Spring 2021 Economic Outlook - Beyond COVID - Bennett Jones

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Spring 2021

Economic Outlook

Beyond COVID

Spring 2021 Economic Outlook i

bennettjones.com

Table of Contents

Executive Summary.................................................................................................................................................2

I. Introduction: Light at the End of the Tunnel, Still a Long Road Ahead.............................................................7

II. The Outlook to the End of 2023: A Strong Recovery.......................................................................................13

The Global Economy....................................................................................................................................13

U.S. Monetary Policy Framework and Its Implications......................................................................20

The Canadian Economy................................................................................................................................22

Fiscal Scenarios for Canada: Can It All Add Up?................................................................................25

Proposed Planning Assumptions for Businesses.......................................................................................28

III. The Labour Market: Retrospective and Perspective.......................................................................................29

IV. A Growth Strategy for Canada: Shifting Our Focus to Investment................................................................37

V. International Trade Relations: Evolving Context and Priorities.......................................................................46

Notes......................................................................................................................................................................55

Spring 2021 Economic Outlook iii

"The pandemic and consequent quarantine have exacerbated many latent economic and social ills and raised fundamental questions. A fractured, less benign world. The role of government. The role of the corporation and the desire to accommodate new priorities—without fully surrendering to views nurtured in prosperity that have become untethered from their own economic patrimony. A prevailing anxiety in a world that has been living under threat. We can see light at the end of the pandemic tunnel. A sense of relief and renewal. Confidence in the continuing promise of Canada. But also longstanding challenges that have to be taken head on. Once again our Public Policy group provides a current state description, and next step guidance. Tools for individuals, corporations, the mediating institutions essential to civic life, and government. Tools to help build a prosperous future. I sincerely hope that you find this report useful." Hugh MacKinnon, Chairman and CEO, Bennett Jones

Executive Summary

Executive Summary

While economic recovery from the pandemic to date, demand for our exports, including tourism; high

internationally and in Canada, has been uneven and commodity prices; the response of business

bumpy, a large share of output and jobs have been investment to the improved outlook; and continued,

regained, and the prospects for advanced economies overall accommodative financial conditions. This

are strong. will be mitigated, but only in part, by reduced fiscal

support from governments, a strong Canadian dollar

If immediate attention must still be focused on and a shortage of industrial inputs and labour in

overcoming the pandemic durably, the time is right some sectors of the economy.

for Canada to look beyond COVID, and to articulate

and execute a strategy for investment and long-term

improvement in our competitiveness, productivity, Key Risks to the Outlook

and standard of living. The evolution of the pandemic continues to

represent the predominant risk to the global and

The Outlook to the End of 2023 Canadian economic outlooks. Sustained vaccination

and effective public health measures, including at

In our baseline scenario, on the assumption that the our borders, are necessary to contain the pandemic

pace of vaccination is maintained, if not accelerated, durably. Indeed, no solution will be definitive until

we expect the recovery in advanced economies to there is wider global success in managing and

shift into higher gear in the second half of 2021, hopefully eradicating COVID-19.

before easing gradually during the next two years.

Output would return to its pre-pandemic level by the The second key risk is inflation and interest rates.

third quarter of 2021, and back to its pre-pandemic Buoyant growth of demand for goods in the United

trend level by the end of 2022. States and China has already stimulated demand

for industrial inputs and pushed up the prices

These near-term prospects are considerably of commodities. Tightness in supply chains and

improved since last fall. A stronger U.S. economy, adjustment to the recovery has also resulted in sharp

aided by larger fiscal stimulus and a faster roll out rises in the prices of some intermediate inputs, from

of vaccines than we assumed, underpins a more shipping to semi-conductors.

positive outlook.

While there is much uncertainty about how

For Canada, similarly, we expect that growth will persistent such cost pressures will be, on balance we

accelerate in the second half of 2021, before slowing expect that they will start to ease by the end of 2021.

during the next two years. Real GDP would grow Against our outlook for the U.S. economy, we think

5.5% during 2021 (i.e., between the fourth quarter that a “data-dependent” Federal Reserve, applying its

of 2020 and the fourth quarter of 2021), 2.6% during new framework, will begin to taper bond purchases

2022, and 1.9% during 2023. in the first half of 2022, and finally begin to raise the

Several factors will support the Canadian economy policy rate by the end of 2022.

in getting back to its potential in the second half There is, however, a risk that U.S. inflation rises

of 2022, and to exceed it slightly in 2023: improved more, and for longer, than anticipated because of

household confidence and spending; strong U.S.

Spring 2021 Economic Outlook 2

more persistent cost pressures and/or overheating In particular, the pandemic accelerated the structural

of the economy. This could lead to higher interest trend of loss of lower-skilled jobs to automation. The

rates in 2022, and slower than projected growth need is greater than ever for a framework of life-long

thereafter. Indeed, there is a serious debate learning and skills development that encompasses

underway regarding the prospects that trend early learning, education (literacy skills and micro

inflation in advanced economies could be higher in credentials), apprenticeship and on-the-job training,

the medium term than has been experienced in the and the re-skilling and upskilling of workers.

last two decades of generally below-target inflation.

Unfortunately, Canada historically has under-

Against this backdrop, we propose in this outlook invested in skills development. In the public sector,

some planning assumptions for businesses to the there is no standardized report card publicly

end of 2023, including GDP growth, inflation, and available on the success of existing skills training

interest rates in the United States and in Canada. programs at federal and provincial levels. In the

private sector, hiring requirements and training

programs typically do not favour acquisition of

Solid Recovery in Labour Market

experience and skills by the most vulnerable workers.

but Pandemic Has Highlighted Numerous reports, and an emerging consensus

Structural Challenges among experts, identify avenues for improvement.

Consistent with our baseline scenario, total

The pandemic has also added to pressure for

employment in Canada is expected to be back to the

Canada to enhance access to childcare. Low-wage,

pre-pandemic level as early as the end of this year.

young female workers were among the hardest hit by

By the second quarter of 2023, the employment rate

the pandemic. Many exited the workforce to care for

and the unemployment rate may also be expected to

their children.

return to their levels of February 2020.

