GLOBAL MARKETS STRATEGY DAILY UPDATE - Monday, January,18 2021 05.01.2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Monday, January,18 2021 GLOBAL MARKETS STRATEGY DAILY UPDATE

Alexander APOSTOLOV, PhD, MBA

Chief Investment Strategist

FX FOCUS www.bluesuisse.com/en/analysis

analytics@bluesuisse.com

Two reports over the past week serve as a reminder of limits to vaccine optimism and the recovery in risk

assets Market Snapshot

EUR: Mutations and potential pitfalls around vaccine rollout suggest risks to Q4 2021 onwards

are higher than previously anticipated and could change parameters of the current virus Main Quotes Heat Map

narrative. Adding to these concerns is confirmation from a key drug manufacturer it will

temporarily reduce vaccine deliveries across Europe, meaning any upsizing in vaccine

distribution will likely be capped.

USD: Distribution challenges aren’t the only issue – monitor the supply situation too - in the

US, Washington Post reports that expanded access to vaccines is unlikely. Bottom Line – the

reports speak to distribution challenges and supply shortfall of Covid-19 vaccines, adding to risks

that vaccination timelines can be further delayed. It also increases global lockdown and growth

risks for Q4 – which poses risks to the global recovery outlook and risk assets (FX).

US data releases Friday - retail sales weaker but firming inflation data may start to see markets

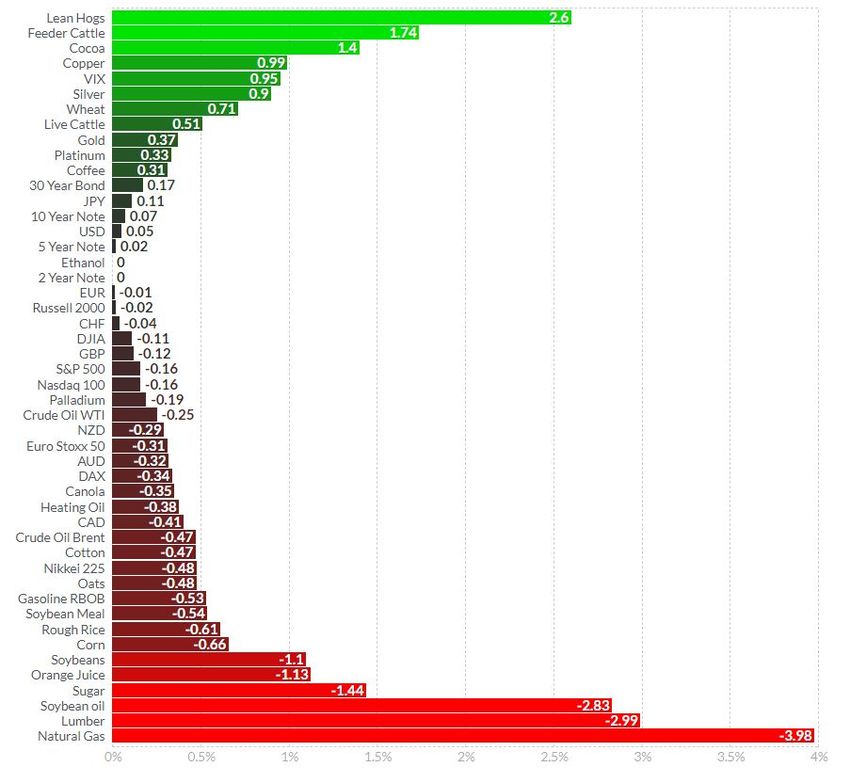

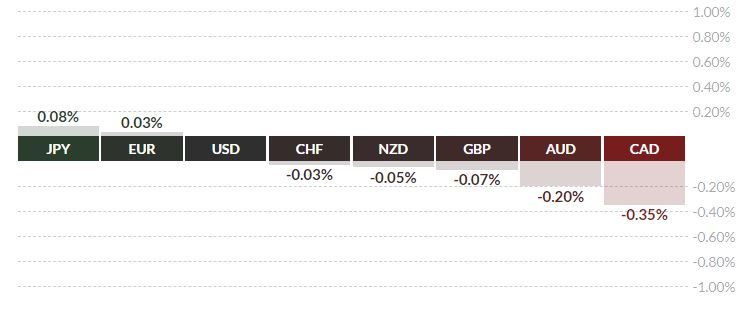

1 Day Relative % Performance [USD]

focused more on Fed tapering watch:

• USD: US December retail sales decline sharply but expected to bounce in January – Friday’s

most significant miss sees headline retail sales down -0.7%MoM in December and the control

group, which strips out strong auto sales also down -1.9%MoM. bluesuisse.com analysts however

aren’t concerned, as spending levels run well above pre-COVID. Looking-ahead, the team expects

stronger sales data.

• USD: US December Industrial production is up 1.6%MoM, above consensus for 0.5% with

manufacturing advancing a strong 0.9%MoM. bluesuisse.com analysts expect the constellation of

industrial data from “soft” survey indicators to point to an ongoing and broad-based rebound in FX Technical Indicators Summary

manufacturing.

• USD: US consumer confidence meets expectations but inflation expectations rise – January

University of Michigan Consumer Sentiment Survey comes roughly in line with consensus

forecasts at 79.2 (80.7 prior). Notably though, the 5-10Yr inflation segment rises to 2.7% from

2.5% amid growing optimism about reflation.

• USD: December PPI imply firmer core PCE inflation - PPI final demand rises 0.3%MoM and

remains at 0.8%YoY in December, closely in line with expectations. The core measure, which

excludes food, energy, and trade services, is also firmer, rising 0.4%MoM. bluesuisse.com

analysts flag that the print reinforces the outlook for core PCE to overshoot 2% temporarily

starting in April of this year.

