GLOBAL PROGRAMMES 2018 - COMPLIANCE OPTIMISE - AIG

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

GLOBAL PROGRAMMES 2018 COMPLIANCE OPTIMISE OECD From the publishers of Collaborate to meet Consolidating (re)insurance Tackling the Beps regulation functions hurdle

FOREWORD

T

he expert contributors featured within the Captive Review Global Programmes

report are focused on guiding readers to best prepare for, and meet, the evolv-

ing challenges affecting large corporates and their insurance requirements.

With multinational business the norm, firms are tasked with raising the bar to en- REPORT EDITOR

Ross Law

sure regulatory compliance is met and to cater for increasingly sophisticated client +44 (0)20 7832 6535

demands. r.law@pageantmedia.com

CAPTIVE REVIEW EDITOR

Due to steadily decreasing premium rates, the insurance and reinsurance markets Richard Cutcher

are also beginning to change. With this rising pressure and the likelihood of greater +1 (646) 891 2133

r.cutcher@captivereview.com

consolidation, there is a growing desire for corporates to use their captives more

actively. GROUP HEAD OF CONTENT

Gwyn Roberts

As a result, enlisting a fronting partner capable of supporting captive managers

and owners through the likes of the OECD’s Base Erosion and Profit Shifting (Beps) HEAD OF PRODUCTION

Claudia Honerjager

regime, is becoming essential.

ART DIRECTOR

Elsewhere, the potential implications of the incoming IFRS 17 rule on captives are Jack Dougherty

outlined, along with the steps firms can take to ensure the wellbeing of their fre-

DESIGNER

quent-flying employees. Nadja Tschopp

We hope this report will give readers valuable insight into how best to structure and SUB-EDITORS

Luke Tuchscherer

manage their global programmes, maximise captive efficiency, and ensure multi- Alice Burton

jurisdictional compliance measures are met. Charlotte Sayers

PUBLISHING DIRECTOR

Ross Law, report editor Nick Morgan

+44 (0)20 7832 6635

n.morgan@captivereview.com

SENIOR PUBLISHING EXECUTIVE

Lucy Kingston

+44 (0)20 7832 6569

l.kingston@captivereview.com

DATA/CONTENT SALES

membership@captivereview.com

+44 (0)20 7832 6513

EVENTS MANAGER

Rachel Magnus

+44 (0)20 7832 6517

r.magnus@captivereview.com

HEAD OF EVENTS

Beth Hall

+44 (0)20 7832 6576

b.hall@captivereview.com

CEO

Charlie Kerr

Published by Pageant Media,

One London Wall, London, EC2Y 5EA

ISSN: 1757-1251 Printed by The Manson Group

© 2017 All rights reserved. No part of this publication

may be reproduced or used without prior permission

from the publisher.

3

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018

CONTENTS | GLOBAL PROGRAMMES

6 PROTECTING THE WELLBEING OF 14 THE CHANGING INSURANCE MARKET

EMPLOYEES OUT ON BUSINESS Paul Wöhrmann and Helene Westerlind, of Zurich,

MAXIS GBN reflects on the potential negative impact outline the benefits of having a fronting insurer

of business travel, and the practices and innovations

firms could implement to protect the wellbeing of their 16 GLOBAL PROGRAMMES: RAISING THE

employees BAR

Carol Barton, of AIG, describes the steps the firm is taking

9 ISSUES AND IMPLICATIONS FOR to enhance their global programmes service offering

CAPTIVES

Matthew Latham and Alex MacInnes, of XL Catlin, 18 SERVICE DIRECTORY

addresses the potential implications of the new IFRS 17

rule on captives

12 COMPLIANCE ACROSS BORDERS

Karen Jenner, of FiscalReps, discusses the need for clarity

in global programmes to ensure multi-jurisdictional

compliance needs are met

4

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018

Protection, delivered

seamlessly around

the globe.

Navigating a complex world can be challenging.

Wherever your business takes you, AIG is there to help you manage your risks with

confidence. Together, we take a proactive approach to build the optimal multinational

program that meets your needs today, and into the future. Refined over nearly a century—

you can count on our global perspective, local insights, and world class service to help

you simplify a complex world. Learn more at www.aig.com/multinational

Insurance and services provided by member companies of American International Group, Inc. Coverage may not be available in

all jurisdictions and is subject to actual policy language. For additional information, please visit our website at www.aig.com.

GLOBAL PROGRAMMES | MAXIS GBN

PROTECTING THE

WELLBEING OF

EMPLOYEES OUT

ON BUSINESS

MAXIS GBN reflects on the potential negative impact of business travel, and the practices and innovations

firms could implement to protect the wellbeing of their employees

B

usiness travel is often seen as and strategies to help improve diet and

glamorous and a perk of being activity while travelling.

successful in your career but the This could include encouraging employ-

reality – especially for employ- MAXIS GBN ees to explore alternative modes of trans-

ees who travel a lot – can be portation – such as taking the train instead

quite different. Indeed, frequent, and par- of flying. If there is no way around flying, it

ticularly long-haul business travel can have is preferable to fly direct instead of taking

a negative impact on a company’s most MAXIS Global Benefits Network (MAXIS GBN), connecting flights that will contribute to

co-founded by MetLife and AXA in 1998 is one of the

important asset: its people. tiredness and jet lag.

leading international employee benefits networks

It might still be considered essential for providing global service capabilities and delivering There may also be opportunities to

economic development and global trade, world-class employee benefits perspectives and solu- substitute face-to-face visits with telecon-

but the inexorable growth in business tions to clients in 115 markets around the world. For ferencing. Often it is necessary to meet

travel is leading to real questions about the more information, please visit www.maxis-gbn.com someone for the first time in person, but

health and wellbeing of the staff undertak- after that, video-conferencing can be an

ing the trips and the impact that frequent tion’. Other impacts can include psycho- acceptable substitute.

business travel has on both their mental logical, social and physical effects, includ-

and physical condition. ing accelerated ageing, and a heightened 2. Create a corporate travel policy

For these reasons, a broader company risk of stroke, heart attack and deep-vein As more and more people travel for busi-

consultation may be required when mak- thrombosis. ness, it is becoming increasingly important

ing corporate travel policy decisions. This So, what should international compa- from an HR and duty of care perspective

means, specifically, including HR and well- nies and, just as importantly, their staff do to consider the impact on staff wellbeing

being teams as well as the procurement and to try and reduce the negative effects of and health, not just in terms of the physical

travel management departments already frequent business travel? Part of the chal- impact of long-distance travelling but also

involved in managing business travel pro- lenge is that the requirements for each the mental and emotional aspects such as

grammes and policies today. person will differ depending on variables being away from family and normal rou-

