From field to fork: The value of England's local food webs - Click to enter - CPRE

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Click to enter > From field to fork: The value of England’s local food webs

< Previous Next > Contents Foreword by Monty Don 1 Summary 2 Introduction 6 About the research 7 National map of locations surveyed and main local supply chains 8 Defining local 10 Context 12 Characterising local food webs 20 Main findings 36 Local food and the local economy 37 Local food and the local community 49 Local food and the local environment 55 Local food and local planning policies 58 Main recommendations 60 Conclusion 64 Endnotes 66 Summary of mapping locations 69

< Previous Next > Return to contents

Foreword 1

Foreword

by Monty Don

It is a sign of our increasing separation from nature that we are losing

sight of where food comes from and how it is produced. The way we buy

it adds to this alienation. Food, once at the heart of towns and communities,

integral to their rhythm and reason, is often now a side show. It is sold in big

boxes on the edge of town. Much of what we buy is highly processed, over-

packaged, branded but anonymous, transported from anywhere available at

any time. It is hard to remember that these ‘food products’ come from plants

and animals, and are a result of myriad complex interactions of seasons and

soil, and from the toil of real people.

An important message of this report, and its companion reports from across

England, is that this direction of travel isn’t complete. It doesn’t have to be

a final destination. There still remain networks of producers, store and stall

holders established in their communities supplying the best fresh, local and

seasonal food. These ‘local food webs’ keep alive links to the recognisable

places and landscapes where food is grown, raised or made. The businesses

they support keep towns and nearby countryside diverse and distinctive.

They are rooted in place and linked to real, meaningful landscapes.

The 800 retailers and more than 1,700 producers identified in this project

show the diversity of these networks and the abundance they offer: from

Cheshire apple juices to Sussex fisheries, from Kent hops to Northumberland

vegetables, and from Cumbrian lamb to Devon beef. They, and many more Local food is a powerful way to

such networks and thousands more such businesses, are supplying food in form our own connections to

ways which bring people closer to the land through community farms and the land, landscape and nature

farmers’ markets, school meals and urban food growing, as well as in

traditional shops and markets.

But this report is an urgent call for action. In too many places these

networks are struggling to survive. The odds are stacked against them.

They must compete against the dominance of the big supermarkets, the

erosion of town centres with the corresponding loss of diversity of outlets

and small-scale producers and the disappearance of food from living streets.

These trends continue to change and challenge the way our towns and

countryside work and feel and the way our food is produced. They threaten

the diversity of the farming system and they force up the scale at which

farms can survive and rewrite how the land is managed.

There are many recommendations here of how we can support local

food. Government must fully support these food networks in its policies and

guidance. Equally local councils must build partnerships with businesses from

retailer to producer and their customers to nurture and grow local food webs.

But we too, as individuals and as consumers, make important choices which

shape the food system where we live. Local food is a powerful way to form our

own connections to the land, landscape and nature. It is a chance to enjoy

seasonal produce, to discover the best, most wholesome and freshest food

around and the most distinctive varieties and tastes. It is our chance to

support a food network that is rich with variety and diversity and meaning.

It is a chance we need to seize.

From field to fork: The value of England’s local food webs

< Previous Next > Return to contents

Summary 2

Summary

This report presents findings and recommendations

from a five-year national project – Mapping Local

Food Webs – to engage local volunteers across England

to research their local food ‘webs’: the network of links

between people who buy, sell, produce and supply

food sourced locally.

The project builds a picture of local and its main ingredients, grown or

food webs, their character, benefits,

the challenges faced and the impact

that these networks have on people,

produced within 30 miles of where

it was bought. For all locations,

outlets were in a core study area of

61,000

their livelihoods and the character of a 2.5-mile radius circle centred on a Estimated number of jobs

their town and local countryside. town or city. Producers based within across England due to local

This report brings together findings a 30-mile supply zone beyond this food sales to shoppers

from 19 locations to describe local food were counted as local.

webs in national terms. We have

collated qualitative and quantitative Main recommendations

data from interviews in all locations

to generate combined statistics and

These recommendations are for

the Government, local authorities,

16.3

shared themes and issues. The report food retail businesses, local million

considers the scale and economic communities and individuals.

importance of local food webs in terms Further recommendations appear Number of customers

of jobs supported, turnover of outlets across the report. English local food outlets

and supply chain businesses, and 1 – Government should develop the could serve each week

also their social and environmental competition policy framework to

importance. We include analysis of the better support retail diversity and

challenging context in which these food entry to markets of new local food

webs operate including current policy.

We draw conclusions about how policy

entrepreneurs by preventing further

market concentration which could £2.7

change and actions can enable local act as a barrier for small and medium- Billion

food webs to grow and thrive for the sized businesses.

long-term future. 2 – Government should develop Potential annual sales

national planning policy guidance from independent local

Definition of a local food web and to provide stronger support for a food outlets in 750 towns

local food sustainable food system by showing

For the project we defined: how planning can promote and protect

across England

• a local food web as the network of the infrastructure and assets needed

links between people who buy, sell, to buy, grow, produce and distribute

produce and supply food in an area. local food.