A Canada-wide Early Learning and Child Care

In Budget 2021, the Government of Canada initiated

Plan represented the most significant long-term

a tapering and adjustment of emergency programs

commitment in federal Budget 2021. While the

introduced during the pandemic. Given the robust

proposed new funding is significant, the details

recovery, the distorting effects of interventions if

of implementation are not tied down. The goal

prolonged, and the large costs of the programs, this

of 50/50 federal-provincial cost-sharing and the

is broadly appropriate.

intention to apply federal standards for delivery

The disruption in the labour market caused by the mean that reaching agreement with provinces will

pandemic was sharply differentiated by sector and by be a daunting task. The best approaches to support

segment of the labour force. Its impacts will be felt long-term growth would address not only the needs

longer by more vulnerable workers. There will also be of working parents, but also the early development

permanent changes in the way we work, for example needs of children.

with more Canadians expected to continue working

from home, at least for part of their work week. Governments in Canada Not on Track of

Drawing lessons from the pandemic, and looking Fiscal Sustainability for Medium Term

beyond at the changing nature of work, labour Our last outlook proposed two fiscal anchors for

market policies require heightened attention to governments to ensure fiscal sustainability: a

foster growth and inclusion. declining debt-to-GDP ratio; and a 10% rule under

bennettjones.com

Executive Summary

which program spending should be restrained so The two trends together result in higher net

that the projected ratio of debt service costs to borrowing from the rest of the world.

revenues does not exceed 10%.

Thus, it is a priority for Canada to allocate a larger

Taking into account debt accumulated during the share of economic activity to investment in the

pandemic, the current fiscal plans of governments, factors of production—physical, human, and

and reasonable assumptions for growth and interest intangible capital—that will enable our economy to

rates, we conclude that the federal fiscal framework perform better in global markets. This will be aided

is unlikely to be sustainable. The sustainability of by a growth strategy for the country.

national finances, including the budgets of federal

and provincial governments, is even more tenuous. A growth strategy is not old-style industrial policy,

with heavy intervention and spending by government

Collectively, federal and provincial governments in every sector of the economy. At its core, a

must publicly acknowledge that if the quality of successful strategy needs to be one which is easily

public services (including income transfers) is to be understood, represents a consensus between policy

even maintained, let alone improved or expanded, makers and the other major actors in the economy,

tax increases will be required. In the long run, fiscal and can be counted upon to last through the

sustainability depends also critically on economic medium term and even beyond.

growth, which in turn depends on investment and

productivity growth. At a more granular level, a strategy requires

an assessment of structural policies such as

competition, taxation (tax rates and structure

The Case for a Growth Strategy of the system), regulation, intellectual property,

With governments and businesses focused to date international trade and investment, as well as

on reopening the economy and recovering losses targeted initiatives to support adjustment to change.

of output and jobs, there has been lesser attention

There have already been many contributions,

on the rebuilding of our economy for a post-COVID

including from private sector leaders, to the

world.

development of a strategy. What is required now is a

While Canadians understandably may wish after a clear articulation, ongoing public and private sector

historic crisis for the economy to get back to normal, engagement, and a focus on execution.

and for businesses and workers to enjoy a greater

A growth strategy must be responsive, in particular,

measure of security, there is, in fact, no comfortable

to two global forces: climate change and the

steady state ahead. Looking beyond COVID,

digitization of the economy.

Canada has to reverse two trends that pre-dated the

pandemic, and that, left unchecked, will be adverse On climate, Canada must not only pursue

to our wealth and prosperity. domestic emission targets, it must seek sources of

competitive advantage as the global energy system

The first trend is declining productive investment as

and economy drive toward lower and ultimately

a share of our economy, which has been significant

net-zero emissions. This includes decarbonization

since the global financial crisis. The second trend,

of our oil and gas industry in a manner that

in part the natural consequence of the first, but also

realizes the value of our resources, and that creates

longstanding and the result of many factors, is a

opportunities for future exports of energy solutions.

gradual erosion of our position in global markets.

Similarly, our motor vehicle and parts industry must

Spring 2021 Economic Outlook 4

situate its future in global supply chains for smart, The global trading system is at a critical juncture.

clean vehicles. Our approach to climate can fit in a The pandemic has highlighted the fragile state of

commitment to take the initiative on ESG, thus also global supply chains and a need to make them more

addressing the evolving expectations of investors resilient. The World Trade Organization (WTO) is

and consumers. struggling to restore both its negotiation and dispute

settlement functions. The Biden administration’s

Similarly, our economy must take the full measure trade policy is still in its formative stages. Canada’s

of the impact of digitization across the economy, major partners—from China to the United

and the value of technology platforms and data for Kingdom—are all grappling with how to manage

the generation of wealth and prosperity. The digital their trade agenda in this evolving context.

economy and its winner-take-all forces require that

there be concerted effort through competition, As the rules of global trade are negotiated, our

investment, intellectual property and data businesses not only have to adapt their business

management policy frameworks to create the space strategies and investment plans for greatest

for Canada-based firms to emerge, grow and capture advantage, they have to engage with governments in

global market share. shaping our trade agenda. At this time, priorities for

Canada include the continued implementation of the

Canada-United States-Mexico Agreement (CUSMA),

Positioning Canada Globally and Managing

reform in the WTO for a well functioning multilateral

Our Trade Relationships trading environment and the diversification of our

A growth strategy will be informed by, and then trade to take advantage of new growth opportunities,

help guide, our relationships with key global geographically and sectorally.

economic partners.

Expanded investment and improved global trade

Despite many challenges, and irritants past, present could help drive long-term growth and ensure, well

and future, there remains no relationship more beyond COVID, and beyond what is now a strong

important to Canada than the one with the United recovery, rising incomes, improved balance sheets

States, and no economic, policy and business for governments, businesses and households and

signals more germane for us than those that come better standards of living for Canadians.

from south of our border. In its first months, the

Biden administration has put in motion ambitious

plans that create a new and evolving context for

Canadian governments and businesses on a least

five fronts: the macroeconomy, competitiveness,

taxation, climate, and international relations. On

each of these fronts, there are opportunities for

Canada, some potential hazards, and areas for

cooperation. Managing the relationship productively,

including on trade, will not be easy, but it is a sine

qua non for any growth strategy.

bennettjones.com

Executive Summary Spring 2021 Economic Outlook 6

I. Introduction: Light at the End of the Tunnel,

Still a Long Road Ahead

Over One Year Into the Pandemic: New virus variants and successive waves of the

Better Than Expected Economic Outcomes pandemic, affecting different countries and regions

with variable intensity, have required prolonged

At this time one year ago, Canada and the world

lockdowns, and more doses of fiscal aids than

were coping with a first wave of COVID-19

hoped. In Canada, uneven and uncertain public

infections, and public health and economic

health responses in a federal system have also sent

prospects were highly uncertain. Our Spring 2020

mixed signals to economic agents and complicated

Economic Outlook set out a path for the Canadian

the reopening of important sectors of the economy.