It is frequent long-haul air travel, in such as number of trips, length of stays, tines.

particular, that is now understood to have distance travelled and other factors such as With corporate travel having a signif-

greater detrimental effects on staff than an employee’s family status (having young icant impact on employees’ wellbeing,

previously realised. And while jet lag is the children, for instance) so a single cover all morale and productivity, it is critical the HR

most commonly cited physiological impact solution won’t help. department be involved in the process of

of frequent business travel, it is not widely developing a company’s travel programme.

realised that the condition can persist for Here are some suggested steps employers They can make sure that duty of care pol-

up to six days after flying. Nor is it under- can take: icies reflect the changing global sentiment

stood that fatigue from jet lag, combined 1. Help employees to help themselves towards business travel and the pressures

with travel stress, may turn chronic and has Companies can look into employee educa- that can result.

been termed ‘frequent traveller exhaus- tion programmes on stress management HR departments can also help to boost

6

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018

MAXIS GBN | GLOBAL PROGRAMMES

can ‘combine virtual and augmented

reality into one experience’ and that

everyone in a business meeting can sit

in the same room together, no matter

where they are physically located. Par-

ticipants can even share virtual white-

boards. Could the VR headset be the

technology that finally replaces business

travel?

5. Revisit work conditions

As well as looking at overall travel wellness

programmes, organisations can consider

amending working terms and conditions.

Bearing in mind the fact that jet lag can

affect travellers for six days, organisations

could also allow staff to work from home,

offer more flexible hours following a

long-distance business travel trip, or space

out long-distance trips around minimum

rest periods. This way a frequent traveller

can also avoid the stresses that a lack of

productivity by influencing the organi- making it easier to take part in meetings, family time can induce.

sation to create policies that enhance the events, conferences, discussions and even Finally, employers should establish

traveller experience and reduce stress. For pitches, virtually – and it is expected that guidelines whereby employees would be

example, if employees are often required this focus will intensify as digital capabili- allowed to fly business class on long-haul

to travel on weekends, HR may work to cre- ties continue to improve. trips or book first class seats on trains when

ate a policy that allows travellers to extend A recent report on the BBC looked at travel time exceeds five hours.

their stay for a few days after completing some of the new technologies focused on

their work and enjoy some leisure time at making travel less stressful. From hotel 6. Manage travel risk

their destination. concierge services offering online check-in The events of 9/11 acted as the catalyst for

and room service at the touch of a button, introducing many standard travel risk pro-

3. Create a travel wellness programme to wireless Bluetooth padlocks for luggage, cedures today, such as systematic traveller

A travel wellness programme needs to focus tech innovations are being developed at tracking.

on specific environments that physically quite a pace – including in the exciting area Over half (51%) of companies provide

impact employees by encouraging certain of artificial intelligence (AI). no traveller safety or travel risk training to

less healthy behaviours: unhealthy eating • Teleconferencing solutions their employees.

choices and getting limited quality sleep. Teleconferencing solutions and other

These and other behaviours all increase remote technologies increasingly offer Evidence suggests that using business travel

the average physical stress load individuals companies, their employees and HR to meet face-to-face definitely results in a

would experience under normal working departments a workable alternative to net positive for multinational companies,

conditions. business travel. but we cannot ignore the science that tells

A travel wellness programme can us there can also be losses in the long term

include advice on eating healthily when • Instant translations if all too frequent travel has a negative

travelling, taking the right exercise, healthy Many well-known companies are work- impact on their employees’ health and pro-

flying, sleep and general stress manage- ing hard to perfect instant translation ductivity.

ment. Companies can also consider book- software that removes the need for Frequent, long-haul and lengthy peri-

ing rooms with hotel chains that have costly human translators and that means ods of business travel have been shown

gyms, and provide rewards for employees more international meetings may be to increase the risk of a variety of mental

who exercise while travelling. possible via video-conference or phone. and physical health problems, as well as

Combine instant translation with virtual exposing employees to security and safety

4. Use the power of technology reality and AI and there may soon be no problems. Unhealthy, tired and stressed

Advancements in technology and the devel- reason to take an international business employees who lack free time, rest periods

opment of new communications platforms trip ever again. and time for a personal life will ultimately

and solutions are giving business travellers affect a company’s bottom line.

and corporations more options when it • Virtual reality in video-conferencing To read more on this subject, down-

comes to long-distance communication. According to a leading multinational load our Whitepaper ‘BUSINESS TRAVEL –

Huge investments are being made by some technology company, wearing a virtual GOOD FOR BUSINESS, BAD FOR HEALTH?’

of the world’s leading technology firms in reality (VR) headset means participants at maxis-gbn.com

7

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018

TAXBOX 2 is the market-leading end to end premium tax database and software – a must for multi-national insurance companies and anyone working with international insurance programmes.TAXBOX 2’s ground-breaking software gives companies everything they need to ensure full compliance – enabling efficient sign-off with tax authorities in multiple tax jurisdictions. TAXBOX 2 simplifies the preparation of premium tax and parafiscal returns. It is comprised of three modules: • INVESTIAGTE • CALCULATE • GENERATE For more information please contact Ilka McHugh t : +44 (0)20 7036 8070 e : ilka.mchugh@fiscalreps.com

XL CATLIN | GLOBAL PROGRAMMES

ISSUES AND

IMPLICATIONS FOR

CAPTIVES

Matthew Latham and Alex MacInnes, of XL Catlin, addresses the potential implications of the

new IFRS 17 rule on captives

I

nsurance buyers, investors and analysts including – notably for captive owners –

have long noted the challenges involved Bermuda and the Cayman Islands. IFRS 17

in comparing insurers’ results. This is would therefore not be relevant in these

particularly the case with insurers that Matthew Latham circumstances.

are not required to report their finan- Companies in many other jurisdictions

cials using US GAAP. are obligated or allowed to report their

Among this set of insurers, there is con- Matthew Latham is XL Catlin’s head of captive pro- results using IFRS. IFRS is used in over 100

siderable variation between companies on grammes, international P&C. He is based in London jurisdictions globally, including the Euro-

and can be reached at matthew.latham@xlcatlin.com

how they measure profitability, account pean Union, Canada and Australia as well

for different types of expenses and con- as parts of Asia, South America and Africa.

solidate country-level data. Our assessment is that IFRS 17 will affect

In response, IFRS 17 was developed captives domiciled in jurisdictions where

to create a common global insurance Alex MacInnes local laws/regulations require that IFRS

accounting standard that will make it be used for entity-level reporting. For

easier for insurance buyers, investors example, a captive domiciled in Malta and

and analysts to understand and compare owned by a US-listed group may need to

Alex MacInnes, XL Catlin’s head of finance, financial

insurers’ results. It achieves this by pre- reporting & accounting, provided valuable support in

follow IFRS 17 under Maltese reporting

scribing a standard accounting method preparing this article. requirements, even though IFRS is not

for valuing insurance contracts. applicable to the listed group accounts.

