Global Economic Outlook - Vaccines versus the second wave November 2020 - Aberdeen Standard ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

November 2020

Global Economic

Outlook

Vaccines versus the second wave

For professional investors only, in Switzerland for Qualified investors only – not for use by retail investors or advisers.

.

Global Overview

Vaccine light emerging at the end of the Covid tunnel

The global economic outlook is dominated by two until w ell into Q1 2021. We therefore expect the Eurozone and UK We continue to think that both the short-term and long-term global

economies to contract again in Q4 2020. In the US, there is less implications of this crisis are likely to be net disinflationary. The

conflicting forces. First, an intense second wave

appetite to impose full lockdow ns even under the incoming Biden scale of this disinflation is likely currently being exaggerated by the

of Covid in Europe and North America is already Administration because stringency is mostly under the control of inability of price indices to keep up w ith changes in the

weighing on recoveries. Second, recent news that individual states. Nevertheless, activity is still likely to flat-line composition of spending. How ever, the global economy has

highly effective vaccines are on the way raises through the w inter. But, from mid-2021 onw ards, these economies enormous spare capacity. This w ill take a long time to erode and

should benefit strongly from vaccine roll-out, given their large pre- thus w ill put sustained dow nward pressure on w age growth and

the likelihood of an eventual return to ‘normal’

orders. firms’ pricing pow er. And, while there has been much speculation

life. Our latest forecasts balance these forces by about ‘policy regime change’, the disappointing timidity of central

revising down global GDP growth in 2021 to 5.0%, A fading US fiscal impulse is another headw ind. Although the new

bank framew ork reviews and increasing reactivity (rather than

President Joe Biden favours much higher, sustained spending,

but then maintaining a strong pace of global proactivity) of fiscal policy is not pointing in that direction.

Democrats’ failure to secure a Senate majority (assuming they

recovery of 4.2% in 2022. don’t w in both of the Georgia run-offs in January) will significantly All this means that monetary policy should remain very loose, w ith

constrain w hat can be done in the face of partisan disagreements. central bank balance sheet expansion the marginal tool of policy.

The initial recovery from the Covid pandemic w as very rapid, for a

Although w e have pencilled in a modest $500 billion-1 trillion We expect the US Federal Reserve to lengthen the duration of its

w hile at least tracing out a ‘V’ shape. Having contracted 10.6%

Covid relief package during the lame-duck session or start of asset purchases around the turn of the year, suppressing long-

over H1 2020, global economic output surged 7.0% higher in Q3

Biden’s term, a 3-4% of GDP structural tightening is in prospect for term bond yields even as the economy recovers. The European

2020. How ever, the outlook has since become much more mixed.

2021. Central Bank and Bank of England are both set to increase asset

New Covid cases have been contained at low levels in China and

purchases further, following earlier moves by a number of smaller

east Asia, and are even bending low er in other emerging markets Meanw hile, increased regulation of the technology, financial,

advanced-economy central banks. Chinese monetary policy has

(EM). But Europe and the US are in renew ed outbreaks, which our pharmaceutical and energy sectors is likely to be a hallmark of the

stopped loosening amid a renew ed focus on financial stability

‘backcasts’ suggest are every bit as large as the first w ave. Biden Presidency, albeit w ithin the constraints of existing

concerns, but w e are not forecasting rate hikes. Indeed,

legislation. Trade barriers between the US and China are unlikely

The prospect of a number of highly effective vaccines being rolled meaningful policy rate increases in any of the major economies lie

to ratchet rapidly low er. How ever, foreign policy w ill at least no

out offers an eventual ‘escape hatch’ out of the pandemic and its w ell beyond our forecast horizon.

longer be done ‘via tw eet’, with a less volatile and more

economics effects. However, we can’t help tempering some of the

multilateral approach pursued instead. This should be positive for As has been the case all year, there are very w ide confidence

recent vaccine optimism. First, realistic manufacture and

animal spirits across the broader Ems in particular. That said, intervals around our central forecasts. In the near term, the

distribution timelines are not going to contain the current w ave of

variation in financial imbalances, structural reform momentum and balance of risks is skew ed to the dow nside, as w inter second

infection. Second, mass vaccination of the entire global population

the ability to manage Covid and then obtain and distribute w aves threaten to overwhelm healthcare systems and shut dow n

w ill be a multi-year, sustained effort. Third, vaccine hesitancy

vaccines will lead to significant performance divergences. economies, w hile fiscal policy mistakes are looming. How ever,

means there w ill be a meaningful number of hold-outs w ho refuse

from around mid-2021 onw ards, the risk is actually of more

vaccines. And finally, vaccine roll-out to EMs other than China and By contrast, w e think China is the large economy emerging from

positive outcomes than w e are forecasting. This is, above all

Russia w ill take much longer than in the advanced economies. the pandemic in the strongest shape. Successful containment of

because global vaccine coverage and its effects on activity could

the virus and a stimulative policy stance mean the level of GDP

Our latest forecasts are founded on a projection for the path of be greater than w e have factored in. This w ould mean a faster

has already surpassed pre-pandemic levels. Domestic vaccine

lockdow n stringency across the major economies. This combines 2021-onw ards recovery, and less long-run damage to the level of

efforts are also bearing fruit. That said, the focus of policy in China

our expectations for the course of the virus, the nature of public- global GDP relative to the pre-pandemic path. In fact, w e attach

w ill progressively move away from fighting Covid, tow ards

health responses to the pandemic and the roll-out of vaccines. We only a slightly low er probability to this upside scenario than w e do

managing financial risks, de-escalating tensions w ith the US, and

think the current re-tightening of restrictions in the US and Europe to our baseline scenario.

achieving China’s long-term grow th and emissions targets.

has further to run, and meaningful loosening w on’t get underw ay

1

Global forecasts

Revising up 2020 on the strength of the Q3 rebound, but revising down 2021, as winter

second waves weigh on activity before a vaccine-driven recovery can get going

Global GDP growth forecasts Implied global GDP levels by forecast date (Q4 2019 = 100)

8% 12% 115

6%

8% 110

4%

4% 105

2%

0% 0% 100

-2%

-4% 95

-4%

-8% 90

-6%

-8% -12% 85

2020 2021 2022 2019 2020 2022

Global growth q/q y/y (RHS) March May Aug Nov Trend

Source: Aberdeen Standard Investments, Haver, November 2020 Source: Aberdeen Standard Investments, Haver, November 2020

*Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual ev ents or results may differ materially.

2

Scenarios – drawn-out recovery and sizeable permanent damage are our base case

The distribution of risks – both upside and downside – around our baseline is unusually large. The

prospect of a highly effective vaccine means that, beyond the northern hemisphere winter, the

distribution of risks is skewed to the upside. But downside risks are still considerable.

