European PV manufacturing - does it make sense? - L. Oberbeck Institut Photovoltaïque d'Île-de-France Total Gas, Renewables and Power

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

European PV manufacturing – does it

make sense?

L. Oberbeck

Institut Photovoltaïque d'Île-de-France

Total Gas, Renewables and Power

May 6, 2021

DFBEW conference, May 6, 2021

TOTAL Classification: Restricted Distribution

TOTAL - All rights reserved

Institut Photovoltaïque d'Île-de-France IPVF

Our ambition Six programmes

Streamline upstream research with a strong industrial

foothold and operate a world-class experimental ❖ Techno-economic and environmental assessment

platform to: ❖ Perovskite on c-Si tandem modules

❖ Radically improve the performances of PV modules ❖ Low-cost III/V on c-Si tandem cells

❖ Develop disruptive PV-based technologies

❖ Advanced characterization & modeling

Founding members ❖ Solar to fuel

❖ PV breakthrough technologies demonstration

A French Institute for Energy Transition

DFBEW conference, May 6, 2021

TOTAL Classification: Restricted Distribution

TOTAL - All rights reserved

Setting the scene (1) – PV markets and manufacturing

• Global cumulative installation ca. 760 GW by end of 2020

• Global installation 2020 ca. 135 GW

• Top 3 markets: China, Europe, US

• Market segments: utility-scale (dominating), industrial & commercial,

residential and specialty markets (floating, integrated PV, …)