The International Accounting Stand- meet the needs of regulatory/tax author- However, another captive, domiciled in

ards Board (IASB) released this new rule ities; although it notes that they could Bermuda and owned by a Spanish-listed

in May 2017. It will apply for accounting benefit from the way certain information group, most likely would not have to apply

periods starting on or after 1 January 2021, is reported on a balance sheet. IFRS 17 for local-entity reporting, since

although companies can implement it The absence of any discussion of the Bermudian insurance companies are not

before then. effect of IFRS on captives is perhaps not required to use IFRS.

surprising since, in our view, it likely will We also believe that, in most cases, the

Implications for captives: what does this have no direct impact on many if not most parent company would not need to mod-

mean for captive insurance companies? captives. ify significantly its IFRS group accounts

In all of the material published so far Nonetheless, for those captives where it to conform to IFRS 17, since a captive’s

about IFRS 17, there is no mention of cap- applies, IFRS 17 could be time and resource transactions and balances are typically not

tives. An “effects analysis” prepared by the intensive due to the heavy operational material to the overall group – although

IASB, for instance, focuses primarily on burden of implementing the standard rel- the company would need to agree on this

“listed insurance companies”. ative to the size of the captive entity. materiality assessment with its auditors.

The absence of any discussion on cap-

tives could relate to the fact that the pri- Some context What you need to know if your captive is

mary objective of IFRS 17 – making it easier Companies listed in the US, apart from required to use IFRS 17

to compare insurers’ results – is not rele- certain foreign corporations, are required The following is intended to outline only

vant to captives. to report their results using US GAAP. Since the most salient provisions of IFRS 17.

Moreover, the IASB explicitly acknowl- US GAAP is widely used and understood, However, if your captive will be affected,

edges that IFRS 17 was not developed to it is also permitted in other jurisdictions we suggest that captive managers con-

9

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018

GLOBAL PROGRAMMES | XL CATLIN

sult with their accounting/audit partners claims have been incurred, and the - changing the presentation of perfor-

about the specific ramifications of this CSM is not calculated at all. mance in the profit and loss account.

new rule on their operations.

Here’s where it starts to get technical: • IFRS 17 also requires the company to In summary, the impact of IFRS 17 on

• IFRS 17 applies to insurance contracts distinguish between groups of con- captives that are required to use it will

as opposed to entities; it also covers tracts expected to be profitable and largely depend on the nature of the con-

reinsurance contracts that are held by groups of contracts projected to be tracts involved. Short-duration, short-tail

a company. loss making. Expected losses are rec- contracts are likely to be least affected,

ognised in profit or loss immediately. partly due to the simplified approach

• It prescribes a standard accounting available for short-duration contracts,

method for valuing contracts and and partly because the discounting and

also stipulates that contracts carried “For those captives risk margin adjustments are likely to be

as assets be presented separately on less material.

balance sheets from those carried as where it applies, IFRS 17 Also, there is no specific guidance on

liabilities. how non-standard solutions like mul-

could be time and ti-line/multi-year contracts are to be

• Insurance contracts, whether car- reported under IFRS 17. This is an issue

ried as assets or liabilities, are to be resource intensive” that warrants further discussions with

reported as the total of the: fulfil- the IASB as the practical impact of split-

ment cashflows – that’s the current ting multiple risks incorporated into a

estimate of the amounts the company Captives that are affected by this new rule single contract, particularly where a CSM

expects to collect from premiums are most likely using IFRS 4 currently. Com- is required, could be problematic.

and pay out for claims, benefits and pared to IFRS 4, some of the most significant XL Catlin is currently assessing how

expenses, including an adjustment for new requirements in IFRS 17 call for: and where IFRS 17 will impact its local

the timing and risk of those amounts; - including extensive – and potentially operations. As we learn more about this

and contractual service margin (CSM) burdensome – additional informa- new accounting standard, we will also be

– the expected profit over time as the tion in the financial statements about cognizant of the potential impacts on our

insurance coverage is provided; claims liabilities, changes in risk and clients and especially our captive clients.

the effects of discounting; As new issues and implications are uncov-

• For certain contracts – including - discounting the liability for claims ered, we will continue to share our obser-

those with coverage terms less than and including an explicit risk adjust- vations with the captive community.

12 months – a simplified approach can ment when measuring it;

be used. With this method, fulfilment - recognising profits using the contractual Source: IFRS Standards, Effects Analysis, IFRS 17, Insur-

cashflows are not calculated until service margin, where required; and ance Contracts

10

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018Local Protection Global Connection Generali Employee Benefits The world’s leading Network, serving multinational companies in over 100 countries. A comprehensive range of employee benefits solutions, including Life, Disability, Accident, Health & Wellbeing, Retirement & Savings, for both local and expatriate employees. geb.com

GLOBAL PROGRAMMES | FISCALREPS

COMPLIANCE

ACROSS BORDERS

Karen Jenner, of FiscalReps, discusses the need for clarity in global programmes to ensure

multi-jurisdictional compliance needs are met

A

s increasing focus on global risk which is exempt from IPT) as: “…such

insurance programmes and amount as, with the addition of the tax

ensuring compliance con- chargeable, is equal to the amount of the

tinues, there is often a lack Karen Jenner premium”. In practice, this means that

of understanding or clarity HRMC view the gross premium to include

on who is responsible for overall compli- tax regardless of whether it is split out on

ance. In theory much onus is placed on the Karen Jenner is client director at FiscalReps. She the invoice. In Germany, however, should

insurance company, however in practice joined the company as an insurance consultant the invoice not separately identify the

and has over 25 years of experience in the insur-

the onus of Insurance Premium Tax (IPT) premium tax, the authorities may view

ance industry. She is ACII qualified and has held

compliance and filing of other indirect previous roles with AIG and Willis. Jenner provides the total premium charged to be net, and

insurance taxes falls on various parties, invaluable global technical insurance guidance to charge tax on this full amount.

depending on the type of taxes due and FiscalReps through her experience of global insur- This is the most common regime for

territories involved. ance programmes and non-conventional insurance. domestic and licensed insurance business,

Aside from who is accountable, there and outside the EU is applied to Goods and

are varying and different requirements separately identifying the premium tax Services Tax (GST) on insurance premiums

around calculation and invoicing which from the risk premium, and the insurer in Australia and New Zealand, premium

are key to ensuring full compliance on any then deducting the tax from the payment taxes in California, and also in South Africa

global insurance programme. received for onwards settlement to the for the purpose of calculating VAT.

