GIGANTE SALMON COMPANY PRESENTATION JULY 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

STRICTLY PRIVATE AND CONFIDENTIAL

GIGANTE SALMON

COMPANY PRESENTATION

JULY 2021

Private and Confidential

STRICTLY PRIVATE AND CONFIDENTIAL

CONTENTS 1. INTRODUCTION 2. MARKET OVERVIEW 3. PROJECT OVERVIEW 4. FINANCIAL INFORMATION 5. RISK FACTORS

Important information and disclaimer

THIS DOCUMENT IS NOT FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR PROJECTIONS OF THE COMPANY OR ASSUMPTIONS BASED ON INFORMATION

IN PART, DIRECTLY OR INDIRECTLY, IN OR INTO OR FROM THE UNITED STATES OF AVAILABLE TO THE COMPANY. SUCH FORWARD-LOOKING INFORMATION AND

AMERICA, AUSTRALIA, CANADA, JAPAN, HONG KONG OR SOUTH AFRICA OR TO ANY STATEMENTS ARE SOLELY OPINIONS AND FORECASTS WHICH REFLECT CURRENT

RESIDENT THEREOF OR ANY OTHER JURISDICTION WHERE SUCH DISTRIBUTION IS VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS, UNCERTAINTIES

UNLAWFUL. THIS DOCUMENT IS NOT AN OFFER OR AN INVITATION TO BUY OR SELL AND ASSUMPTIONS. NONE OF THE COMPANY OR ANY OF ITS REPRESENTATIVES

SECURITIES. PROVIDES ANY ASSURANCE THAT THE ASSUMPTIONS UNDERLYING SUCH FORWARD-

LOOKING STATEMENTS ARE FREE FROM ERRORS, NOR DO ANY OF THEM ACCEPT ANY

ABOUT THIS PRESENTATION

RESPONSIBILITY FOR THE FUTURE ACCURACY OF THE OPINIONS EXPRESSED IN THIS

PRESENTATION.

THIS PRESENTATION (THE “PRESENTATION") HAS BEEN PRODUCED BY GIGANTE

SALMON AS (“GIGANTE SALMON” OR THE “COMPANY”) FOR INFORMATION PURPOSES

ONLY AND DOES NOT IN ITSELF CONSTITUTE AN OFFER TO SELL OR A SOLICITATION OF NO REPRESENTATION OR WARRANTY

AN OFFER TO BUY ANY FINANCIAL INSTRUMENTS. BY ATTENDING A MEETING WHERE

THIS PRESENTATION IS PRESENTED, OR BY READING THIS PRESENTATION, YOU (THE THE INFORMATION CONTAINED IN THIS PRESENTATION IS FURNISHED BY THE COMPANY

“RECIPIENT”) AGREE TO BE BOUND BY THE FOLLOWING TERMS, CONDITIONS AND AND HAS NOT BEEN INDEPENDENTLY VERIFIED. NO REPRESENTATION OR WARRANTY

LIMITATIONS.

(EXPRESS OR IMPLIED) IS MADE AS TO THE ACCURACY OR COMPLETENESS OF ANY

INFORMATION CONTAINED HEREIN. NONE OF THE COMPANY, ANY REPRESENTATIVE

NEITHER THE DELIVERY OF THIS PRESENTATION NOR ANY FURTHER DISCUSSIONS WITH

ACTING ON BEHALF OF THE COMPANY, OR ANY OF ITS RESPECTIVE PARENT OR

THE RECIPIENT OR ANY OTHER PERSON SHALL, UNDER ANY CIRCUMSTANCES, CREATE

SUBSIDIARY UNDERTAKINGS OR ANY SUCH PERSON’S DIRECTORS, OFFICERS,

ANY IMPLICATION THAT THERE HAS BEEN NO CHANGE IN THE AFFAIRS OF THE

EMPLOYEES, ADVISORS OR REPRESENTATIVES (COLLECTIVELY THE

COMPANY SINCE THE DATE OF THIS PRESENTATION. THE COMPANY DOES NOT

“REPRESENTATIVES”) SHALL HAVE ANY LIABILITY WHATSOEVER ARISING DIRECTLY OR

UNDERTAKE ANY OBLIGATION TO REVIEW OR CONFIRM, OR TO RELEASE PUBLICLY OR

INDIRECTLY FROM THE USE OF THIS PRESENTATION OR OTHERWISE ARISING IN

OTHERWISE TO THE RECIPIENT OR ANY OTHER PERSON, ANY REVISIONS TO THE

CONNECTION THEREWITH, INCLUDING BUT NOT LIMITED TO ANY LIABILITY FOR ERRORS,

INFORMATION CONTAINED IN THIS PRESENTATION TO REFLECT EVENTS THAT OCCUR

INACCURACIES, OMISSIONS OR MISLEADING STATEMENTS IN THIS PRESENTATION. THE

OR CIRCUMSTANCES THAT ARISE AFTER THE DATE OF THIS PRESENTATION. THE

RECIPIENT ACKNOWLEDGES THAT IT WILL BE SOLELY RESPONSIBLE FOR ITS OWN

COMPANY DOES NOT INTEND TO UPDATE THE INFORMATION AFTER ITS DISTRIBUTION,

ASSESSMENT OF THE COMPANY’S BUSINESS AND THE MARKET, THE MARKET POSITION

EVEN IN THE EVENT THE INFORMATION BECOMES MATERIALLY INACCURATE.

AND CREDIT WORTHINESS OF THE COMPANY. THE RECIPIENT WILL BE REQUIRED TO

CONDUCT ITS OWN ANALYSIS AND ACCEPTS THAT IT WILL BE SOLELY RESPONSIBLE

FORWARD LOOKING INFORMATION AND STATEMENTS FOR FORMING ITS OWN VIEW OF THE POTENTIAL FUTURE PERFORMANCE OF THE

COMPANY, ITS BUSINESS AND THE SHARES. THE CONTENT OF THIS PRESENTATION IS

THIS PRESENTATION INCLUDES AND IS BASED ON, AMONG OTHER THINGS, FORWARD- NOT TO BE CONSTRUED AS LEGAL, CREDIT, BUSINESS, INVESTMENT OR TAX ADVICE.

LOOKING INFORMATION AND STATEMENTS. SUCH FORWARD-LOOKING INFORMATION THE RECIPIENT SHOULD CONSULT WITH ITS OWN LEGAL, CREDIT, BUSINESS,

AND STATEMENTS ARE BASED ON THE CURRENT EXPECTATIONS, ESTIMATES AND INVESTMENT AND TAX ADVISERS AS TO LEGAL, CREDIT, BUSINESS, INVESTMENT AND

TAX ADVICE.

3

01 INTRODUCTION

01 Introduction

Current progress and milestones

✓ The Ministry of Fisheries ✓ Entered into a lease ✓ Plan and impact ✓ Rødøy approves final ✓ The Norwegian Food

repealed the requirement agreement with an option assessment together with zoning plan for industry, Safety Authority gives its

for a license for land- to purchase Indre Lille Rødøy municipality land based aquaculture. permit for a production of

based aquaculture Rosøya in Rødøy started. 20,000 tons of salmon,

facilities in Norway. municipality. ✓ Plan approved by Rødøy with 13,731 tons MAB.

