Re-entering Agflation - World Food Prices to Hit Record High

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Re-entering Agflation World Food Prices to Hit Record High

Re-entering Agflation

World Food Prices to Hit Record High

Luke Chandler

luke.chandler@rabobank.com

Nick Higgins

nicholas.higgins@rabobank.com

Rabobank International Disclaimer: This document is issued by Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A. incorporated in the Netherlands, trading as

Rabobank International (“RI”). The information and opinions contained in this document have been compiled or arrived at from sources

Agri Commodities Market Research believed to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness.

This document is for information purposes only and is not, and should not be construed as, an offer or a commitment by RI or any of its

Food & Agribusiness affiliates to enter into a transaction, nor is it professional advice. This information is general in nature only and does not take into account

Research and Advisory an individual’s personal circumstances. All opinions expressed in this document are subject to change without notice. Neither RI, nor other

legal entities in the group to which it belongs, accept any liability whatsoever for any loss howsoever arising from any use of this document

agrimarketsresearch@rabobank.com or its contents or otherwise arising in connection therewith. This document may not be reproduced, distributed or published, in whole

www.rabotransact.com or in part, for any purpose, except with the prior written consent of RI. All copyrights, including those within the meaning of the Dutch

Copyright Act, are reserved. Dutch law shall apply. By accepting this document you agree to be bound by the foregoing restrictions.

© Rabobank International Utrecht Branch, Croeselaan 18, 3521 CB, Utrecht, the Netherlands +31 30 216 0000

Contents | i

Contents

Page

Executiv e summar y . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Section 1

The price of food will incr ease fur ther . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Not a case of déjà vu for food prices: Why 2013 will be different to 2008 . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Regional effects: Asia, the Middle East and North Africa to slow demand . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Free markets are out the window when food prices are on the table . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Section 2

Global agr icultur al prices spik e, again . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Agricultural commodity prices to remain high for some time yet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Speculative influence has diminished . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Demand rationing to hit biofuels and animal protein industries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Second order impacts—the knock-on effects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Grains and oilseeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Animal protein . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Chicken . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Pork . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Beef . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Dairy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Beverages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Soft drinks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Beer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Value-added processing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Farm inputs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Executive summary | 1

Executive summary

Skyrocketing agricultural commodity prices and, consequently, we expect agricultural

are causing the world to re-enter a period of commodity prices—particularly for grains

agflation, with food prices forecast to reach and oilseeds—to remain at elevated levels

new record highs in 2013. for at least the next 12 months.

• Agricultural commodity production has This time around, the most affected

plunged as droughts in the US, South commodities are largely used in animal feed

America and Russia have diminished crop and are not core food staples of the world’s

prospects and tightened already low developing economies. This is a very different

inventory levels. scenario from that in 2008, when declining

wheat stocks and several national bans on

• The social impact should be different to

rice exports limited the amount of grains

2008 as this time around crop shortages

available for direct human consumption.

are affecting feed intensive crops such as

We estimate that world corn (soybean) stocks

corn and soybeans, rather than core food

will fall to only 51 (73) days of use at the

staples such as wheat and rice.

end of 2012/13, compared to 62 (83) days in

• Food security remains a highly sensitive 2007/08, whereas wheat and rice stocks are

issue in many regions, and we expect to expected to improve over the same period

see a return of government interventions, (see Figure 0.2). Stocks of core food staples,

which could exacerbate food and such as rice and wheat, are forecast to

commodity price volatility. comprise a larger share of total grain and

oilseed stocks in 2012/13 at 61 percent versus

• The rally in grain and oilseed prices will

53 percent in 2007/08. As a result, while corn

have a significant knock-on effect to

and soybean prices are at record highs, wheat

animal protein industries and other

and rice prices are more than 30 percent

processing supply chains−raising prices

lower than their 2008 peaks.

for meat consumers and challenging

processor margins around the globe. A more subdued non-food inflationary

environment will result in less social pressure

Food price inflation is once again

from rising food prices this time around. Non-

accelerating, triggered by the worst drought

food inflationary pressure relative to 2008 will

the United States (US) has seen in nearly a

also be reduced by weaker global growth,

century and exacerbated by droughts in

lower energy prices and reduced freight costs.

South America and Russia. Rabobank analysis

However, as in 2008, increased government

suggests world food prices may reach an

stockpiling, trade restrictions and other forms

all-time high in Q1 2013, peaking in Q3 2013

of intervention remain a significant threat as

(see Figure 0.1). In order for demand rationing

governments look to abate the local effects

to take place and encourage a supply

of higher international prices.

response, prices will need to stay high

2 | Rabobank Re-entering Agflation

The impact of higher grain and oilseed prices

will be significant for the animal protein and

dairy sectors as they are likely to be squeezed

by higher feed costs. The long production

cycles of the animal protein and dairy

industries will have lingering effects on global

food prices as herds (especially cattle) take

longer to rebuild—maintaining upward

pressure on food prices. The full effect of this

commodity price rally and the subsequent

lower meat and milk output, will be a multi-

year rebuilding of herds, which will sustain

high price levels of these products.