Scenario Description Probability*

Economic openness: no major increase in infection rates through the fall and winter allows restrictions to be lifted. 5%

Virus &vaccine: effective vaccine found and rolled out internationally before end-2020, with most of the G20 inoculated by end 2021; therapeutics reduce

‘V’

mortality and strain on health systems.

Deep recession then rapid

Behavioural response: lower viral prevalence allows resumption of pre-Covid socially intensive activity.

recovery

Policy: monetary, fiscal and structural policies remain proactively focused on supporting a rapid recovery.

Economic impact: The rapid rebound in activity continues so that all the output lost relative to the pre -Covid trend is made up by end-2021.

Economic openness: lockdown is phased out across major markets through Q3 as political support wanes. 27.5%

Virus & vaccine: a vaccine is found and a few hundred million doses produced by end 2020/early 2021, while therapeutics reduce mortality and strain on health

Mild reverse √

systems.

Deep recession with recovery

Behavioural response: economic activity supported by gradually more confident consumers and corporates.

helped by early vaccine leading

Policy: generous programmes for economies sustained through 2021.

to limited permanent loss

Economic impact: recovery continues through 2021 as uncertainty declines. Most sectors return to normal function, but some pe rmanent damage from weaker

potential output (1-2% permanent hit to growth).

Economic openness: lockdown is phased out slowly through Q3 and Q4 with modest, localised re-tightening. 30%

Virus & vaccine: virus persists but not to the same extent; vaccine approved and rolled out with good take-up across major markets mid-late 2021, while

Reverse √ therapeutics reduce mortality and strain on health systems.

Deep recession with drawn out Behavioural response: economic activity gradually returns, but incomplete vaccine coverage and uncertainty continue to create some caution among corporates

recovery and permanent loss and consumers.

Policy: policy helps avoid a worse outcome by bridging some of the liquidity issues faced by households and firms.

Economic impact: deep recession in short term, with more gradual recovery and lasting damage resulting in the permanent loss of 3-5% of output.

20%

Economic openness: extreme lockdowns are phased down through H2, but then periodically re -imposed across multiple major markets.

‘W’

Virus & vaccine: virus is relatively persistent with vaccine approval delayed & roll-out pushed to mid-late 2021, but with low efficacy.

Deep recession; very uneven

Behavioural response: ongoing outbreaks and lockdowns lead to weak business investment and consumer caution.

recovery, with permanent output

Policy: policy mistakes occur in key major markets as politics trumps economic need.

loss

Economic impact: economic and financial volatility amid persistently depressed activity with permanent output hit 6-9% versus previous trend.

2.5%

Economic openness: extreme lockdowns phased down through H2, but re-imposed next winter and spring.

‘L’ Virus & vaccine: safe, efficacious vaccine not found in 2020 or 2021.

Deep, protracted, depression like Behavioural impact: this yields significant behavioural changes and makes it much harder to mend broken cash flow cycles.

loss of output Policy: premature fiscal tightening in key markets/ loss of faith in ability of central banks to act or fears of politicisation.

Economic impact: recovery looks more like the post-financial crisis pattern with much larger permanent losses worth around threeyears of global growth (10%).

Source: Aberdeen Standard Investments (November 2020)

*The probabilities assigned to these scenarios do not add up to 100%. This reflects the w ide range of alternative potential outcomes that cannot be captured in this exercise. Importantly, missing scenarios

are assumed to be evenly distributed to the upside and dow nside relative to the base case.

3

Quantitative indicators

Slowing high-frequency measures in Europe at odds with the US, Japan and emerging

markets

Tracking economic activity during the pandemic remains a

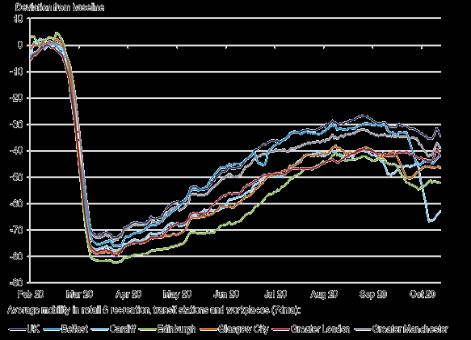

challenge We have therefore added alternative ‘big data’ to our

Google mobility data highlight diverging outlooks

suite of indicators. Divergent responses to second waves are 20 Deviation from baseline

10

creating dispersion in regional and sectoral recoveries.

0

We continue to monitor a range of high-frequency measures as economies recover -10

from the Covid shock. For example, mobility data from Google allow us to track -20

visits to certain locations. In our analysis w e tend to focus on those areas of mobility -30

most likely to be correlated w ith economic output - visits to retail and recreation -40

settings, w orkplaces and transit stations. -50

In the Eurozone and the UK, there has been a clear w orsening in the normalisation -60

of mobility, sometimes ahead of formal restrictions. This may signal that some of the -70

slow ing we had already seen in retail and industrial activity w ill continue in the -80

coming months. Feb 20 Mar 20 Apr 20 May 20 Jun 20 Jul 20 Aug 20 Sep 20 Oct 20

Elsew here, the plateauing in the mobility data seen last quarter has continued into Google Mobility Data - Average of Retail & Recreation, Workplaces & Transit Stations:

Q4. The question is whether this signals the emergence of a ‘new normal’. Activ ity India Brazil United States United Kingdom Australia Eurozone* Japan

in the United States, for example, is as close to normal as is possible w ith the

ongoing social distancing policies in place. It is certainly the case that the plateauing *GDP w eighted average across 17 EZ economies

in mobility in the US has not fed through into a reversal in the strength of the partial

hard indicators like retail sales. US weekly economic indicator continues to improve week to week

6 %y/y

Looking at the pattern in mobility across the individual states, those states where 4

the normalisation in mobility has declined relative to last quarter have a smaller

GDP share, so this is less likely to w eigh on aggregate economic activity. In fact,

2

our US Weekly Economic Indicator (WEI) continues to go from strength to strength, 0 -0.24

as retail activity props up the indicator. Nevertheless, questions over the durability of -2

spending remain, as w e end the year w ith a disappointing outlook for fiscal support.

-4

Tying these signals together, we expect a slowing in activity from the blockbuster -6

Q3 prints across most economies, w ith the Eurozone and UK slow ing most -8

markedly.

-10

2008 2010 2012 2014 2016 2018 2020

The latest indicator updates can be found in the macro tools tab of our SharePoint ASI Weekly Economic Indicator (scaled to GDP) US GDP

site here.