✓ Gigante Havbruk AS by end of the year. For the first 24 months,

(«Gigante Havbruk») the license is limited to

started the planning to 3,600 tons MAB.

realise a land based ✓ Discharge permit

aquaculture facility. granted.

✓ Final aquaculture license

approved.

✓ Equity capital raise

MNOK 65

2016 2017 2018 2019 2020

5

01 Introduction

At a glance

Gigante Salmon… …a part of the Gigante Havbruk group

▪ Gigante Salmon is a part of the Gigante Havbruk group, which is a

major player in the Norwegian aqua culture industry.

▪ Gigante Salmon will employ the management team and lead the

project. In addition to the shares of Gigante Salmon Rødøy AS, the

company owns a second island that has been acquired for future Revenue1: 603 NOKm EBIT1: 170 NOKm

development of a potential second production site.

▪ Construction on Lille Indre Rosøya is scheduled to start in the

second half of 2021 and planned production start is in 2023.

▪ The planned facility will consist of three pools with a total

production capacity of approx. 16,000 tons.

FTE: 63 Production: 10,000 tons

Projected harvest volumes HOG (tons) Favorable location on the Helgeland coast

16,000

7,000

5,000

900

2024 2025 2026 2027

1 Annual accounts 2019

6

01 Introduction

Investment highlights

1

▪ Main owner and project initiator with extensive experience in the Norwegian aquaculture industry.

EXPERIENCE ▪ Gigante Havbruk group has 30 years of experience of successful salmon farming.

▪ The group is present in the whole value chain from broodstock to export and Gigante Salmon will have access to necessary know-how.

2

▪ The design of the production site and processes builds on technology proven in conventional sea-based aquaculture.

TECHNOLOGY ▪ The concept has been dilligently designed to minimize technological risk.

▪ The site has been designed to optimise both fish welfare and economic efficiency.

3

▪ Extensive work has been put into finding the most suitable location for realising the project.

CAPITAL ▪ The production site has been carefully selected to provide a cost efficient facility, with a high level of flexibility and low CAPEX levels.

EXPENDITURES ▪ The Rødøy site enables Gigante Salmon to construct a land-based salmon farming site with industry leading capital expenditures per kilo

produced salmon.

4

▪ The demand for salmon expected to stay strong due to increased focus on sustainability and health.

PROFITABILITY ▪ No sea lice, efficient feed utilization, large capacity with intensive production and biomass optimization gives favorable costs per kg HOG.

▪ High expected profit margins creates resilience to market price fluctuations.

5

• The company will produce high quality food with a sustainable environmental footprint and creating valuable rural jobs.

SUSTAINABLE

• Land based production allows for control of water quality parameters and emissions.

PRODUCTION • Sludge from the operations will be separated off and utilised for fertilizer production.

6

▪ Financing for construction phase granted. Refer to slide 42 for details.

FUNDING IN ▪ Long term financing granted.

PLACE ▪ Overdraft facility for working capital granted.

▪ Leasing financing for work barge and machinery granted

7

02 MARKET OVERVIEW

02 Market overview

Increasing demand for healthy protein sources

Comments Population growth Global fish consumption per capita

▪ A growing global population will billion kg

increase the global demand for 20.6

21.4

10.9

proteins. 9.7

8.5 15.8

7.8

6.1

9.9

▪ Health benefits and limitations in 5.3

traditional meat production is

expected to increase fish

consumption per capita. Global

1990 2000 2020 2030 2050 2100 1960 2000 2019 2029

fisheries are to a large extent fully

exploited, meaning that the supply Resource-efficient production Climate friendly production

of wild fish has limited potential to 1000

meet the growing demand for 60 56 12.0 20 70.0

marine protein. 50 10.0 15.4 60.0

39 15

50.0

40 8.0

8.0 40.0

30 6.0 10

▪ Environmental issues are 20

19

4.0

6.0

39.0 30.0

4.3 20.0

increasingly influencing peoples 10

3.9 7 2.0

5

2.0

10.0

1.9

dietary choices. Increased fish 0

1.3

0.0 0 7.9 6.2 12.2

0.0

consumption will contribute to Salmon Poultry Pork Beef Salmon Poultry Pork Beef

Litre water / kg edible meat kg CO2 / kg edible meat

reducing global emissions. Edible Meat per 100 kg fed Feed conversion ratio

Source: Salmon farming industry handbook

9

02 Market overview

Significant growth potential for Atlantic Salmon in most

geografical markets

Market size Consumption per capita

600 9

8.2

8

500

7

6.3

6.1

400 6

Market size tons (1000)

Kg WFE per capita

5

4.8

300

4

3.4 3.3

200 3

2.7 Average

2.6 2.6

2.5

2.4 consumption

2

1.7 1.8 1.8

100 1.4

1.3

0.9 1

0.8

0.5 0.6 0.6

0.4 0.3

0.1

0 0

France

Germany

USA

South Korea

Vietnam

Italy

Taiwan

Canada

Belgium

Israel

Thailand

Chile

Spain

Brazil

Poland

Finland

Japan

Norway

UK

China/Hong Kong

Australia

Sweden

Netherlands

Russia

Sources: Kontali

1002 Market overview

Stagnating growth in traditional farming

Global Atlantic salmon supply (1000 tons GWT) Comments

3000

CAGR +3% ▪ The supply of Atlantic

salmon has increased by

CAGR +7% 7% p.a. from 2010 to 2019.

2500

▪ Due to biological and

regulatory constraints it is

2000

expected that the annual

growth rate going forward

will be reduced to 3%.

1500

▪ The increased production

1000 volume necessary to meet

increased demand needs

to come from new

500 production methods.

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020E 2021E 2022E 2023E

Sources: Kontali

1102 Market overview

Challenges in traditional fish farming

▪ Traditional open pen fish farming is constrained by availability of suitable locations.

Limited locations ▪ Area needs of new aquaculture sites creates potential conflicts with established users.

▪ New locations need adequate spacing from existing fish farms to reduce risk of spread of diseases and parasites.

▪ Water potentially carrying parasites and harmful microbes enter open pens without treatment creating vulnerability.

▪ Sea lice larvae spread between aquaculture locations and multiply quickly in pens, threatening fish welfare and resulting in

substantial treatment costs.

Sea Lice & Diseases ▪ Sea lice treatments stresses the fish and some delicing methods may be forbidden due to animal welfare concerns although

alternative treatments are not clear.

▪ High concentrations of sea lice may force fish farmers to slaughter fish early and to rotate fish farming locations to prevent build

up.

▪ Fish waste and uneaten feed is emitted to surroundings without collection or treatment.

Emissions ▪ Chemicals and medicine used for treatment of disease or parasites are emitted into local waters affecting wild sea life.

▪ Parasitic sea lice from open pen farms spreads to and threaten wild salmon populations.