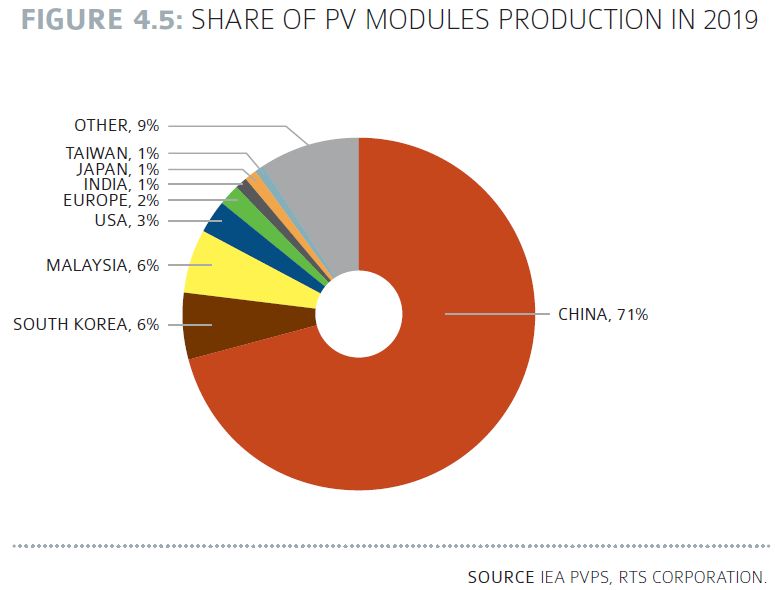

• Production capacity ca. 270 GW

• Production strongly dominated by China

Si wafers Cells Modules

IEA PVPS, 2019

DFBEW conference, May 6, 2021 3

TOTAL Classification: Restricted Distribution

TOTAL - All rights reserved

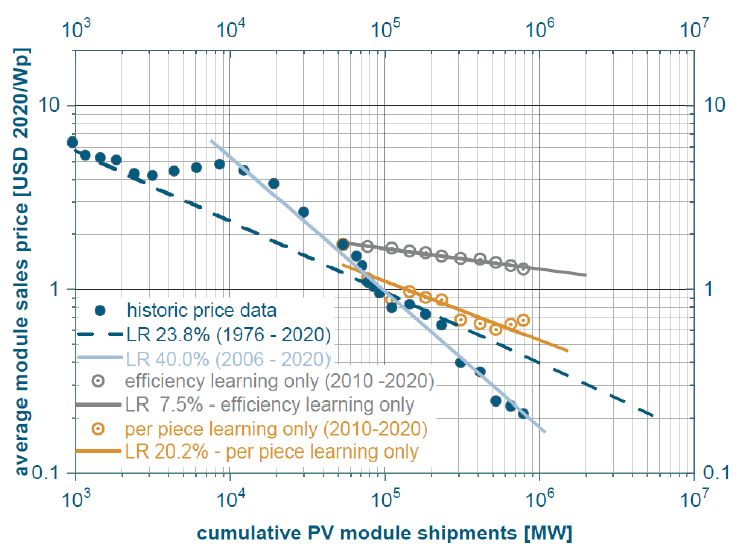

Setting the scene (2) – PV technologies and prices / costs

Thin-film IBC

Graph courtesy of Pietro Altermatt, Chen Yifeng

22.6% Maxeon 5

Multi-Si

Mono-Si

• Market share of crystalline Si PV

technology ca. 93% in 2020

• Current workhorse of PV industry: PERC

(Passivated Emitter and Rear Cell),

module efficiency ca. 20.5% currently

• Module price ca. 20 c$/W

• Module price learning rate 40%

DFBEW conference, May 6, 2021 4

TOTAL Classification: Restricted Distribution

TOTAL - All rights reserved

European markets and manufacturing

Annual installations Annual installations Cumulative installations

Europe Germany and plans France

SolarPowerEurope, 2020

• Cumulative PV installation in Europe ca. 137 GW, annual growth of

13-23% expected

• Cumulative PV installation in Germany ca. 55 GW (largest PV fleet in

Europe), ca. 6 GW installations expected for 2021

• Cumulative PV installation in France ca. 10 GW, ambitious targets of

up to 44 GW by 2028

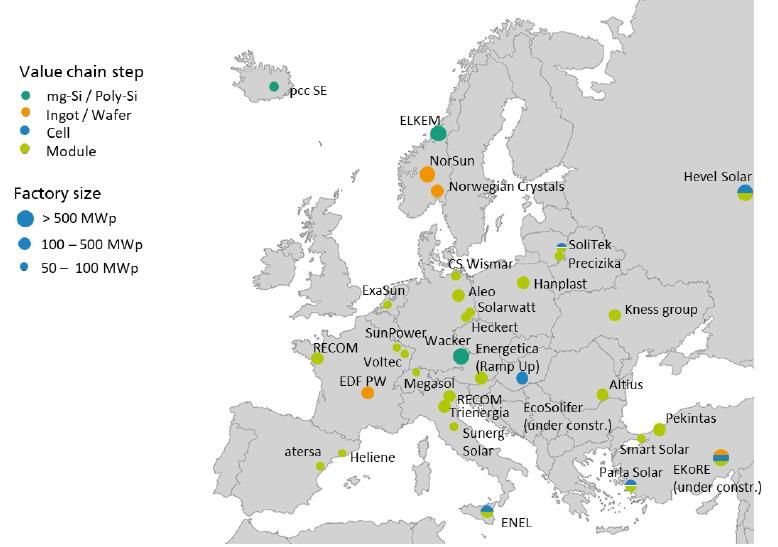

• Current PV production in Europe: mainly small-scale (

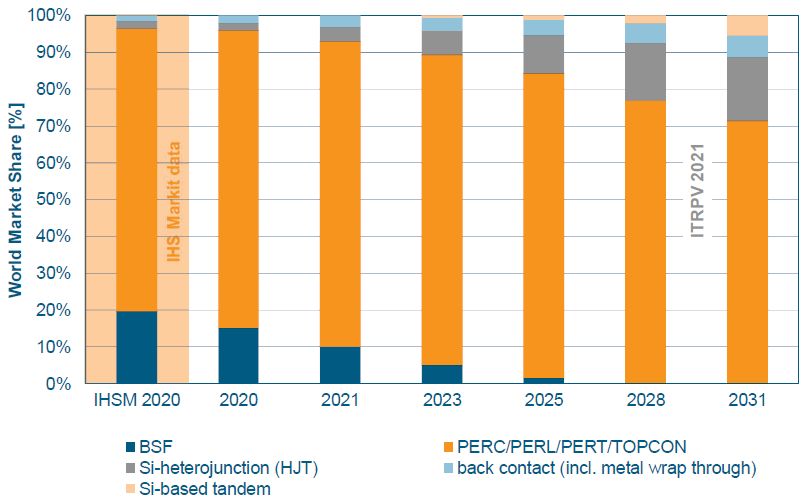

PV technology options for manufacturing in Europe

Expected evolution of market shares of different

solar cell technologies

Five PV technology options for European manufacturing:

• PERC (current standard technology)

• Pathways to higher PV module efficiencies >22%

o Upgrade of existing PERC production lines:

passivated contact technologies (“TOPCon”

Tunnel Oxide Passivated Contact)

o New production lines: silicon heterojunction

Technology comparison (indicative only)

HJT or interdigitated back-contact IBC

PERC TOPCon SHJ / IBC Perovskite / Si

technologies tandem

o Market entry of novel technology expected in

Efficiency

potential • ✓ ✓✓ ✓✓✓

Bifaciality Depending on

2022: perovskite on silicon tandem modules • ✓ ✓✓ / •* Si cell

TempCo

• ✓ ✓✓* ✓✓✓

DFBEW conference, May 6, 2021

Manufact.

cost ✓✓✓ ✓ (?) •* (?) ?

