Foreign-Owned U.S. Real Estate: To Rent or Not to Rent

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Foreign-Owned

U.S. Real Estate:

To Rent or Not to Rent

With the right structure, rent-free use of corporate-owned real property

need not have any adverse U.S. income tax consequence.

DINA KAPUR SANNA AND STEPHEN ZIOBROWSKI, ATTORNEYS

onresident aliens frequently her family members be charged rent dent consists of only property that

N purchase U.S. real property

for personal use. To avoid U.S.

estate tax, the most common

structure to hold the U.S. real prop-

erty is through a foreign corpora-

for their personal use of U.S. real

property when the property is

owned through a foreign corpo-

ration to avoid adverse U.S. tax

consequences?

has, or is deemed to have, a "U.S.

situs" at the time of the nonresident's

death, or when certain lifetime trans-

fers occur that come under the

"retained string provisions" of Sec-

tion organized and owned by the tions 2035 through 2038.1 Under

nonresident. Because the property U.S. taxation of these Code sections, a decedent is

is owned by the foreign corporation nonresident individuals subject to estate tax on property

rather than the nonresident, for pur- Nonresident individuals could he or she has transferred during life,

poses of U.S. estate tax the nonres- potentially have U.S. estate tax and by trust, or otherwise, where the

ident is treated as owning the stock income tax exposure. decedent retained the right, either

of the foreign corporation rather alone or in conjunction with any

than the underlying U.S. real prop- Estate tax. For U.S. estate tax pur- person, to designate the persons who

erty. Stock in a foreign corporation poses, a nonresident is a nonciti- would possess or enjoy the proper-

is not a U.S. situs asset, so it is not zen who is not domiciled in the U.S. ty or the income therefrom or where

subject to estate tax. (U.S. domicile is acquired by living the enjoyment is subject at the date

Although the foreign corpora- in the U.S. with no definite present of his or her death to any change

tion structure addresses U.S. estate intention of later moving from the exercisable by the decedent alone

tax issues, it is not without its com- U.S.) The gross estate of a nonresi- or in conjunction with another

plications. The discussion below person to alter, amend, revoke, or

begins by describing the more stan- DINA KAPUR SANNA and STEPHEN ZIOBROWSK. are terminate (or such power was re-

dard issues implicated by the struc- partners with the law firm of Day Pitney LLP who reg- linquished within three years of

ture. The balance of the article u any advise high net worth cl'ents on cross border death).2

tax and trust planning matters. aria practices in the

addresses an issue that has not pre- A nonresident's gross estate is

New York office and Stephen practices in the Boston

viously received much attention but office The authors wou:d Ike to thank the r colleague

determined in the same manner as

plagued practitioners nonetheless: Andrew Wogman, for his research and preparation in the gross estate of a U.S. resident

Should the nonresident or his or connection with parts of this article. or citizen, except that:

3

•

•4

1. Property outside the U.S. is obligations of a U.S. person or a U.S. number of days of presence for the

excluded. governmental entity, the written evi- first preceding year is multiplied by

2. Special rules apply to joint dence of which is not treated as a factor of V3, and the number of

property where the surviving the property itself.° There are excep- days of presence for the second pre-

spouse is not a U.S. citizen. tions for portfolio debt, certain ceding year is multiplied by a fac-

(These rules apply to U.S. short-term original issue discount tor of 1/6. There are exceptions for,

decedents with noncitizen obligations, and bank deposits. Also, among others, students, teachers,

spouses as well.) stock of a corporation organized foreign diplomats, and those who

3. The deductions and credits under U.S. law (or the law of a U.S. can claim a closer connection to

available to a nonresident's state) is deemed to have a U.S. situs, another country. In addition, a

gross estate are limited. regardless of where the share cer- bilateral income tax treaty can pro-

tificates are physically located.° vide relief for dual-resident tax-

Although a nonresident is sub-

Notably, the situs rules fail to men- payers who can claim residence in

ject to estate tax on U.S.-situs assets

tion partnership interests, nor does the treaty country, if they satisfy

at marginal rates of up to 40%, the

any case law apply the relevant pro- the provisions of the treaty tie-

applicable estate tax exemption is

visions to partnership interests. In breaker.

only $60,000, unless a bilateral

the absence of authority, the fol- A nonresident is subject to U.S.

estate tax treaty provides other- income tax on his or her:

wise, compared to $5 million (infla- lowing analysis may apply.