The people, businesses, towns, 3 – Government should strengthen

villages and countryside in the the ability of the planning system to

web depend on each other ensure the vitality of town centres by

• local food as raw food, or lightly enabling local authorities to set

processed food (such as cheese, conditions on the location, scale and

sausages, pies and baked goods) accessibility of retail as well as to

From field to fork: The value of England’s local food webs

< Previous Next > Return to contents

Summary 3

restrict the dominance of particular high levels of seasonal local food and turnover; by comparison at three

operators in local market areas. persuading others to do so. national chains one job is supported

4 – Government should provide per £138,000 to £144,000 of

strong leadership on sustainable Key findings annual turnover.2

food procurement by setting Local economies

challenging long-term targets for For the 19 locations surveyed combined Local food webs have other important

food procurement for its Whitehall our analysis shows that: economic benefits:

departments, agencies and other • local food sales through independent • distinctive, fresh local produce gives

non-departmental public bodies outlets support total turnover of £132 outlets a strong selling point

to increase food supplied from million a year; over half – £68 million • outlets contribute to the character of

sustainable sources. – can, we estimate, be attributed market and other towns, drawing

5 – Local authorities and other public directly to local food sales visitors and food tourists

bodies should form partnerships in • local food outlets support over 2,600 • networks of local outlets reduce risk

their areas to develop food strategies jobs full-time and part-time of which for producers of relying on fewer

and action plans. over 1,500 can be attributed directly larger contracts

6 – Local authorities updating their to local food sales • they offer markets for smaller

local plans in the light of the • there are 2,000 supply chain businesses producers (69% were micro-

National Planning Policy Framework providing locally sourced produce businesses and 28% small businesses)

(NPPF) should develop policies to to these locations supporting total • local food webs are vital seed beds

support local food networks by turnover of an estimated £718 for innovation and new enterprises

building on NPPF policies on retail million a year and employment of trialling products.

diversity and town individuality, support 34,000 people.

for markets and protection of fertile land. Local communities

7 – Businesses within local food Nationally, based on extrapolations Across the 19 locations surveys showed:

networks should work together to from data from all locations, we • local food outlets serve 415,000

promote awareness, access, broadly estimate: customer visits weekly; nationally,

affordability and availability of local • local food sales in some 750 towns across England such outlets could

food by developing a clearly defined across England through independent serve, we estimate, 16.3 million

‘local’ brand, developing shared delivery outlets (including social enterprises customers a week

and distribution services, and and co-operatives) could currently be • national supermarket chains

considering extended opening hours. £2.7 billion a year dominate grocery spending

8 – Supermarket chains should set • these outlets are supporting over (77% of all main shopping trips)

themselves demanding targets for 103,000 jobs (full-time and part- • shoppers gave convenience (44%),

stocking more local food in ways time), of which over 61,000 can be proximity/location (36%) and price

which reinforce trust in local food by attributed directly to local food sales.1 (24%) as the main reasons they

stocking fresh, seasonal local produce, • money spent in local food networks use supermarkets

clearly defining local food, minimising will be re-circulated within the local • despite this dominance of chains,

transport and committing to equitable economy for longer: it could be local independent stores and markets

trading with local food producers. contributing £6.75 billion of total matter to shoppers: one fifth of

9 – Community groups should engage value to local economies shoppers used independent stores

in initiatives to shape their local food • pound for pound, spending in for all or part of their main shopping;

networks such as food partnerships, smaller independent local food they account for 60% of extra or

neighbourhood planning, food web outlets supports three times the ‘top-up’ shopping visits

mapping and community food growing. number of jobs than at national • the main reasons for using

10 – Individuals can and should act grocery chains: outlets selling smaller independent stores were:

to change the way our food system significant to high percentages of quality/freshness/taste (46%),

works by shopping at a wide variety of local food support on average one specific products (32%) and local

outlets, supporting those that stock job for every £46,000 of annual produce (19%)

From field to fork: The value of England’s local food webs

< Previous Next > Return to contents

Summary 4

• shoppers’ main reasons for buying way, and should be built on to convey

local food were: supporting local

farmers and producers (56%); quality

(54%); supporting the local economy

the wider environmental benefits of

local food. 34%

(51%); taste (41%); food miles (34%); There are other environmental benefits: Percentage of shoppers

value for money (19%); seasonal • local goes hand in hand with seasonal seeing cutting food miles as

food (19%). food and reinforces an understanding a key reason to buy local

of seasonality; it helps people to buy

Local food webs extend choices of food that needs less energy to produce

where to buy the freshest, high quality • local food needs less packaging

food and enable people to shop to

support local producers and the local

than food needing protection during

long-distance journeys

£6.75

economy, to reduce food miles and to • local food supports the viability Billion

eat seasonally. of independent outlets which keep

Short supply chains also mean buildings in use; especially in Estimated total value of local

closer connections to where food comes historic market towns this maintains food spending re-circulating

from and support an awareness of character, individuality and sensitive in the local economy

seasonality and the realities of food scale of use

production. Benefits also come from • local food webs underpin local

outlets selling local food being smaller diversity in the scale and type of

local shops anchored in their local

community: acting as social hubs;

farming in the area from livestock to

cheese to fruit cropping; they support £718

offering personal service and often

informal support for the elderly and

genetic diversity in traditional and

rare breeds, heirloom and heritage

million

less mobile ; and supporting a wide varieties not suited to large-scale Estimated annual turnover

range of very local good causes through processing and distribution systems. of local food suppliers

donations, gifts in kind, sponsorship

and advertising. The scale and character of local

we researched

food webs

Local environment This national project provides for the

• The concept of ‘food miles’ resonates first time strong evidence from across

with shoppers and businesses: 34% of England of the scale and attributes of

shoppers gave reducing food miles as local food webs. It confirms aspects of

a main reason to buy local food; local food networks that many people

numerous food web businesses cited instinctively understand. In certain

it as an advantage of local food linked towns – such as Ledbury, Otley, Penrith

to lower transport costs, freshness of and Totnes – there are relatively high

produce and less pollution. Local food numbers of outlets selling local

webs show producers across many produce, a large number of suppliers

locations clustered within 10-15 miles and good availability. For their size,

of outlets. Food miles indicate closer local food supports a relatively high

connection to food provenance as number of jobs and turnover in and

much as distance travelled. around these towns.