▪ Farmed fish escaping from net pens can occur in extreme weather or if nets are damaged during maintenance or handling of

fish.

Escapes ▪ Escaped salmon have been shown to enter rivers during spawning season disturbing the eggs of wild salmon and

interbreeding.

▪ Interbreeding with wild salmon populations pollutes the gene pool of the salmon populations indigenous to its particular

waterways.

1203 PROJECT OVERVIEW

03 Project overview

Project summary

16,000 ~31 NOK 24 ~71 NOK ~24 NOK

tons HOG per year production cost per kg months production capex/kg HOG capex/kg HOG

HOG cycle 1/3 production full production

1403 Project overview

Gigante Salmon’s innovative production concept helps to increase

area efficiency and reduce emissions and diseases

SOCIAL

Lasting Righteous

NO SEA LICE NO ESCAPES

Sustainability

The water is collected under No escapes that could affect the

the lice larva’s habitat wild salmon population ENVIRONMENT ECONOMY

Viable

Objective

▪ Good fish welfare

PURIFICATION JOBS ▪ Social responsibility

Collected waste can be included Contributes to new green jobs in ▪ Creating a climate footprint as small as possible

in the circular economy rural areas

The biggest challenges associated with traditional salmon farming are sea lice and escapes

1503 Project overview

Gigante Havbruk is the project initiator and will own the majority of

the shares after the placement

About Gigante Havbruk group Financial performance

▪ Gigante Havbruk group was established in 1988 by Kjell Lorentsen. 700 37.7 % 40.0 %

606 603

600 35.0 %

555

▪ From humble beginnings, the group now has a fully integrated value 500

28.2 % 28.2 % 30.0 %

chain and annual revenues of 600 NOKm. 24.1 %

25.0 %

400 20.5 %

331

20.0 %

290

300

▪ The group is located in the Norwegian municipalities Meløy, 15.0 %

Gildeskål, Rødøy and Bodø. 200 171 170

125 10.0 %

114

100 70

5.0 %

▪ Gigante Havbruk group operates 7 licenses for salmon and co-

0 0.0 %

operates 4 further licences for salmon. 2015 2016 2017 2018 2019

Revenue EBIT EBIT %

Product and service offering

BREEDING SMOLT FARMING HARVEST PROCESSING SALES/EXPORT

1603 Project overview

Gigante Havbruk consists of four main segments

Corporate structure Comments

▪ Gigante Havbruk AS is owned by the

families Lorentsen and Storholm.

Fam. Lorentsen Fam. Storholm

▪ Gildeskål Forskningsstasjon AS

80% 20% («GIFAS») is the group’s main

Gigante Havbruk AS aquaculture operation. The company

also conducts small and large scale

commercial research projects.

100% 35% 51% 100%

▪ Salten Aqua AS («Salten Aqua»)

Gigante Salmon

GIFAS Salten Aqua AS KapNord AS produces the salmon from roe to

AS

international markets.

▪ R&D ▪ Broodstock ▪ Smolt

▪ Aqua culture ▪ Smolt ▪ R&D ▪ KapNord AS («KapNord») provides

▪ Salmon Center ▪ Harvest ▪ Aquaculture smolt, land based competence, fish

Gildeskål health and environmental services.

▪ Processing ▪ Land based

▪ Sales

▪ Gigante Havbruk AS owns 60.86% of the

shares in Gigante Salmon AS following

the completed private placement.

1703 Project overview

Gigante Havbruk group has a fully integrated value chain

BROODSTOCK ROE FRY SMOLT

2 MONTHS 6 MONTHS 7 MONTHS

WELLBOAT TRANSPORT - Smolt is pumped straight from well boat into raceways

PRODUCTION FREIGHT HARVEST SALES/EXPORT

14-24 MONTHS

Resources and expertise

1803 Project overview

All key agreements are in place

# Agreement Counterparty Ownership

Management Gigante Havbruk AS owns 35% of the shares in Salten Aqua AS, directly and

1 Salten Aqua AS

agreement indirectly.

Gigante Havbruk AS owns 51% of the shares in Grytåga Settefisk AS, directly and

2 Smolt agreement Grytåga Settefisk AS

indirectly.

Gigante Havbruk AS owns 28% of the shares in Salten N950 AS, directly and

3 Slaughter agreement Salten N950 AS

indirectly.

Research

4 GIFAS Gigante Havbruk AS owns 100% of the shares in GIFAS.

Agreement

Other relevant agreements with related parties are assessed continuously as needed

1903 Project overview

GIFAS provides years of aquaculture experience and reasearch and

development capabilities

About GIFAS Financial performance

▪ GIFAS is headquartered in Sund, in the middle of Gildeskål 700 50.0 %

municipality. The company currently has two departments: a 600

596 591

547

40.5 %

research station on Langholmen outside Inndyr and an ordinary 40.0 %

500

part for salmon farming.

31.3 %

29.5 % 30.0 %

400

26.2 % 327

▪ The localities extend from Røssøya in Gildeskål to Hallsteinhamn in 282 22.4 %

300

Festvåg. The company offers customers research services in 20.0 %

185

addition to salmon farming. 200 176

132 122

10.0 %

100 74

▪ As a research station, GIFAS' staff has unique expertise, which

0 0.0 %

contributes to developing the industry in a positive direction. 2015 2016 2017 2018 2019

Revenue EBIT EBIT %

Product and service offering

AQUACULTURE RESEARCH AND DEVELOPMENT

2003 Project overview

Salten Aqua will provide both administrative and operational

resources

About Salten Aqua Financial performance

▪ Salten Aqua is owned by Gigante Havbruk, Edelfisk and Wenberg 1,800

1,612

5.0 %

Fiskeoppdrett. 1,600

1,430

1,400 4.0 %

1,300

1,233

1,200

▪ Salten Aqua gives the owners and subsidiaries a common platform 1,015 3.0 %

1,000 2.9 %

to reach the outside world. 2.7 %

2.4 %

800

2.0 %

600 1.8 %

▪ The Salten Aqua grouping handles the salmon from roe grain, to 1.4 %

400 1.0 %

processed product shipped to customers locally, nationally and

200

internationally. 27 31 41 22 22

0 0.0 %

2015 2016 2017 2018 2019

Revenue EBIT EBIT %

Product and service offering

BREEDING SMOLT SLAUGHTER PROCESSING SALES EXPORT

2103 Project overview

Smolt and fish health capabilities will be sourced from KapNord

About KapNord Financial performance

▪ KapNord is a company that invests primarily in aquaculture in 450 14.0 %

399

Northern Norway. 400

12.0 %

358

11.5 %

350

10.0 %

▪ The company owns: 300 9.1 %

▪ Grytåga Settefisk – has built a hatchery for salmon and trout in Grytåga, 250 8.0 %