A partnership that does not ter- 1. U.S.-source fixed or deter-

tion adjusted to $5.34 million in minable annual or periodical

2014) for a U.S. citizen or resident.3 minate on the death of a partner

can be viewed as a separate and dis- (FDAP) income, the tax on

The situs rules are found in Sec- which is collected by with-

tions 2104 and 2105, as ampli- tinct entity from its owners or as

an aggregate of their interests. Case holding at a 30% rate (or

fied by Treasury Regulations, but lower treaty rate) on gross

may be modified by a bilateral law and commentary support enti-

ty theory more than aggregate the- FDAP income.

estate tax treaty. These situs rules 2. Income that is effectively con-

provide as follows. ory in this context. When applying

the entity theory however, there are nected (ECI) with a U.S. trade

With few exceptions (e.g., works or business, which is taxed at

of art on loan and personal prop- two possible outcomes for deter-

mining situs: graduated rates of up to

erty accompanying a nonresident 39.6% on a net basis.13

who dies while in the U.S.), tangi- 1. Situs is determined based on

the location where the part- FDAP. FDAP income includes,

ble personal property located in the

nership conducts its business.10 among other items, interest, divi-

U.S. is a U.S.-situs asset.

2. Situs is determined based on dends, and rents from U.S. sources.14

Real property located in the U.S.

has a U.S. situs.4 If the real prop- the residency of the partnership

1 Sections 2101-2104. Under Section 2104(b),

erty is subject to a nonrecourse for income tax purposes (i.e., any property subject to the string provisions

of Sect ons 2035 through 2038 is included

mortgage, the real property is its place of organization).” in the gross estate of a nonresident, if it had

or was deemed to have a U.S. situs at the time

included in the gross estate at its No clear rule has emerged. of the transfer or death.

net equity value.5In contrast, where 2 Sections 2036 and 2038.

the real property is subject to a Income tax. For U.S. income tax 3 Section 2102(b).

4 Reg. 20.2104-1(a)(1).

recourse mortgage, the real prop- purposes, a nonresident is a nonci- 5 Reg. 20.2053-7.

erty is included at its full value, but tizen who does not hold a green 6 Id.

only a pro-rated deduction for the card or satisfy the substantial pres- 7 Reg. 20 2104-1(a)(4).

9 Section 2104(c); Reg. 20.2104-1(a)(7).

mortgage is allowed, based on the ence test.12 To satisfy the substan- 9 Section 2104(a); Reg. 20.2104-1(a)(5).

proportion that the nonresident's tial presence test, an individual 10 See, e.g.. Rev. Rul. 55-701, 1955-2 CB 836.

U.S. assets bear to his or her world- must be physically present in the 11 See, e.g., Reg. 301.7701-5, which is consis-

tent with the rules applied to corporations

wide assets.6 U.S. for 31 days in the current cal- under Section 2104(a) and Reg. 20.2104-

Intangible personal property, the endar year and for a weighted total

12 Section 7701(b)(1)(A).

written evidence of which is not at least 183 days during the current 13 Sections 871(a) and (b). Nonresident alien indi-

treated as the property itself, is year and the two preceding calen- viduals are not subject to the 3.8% Medicare

tax that may apply to the net investment income

deemed to have a U.S. situs if it is dar years. For this purpose, the of U.S. taxpayers Section 1411(e)(1)

issued by, or enforceable against, a number of days of presence in the 14 Section 871(a)(1)(A). Exceptions exist for inter-

est earned on portfolio debt instruments and

U.S. resident. 7 This includes debt current year is counted in full, the bank deposits. Sections 871(h) and 871(i)(3).

FS'ATE PI ANNING APRIL 2014 VOL 41 / NO 4

•6

FDAP income, however, generally porate stock, if the nonresident an agreement for the payment of

does not include capital gains rec- owns 5% or less of such stock).20 tax.25 A withholding certificate that

ognized on sales or exchanges of is obtained prior to the transfer

assets held for investment.15 Also, relieves the transferee from with-

FDAP income does not include gain holding obligations.25

recognized on the disposition of a A nonresident taxpayer who has

Because U.S. real

"U.S. real property interest," which, property is a

FIRPTA gain must file a U.S. tax

as discussed in detail below, is taxed U.S.-situs asset return and apply the taxes with-

as if it were ECI.15 A nonresident for estate held against the tax liability shown

taxpayer whose only income is tax purposes, on the return. The lower long-term

nonresidents often capital gains rate (currently 20%)

FDAP income on which tax has been

hold U.S. real

withheld is not required to file a U.S. is available to a nonresident indi-

property through

tax return. a blacker foreign vidual on a sale of a USRPI, if the

EC/. A nonresident who has ECI corporation. sale otherwise qualifies.

must file a U.S. tax return and may

FIRPTA applies a look-through U.S. taxation of corporations

deduct expenses that are directly

rule to partnerships and trusts. The first step in determining the

connected with the Ed. ECI is gen- Under this look-through rule, a dis-

erally not subject to withholding U.S. taxation of a business is to

position of an interest in a USRPI identify the form in which the enter-

in the U.S. except where it is derived by a partnership is treated as a dis-

through a partnership. prise is organized.