economy in three steps: reopening, recovering and

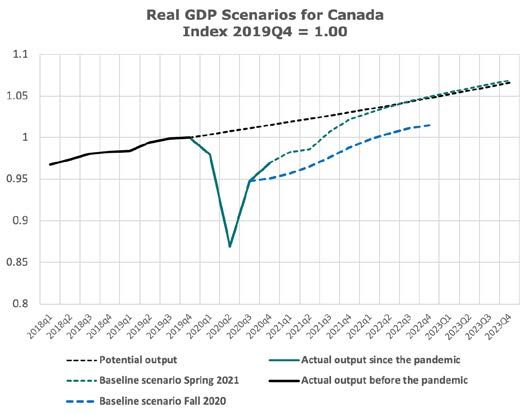

rebuilding. The recovery has nevertheless been solid, and

a return to pre-COVID output in Canada is now

• Reopening was about prudently lifting

projected to occur as early as the third quarter of

economic restrictions by stepping up testing

2021. Employment is also recovering steadily, with

and contact tracing, providing personal

a normal lag relative to the level of activity. The

protective equipment, securing the workplace,

massive aids to individuals and businesses, the

containing new outbreaks, and preventing new

capacity of the private sector to adapt to evolving

waves of infection.

public health guidelines and the earlier than

• Recovering was about getting the economy projected, effective vaccine distribution have largely

back to its pre-pandemic level of activity while offset the effects of a prolonged pandemic.

tapering the exceptional fiscal aids introduced

in the first months of the pandemic for workers Indeed, as discussed in chapter 2, the short-term

and businesses. prospects are positive. The continued roll out of the

vaccines, with at least one dose already delivered to

• Rebuilding was about preparing the ground for

a large proportion of adult Canadians, and second

growth in the post-pandemic world, taking into

doses now being distributed, is a shot in the arm

account global structural trends, including those

of the economy. Importantly, Canada should be

such as digitization of the economy that had

able to ride on the coattails of a strong recovery in

been accentuated and accelerated through

the United States, itself enabled by fast vaccination

the crisis.

and by successive, exceptional fiscal stimulus

Our baseline scenario last June projected that under packages. Indeed, the U.S. economy is giving a

an orderly reopening, with a vaccine assumed to considerable boost to global growth. An added

be available for wide distribution by mid-2021, the benefit of strengthened U.S. (and Chinese) demand

Canadian and other advanced economies would is a strong pick up in commodity prices. Oil prices,

return to their pre-COVID level of output roughly by now exceeding US$70 per barrel for West Texas

the end of 2021. Intermediate (WTI), are supplying much needed

oxygen to our energy industry. Our minerals, forest

The reopening of the economy, globally and in

products, and agricultural sectors are benefiting,

Canada, has proven more bumpy than hoped.

bennettjones.comChapter I

with some offset for other exporters through the public health measures, including at our borders,

resulting higher exchange rate. Strong momentum in are necessary to contain the pandemic durably.

the recovery across a range of sectors provides that Indeed, no solution will be definitive until there is

by the end of 2022, aggregate output not only will wider global success in managing and hopefully

have recovered losses from the crisis, it may be back eradicating COVID-19. As the recovery builds,

on the trendline that preceded the pandemic. notably in the United States with continued strong

fiscal support, there is already evident tightness in

With governments and businesses focused on supply chains, pressure on costs and prices, and

reopening and recovering, there has been lesser some concern that an accommodating Federal

attention to date on the rebuilding of our economy Reserve could react too slowly to prevent more

post-COVID and to the pursuit of long-term growth. durable inflationary pressures to set in. This could

Indeed, in the Budget it tabled in April, the push up market interest rates in the United States

Government of Canada largely focused on and globally, raising costs for borrowers and

consolidating the recovery and securing the incomes potentially also disrupting capital markets. For

of Canadians through to the end of the crisis. It Canada’s federal and provincial governments, higher

extended exceptional aids for workers and firms to debt costs than now built into budget plans could

September, and front-end loaded budgetary actions exacerbate already difficult fiscal challenges. Indeed,

across a wide range of initiatives. Measures were as explained in chapter 2, the large accumulated

for the most part incremental. There was no signal public debt and ongoing expenditure pressures for

of major structural policy initiatives, or launch of federal and provincial governments pose significant

consultations thereon. The one exception, discussed risks for long-term fiscal sustainability.

in chapter 3, was a large new commitment for a

Canada-wide early learning and child care system A Key Vulnerability: Declining Productive

to be cost shared with the provinces, and thus Investment and Loss of Global Market Share

requiring further discussion.

After a period of crisis, it is sensible to wish for the

Medium term, the Budget projected a return to more economy to get back to normal, and for businesses

normal economic and fiscal conditions. Real and and workers to enjoy a greater measure of stability,

nominal growth would trend down to annual rates predictability, and security.

of 1.8% and 3.8%, respectively, by 2025, at or closer

to potential and consistent with an inflation target of However, there is no comfortable steady state ahead.

2%. By 2025-26, the deficit to GDP would be 1.1%, Looking beyond COVID to rebuild the economy for

lower than 1.7% in 2019-20. The most material policy the medium to long term, Canada has to reverse

legacy of the crisis would be the larger federal net two trends that pre-dated the pandemic and that,

debt, at 49.2% of GDP, 18 percentage points higher left unchecked, will be adverse to our wealth and

than pre-pandemic. However, even with allowance prosperity.

for a modest rise in interest rates, federal debt The first trend is declining productive investment

charges would be only slightly higher in percentage as a share of our economy. It is striking that in

of GDP in 2025-26 (1.4%) than pre-COVID (1.1%). the aftermath of the Global Financial Crisis of

This scenario for the medium term may be 2008-09, when oil prices came off their historical

reassuring, but there are considerable risks. peak, and even more dramatically after mid-2014

Immediately, sustained vaccination and effective when oil prices again dropped precipitously, and