Source: Google Mobility Reports, Haver, Bloomberg, Aberdeen Standard Investments (November 2020)

4United States

Already longing for spring

The rebound in US growth has been more robust than expected, and

encouraging headlines around vaccines offer hope for a fuller recovery. US new Covid cases (5-day moving average)

However, the economy will need to get through a renewed Covid crisis first,

and alongside fading fiscal support. The Fed is likely to provide further 160000

stimulus in the near term, but the economy is still set to struggle over

140000

coming months, before reaccelerating notably through 2021.

The US delivered a record rebound in Q3, helped by easing Covid restrictions and generous fiscal 120000

support. How ever, these foundations are looking shaky. New Covid infections have surged to record

highs, even taking into account low testing in early 2020. States are responding w ith localised and 100000

targeted measures, but rising hospitalisations mean further restrictions will be needed. While these

are likely to fall short of April’s lockdow n, they are still expected to hurt the recovery. 80000

Fading fiscal support w ill be another drag. President Biden w ill likely need to w ork with a split

Congress on a new Covid relief package. The upshot is that w e expect only a ‘skinny’ deal of

60000

betw een $500-1,000 billion to pass next year. This reflects a preference for more modest spending

among Senate Republicans, w ith the possibility of no deal at all. This w ill soften, but not eradicate, 40000

the fiscal cliff taking hold, w ith 2021 to see a 3-4% of GDP tightening in the structural deficit.

20000

Both these drivers point to w eaker short-term growth, and w e expect the recovery to stall around the

turn of the year. In response, the Fed is expected to loosen policy in December, or January at the 0

latest. Fed chair Pow ell has pointed to asset purchases as the most likely lever. The Fed could also

05/Feb/20 08/Apr/20 10/Jun/20 12/Aug/20 14/Oct/20

increase the pace of quantitative easing (QE), or extend the maturity of its Treasury purchases to

help reduce longer-term interest rates (or both). Another option w ould be to promise to maintain Adjusted for low testing New cases (average)

open-ended QE until the Fed is on track to deliver an inflation overshoot – mirroring its commitment

on short-term rates. How ever, recent communications do not suggest the FOMC (Federal Open Adjustment f or low testing applies recent death rates to trends seen ov er Q2 to estimate case loads

Market Committee) is ready to take this step just yet.

The economy is set to rebound from Q2 2021 onw ards, helped by improving seasonal Covid trends 2017 2018 2019 2020 2021 2022

and a vaccine roll-out w hich we think w ill effectively immunise close to tw o-thirds of the US

population by end 2021. If w e are right that the US can deliver this logistical challenge, and large GDP (%) 2.3 2.9 2.2 -3.6 3.5 3.7

portions of the population are w illing to take a vaccine, this progress will significantly reduce Covid

disruptions, particularly in the beleaguered services sector. With this in mind, w e have raised our CPI (%) 2.1 2.4 1.8 1.2 1.7 1.8

forecasts for growth above consensus for the second half of 2021 and into 2022. 1.4 2.4 1.6 0.1 0.1 0.1

Fed Funds (%)

Source: Haver, Aberdeen Standard Investments (November 2020)

*Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual ev ents or results may differ materially.

5China

Doubling down

China continues to stage an impressive recovery, standing out from other

emerging markets and advanced economies. Containment of the virus and

accommodative policy have allowed the economy to achieve a greater

Alternative measures of activity are consistent with a strong,

degree of normalisation, while the rotation of demand in the West towards

but less ‘V’-shaped recovery

goods consumption has given a further boost. Positive news on vaccine

development provides another reason to expect only minimal long-run Quarterly growth rates, %

damage. Finally, President-elect Biden is likely to reduce the volatility of

US-China relations, even if a hard line persists. 15

Chinese Q3 GDP came out a bit below expectations at 4.9% year-on-year (y/y) growth. But, even

w ith this miss, the official data are still painting a very upbeat picture of the economy, w ith the level of 10

GDP 3.2% higher than Q4. Our China Activity Indicator suggests a still robust, but less complete,

rebound. Mapping it to GDP suggests more momentum in Q3 (expanding 3.6% quarter-on-quarter 5

(q/q) vs 2.7% q/q official). How ever, the economy could still have some w ay to recover as it implies a

less impressive rebound in Q2. 0

Looking forward, near-term growth may moderate slightly, as second Covid w aves in Europe and the

US disrupt their recoveries. But those renew ed outbreaks also mean that the rotation tow ards goods -5

consumption may hold up for longer, reducing the negative spill-over to China via global trade.

Policy remains accommodative, but the rebound in official GDP and a renew ed focus on financial -10

stability concerns – as illustrated by the ANT IPO postponement – suggests that policy is unlikely to

loosen further. Indeed, even w ith CPI inflation set to turn briefly negative around the new year, we -15

expect that our policy gauge – the ASI China Financial Conditions Index - w ill tighten in 2021 and w e Official GDP China Activity Indicator (3m3m)

have removed our previous call for a modest easing of key policy rates (seven-day reverse repo,

MLF and RRR).

Q1 '20 Q2 '20 Q3 '20

Positive new s on vaccine efficacy and deployment helps to remove dow nside risks and improve

confidence in China’s grow th outlook over our forecast horizon. At the same time, an unw inding of

the global rotation tow ards goods may w eigh somewhat on trade as developed markets eventually

recover. 2017 2018 2019 2020 2021 2022

Looking further ahead, the authorities announced that they w ould aim to double GDP by 2035, a ASI GDP (%) 6.8 6.6 6.1 -2.6 9.8 7.3

clear commitment to keep China on the path to achieving advanced-economy status. Much w ill

Official GDP (%) 6.9 6.8 6.1 1.7 9.9 6.3

depend on US-China relations and, w hile a Biden administration may bring more consistency to

foreign policy, a roll-back of tariffs or a broader detente is unlikely. CPI (%) 1.6 2.1 2.9 2.4 1.1 2.1

Source: Haver, Refinitiv, Aberdeen Standard Investments (November 2020)

*Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual ev ents or results may differ materially.

6Eurozone

Heading into a renewed contraction

The Eurozone economy is heading into a renewed contraction amid the

large second wave of Covid cases and increasing lockdowns.

The Eurozone GDP profile will be a lopsided ‘W’

We’ve learned tw o important things about the Eurozone economy since our previous forecasting

round. First, the Q3 2020 rebound from the initial contraction w as much larger than w e had expected. 105

GDP grew by 12.7% q/q in Q3, by far and aw ay the largest increase on record, and confirmation that,

for a w hile at least, the recovery was ‘V’-shaped.

100

And second, the next w ave of coronavirus and lockdow ns has been larger and faster than w e

anticipated. Indeed, daily new cases numbers are more or less in line w ith our attempt at 95

‘backcasting’ the true size of the pandemic during the spring. In turn, this second w ave is taking its

toll on economic activity. There has been a meaningful decline in daily mobility measures, and the

Eurozone composite PMI (Purchasing Managers’ Index) dropped back into contractionary territory in 90

October.