• The scale of environmental challenges On average across all locations the

Local food webs capture the

can prevent people believing they highest levels of local produce are

can make a difference. The food miles found at farmers’ markets and farm interactions between those

concept helps shoppers to change shops as expected, but also at butchers. who produce and buy food

their habits in a meaningful, intuitive They are closely followed by bakeries, from farmer to shopper

From field to fork: The value of England’s local food webs

< Previous Next > Return to contents

Summary 5

general grocers and fishmongers with sales and collapse of high street chains should enable better enforcement of

high levels (50-75%), and delicatessens, have accelerated town centre decline. equitable supply chain relationships.

greengrocers and street market stalls Further store closures are forecast. But with the NPPF failing to strengthen

with significant levels (above 25%). town centre planning policy, ‘business

These traditional stores, some in Farming context as usual’ seems likely.

markets, are vital to thriving food webs. Farming, often undervalued, supports

Excellent farm shops and farmers’ the food chain, a major employer and Conclusion

markets can help increase access part of manufacturing and service Local food networks can address the

where such stores are few but generally industries. But the sector faces major range of challenges set out here in three

where traditional local shops have challenges. These include population important ways:

disappeared there are smaller networks growth, demand shift, climate change • by contributing to the strength of

of local producers and less varied local and resource depletion. Farming must smaller outlets, maintaining the

produce available. National supermarket produce more with fewer resources. attraction of town centres through

and some regional chains were present The food chain from farming to local food and contributing

in all locations. In the main, research domestic consumption has major towards their diversity, character

shows they do not stock a high impacts on greenhouse gas emissions and the community

percentage of local food – from 0-4% in production, transport and the home. • by providing channels to market for

at most by turnover – but with a few Food has major implications for energy new and micro, small and medium-

notable exceptions. use, water use and waste, and depletion sized businesses, supporting producer

of soils. The costs of many such businesses and enabling farming to

Wider context impacts are not reflected in the price remain diverse and varied in production

Local food webs capture the of food. There are other significant and outputs including values

interactions between those who farming trends: an increase in farm size supported by consumers such as

produce and buy food from farmer to and drop in farm numbers coupled with freshness, provenance and seasonality

shopper. They link the retail system rising imports in recent decades. Fruit • by encouraging engagement of

to the farmed land. is one example of how market forces consumers with food and, through the

shaped by price and supermarket power human scale and connection within

Retail and town centres have undermined domestic production. local food networks, enabling

Supermarkets have risen to dominate shoppers to understand the realities,

food retail and their growth has seen Land-use planning challenges and impacts of food

massive decline in smaller shops, Land-use planning through national production and to choose to make a

especially traditional specialist stores planning policy has a major role to difference individually and collectively.

– down from 120,000 (1950s) to 18,000 play in shaping retail development,

(late 2000s). Many such as butchers the nature of town centres and retail There is an urgent need for national

and greengrocers sold high proportions diversity. Policy since 1996 has and local government to act to put in

of local produce supplied through local sought to focus development on place the strong policy framework

wholesalers and direct to store. Their town centres to keep them vibrant. needed to protect retail diversity and

replacement by supermarkets with Despite supportive policy supermarket through it local food webs. Businesses,

(inter)national supply chains has expansion out of town and into the community and we as individuals

‘de-localised’ our food shopping. superstores has undermined centres, all have a role to play in supporting

Expansion of market share by weakened diversity and concentrated their future health.

chains has been fed primarily by ownership with fewer, larger companies.

out-of-town development of superstores These trends affect the markets for

and hypermarkets and this growth is producers. Loss of retailers has

set to continue despite recession: 44 narrowed their options. Supermarkets

million square feet of new supermarkets are able, through buyer power, to drive

with just 20% in town centres are down prices, forcing producers to scale

planned or have permission. Internet up. The Groceries Chain Adjudicator

From field to fork: The value of England’s local food webs

< Previous Next > Return to contents

Introduction 6

Introduction

Food is an essential part of our lives. It has been

central to the nature of our towns and countryside

since the beginnings of civilisation.3

Farming has shaped England’s they are below the radar. But as Carolyn

countryside over millennia: the

food it produces and the landscapes

it maintains are invaluable assets.

Steel puts it: ‘Food is all about networks;

things that when connected add up to

more than the sum of their parts.’4

30 miles

Yet the wider role of food is being The overarching aim of this report The radius around a

forgotten. A multitude of factors is to make local food webs more visible location defined as the

has changed the way we buy, and and better understood – to put them local supply area

experience, our food. The weekly literally on the map – and make clear

supermarket shop has displaced food their ability collectively to make a

from market places and town centres. difference. In so doing, we argue that

The scaling up of our stores into retail

sheds has increased standardisation of

local food networks need sustained

support from individuals, the

1,873

food. National and global sourcing and community, business and policy- Number of shoppers

increased distribution distances mean makers locally and nationally.

food has to be packaged for transit This report begins with a summary

we interviewed

and for a long shelf-life. of the research and a discussion of

This system has disconnected us the challenges of defining local food.

from our food’s origins. Plants and

animals disappear into large sheds too.

The ‘denaturing’ of food has added to

The first main section reviews the wider

context, considering national trends

in retail, pressures on agriculture,

804

our nature deficit – our decreasing and recent developments in planning The businesses we screened

contact with nature – at a time when policy, particularly for town centres. for sales of local food across

climate change and resource depletion The second main section builds on 19 locations

pose huge challenges. Farming faces the project findings to characterise

numerous challenges in an increasingly local food webs, the types of food

volatile future. At the same time, available, and business models.

recession and austerity bite and our The third main section brings

high streets are in crisis. together findings from 19 locations

These issues raise questions to form a national picture. These

about the sustainability of our food findings are divided broadly into

system. While some suggest that economic, social, and environmental

global economic and resource pressures themes, followed by analysis of local

make intensive large-scale production policies. They combine statistical and

systems inevitable, our analysis of local qualitative analysis from shoppers and

food webs suggests a different set of businesses to identify the benefits of

priorities for the future. Local food local food webs and the challenges

systems underpin the viability of they face. We set out recommendations

farming, support the economy of rural on how local food webs can be better

areas and towns, innovate and create supported and a conclusion.

jobs, build community and connections, Throughout the report we include

and enhance the countryside. The case studies which illustrate some of

businesses in these networks are most the attributes and benefits we explore

often small and dispersed. Individually or offer solutions and ideas for action.