In considering who should ‘pay’ the tax, authorities.

we are confronted with two key parties: Insurer borne tax

the tax debtor – the party who bears the Here the insurer is expected to bear

economic cost of the tax – and the tax the economic cost of the tax, and is also

payment debtor – the party responsible “There is often a responsible for filing and settlement to

for filing returns and settling taxes with

the authorities.

misconception that the authorities. The insurer should gen-

erally not invoice the tax to the insured,

Regardless of who bears the economic intermediaries do not but must deduct this amount from the

cost of the tax, the responsibilities of risk premium invoiced to the insured

the tax payment debtor can fall to vari- have any liabilities for filing and settlement. Generally, in

ous parties to the global insurance pro- this model the tax is not calculated on

gramme: arising from taxes a per policy basis, but across all risks

• Insurer on the insurer’s book of business over a

• Policyholder on global insurance fixed period. While many insurers gross

• Insured

• Intermediary or broker

programmes” up risk premiums to factor this addi-

tional cost in the total premium cost,

• Fiscal representative the insurer should not itemise the tax

amount on any policy documents or

Traditional indirect tax Although simple, the traditional model invoices. Examples of this regime are more

In this model the tax debtor is generally can cause some issues around the calcula- common in Europe, and are applied to IPT

the policyholder, with the tax payment tion method as, even across the EU, differ- in Hungary and the Non-Life Insurance

debtor being the insurer, with tax invoiced ent tax authorities look for different cal- Levy in Slovakia.

in addition to the risk premium. Responsi- culation models. In the UK Section 50(2),

bility for calculating, collecting and settling FA 1994 describes the chargeable amount Cross border

the tax falls to the insurer, with the invoice (where no part of a premium relates to a For cross-territory insurance, not includ-

12

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018FISCALREPS | GLOBAL PROGRAMMES

and paying to the authorities, in addition

to the full amount of premium invoiced by

the insurer.

It is important to consider whether the

recipient of the supply is GST/VAT regis-

tered and whether the transaction is B2B or

B2C. Other issues with this model include

understanding the place of supply rules for

services. Where the policyholder is respon-

sible for settlement, the administration is

fairly simple, with any reverse charge being

added to their period GST/VAT return. The

taxpayer may be able to recover the tax if

they are making taxable supplies.

Other parties

In global programmes where the insurer is

ing Freedom of Services (FoS), the onus in making tax declarations, communica- liable to account for the tax, the question of

of collection and settlement of indirect tions with the taxpayer, and legal juris- co-insurance arises. Unfortunately, there

taxes tends to fall on the policyholder, or diction failing to be applicable to overseas is not always a consistent approach as to

an insurer’s agent or fiscal representative. taxpayers. whether it is the lead insurer, or the lead

As ever, where there is a rule, there is an The more common result of writing and follow who are responsible for taxes.

exception: in the UK, the responsibility to non-admitted business is for a tax regime In the UK, HMRC expect each co-insurer to

make declarations on insurance under- to apply to the insurance buyer i.e. local account for IPT on their share of the risk,

written overseas remains with the insurer. insured. In these regimes the ultimate whereas in the Netherlands, the lead may

In some territories a fiscal representative is policyholder can find themself liable for account for the full tax if certain condi-

required to settle taxes on behalf of over- Income or Withholding taxes, Goods and tions are met (including the absence of a

seas insurers writing on a cross border Services tax, VAT and Stamp Duties. taxable intermediary). In France, the lead

basis. A fiscal representative is a person or is expected to account for the full IPT on a

company resident in the country of taxa- Withholding taxes contract, whereas in Germany, one EU/EEA

tion who agrees to accept joint and several Where withholding taxes apply to co-insurer can be nominated, in writing,

liabilities, together with the taxpayer, for cross-border insurance, the tax debtor is by other co-insurers to account for full IPT.

the payment of taxes due. These are legal commonly the insurer, and the tax pay- In many more countries, the law is silent.

appointments and differ from tax agency, ment debtor role falls to the policyholder, There is often a misconception that

and are a voluntary arrangement governed responsible for calculating the tax, (not evi- intermediaries do not have any liabilities

by a contract between the insurer and denced on policy documents or invoices) arising from taxes on global insurance pro-

agent. and then for deducting and withholding grammes. This is not the case. In Europe,

The fiscal representative takes responsi- the tax from the invoiced amount and set- in the UK, fees charged by an intermedi-

bility for filing all tax returns and payments tling to the authorities. With no obligation ary on policies subject to the higher rate

due on behalf of the insurer and can be a to the insurer the policyholder needs to be of IPT must be settled by the intermediary.

connected person. A captive may choose aware of the tax regime in existence and In the Netherlands, local intermediaries

to appoint a local subsidiary to act as fiscal its operation. The insurer cannot be pur- tend to be the default taxpayer, not the

representative. Other insurers may utilise sued for unpaid amounts and therefore insurer. Outside of Europe, in Australia

their own branch network, though many has no legal requirement to be aware of the where non-admitted business is written

appoint a formal independent fiscal repre- impact on their premium. This can lead to via an authorised agent in Australia, the

sentative. uncompetitive pricing in writing non-ad- agent assumes responsibility for premium

The requirement to appoint a fiscal rep- mitted business, as the insurer may choose tax compliance. In Germany, an agent

resentative has decreased over recent years to gross up premiums to avoid eroding with residence in the EU/EEA is authorised

for FoS business as it is seen to conflict with technical underwriting premiums. to receive insurance premium and take

EU principles. However a few territories It may be possible to mitigate, avoid or responsibility for premium tax settlement

still uphold this requirement (Cyprus and recover tax due depending on the terms of if authority has been delegated in writing.