at the entrance to Vefsnfjorden. 200 6.0 %

150

▪ Fishbase Group – produces lumpfish and juveniles of salmon, trout and 4.0 %

cod. 100

46 2.0 %

50 32

▪ LetSea – Provides research and services related to fish health and the 0 0.0 %

environment on salmon and other maine species. 2018 2019

Revenue EBIT EBIT %

Product and service offering

GRYTÅGA SETTEFISK FISHBASE GROUP LETSEA

SMOLT RESEARCH, FISH HEALTH, ENVIRONMENT

2203 Project overview

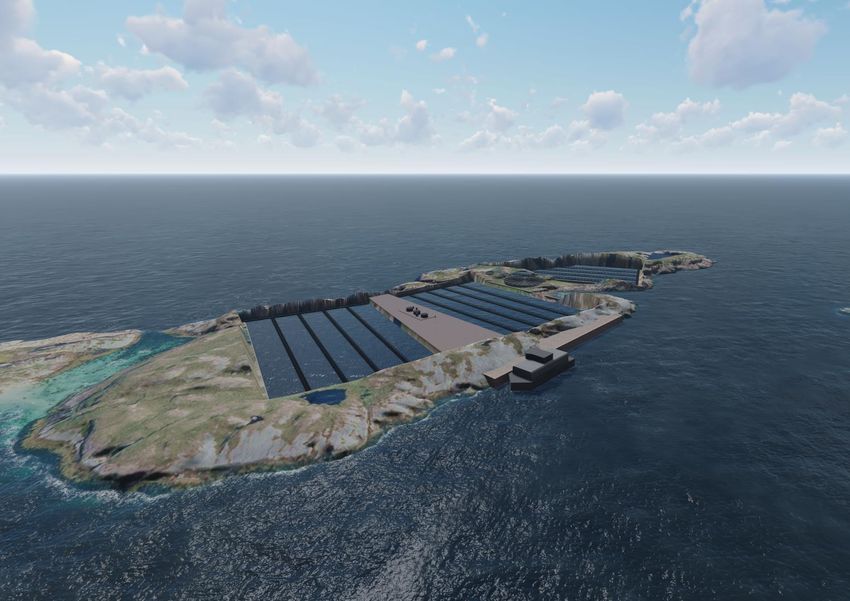

The land based facility will be constructed on Lille Indre

Rosøya on the Helgeland coast

1

Lille Indre Rosøya

1

Rødøy

Mo i Rana

2303 Project overview

A carefully selected location …

Why the chosen location?

✓ Environmentally assessed in the best category by AkvaPlan Niva.

✓ Centrally placed between hatchery and slaughterhouse.

✓ Over 5 km to nearest fish farm and no need for treatment of intake water.

✓ The island is conveniently designed with low and flat areas which leads to lower

construction costs.

✓ The long narrow island provides short inlet and outlet pipes.

✓ The water around the island satisfies the depth requirements for the intake pipes

and flow mapping does not reveal any danger of effluent being mixed with intake

water.

✓ Strong current around the island ensures that organic load will not accumulate

around the discharge points.

“Based on the assessment criteria in NS 9410: 2016, it is documented that

the site at the time of the test received condition [1 - Very Good]. A total of

40 grab cuts were made with the Van Veen grab (0.1 m2), distributed over

20 stations. All stations received a grade of [1 - Very good]”

2403 Project overview

… makes it possible to bring the sea on land

Comments

▪ The facility will consist of three large pools.

▪ Five raceways are established in each pool.

The raceway setup can be modified

according to changes in futures needs.

▪ The water is pumped into the end of each

raceway and out the other end.

▪ Each raceway has a partition and

arrangements to circulate water and create

optimal currents.

▪ The water intake is secured with an electric

net, flashing lights and ultrasound.

▪ At the bottom of each raceway, there is a

commercially tested sludge removal system.

Intermediate storage is established in

separate tank.

▪ The plant is operated from a commercial

feed/work barge.

▪ Oxygen will be produced at the facility.

Alternatively, supply of liquid oxygen will be

considered.

A commercial cage with a circumference of 120 meters to illustrate dimensions

2503 Project overview

The facility will be a land based flow-through system with a

conventional operational setup

Pool and raceways Current control

▪ 5 raceways installed in each pool: ▪ Each raceway is split with a partition and

▪ 5x9,000m3 = 45,000m3 mixers to create optimal water dynamics for

aquaculture.

▪ Dimensions per raceway:

▪ Width: 15 m.

▪ Dybde: 5 m.

▪ Length: 120 m.

Work barge Sludge collection

▪ Uses a conventional operational setup with a ▪ Grates and a sludge collection system are

work barge. mounted at the bottom of each raceway to

keep the water clear.

▪ Employees will live on the barge.

▪ Ratio in raceway: 1% sludge, 99% water.

▪ The production is monitored and remotely

controlled. ▪ Separation tank: 10% sludge, 90% water.

Water intake

▪ Water intake from 20 meters depth with drains

on the other side of the island.

▪ The system uses two pumps for safety and a

O2 system for each raceway All dimensioning parameters for water chemistry and

▪ Water replacement time: 30.0-40.9 minutes

dynamics have been carried out together with external

consultants.

2603 Project overview

Pools designed with flexibility to adjust to regulatory

changes

The pools will be excavated down to an elevation of -7 meters.

In the event of a change in the regulations, water may be moved in and out of the facility without lifting the water.

This will both increase total pool volume and lower operating costs by approx. 2/3.

2703 Project overview

Gigante Salmon expects low CAPEX and production cost

Risk Gigante Salmon RAS technology Traditional farming

Technology ▪ Flow-through of fresh sea water ▪ Recycled sea water ▪ Open pens

▪ Low degree of new technology implementation ▪ High degree of new technology implementation ▪ Well established production method

Sea lice ▪ Water intake is below depths inhabited by sea ▪ No sea lice ▪ Sea lice enters from surface water and

lice proliferate in pens. Sea lice is a substantial

issue both economically and for fish welfare

Water Quality ▪ Continuous replacement of water ▪ Closed system allows for control with ▪ Water continuously replaced by surrounding

▪ Location far from existing aquaculture temperature and chemical water quality sea water. Low risk, but no possibility to control

minimizes contamination risks parameters. water quality parameters

▪ Raceways provide controlled waterflow and ▪ Dependency on biofilters create risk for sudden

easy separation of waste changes in levels of chemical compounds and

▪ Supplemental oxygenation long term build up of pathogens

▪ No dependency on biofilters ▪ High dependency of oxygen supplementation

Environment ▪ Sludge is collected and separated off for ▪ Sludge is collected and separated off for ▪ Little control over emissions of fodder and fish

fertilizer production repurposing waste to nature

▪ Fish can not escape ▪ Fish can not escape

▪ No need for chemical treatment for sea lice ▪ Emissions of harmful chemicals from some sea

lice control methods

▪ Potential escapes if pens are damaged by

weather or handling

Energy Energy cost estimated at NOK 3-4/kg HOG Energy cost strongly dependent on location and Low energy consumption

water source.