position of each partner's ratable

Rental income from U.S. real share of the USRPI held by the part- Entity classification. The U.S. tax

property can be FDAP or ECI, nership.2i Under Treasury Regula- classification of a business entity is

depending on the facts. To elimi- tions, an interest in a partnership not always consistent with its form

nate uncertainty, an election is is a USRPI if 50% or more of the of organization. Under the "check-

available that allows a nonresident value of the partnership's gross the-box" rules found in Reg.

to treat income from U.S. real prop- assets are USRPIs and 90% or more 301.7701-3, many types of busi-

erty as ECI.17 Despite the fact that of the value of the gross assets of the ness entities are permitted to elect

ECI may be subject to a higher mar- partnership consists of USRPIs plus their classification for U.S. tax pur-

ginal tax rate than FDAP, this elec- cash or cash equivalents (but only poses. In particular, most partner-

tion is often favorable because it to the extent that the gain on dis- ships or limited liability companies

results in tax on net income, not position is attributable to USRPIs). (whether U.S. or foreign) can elect

gross income, and net rental income FIRPTA withholding (discussed to be taxed as corporations; other

may be modest due to depreciation below) may be imposed on the entire types of foreign entities are "per

and deductible expenses such as proceeds of disposition of a part- se" corporations for U.S. tax pur-

insurance and real estate taxes. nership interest that is a USRPI.22

FIRPTA. Under the Foreign FIRPTA is enforced through 19 Sect on 871(a)(1)(A) (listing types of income

Investment in Real Property Tax withholding obligations imposed other than capital gains). Despite the gener-

al exemption from U.S. tax for capital ga . ns

Act (FIRPTA), gains from the dis- on the transferee, who must gen- that are not treated as ECI, Section 871(a)(2)

position of a "U.S. real property erally withhold 10% of the provides that net U.S.-source capital ga'ns

are taxable at 30% in the hands of nonresi-

interest" are taxed as ECI to a non- "amount realized."23 Relief from dent aren individuals physica ly present

in the U.S. for 183 days or more during the

resident.15 In general, a U.S. real FIRPTA withholding may be avail- tax year.

property interest (USRPI) is (1) a able for nonrecognition transac- 16 Section 897.

direct interest in U.S. real proper- tions under the Code, provided cer- 17 Section 871(d)(1).

16 Section 897(a).

ty (other than an interest solely as tain filing requirements are met.24 19 Section 897(c)(1).

a creditor) and (2) an interest in In other cases, withholding may be 29 Sectons 897(c)(2) and (3).

stock of a domestic corporation reduced or eliminated pursuant to Sect'on 897(g).

22 Tem p . Reg. 1.897-7T(a). Despite the limrta-

that is a U.S. real property holding a withholding certificate issued tions of the regulations, the IRS has indicat-

company (USRPHC).19 A USRPHC by the IRS. The IRS may issue such ed that the applicability of the Code section

is not contingent on the :ssuance of regula-

is a corporation more than 50% a certificate where it determines t ons. Notice 88-72, 1988-2 CB 383.

23 Section 1445.

the value of which is attributable that reduced withholding is appro-

24 Section 897(e), Temp Reg 1.897-6T(a)

to U.S. real property (with an priate, the transferor is exempt 25 Reg. 1.1445-3(a).

exception for publicly traded cor- from U.S. tax, or the IRS enters into 26 Id .

ESTATF P. ANNING APFi 2014 VOL 41 I NO 4

poses and are not eligible to elect ing through a disregarded entity). cable), because it is FDAP income.

their classification. This article pre- Assuming that the property pro- However, if no dividends are paid

sumes that the entity holding U.S. duces rental income and the cor- during the life of the U.S. corpora-

real property is taxed as a corpo- poration has made an election to tion, the 30% withholding tax can

ration in the U.S. treat the rental income as Ed, the be avoided. If the U.S. corporation

corporation will be required to file is liquidated following the sale of its

General rules of corporate taxa- a U.S. tax return and pay tax on its property, the corporation can avoid

tion. In the U.S., a corporation is net income at rates of up to 35%. FIRPTA withholding tax if both:

generally a separate and distinct Gain on the sale of the property

taxable entity. The character of a will be subject to tax under FIRP- 1. The distributing corporation

corporation's income is not "passed TA as Ed, and, absent an excep- did not hold any USRPIs at the

through" to its shareholders.27 Fur- tion, FIRMA withholding will date of distribution.

thermore: apply to the sale proceeds. In addi- 2. All of its USRPIs were dis-

tion, a 30% tax may be imposed posed of in transactions

• A corporation is subject to tax

on the after-tax earnings that are in which the full gain was

on its net income, at tax rates

not reinvested in the U.S. business recognized.31

currently ranging from 15%

to 35%. (the "branch profits tax").

