Energean in 2021: Our Year of Transition The Leading Independent E&P Player in the East Mediterranean

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Energean in 2021: Our Year of Transition The Leading Independent E&P Player in the East Mediterranean

Disclaimer

This presentation contains certain forward-looking statements that are subject to

the usual risk factors and uncertainties associated with the oil and gas exploration

and production business.

Whilst Energean believes the expectations reflected herein to be reasonable

considering the information available to them at this time, the actual outcome may

be materially different owing to factors beyond the Group’s control or within the

Group’s control where, for example, the Group decides on a change of plan or

strategy.

The Group undertakes no obligation to revise any such forward-looking statements

to reflect any changes in the Group’s expectations or any change in

circumstances, events or the Group’s plans and strategy. Accordingly, no reliance

may be placed on the figures contained in such forward-looking statements.

2

Energean – The Largest E&P Company Listed on LSE

& First in the World to Commit to Net Zero Emissions

9 Countries +1 Billion Boe

Of operation 2P reserves &

Med-focused 2C resources*

+200 Kboed +70%

Medium-term Gas-weighted

production target portfolio

Governance Management

Premium listing 30 years

on LSE experience in gas

Net Zero ESG & HSE

Emissions A rating MSCI

Commitment by 2050 Gold by MAALA

* Pro forma as at 31.12.2020. Includes an additional 219 MMboe of 2P reserves to be acquired from Kerogen Capital. Reserves information is unaudited and subject to further

review. 3

2020: Strong Delivery Despite a Challenging Year

Key Milestones Achieved

Strong Delivery Against Strategic Goals Despite COVID-19 Related Challenges

80% Y-o-Y Increase in 2P reserves to 956 MMboe (2019: 341 MMboe)*

Production 48.3 Kboepd (74% gas)

Strong Operational

Performance Karish development 87% Complete at 31 December 2020

Took FID on Karish North (Israel) and NEA / NI (Egypt)

Closed Edison Acquisition – Operational Footprint Expanded to 9 Countries

Continued Agreed to Acquire Kerogen’s 30% Holding in Energean Israel

Commercial Success

Increased signed GSPAs in Israel to 7.4 Bcm/yr

Optimised Capital $437 Million Capex Reduction versus January 2020 guidance

Structure & Strong

Financial Discipline $1.2 Billion Cash & Undrawn Facilities at 31 December 2020**

67% Y-o-Y Reduction in Carbon Intensity to 22.2 kgCO2/boe

Advanced Net Zero

Strategy Roll Out of ‘Green Electricity’ at Prinos in Greece

* Pro forma as at 31.12.2020. Includes an additional 219 MMboe of 2P reserves to be acquired from Kerogen Capital. Reserves information is unaudited and subject to further

review. 5

** Adjusted for the new $700 million term loan that was secured post-balance sheet

Our Transition into the Top Tier of European E&Ps

Moving into the top tier of E&Ps expected to enhance liquidity, valuations & investor attention

1.200 Norwegian Peers LSE-Listed Peers

WI 2P Reserves

1.000

800

(MMboe)

600

400

200

0

Energean Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11

250

WI Production

200

(Kboed)

150

100

50

0

Peer 1 Peer 2 Peer 3 Energean Peer 4 Peer 5 Peer 6 Peer 7 Energean Peer 8 Peer 9 Peer 10

Target Today

Top 5 European E&Ps by scale

6

2021: Our Year of Transition

2021 Guidance and Medium-Term Targets

Substantially Improved Medium-Term Outlook

Through successfully delivering our strategic objectives in 2021 we will achieve our Medium-Term Targets which underpin

our goal of generating sustainable Free Cash Flow and delivering a sustainable dividend

2021 Guidance Medium-Term Targets

Production

(excludes any contribution 35.0 – 40.0 kboed Production

200

Kboed

from Israel) (up from 160))

Cost of Production* $195 – 215 million Revenues

$2,000

Million

(up from $1,400)

Development &

Production Capital $510 – 590 million Cost of Production*

$9 – 11

/ boe

Expenditure Down from 10 -12

Exploration Capital

$35 – 50 million G&A

$25 – 35

Expenditure Million

=

Decommissioning

$25 – 32.5 million EBITDAX $1,400

Expenditure Million

(Up from $900)

Consolidated Net

$2,000 – 2,200 million Net Debt / EBITDAX < 2.0x

Debt

* Operating Costs plus all royalties.

