Finance is not the dark side of the force - Università degli studi ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Finance is not the dark side

of the force

How to build a theoretical representation of financial

instability and sustainability

Alternative ways to understand the role

of finance in Macroeconomics

© Prof. AnnaMaria Variato – Fall 2019 1

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

FACING THE FINANCIAL CRISES OF THE

RECENT PAST

Overview of the Presentation

1. Empirical evidence: contrasting facts and theoretical

implications

2. Attempts to rationalize puzzling evidences related to

financial crises

3. Dangers of reductionist views of finance: two extremes

and a middle ground nearby speculation

4. Critical perspectives on financial crises after the 1990:

historical overview

5. Critical perspectives on mainstream approach to

financial crises: peculiar focuses

© Prof. AnnaMaria Variato – Fall 2019 2

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

1. Empirical evidence

• In the last decades events at international level have

shown that finance have strong destabilizing effects

• Crisis of financial nature become more frequent,

deeper, contagiuos and affect all kind of systems

(even highly developed economies)

Two kinds of problems:

• Interpretation (collect the relevant issues)

• Representation (build a theoretical synthesis)

«The Curious Case of Reinhart and Rogoff»

Reinhart and

Rogoff AER

Reinhart and Papers and

Rogoff NBER Proceedings

n. 15639 (2010)

Reinhart and (2010)

Rogoff

Princeton

University

Reinhart and Press (2009)

Rogoff NBER

n. 13882

(2008)

© Prof. AnnaMaria Variato – Fall 2019 3

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Reinhart and Rogoff (2008) Reinhart and Rogoff (2009)

• This time is different: a

panoramic view of eight

centuries of financial

crises

NBER n. 13882

© Prof. AnnaMaria Variato – Fall 2019 4

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

What does drive

the success of an economic paper?

R&R 2008: who

does know this

paper? …

But it is the most

interesting

R&R 2009 and

2010: best sellers…

but mistaken

© Prof. AnnaMaria Variato – Fall 2019 5

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Types of financial crises:

Reinhart and Rogoff (2008)

Currency

• Crashes

Inflation • Debasement

type I

• Debasement

type II

Banking Debt

• Systemic/Severe • Domestic

• Financial distress • Foreign

Source: Reinhart e Rogoff (2008)

© Prof. AnnaMaria Variato – Fall 2019 6

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Source: Reinhart e Rogoff (2008)

Mainstream puzzle 1: Does the foreign market have a long memory on default?

Foreign Public Debt: 1800-2006

% Countries Default or Restructuring

Percentuale di Paesi

Anno

Source: Reinhart e Rogoff (2008)

© Prof. AnnaMaria Variato – Fall 2019 7

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

• Mainstream puzzle 1a: Is

default on sovreign debt a

country specific

phenomenon? Direct quote from Reinhart

and Rogoff (2008, p. 6)

• The role of systemic forces

appear to be determinant «…global economic factors,

in order to characterize including commodity prices

either the speed or the and center country interest

depth of the crisis. rates, play a major role in

• In other words, financial precipitating sovereign debt

crises seem complex crises».

phenomena, that can be

understood only taking into

account macroeconomic

interactions.

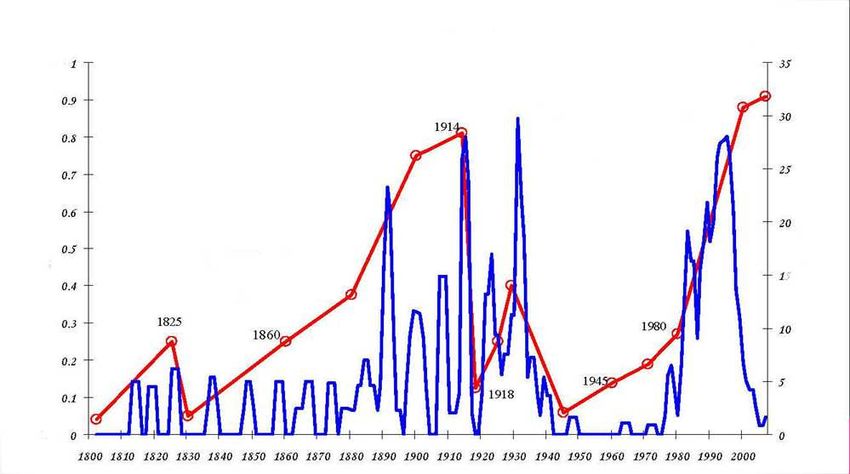

Mainstream puzzle 2: Does capital mobility foster financial markets stability?

Capital Mobility and Incidence of Bank Crisis: all countries 1800-

2007

% of contries experiencing crisis,

cumulative 3 years

Index of capital mobility

(right axis)

Capital Mobility

Share

(left axis)

Source: Reinhart e Rogoff (2008)

© Prof. AnnaMaria Variato – Fall 2019 8

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Mainstream puzzle 3: Does the presence of international institutions

reduce instability?