From field to fork: The value of England’s local food webs

< Previous Next > Return to contents

About the research 7

About the research

Background

The concept of a local food web stems from

the work of Caroline Cranbrook.

In 1998 Caroline grew concerned Hastings, Darlington, Norwich and primarily through interviews with

about the impact of a proposed Sheffield. Individual mapping locations local food web businesses and other

superstore on her local market town were selected on population size (below stakeholders such as local councillors,

of Saxmundham in east Suffolk. 10,000, 10,000–30,000, over 30,000), to town centre and market managers and

She produced research to show the achieve broad coverage of the relevant local chambers of commerce.

importance of the local food network. region and where there was good Data was entered and collated at

This research suggested local food support from local community groups. CPRE National Office and analysed

networks with similar benefits existed In each location a core study area was statistically and thematically to provide

elsewhere, but further evidence defined by a 2.5-mile radius circle, findings for each location report and

was needed. usually centred on the town or urban then to generate findings reported here.

area. Beyond that, a 30-mile radius circle Case studies from location reports are

Aims of the national project was defined as the local supply area. replicated here where relevant and are

The national Mapping Local Food Webs The project employed regional based on interviews with businesses

project engaged people in researching co-ordinators to recruit and support – supplemented by desk-based research

their own local food web in up to three local volunteers to research shoppers’ – and with other stakeholders including

towns and cities in each of the eight attitudes to local food, identify and volunteers, food activists, town and

English regions. The project was interview outlets selling locally sourced market managers and planners.

developed with support from Sustain food in the core study area, and For detail of the mapping research

and received funding for 2007 to 2012 interview a sample of their suppliers. process for individual locations see

from the Big Lottery Fund through the Co-ordinators carried out survey work Field to Fork location reports.

Making Local Food Work programme. alongside volunteers. Open public

The project aimed to: meetings and workshops were held to

• increase the local community’s involve and consult local residents and

understanding of the size and businesses, to raise awareness of issues,

importance of their local food web to gather information on barriers and

and its impact on local people’s lives, opportunities, and in several locations

livelihoods, places and the countryside to verify findings and explore actions to

• explore the relationships between support local food. Report writers and

what people buy and eat and the volunteers researched case studies

character of their town and the

surrounding countryside

• build support for greater local food Shopper surveys, business interviews and public meetings

production and better supply in

local outlets Engaging the local community Talking to businesses

• strengthen and secure local food webs Numbers of local Number of businesses screened in 19

across the country through local and volunteers involved: 262 locations (for sales of local food): 804

national action and policy change. Numbers of shoppers Number of outlets interviewed: 403

interviewed: 1,873 Number of supply chain businesses

Overview of project activities Number of public meetings held interviewed: 219

The project explored 19 locations from (launch meetings/workshops): 52 Number of case study interviews: 102

2009. These included markets towns Number of people attending and

such as Totnes, Ledbury and Penrith contributing views: 1,735

and larger urban areas including

From field to fork: The value of England’s local food webs< Previous Next > Return to contents

Maps 8

Map of locations surveyed and

supply chain links identified

KEY

Supply chain links

Boundary of local food supply area

Area of Outstanding Natural Beauty (AONB)

Hexham National Park

Settlements

Penrith

Darlington

Otley

Burnley

Sheffield

Knutsford

Newark on Trent

Norwich

Shrewsbury

Birstall

Reproduced from Ordnance Survey digital map data © Crown copyright 2012. All rights reserved. Licence numbers 100047514, 0100031673.

Kenilworth

Ely

Ledbury

Faversham

Yeovil Haslemere Hastings

Totnes N

0 20 40 km

Map Scale @ A3: 1:2,000,000 W E

S

From field to fork: The value of England’s local food webs< Previous Next > Return to contents

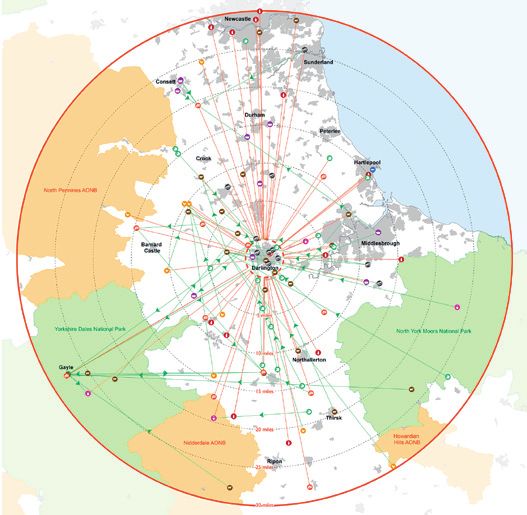

Maps 9

Local supply chain

into Darlington

Contains Ordnance Survey data © Crown copyright and database right 2011

N

W E

S

Core study area and location of main

local food outlets in Darlington

KEY

Meat/processed meat

Fruit/vegetables

Dairy

Cereals

Eggs

Fish/shellfish

Drinks

Preserves

Baked goods

Other

Supply chain link

Multistage supply chain link

Boundary of core study area

Boundary of local food supply area

Area of Outstanding Natural Beauty (AONB)

National Park

Settlements

From field to fork: The value of England’s local food webs< Previous Next > Return to contents

Defining local food 10

Defining local food

The term ‘local’ is deceptively simple. It is used widely

and loosely but in many ways which defy definition.