Investment NOK 24/kg HOG yearly production at full Dependent on project. Typically NOK 120-200/kg Comparable purchase capex of license + site

production HOG capex 150-200 NOK/kg

Production cost NOK 31/kg HOG at full production. NOK 37-45/kg HOG Average production cost 43/kg HOG

NOK 38/kg HOG at phase 1

2803 Project overview

Team with extensive construction and aquaculture

experience

HELGE EGIL WÅGØ ALBERTSEN RUNE JOHANSEN

CEO CFO

▪ Extensive experience with project management in building ▪ Worked as CFO in Salten Aqua and has through the

and construction. administration agreement with Gigante group gained in-

dept knowledge of the Gigante companies and their

▪ Former project director in Avinor. Responsible for the

projects.

development of the new airport in Bodø.

▪ Experience from Statoil/Equinor.

▪ Experience from Insula AS and Equinor ASA.

▪ Starting the position as CEO 1 August 2021.

▪ MSc from Handelshøgskolen i Bodø.

KEY COMPETENCE SOURCED FROM GIGANTE HAVBRUK GROUP

ASBJØRN HAGEN MONICA BRUNSVIK

Quality and environmental manager HR director

▪ Environmental manager in Salten Aqua. ▪ HR-director in Salten Aqua.

▪ Has extensive experience in research and inspection. ▪ Former HR-director in ISS Facility Services AS.

PICTURE ARVE MOEN STORHOLM PICTURE KJELL ARILD LORENTSEN

Project manager Interim COO

▪ Currently holds the position as project manager for ▪ Project initiator and main owner.

Gigante Havbruk Group.

▪ Extensive experience from establishing and developing

▪ Former area manager in GIFAS. aquaculture businesses.

▪ BSc. Aquaculture operations and management. ▪ Detailed knowledge of the project from birth phase on

through detailed planning and contract structuring.

2903 Project overview

Board of Directors

EIRIK SØRGÅRD KJELL ARILD LORENTSEN

Chairman of the board Board member

▪ CEO KapNord AS. ▪ Founder and CEO of Gigante Group.

▪ Broad experience from marine sector, oil & gas, IT and ▪ Has held leading positions in the fishery and

finance. aquaculture industry since the 70’s.

▪ Currently holds board positions in several companies in ▪ Former captain on the fishing boat Selvåg Senior.

the marine sector.

▪ 6.5 years education in fishery and fishery economics.

KRISTIN INGEBRIGTSEN AVAILABLE POSITION

Board member Board member

▪ Advisor in SpareBank 1 Nord-Norge.

▪ Former HR and Strategy/market director in North

Energy ASA.

▪ Long experience from VC asset management.

✓Board position(s) available for key investor(s)

3003 Project overview

The completed private placement of MNOK 222 will be

used to fund construction and commercialization1

1 2 3

Construction phase Production first batch Sales/export

2021 - 2023 2023 - 2025 2024 - 2025

3 1

2

▪ Acquistion of Lille Indre Rosøya finalised. ▪ 1,100,000 smolt to be released into pool 1 in ▪ Salten Aqua’s sales and export company,

August 2023. The fish stays in pool 1 for 11 Polar Quality AS, will assist with sales/export.

▪ Excavation work and land preparation to start

months. First fish ready for sale expected in October

August 21, and will be carried out by Gabbro

2024.

Nor AS. ▪ When the fish is approx. 1.4 kg it is moved to

▪ Stone to be transported continuously. pool number 2 and 3 for further growth. ▪ The company plans to optimize production to

Expected to be sold for NOK 65m. ▪ First batch of slaughter-ready salmon take advantage of seasonal price fluctuations

expected after 14 months. and premiums on larger fish.

▪ Work barge to be acquired start of 2022.

▪ Piping installation to start beginning of 2022.

▪ The slaughter is carried out continuously with

the last batch in July (24 months).

▪ Final installation phase second half of 2022.

Note: 1. The project is considered fully funded as the company received gross proceeds exceeding NOK 192 million through the completed private placement. The additional NOK 30 million that were

raised will be used as an additional cash buffer. 3103 Project overview

Timeline towards 16,000 tons of yearly production

2021 2022 2023 2024 2025 2026 2027

Pilot raceway – optimisation velocity, exchange,

Pilot phase

purification

Startup constructon on Lille Indre Rosøya

Construction

Testing

Startup production – 1.1 mill smolt

Slaughter 5,300

tons HOG

Phase 1

Startup production – 1.1 mill smolt

Slaughter 5,300

tons HOG

Full production – 3.3 mill smolt

Slaugther 16,000

tons HOG

Full production

Full production – 3.3 mill smolt

Slaughter

3204 FINANCIAL INFORMATION

04 Financial information

Low CAPEX due to an efficient location acquired at a low

price

# Description Budget (MNOK) Comments

1 Acquisition Lille Indre Rosøya 1.0 Acquisition complete

2 Stone excavation and land preparation 62.0 Estimated volume 468.000 m3. Agreement with Gabbro Nor AS

3 Establish dock 15.0 Budget price from Moldjord AS

4 Transportation stone 36.0 Budget price from Polartugs at Dønna

5 Concrete walls around pools 18.0 Budget price prepared by Sweco

6 Work/feed barge 40.0 Based on similiar acquisition in 2020 + NOK 10m in equipment, transport etc

7 O2 system with generator (12 stk a NOK 1,7m) 21.0 Budget price from Nippon Gas. Liquid O2 system under consideration.

8 30 pumps/ generators / current controller 39.0 Budget price obtained by Arvid Fossum

9 Walkways 20.0 Budget price from Polarplast

10 Raceways 14.0 Quote from supplier for pilot

11 Cleaning systems 31.0 Budget price from Mivanor

12 Engineering and testing 23.0 Detailed design of facilities with equipment. Testing costs pilot

13 Interest construction financing 11.0 According to bank agreement

14 Raceway frames and bottom 10.0 Based on pilot experience

15 Automation (oxygen, pumps, current control) 5.0 Based on experience from other construction projects

16 Electrical 6.5 Engineering to begin autumn 2021

17 Personnel cost 12.0 Current personnel + staffing until start of operation

18 Water and sewage pipes 18.0 Engineering to begin autumn 2021

19 Shore power 18.0 Estimate based on other projects

20 Unforeseen 44.5 Estimate 10% to account for unforeseen costs/items and risk

TOTAL CAPITAL EXPENDITURES 445.0

21 Sale of extracted stone -65.0

NET CAPITAL EXPENDITURES AFTER SALE OF STONE 380.0

3404 Financial information

Gigante Salmon has construction financing and overdraft

facility from SpareBank 1 Nord-Norge in place

▪ Construction loan: NOK 204,000,000 – term approx. 12 months to be

converted to a long term loan: NOK 204,000,000 – Term 1+7 years upon

Granted financing: completion of construction.