Although the branch profits tax Corporate ownership:

• A corporation does not pay a benefits and downsides

lower rate of tax on capital is intended to parallel the 30%

withholding tax imposed on divi- Because U.S. real property is a U.S.-

gains than on ordinary income. situs asset for estate tax purposes,

• A shareholder who receives a dends paid by U.S. corporations to

foreign shareholders (discussed nonresidents often hold U.S. real

distribution in respect of his or

below), the branch profits tax often property through a blocker foreign

her stock realizes taxable

results in a higher effective tax corporation. This approach has the

income to the extent of the cor-

because the tax is imposed regard- advantages of low cost and sim-

poration's current and accumu-

less of whether a dividend has been plicity. The downside is loss of

lated earnings and profits.29

paid. There is, however, an excep- the lower capital gains tax rate on

These amounts are treated as

tion from the branch profits tax a sale of property and potential for

dividends. The portion of a dis-

when property is sold if the cor- a second entity-level tax (i.e., the

tribution in excess of the cor-

poration terminates its U.S. trades branch profits tax).

poration's current and accumu-

or businesses and does not reinvest Conduit structures, such as for-

lated earnings and profits is the sales proceeds in the U.S. for at

treated as a nontaxable return eign partnerships or foreign non-

least three years.30 grantor trusts, can preserve quali-

of stock basis. To the extent Alternatively, a foreign corpora-

amounts distributed exceed the fication for the lower capital gains

tion could set up a U.S. corporate rate, but those alternatives present

corporation's current and accu- subsidiary, which in turn would own

mulated earnings and profits their own downsides:

the U.S. real property. If the prop-

and the shareholder's basis in erty produces net rental income, the • In the case of a foreign partner-

his stock, the distribution is U.S. corporation will file a U.S. tax ship holding U.S. real property,

treated as gain from the sale or return and pay tax at regular cor- the nonresident must be willing

exchange of property (which porate rates. A dividend paid by the to accept a risk of estate tax

may qualify as capital gain).29 U.S. subsidiary to its foreign par- exposure because of the lack of

A foreign corporation may hold ent will be subject to 30% with- clear guidance on the situs of

U.S. real property directly (includ- holding (or lower treaty rate, if appli- partnership interests.32

.:.1MMEN ■•=11..

22 This general statement has several excep- ness activities, it must (1) cease to have any should be subject to estate tax only if it rep-

tions. For instance, under certa n circum- U.S. assets, (2) not reinvest in a U.S. trade resents an obligation enforceab e aga;nst a

stances, corporations can make an election or business within three years (nor can any U.S. partnership. McCaffrey, "Tax Planning

to be treated as corporations," which related corporation make such an investment), for Foreign Ownersh:p of United States

are generally taxed as 'pass throughs." An (3) have no ECI for three years from the end Homes" ACTEC Fall Meeting (October 2012).

"S corporation" cannot, however, have a non- of the termination year, and (4) comply with The IRS has refused to rule on whether a part-

resident alien shareholder. certain procedural requirements See gen- nership interest is intangible property for pur-

29 Sections 301(a) and (c), and 316. erally Temp. Reg. 1.884-2T(a)(2)(i) poses of Section 2501(a)(2) (dealing w th

23 Section 301(c). 31 Sections 897(c)(1)(B) and 1445(e)(3). transfers of intangible property by a nonres-

3 ° Temp. Reg. 1.884-2T(a)(1). In order for the 32 Some practitioners have suggested that an ident for purposes of the U S. federal gift tax).

foreign corporation to be treated as com- interest in a partnership that surv yes the death Rev. Proc. 2013-7, 2013-1 IRB 233, section

pletely terminating all of its U.S. trade or busi- of a partner is intangible property which 4.01(28).

