First Quarter 2019 Washington Update - Robert M. Kaplan, CFP, CPC, QPA Director of Technical Education American Retirement Association ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

First Quarter 2019

Washington Update

Robert M. Kaplan, CFP, CPC, QPA

Director of Technical Education

American Retirement Association

bkaplan@usaretirement.org

1

Agenda

• New Congress – Committee Leadership

• DoL COLAs for Penalties

• DoL – Input on Auto Portability

• Treasury Priority Plan

• Proposed Regulations – Hardship Withdrawals

• Safe Harbor 402(f) Updated

• ARA Letter on Electronic Disclosure

• Pending Bills in Congress

2

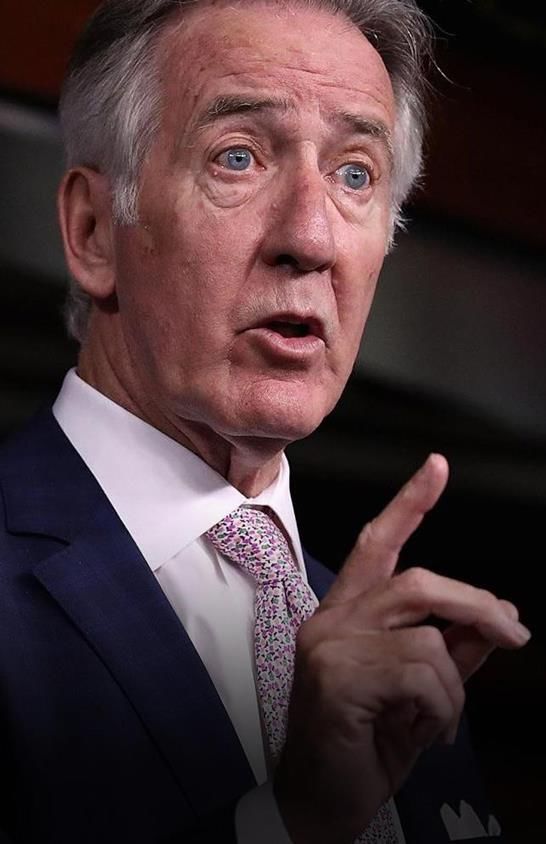

Committee Leadership

• Richie Neal (D-MA, 1st) - Chair of the House

Ways and Means Committee

• Mr. Neal became Chairman in the 116th

Congress which began in January

• Remember that all bills introduced in prior

Congress would have to be reintroduced

• As Chairman, he will be able to control the

Committee’s agenda.

• Retirement policy has always been a high

priority

• Late last year he introduced the Automatic

Retirement Plan Act

3

2019 DoL COLAs for Penalties

• Form 5500 from $2,140 to $2,194

• Auto Contribution Notice – from $1,693 to

$1,736

• Blackout or diversification notice – from

$136 to $139

• Recordkeeping or Reporting for

participants ERISA 209(b) – from $29 to

$30

4

DoL – Input on Auto Portability

• December 21st – ARA wrote a comment letter supporting this

proposed exemption

• 401(k) savings transferred to IRA (automatically) when sever

employment or plan terminated

• IRA would automatically transfer to 401(k) of new employer when

participant gets a new job

• Estimated increase of retirement savings by $1.5 trillion by preventing

leakage

5

Treasury – Priority Plan for 2018-2019

• Guidance on extended rollover period for qualified plan loan

offsets

• Updating ESOP rules

• Regulations on RMD life expectancy and distribution tables

• Timing of amendments to 403(b) plans

• Universal availability requirement under 403(b)

• RMD use of lump sum payments to replace lifetime income

being received by retirees

• Hardship regulations (Proposed were released)

• Missing participants

6

Hardship Rule Changes

• IRS Guidance – Proposed Regulations

released November 14th

– 60 day comment period

– January 14th – ARA commented

• Major issue is whether we can rely on them

7

Hardship Rule Changes

• Added “primary beneficiary..” as individual who

qualifies for medical, educational or funeral expenses

• Clarified that the home casualty reason does not

have to be in a federally declared disaster area (this

was an unintended consequence of TCJA 2017) – can

be applied retroactively to 2018

8

Hardship Rule Changes

• Added a new item to the list of reasons –

expenses occurred as a result of certain

federally declared disasters (the type the

IRS and Congress have previously given

relief for such as hurricanes, floods,

wildfires, etc.)