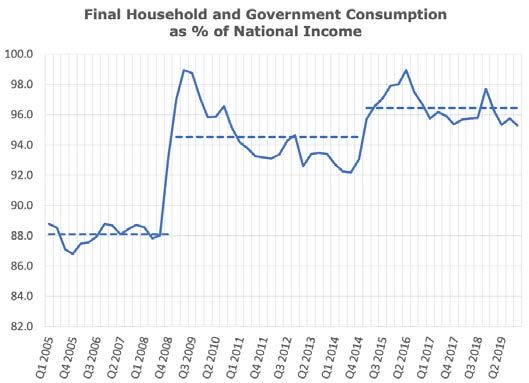

Spring 2021 Economic Outlook 8durably, government and household consumption and the accumulation of mortgage debt increase

became a larger share of our GDP, at the expense the risk to the economy and the financial system

of investment. The same shift is observed in the over the medium term.1 With interest rates kept

course of the pandemic, with again a sharp drop low to support the recovery, other policy tools like

in commodity prices (now more than reversed), a rules for mortgage insurance, or prudential rules

pause in investment across a wide range of sectors, for mortgage origination, are required to moderate

and a relative shift to government consumption and the market. The May 2021 announcement, made

to housing. The federal Budget did not contribute to by the Office of the Superintendent of Financial

correcting this bias to consumption, with the larger Institutions, of the changes to the minimum

share of the $100 billion+ of new actions allocated qualifying rate for uninsured mortgages may be

to supporting income and consumption. Unless helpful. Medium term, the supply side will need

investment rebounds strongly after the pandemic, to be aided by more flexible and efficient local

and takes a larger share of our economy, there is regulation. Of course, this may entail again more

a threat to prosperity. Our resources cannot all investment in housing.

be channelled to consumption: we need to build

Chart 2

capacity for tomorrow.

Chart 1

Sources: SOECD Dataset: National Accounts at a Glance.

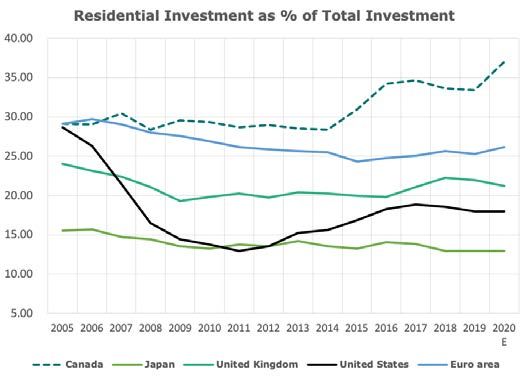

Source: Statistics Canada, Table 36-10-0111-01. Moreover, compared with the United States,

Canada’s non-residential investment has been

The drop in investment is even more worrisome historically heavy on structures (e.g., buildings),

taking into account that, compared with other but lighter on machinery and equipment, software,

advanced economies, Canada allocates a larger research and development and intellectual property

proportion of its total investment to housing. This products that are drivers of productivity in today’s

gap has widened since 2014, and it may again be economy. As we explain in chapter 3, as an economy

accentuating as we come out of the crisis. The we under-invest in training and skills development

housing sector is ebullient across the country as to prepare our workforce for an evolving labour

households seek to take advantage of record low market. We also tend to do poorly, under a complex

mortgage rates to relocate, or to upgrade their architecture of federal and provincial intervention,

residence (and now in many cases their place in measuring the return on public investment in

of work). The Bank of Canada noted in its latest training, and then allocating our effort accordingly.

Financial System Review that the housing boom

bennettjones.comChapter I

The second trend, in part the natural consequence The two trends together, a shift to consumption from

of the first, but also longstanding and the result of investment and a loss of global market share, result

many factors, is a gradual erosion of our position in in larger current account deficits, and therefore,

global markets. A recent report by RBC Economics higher net borrowing from the rest of the world.

captured a set of indicators that are compelling, if Since 2008, Canada has relied on foreign sources of

not alarming:2 capital to fund a deficit in the current account of

2%–4% of GDP, and there is no sign of a turn

• Over the last 20 years, Canada’s exports have around in our performance.

grown at just half the pace of the overall

economy—continuing that performance, versus A deficit in the current account would not be

growing exports 50% faster than the overall problematic if it were caused by a surge of

economy as a goal, would represent a loss of investment that would in part be financed by foreign

exports of $1 trillion by 2030. savings; it is another matter when the foreign

• Despite the growth of Asia, and despite calls borrowing is consistently funding consumption.

from governments and businesses to diversify The Canadian economy, in particular the resource

our exports and to take advantage of new sector, historically has attracted foreign capital

trade agreements, the United States is still the that was allocated on the expectation of a return

destination for close to 75% of our merchandise on productive investment. Over time, a stronger

exports.3 Canadian economy enabled domestic investors in

turn to invest globally and to earn solid returns.

• Yet, our share of the U.S. market is down sharply, Borrowing to finance consumption can work

with China, and more recently Mexico, having through a cycle, but it is not sustainable without

overtaken Canada in exports to the United States. some painful correction elsewhere in the economic

• Accepting that some of this loss of business accounts. Foreign lenders can lose confidence in the

is the effect of a normal process of catch-up value of their Canadian dollar assets. A depreciation

for emerging economies in an open trade of the dollar, and rising interest rates, may be the

environment, it is more concerning still that consequence. This may happen gradually, or it may

Canada is also losing ground to China on happen more abruptly if triggered by any global or

indicators of the sophistication of our exports. domestic event.

It is one thing for Canada to lose out to lower-cost Thus, Canada has surfed over the last decade by

economies on commoditized goods or services, it borrowing to sustain its consumption, and in very

is another to be outranked by them on value-added concrete terms this has been exacerbated—perhaps

goods, and in industries that rely on a high intensity inevitably—during the pandemic. Against this

of innovation and research and development. Yet, backdrop, the scenario in Budget 2021 of a return to

that is what the analysis reveals. As we explain in an economic and fiscal normal is at best incomplete

chapter 5, Canada has done a good job overall of for the medium term, at worst illusory. Governments

negotiating trade agreements with most of our and businesses have to step back from the crisis,

major economic partners, but sustained public and take a hard look at structural trends and

and private sector effort has to go into turning challenges.

agreements into greater, more diversified and

more value-added trade.