▪ Overdraft facility: NOK 90,000,000 – Yearly renewal

Borrower: ▪ Gigante Salmon Rødøy AS

Lender bank: ▪ Sparebank 1 Nord-Norge

Guarantor: ▪ GIEK for 50 % of construction loan and 50 % of long term loan

▪ Mortgage land no. 74, title no. 7, Municipality of Rødøy ▪ Aquaculture licenses

▪ Operating assets ▪ All shares in Gigante Salmon Rødøy AS

Collateral: ▪ Livestock ▪ Insurance claims

▪ Receivables and inventory ▪ Bank accounts

▪ New share equity of min. NOK 192,000,000 ▪ Contracts, permits, insurances submitted

▪ Cash deposit NOK 65,000,000 as buffer for investment overruns. ▪ Contractors security arrangements established

▪ Investment overruns above buffer amount to be guaranteed for by ▪ Leasing agreement for work/feed barge established with

Conditions Precedants Gigante Havbruk AS Sparebank 1 Finans

▪ Payment and progress plan with milestones approved by bank ▪ Guarantee from GIEK established

▪ Construction inspector appointed ▪ Equity invested before draw down on construction loan

▪ Min. equity ratio 35%

▪ Drawn amount on overdraft max. 60% of biomass & receivables

▪ Working capital > 0

Covenants ▪ Negative pledge

▪ Cross default

▪ Gigante Havbruk AS to remain ownership of > 50% of Gigante Salmon

Rødøy AS (directly or indirectly)

Construction loan:

▪ Interest NIBOR + 3.10%

Overdraft facility:

▪ Quarterly fee: 0.30% of limit

• Interest NIBOR + 2.95%

▪ Commitment fee: 0.35% of margin from accept to opening

Pricing: ▪ Establishment fee: NOK 450,000

• Quarterly fee: 0.20% of limit

• Commitment fee: 0.35% of margin from accept to opening

• Establishment fee: NOK 50,000

Long Term loan:

• Interest NIBOR + 2.95%

3504 Financial information

Cost levels below traditional salmon farming

Estimated operating costs per kg HOG Comments

NOK ▪ Supplier agreement with Grytåga Settefisk

(group comapny) for delivery of smolt.

50

Lower cost per kg relative to traditional

45

farming due to use of 100g smolt and a

43

higher expected average slaughter

40 weight.

38

10.1

35

▪ Feed costs reduced compared to

9.9 31

4.2 traditional farming due to less feed waste

30

in raceways relative to open pens.

6.8 2.9

25 4.1

3.6

3.2 4.1 0.2 ▪ Personnel cost significantly lower relative

20 1.1

2.2 0.7 to traditional farming due to compact

0.2 0.2

layout and intensive production.

15

17.6

10 15.5 15.8 ▪ Logistics and slaughter costs corresponds

to traditional salmon farming in cages.

5

4.6

2.4 2.4

0

Phase 1 Full prod. Traditional

Smolt Feed Insurance Personnel Depreciation Slaughter inc. freight Other opex

1Fiskeridirektoratet

3604 Financial information

Atlantic salmon – Historical price development

Fish Pool Index NOK/kg Atlantic salmon, head on gutted (HOG) Comments

90 ▪ According to the Fish Pool

Index (FPI), the average

80 salmon price between

January 2018 and April

70

2021 has been 58 NOK/kg.

Lower and upper quartile

60 Avg. 58.0

ranging between 50.1

NOK/kg and 65.4 NOK/kg.

50

40

30

20

10

0

1

2018 2019 2020 2021

2018 2019 2020 2021

Source: Fishpool.eu

3704 Financial information

Production, capacity and sensitivity

Phase 1 Full production EBIT Sensitivity (MNOK)

Harvest tons (1000) HOG

Smolt released 1,100,000 3,300,000 5 8 10 13 16

38 100 160 200 260 320

36 110 176 220 286 352

Cost / kg

Harvest (tons, WFE) 6,350 19,050

34 120 192 240 312 384

32 130 208 260 338 416

30 140 224 280 364 448

Harvest (tons, HOG) 5,334 16,002

*Assumed average sales price : NOK 58 per kg.

Comments

Utilisation MAB 0.5x 1.4x

▪ The first generation will be limited to 1/3 of

licensed MAB due to clauses in granted

licences.

Prod. cost

37.5 31.1

NOK/kg HOG

▪ From year 3 production can be increased to

full capacity.

CAPEX/kg HOG 71 24

3805 RISK FACTORS

05 Risk Factors

Risk factors

1 RISK FACTORS 1.1 Risk related to the business and industry in which the Group operates

Investing in the Shares involves inherent risks. Before making an investment decision, investors Risk relating to the Group's ability to meet its objectives

should carefully consider the risk factors and all information contained in this Investor

Presentation, including the Financial Information and related notes. The risks and uncertainties The Group is in an ongoing developing process and is still in the preoperational phase. The

described in this Section 1 ("Risk factors") are the principal known risks and uncertainties faced Group has limited operating history and implementing its strategy will require Management to

by the Group as of the date hereof that the Company believes are the material risks relevant to make complex judgments. Hence, no assurance can be given that the Group will achieve its

an investment in the Shares. An investment in the Shares is suitable only for investors who objectives or other anticipated benefits. Further, risks relating to the successful implementation

understand the risks associated with this type of investment and who can afford a loss of all or of the Group’s strategies may be increased by external factors, such as downturn in salmon

part of their investment. The absence of a negative past experience associated with a given risk prices, increased competition, unexpected changes in applicable regulations or the

factor does not mean that the risks and uncertainties described herein should not be considered materialisation of any of the risk factors mentioned herein, which may require Management's

prior to making an investment decision. focus and resources, and which could in turn imply failure or delay in the successful adoption of

the Group’s business strategy. Failure to implement the Group’s business strategy could have a

If any of the risks were to materialize, individually or together with other circumstances, it could material adverse effect on the Group's results, financial condition, cash flow and prospects.

have a material and adverse effect on the Group and/or its business, financial condition, results

of operations, cash flow and/or prospects, which may cause a decline in the value of the Shares The Group is subject to risks that are inherent to significant construction projects

that could result in a loss of all or part of any investment in the Shares. The risks and

uncertainties described below are not the only risks the Group may face. Additional risks and There are numerous risks associated with construction of the Group’s facility at Lille Indre

uncertainties that the Company currently believes are immaterial, or that are currently not Rosøya (the “Rosøy Facility”), including delays, cost overruns, shortages or delays in equipment,

known to the Company, may also have a material adverse effect on the Group's business, materials or skilled labour; failure of the equipment to meet quality and/or performance

financial condition, results of operations and cash flow. The order in which the risks are standards, inability to obtain required permits and approvals, unanticipated cost increases,

presented below is not intended to provide an indication of the likelihood of their occurrence nor design or engineering changes, labour disputes or any events of force majeure, all of which

of their severity or significance. individually or in the aggregate may cause delays or cost overruns. Significant cost overruns or

delays could have a material adverse effect on the Group’s business, results of operations, cash

The risk factors described in this Section 1 ("Risk factors") are sorted into a limited number flows, financial condition and/or prospects. The construction project is also dependent on

categories, where the Company has sought to place each individual risk factor in the most external financing, under which the Group is required to fulfil a number of conditions, including

appropriate category based on the nature of the risk it represents. This does not mean that the raising an additional NOK 192,000,000 in equity before the construction loan can be drawn on.

remaining risk factors are ranked in order of their materiality or comprehensibility, and the fact The loan agreements also contains a change of control that is triggered if Gigante Havbruk AS

that a risk factor is not mentioned first in its category does not in any way suggest that the risk no longer controls, directly or indirectly, Gigante Salmon Rødøy AS.

factor is less important when taking an informed investment decision. The risks mentioned

herein could materialize individually or cumulatively.