9

Hardship Rule Changes

• Suspension of elective deferrals or after-

tax contributions no longer required

– Can wait until 2020 to implement

– Also added an optional transition rule that would

allow a suspension that started to be lifted as of

the first day of the 2019 plan year

10Hardship Rule Changes

• Eliminates the requirement to take all

available plan loans prior to the hardship

– Note: the rule change is only for loans and NOT all other

available distributions

– Plan may voluntarily retain this provision

• Eliminates the facts and circumstances

methodology and now there is ONE general

standard for determination (see next slide)

11Hardship Rule Changes

• General standard

– Hardship may not exceed amount of need adjusted for

anticipated taxes and penalties

– Must have obtained all other available distributions under

the employer’s plans (but remember not loans)

– Employee must represent that he or she has insufficient

cash or liquid assets to satisfy financial need

• Employer may rely on this representation unless they have

knowledge to the contrary

• This provision effective in 2020

12Hardship Rule Changes

• Sources for hardship expanded

– Elective deferrals PLUS earnings

– QNECs, QMACS, Safe harbors, QACA – all of these

plus earnings

– Generally, effective after 2018 PY

– Note that plans may limit the sources for hardship

availability

13Hardship Rule Changes

• §403(b) arrangements

– Income attributable to elective deferrals are still

not eligible for hardship – this needs a technical

correction in the law

– QNECs and QMACs in custodial accounts are

ineligible for hardship

– QNECs and QMACs that are not in custodial

accounts are eligible for hardship

14Hardship Rule Changes

• Timing

– Generally can be relied upon currently

– The employee representation standard applies to

distributions made on or after January 1, 2020

– The updated list of reasons may be relied upon

any date as early as January 1 ,2018

• This may help with confusion that occurred due to the

need to be in a federally declared disaster area

15Hardship Rule Changes

• Plan Amendments

– IDPs – the end of second year after the issuance of

the Required Amendments list

– Pre-approved plans – ????

16Hardship Rule Changes

• What do we need to do at this point

– Update administrative systems

– Communicate rules to Plan Administrators

– Communicate rules to plan participants

– Re-train our employees on new rules

– Adopt the interim amendment

– Track administrative practices during the

transition period so can update document later or

be prepared in case of future audit

17Notice Updated

Updated 402(f) Special Tax Notice

– IRS Notice 2018-74

• Appendix A – Pre-tax funds

• Appendix B – Roth funds

• Incorporates loan offset rules

• Also has language that rollover time frames may be

extended due to declared disasters

• Other changes that impact federal retirees and

government employees (expansion of exemption from

10% penalty)

18Speaking of Updates

IRS updated its “Fix-it” guide on their website for Participant

Loans that do not conform with the plan document or §72(p)

https://www.irs.gov/retirement-plans/401k-plan-fix-it-guide-

participant-loans-do-not-conform-to-the-requirements-of-

the-plan-document-and-irc-section-72p

No new rules BUT this is a great tool to show plan sponsors

or administrators

19ARA Letter on Electronic Disclosure

To DoL – December 12th

– Trump 8/31 Executive Order mentioned making

disclosures more understandable and useful

– ARA suggested electronic disclosure as a default

• Paper would be allowable if elected by employee

– Enhance effectiveness (particularly to special needs or non-English

speaking participants)

– Significant cost savings

– Reduce environmental impact

– Simplify content – shorter and more pointed

– Reduce number of notices

• Eliminate redundant and ineffective notices

• Coordinate timing

• Permit combining of notices

20RESA Resurrected

Reintroduced in House by Kind (D-WI) and Kelly (R-

PA)

Many retirement plan enhancements including..