Spring 2021 Economic Outlook 10The Key Item of Unfinished Business: A strategy can address how governments and

A Growth Strategy businesses together may facilitate and accelerate

the investments necessary to transform our energy

Thus, it is a priority for Canada to allocate a larger

system, digitize our economy, grow our productivity,

share of economic activity to investment in the

and capture market share. This will include public

factors of production—physical, human, and

investment in infrastructure, as well as private

intangible capital—that will enable our economy to

investment in tangible and intangible capital. It will

perform better in global markets and to create wealth

comprise policies and investments to grow and to

and prosperity.

diversify our labour force, and to adjust and upgrade

If immediate attention must still be focused on skills. It will set out plans to manage relations with

reducing the human and economic costs of the our key trading partners, bilaterally and multilaterally.

pandemic across the country, the time is right to

Businesses individually, while needing to engage

articulate, and then to execute, a strategy to realize

in the conversation, cannot wait for a national

this shift for the medium to long term. With reports

strategy—standing still is a sure way to stagnation

and advice already received from many sources, the

and decline. While in some cases tending to balance

federal government has to step up by working with

sheets damaged by the crisis, they are moving

provinces and business leaders.

forward with investments, driven by market signals

As we explain in chapter 4, a growth strategy is not and founded on careful risk assessments to innovate

old-style industrial policy with heavy intervention and to position their firm for future growth. For

and spending by government in every sector of the example, energy businesses are investing in projects

economy. It is the contours of a plan that builds on that will decarbonize their operations, strengthen

Canada’s resources and strengths, that responds to their ESG performance, and create new platforms for

global forces, and that identifies the combination growth. In doing so, they can engage governments

of policy and investments that can position Canada on the obstacles to lift and the gaps to close to

for success. The activist agenda of the Biden expand and accelerate those plans. A growth

administration, the challenges it poses for Canada strategy may then be informed and shaped by

and the opportunities it opens up, underscore the concrete projects.

need for a strategy that takes account of global

change.

bennettjones.comChapter I

This outlook underscores the need, as the recovery • Chapter 4 sets out key considerations for the

is now well underway, for governments and articulation of a growth strategy for Canada

businesses, aided by a strategy, to look beyond and the promotion of investment, including a

the pandemic, to invest and to pursue long-term necessary positioning relative to the policies and

improvement in our competitiveness, productivity, plans of the Biden administration, and responses

and standard of living. to key global trends and pressures.

• Chapter 2 sets out economic projections for • Chapter 5 analyzes the global trade environment

advanced economies and for Canada over the and how Canada may advance trade relationships

next two years, along with some analysis of bilaterally and multilaterally to bolster its trade

the monetary and fiscal policy frameworks that and to support investment.

will affect interest rates, public expenditure,

taxation and the investment climate. The analysis

supports a proposed set of assumptions to guide

businesses in their planning.

• Chapter 3 drills down on the impact of the

pandemic on jobs, the planned tapering of

emergency supports for workers and employers

and major policy initiatives that may impact the

labour market through the recovery and beyond.

Spring 2021 Economic Outlook 12II. The Outlook to the End of 2023:

A Strong Recovery

While economic recovery from the pandemic to date, Overall, buoyant growth of demand for goods in the

internationally and in Canada, has been uneven and United States and China has stimulated demand

bumpy, a large share of output and jobs has been for industrial inputs and pushed up the prices of

regained, and the near-term prospects are strong. commodities. The WTI oil price climbed from $41

per barrel in November 2020 to $65 in May. Over the

The Global Economy same period, copper prices rose 44%, and lumber

prices more than doubled, both to record levels.

Recent Developments In May 2021, the Bank of Canada’s non-energy

The economic impacts of the pandemic, and commodity price index in U.S. dollars reached its

the pace of recovery to date, have been uneven highest level in 50 years. Strong final demand and

internationally: in the first quarter of 2021, output tightness in supply also resulted in sharp rises in the

in the United States was 0.9% below its level of prices of some intermediate inputs, from shipping to

the fourth quarter of 2019; the gap was 1.8% in semi-conductors.

Japan, and 5.5% in the euro area; in China, output Marked increases in U.S. headline year-to-year

in the first quarter of this year already exceeded its inflation in March, April and May reflected the

pre-pandemic level by 6.9%. The pattern of growth collapse of prices a year earlier, as well as faster

since last fall has varied greatly across economies, month-to-month increases in prices. In the United

depending mostly on the local evolution of the States, the all-items CPI increased 5.0% in May on

pandemic, the capacity to grow in the face of health- a year-on-year basis, and 0.6% from April to May on

related impediments to activity, and the amount of a seasonally-adjusted basis. Base-year effects have

fiscal support. Overall, after last summer’s strong been fairly widespread across product prices, but

rebound of economic activity, on average advanced particularly pronounced for gasoline prices, which

and emerging economies experienced much slower plummeted last year in concert with oil prices. In

growth in the fourth quarter of 2020, and in the April, the core inflation measure preferred by the

first quarter of 2021. Several countries showed Federal Reserve jumped to an unexpectedly high

continued above-trend growth rates over the period, 3.1%, due in part to base-year effects, but also

including Canada, the United States and Korea. due to the impact of supply chain bottlenecks and

Other countries saw their GDP suddenly decline in shortages on monthly price increases for many

the first quarter—Japan, the United Kingdom, and goods and services. Moreover, the annualized

Norway among them. The euro area experienced a growth rate of the employment cost index for wages

two-quarter recession, albeit one shallower than may and salaries of private industry workers rose sharply

have been expected given the severity of lockdown to 4.6% in the first quarter of 2021, from 3.4%

measures to counter the pandemic’s third wave. in the fourth quarter. By contrast, in Europe and

China grew for a fourth quarter in a row in the first Japan, measures of inflation excluding energy and

quarter, although the rate of expansion, at 2.4% at an food remained very weak, consistent with general

annual rate, was well below potential growth. economic slack.

bennettjones.comChapter II

Monetary policy in large advanced economies has In our baseline scenario, on the assumption

continued to be exceptionally accommodative since that the pace of vaccination is maintained, if not

the fall. Policy rates have remained near zero (United accelerated, we expect the recovery in advanced

States) or below zero (Europe and Japan), and economies to shift into higher gear in the second

quantitative easing (QE) programs have been kept half of 2021, before easing gradually during the next

largely intact. In fact, a broad indicator of financial two years. With a continuously rising proportion

conditions in the United States shows a fairly steady of the population immunized during the second

easing between mid-October and mid-May, implying half of 2021, local transmission falls to increasingly

that policy has become more supportive of short- low levels. This boosts confidence and stimulates

term growth.4 economic activity.