Meanwhile, effects on the beverages and

value-added products (VAP) sectors will be

more muted as grains and oilseeds constitute

a smaller part of the overall production costs.

Figure 0.1: Rabobank forecasts that the FAO Food Price Index Figure 0.2: Soybean and corn inventories are set to decline to

will hit new record highs in early 2013 lower levels than 2008, while wheat and rice are more abundant

550 275 110

500 250 100

global stocks (million tonnes)

450 225 90

400 200

80

index

index

350 175

70

300 150

250 60

125

200 100 50

150 75 40

Mar 01

Mar 11

Mar 00

Mar 02

Mar 03

Mar 04

Mar 05

Mar 06

Mar 07

Mar 08

Mar 09

Mar 10

Mar 12

Mar 13

Corn Soybeans Rice Wheat Combined

S&P Agri Index FAO Food Price Index (RHS) Average (97-06) 07/08 12/13f

Source: FAO, Rabobank, 2012 Source: USDA, Rabobank, 2012Section 1 The price of food will increase further | 3

1 The price of food will increase further

The coming year will likely see the world Q1 2012. These impacts, combined with

economy re-enter a period of agflation as a less certain outlook for Australian grain

grain and oilseed stocks decline to critically production, have accelerated the trend

low levels, pushing the FAO Food Price Index of decreasing inventories across the grains

above record nominal highs set in February and oilseeds complex and pushed agricultural

2011. These high food prices have been commodity prices near record highs. Global

triggered by droughts in several key growing grain and oilseed stocks are now forecast to

regions, led by the 2012 US drought, the worst decline for the third consecutive year, and

since 1936. At the end of August, severe (or higher food prices are still needed to meet

worse) drought conditions covered over the clear and present need for a reduction

42 percent of the US mainland (see Figure 1.1). in global demand.

As a result, 2012/13 grain and oilseed

Our modelling suggests that the FAO Food

production is likely to see a reduction of

Price Index will rally another 15 percent from

over 8 percent YOY, from already depressed

31 August 2012 levels to 243 points by

levels. Despite higher planted acreage, this

30 June 2013 (see Figure 1.2). July readings of

year has also seen a drought in Russia as well

the index saw a 6 percent increase after prices

as La Niña-related dryness, which impacted

had fallen during the previous four months,

the harvesting of South American crops in

although the index stagnated in August.

Figure 1.1: Drought conditions in the US are the worst since 1936, the Dust Bowl era

L S

SL

SL SL

SL

SL L

SL

SL SL

SL

L L

Drought Impact Types:

L

Delineates dominant impacts

L L S = Short-term, typically 6 months

(e.g. hydrology, ecology)

D0 Abnormally dry D1 Drought - moderate D2 Drought - severe

D3 Drought - extreme D3 Drought - exceptional

Source: USDA, Rabobank, 20124 | Rabobank Re-entering Agflation

We expect future gains in the FAO Food Price for placement onto feed lots (CME Feeder

Index to be faster in the near term, with food Cattle) are expected to increase by 6 percent

prices expected to rally 12 percent from 31 and 8 percent, respectively, over that same

August levels by the end of 2012 and growth period. Price rallies in these markets lag those

slowing to 2 percent for the first half of 2013. of grains markets due to the downstream

Peak aggregate food prices, according to our nature of the industry, with animal protein

current estimates, should therefore occur companies needing to adjust to higher feed

during the Q2/Q3 transition in 2013. costs. This involves reducing the size of the

animal herd, initially creating a supply glut,

Fundamentals remain much tighter than

which then leads to higher prices as supplies

current official market estimates, with existing

drop. Dairy prices are expected to respond

food price records, set in 2011, likely to be

more quickly as herd reductions translate into

broken as the severity of the situation

higher milk prices on a shorter scale—

becomes clear. As a result of droughts in

although rebuilding dairy herds also has a

key exporting countries and rapid demand

long cycle, prolonging any shortage created.

growth in developing countries, the

Grain and oilseed prices are not expected to

combined global wheat, rice, corn and

be major direct contributors to further food

soybean stocks-to-use is expected to fall to

price moves, with average grain prices

19.6 percent in 2012/13—only 0.4 percent

increasing 6 percent by 30 June 2013, offset

above 2007/08 levels. Combined stocks-to-

by falling CBOT Soybean prices, which we

use for these key commodities had fallen

expect to fall nearly 12 percent over the same

14 percentage points in the eight years

period. Divergence between grain and oilseed

to 2007/08. Although the timing of price

prices is driven by the relative importance of

changes remains uncertain, we believe that

South America in the oilseeds complex, where

the FAO Food Price Index provides a useful

a good harvest is expected to relieve some of

proxy for prices paid by world consumers

the supply-driven price pressure.