85

Incorporating these developments into our forecasts means that the Eurozone grow th profile is now

decidedly ‘W’- shaped. The initial contraction and subsequent rebound have been very sharp, but we

think that the Eurozone is going to dip back into a renew ed contraction in Q4 2020. Moreover, 80

lockdow n stringency is unlikely to be meaningfully lifted until w ell into Q1 2021, w hich means w e are

forecasting no grow th that quarter. The risk of a full-blow n double-dip recession (consecutive 75

quarterly contractions in both Q4 and Q1) is very real.

Q1 2019

Q1 2020

Q1 2021

Q1 2022

The eventual vaccine-driven recovery should be strong, but w e incorporate long-term damage to the

level of GDP w orth about tw o years of economic growth.

This W-shaped profile, as w ell as low inflation expectations, means that even after the current

deflationary period ends in early-2021, inflation w ill remain w ell-below the ECB’s target. This in turn November 2020 August 2020

means that w e expect additional monetary policy stimulus, starting w ith another €500 billion of asset

purchases and subsidised bank loans in December 2020. This probably w on’t be the last easing May 2020 Pre-crisis trend

move in this cycle, and w e have pencilled in further QE in 2022.

Fiscal policy, w hich has been highly expansionary so far in this crisis, is now set to be a small drag.

2017 2018 2019 2020 2021 2022

But this is on nothing like the scale of the post-financial crisis retrenchment that set the scene for the

Eurozone sovereign debt crisis. In any case, w hile it has hit some near-term roadblocks, the EU GDP (%) 2.7 1.9 1.3 -7.7 4.1 3.4

Recovery Fund should replace at least some of the w aning domestic fiscal stimulus. The bottom line,

though, is that Eurozone economic prospects are more dow nbeat than elsew here. CPI (%) 1.5 1.8 1.2 0.3 0.6 1.0

Depo rate (%) -0.40 -0.40 -0.50 -0.50 -0.50 -0.50

Source: Thomson Reuters Datastream, Aberdeen Standard Investments (November 2020)

.*Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual ev ents or results may differ materially.

7Japan

Sustaining a modest recovery

The Japanese recovery has been driven by consumption and trade, but a

third Covid wave in Japan, and resurgences in the US and Europe, will

weigh on both. The recovery should continue, but at a modest pace. Timing the election before the end of the Presidential term

Meanwhile a snap election is likely in late spring.

Covid infection rates remain low relative to Europe and US. How ever, they doubled over the first tw o

w eeks of November amid a modest local third w ave. Mobility has so far only declined in the w orst hit

areas (Hokkaido) and none of the hotspots have entered ‘Stage 3’ alert w hich triggers increased

stringency. The government plans to tackle the pandemic through increased testing, tracking and

localised measures. It has promised vaccines to all citizens, having signed basic agreements for

vaccine supplies from Pfizer and AstraZeneca. The government continues to plan for the

rescheduled Tokyo Olympics next summer. This includes the selective easing of Japan’s entry bans

for athletes as long as they provide negative test results and w ritten itineraries.

Q3 GDP w as stronger than expected at 21.4% q/q saar (seasonally adjusted annual rate). How ever,

Q4 is likely to be a much more mixed quarter, given the impact of the third w ave on consumption,

and resurgences in the US and Europe on export demand. Admittedly, upbeat prospects for China

grow th, signalling continued support for Sino-Japanese trade, are a positive offset.

On the policy front, Prime Minister Suga has requested the government compile a third

supplementary budget for FY2020 in November. The budget is expected to include an extension of

the government-funded Go To Travel campaign, as w ell as furlough and income support schemes.

How ever, this stimulus w ill be much smaller than the first tw o, in the region of Y10-15 trillion

(including the unused Y8 trillion of the second supplementary budget set aside as a reserve). The

Bank of Japan has acknow ledged that the inflation target of 2% is not a priority for now , and stands

ready to support fiscal policy and any future structural reforms.

Meanw hile election risks remain elevated. Tw o major deadlines influence the timing of the snap

election. First, the end of the low er-house term (Oct 2021) and, second, the end of Mr Suga’s term

as LDP president in September 2021. We expect the Suga administration to w ait for the third Covid 2017 2018 2019 2020 2021 2022

w ave to subside, and to then hold an election ahead of the Tokyo Olympics. Suga is very likely to win

GDP (%) 1.9 0.8 0.7 -5.3 3.0 1.3

this election. His policy agenda w ill focus on digitalisation, SME (small and medium enterprises)

reforms and bank reforms. But the mixed success of Abenomics suggest none of these w ill be a CPI (%) 0.5 1.0 0.5 -0.3 -0.8 0.5

game-changer for the economy.

Key rate (%) -0.1 -0.1 -0.1 -0.1 -0.1 -0.1

Source: Haver, Aberdeen Standard Investments (November 2020)

*Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual ev ents or results may differ materially.

8United Kingdom

Winter has come

Over the summer, the UK economy recovered roughly 50% of the economic

activity lost in the first half of the year. However, even before the latest

lockdown was announced, there were signs that the economy was losing The latest lockdowns do not appear to be biting hard yet

momentum. We expect the recent re-tightening of lockdown across the

country to tip the economy into contraction again in Q4.

There are good reasons for thinking that the scale of the dow nturn this time w ill be smaller than

during the spring lockdow n. The economy is starting at a low er level, more sectors are open, and

households and businesses are better placed to deal w ith the challenges of lockdow n. Still, w e do

not expect large parts of England to exit the current lockdow n at the early-December review date,

and forecast only modest easing in stringency in Q1. As such, the economy only narrowly avoids a

technical recession, eking out marginally positive grow th in Q1 next year.

Over the medium term, the UK is w ell-placed to benefit from vaccine developments. The government

has placed early orders for 340 million vaccines. And the UK has a w ell-developed vaccine

distribution netw ork, while surveys suggest that uptake w ill be high. So, w hen the recovery does

come, it should be rapid in the first instance, even if a degree of permanent damage is still likely .

Furlough has been extended until March 2021. This w ill provide more support – and save more jobs

– than the superseded Job Support Scheme. The announcement is w elcome and helps to

temporarily assuage some of our near-term w orries about premature fiscal tightening delivered in the

name of “embracing structural change”. How ever, it is likely that uncertainty about the direction of

policy w ill have cost some jobs, and unemployment w ill continue to rise over the w inter.