Similarly, and throughout the world, fiscal policy The projected robust growth in global demand,

has remained very supportive of economic activity. alongside a slow response of supply, will support

This was most evident in the United States, notably elevated commodity prices, and push up input

with large direct payments to individuals through costs across a range of industries. Oil prices (WTI)

the US$0.9-trillion Coronavirus Response and are expected to remain volatile, evolving in a range

Relief Supplemental Appropriations Act (mostly in of $65–$75 per barrel in the rest of 2021, $55–$65

January), and the US$1.9-trillion American Rescue in 2022, and $50–$60 in 2023. Metals and lumber

Plan Act (in March). In the first quarter, transfers prices should remain very high for the rest of this

to persons boosted disposable income by 13% (at year, before retreating somewhat in 2022 as supply

quarterly rate) and contributed to a strong growth in increases. For at least the remainder of this year,

personal consumption. input costs in the production of final goods and

services are expected to be pushed up by pressures

The strong recovery, and the expected pressure on in the prices of commodities, industrial inputs,

prices, have led to adjustment in market interest construction materials, semi-conductors and

rates. Despite continued large bond purchases, and shipping, as well as by wage pressures in a range of

dovish statements by the Federal Reserve, the U.S. industries, including construction.

10-year bond yield has risen from 0.9% in November,

to 1.6% at the end of May, pushed upward by While there is much uncertainty about how

continued heavy issuance and a rise in market persistent such cost pressures will be, on balance

inflation expectations from 1.7% to 2.4%.5 we expect that they will start to ease by the end of

2021. Core inflation in the United States, however,

should stay well above 2% through the rest of

The Assumptions for the Global Outlook

2021, as the higher costs feed into consumer price

to 2023 inflation. While inflationary pressures from the

While the course of the pandemic remains a key risk, rising cost of industrial inputs should start winding

prospects for advanced economies have brightened down before mid-2022 as supply adjusts, inflation

markedly since last fall. A more positive outlook is will still be significantly above 2% during 2022 and

supported by the gradual deployment of effective beyond. In Europe and Japan, core inflation should

vaccines, the budgeting of additional fiscal support, remain below target to the end of 2023, as persistent

notably in the United States, and the demonstrated economic slack and low inflation expectations hold

capacity of economies to grow despite health-related down the pace of price increases.

impediments to activity.

Spring 2021 Economic Outlook 14While policy interest rates likely will remain at their economies are set to wind down progressively over

current zero or negative levels in Europe and Japan, the next 12 months. However, the overall fiscal

the Federal Reserve may start raising the Federal track will be one of gradual adjustment. General

Reserve funds rate before the end of 2022 in order to government deficits as a percentage of GDP are

prevent the economy from overheating and inflation projected to decline in advanced economies from

expectations from diverging from the inflation 11.7% in 2020, to 10.4% in 2021, 4.6% in 2022

target. The Federal Reserve has been holding the and 3.2% in 2023 (they were equivalent to 2.9% in

view that before tightening monetary policy it would 2019 before the pandemic). In the United States,

be appropriate that the economy be at “maximum under current legislation, the general government

employment” and inflation moderately above 2% for deficit is projected to barely contract in 2021,

some time, in accordance with their average inflation from 15.8% of GDP to 15%, then to fall to 6.1% in

targeting (see U.S. Monetary Policy Framework and 2022, and to 4.6% in 2023, compared with 5.7%

Its Implications). We think that if inflation were in 2019. Note that the IMF estimates ignore the

to greatly exceed the 2% target by mid-2022, as Biden administration’s plans for US$4 trillion of

could happen under our current outlook, instead infrastructure and social spending over the next

of stabilizing at levels slightly above 2%, the decade, to be funded at least in part by tax increases.

Federal Reserve would likely start increasing the These proposals have yet to be passed in Congress.

Federal Reserve funds rate before the end of 2022.

At 0.25%, the U.S. policy rate currently stands Still, the reduction of fiscal deficits will slow down

some 2 percentage points below the long-run level GDP growth, especially in 2022, even as household

considered appropriate by the Federal Reserve, the consumption and business investment increase at

so-called neutral rate that keeps the economy in solid paces. For some countries an increase in net

balance and inflation on target. exports will also support growth, but inevitably other

countries will experience a drag on growth from a

Over our projection horizon, the expected decrease in net exports (as rising domestic demand

normalization of monetary policy, including the also stimulates imports).

scaling down of quantitative easing, and continued

large volumes of debt issuance by the U.S. The Baseline Scenario for the Global

government should push longer-term U.S. interest

rates up, probably to around 2.5% by the end of 2023 Economy to 2023

for 10-year Treasuries. On the basis of the foregoing assumptions, in our

baseline scenario world output, after falling by 3.3%

Governments in advanced economies are expected in 2020, rebounds by 5.8% in 2021; it then grows by

to provide declining, but still substantial, fiscal 4.4% in 2022, and 3.3% in 2023 (Table 1).

support to economic activity. Based on projections

from the International Monetary Fund (IMF), which

in part reflect announced fiscal plans for the near

term, emergency fiscal measures in advanced

bennettjones.comChapter II

Table 1

SHORT-TERM PROSPECTS FOR OUTPUT GROWTH (%)

2020 Share (%)1 2019 2020 2021 2022 2023

Canada 1.4 1.9 (1.7) -5.3 (-5.7) 6.2 (3.6) 4.1 (3.7) 2.1

United States 15.9 2.2 (2.2) -3.5 (-3.6) 6.9 (3.6) 4.0 (3.3) 1.9

Euro Area 12.0 1.3 (1.3) -6.7 (-7.2) 4.2 (3.8) 4.4 (4.0) 1.9

Japan 4.0 0.0 (0.7) -4.7 (-5.4) 2.5 (2.7) 2.4 (2.2) 1.0

Other Advanced Economies 9.1 1.7 (1.7) -4.0 (-5.7) 4.6 (4.4) 3.8(3.1) 2.4

All Advanced Economies 42.5 1.6 (1.6) -4.7 (-5.3) 5.2 (3.8) 3.9 (3.3) 1.9

China 18.3 5.8 (6.1) 2.3 (2.0) 8.4 (8.1) 5.6 (5.6) 5.4

India 6.8 4.0 (4.2) -8.0 (-10.3) 9.0 (8.8) 8.0 (8.0) 6.8

Other Emerging &

32.4 2.4 (2.3) -3.6 (-4.2) 4.5 (4.5) 3.5 (4.0) 3.2

Developing Economies

World 100.0 2.8 (2.8) -3.3 (-4.2) 5.8 (5.1) 4.4 (4.3) 3.3

*Figures in brackets are from the Bennett Jones Fall 2020 Outlook

1

Shares of world output are on a purchasing-power-parity basis. Source: IMF, World Economic Outlook, April 2021.