– Unrelated employers adopting MEPs

– Initial plan adoption to due date of tax return

– Greater flexibility in Safe Harbor 401(k) plan

design

– Tax credit increase for adopting a small plan and

additional credit for adopting auto enroll

21Pending Bill in Congress

Rehabilitation for Multiemployer Pensions Act

– Introduced by Richard Neal (D- MA) in January

– Would establish Pension Rehabilitation

Administration (PRA)

– Not a bailout

– Agency issues bonds to raise funds for plans and

plans must pay back PRA loans

22Pending Bill in Congress

SIMPLE Plan Modernization Act

– Introduced by Collins(R- ME) and Warner (D-VA)

last week

– Increase SIMPLE limits

• Deferrals from $13,000 to $16,000

• Catch-up from $3,000 to $4,500

• Allow higher limits for plans with 26-100 employees but

only if they increased employer contribution by 1

percentage point

– Directs Treasury to study the use of SIMPLE Plans

and report to Congress with recommendations

23Pending Bill in Congress

Retirement Security Act

– Introduced by Collins(R- ME) and Hassan (D-NH)

last week

– MEPs

• No nexus needed to join MEP

• Eliminate “one bad apple rule”

– Direct Treasury to simplify, clarify and consolidate

notices

– Simplify compliance for small businesses that

provide match up to 10% of pay

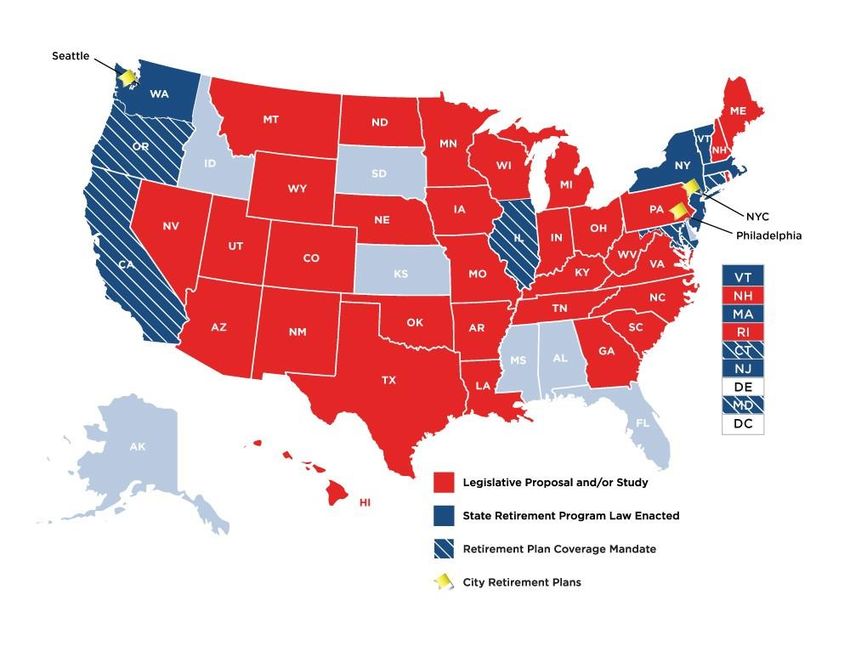

24PLAN COVERAGE CHALLENGE Source: unpublished Employee Benefit Research Institute estimates from 2013 Current Population Survey

STATE LEGISLATIVE ACTIVITY

Nevada Propose Regulations

• Fiduciary standard proposed by the State of Nevada

• ARA will comment (comments due by March 1st

• No ERISA exemption

• If challenged will the preemption issue arise

• Defines fiduciary obligations to a client as:

• Provides investment advice

• Performs discretionary trading

• Maintains assets under management

• Acts in fiduciary capacity toward client

• Discloses fees or gains

• Through completion of any contract

• And through the term of the engagement of services

• Stay tunedQuestions?

Join me for the Second Quarter 2019 Washington Update on

May 22, 2019You can also read