The information in this Section 1 ("Risk factors") is as of the date of this Information Document.

4005 Risk Factors

Risk factors

The Group may not have sufficient insurance coverage to cover any damage to the Rosøy Risks related to existing and increasing competition in the farmed salmon market

Facility, during and after the construction has completed

The market for farmed salmon in general is global and highly competitive, and the Group will

The Rosøy Facility is subject to risk for damage during the construction work, and even after face strong competition from both domestic and international players within the farmed salmon

completion of the construction the Rosøy Facility may be damaged and/or subject to downtime market. If the Group is unable to compete efficiently, e.g. due to overcapacity, consolidation,

which may limit or slow down the construction and/or the production (as the case may be), and increased competition and price pressure in the market, this may have a material adverse effect

be costly to repair. The Group may not have sufficient insurance coverage for such damages on the business, financial condition, results of operations or cash flow of the Group.

and/or downtime, which could subject the Group to significant costs which in turn could have a

material adverse effect on the Group’s financial position and results. The Group’s operations are expected to be subject to several biological risks which could

have a negative impact on the Group’s future profitability and cash flows

While the Group has confirmed that it will obtain project insurance prior to the commencement

of the construction of the Rosøy Facility, there is no guarantee that the insurance will sufficiently Upon commencement of operations of the Rosøy Facility (in part or in whole), the Group will be

cover any damage to the Rosøy Facility brought about by the forces of nature. exposed to biological risks, such as for instance oxygen depletion, diseases, viruses, bacteria,

parasites, algae blooms, jelly fish and other contaminants, which may have adverse effects on

Land based salmon farming is a new industry subject to inherent risks fish survival, health, growth and welfare and result in reduced harvest weight and volume,

downgrading of products and claims from customers. An outbreak of a significant or severe

Land based salmon farming is a fairly new industry and, as a consequence, experience with land disease represents a cost for the Group through e.g. direct loss of fish, loss of biomass growth,

based salmon farming has been developing rapidly due to practical implementation of research accelerated harvesting and poorer quality on the harvested fish and may also be followed by a

taking place in several different companies. The Group seeks to benefit from the fish farming subsequent period of reduced production capacity and loss of income. The most severe

knowledge built up from traditional salmon farming, even though realizing that land-based fish diseases may require culling and disposal of the entire stock, disinfection of the farm and a long

farming has its own challenges such as limited numbers of independent water systems, subsequent fallow period as preventative measures to stop the disease from spreading. Market

management of gas injection (such as oxygen) and gas stripping (such as carbon dioxide) and access could be impeded by strict border controls, not only for salmon from the infected farm,

dependency on constant, uninterrupted electrical power. As such, there are still major biological but also for products originating from a wider geographical area surrounding the site of an

challenges to overcome prior to establishing a fully predictable production cycle. This will impact outbreak. Continued disease problems may also attract negative media attention and public

the success of the Group. concerns. Salmon farming has historically experienced several episodes with extensive disease

problems and no assurance can be given that this will not also happen in the future. Epidemic

As the concept of land based salmon farming is relatively new and still in the development outbreaks of diseases may have a material adverse effect on the business, financial condition,

phase, there is no guarantee that it will be competitive with traditional salmon farming. In results of operations or cash flow of the Group.

addition to the inherent risks involved due to the Group being in a development phase in a new

industry, such as risks related to faults in production, operations, maintenance, faults in the As the Group will not have any stable income until 2024, the Group is disproportionality more

Group’s technology, etc., there is also a risk that the Group's commercialisation strategy is found exposed to biological risks compared to its peers in the land-based salmon industry that have

limiting, and that other players in the industry are able to commercialise at a more rapid pace more sources of revenue and thus better financial prerequisites of dealing with a biological risk

than the Group, which may in turn have material adverse effects on the Group's results, financial materializing.

condition, cash flow and prospects.

4105 Risk Factors

Risk factors

Aquaculture is vulnerable to errors in technology, production equipment and transportation, processing and sale of fish products, the Group must to a significant extent rely

maintenance routines upon its counterparties, and their contracting parties, to fulfil their contractual obligations

towards the Group. Should any supplier and transporter, processor or vendor of fish products,

Aquaculture as an industry is vulnerable to errors in technology, production equipment and or their third-parties, fail to deliver according to contract, the Group may be at risk of suffering

maintenance routines. Such errors could cause damage to production and biomass, which will significant reputational damage, which may lead to impaired relationships with buyers and other

become the Group's most valuable assets, and as such be detrimental to the Group's future important business connections. Furthermore, breach of contract by counterparties may i.e. also

business and to the value of the Group as a whole. Hence, it is imperative that the Group ensure expose the Group to risk of disputes and legal proceedings arising from contractual liability, as

that it is able to implement routines and safety measures to protect its production line and well as a reduction of revenues.

develop its biomass. The Group will partly be reliant on third-party suppliers of technical

production equipment and sufficient maintenance routines for its production facilities. Despite The Group’s operation will be dependent on the quality and availability of salmon smolt,

the security and maintenance measures in place, the Group's facilities and systems, and those and there are risks related to the transportation of such smolt

of its third-party service providers, may be vulnerable to technical errors, limits in capacity,

breaches in routines, lack of surveillance, acts of vandalism, human errors or other similar The Group’s operation will be dependent on the quality and availability of salmon smolt. Smolt

events. may perish when being transported to production facilities and, although mortality related

transportation of smolt is normal, a higher mortality rate could have a severe effect on the

Cybersecurity risks could adversely affect and disrupt the Group's future business and Group’s business. Further, the quality of smolts impacts the volume and quality of the harvested

operations fish. Poor quality or small smolts may cause slow growth, reduced health, increased mortality,

deformities, or inferior end products, which in turn may have a material adverse effect on the

Threats to network and data security are increasingly diverse and sophisticated and the Group's Group’s results, financial condition, cash flow and prospects.

servers, computer systems and those of third parties that it uses in its operations are vulnerable

to cybersecurity risks, For example, the Group's future operations will depend on the Production related disorders may negatively affect the Group

maintenance and monitoring of its general operations, production facilities and biomass, and

such maintenance and monitoring depend to a large extent on uninterrupted performance of IT As the aquaculture industry has intensified production levels, the biological limits for how fast

systems. Implementing and maintaining sufficient surveillance is critical for growth and wellbeing fish can grow have also been challenged. As with all other forms of intensive food production, a

of biomass. Any cyber-attack or other security breach could jeopardize the performance of IT number of production-related disorders may arise, i.e. disorders caused by intensive farming

systems, leading to a disruption or tampering of the systems and, potentially, the loss of methods. As a rule, such disorders appear infrequently, are multi factorial, and with variable

biomass. Any cyber-attack that attempts to disrupt system service or otherwise access IT severity.