Take the example of the local shop: Defining ‘local food’ area to be processed and packaged

surely a shop close to home. But There is no legal definition of local food elsewhere – sometimes exported to

how close is close, and how distant is in use, except reference in a relatively do so – then transported to regional

not local? Setting a boundary is more obscure EU regulation on food hygiene distribution centres before being

difficult than it seems and depends on for animal products.9 The Policy delivered to the store where it is sold.

context: a rural local shop may be in the Commission on the Future of Farming This means food produced within a few

next village several miles away; in town and Food, set up by the UK Government miles of a store may have travelled

it might be at the end of the street. in 2002 to advise on a sustainable hundreds of miles to get there.

Local can also be set against much future for the food and farming sectors

larger geographical areas – regional, in England, stated in its 2002 report Different modes of defining

national or global. that ‘once local food becomes more ‘local food’

Local can also mean different things established, DEFRA, the Food Standards Local food has nevertheless been

to different people, and is used in Agency and FFB [Food from Britain] will defined in a number of ways which are

different ways depending on the need to devise an enforceable definition relevant to our project. Kneafsey et al.

purpose. In terms of food, there has of “local” [as] a necessary first step for define three overlapping modes to

been a rapid growth of interest in local the full benefits of local branding to be which a fourth (d) is added below.13

in recent years. Farmers’ markets, realised.’10 However, FSA research

community-supported agriculture, showing that consumers have differing (a) Local food defined according to

vegetable box schemes and local food views on the meaning of ‘local food’ led product, process and place attributes

festivals have mushroomed across the them to conclude that it would not be This definition attributes particular

country. These support a natural and possible to provide a definition for foods to a district or geographical area,

simple association of local food and regulatory purposes.11 based on special attributes such as

proximity – geographical closeness – There are further barriers to soils, topography, climate, local skills

and are represented by businesses and establishing a tight definition of and knowledge. The best-known

initiatives rooted in the area. However, local food, particularly for legal or example is the French Appellation

supermarkets, operating nationally and certification use. Food production d’Origine Contrôlée system, now

internationally, now reserve shelf space systems ‘can consist of complex extended across the EU via the

to sell popular local or regional foods; networks of relations stretched over Protected Designation of Origin (PDO)

in some cases a region or country can a variety of spatial scales’: even for and Protected Geographic Indication

be described as a ‘local’ source.6 Where simple commodities many of the (PGI) systems. UK products covered

the boundaries lie between a local area resources required to produce them – include Melton Mowbray pork pies,

and the next scale up is open to debate, seeds, fertiliser, pesticides, machinery Yorkshire Triangle rhubarb and

and ultimately depends on the context – are likely to be produced in many West Country Farmhouse Cheddar.14

and the uses to which any definition is different places.12 While few would The regulations are legally binding,

put.7 Research for the Food Standards claim that all such inputs need to which protects small producers from

Agency (FSA) found that consumers or could be locally produced, the imitation and consumers from

also interpret the term differently importance of the issue is clear when deceptive claims. These products do not

with 40% of respondents seeing it as Brazilian soybeans – a driver of have to be sold locally, which shifts the

within a 10-mile radius, 20% within Amazonian deforestation – may be definition away from point of sale.

the same county, 20% from a number used to fatten chicken, pork or beef sold

of neighbouring counties and 20% as ‘local’ in the UK. This complexity is

from a region.8 compounded by distribution systems

which, for economic and logistical

reasons, require food produced in one

From field to fork: The value of England’s local food webs< Previous Next > Return to contents

Defining local food 11

(b) Local food produced, processed Association, a sustainable local food Defining ‘local food webs’ in

and retailed within a defined radius economy is ‘A system of producing, the project

Definitions based on distance (usually processing and trading, primarily of While the definition of local food

within 30 miles) or geographical area sustainable and organic forms of food remains unresolved, this project needed

(such as a county) have an appealing production, where the physical and a working definition for survey work to

simplicity. In England CPRE has economic activity is largely contained proceed. The academic review which

promoted a definition of local food as and controlled within the locality underpinned our research described

food produced, grown and processed or region where it was produced, local food webs as ‘networks of

within 30 miles of the store. This which delivers health, economic, relationships between food producers,

distance has also been adopted by a environmental and social benefits to processors, retailers and consumers

number of large retail chains including the communities in those areas.’15 which deliver economic, social and

Waitrose, Asda, Booths and The Sustain’s definition incorporates environmental benefits within a defined

Cooperative. Tesco uses a county or similar criteria such as proximity, geographical radius’.19 This combines

neighbouring county definition. The fair or co-operative trade, and being concepts b) and c) above. It also

National Farmers Retail and Markets environmentally beneficial or benign.16 recommended defining the scale of a

Association (FARMA) has developed this Research in the US for Congress also retail study area and local area for food

definition into a set of certification suggests the category of ‘local’ based supply. This conceptual understanding

criteria for farmers’ markets to protect on attributes ‘mostly based on supports the final definitions used in

their integrity. It uses 30 miles as the consumer perceptions of certain the project. To ensure the research

ideal radius, but this can be stretched desired social or supply-chain remained practical for volunteers as

to 50 miles for larger cities, or coastal or characteristics in producing “local” well as enabling CPRE to quantify

remote regions, with 100 miles as the foods, such as production by a small and compare the importance of food

maximum recommended. FARMA also family farm, urban farm or garden, or webs in different areas, the standard

recognises distinct geographical areas farm using sustainable agricultural definitions below were used across

such as counties and National Parks. practices’.17 These factors link to many all locations.

others which influence demand for local

(c) Local food that delivers food, such as quality and freshness, Project definitions

certain benefits traceability, supporting the local Our research was based on:

Sustain and The Soil Association have economy and environmental impacts. • a core study area for researching food

developed definitions based on criteria outlets, based within a 2.5-mile radius

related to food’s social, environmental (d) Local based on type of outlet circle from the centre of the location

and economic benefits. For The Soil The US Congress research above goes • a local supply area, covering a 30-mile

on to suggest a further definition based radius circle beyond this.

on type of outlet. This is where ‘local’

refers to the ‘types of marketing A local food web is the network of

channels used by farmers to distribute links between people who buy, sell,

food from the farm to the consumer’. produce and supply food in an area.

