 years’ time to pay their adjusted gross

revenue (AGR) dues to the government.

What is AGR?

Adjusted Gross Revenue (AGR) is the usage and licensing fee that telecom operators are charged

by the Department of Telecommunications (DoT). It is divided into spectrum usage charges and

licensing fees, pegged between 3-5 percent and 8 percent respectively.

How is it calculated?

As per DoT, the charges are calculated based on all revenues earned by a telco – including non-

telecom related sources such as deposit interests and asset sales.

What are issues associated? When it all began?

The telecom sector was liberalised under the National Telecom Policy, 1994 after which licenses

were issued to companies in return for a fixed license fee.

However, to provide relief from the steep fixed license fee, the government in 1999 gave an

option to the licensees to migrate to the revenue sharing fee model.

• Under this, mobile telephone operators were required to share a percentage of their AGR

with the government as annual license fee (LF) and spectrum usage charges (SUC).

License agreements between the Department of Telecommunications (DoT) and the

telecom companies define the gross revenues of the latter.

The dispute between DoT and the mobile operators was mainly on the definition of AGR.

• The DoT argued that AGR includes all revenues (before discounts) from both telecom and

non-telecom services. The companies claimed that AGR should comprise just the revenue

accrued from core services and not dividend, interest income or profit on sale of any

investment or fixed assets.

11. Gross value added (GVA)

It is a measure of total output and income in the economy. It provides the rupee value for the

amount of goods and services produced in an economy after deducting the cost of inputs and raw

materials that have gone into the production of those goods and services. It also gives sector-

specific picture like what is the growth in an area, industry or sector of an economy.

GVA is sector specific while GDP is calculated by summation of GVA of all sectors of economy

with taxes added and subsidies are deducted.

While GVA gives a picture of the state of economic activity from the producers’ side or supply

side, the GDP gives the picture from the consumers’ side or demand perspective. Both measures

www.insightsonindia.com 19 InsightsIASYou can also read