SG&A costs of approximately $35 - 40 million anticipated in 2021 8

Focused on Monetising 1 Billion Barrels of Reserves

to Deliver Production of more than 200 Kboed

W.I. 2P Reserves + 2C Resources 2016-20E* W.I. Hydrocarbon Production 2021+

1.200 250

2016-20E CAGR 45%

Medium-term Target

200 kboe/d

1.000

200

Key growth drivers

800 • Karish & Karish North

150 • Incremental liquids

MMboe

Kboed

600 • Abu Qir infill drilling

• NEA/NI development

100

400

50

200

0 0

2016 2017 2018 2019 2020 2021 Medium-term Target

Israel Egypt Europe Israel Egypt Europe

* Pro forma as at 31.12.2020. Includes an additional 219 MMboe of 2P reserves to be acquired from Kerogen Capital. Reserves information is unaudited and subject to further

review. 9

Revenues Forecast to Reach Over $2 Billion

Growth Underpinned by Gas Sold Under Fixed-price Contracts

Revenue Outlook 2021-25 Revenue Outlook % 2021-25

3% 2%

9% 7% 7%

Medium-term Target

$2 billion

41% 42%

37% 36%

39%

56% 56% 56% 56%

53%

2021 2022 2023 2024 2025 2021 2022 2023 2024 2025

Gas sold under fixed price contracts Gas sold at market prices Gas sold under fixed price contracts Liquids with Brent-linkage

Liquids with Brent-linkage Gas sold at market prices

Based on a Brent price of $50/bbl in 2021, $55/bbl in 2022 and $60/bbl flat real 2023+

10Creating a Sustainable Low-Cost Business

Secured Lower Unit Cost of Production Further Targeted Cost Optimisation Expected

18 • Full, bottom-up internal review initiated

• Operating cost reductions

16

• Third party tariff optimisation

14

• Mothballing

12 Medium-term Target • Production efficiencies, such as gas

$9 - 11 / boe reinjection, to reduce power consumption

10

• Cost driven performance-management

$/boe

8 • Further savings expected and not yet reflected in

forecasts

Medium-term Target

6 $4 - 6 / boe • Karish, Karish North & Tanin operating costs

expected to be $70 – 80 million per year

4

• Approximately $1/boe on plateau (excludes

royalties)

2

• Limited variable costs

0

2021 2022 2023 2024 2025

Unit Operating Costs Unit Operating Costs + Royalties

11Disciplined Capital Allocation Remains a Priority

Development & Production Capex 2021-24 W.I. Capex Allocation 2021-24

600 100%

17% 21%

33%

80%

52%

500

60%

40% 83% 79%

400 67%

48%

20%

$ Million*

300 0%

2021 2022 2023 2024

Greenfield Brownfield

200

Strong ability to reduce capital spend in a

low commodity price environment

100

Investing ~80% of capital expenditure in

greenfield assets in 2021

0

2021 2022 2023 2024 Increasing spend on brownfield assets

Israel Croatia Egypt Italy UK through 2024 to optimise Edison portfolio

* Excludes exploration and appraisal expenditure

12Capital Allocation Prioritising Total Shareholder Return

With Core Focus On Distribution Policy That Underpins Sustainable Dividend

Sustainable Target for inaugural

Dividend

2022 dividend

Organic > 20% 40% IRR Karish North

Growth IRR Project Sanctioned

Capital

Structure < 2x Net debt / EBITDAX target

$1.85/boe acquisition price

Disciplined Value for Kerogen’s 30% holding

M&A Accretive in Energean Israel

13Current Capital Structure

Net Debt Position* Committed Facilities

To be refinanced in 2021

Group net debt: $1,241 million • $1.45bn PFF ($1.15bn drawn)