Lenght of Default episodes: 1800-2006 relative

frequency

1946-2006

169 episodes

Median 3 years

1800-1945

127 episodes

Median 6 years

Source: Reinhart e Rogoff (2008)

Mainstream puzzle 4: Does higher exchange rate flexibility reduce instability?

Currency crashes: share of contries showing

annual depreciation higher than 15%: 1800-2006

Napoleonic Wars

Source: Reinhart e Rogoff (2008)

© Prof. AnnaMaria Variato – Fall 2019 9

Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Mainstream puzzle 5: Crisis never have a unique sympthom

Variety of crisis: 1800-2006

Average number of crisis per country 5 years average

Asia

All Countries

Source: Reinhart e Rogoff (2008)

International financial

institutions seem not

Financial Markets able to reduce

do not instability

seem to have a

long lasting

memory

Higher international

price flexibility does

not seem to produce

higher stability

More complex financial Financial Crises are not

markets do not seem to • Idiosyncratic

enhance financial stability • Exceptional

• Simple

As they are both systemic and

systematic

© Prof. AnnaMaria Variato – Fall 2019 10Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Further puzzles: Micro-macro conflict

(fallacy of composition in financial markets)

Savers are rational

(as any other

economic agent)

Financial markets are

competitive

(as any other market)

The linkage between

remuneration and

productivity has an

incentive effect

Market rewards

innovative ability

Why do markets fail?

Limited Information

Prices cannot

perform their role

(convey all relevant information)

Uncertainty

Asymmetric Information

Bounded rationality

© Prof. AnnaMaria Variato – Fall 2019 11Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Examples of price inefficiency

Euphoria and panic

Distorted use of

information

Herd behavior

Human error: Insufficient

fraud and ignorance liquidity

Lack of

competition

Contagion

Main causes of recent financial crises

(standard view)

Microeconomic Macroeconomic

Financial fragility of

Risk appetite (too

emergent countiries

high)

(idiosynchratic)

Global real (?)

Risk evaluation convergence as

(wrong) opposed to global

financial divergence

© Prof. AnnaMaria Variato – Fall 2019 12Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Lessons from the past

Before the crisis

Foreign capital inflows without

adequate financial reforms or gains in

productivity

(possibly excessive) credit expansion…

…mostly true for emergent economies

Structural deficiencies and/or not sound

economic policies

Lessons from the past

When the crisis sets in

Real sensitivity as a function of financial fragility

Risk evaluation as a function of complexity

Liquidity as an uncertain variable

Contagion as a qualitative phenomenon

© Prof. AnnaMaria Variato – Fall 2019 13Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Even though stability is not an

autonomous feature of financial

markets, why do we need stable and

efficient financial markets?

• Dimension

• Connection contagion

• Instability determined

– Directly: type of good exchanged

– Indirectly: income effect

Whenever a crisis hits a system, the Economsit is

supposed to provide a satisfactory vision explaining

the originating prcess, the transmission mechanism

and the possible solution …

Of course it would be much better to be able to

predict and then prevent…

© Prof. AnnaMaria Variato – Fall 2019 14Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Elements of the «vision»:

choices one has to make

Genesis of instability

Exogenous Endogenous

Individual Behaviour

Rational Irrational

Role of Speculation

Stabilizing Destabilizing

Systemic behaviour

Random Complex

Recurrence of instability

Sporadic Cyclical

Impact of the crisis

Localized and temporary Widespread and persistent

The choices related to a Theory of

Endogenous Rational Financial Instability

Genesis of instability Endogenous

Rational

Individual Behaviour (limited rationality)

Role of Destabilizing

Speculation (mostly)

Systemic Behaviour Complex

Recurrence of

instability Cyclical

Widespread

Impact of the crisis

and persistent

© Prof. AnnaMaria Variato – Fall 2019 15Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

In order to have Rational and

Endogenous Instability

1. Simultaneous

interaction between

real and financial sides 2. Potential

of the economy conflict

(already mentioned) between micro

and macro

instances

(already mentioned)

3. Instability as an effect of the interaction between the

structure of the economy (fundamentals) and

automatic market adjustments

Role of

fundamentals

• Economic Policy mistakes

• (1929, Asia 1997, Brazil 1998, EU austerity)

• Correct Policy but mistaken

anticipation

• (Usa 1994 and following Messico 1995)

• role of communication and risk of moral

hazard (USA 1987, Giappone 1989)

© Prof. AnnaMaria Variato – Fall 2019 16Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

2. Attempts to rationalize puzzling

evidence (just a synthesis)

• Many attempts, different languages, different emphasis…

• Usually no need to come up with a unifying theory of financial

instability

• Common criticism against mainstream: fallacious implications due to

excess of reduction.