This lists ‘direct-to-consumer outlets’ The people, businesses, towns, villages

such as road-side stands, on-farm and countryside in the web depend on

stores (farm shops), farmers’ markets each other, and this interdependence

and community-supported agriculture benefits livelihoods, quality of life and

(CSA), and ‘intermediated outlets’, the quality of places.

Sourced within 30 miles – such as grocers, restaurants and This project defined local food as

regional distributors.18 raw food, or lightly processed food

definition of local food used (such as cheese, sausages, pies and

by Asda, Booths, CPRE, East baked goods) and its main ingredients,

of England Co-op, FARMA grown or produced within 30 miles of

and Waitrose where it was bought.20

From field to fork: The value of England’s local food webs< Previous Next > Return to contents

Context 12

Context

Local food webs are about connections: the interactions between

those who buy, sell and produce food, and the relationship

between where food is produced and where it’s consumed.

The concept goes beyond that of a the grocery chains: the Competition (excluding co-ops, discount groups

supply chain to look at the retail Commission found that ‘the number and independents) operated some

system, and food’s wider impact on the of larger stores [over 2,320m2] located 8,400 stores, including over 5,400

quality of places, the environment and out-of-town increased from just under supermarkets (over 3,000 square feet).24

community life in both urban and rural 300 in 1980 to more than 700 by 1990 Further research by commercial

areas. Because of the breadth of the and to almost 1,500 in 2007’.22 property adviser CBRE reported in

idea, many factors in the wider national The net effect has been to move late 2011 that this expansion is set

and international context are relevant shopping out of towns to their margins to continue well into the future with:

to local food webs. or elsewhere, as well as to increase • almost 4 million square feet of

car-based shopping. This scaling up new grocery retail space under

Retail and town centres by national chains with access to construction

The ‘death of the high street’ high levels of capital leaves smaller • planning permission already given

The state of the nation’s high streets is independent stores – which to national chains for another 21.4

the subject of much media coverage proportionately sell much higher levels million square feet

and an area of great concern. The 2000s of local food – losing trade, as town • applications submitted for a further

saw the economy buoyed by a retail centres where they operate struggle 19 million square feet

and house-price boom – and rising to compete. • more than 80% of new space in

debt. With the 2008 crash, growth out-of-town developments.

turned to recession. Other trends The expansion of the supermarkets

affecting how, where and when we shop Supermarkets have expanded in other This 44 million square feet (4.01 million

are well analysed in the Portas Review. respects. Firstly, the number of stores m2) of projected development is

Portas recognises that the nation’s high operated by the national grocery equivalent to 1,635 new superstores

streets are changing in multiple ways.21 chains has continued to grow rapidly (at 2,500m2).25

across all scales – convenience Secondly, the market share of the

The growth of out-of-town shopping stores, supermarkets, superstores multiples has escalated. Competition

A key trend over the past three decades and hypermarkets. BBC research for Commission statistics show the market

has been the development of ‘supersize’ Panorama in 2010 gave an overview of share of ‘large or regional grocery

regional shopping centres, often the expansion of supermarket stores of retailers’ expanding from 20% in 1950

heralded as drivers of regeneration and the ‘big four’ (Tesco, Asda, Sainsbury’s, (estimated) to 44% by 1971 to 85%

retail growth. These may be out-of-town Morrisons) from 2004 to 2010, by 2007.26 Most recent 2012 figures

centres (Lakeside in Essex, Bluewater in shown below.23 In 2012, the multiples indicate supermarket chains account

Kent), or developed within urban areas

(such as London’s newest Westfield Table A: Number of supermarket stores

shopping centres at White City and

Stratford). Both represent a challenge to Location (by postcode) 2004 2010

existing town centres and high streets.

Birmingham 19 104

These are complemented in many

towns and cities by the move to Bristol 19 76

out-of-centre stores and retail parks,

Cleveland 7 59

which have enabled retailers to expand

massively from relatively constrained Nottingham 12 82

town centre sites into superstores. In

Sheffield 16 104

the vanguard of this trend have been

From field to fork: The value of England’s local food webs< Previous Next > Return to contents

Context 13

for 97-98% of grocery sales, with the stores mentioned above and of can bring a vicious cycle: stores close

‘big four’ around 75-76%.27 e-commerce. The decline in spending down, leading to still lower footfall,

Thirdly, buildings have become on the high street as a percentage of leading to further store closures. Fewer

physically much larger. Between 2006 total retail spending illustrates the shops and shoppers in town centres

and 2010, Tesco increased the number long-term nature of the problem: may weaken traditional specialist food

of its Extra hypermarkets (above 60,000 from 49.4% in 2000 to 42.5% in stores – butchers, greengrocers,

sq ft) by 50%, from 118 to 177.28 Huge 2011, to a projected 39.8% by 2014.31 fishmongers and markets, many of

superstores have appeared not only in Conversely, though not seen as a sign which are key outlets in local food webs.

large urban centres but attached to of resilience, new outlets have been The trend to e-commerce in food is

small market towns, where they can opening: noticeably convenience food most obviously seen in the move to

dwarf the existing retail offer. For stores, supermarkets, charity shops, online ordering for home delivery by

example, Hexham, Northumberland pawnbrokers, pound shops, credit the likes of Ocado, Waitrose, Tesco and