The Bank of England announced a further £150 billion of quantitative easing (QE) in early

November, and purchases will run until Q1 2022. Given that the yield curve is already very flat, the

degree of extra stimulus from QE is modest. How ever, to the extent that it keeps yields low as the

government runs huge deficits, this is supportive. Feasibility studies on negative rates continue, but

rate cuts are unlikely in the near term. The Bank has signalled that it thinks negative rates are more

helpful w hen the economy is enjoying a recovery, rather than a tool for providing stimulus as the

economy w eakness. As such, we expect QE to remain the marginal policy, and another £50 billion to 2017 2018 2019 2020 2021 2022

be announced in due course.

GDP (%) 1.8 1.4 1.2 -11.5 6.2 5.3

Finally, w e think Brexit negotiations w ill result in a narrow free trade agreement betw een the UK and

the EU. But even this w ill be an economic drag relative to the previous relationship, and there is still CPI (%) 2.7 2.1 1.8 0.5 1.0 1.2

some residual chance of a ‘no-deal’ exit.

Bank rate (%) 0.5 0.75 0.75 0.1 0.1 0.1

Source: Haver, Google Community Mobility Reports, Aberdeen Standard Investments (November 2020)

*Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual ev ents or results may differ materially.

9Emerging markets (ex-China)

Geopolitical backdrop has improved, but short-term and long-term challenges remain

Emerging markets (EM) could benefit from reduced trade policy uncertainty

under a Biden presidency, while positive news on vaccines may aid a more Wide dispersion in shocks and pace of recovery across EM

complete recovery. However, much still depends on the region’s ability to

manage the coronavirus. New case numbers have been falling in LATAM 5%

and Asia, but eastern Europe is now suffering a second wave. A difficult

balancing act remains, which is likely to drive further dispersion across the 0%

EM landscape, reflecting constraints on policy and variation in state

capacity. -5%

The economic shock across EM has been very marked and varied. The peak-to-trough falls in GDP -10%

for major EM range betw een 5 -15%. And, w hile countries are recovering, the extent of the recovery

and the outlook is far from uniform.

-15%

The first w ave of coronavirus is showing signs of breaking in LATAM and Asia – India in particular.

Nevertheless, the second w ave in eastern Europe illustrates the difficulty in balancing the desire to -20%

re-open the economy against public health needs. It remains unclear w hether localised containment

strategies w ill prove effective.

-25%

Positive new s on vaccine development potentially signals a more complete and earlier recovery in

the global economy. As developed markets (DM) roll out vaccinations, some EM may benefit from

-30%

the resumption of tourism and travel. How ever, the boost seen to global trade from a rotation of

consumption tow ards goods could unw ind as services are freed from restrictions, in turning hurting

EM exporters. And we continue to believe that most EM – w ith the exception of China and Russia -

w ill not be in a position to inoculate their populations until about one year after DM. Deviation from Q4 2019 GDP level (post Q3 2020 GDP) Trough in GDP

A Biden administration could lead to a decline in policy uncertainty, helping to underpin foreign direct *ASIRI forecasts **BBG forecasts

investment and lessening de-globalisation pressures. How ever, a tough line on China is likely to

remain, contributing to some lingering uncertainty.

2017 2018 2019 2020 2021 2022

Overall, w hile w e have seen some positive developments, EMs are not out of the w oods yet. A

slow er vaccination deployment leaves them at risk of further w aves of Covid, w hile macroeconomic Russia GDP (%) 1.7 2.4 1.3 -3.2 1.9 2.0

support risks becoming increasingly insufficient relative to the duration of the shock.

India GDP (%) 6.6 6.8 4.9 -9.6 10.2 5.9

Brazil GDP (%) 1.6 1.2 1.1 -5.5 3.8 2.6

Source: Haver, Refinitiv, Bloomberg Aberdeen Standard Investments (November 2020)

*Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual ev ents or results may differ materially.

10Australia, Canada, Sweden

Mixed fortunes in the fight against Covid

Australia, Canada and Sweden have had quite different Covid experiences.

In part, this reflects different strategies for fighting the virus, with Sweden

taking a now famously light-handed approach. Seasonal factors are also at Average new daily Covid cases per million people

play, with parts of Australia struggling with a second wave during its winter

500

Australia’s initial recovery was constrained by Victoria’s decision to impose a harsh lockdow n through

the southern w inter and early spring. Now that is ending and internal border restrictions are being 400

dismantled, the recovery will gather pace just as it’s losing steam in the rest of the advanced w orld.

Although Australia has used its fiscal headroom to deliver considerable easing this year, the most

300

recent tax measures w ill have only moderate multiplier effects. This, together w ith continued w eak 200

inflation, w ill keep the cash rate at rock-bottom levels, w ith the Reserve Bank of Australia anchoring

yields via bond purchases. 100

New Covid cases have been rising in Canada, prompting Prime Minister Trudeau to demand more 0

aggressive measures by the provinces and to extend a number of fiscal relief programs. Trudeau has

200302 200403 200507 200610 200714 200817 200918 201022

promised to keep the fiscal taps flow ing even after the crisis has subsided, by replacing support

schemes w ith infrastructure investment. Prolonged fiscal support w ould deliver a speedier recovery, Australia Canada Sweden

especially w ith the Bank of Canada’s commitment to hold rates unchanged until it has hit its inflation

target.

In Sw eden, our 2020 GDP forecast has been revised up to -3.8% after strong activity figures in Q3.

This is despite the official flash GDP estimate for the quarter casting some doubt over the extent of The Canadian labour market has been badly hit

the rebound. In addition, the recovery will slow in Q4 due to renew ed social distancing measures in

Sw eden and across much of Europe. We now expect weaker growth in Q4 2020 and H1 2021, 15

leading to a cut in our 2021 GDP grow th forecast to 2.8%. After a huge fiscal package in 2020, the

2021 budget proposes a fiscal stimulus of another 2% of GDP. In addition, the Riksbank has

launched a new round of quantitative easing, purchasing assets equal to 10% of GDP. How ever, it’s 10

unlikely to cut the policy interest rate below its current level of zero.

5

2017 2018 2019 2020 2021 2022

Australia GDP (%) 2.4 2.7 1.8 -3.7 3.6 3.2 0

Jan-20 Mar-20 May-20 Jul-20

Canada GDP (%) 3.2 2.0 1.5 -5.6 4.4 4.0

Sweden: Unemployment Rate (SA, %)

Sweden GDP (%) 2.8 2.1 1.2 -3.8 2.8 2.7 Canada: Unemployment Rate: 15 Years and Over (SA, %)

Australia: Labor Force: Unemployment Rate (SA, %)

Source: Haver, Aberdeen Standard Investments (November 2020)

*Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual ev ents or results may differ materially.