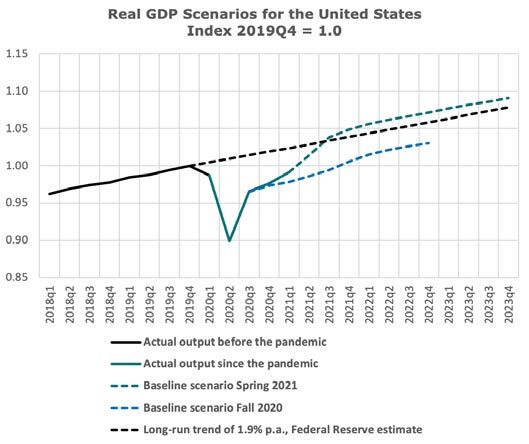

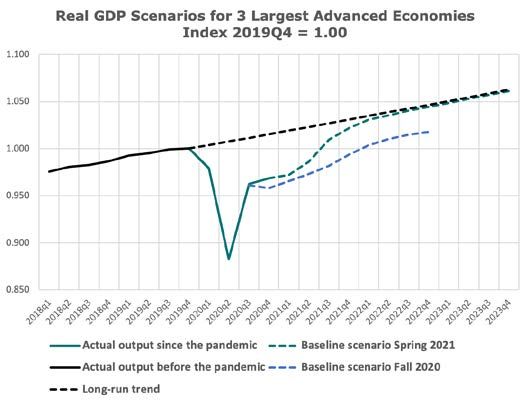

Spring 2021 Economic Outlook 16Projected growth in the advanced economies is and above its long-run trend by the third quarter.

markedly stronger than last fall, with output set to The economy then moves toward a situation

return to its pre-pandemic level by the third quarter of “maximum employment,” keeping inflation

of 2021, and back to its pre-pandemic trend level by significantly above 2% during 2022 and beyond

the end of 2022. After a drop of 4.7% in 2020, real (Chart 4).

GDP is projected to grow by 5.2% in 2021, 3.9% in

2022 and 1.9% in 2023. This is a much-improved Chart 4

track compared to that projected last fall when the

economies of the United States, Japan, and Europe

appeared to be on a course to recover lost output

only by the first quarter of 2022, and then by the

end of that year to still be 2.7% short of returning to

the pre-pandemic trend (Chart 3). A stronger U.S.

economy, aided by larger fiscal stimulus and faster

roll out of vaccines that we assumed last fall, largely

explains the improvement in the prospects for the

advanced economies.

Chart 3

The buoyant growth projected for the United States

during 2021 stems from a fast rollout of vaccines and

from the exceptionally large fiscal stimulus which

is now legislated, while financial conditions remain

very supportive. These factors buttress the recovery

by strengthening activity, income, and confidence.

Households are expected to draw down their large

savings, or at least reduce their relatively high saving

rate, in order to increase spending. Businesses

are also projected to increase investment, driven

After a drop of 3.5% in 2020, real GDP in the United by domestic consumption, rising global demand,

States is rebounding strongly, with a projected improved confidence, a drive to adopt both digital

growth of 6.9% in 2021, slowing to 4.0% in 2022, and clean technologies and the need in some firms

and 1.9% in 2023. On a fourth quarter to fourth to alleviate capacity constraints. Real net imports,

quarter basis, U.S. growth reaches 7.4% in 2021, on the other hand, make a negative contribution to

2.2% in 2022, and 1.8% in 2023, such that at the growth in 2021, given stronger aggregate demand

end of 2023 output is 9.1% higher than at the end growth in the United States than in its trading

of 2019. On this track, real GDP grows above its partners.

pre-pandemic level in the second quarter of 2021

bennettjones.comChapter II

Growth slows during 2022 and 2023 as pent-up projected global recovery will support yet stronger

demand by households tapers off, the general export growth, while household consumption and

government deficit narrows considerably, financial private investment are expected to make a stronger

conditions become somewhat less easy and contribution to growth. The IMF’s Fiscal Monitor of

pressures on capacity increase. April 2021 notes that after bringing the pandemic

under control, China’s fiscal policy has shifted to

The strong performance of the U.S. economy in our broader demand support. Correspondingly, the IMF

projection does not depend on any stimulative effect projects China’s large fiscal deficit to narrow only

from the administration’s proposed US$2.3-trillion very gradually, as a percentage of GDP, through

infrastructure plan and US$1.8-trillion family plan to 2023.

that have yet to be passed in Congress.

There is wide variation, and greater uncertainty,

In the euro area, the drop of output in 2020 was in projections for other emerging and developing

severe, at 6.7%, and the recovery will be more economies. Once the current high incidence

protracted than in other advanced economies. of COVID-19 is brought under control, these

We project growth of 4.2% in 2021, 4.4% in 2022, economies should recover, aided by the pick-up of

and 1.9% in 2023, with output exceeding its pre- global demand and high prices for commodities.

pandemic level by the first quarter of 2022. With This being said, the strength of the recovery in India

more rapid progress in vaccination, increasing and Latin America in 2021 is very uncertain given the

confidence and faster global growth, the recovery will evolution of the pandemic. For many other emerging

accelerate in the second half of 2021. Consumption and developing economies, the recovery remains

spending will make an important contribution precarious because of limitations in the ability of

to growth in 2021, as will net exports, partly in governments to contain the virus, slower access to

consequence of large U.S. and Chinese demand. vaccines, sub-par health systems for treatment of the

The pace of growth will slow during 2022 and 2023, illness, dependence on tourism and remittances and

but it will still be well above the longer-run trend. At lesser capacity for fiscal support.

the end of 2023, output would be 4% higher than

at the end of 2019, but still short of its longer-run

trend level. Fiscal and monetary policies are likely Risks to the Global Outlook

to remain quite accommodative. Fiscal assistance The evolution of the pandemic continues to

has been extended by the European Commission to represent the predominant risk to the global outlook.

counter the severe infection outbreaks that have hit In the last six months or so, despite new waves of

the eurozone this year. It will be supplemented over contagion in advanced economies, surprises on

the next five years by substantial amounts of grants the economic front have been on the upside. Such

and loans from the European Union (EU) recovery demonstrations of economic resilience could happen

fund, known as Next Generation EU. again. The downside risk remains, however, that the

pandemic proves more severe and more persistent

China’s prospects remain substantially the same

than anticipated given the predominance of variants

as last fall, with growth of 2.3% in 2020, 8.4%

of the virus in future contagion, and the uncertain

in 2021, 5.6% in 2022, and 5.4% in 2023. By the

effectiveness of the existing vaccines against

end of 2023, output will be an extraordinary 23%

these variants.