6

*Depending on concrete process flow

TOTAL Classification: Restricted Distribution

TOTAL - All rights reserved

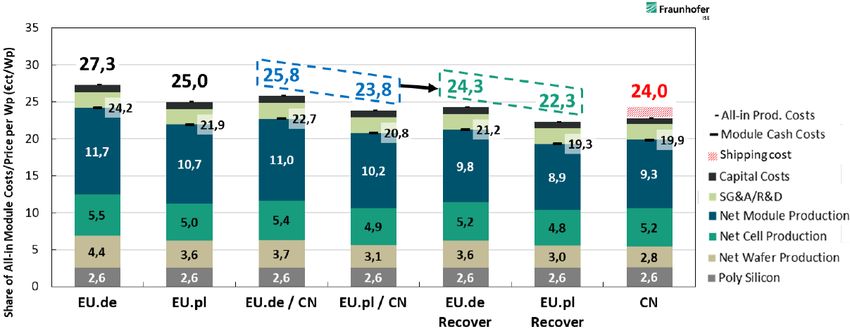

Cost competitiveness of European manufacturing?

PERC 144 half-cells, bifacial module with transparent backsheet and Al frame “Recover”: EU

supply chain at Assumptions for relative differences between EU and

Chinese costs Chinese performance parameters

Competitiveness of a European PV

manufacturing chain, VDMA, 2020

World market share for size of cell production fabs

• VDMA / Fraunhofer ISE study for 1 GW integrated fab (Si ingot to module) finds that PV module

manufacturing in Europe can be competitive if

o transport costs add significantly to the price of imported modules (around 10%)

o European fabs reach sizes of ≥5 GW

o GW-scale supply chain returns to Europe

o environmental impact / CO2 emissions are valued

• However, some assumptions questionable and available supply chain crucial

• Note: size of cell / module fabs is growing, fabs >5 GW becoming standard over next years

• Note also: historically, PV manufacturing is a low-margin business

DFBEW conference, May 6, 2021

7

TOTAL Classification: Restricted Distribution

TOTAL - All rights reserved

Some comments on European manufacturing

✓ Securing PV energy autonomy − European materials supply chain needs to be re-

established

✓ Large and growing European markets available

− Difficult to compete on cost basis

✓ Sustainable production with European energy mix

✓ Creating / securing jobs in Europe, incl. supply chain − Higher quality of manufacturing and product?

− Financing of European fabs

✓ World-leading research institutes

Other considerations:

• PV cell manufacturing in Asia and module manufacturing in Europe?

• Investment in European fabs by Asian PV manufacturers?

DFBEW conference, May 6, 2021

8

TOTAL Classification: Restricted Distribution

TOTAL - All rights reserved

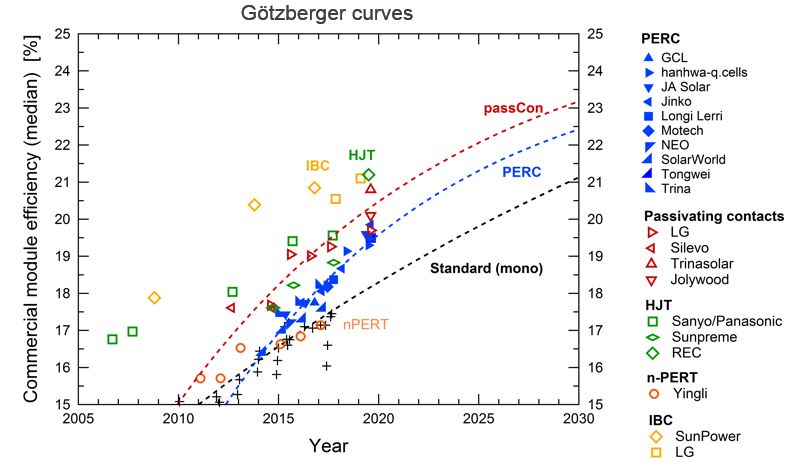

Summary and discussion points

Potential PV module efficiency evolution

• PV manufacturing largely dominated by Chinese companies

W. Hoffmann, A. Metz, EUPVSEC 2019.

• Monocrystalline Si PERC is workhorse of the PV industry, current module efficiencies

ca. 20.5%

• Module prices decrease with learning rate of 40%

• Markets in Europe and world-wide are growing

• European manufacturing mainly small-scale (

Thank you very much for

your attention

lars.oberbeck@total.com

DFBEW conference, May 6, 2021

TOTAL Classification: Restricted Distribution

TOTAL - All rights reservedYou can also read