APRIL 2014 VOL 4 1 NO 4 FOREIGN-OWNED REAL ESTATE

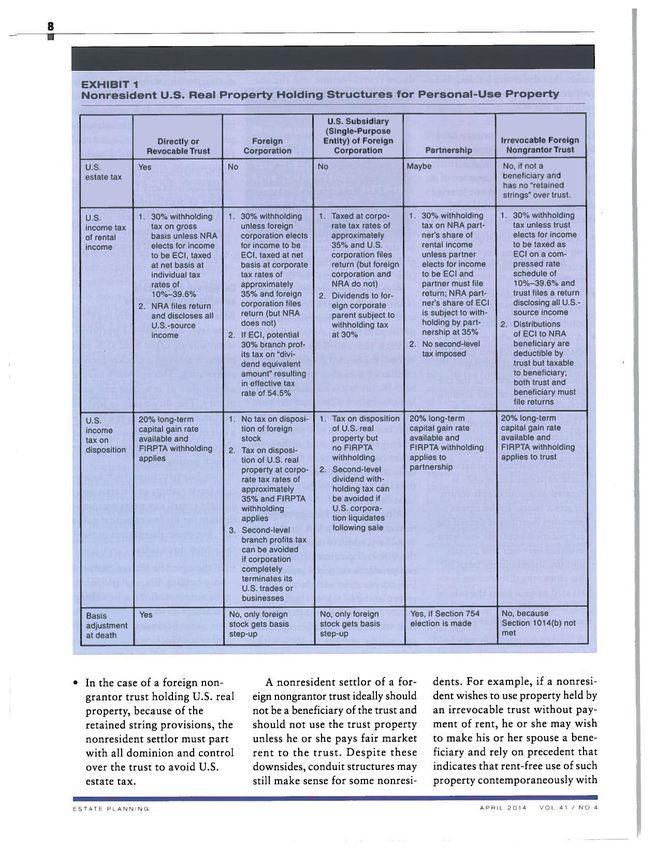

EXHIBIT 1

Nonresident U.S. Real Property Holding Structures for Personal-Use Property

U.S. Subsidiary

(Single-Purpose

Directly or Foreign Entity) of Foreign Irrevocable Foreign

Revocable Trust Corporation Corporation Partnership Nongrantor Trust

U.S. Yes No No Maybe No, if not a

estate tax beneficiary and

has no "retained

strings" over trust.

U.S. 1. 30% withholding 1. 30% withholding 1. Taxed at corpo- 1. 30 0/0 withholding 1. 30% withholding

income tax tax on gross unless foreign rate tax rates of tax on NRA part- tax unless trust

of rental basis unless NRA corporation elects approximately ner's share of elects for income

income elects for income for income to be 35% and U.S. rental income to be taxed as

to be Ed, taxed Ed, taxed at net corporation files unless partner ECI on a com-

at net basis at basis at corporate return (but foreign elects for income pressed rate

individual tax tax rates of corporation and to be ECI and schedule of

rates of approximately NRA do not) partner must file 10%-39.6% and

10%-39.6% 35% and foreign 2. Dividends to for- return; NRA part- trust files a return

2. NRA files return corporation files eign corporate ner's share of ECI disclosing all U.S.-

and discloses all return (but NRA parent subject to is subject to with- source income

U.S.-source does not) withholding tax holding by part- 2. Distributions

income 2. If ECI, potential at 30% nership at 35% of ECI to NRA

30% branch prof- 2. No second-level beneficiary are

its tax on "divi- tax imposed deductible by

dend equivalent trust but taxable

amount" resulting to beneficiary;

in effective tax both trust and

rate of 54.5% beneficiary must

file returns

U.S. 20% long-term 1. No tax on disposi- 1. Tax on disposition 20% long-term 20% long-term

income capital gain rate tion of foreign of U.S. real capital gain rate capital gain rate

tax on available and stock property but available and available and

disposition FIRPTA withholding 2. Tax on disposi- no FIRPTA FIRPTA withholding FIRPTA withholding

applies tion of U.S. real withholding applies to applies to trust

property at corpo- 2. Second-level partnership

rate tax rates of dividend with-

approximately holding tax can

35% and FIR PTA be avoided if

withholding U.S. corpora-

applies tion liquidates

3. Second-level following sale

branch profits tax

can be avoided

if corporation

completely

terminates its

U.S. trades or

businesses

Basis Yes No, only foreign No, only foreign Yes, if Section 754 No, because

adjustment stock gets basis stock gets basis election is made Section 1014(b) not

at death step-up step-up met

• In the case of a foreign non- A nonresident settlor of a for- dents. For example, if a nonresi-

grantor trust holding U.S. real eign nongrantor trust ideally should dent wishes to use property held by

property, because of the not be a beneficiary of the trust and an irrevocable trust without pay-

retained string provisions, the should not use the trust property ment of rent, he or she may wish

nonresident settlor must part unless he or she pays fair market to make his or her spouse a bene-

with all dominion and control rent to the trust. Despite these ficiary and rely on precedent that

over the trust to avoid U.S. downsides, conduit structures may indicates that rent-free use of such

estate tax. still make sense for some nonresi- property contemporaneously with

a spouse beneficiary is not a the corporation based on the trans- to its foreign parent and then to the

retained interest. 33 Although the fer pricing rules of Section 482.34 nonresident shareholder. Because

balance of this article is dedicated The imputed rent would be U.S.- the U.S. corporation had earnings

to the corporate holding structures, source income, taxable as FDAP or and profits from the business activ-