• $(201) million cash Israel • Extended maturity to September 2022

• $1,442 million debt • Non-recourse to parent

PFF • Interest payments & other project costs covered by

facility

Energean Israel net debt: $1,057 million

• $(37) million cash • $700 million Term Loan

• $1,094 million debt Term • Maturity July 2022

Loan • Primary uses to fund Kerogen acquisition and Karish

North development

Energean PLC excl. Israel net debt: $184 million

• $(164) million cash

• $348 million debt • $280m RBL facility (current borrowing base $237m;

availability expected to increase June 2021) with

Egypt $75m accordion

RBL • LIBOR + 4.75% yrs 1-3 / LIBOR + 5.75% yrs 4-6

• 6-year term, semi-annual redeterminations

Full Year 2021 Guidance • 3-year grace period with first amortisation July 2023

•

$2,000 – 2,200 million Greek •

Outstanding loans as of 31 December $127m

Scheduled principal repayments of $19m per

RBL semester

* Accounting net debt

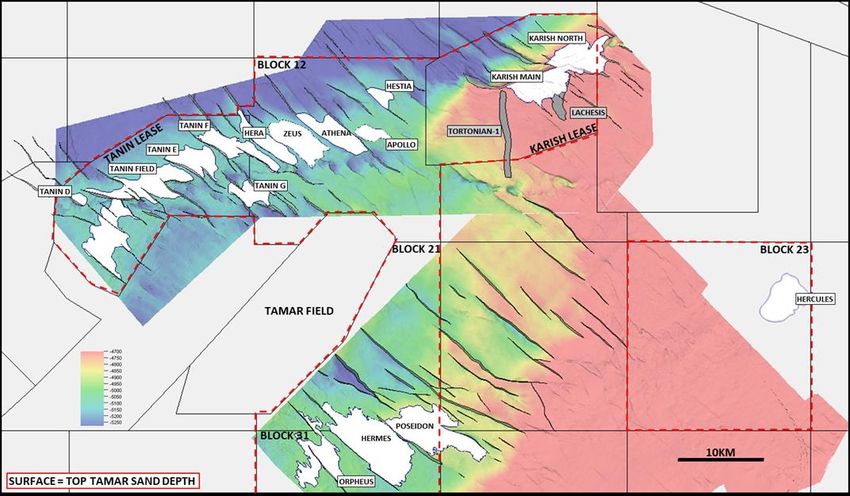

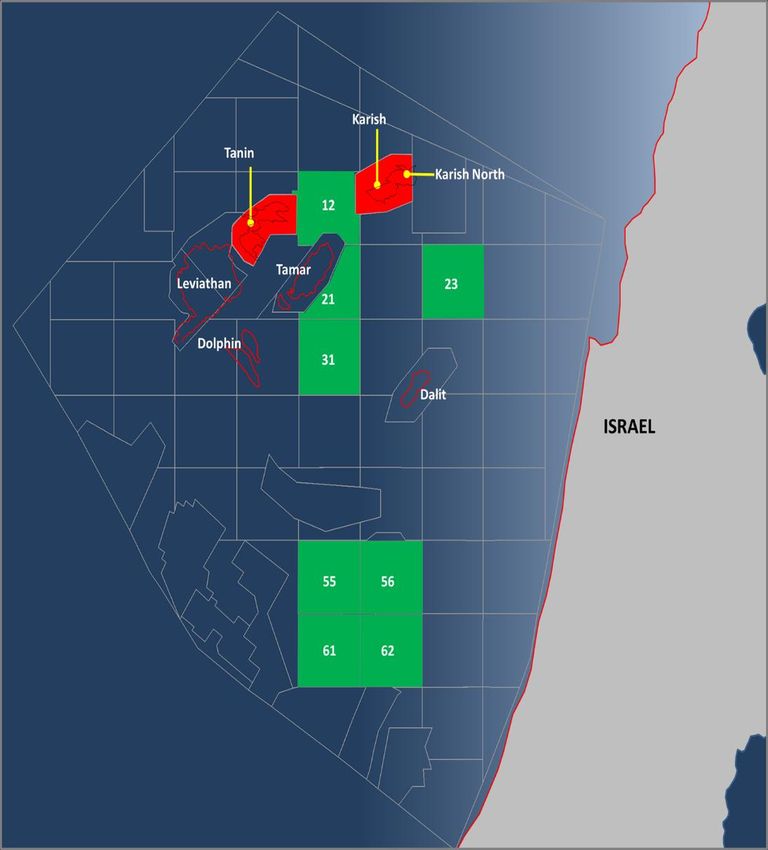

14Project Updates: Israel

Karish Project – First Gas Expected Late 2021

Project Close to 90% Complete Despite COVID-19 Related Challenges in 2020

At 31 Dec 2020

KARISH

FPSO SUBSEA ONSHORE

PROJECT

~93% ~76% *90-100%

complete complete complete ~87%

complete

• Main modules & pipe racks • 14-line mooring system & • Installation of production rate

lifting campaign completed deepwater subsea production measurement system at Dor

3Q 2020 system fully installed commenced Aug 2020

• Final lifts of module-1 & flare • 90-km gas sales pipeline • Mechanical completion & First Gas Dec 2021 –

expected in 1Q 2021 scope close to completion commissioning expected 1Q 1Q 2022 depending on

• Sailaway to Israel expected • Tie-in manifold successfully 2021

in Sept / 4Q 2021 installed Oct 2020 & • Installation of onshore pipeline

further ramp up of

connected to gas sales commenced Jun 2020 & workforce in

pipeline Nov 2020 expected to complete 1Q 2021 Singapore

• Riser installation campaign • Civil works progressing well &

expected to commence & expected to complete 2Q

complete 1Q 2021. 2021.

* 90% inclusive Energean scope of work; 100% under the TechnipFMC EPCIC

16Karish North Sanctioned – First Gas Expected 2H 2023

FID Reached 21-Months After Announcement of 32 Bcm Discovery

Low-Cost High-Return Tieback to FPSO

2P Reserves 241 MMboe (84% Gas)

Initial Capex ~$150 Million

($0.6 / Boe)

300 MMscf/d

Well Deliverability (per well)

Minimal