• Mainstream approach fails because of its inductive approach. This

kind of reductionism transforms what is supposed to be a

representative expedient (or a tool for representation) into an

homologation instrument (a model which drives out of the system

the varieties not implied by the representation).

• Whenever finance is depicted through an extreme reductionist

approach, the likely effect is to have it represented by myths instead

of facts. This becomes especially dangerous when the models are

used as frameworks for economic policy design.

3. Dangers related to reductionsit views

Myth 2 - Positive:

financial markets are efficient

Fact 1 – Not so negative: Financial

markets are the places where operators

mainly entertain speculative activities

Myth 1 - Negative:

financial markets are like casinos

Fact 2 – Negative: The target of financial

stability is far more difficult to reach today

than in the past

© Prof. AnnaMaria Variato – Fall 2019 17Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

Stop and ask:

Implicitly the myths deal (at least) with

four fundamental concepts, treating

them in a particular (simplified and

opposite) perspective.

Can you tell which they are?

3a: Speculation: stabilizing or destabilizing?

The characterizing

elements

of speculation Conjectures

(limited

information)

Individual

Gambling

advantage

(distribution)

(arbitrage)

In order to assess whether speculation is destabilizing or not,

one has to evaluate which of the three aspects is prevailing

© Prof. AnnaMaria Variato – Fall 2019 18Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

3a: Speculation: stabilizing or destabilizing?

• The fact information is

limited is the intrinsic

structural feature of any

speculative framework

• It implies the need to form

expectations and/or to extract

Conjectures signals in order to come up to

a decision.

• the type and qualitative

features of information limit

will eventually determine The

kind of inefficiency.

i.e. one cannot say in principle

Sign: ?

whether speculation is

destabilizing or not

3a: Speculation: stabilizing or destabilizing?

• The exploitation of

existing inefficiences by

some individuals make the

market converge towards

efficient equilibrium Individual

• The pursuit of individual

self-interest does not

advantage

produce negative (arbitrage)

effects at market level

• This leads to a policy

implication of laissez-

faire Sign: stabilizing

© Prof. AnnaMaria Variato – Fall 2019 19Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

3a: Speculation: stabilizing or destabilizing?

• Even though it requires

conjectures, it does not need them

essentially:

• the scope of this activity

is to alter resource distribution (like

arbitrage): differently from arbitrage,

gambling activity involves agents who are

Gambling aware of the bet

• If one wants to bet and then looses, this

is not the business of the economist

• The economist is interested when the

gamble implies cheating from one side,

and the other is not aware of the

existence of the gamble (or of its true

nature)

i.e. what matters is unfair gambling

Sign: destabilizing This leads to policy implication of

increasing rules in order to limit the

inefficiency due to undue redistribution

3a: Speculation: stabilizing or destabilizing?

conjectures conjectures

conjectures conjectures

© Prof. AnnaMaria Variato – Fall 2019 20Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

4. Historical overview of recent

financial crises

If so many and articulated explanations, why no sign to prevent

2007 crisis? It was not a surprise, but…

4.1 Main critical accounts prior 2007 crisis

Representation

Complex Waves of

of the Regulation and What kind of

money but popularity of

trasmission of supervions not representative

simple finance authors from

monetary effective tool? ABM vs.

(which is the past: are

policy (more because of SFCA instead of

somewhat we all

complex than unique model DSGE

paradoxical) minskian?!

mainstream)

© Prof. AnnaMaria Variato – Fall 2019 21Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

The stabilization chain of events according to

mainstream view (an example inspired to R&R, 2008)

Liquidity reduces the

likelihood to face a banking

crisis

• Directly because firms have access

Higher capital to alternative financing

mobility instruments Risk reduction due to

implies • Indirectly: the existence of

Banks have more liquidity even Customization

higher when borrowers become insolvent

varieties of financial

liquidity in (lower risk of contagion) asset side instruments

the system explanation

• Indirectly: Banks have more

liquidity to face deposit runs ;

liability side explanation

• Indirectly: depositors know about

liquidity then become less prone to

withdraw

Policy implications arising from the

stabilization chain of events according to

mainstream view

• Banking oriented systems are less efficient than market

oriented systems

• The presence of a banking oriented system is symptom of

backwardness

• Banking oriented systems are more unstable than market

oriented systems

Hence promote market oriented systems (and let banks

disappear… One may quote Bill Gates…)

© Prof. AnnaMaria Variato – Fall 2019 22Macroeconomics Applications Università degli Studi di Bergamo a.a. 2019-2020

5. Critical Approaches to Financial

Crises: peculiar focuses

Credit lever

Individual

History behavior

(or priors) rationality, risk attitude,

imitation and power

Risk reduction +

Institutions

instruments

Liquidity

© Prof. AnnaMaria Variato – Fall 2019 23You can also read