higher than at the end of 2019. Exports of goods,

notably medical equipment and electronic products,

buttressed growth in 2020. Going forward, the

Spring 2021 Economic Outlook 18Another downside economic risk is that U.S. core Beyond uncertainty about the pace of expansion

inflation rises more and for longer than anticipated over the short term, there is a high degree of

because of more persistent cost pressures and/ “structural” uncertainty—how longer-term trends

or overheating of the economy. This could lead to will affect global economic activity. The pandemic

higher interest rates, and slower than projected has intensified and accelerated the response to

growth later in 2022. such forces as climate change and technological

innovation, while also exacerbating pressure

Indeed, there is a serious debate underway regarding for changes in domestic policy, rules and global

the prospects that trend inflation could be higher in arrangements for international trade, investment,

the medium term than has been experienced in the and tax policy. Such changes not only create upside

last two decades of generally below-target inflation and downside risk for the global economy, they can

in advanced economies. First, demographics, affect economies differentially, and thus affect the

in particular population aging, will tend to slow distribution of activity and wealth across countries.

labour force growth and hence aggregate supply.

Some retreat of globalization would also have a

negative effect on supply. Second, fiscal authorities

may continue after the pandemic to pursue more

expansive policy than during the decade before

the pandemic, thereby providing more support to

aggregate demand than used to be the case. As a

result of these adjustments to supply and demand,

upward price pressures may turn out to be more

intense than in the last two decades and inflation to

evolve more in line with, or above, target.

bennettjones.comChapter II

U.S. Monetary Policy Framework and Personal Consumption Expenditure (PCE) deflator.” The

Its Implications employment objective was less precisely formulated

“to minimize deviations of employment from the

The future course of interest rates and inflation

maximum level that could be sustained given non-

depends on two sets of factors:

monetary factors.”

• the structural trends (demography, productivity)

In August 2020, after many years of consistently

and the policies of governments which influence

under achieving its 2% inflation target (even though

the balance between aggregate supply and

for much of the time the key policy rate was near,

demand in the real economy; and

or at, its effective zero lower bound) the Federal

• the monetary policies carried out by central Reserve introduced a policy of “flexible average

banks as they anticipate, or react to, the excess inflation targeting” designed to achieve “inflation

or deficiency in aggregate demand relative that averages 2% over time” without tying the Federal

to supply. Reserve to “any particular mathematical formula that

Our projections of real GDP in this outlook largely defines the coverage.” The concept of “maximum

depend on the first category of factors, while our employment” was redefined as one in which

projections for nominal GDP, inflation and interest employment is “a broad based and inclusive goal”;

rates largely depend on how we expect central banks its assessment would be based on “shortfalls” not

will apply their monetary policy tools to manage “deviations” from its maximum level.6

nominal interest rates.

Under its new policy of flexible average inflation

We examine below how the Federal Reserve might targeting, the Federal Reserve will be more tolerant

apply its policy framework in light of the uncertain of inflation being above 2% for some time. The

evolution of the real economy over the next years, Federal Reserve in its June 16, 2021 press release

and hence the implications for the future course of stated that “the [FOMC] Committee will aim to

inflation and interest rates. achieve inflation moderately above 2 percent for

some time so that inflation averages 2 percent over

The U.S. Monetary Policy Framework time and longer‑term inflation expectations remain

well anchored at 2 percent.”

For many years the mandate of the Federal Reserve

has been to manage monetary policy to achieve two This “flexible average inflation target” approach has

key objectives: price stability defined as a reasonably raised fears among a number of market participants

low and stable rate of inflation; and a high and rising and economic analysts that the Fed will not act

level of employment. The Federal Reserve aimed to until the inflation genie is out of the bottle (as was

pursue these goals while keeping interest rates at the case in the 1970s), and that it will then have to

reasonable levels. react harshly (as it did in the early 1980s), resulting

in a very serious economic and financial market

Since 2012, the price stability mandate was refined

correction.

more precisely to “symmetrically target inflation of 2%

by minimizing deviations from 2% as measured by the

Spring 2021 Economic Outlook 20Outlook for Policy and Interest Rates in the second half of this year and the first half of

How is this revised monetary policy framework likely 2022, will likely recede in the second half of 2022.

to impact interest rates over the period to 2023? However, with persisting excess demand in the

economy, it is likely to continue above the 2% target

Many market participants and economists (including during 2023.

those at the Federal Reserve) project strong growth

in the United States through 2021, and to a lesser Against our outlook for the U.S. economy, we think

extent 2022, slowing only somewhat to about that a “data-dependent” Federal Reserve, applying its

potential (1.9% real) in 2023, even without any new framework, and despite its current statements,

additional stimulus from the Biden plans. Were his will begin to taper bond purchases in the first half of

plans to be enacted, there would be an increased 2022, and finally begin to raise the policy rate by the

chance that excess demand and inflation above end of 2022.

2% would continue in 2023 and beyond. Indeed, While the Federal Reserve will look through the

the Federal Reserve in March projected inflation temporary jump in prices this year, as it should, it

rising to 2.1% during 2023 when the unemployment should not ignore inflation continuing above 2%

rate is expected to fall significantly below its full- in 2022. If some portions of the Biden plans for

employment level. With an upward revision to U.S. infrastructure and families are enacted without

growth since then, it is likely that the Federal Reserve commensurate tax increases, we think that inflation

itself would now project significantly higher inflation would rise even further than otherwise in 2023, again

than 2.1% during 2023. forcing the Federal Reserve to raise the policy rate

Hence a number of economists and market and to further taper bond purchases. These views

participants judge that the Federal Reserve will have form the basis for interest rates reflected in our

to move as early as 2022 to raise the policy rate and planning parameters shown at the end of

to taper bond purchases. For this reason, the yield this chapter.

on 10-year Treasuries was bid up from 0.7% last fall, In this context, we note that the Bank of Canada

to a monthly peak of 1.64% in April. very sensibly is continuing with its original flexible

In our view, the U.S. economy will continue to inflation-targeting framework. In the face of a

grow very strongly over the next 18 months, and stronger economic outlook for Canada, it has already

by the second half 2022 and through 2023, it will begun to reduce its weekly purchases of bonds from

be operating above potential. Inflation, which will $4 billion to $3 billion.

temporarily spike above 3% as the economy adjusts

bennettjones.comYou can also read