systems of the Group or those of third parties which the Group uses or will use, if successful,

could adversely affect the Group's future business, financial condition and operating results and The most important production-related disorders relate to physical deformities and cataracts,

be expensive to remedy. which may lead to financial loss in the form of reduced growth and fish health, reduced quality

on harvesting, and damage to the overall reputation of the industry, which in turn may have a

Risks arising from the Group’s contractual relationships with suppliers and transporters, material adverse effect on the Group's results, financial condition, cash flow and prospects.

processors and vendors of fish products

In connection with development of the Group’s fish farms and, upon commencement of

4205 Risk Factors

Risk factors

Risks related to feed costs and supply management. Any loss of the services of key management or future key employees, particularly

to competitors, or the inability to attract and retain highly skilled personnel could have a material

Feed costs are expected to account for a significant portion of the Group's total production adverse effect on the Group's business, results of operation, cash flow, financial condition and/or

costs, and an increase in feed prices could thus have a major impact on the Group's future prospects.

profitability. The feed industry is characterized by large global suppliers operating under cost

plus contracts, and feed prices are accordingly directly linked to the global markets for fishmeal, Risks related to power sources for the production facilities

vegetable meal, animal proteins and fish/vegetable/animal oils which are the main ingredients in

fish feed. Increases in the prices of these raw materials will accordingly result in an increase in The Group's future development and growth is dependent on it being able to obtain access to

feed prices. The Group may not be able to pass on increased feed costs to its customers in the the necessary onshore power outlets. The Rosøy Facility will at first, for a limited period of time,

future. Due to the long production cycle for farmed salmon, there may be a significant time lag be dependent on power generated from on-site fossil fuel generators, but is required to establish

between changes in feed prices and corresponding changes in the prices of farmed salmon and a connection with the power grid on the mainland. No assurance can be given that such outlets

finished products to customers. As the main feed suppliers normally enter into fixed contracts will be available continuously and without risk. The Group's power outlets and access thereto

and adapt their production volumes to prevailing supply commitments, there is limited excess of may be subject to risks, including denial of authority approval for connection, power shortages

fish feed available in the market. If one or more of the feed contracts the Group may enter into in or failure or delays in equipment or maintenance. If the Group's power sources fail, or if the

the future were to be terminated on short notice prior to their respective expiration dates, the Group is unable to obtain access to necessary power sources in the future, this could have a

Group could not be able to find alternative suppliers in the market. Shortage in feed supply may material adverse effect on the Group's business, results of operations, cash flow, financial

lead to starving fish, accelerated harvesting, loss of biomass and reduced income. condition and/or prospects.

Risks related to food safety and health concerns Risks related to contractual default by future counterparties

Food safety issues and perceived health concerns may in the future have a negative impact on Lack of payments from future customers/clients may impair the Group's future liquidity. The

demand for the products of the Group. It will be of critical importance to the Group that its future concentration of the Group's future customers may impact the Group's overall exposure to credit

products are perceived as safe and healthy in all relevant markets. The food industry in general risk as customers may be similarly affected by prolonged changes in economic and industry

experiences increased customer awareness with respect to food safety and product quality, conditions.

information, and traceability. If the Group should fail to meet new and existing market or

governmental requirements, this may reduce the demand for its products which, in turn, may

have a material adverse effect on the Group.

The Group's development and prospects are dependent upon the continued services and

performance of its key personnel

The Group's key employees are important to the development and prospects of the Company.

Further, the Group's performance is to a large extent dependent on highly qualified personnel

and management. Currently, the only employees in the Group is the key management. Moving

forward, the Group's continued ability to compete effectively and implement its strategy depends

on its ability to attract new and well qualified employees and retain and motivate existing

4305 Risk Factors

Risk factors

If the Group is not able to attract and retain customers and commercial partners, this cyclical pattern based on the balance between total supply and demand. No assurance can be

could adversely impact the Group's business and financial position given that the demand for farmed salmon will not decrease in the future.

The Group's commercial success depends on entering into agreements with customers, Further, farmed salmon is more generally sold as a fresh commodity with limitation on the time

distribution, marketing, sales and other agreements with third parties on commercially available between harvesting and consumption. Short-term overproduction may therefore result

favourable terms. If the Group does not succeed in attracting and retaining new customers, this in very low prices obtained in the market. The entrants of new producing geographical areas or

could have a material adverse effect on the Company's results, financial condition, cash flow and the issuance of new production licenses could result in a general overproduction in the industry.

prospects. Short term or long term decreases in the price of farmed salmon may have a material adverse

effect on the business, financial condition, prospects, results of operations or cash flow of the

The Group's business depends on clients goodwill, reputation and on maintaining good Group.

relationship with clients, partners, suppliers, employees, authorities and end-consumers. The

Company is exposed to the risk that negative publicity may arise from activities of legislators, Fluctuations in the global economy have the potential to adversely impact the Group's

pressure groups and the media, for instance that fish and other commodities are being bred financial position and its business

only to generate profit, which may tarnish the industry's reputation in the market. Loss of

certification may furthermore lead to reputational risks. Negative reputational publicity may arise The Group is exposed to fluctuations in the global economy in general, including with regards to

from a broad variety of causes, including incidents and occurrences outside the Company's the spending of end consumers, which could result in a higher demand for low cost alternatives

control. No assurance can be given that such incidents will not occur in the future, which may and thus difficulties for the Group in selling its product, which could in turn have a material

cause negative publicity about the operations of the Company, which in turn could have a adverse effect on the Group’s business, results of operations, cash flow, financial condition

material adverse effect on the Company. Negative publicity could further jeopardize the and/or prospects.

Company's relationships with customers, suppliers and local, regional or national authorities, or

diminish the Company's attractiveness as a potential investment opportunity. In addition, Risk related to activism

negative publicity could cause any customers of the Company to purchase products from the

Company's competitors, i.e. decrease the demand for the Company's products in the future. Any Certain global environmental organisations aim to eradicate salmon farming. Therefore, salmon

circumstances that publicly damage the Company's goodwill, injure the Company's reputation or farming companies such as the Group may be targets for activism of various kinds such as

damage the Company's business relationships, may lead to a broader adverse effect in addition spread of information, sabotage etc. with the aim to cause reputational damage or damage to

to any monetary liability arising directly from the damaging events by way of loss of business, production facilities, which in turn could have an adverse impact on the Group's business and

goodwill, clients, partners and employees. financial position.

Fluctuations in salmon prices could have an adverse impact on the Group's business and Certain environmental organisations have already criticised the Group's planned aquaculture

its financial position operations, and at least one organisation has submitted protests to Gildeskål municipality in

connection with the Company's application for planning permission. Furthermore, although the

The Group’s financial position and future prospect are dependent on the price of farmed aquaculture permit was granted, it should be noted that the county governor in Nordland county

salmon, which has historically been subject to substantial fluctuations. Farmed salmon is a submitted a letter of formal criticism in connection with the Group's application for aquaculture

commodity, and the Group therefore assumes that the market price will continue to follow a licenses at Lille Indre Rosøya.

44You can also read