Exhibit 1 includes a chart of vari- ECI. However, there do not appear ities of its U.S. subsidiaries, the

ous real property holding struc- to be any cases, rulings, or other deemed dividend from the U.S cor-

tures, including their advantages guidance that take this approach. poration was subject to U.S. with-

and potential disadvantages. In addition, Section 482 by its terms holding tax of 30%. The Tax Court

applies to only allocations of stated that "[w]hen a shareholder

Payment of rent to corporation income between or among com- or his family is permitted to use cor-

When property held through a for- monly controlled entities, not to porate property for personal pur-

eign corporation is used for per- allocations between individual poses, the fair rental value of the

sonal purposes by a nonresident shareholders and corporations. property is includable in his

shareholder or that individual's

Thus, Section 482 seems not be or her income as a constructive

family members, the question of

likely to apply in this situation. dividend to the extent of the cor-

imputed rent or constructive dis-

Constructive distributions. In a poration's earnings and profits ...

tribution becomes relevant.

2012 case,35 the Tax Court con- [and] ... [f]or a corporate benefit

Imputed rent. Some commentators sidered a situation where U.S. real to be treated as a constructive div-

have suggested that the IRS might property was owned by a U.S. sub- idend, the item must primarily ben-

attempt to impute rental income to sidiary of a foreign corporation efit the taxpayer's personal inter-

owned by a nonresident share- ests as opposed to the business

Gutchess Est., 46 TC 554 (1966), acq. 1967-

holder. The U.S. subsidiary was the interests of the corporation" (cita-

1 CB 2; Rev. Rule 70-155. 1970-1 CB 189 common parent of an affiliated tions omitted).36

34 Karlin and Ruchelman, "Home Thoughts from

Abroad: Foreign Purchases of U.S. Homes."

group of corporations filing a con- The Tax Court's holding seems

116 Tax Notes 863 (2007). solidated tax return in the U.S. The to be consistent with the weight of

35 G.D. Parker, Inc., TCM 2012-327

36 Id. The personal use of corporate property

Tax Court held that the rent-free authority in this area. From a review

also resulted in disailowance to the U.S. use of the corporate property by of the existing law, it seems well

corporation of tax benefits generated by the

property, such as depreciation or the invest- family members of the nonresident established that uncompensated use

ment tax credit, because the corporation was shareholder was a deemed distri- of corporate property by a share-

not using the leased property for business

purposes. bution from the U.S. corporation holder may be treated as a con-

Yes! I m ould like to order the WG&L Reprints listed below.

REPRINTS Please contact me with pricing information.

NEW SERVICE FOR WG&L SUBSCRIBERS Quantity of Reprints No. of Pages

Publicat on (include Vol , No.)

The professional way to share today's best thinking on

crucial topics with your colleagues and clients. Article Title

Noss it's easy for you to obtain affordable, professional!) bound copies of

V c lip or photocopy an d m ail today •

Author

especial!) pertinent article; from thi , 2ournal.

With WG&L Reprints, you Lan: Shp/al to.

• Communicate new ideas and techniques that have been developed

by leading industry experts Name 0 Mr. r.= Ms.

(please pant)

• Keep up with new developments and how they affect you

Title

and your company

• Enhance in-house training programs Firm

• Promote your products or services b) offering copies to clients

• And much more Address

For additional information about WG&L Reprznts or to place an order for

City/State/Zip

100 copies or more, mail the coupon or call:

Phone ( ) 0 Office 0 Home

1-973-942-2243 • REPRINTS

Please remember that articles appearing in this journal may not be Mall to: Reprints

reproduced without permission of the publisher. For orders of fewer than 175 U.S. Highway 46 West • Fairfield, NJ 07004

100 reprints, call the Copyright Clearance Center at 978-750-8400. or Fax: 973-233-6701.

APRIL 2014 VOL 41 NO 4 FOREIGN-OWNED REAL ESTATE

10

structive distribution from the cor- the same as a dividend actually paid Conclusion

poration to the shareholder. While to the shareholder.40 If a nonresident shareholder of a for-

a few cases have characterized such The FSA is consistent with other eign corporation uses real proper-

use as gifts from the corporation rulings. The IRS's position is set ty held by the corporation without

to the shareholder, these cases are forth most succinctly in Rev. Rul. paying a fair market rent, the

dated and seem to be outliers.37 58-1.41 In that ruling, the IRS stat- uncompensated use of the property

In determining the nature of the ed that where shareholders are may be treated as a constructive dis-

constructive distribution, some allowed to use an apartment owned tribution by the corporation to the

courts have treated the corpora- by a corporation for below-market shareholder. This may or may not

tion's depreciation charges and rent, the excess of the fair market have adverse U.S. tax consequences.