Greece). Aside from FoS business there are any double tax treaty in force between the In conclusion, it is important that all par-

some notable countries where a fiscal rep- territory of the non-resident insurer and ties involved in a global programme be

resentative is required for other cross-bor- the territory of taxation. aware of who was primarily responsible

der insurance, including the Netherlands, for the compliance and the hierarchies

Denmark and Finland. This requirement GST/VAT – reverse charge in place. If tax authorities are not able to

has historically resulted from the insurer Here the roles of the tax debtor and tax recover from the tax payment debtor in the

not having a presence in the territory of the payment debtor fall to the policyholder first instance, the law often provides them

tax liability, therefore creating difficulties who is responsible for calculating the tax with the right to pursue other parties.

13

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018GLOBAL PROGRAMMES | ZURICH

THE CHANGING

INSURANCE MARKET

Paul Wöhrmann and Helene Westerlind, of Zurich, outline the benefits of having a fronting insurer

C

urrently the entire insurance now better informed about their risks and

and reinsurance market is in keep the captive share on net. These own-

a state of great change, and ers ask for cross-class balance sheet pro-

over time could become even Helene Westerlind tection (see further Wöhrmann/Cunning-

more consolidated, because the ham) which can include the reinsurance of

industry is under rising pressure. This is Employee Benefit programmes.

largely due to the steadily decreasing pre- Helene Westerlind joined Zurich Insurance in Stock- On the other hand captive owners move

mium rates leading to lower margins while holm, Sweden in 2003 as a liability claims adjuster from a non-proportional to a proportional

and subsequently moved into liability underwriting

additional capacity is entering from the reinsurance structure in order to capture

where she was responsible for both domestic and

financial market. international programme business. Westerlind was the entire arbitrage market potential by

Interestingly, we have experienced these appointed into her current role as global head of accessing the reinsurance, retrocession

trends in our current competitive mar- International Program Business for Commercial Insur- and ILS market (Amar/Braun/Eling).

ance in 2016 managing a global team of 200 FTEs

ket environment. We are seeing that large Fronting insurers are then faced with

and responsible for the international customers of

European captive owners are using their commercial Insurance. complex customer service expectations,

captives more actively (Wöhrmann/Ruof) especially if the fronting insurer is also

in order to: acting behind the captive on a retroces-

- optimise insurance and reinsurance sion panel. Such risk transfer levels require

structures proven IT interfaces between the retroces-

- bring two worlds (life and non-life) Paul Wöhrmann sion, reinsurance and insurance level.

into one reinsurance captive Therefore, it is vital that captive owners

- benefit from arbitrage opportunities select a well-rated and reliable corporate

in the markets (pricing, coverage and Paul Wöhrmann, head of Captive Services Europe, insurer capable of paying and servicing

capacity) Middle-East, Africa, Asia Pacific and Latin America, claims, which are ultimately reinsured to

- strengthen the core business of the has developed a reputation as one of the world’s lead- the captive.

captive owner ing authorities on captive strategy and was ranked Zurich has the experience required

the third most influential person in the industry by

- develop solutions for new risks to manage such complex captive owner

Captive Review in 2016. He has been with Zurich for

As a consequence, larger internationally more than 25 years and leads a team of experts which requirements on a global scale and captive

operating industrial captive owners need is located in four countries across the world. owners can expect comprehensive support

highly experienced insurance companies that is consistent, end-to-end and world-

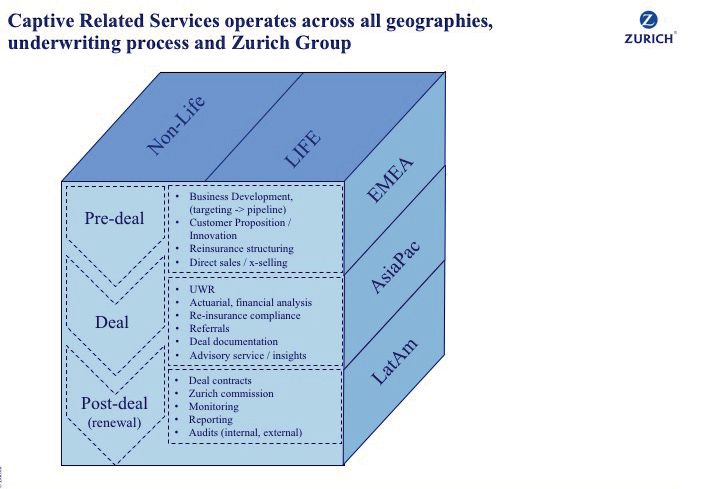

as fronting partners, to allow them effi- the financial incentive for captive own- wide (see Captive Related Services operates

cient access to the reinsurance market (see ers to influence future frequency claims across all geographies, underwriting pro-

Common Single Parent Reinsurance Cap- through active risk management and the cess and Zurich Group, p. 15).

tive Structures, p. 15). systematic identification, assessment and Zurich can provide their captive cus-

Having a captive on board allows their improvement of risk. As a consequence, tomers with so-called “captive health

owners to optimise pricing, coverage and the cost of risks can be reduced, and prof- checks” (Webinar) as a separate service.

capacity strategies across the insurance itability will be protected by introducing The individual captive retention is bench-

cycle. appropriate risk control measures, which marked across the same industry by actu-

Large European captive owners have reduce future claim frequencies and the arial methodologies. Zurich’s comprehen-

successfully started to follow such a strate- cost of premiums (Krause/Wöhrmann). sive data makes such analysis possible and

gic approach under a holistic view (life and Despite the soft market development, provides added value for captive customers

non-life/ see further Wöhrmann/Marini). we have observed that within the portfolios using this service.

In the past, the majority of captive rein- of our captive customers, there has been a Furthermore, captive owners should

surance programmes were reinsured by more active use of reinsurance captives – consider selecting one strategic insurance

fronting insurers on a non-proportional especially for large captive owners. fronting partner that can operate wherever

basis within primary layers. This is due to On the one hand, captive owners are the customer has a presence, someone who

14

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018ZURICH | GLOBAL PROGRAMMES

can cope with the increasingly complex

regulatory and tax landscape. An exam-

ple of such an increase in tax complexity

is OECD’s Base Erosion and Profit Shifting

(Beps) initiative, which may make it nec-

essary for captive owners to review their

captive set-up from a tax perspective (see

further D. San Millan and D.J. Kusaila).