UK data releases Friday - GDP notably more resilient than expected:

• GBP: UK GDP falls - 2.6% in November – though still substantially stronger than consensus for

a - 4.6% decline. This leaves UK GDP 8.5% below the pre-pandemic level (Feb-2020) even as

growth on a three month by three-month basis is now running at 4.1%. The print coincides with

the England wide lockdown measures imposed during November, and similar restrictions in

Scotland, Wales, and Northern Ireland. In comparison with April though, nearly all sectors

(particularly manufacturing and construction) prove more resilient except consumer services.

bluesuisse.com analysts downgrade 2021 growth – drivers behind the 2020 resilience are

unlikely to provide the same support in early 2021 and the team now expects a sharp reduction

in output in Q1-2021, with activity in January 2021 falling to 14.9% below February 2020 levels

(a similar hit to June 2020).

Week Ahead:

• EUR: ECB Monetary Policy meeting – Refi Rate Forecast: 0.00% Prior: 0.00%; Deposit Facility

Forecast: -0.50% Prior: -0.50%; Marginal Lending Facility Forecast: 0.25% Prior: 0.25% -

bluesuisse.com analysts do not expect any changes on policy or communication but it is of

interest to see what message President Lagarde sends with respect to the near-term outlook and

risks surrounding the baseline and current strength in EUR and impact on euro area’s longer-

term inflation outlook.

• EUR: Euro area Manufacturing PMI, January Flash Forecast: 57.0 Prior: 55.2; Services PMI,

January Flash Forecast: 43.0 Prior: 46.4; Composite PMI, January Flash Forecast: 47.5 Prior:

49.1 – bluesuisse.com analysts estimate that the flash composite PMI will fall back in January, by

around 1.5 points to a two-month low of 47.5, signaling economic activity is contracting due to

lockdowns but the impact is smaller than in November, let alone than in the spring.

• EUR: German ZEW Expectations, January Forecast: 60 Prior: 55.0; ZEW Current Assessment,

January Forecast: -70 Prior: -66.5 - On the back of vaccine roll-out, hopes for more US fiscal

stimulus and continued central bank support, equity markets in Germany continue to surge,

which will likely be reflected in investor expectations.

• GBP: Manufacturing PMI, January Flash Forecast: 52.5 Prior (Nov Final): 57.5 – bluesuisse.com

analysts expect the UK headline manufacturing PMI to fall back sharply this month as recent

data has been flattered by both Brexit stockpiling effects and growin

Alexander APOSTOLOV, PhD, MBA

g pressure on supply chains. Chief Investment Strategist

• GBP: Services PMI, January Flash Forecast: 40.3 Prior (Nov Final): 49.4 – bluesuisse.com www.bluesuisse.com/en/analysis

analysts expect the UK services sector to be hit hard by the move on 4 January back into a analytics@bluesuisse.com

national lockdown though not by the same order as in April 2020.

• CAD: Bank of Canada Rate Decision – 0.25%, median: 0.25%, prior: 0.25% - bluesuisse.com

analysts are most curious to hear about any possible guidance around upcoming changes to Market Snapshot

monetary policy. bluesuisse.com base case continues to be that the next adjustment to monetary

policy will be to allow for a slower pace of weekly bond purchases later this year (possibly the

April BoC meeting).

.

Main Quotes Heat Map

1 Day Relative % Performance [USD]

FX Technical Indicators Summary

Chart of the Day Crude Oil: Pullback at Hand Before Next Leg Higher? Crude oil prices are over 11% higher this month, bolstered by an improving economic outlook, higher global trade activity, and positive OPEC+ developments. West Texas Intermediate (WTI) prices are hovering below the yearly high set last week at 53.90. Prices look poised for higher ground, but a short-term pullback may be the most likely course of action before a subsequent rally takes shape. The 9-period Exponential Moving Average on the 4-hour timeframe supported prices leading up to 2021 high before fading. An ensuing push upward fell short and WTI proceeded lower. Now, the approaching 9-period EMA may provide support once again for a quick retest, though a period of consolidation appears to be an equally likely short- term outcome. One point of concern for buyers is the bearish divergence between the Relative Strength Index and recent swing highs in crude oil prices themselves. A move down to trendline support from last November would give bears a short-term victory while allowing the broader trend to remain intact, conceding some profit-taking in the process. That said, an extension higher may still be the most likely scenario following a short-term move lower or a period of consolidation. • CRUDE OIL - 4-HOUR

Alexander APOSTOLOV, PhD, MBA

Chief Investment Strategist

Capital Markets Overview www.bluesuisse.com/en/analysis

analytics@bluesuisse.com

Down Week Ends on Lower Note

Market Snapshot

Crude oil prices are over 11% higher this month, bolstered by an improving economic outlook, World Exchanges Performance Heat Map

higher global trade activity, and positive OPEC+ developments. West Texas Intermediate (WTI)

prices are hovering below the yearly high set last week at 53.90. Prices look poised for higher

ground, but a short-term pullback may be the most likely course of action before a subsequent

rally takes shape. The 9-period Exponential Moving Average on the 4-hour timeframe supported

prices leading up to 2021 high before fading. An ensuing push upward fell short and WTI

proceeded lower. Now, the approaching 9-period EMA may provide support once again for a

quick retest, though a period of consolidation appears to be an equally likely short-term outcome.

One point of concern for buyers is the bearish divergence between the Relative Strength Index

and recent swing highs in crude oil prices themselves. A move down to trendline support from

last November would give bears a short-term victory while allowing the broader trend to remain

intact, conceding some profit-taking in the process. That said, an extension higher may still be

the most likely scenario following a short-term move lower or a period of consolidation.

1 Day Relative Performance

• CRUDE OIL - 4-HOUR

Technical Indicators Summary

You can also read