11Inflation

Laying to rest the ghosts of inflation past

Using our new framework to assess the probability of meaningful changes in

long-term inflation dynamics, we maintain our base case of underlying Drawing the right lessons from history

inflation at or below central bank target for most countries over the next

decade. However, both tails of the inflation distribution have become fatter. 18 Inflation expectations became OECD Headline

unanchored through the 1960s before inflation

Our reading of the literature on the determinants of inflation suggests that the follow ing three oil prices trigged a negative supply

conditions are jointly necessary and sufficient to herald a change in the inflation regime. 16 shock in the 70s

OECD core inflation

1. A fragile anchor for prices, such that inflation expectations are able to adjust quickly to changing Central bank

economic conditions and policy framew orks. 14 frameworks

2. A sustained period in w hich the economy is operating a long w ay above (below) its potential, change: Volker's

such that the prolonged excess (shortfall) in demand persistently feeds through into higher tough medicine

12

(low er) wage and price growth. triggered two

recessions in the

3. Central banks must cease to set policy in accordance with the Taylor principle. This requires that, 10 early 1980s, before

over the medium term, nominal interest rates increase more than one-for-one in response to any inflation 2008 financial

increase in inflation. expectations and crisis triggered a

8 disinflationary

Other drivers such as money supply, the size of government debt or deficits, or structural forces like prices started to

trend lower. shock, with

globalisation, technological change only matter for long-term inflation dynamics and regimes to the

6 persistent slack.

extent that they influence or are influenced by our three core criteria above.

Covid crisis will

Given that expectations remain extremely w ell-anchored, we expect the global economy to be do the same in

operating below its potential until at least the end of 2023. Central bank policy (for all the apparent 4 1970s: Persistent the near term

aggressiveness) has been characterised by institutional conservatism, suggesting the current baseline negative output

of low inflation remains in place. And, w hile fiscal policy has been quite supportive, the risk of 2 gap + fiscal

premature fiscal tightening remains. Indeed, Biden seems likely to face a split Congress, w ith the indiscipline +

prospect of policy gridlock and more rapid fiscal consolidation. Meanw hile in Europe, low inflation central banks that

expectations coupled w ith a ‘W’-shaped recovery point to persistent disinflation over the coming years. 0 prioritised

Turning to the supply side, globalisation has turned from an inflationary headw ind to a tailw ind over unemployment

recent years, and the era of product and labour market deregulation appears to be draw ing to a close. -2 over inflation.

But disinflationary digital technological changes continue unabated, w hile the global population is still 1970 1980 1990 2000 2010 2020

ageing. On balance, then, these forces also point to low er inflation outcomes.

Source: Haver, Aberdeen Standard Investments (November 2020)

12Monetary policy

Take it easy

We expect US Federal Reserve (Fed) policy lift-off to remain outside our

forecast horizon. Nevertheless, the market is now pricing in a rate hike at

end-2023 after recent vaccine news. Given the near-term outlook of slower

growth, a smaller fiscal package, and the Fed’s new target (which is meant Chinese policymakers appear to have condoned a ‘V’-

to commit them to allowing some inflationary overshoot), this seems way shaped recovery in yields

too early to us. Indeed the Fed dots are consistent with lift-off in 2025,

which seems more realistic.

In fact, w e expect the next policy move to involve further easing on the back of slow er growth and

delayed fiscal support. This may take the form of higher quantitative easing (QE) purchases, or a

‘tw ist’ of the program, w here purchases are directed at longer-duration assets. The shape of the US

yield curve is such that the Fed continues to put dow nward pressure on rates through asset

purchases, which should help at the margin. Nevertheless, as all yields get closer to zero, it becomes

harder for asset purchases to get much additional traction on the actual economy. Another option is

to explicitly tie asset purchases to the Fed’s objectives w ith formal state contingent forward guidance

in the manner it has w ith rates policy. This w ould be a helpful move, but again is unlikely to offer a

huge amount of extra stimulus.

The potential appointment of Judy Shelton to the Fed Board reflects the Republican Party’s desire to

deprive Biden of his ow n Fed pick. How ever, it probably doesn’t come w ith the same politicisation

risks that her appointment under a second term for Trump w ould have implied. If appointed, it’s very

likely that Shelton w ill (cynically) switch back to being a haw kish voice. She may re-discover the

apparent allure of a gold standard, but she should have little impact on the broader Committee, or

policy in general.

In Europe, w e expect a package of measures built around an additional €500 billion of QE purchases

as part of the Pandemic Emergency Purchase Programme (PEPP) to be announced in December.

Other parts of the package could include low ering the interest rate on longer-term refinancing

operations (LTROS - i.e. increasing the subsidy to banks); expanding the Asset Purchase

Programme (APP) or rolling the PEPP into the APP; and skew ing asset purchases to particular

Policy rates 2020 2021 2022

member states. We then expect a further QE announcement in 2022, w hen the initial vaccine-driven

rebound proves insufficient to generate enough inflationary pressure to achieve the ECB’s target. US 0.1 0.1 0.1

In China w e see a near-term easing of key rates (7-day reverse repo, MLF and RRR) as unlikely; UK 0.1 0.1 0.1

indeed the authorities appear to have condoned the recent increase in some money market rates. In

2021, w e still think that monetary policy is unlikely to tighten and that the PBoC’s bias is for marginal Japan -0.1 -0.1 -0.1

easing further out; equilibrium rates are trending low er.

Eurozone (depo rate) -0.5 -0.5 -0.5

Source: Haver, Aberdeen Standard Investments (November 2020)

*Forecasts are offered as opinion and are not reflective of potential performance. Forecasts are not guaranteed and actual ev ents or results may differ materially.

13Fiscal policy

Supportive... for now

Fiscal policy on the whole remains supportive and – outside of the US – has

been broadly responsive to changes in viral trends, with more support

delivered as economies have re-entered lockdown. However, supporting European

Source: fiscal

IMF policy

Fiscal to remain supportive

Sustainability in 2021

Report, Aberdeen

households and businesses through the acute phase of the virus when Standard Investments (May 2020)

Structural

large parts of the economy are turned off is quite different to providing -8 fiscal deficit

stimulus to the economy when lockdown is eased and the goal is to (% GDP) 2020 2021 2022

achieve full employment. We remain concerned that fiscal policy will

ultimately repeat the mistakes of the past, and prove too restrictive. -7

The outlook for fiscal policy in the US depends on the outcome of the Senate run-off elections in

Georgia in January. The most likely scenario appears to be Republicans maintaining control of the -6

Senate. In this scenario, w e expect a Covid relief package costing betw een $500 billion-1 trillion to

be passed in early 2021. How ever, it is important to note that stimulus of this scale w ould moderate,

and not eliminate, the tightening in fiscal policy current taking hold as large parts of the CARES act -5

expire. Indeed, even if w e assume a stimulus bill at the top of this range, w e w ould still see a US

structural tightening of around 3% of GDP in 2021. Moreover, the rest of Biden’s fiscal agenda –

higher taxes but even higher spending – looks impossible to pass w ithout full Congressional control, -4

w hile also w eakening the responsiveness of fiscal policy to economic conditions.