maintenance expenses as a con- rent over the amount paid by the Where the foreign corporation

structive distribution, to the extent shareholder is treated as a distri- holds U.S. real property directly,

that they exceeded the rent paid by bution by the corporation and is a constructive distribution should

the shareholder.38 The more typi- generally have no U.S. tax conse-

includable in the shareholder's

cal result, however, is that the con- quence to the foreign corporation

income, to the extent that it is a div-

structive distribution is the differ- or the nonresident shareholder

idend. The ruling goes on to con-

ence between the property's fair because neither are U.S. taxpayers,

firm that the amount constituting

rental value and the amount paid and the distribution is not FDAP

a dividend is that part of the con-

by the shareholder for its use. or Ea. In contrast, if the real prop-

In IRS Field Service Advice, FSA structive distribution derived from erty is held indirectly, through a

199945017, the majority share- the corporation's earnings and prof- U.S. subsidiary, as was the case in

holder of an S corporation used a its.42 Although one commentator G.D. Parker, the constructive dis-

corporate asset on a rent-free basis has suggested that rent-free use of tribution could be subject to a 30%

after previously paying the corpo- corporate property by sharehold- withholding tax if the U.S. corpo-

ration for use of the asset.38 The ers should always be treated as ration has earnings and profits.

IRS advised that this could be treat- income to the shareholders,43 case However, if the U.S. corporation

ed as a constructive dividend to the law is generally consistent in hold- holds no other income-producing

majority shareholder, as he per- ing that shareholders must report property, and if the U.S. real prop-

sonally benefited from the use of the value of use of the property as erty is not rented, then the con-

the asset. The amount of the con- a constructive distribution,44 which structive distribution would gen-

structive dividend was the fair could result in no tax liability to erally not be taxable because the

rental value of the asset. This con- the shareholder (e.g., if the corpo- U.S. corporation would have no

structive dividend would be taxed ration has no earnings and profits). current or accumulated earnings

37 Moreover, the IRS has ind cated that corpo- er, the entire amount would be taxable as ordi- tors have indicated that given the subsequent

rations generally do not make gifts. See FSA nary income and subject to applicable employ- case history and guidance from the IRS, these

199945017 (re-released on 4/29/2005, with . ment taxes and income tax withholding. early gift characterizations were "question-

additional information) (see below discussion 41 1958-1 CB 173. able" and examples of the courts "dabbling"

of this guidance). Section 643(i) treats the with the idea. See id. (stating that the courts

42 See 58th St. Plaza Theatre, Inc., 195 F.2d 724,

uncompensated use of trust property as a "... dabbled with the idea that where the share-

constructive distribution, but Section 643(i) 41 AFTR 1130 (CA-2, 1952) cert. den. 344 holder did not provide any serv ces to the cor

has no corporate counterpart. U.S. 820(1952) (lease to shareholder's wife); poration, the free use of corporate property

Nicholls, North, Buse Co., 56 IC 1225 (1971) should be considered a tax-free gift to the

39 Riss & Company, Inc., TCM 1964-190 (find-

("It is well established that any expenditure shareholders ... [but the courts] eventual)/

ing that disa .owed deductions for mainte-

made by a corporation for the personal ben- decided that the rent-free use of corporate

nance costs and depreciation on three resi-

efit of its stockholders, or the making avail- property by shareholders 's properly classi-

dential properties occupied by the

able of corporate-owned facilities to stock- fied as a constructive dividend."); Daniel M.

corporation's shareholder and members of

the family were instead taxab e dstributions holders for their personal benefit, may result Schneider, "Characterization and Assignment

from the corporation to its shareholder to in the receipt of a constructive dividend."). of Corporate and Shareholder Income," 14 N.

the extent the disallowed deductions exceed- 43 Elkins, "Tax Consequences of Sharehold- III. U. L. Rev. 133 (1994) (citing the 1958 deci-

ed rents paid), aff'd sub nom. Transport Mfg. ers' Rent-Free Us of Corporate Property," 5 sion, but calling it "questionable").