(population 11,000), has a Tesco Extra unions and shoe shops.32 The overall Sainsbury’s. Potentially more positive

store which accounts for 45% of all impact of this decline is fewer shoppers, for local food is the growth of weekly

main shopping trips in the Tynedale spending less. Town centres lose their box schemes. There are many smaller

district. Kingsbridge, Devon (pop. 6,000) attractiveness to high-spending such schemes but the major market

has recently acquired a 3,700m2 shoppers, leaving those who are less share belongs to Abel & Cole and

superstore and Blandford Forum in mobile or cannot afford to travel to cope Riverford. Riverford currently delivers

Dorset (population 9,000) awaits a with a declining centre. Their shopping around 40,000 boxes of organic fruit

4,066m2 superstore development.29 choices are limited further. and veg a week in the UK from regional

Fourthly, the grocery multiples have Recent research by Deloitte farms. Riverford advertises that it does

expanded from convenience (everyday) suggests further significant reductions not air freight and has a strong emphasis

goods into comparison goods – items – ‘by as much as 30-40% are foreseeable on seasonal and local, though how

such as homeware, stationery, flowers, over the next 3-5 years’ – in the portfolios much would meet our project definition

books, electricals, pharmacy products of stores held by retailers, a rate of loss (sourced within 30 miles) is not clear.37

and clothes as well as fuel. It is well likely to seriously damage already

known that Tesco takes £1 in every £8 fragile town centres.33 Other changes

of total retail spend in the UK but Related – directly and indirectly –

Sainsbury’s is now the seventh largest Fundamental changes to the way to these significant changes in town

clothing retailer by volume.30 Shoppers we shop centre retail are other trends. Recent

may be left with little reason to visit the There has also been a marked shift to decades have seen steep declines in:

town centre, threatening a whole range online shopping, or e-commerce, which • traditional specialist shops –

of outlets. As the centre declines, is likely to continue to grow rapidly: smaller stores have been disappearing

smaller shops find it increasingly hard internet sales of all goods have doubled since before the meteoric rise of

to compete and traders disappear, since 2000 from 5.1% to 10.2% – and supermarkets, but there seems little

leaving less choice, not more. even this may be an underestimate, doubt that competition from chains

according to the Local Data Company.34 has weakened and subsequently

The decline of town centres They anticipate internet sales could caused the closure of thousands of

The recent recession has led to reach 12.2% by 2014 and 20% by independent shops, including

widespread failure of high street 2020. Shopping on mobile devices butchers, greengrocers, bakeries,

businesses, including household names (m-commerce) is another emerging off-licences and fishmongers,

such as Woolworths, Barratts, Focus DIY, trend: BIS data indicates a growth of permanently changing the character

Comet, Peacocks, Habitat and Clinton over 500% in the past two years.35 of many if not most towns

Cards. Town centre vacancy rates None of this analysis considers food • pubs, which were closing at a rate of 40

average 14% nationally, though they retail as a discrete category, but there a week in 2009 and 25 a week in 201038

vary considerably. As well as the effects are clear implications. Virtual sales • bank branches and post offices –

of the recession, other trends behind reduce real footfall in town centres and over 2,300 rural post offices closed

this include the growth of out-of-town local high streets.36 The loss of trade between 1999 and 2009

From field to fork: The value of England’s local food webs< Previous Next > Return to contents

Context 14

• village stores, with an estimated 400 long about the forces which shape the challenges the global food

closing a year39 food system and the wider impact our system faces.

• traditional farm and food distribution food choices may have. But our food • Climate change will alter patterns of

infrastructure, including abattoirs, supply – and our local food webs – do rainfall, affect crop growth and the

livestock auctions and wholesalers.40 not operate in a vacuum. They depend way ecosystems function and mean

upon regional, national and global forces, more extreme weather events, causing

Scale of the food sector 41 from trade, finance and policy systems production and price volatility; this

The importance of agriculture to the to resource and environmental issues. presents ‘the challenge of feeding a

national economy is often undervalued. larger global population ... while

Around 2% of the UK workforce – Global issues – The Foresight report 43 delivering a steep reduction in

some 185,000 people – work in primary In 2011 the Government published the greenhouse gas emissions’.

production: growing crops, raising Foresight report on The Future of Food • Competition for key resources

livestock and harvesting the land and and Farming which draws on advice related to food production: pressures

sea. They supply around 60% of our from a lead expert group, several on land for food production

national food requirement, and hundred researchers as well as over 100 (soil erosion and degradation,44

contribute 7% of the £412 billion peer-reviewed evidence papers. The salinisation, desertification, use

turnover of the food supply chain – report sets out six important drivers of for biofuels, loss to development);

almost £30 billion annually.42 change which ‘will converge in the food increased global energy demand

Farming underpins the food supply system over the next 40 years’ to create leading to increased prices and price

chain, which employs more than 3.5 ‘the perfect storm’: volatility, with knock-on effects on

million people and generates £87.4 • Global population growth from the energy-intensive fertilisers and

billion in Gross Value Added (GVA). Food current seven billion to eight billion fishing costs; rapidly increasing

manufacturing and processing account by 2030 then a likely nine billion or global water demand even as aquifers

for 370,000 jobs and £78 billion in more by 2050; this will occur become depleted.

turnover; it is questionable how much particularly in Africa and will be • Changes in consumers’ values and

of this would take place without marked by movement from rural to ethics, which will influence policy

home-produced ingredients. Similarly, urban areas. and consumption patterns on issues

the success of many shops and • Increased demand per person linked such as national food sovereignty,

restaurants, from the humble fish-and- to rising incomes, particularly for technologies (GM, nanotechnology,

chip shop to triple-starred Michelin meat and fish in emerging major cloning), environmental sustainability

restaurants, depends on the freshness economies such as Brazil and China; and biodiversity, and fair trade and

and quality of British produce. this will increase pressure on land, social concerns.