Operating Costs (Incremental)

IRR +40%

Capex Profile (Including Riser & Oil Train)

200

150

$ Million

First Second

100 Gas Development Well

50

0

2021 2022 2023 2024 2025

Initial Capex Riser + Oil Train

17Focused on Developing & Expanding Liquids Output

Through Committed Investment Programme

• 100 MMbbl 2P liquids certified by DeGolyer & MacNaughton CPR:

Material Reserves • 17.4 MMbbl (21.4%) increase in 2P liquids (light oil) volumes

& Production • 28 kbpd production over a 5-year plateau period

• Further growth targeted from appraisal of potential oil rim in 2022

• Project to install second oil train and riser on Energean Power FPSO sanctioned

• Oil train increases liquids production capacity to 40 kbopd (from 21 kbopd)

Committed & Fully- • Allows maximum gas output of 8 Bcm (from 6.5 Bcm)

Funded

• Approximately $100 million of capex fully funded by new term loan

Infrastructure

• Expected to become operational in 2022

• 800,000 barrels of liquids storage capacity on FPSO

Ample Storage • Storage capacity not a restricting factor to liquids production

Capacity • Additional gas debottlenecking opportunities under evaluation that would allow gas

production above rates of 8 Bcm/yr

• Low carbon barrels added to portfolio

Low Carbon • Liquids production expected to have no discernible impact on Scope 1 & 2 CO2

emissions

Emissions

• Carbon intensity of 4.5 kg CO2/boe anticipated

18Investment Synergies Targeted from Low-Cost

Deepwater Tie-Back Options

Approx. Distance from FPSO 5 km 15-30 km 40-55 km

Karish Karish North Block 12 Tanin

Approximate Life of Field

capex/boe

$6/boe $1.5/boeIsrael – 7.4 Bcm/yr Gas Sales Agreements

Secured Revenues with 93% of Energean Power FPSO Capacity Utilised

Protection

1.8 Bcm/yr new Against

Take-or-Pay / High Quality

GSPAs Signed Floor Pricing Downside

Exclusivity Counterparties

in 2020 Commodity

Price Risk

9

Energean Israel Gas Supply Profile

8

7,4 7,4 7,4 7,4 7,4

7,2 • December 2021 – Karish first gas

7 6,7 6,8

• 2022-23 – Ramp up of 18 contracts

6 signed with independent power

producers (IPPs) including both recently

5 privatised IEC stations, Alon Tavor &

Bcm/yr

4.2*

Ramat Hovav, and blue-chip industrial

4

customers including ORL and ICL

3

• 2024 – Continued ramp up

2

• 2025 – Commencement of IPM contract

1 & continued ramp up of other contracts

0 • 2026 – Plateau gas supply reached

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Karish, Karish North & Tanin Gas Supply