An effective and professional captive

fronting partner should be able to:

• simplify management across lines of

business

• solve complex insurance problems

• access a strong and reliable global net-

work

• address insurance premium tax com-

pliance for captive programmes

• provide accurate, transparent and

timely bordereaux reporting through a

single ceding party

Customers who consider a change

in their buying behaviour for arbitrage

requirements, need an insurance partner

with a specific proposition to meet their

needs. This partner should be able to deal

with the new and growing demand by

reinsurance captives to leverage tangible

benefits of portfolio diversification and to

ensure that capital requirements are met.

At Zurich, we see arbitrage in three differ-

ent categories where captive owners can

capture tangible benefits.

Firstly, pricing arbitrage especially for

medium and high excess layers between

the insurance, reinsurance and ILS market.

Secondly, coverage and wording arbi-

trage in order to issue tailor-made insur-

ance programmes, for example on cyber

risk with wordings that meet the captive

owner’s expectations. Captives would

accept insurance policy exclusions. Hence,

the wording of the insurance coverage

could be much broader than that of the

retrocession level behind the captive. In Conclusion work infrastructure available, for a fee,

other words, the captive would cover any The current market environment provides for more lines of business. Since the retro-

deviation. attractive and comprehensive risk self- cession level, in addition to the insurance

Finally, capacity arbitrage. Capacity financing and risk transfer solutions, programmes, is often an integral part of a

arbitrage has been experienced in the which could create persistent business captive’s involvement, insurers who can

banking and mining industry. Such a solu- opportunities for various market partici- serve in a customised manner, with trans-

tion generally requires substantial captive pants. Corporate insurers which operate parent premiums and claims information,

risk retention and attention for counter- globally might find they are increasingly will be prioritised as future partners of

party credit risk matters. asked by captive owners to keep their net- captive owners.

Quotes: S.B. Amar/A. Braun/M. Eling, Alternative Risk Transfer and Insurance-Linked Securities: Trends, Challenges and New Market Opportunities, Institute of Insurance Economics I.VW-HSG,

University of St. Gallen (2015)

P. Wöhrmann/A. Ruof: “What to look for in an insurer’s captive proposition”, in: Captive Review Magazine, October 2013, p. 44 f.

P. Wöhrmann/P. Marini: Captives come of age, in: Captive Review Solvency 2 Report, October 2014, page 6 f.

P. Wöhrmann/Jean-Pierre Krause: “Are you engineering your risks effectively”, in: Captive Review Magazine, March 2014, p. 46 f.

P. Wöhrmann/T. Cunningham: Efficiency and Profitability, in: Captive Review - Global Programme Report, edition October 2015, P. 14-15

D. San Millan: BEPS not a threat to captives if used correctly: San Millan, in: Commercial Risk Online on August 9, 2017 (http://www.commercialriskonline.com/beps-not-threat-captives-used-

correctly-san-millan)

D.J. Kusaila: How Will BEPS Affect Captive Insurance?, in: Captive Review February 2016, p. 23 f.

Webinar: How To Optimise Captive Underwriting, Captive Review January 26, 2017 (http://captivereview.com/features/webinar-how-to-optimise-captive-underwriting/)

15

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018GLOBAL PROGRAMMES | AIG

GLOBAL

PROGRAMMES:

RAISING THE BAR

Carol Barton, of AIG, describes the steps the firm is taking to enhance their global programmes service offering

A

s our new chief executive Brian Larger clients with captives can take a

Duperreault commits to a new more centralised approach to local risks

era of growth, AIG is respond- and benefit from geographical diversifica-

Carol Barton

ing to the increasingly sophis- tion. Of course, captives also enable access

ticated needs of its multina- Photo by Barbie Schwartz to reinsurance markets that would not be

tional client base. Carol Barton, president available at a small, local level. And, it’s not

Carol Barton is president of AIG Multinational. She is

of AIG Multinational, explains why AIG has responsible for the worldwide leadership and strate- just large clients who benefit; more and

been making significant investments in gic direction of AIG’s multinational business as well more middle-market companies expand-

people, process and technology in order as a number of assigned countries around the world. ing outside their borders are realising the

to set a new industry standard for delivery value of a global approach and are looking

of global programmes to help clients meet ing and have the potential to lead to some to their brokers and insurers to assist.

their risk, governance and contract cer- uncomfortable questions from the C-Suite As a result, our multinational business

tainty objectives. at the time of a major event. has been experiencing exponential growth

Many risk and insurance managers of in new clients and programmes year-on-

large corporates will be familiar with the Scaling up to meet the challenge year. The AIG Global Network comprised of

challenges around structuring optimal In an increasingly global and intercon- strong local country operations and strate-

compliant multinational programmes and nected world, the past decade has seen a gic network partners is committed to deliv-

then fulfilling regulatory requirements to steady shift towards multinational insur- ering world class expertise, solutions and

enable issuance of local policies. Policies ance programmes. And this is expected to service to clients in over 215 jurisdictions

can be days, weeks or even months late as continue, particularly with new growth in around the world.

multiple stakeholders chase after missing emerging markets. Forty per cent of For-

documentation. This leads to unnecessary tune’s Global 500 multinational companies Re-engineering the process

frustration and unintended and redundant are now headquartered in Asia Pacific, In a significant effort to reshape how mul-

costs at a time when efficiency is of utmost from only 24% in 2006. From an industry tinational business is conducted, AIG has

importance in today’s globally competitive sector perspective, financial services insti- spent the last two years reengineering the

landscape. Additionally, financial and reg- tutions are leading the charge, according to process in collaboration with our broker

ulatory risks associated with not having a research by Willis Towers Watson. partners and clients. And it is no mean

contract in place at coverage inception can For large global corporate insurance feat to deliver all policies within a multina-

have a devastating impact. What if there buyers, the benefits are clear. They maxim- tional programme by inception – whether

is a loss in the days following the effective ise global insurance capacity and minimise you have exposures in 10 countries or 100.

date and the wording has not materialised? cost, while maintaining centralised con- However, this has now been achieved on

What if the claim occurs in a country where trol over risk management and risk trans- multiple occasions through close collabo-

there is no coverage if the local policy has fer practices. And in an age of data and ration with all parties, including our bro-

not been accepted and signed? Will the automation, they allow organisations to ker partners and multinational clients.

insurer be able to adjust the claim locally? consolidate and analyse loss information, Last year, we rolled out a globally con-