Beyond the US, the risk of premature fiscal tightening has reduced slightly. In Europe and Japan,

short-time w ork schemes are being extended into 2021. The UK has extended the generous Job -3

Retention Scheme until March 2021, avoiding w hat would have been a significant policy error in

ending this scheme in October. More comprehensively, the aggregate Eurozone structural budget

deficit is forecast to move from 4.8% this year to 4.3% next year. While that is technically a small -2

tightening in the fiscal impulse, the bigger picture is that the grow th in private sector demand w ill

more than make up for this. And, in any case, 4.3% is still a very large deficit. By 2022 the supra-

national stimulus from the Recovery Fund should be quite meaningful, offsetting some of the -1

national-level tightening. The Eurozone does not face imminent fiscal cliffs, and is not yet repeating

the mistakes of the premature fiscal tightening. How ever, risks remain w hen a pivot to outright

stimulus is required. In the UK, rhetoric is already turning to how various Covid support schemes w ill 0

Germany

Italy

France

Spain

EZ

Netherlands

be paid for, suggesting an early turn to tighter fiscal policy is likely in due course

In stark contract to the 2008 financial crisis, China’s fiscal support has been smaller than other major

economies. Policymakers are expected to remain attentive to the risks of a slow down and to ease if

necessary.

Source: European Commission, Aberdeen Standard Investments (November 2020)

14A Biden split Congress appears the most likely outcome

But we won’t know until January

Joe Biden is set to be the 46th President of the United States, in spite of

Scenario Description Policy Impact Probability

legal challenges by President Trump. While Biden managed to carve out

a path to victory even with a narrower win than polls had sugge sted, it

wasn’t strong enough for House and Senate candidates to ride on hi s Biden leads Trump in head to head at this stage

Democrat President Very slow tightening in fiscal policy. 30%

coat-tails. The Democrats maintain a (reduced) majority in the House, but Clean

the big question mark for investors is who wins the Senate majority. Sweep Biden with Higher spending on entitlements,

Democrat infrastructure, education, green

We w ill have to w ait until 5 January for tw o Georgia run-off elections to find out w hether the

Democrats can get to 50 in the Senate. This w ould allow the Vice President to cast the deciding majority in technology and jobs partly funded by

vote in a tie. The Republicans are early favourites to w in the run-offs in this traditionally

Republican state given their results in the first round and the expectation that low er turnout in House and higher taxes for corporates and high

January benefits Republicans. Indeed, w e think Republicans have a 70% chance of w inning both Senate earners.

Georgia run-offs.

Tighter environmental, tech and

How ever, we shouldn’t rule out the Democrats completely. This election is set to be a very high financial regulation.

profile and expensive race, given w hat is at stake for the new administration. We w ill be w atching

closely for signs that momentum is building for the Democrat candidates through high-profile Multilateral approach to China and

political efforts, polling and race-funding. progress on the OECD digital tax

The outcome of these races is crucial to the outlook for fiscal policy as w ell as the regulatory initiative.

outlook, w ith vastly different policies likely depending on those tw o Georgia seats. If President

Biden faces a split Congress, w e are pencilling in a Covid relief package costing betw een $500 Biden with President More rapid fiscal consolidation due 70%

billion-1 trillion to be passed in early 2021. Beyond that, w e expect partisan gridlock to stymie split

further fiscal stimulus and prevent the type of regulatory changes that require new legislation. Congress Biden with to gridlock in Congress.

Biden’s policy program for higher taxes and even higher (greener) spending looks impossible to Democrat Legislative stasis on tax and

pass w ithout control of the Senate. Our Senate Republican contacts did suggest that their

members might be open to an infrastructure plan, but w arned that financing this through tax hikes majority in spending issues.

or debt w ere unrealistic. If the Democrats do secure a narrow majority in the Senate, a larger

House and Tighter environmental, tech and

Covid relief bill is likely, w ith additional net fiscal stimulus of around $1 trillion likely to follow within

the year. Republican financial regulation.

majority in Multilateral approach to China and

Although an inability to pass new legislation w ill constrain regulatory changes, presidential powers

do allow for new rule-making and interpretation of existing legislation. We therefore expect the Senate progress on the OECD digital tax

Biden administration to look for w ays to increase restrictions on fossil fuel emissions to help

initiative.

tackle climate change, w hile also tightening regulation on the tech sector and financials. That

said, this agenda w ill face challenges in the courts.

Source: Aberdeen Standard Investments (November 2020)

15US-China relations will remain icy

But trade policy no longer by ‘tweet’

We expect Biden to take a more strategic, multilateral foreign policy

approach, looking to improve relations with European and Asian allies. On

China, Biden is unlikely to rapidly reduce trade barriers given the domestic

US China trade has not changed markedly since Phase-

political backdrop, opting instead for a review of the relationship and One deal. Biden likely to launch strategic review

engagement with multilateral organisations. Thi s should nonetheless help

reduce headline volatility and fears of rapid de-globalisation. Chinese imports from US, $bn

300

We can divide US-China relations into three buckets: politics, non-tariff barriers, and tariffs.

Politically, the Democrats have concerns regarding the Chinese human rights approach, w hich may

be more visible under Biden. He could be vocal regarding the treatment of minorities, Hong Kong

and others in a w ay that Trump w as not, because the ethics of the Chinese regime w eren’t Trump’s

Tracking line

250

focus.

Biden is likely to use traditional geopolitical tools like political sanctioning for actions that he Total: rolling 12 month sum

considers egregious abuses. He may also w ork within a strengthened European partnership to 200

mount coordinated rebukes. Equally, though, Biden may try to build political bridges w ith China on

issues like climate change, or through involvement in multilateral organisations. Monthly trade (annualised)

The escalation in non-tariff barriers (limitations on technology, supply chains and investment 150

betw een the tw o countries) over the past few years has mostly been a bipartisan effort, as opposed

to Trump-led. Given Democrats have deep concerns about the transparency and ethics of the

Chinese administration, w e expect an ongoing erosion of ties in areas like technology and

investment. How ever, we expect that Biden w ill w ork much more w ith allies to try to build a 100

multilateral approach to attempt to influence China.