Energean Power FPSO Capacity

* Company estimate during 12-month transition from existing suppliers

204-Well E&A Programme Targeting >1 bn boe

Prospective Resources to Commence Early 2022

Karish North drilled as part of a 5-well programme providing cost synergies

KM 04 + Pilot Hole (PH)

ATHENA 01

A discovery would significantly

de-risk prospects in the rest of

Block 12

Audited

Approx.

Prospect Size

Well Type Cost PoS

(Recoverable)

$ Million

MMboe*

Athena-01 Exploration 35 140 84%

94% +

KM-04 + PH Appraisal 45 176 + 64

72%

Exploration

Hermes-01 40 200 56%

(Optional)

Hercules- Exploration

50 488* Tbc

01** (Optional)

KN-01 ST-

04

Development 50 NA 100% HERMES 01 HERCULES 01

* Recoverable Volume”: is the sum of the unrisked mean recoverable volumes with recovery factor (gas) = 0.7 and recovery factor (oil) = 0.4. This represents the total recoverable

reserves targeted by the well bore 21

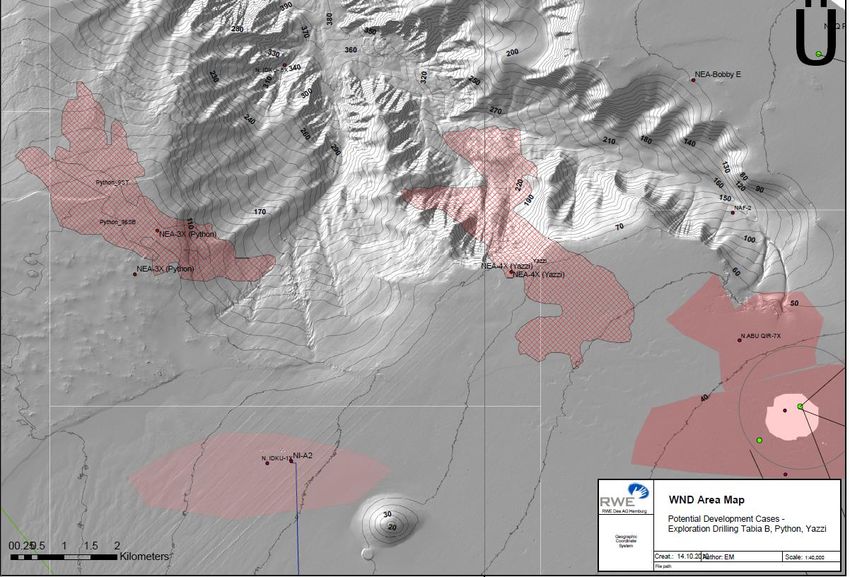

** Not yet audited. Management estimates presentedProject Updates: Egypt

NEA / NI Sanctioned – Monetisation of Well Defined,

High Return Drilling Opportunities

Key Project Metrics

Peak Production 15 – 16 Kboed

2P Reserves 49 MMboe

(87% Gas)

PYTHON

SUBSEA

WELL

CapexProposed Acquisition of Kerogen’s 30% Holding in Energean Israel Limited

Agreed to Acquire Kerogen Capital’s 30% holding in

Energean Israel Limited (EISL) for $380-405 Million

Compliments our gas-weighted portfolio Group 2P+2C to reach +1 billion boe

Energean Acquired assets Pro-forma

• Natural strategic fit that gives full control over capital

14%

structure of EISL 29% 26%

• Adds 219 MMboe 2P reserves (86% gas)

71% 74%

86%

• Group 2P + 2C set to grow to >1 Bnboe (74%

gas)