Can the claim settlement be made locally? enabling them to strengthen resilience by sistent end-to-end process across the full

What penalties or fines may be incurred? identifying areas of weakness or potential breadth of AIG general insurance prod-

These are just some of the concerns vulnerability before they become an actual ucts delivered around the world. This new

arising from the traditional way of work- problem. approach shifts all of the key activities from

16

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018AIG | GLOBAL PROGRAMMES

after the effective date to well in advance pre-inception policy issuance. Our award-winning MN Xpress tool

of inception. Several months later, for the Another important part of the process enables the end-to-end process by stand-

first time in our company history, we were involves scenario planning and testing, sit- ardising and automating the workflow pro-

able to deliver all local policies for a major ting around a table with all parties – includ- cess for our clients’ programmes, however

multinational client before the effective ing claims handlers – to consider how global, however complex in nature. It pro-

date, ensuring full contract certainty. Now the programme would actually respond vides territorial information and key doc-

this is not something that can be achieved in the event of a major loss anywhere in umentation requirements upfront, rather

in isolation; it is very much a collaborative the world. Such exercises challenge risk than post-purchase. Customer require-

process that relies on following pre-estab- and insurance managers to think about ments are communicated at the quotation

lished timelines with effective stakeholder what limits they really need, whether they stage well in advance of binding.

communication, so roles and responsi- The myAIG Multinational Client Por-

bilities are clear. Additionally, significant tal offers clients instant insight into their

investments have been made in tech- controlled master programme and spe-

nology to deliver tools to both simplify “We have taken our cific policy details, such as key dates and

and efficiently manage the process and premium amounts. We have taken our

advanced timeline. portal a step further portal a step further than most, ensuring

It is truly encouraging to see both cli- it captures information at a highly gran-

ents and broker partners getting excited

than most, ensuring it ular level, allowing clients to download

about these capabilities and working

together; our goal of full contract cer-

captures information at policy documents and invoices and to

tap into robust business intelligence.

tainty at inception has now become a a highly granular level” Without these technology platforms

reality for multiple clients having pro- to enable our process we would fail to be

grammes across all of our products. competitive in a rapidly-growing mar-

Feedback has been extremely positive ket. And as is always the case, it is impor-

from those who have embarked on this require local policies or can replicate the tant to keep one eye on the future. Take our

journey. So much so that we are beginning master coverage everywhere. There is no blockchain pilot with IBM that successfully

to see contract certainty become an inte- one-size-fits-all, which is why it is essen- completed a multinational programme on

gral part of the renewal conversations with tial to understand the client’s risk appetite, behalf of Standard Chartered. The pio-

our multinational clients. For example, philosophy and multinational exposures. neering programme uses blockchain to

one company is currently restructuring its manage complex coverage across the UK,

financial lines programmes with the inten- Blockchain, automation and the missing link US, Singapore and Kenya for the bank, and

tion of placing part of it out of the London Investment in technology and analytics has is certainly indicative of further efficiencies

market. Part of the discussion as they went been the secret sauce in achieving contract that are likely to be brought to the process

through this was around who could deliver certainty for multinational programmes. in the future.

17

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018SERVICE DIRECTORY

AIG FRONTING AND CAPTIVE SERVICES

Salil Bhalla, email: salil.bhalla@aig.com, Tel: +44 (0)207 954 8492

58 Fenchurch Street, London EC3M 4AB

We offer a full range of fronting and captive services. Our Captive Management Services group provides captive advisory

and managment services regarding the feasibility, structuring, formation and overall management of captives, and offers

cell captive facilities. Our programs extend to all types of exposures and industries.

www.aig.com/frontingandcap- Disclosure: Insurance and services provided by member companies of American International Group, Inc. Coverage may not be available in all

tiveservices jurisdictions and is subject to actual policy language. For additional information, please visit our website at www.AIG.com.

© American International Group, Inc. All rights reserved.

EY LLP

Paul H. Phillips III, Partner, EY Global Captive Network Co-Leader, email: Paul.Phillips@ey.com, Tel: +1 214 754 3232

2323 Victory Avenue, Suite 2000, Dallas, TX 75219

EY takes a multidisciplinary approach in addressing the alternative risk market through the EY Captive Services Team. The

EY Captive Services Team provides technical knowledge and industry experience, paired with a holistic portfolio of service

offerings (including assurance, actuarial, risk management, tax consulting, transfer pricing and compliance services) to

help clients navigate the current environment, evaluate risk and risk financing structures, reduce expenses, maintain com-

www.ey.com pliance and use capital more effectively within their organizations.

FISCALREPS

Karen Jenner, email: Karen.Jenner@fiscalreps.com, Tel: +44 (0)207 036 8070

200 Fowler Avenue, Farnborough Business Park, Farnborough, Hampshire GU14 7JP

Established in 2003, FiscalReps is an independent specialist indirect tax consultancy and market leader in premium taxes

globally serving over 400 clients. It transfers over €500m in client funds to tax authorities and processes over 25,000 tax

returns annually.

From its UK head office, FiscalReps provides clients with a guaranteed single point of contact and provides four core ser-

www.fiscalreps.com vices: Outsourcing, Technology, Consulting and Training.

GENERALI EMPLOYEE BENEFITS

Simona Frisoli, email: marketing@geb.com, Tel: +32 2 537 27 60

Avenue Louise 149, Brussels - Belgium

The Generali Employee Benefits (GEB) Network is a strategic unit of the Generali Group and exclusively focused on provid-

ing employee benefits solutions for corporate clients.

With 50 years’ experience in supporting the success of its global clients, GEB is recognized as a leading employee benefits

provider. It operates the world’s largest network by bringing together the capabilities of over 120 countries to serve more

www.geb.com than 1,500 multinational companies.

MAXIS GLOBAL BENEFITS NETWORK

Farzana Akther, email: farzana.akther@maxis-gbn.com, Tel: +44 (0)20 3876 2921

1/F The Monument Building, 11 Monument Street, London, EC3R 8AF

Co-founded by MetLife and AXA, two of the biggest and most trusted insurance companies in the world, MAXIS Global

Benefits Network is a network of nearly 140 insurance companies in 115 markets combining local expertise with global

insight. Together, we help multinational employers deliver the employee benefits they need to care for their people and

www.maxis-gbn.com meet their strategic goals.