In total, the food supply chain – water and other resources, raising

from production through processing serious questions about the The food system and

to the retail and hospitality sectors – sustainability of food production. environmental issues

accounts for 10% of UK GVA, making it • The way the food system is managed This section sets out environmental and

the fifth largest contributor to GVA. At a at national and international levels: socio-economic challenges the UK food

time when the Government is seeking issues include the globalisation of and farming system faces.

to rebalance the economy away from markets; the emergence of new food

financial services, farming and the food superpowers in BRIC nations (Brazil, Greenhouse gas (GHG) emissions

industry can play an important role, Russia, India, China); consolidation Food production, distribution and

particularly by reducing imports and of retail, food processing and consumption contribute significant

potentially exporting, in redressing the agribusiness into few very large GHG emissions globally and nationally.

imbalance in the UK’s external trade. transnational corporations; the role of Energy, mainly produced from burning

subsidies and market interventions; fossil fuels, is needed at every stage

Global food and farming issues the ability of political and of the food system: to drive farm

The plentiful supply of food in our institutional frameworks to enable machinery; to produce inorganic

shops discourages us from thinking too collective responses to the many fertilisers such as nitrates; in food

From field to fork: The value of England’s local food webs< Previous Next > Return to contents

Context 15

400 70%

Estimated number of village Amount of land area in

stores that close each year England that is farmed

manufacturing, packing, transport The loss of these and other habitats Refrigeration

and retail, particularly for refrigeration; is linked to major declines in diversity Refrigeration makes up around 15% of

in catering; for cold storage and in plants, terrestrial invertebrates and total food chain emissions in the UK, or

cooking in the home. Further sources vertebrates. At the end of the 20th 3-3.5% of the UK’s total GHG emissions.57

of emissions include methane from century, some 333 farmland species Supermarkets tend to be more energy

livestock, manure and food waste (broadleaved plants, butterflies, intensive than other food shops.58

in landfill, and loss of stored carbon bumblebees, birds and mammals) were Unlike greengrocers, supermarkets

through cultivation and degradation declining due to agricultural practices. often put fruit and vegetables in

and from cultivating wetlands. Meat Numbers of farmland birds fell by 40% refrigerated cabinets. They also tend

and dairy account for around 8% of UK between 1970 and 2000, and a further to have longer opening hours (in some

food consumption-related GHGs. 4% since. The number of bee colonies cases 24 hours a day).

Globally, agriculture causes an in England has declined by 54%

estimated 10%-12% of GHG emissions45 since 1985.52 Waste

– more if the effects of land-use change An estimated 20 million tonnes of CO2

such as deforestation are considered. Transport is associated with avoidable food and

In the EU, the figure is around 9% for The transport of food is the single drink waste in the UK each year.59

agriculture (2005 data), but nearer 31% largest energy user in the food system Waste occurs at every stage of the

for the whole supply chain from field and accounts for around 3.5% of the food supply chain – agriculture,

to fork.46 Food generates around 18% UK’s total GHG emissions.53 There are food manufacturing and packaging,

of total UK GHG emissions, and 30% also additional impacts such as distribution, retail, storage at home and

if emissions from land-use change damage to roads and verges from during preparation for consumption.

abroad to supply UK food consumption heavy goods vehicles (HGVs), noise There are opportunities to significantly

are included.47 and air pollution as well as congestion. reduce waste at every stage.

Main UK GHG emissions related to food

Biodiversity and landscape transport are UK HGVs (29%), consumer Water

In the UK the quality of the natural cars (23%), sea transport (15%), air The UK’s water footprint – the total

environment and farming are transport (12%) and overseas HGVs amount of freshwater used to produce

intimately connected. Some 70% of the (12%).54 A quarter of UK HGV movements all the goods and services in the

land area in England is farmed,48 and relate to food transport.55 Air freight country – is 102 billion cubic metres

much of the landscape is semi-natural, contributes disproportionately to total per year, equivalent to 4,645 litres per

shaped by agriculture over millennia. transport GHG emissions: only 1.5% of person per day. Agriculture accounts for

The post-war modernisation of fruit and vegetables are transported by around three-quarters of this – but 62%

agriculture has increased productivity, air, but they make up 40% of all fruit of the water we use is imported ‘virtual’

but at a heavy cost to the environment. and vegetable transport emissions. water, making the UK the world’s sixth

From 1947 to 1990, over 335,000km of Between 1992 and 2010, food air miles largest net importer of virtual water. Oil

hedgerows were lost, with 100,000km increased by 262%, although they have crops, cotton, livestock, and coffee, tea

alone from 1984 to 1990.49 Semi- recently stabilised; customer car travel and cocoa take up the largest share of

natural grasslands have suffered huge increased by 31% and urban kilometres the UK’s external water footprint.60

loss through conversion to arable since – a measure of congestion – by 26%. UK food consumption has a

the 1940s, with 90% of wildflower-rich Main reasons are people are driving considerable impact on the water

meadows lost.50 Much of what remains further to shop owing to the rise of footprints of other countries. Spain

is now protected in Sites of Special out-of-town grocery stores, increased contributes 3% of the UK’s total

Scientific Interest (SSSIs) and Special demand for overseas goods and more agricultural water footprint through

Areas of Conservation, but only 26 of transport between businesses as more exporting water-intensive products

710 areas/SSSIs on enclosed farmland processing and packaging of food such as salad crops, olives, grapes,

are in ‘favourable condition’. Pond takes place.56 oranges, rice and certain meat products.

numbers and quality have declined, Some of these are produced in water-

especially in arable areas.51 stressed regions like Almeria, where

From field to fork: The value of England’s local food websYou can also read