Regarding tariffs – w here President Trump has been most active – Biden w ill probably leave existing

tariffs in place and initiate some kind of strategic trade relationship review . This review could tie 50

issues of political and economic transparency with any future reduction in tariffs. This process would

buy the Biden administration time, but w on’t necessarily result in a much more accommodative

arrangement w ith China. Nonetheless, this more strategic, measured approach to US-China trade

relations and more predictable, constructive relations w ith Europe should help to reduce headline 0

trade policy volatility compared w ith the past four years. December December December December December

2017 2018 2019 2020 2021

One of the big challenges for the administration w ill be how to manage America’s side-lining from

Asian regional trade integration through its absence from TPP (Trans-Pacific Partnership) and the

new RCEP (Regional Comprehensive Economic Partnership) agreement.

Source: Aberdeen Standard Investments (November 2020)

16Brexit drags on the economy either way, with uncertainty rife even under a deal

When is a deadline not a deadline?

As usual, Brexit deadlines are proving somewhat flexible as both sides Scenario Definition

move forward with legal text but are still debating the same issues of

state aid, level playing field and fish. We continue to expect negotiations

to result in an agreement on a narrow free trade agreement (FTA) thi s

winter, given the strong incentives for both the EU (vi s-à-vi s

management of the Irish border) and the UK (vi s-à-vi s the Union and the

economy) to secure a deal.

Negotiations to date have largely confirmed our view on the likely shape of the deal as a narrow Zero tariffs, zero quotas on goods with exclusions for

FTA focused on goods trade (click here to read The Brexit Destination, January 2020). How ever, highly regulated sectors

w e would caution that little firm detail has emerged so far on specific aspects of the deal. Narrow FTA* Customs checks at borders

Services sector access based on WTO terms

We understand that a landing zone is emerging on state aid, based on a framew ork which Full discretion over EU migration in UK and vice versa

includes joint principles, strong domestic regulation and robust dispute settlement. Closing this

issue w ould be a major step tow ards concluding a deal. With negotiations apparently entering the

final stages, w e would expect negotiators to remain focused on industrial sectors and on

measures to cushion (but not prevent) disruption to cross-border supply chains.

On goods, the headline commitment to tariff -free and quota-free trade remains intact. There is the

potential for some limited upside if mutual recognition provisions can be agreed in key sectors

such as cars, chemicals and pharma. Nevertheless, there is also the potential for significant

dow nside if the EU insists on more restrictive rules of origin, putting UK producers (particularly in

the auto sector) at a clear disadvantage.

UK exits EU transition period without trade agreement

On services, the deal is likely to significantly restrict the scope of cross -border trade. We expect UK and EU trade on WTO rules, resulting in different

the FTA to fall w ell-short of mutual recognition for professions. On financial services, EU tariff levels for different sectors, and services

authorities have indicated that very few sectors will benefit from equivalence and are pushing UK- ‘No-deal’ Brexit

unprotected

based firms to continue building up their EU operations. Customs checks at borders

Full discretion over EU migration in UK and vice versa

Of course, a ‘no-deal’ outcome remains a real possibility in such a fractious political environment.

Investors should not completely discount this scenario. Moreover, deal or no deal, the UK is

headed for a much less extensive trade relationship w ith the EU, and for a rocky political

relationship. Even if a deal is done, Brexit tensions are likely to recur continually over the coming

years as both sides find a new normal.

Source: Aberdeen Standard Investments (November 2020)

17Vaccines now look set to effectively inoculate 1.4 billion people by end-2021

Strong efficacy signs encouraging, but mass roll-out later than we previously expected

We have updated our framework approach to allow for bottom -up assumptions to End 2021 Vaccine Estimate UK US EU China G20

improve the accuracy of our estimates. News of better-than-expected vaccine Component

efficacy allowed us to upgrade the efficacy estimate across major markets. But

these results have come slightly later than we previously expected. The upshot i s Vaccine approval probability 95% 95% 95% 100%

we now expect 1.4 billion people to be effectively vaccinated by end-2021.

The publication of Pfizer/Biontech’s initial vaccine efficacy of 94% was a welcome upside surprise to vaccine

watchers. Additionally, Pfizer manufacturing capacity has been boosted since our last update, from estimates Manufacturing capacity 170 330 350 750

of 300 million by end-2021 to the latest estimates of 1.2 billion in the same period. Likew is e, signs of 95% (million)

efficacy from the Moderna vaccine candidate, which uses similar mRNA technology but does not require the

same deep-freeze temperatures for transportation, confirms the Pfizer result is not a one-off. We now await Roll-out to vulnerable 95% 95% 95% 90%

results in the coming weeks from Oxford/Astra Zeneca and other frontrunners in the vaccine race. population

Manufacturing capacity constraints and potentially differing efficacy across risk groups mean that multiple

vaccines will be needed to effectively inoculate multiple populations. While efficacy results are very Roll-out to general population 90% 95% 90% 90%

encouraging, they have actually been a little delayed relative to our previous expectations. This has had a

knock-on impact on pre-Christmas roll-out, which is likely to be much more limited compared w ith our last

update. Take-up in vulnerable 95% 90% 73% 90%

There is striking variation in take-up rates across different major markets in our estimates. This reflects population

worrying public opinion polling show ing accelerating vaccine scepticis m in the US and some European

countries, such as France. In the US in particular, the issue of vaccine safety was highly politicised in advance Take-up in general population 90% 75% 68% 90%

of the US election. It may be that once w e have vaccine results, and public health campaigns kick into gear in

more sceptical countries, those trends can be arrested or somewhat reversed. This framework allows us to

adjust figures if public opinion shifts to help us understand the effect on overall inoculations. Efficacy 80% 80% 80% 70%

The upshot of greater manufacturing and better-than-expected effic acy results,which nonetheless arrived later

than w e had expected, is that w e think about 30% of the G20 population w ill be effectively inoculated by end-

2021. How ever, variation is wide in those figures. Broadly,we expect inoculation rates in emerging markets ex-

China to be much low er than in developed markets. The UK stands out as the developed market with the Vulnerable population effective 10 44 50 176

single largest effective inoculation rate of 70% of the total population. That said, w e have yet to get Oxford inoculations (million)

vaccine efficacy results, which is a crucial element of the UK vaccine plan. It uses different technology to Pfiz er

and Moderna so uncertainty is higher about its efficacy – though earlier Phase II trial results w ere encouraging. General population effective 46 214 136 425 1397

Taken together, our vaccine expectations start to gain macroeconomic traction from the second or third quarter

inoculations (million)

of 2021 onwards. Before that time, our economic forecasts are still dominated by the effects of the second

w ave. After that time, the vaccine should allow an increasing normalisation of economic activity. *General population includes vulnerable population.

Source: Aberdeen Standard Investments (November 2020)

18You can also read