XL CATLIN

Matthew Latham, email: matthew.latham@xlcatlin.com, Tel: +44 (0)207 933 7203

20 Gracechurch Street, London, EC3V 0BG, United Kingdom

XL Catlin. From insurance to reinsurance, a changing world needs new answers. We’re here to find them.

We are one of the world’s largest providers of global commercial insurance programs with 30+ years of network manage-

ment experience. We lead more than 70% of the 3000+ global programs we participate in. We also help clients use, opti-

xlcatlin.com mize and modify their captive structures, allowing each captive to meet its strategic goals.

ZURICH INSURANCE COMPANY LTD

Dr. Paul Woehrmann, email: paul.woehrmann@zurich.com, Tel: +41 (0) 44 628 82 82

Austrasse 46, 8045 Zurich, Switzerland

Zurich Insurance Group (Zurich) is a leading multi-line insurer that serves its customers in global and local markets. With more

than 55,000 employees, it provides a wide range of general insurance and life insurance products and services. Zurich’s custom-

ers include individuals, small businesses, and mid-sized and large companies, including multinational corporations, in more

than 170 countries. The Group is headquartered in Zurich, Switzerland, where it was founded in 1872. The holding company,

Zurich Insurance Group Ltd (ZURN), is listed on the SIX Swiss Exchange and has a level I American Depositary Receipt (ZURVY)

www.zurich.com/captives program, which is traded over-the-counter on OTCQX. Further information about Zurich is available at www.zurich.com.

18

CAPTIVE REVIEW | GLOBAL PROGRAMMES REPORT 2018WANT A CAPTIVE PARTNER THAT CELEBRATES YOUR BUSINESS AS MUCH AS YOU DO? LET’S TALK. When it comes to choosing a partner for your Captive programme, you’ll want one that has been awarded not just for its own success, but the success it brings to a client’s business. By combining global and local expertise, we can give you a solution that meets your individual needs, and together build a Captive programme everyone can raise a glass to. xlcatlin.com XL Catlin, the XL Catlin logo and Make Your World Go are trademarks of XL Group Ltd companies. XL Catlin is the global brand used by XL Group Ltd’s (re)insurance subsidiaries.

Road to the top

is full of risks —

to be ahead,

plan ahead

;gehYfa]kgh]jYlaf_afl`][mjj]flZmkaf]kk]fnajgfe]fleYqÕf\`YrYj\k`a\af_

Yjgmf\]n]jq[gjf]j&LgZ]hjm\]flYf\hj]n]fl][gfgea[d]YcY_]$]flala]kk`gmd\

hjgY[lan]dqa\]fla^ql`gk]`YrYj\kYf\kljm[lmj]l`]ajY^^YajklgeYfY_]jakcafY

`gdakla[$lYp%]^Õ[a]fleYff]j&Oal`=QÌk_dgZYdafl]_jYl]\YhhjgY[`$qgm[Yf

aehjgn][Yk`Ögo$j]\m[]]ph]fk]kYf\mk][YhalYdegj]]^^][lan]dq&

=QÌkMK;Yhlan]K]jna[]kL]Ye[Yf\]l]jeaf]o`]l`]jqgmjZmkaf]kkkljm[lmj]

Yf\gh]jYlagfkYj]kmal]\^gjY[Yhlan]afkmjYf[]YjjYf_]e]fl$]nYdmYl]qgmj[mjj]fl

jakcÕfYf[af_kljm[lmj]k$Yf\\]n]dgh^]YkaZd]Yf\]^Õ[a]flYdl]jfYlan]kÈYddlg

ka_faÕ[Yfldqaf[j]Yk]qgmj[gn]jY_]ghlagfko`ad]aehjgnaf_[Yk`ÖgoYf\]ph]fk]

eYfY_]e]flYf\j]\m[af_gn]jYdd][gfgea[[gklk&9khYjlg^=QÌk?dgZYd;Yhlan]

K]jna[]kf]logjc$=QÌkMK;Yhlan]K]jna[]kL]Yeakmfaim]dqhgkalagf]\lg]^Õ[a]fldq

©2017 EYGM Limited. All Rights Reserved.

Yf\]^^][lan]dqY\\j]kk\ge]kla[gj[jgkk%Zgj\]j'^gj]a_fakkm]kYf\Y\nak]gf

hdYffaf_ghhgjlmfala]k&

JakcakfÌl_gaf_YoYq$Yf\f]al`]jakmf[]jlYaflq&Qgmf]]\YhdYfl`Ylo]a_`kYdd

l`]ghlagfkkgl`Ylqgmjgj_YfarYlagf\g]kfgl`Yn]lgk]lld]^gj`a_`]ph]fk]k

YkYf][]kkYjq[gklg^\gaf_Zmkaf]kk&D]l=Qk`goqgm`go&

>gjY\\alagfYdaf^gjeYlagf$hd]Yk][gflY[lYfqg^l`]^gddgoaf_af\ana\mYdk&

Paul H. Phillips III Karey Dearden James Bulkowski

:mkaf]kkLYpK]jna[]k Afl]jfYlagfYdLYpK]jna[]k AfkmjYf[]Yf\9[lmYjaYd

=jfkl

Qgmf_DDH MK! =jfkl

Qgmf_DDH MK! 9\nakgjqK]jna[]k

+1 214 754 3232 +1 212 773 7056 =jfkl

Qgmf_DDH MK!

hYmd&h`addahk8]q&[ge cYj]q&\]Yj\]f8]q&[ge +1 212 773 3567

bae&Zmdcgokca8]q&[ge

Mikhail Raybshteyn Nikolaos (Nikos) Analitis Lisa Martell

:mkaf]kkLYpK]jna[]k ?dgZYd;gehdaYf[]

AfkmjYf[]Yf\9[lmYjaYd

=jfkl

Qgmf_DDH MK! J]hgjlaf_K]jna[]k 9\nakgjqK]jna[]k

+1 516 336 0255 =jfkl

Qgmf_DDH MK! =jfkl

Qgmf_DDH MK!

eac`Yad&jYqZk`l]qf8]q&[ge +1 312 879 4229 +1 312 879 5042

facgdYgk&YfYdalak8]q&[ge dakY&eYjl]dd8]q&[ge

Qgm[YfYdkg[gflY[lmkoal`qgmjim]klagfkYf\[gee]flknaY]eYad2

MK;Yhlan]K]jna[]k?jgmh8]q&[ge&

Ernst & Young LLP (EY US) Captive Services Team — Innovating Risk ManagementYou can also read