Gas Liquids

• Attractive transaction metrics

• $1.74 - $1.85 /boe Group production to reach +200 kboed

• 1x forecast Minority EBITDAX 250

• Payback achieved within three years

• 43% discount to EV 200

150

• Full control over EISL enables capital structure Kboed

optimisation 100

• Low carbon intensity hydrocarbons (< 4.5 kg 50

CO2/boe)

0

2021 2022 2023 2024 2025

Energean Acquired Assets

25Transaction Structure & Financing

Part of use of proceeds for Term

Up-Front

$175 Million Payable on completion Loan provided by J.P. Morgan &

Consideration Morgan Stanley

Deferred Cash Contingent on Practical Completion To be funded by optimised capital

$125-150 Million of Karish structure

Consideration

Additional Deferred

$30 Million Payable December 2022 Funded by free cash flows

Consideration

Conversion price £9.50 / 0% coupon

Convertible Loan

$50 Million rate / Maturity 31/12/2023 December Satisfied by new share issuance

Notes 2023

$380-405 Total

Highly accretive to plc leverage ratio

Million Consideration

26Milestones to Completion

Transaction Close Expected 1Q 2021

Timing Milestone

30 Dec 2020 Transaction announcement

Jan / Feb 2021 Israeli Petroleum Commissioner Approval

Feb 2021 Publication of Circular

Feb 2021 EGM & shareholder votes

Feb / Mar 2021 Closing of the Proposed Transaction

27ESG & Our Path to Carbon Neutrality

Creating a Low Carbon Business with Industry-

Leading ESG Credentials

First E&P Company Globally to Commit to

Net Zero Emissions by 2050

Net Zero

Carbon emissions by 2050

Visibility on Absolute Carbon Emissions

Intensity to Half the Current Global Average

Rolling Three-year Emissions Target

30

Current global average

25

+70% Gas-Weighted Portfolio (2P + 2C)

+85% reduction by 2023 versus

20 2019 base year

2023 target = Approx. half the

15 current global average for oil &

gas industry

10

Executive compensation tied to ESG

performance targets from 2020

5

0

2020* 2021 2022 2023 2024 2025

Committed to Transparency & Adherence to

Carbon emissions intensity – kgCO2e/boe the 17 UN SDGs

• Pro forma Energean + Edison

29Prinos – Carbon Capture & Storage Initiatve

Multiple CC&S Opportunities Under Evaluation in Greece

Greece Sources of CO2 Emissions Possible CO2 Storage Sites in Greece

Mesohellenic Western Prinos

Industry Facilities # CO2 Emitted (kt)

Trough Thessaloniki Basin

Energy Sector 21 36,463

Minerals 6 13,422

Production &

Processing of 2 708

Metals

2

Chemicals 490

Total 31 51,083

Prinos CC&S Project Under Evaluation

• Focused on meeting our carbon neutral by 2050 target and

leading the Mediterranean region’s energy transition

• Evaluation of Carbon Capture & Storage projects in the

Prinos basin initiated in late 2020

• Prinos subsurface volumes sufficient to sequester up to 50

million tonnes of CO2

• Use of captured CO2 for enhanced oil recovery (EOR) also

under investigating – to unlock additional upstream value

* Enhanced Oil Recovery

302021: The Outlook

2021-22 Outlook

Continue Strong Performance Versus Strategic Goals & Deliver Our Year of Transition

Deliver First Gas at Karish & Develop Karish North 2021 - 2023

Operational Develop NEA / NI in Egypt 2021 - 2022

Performance

Deliver (up to) 5-well E&A programme, offshore Israel 2022 - 2023

Kerogen Acquisition Close 1Q 2021

Commercial Success Sign GSPAs to fill remaining space in the Karish FPSO 2021

Sign offtake agreement for Karish liquids 2021

Optimise EISL capital structure through refinancing 2021

Optimised Capital

Structure & Strong Define dividend policy 2021

Financial Discipline

Bring net debt / EBITDAX below 2.0x Mid-term

Align with TCFD recommendations 2021

Advanced Net Zero Roll Out of ‘Green Electricity’ across operated assets Ongoing

Strategy

Evaluating converting Prinos into Greece’s first CC&S Project Ongoing

32Q&A

33You can also read