& Equipment Co., 434 F.2d 373, 26 AFTR2d FIU L. Rev. 41(2009) 45 Fillman, 355 F.2d 632 (Ct. Cl., 1966); Estate

70-5556 (CA-8, 1970) (affirming that deduc- 44 Id. (note 14 of that article lists numerous cases of Swan, 247 F.2d 144 (CA-2, 1957); Stran-

tions were properly denied on one of the three in which shareholder use of corporate prop- gi, 417 F.3d 468 (CA-5, 2005), aff'gTCM 2003-

properties; holdings with respect to other two erty is found to be a constructive distribution). 145.

properties not appealed). There are three cases going back to 1934, 46 It would also be helpful if the corporation Is

39 IRS Field Service Advice Memoranda are non- 1940, and 1958 n which courts held that the funded with cash and purchases the U.S. real

binding, taxpayer-specif c rulings furnished rental value was properly treated as a gift from property, rather than the real property bemg

by the IRS National Office issued in response the corporation to the occupying sharehold- contributed to the corporation. In the former

to requests made by IRS officials in the field. ers. As stated above. the IRS has indicated situation, there is no transfer of a U.S. s tus

49 The FSA also noted that if the use of the asset that corporations generally do not make gifts. asset that could, even in theory, result in estate

was compensation to the majority sharehold- See supra note 37 In addition, commenta- tax inclusion under Section 2036.

ESTATE PLANNING APRIL 2014 VOL 41 NO 4

and profits. This suggests that a a U.S. subsidiary that has no other ration holding U.S. real property

U.S. corporation used for this pur- income or assets), rent-free use of will need to fund expenses associ-

pose should be a single-purpose corporate-owned real property ated with the property (taxes, insur-

holding entity, with no other assets, need not have any adverse U.S. ance, etc.). These expenses could

and should not be included in any income tax consequence. be financed by capital contribu-

consolidated return with other U.S. There may, however, be some tions or loans by the shareholder,

corporations that could generate risk that the IRS could argue that or they could be financed through

earnings and profits. a shareholder's failure to pay rent rental payments. If the corporation

for U.S. real property held by a cor- collects rent for the property, it can

poration could be a retained inter- claim deductions for depreciation,

est in the property, resulting in insurance, utilities, and other

inclusion of the property in the tax-

Although the expenses that would not be

balance of able estate of a deceased nonresi-

deductible if the property were used

this article is dent shareholder. Section 2036 pro-

solely for personal purposes.

dedicated to the vides that the gross estate includes

corporate holding These deductions could result

the value of property transferred

structures, without adequate consideration by in a net tax loss to the corpora-

Exhibit 1 includes tion, particularly if the nonresident

a chart of various the decedent by trust or otherwise,

under which he or she has retained shareholder uses the property for

real property

holding structures, the right to designate the persons only portions of the year (as opposed

including their who will possess or enjoy the prop- to paying a full year's rent). Those

advantages erty or the income therefrom. Sec- losses can be carried over into future

and potential tax years and be used against net

tion 2038 provides for inclusion in

disadvantages.

the gross estate of the value of prop- income arising in those later years,

If the U.S. corporation had no erty transferred by trust or other- including gain on the sale of the

earnings and profits, a constructive wise, where enjoyment thereof was property. As a result, the overall U.S.

distribution would reduce the for- subject at the date of decedent's income tax resulting from the cor-

eign corporation's basis in the stock death to any change through the poration's ownership of U.S. real

of the U.S. corporation. At some exercise of a power to alter, amend, property could actually be lower if

point, the basis in the stock could revoke, or terminate. the nonresident shareholder paid

be reduced to zero so that future Some practitioners have raised rent for the periods of time that he

constructive distributions would concerns that the IRS, emboldened or she used the property.

be gains taxable as ECI and subject by its recent successes in litigating Payment of rent would also

to FIRPTA withholding (because cases involving family limited part- avoid the risk that the IRS could

the U.S. corporation is a USRPHC). nerships, might launch a similar assert that the rent-free use of cor-

It could be a long time before that attack against foreign corporations porate property was a constructive

would happen, though, and the holding U.S.-situs assets used for distribution potentially subject to

property might be sold before then. personal purposes. There are, how-

U.S. income tax or a retained inter-

Moreover, if the U.S. corpora- ever, no cases or rulings to date

est in the property potentially sub-

tion were liquidated following a applying either Section 2036 or

2038 to that situation. 45 There- ject to U.S. estate tax. It would be

taxable sale of all of its U.S. real

property, there is no authority for fore, this potential concern does not prudent to run projections for rev-

taxing the foreign corporation on appear at this time to justify the pay- enue and expenses of the corpora-

the liquidating distribution, even ment of rent, so long as the corpo- tion before having a nonresident

if the foreign corporation's basis ration observes corporate formali- shareholder pay rent, but under the

in the stock of its U.S. subsidiary ties so as not to be treated as the right circumstances, payment of

is zero or near zero. This suggests nonresident shareholder's alter ego.46 rent by the corporation's share-

that with the right structure (i.e., On the other hand, the payment holder could be a tax efficient way

a foreign corporation holding the of rent by the shareholder may offer to fund the expenses of owning the

real property directly or through a planning opportunity. A corpo- property. •

Ar9 I 201.1 VQ3 41 ! NO 4 4- 01REIGN•OWNE RUAI I5TATEYou can also read