for food, and gives an indication of how

agricultural commodity prices may translate

Not a case of déjà vu f or f ood pr ices:

into prices at the local shop. The model uses

Why 2013 will b e diff erent to 2008

our house forecasts for commodity futures

The spike in world food prices this year is

prices, futures curves for livestock prices,

expected to ration animal feed, unlike the

and momentum factors to anticipate

staple grain shortage of 2008. We estimate

future changes.

that world grain and oilseed stocks will fall

Meat and dairy prices, which comprise to only 71 days of use by the end of 2012/13,

52 percent of the FAO Food Price Index, are the compared to 70 days in 2007/08. Despite

primary drivers of our forecast for further food the two events seeming similar, we expect

price increases (see Figure 1.3). The price of social pressure for food availability to be

pork, demonstrated by the lean hog futures lessened as consumers switch consumption

curve, is expected to rally 31 percent from from animal protein back towards staple

spot prices by 30 June 2013. Cattle ready grains—an option not available in 2007/08

for slaughter (CME Cattle) and cattle ready due to severe shortages of wheat and rice.

Figure 1.2: The FAO Food Price Index is forecast to rise to new Figure 1.3: Meat and dairy prices comprise 52% of the FAO Food

record levels in 2013 Price Index

550 275 Sugar 7%

500 250

450 225

S&POils

FAO Agri

Food14%Index

Price Index (RHS) Meat 35%

400 200

index

index

350 175

300 150

250 125

200 100

150 75 Cereals 27%

Mar 01

Mar 11

Mar 00

Mar 02

Mar 03

Mar 04

Mar 05

Mar 06

Mar 07

Mar 08

Mar 09

Mar 10

Mar 12

Mar 13

Dairy 17%

S&P Agri Index FAO Food Price Index (RHS)

Source: FAO, Bloomberg, Rabobank, 2012 Source: FAO, Rabobank, 2012Section 1 The price of food will increase further | 5

Our analysis indicates that world stocks of in five of the thirteen marketing years since

soybeans in the 2012/13 season will fall to the turn of the millennium (see Figure 1.4).

just 73 days of use (-6 YOY) while corn stocks

In fact, world wheat stocks are expected to

will fall to just 51 days of use (-4 YOY). These

end this season with 90 days of use (-14 YOY)

numbers compare to 83 days and 62 days,

and should remain considerably higher than

respectively, for the 2007/08 season. As this

the 76 days of use reached in 2007/08

season’s decline in stocks is concentrated in

(see Figure 1.5). Rice stocks are also significantly

corn and soybeans (used largely in animal

more plentiful this time around with 81 days

feeds), stock tightness can be alleviated

of use (-2 YOY) compared with just 69 days in

through reduced meat and dairy consumption.

2007/08. Export bans in major rice exporting

These effects will be masked in the shorter

countries, including India and Vietnam, were

term as higher slaughter rates temporarily

a key component of the 2008 record rally in

increase meat supply. The longer term effect

rice prices, with August 2012 rice prices of

will be reduced animal herd sizes, which will

USD 15.6 per cwt still 34 percent below the

drive down production and increase prices.

2008 peak. While there have been some

Unlike in 2007/08, higher prices will linger this

concerns with the sub-par Indian monsoon,

time, even if increased production alleviates

at this stage production has not been as

pressure on underlying grain fundamentals

adversely affected as in 2008. Additionally,

as herds take time to rebuild.

non-grain and oilseed prices have remained

The crisis of 2008 was many years in the more subdued, with sugar—a large food-

making, with stocks-to-use declining across price component—falling 16 percent YTD.

the grains and oilseeds complex beginning However, with the reference #11 sugar price

in 2000 as emerging market and biofuel trading at USc 20 per lb, prices remain well

demand accelerated. The 2008 crisis was above the 2008 average price of USc 12 per lb,

a signal that there was not enough growth with prices declining from their peak of USc

in production or investment in agriculture 35 per lb in February 2010.

to meet the accelerated growth rate in

Meat consumption will be significantly more

consumption. The subsequent price response

affected than the consumption of grain

incentivised the largest grain and oilseed

(e.g. bread) as demand rationing will be

harvest ever in 2008/09. However, the record

focused in the feed grains complex. One

crop was not sufficient to rebuild depleted

direct consequence of this, due to the long

inventory levels as consumption growth

animal protein and dairy production cycles,

kept pace with production increases.

will be that price effects will linger longer as

Ultimately, prices dropped and output

herds (especially cattle) take longer to rebuild.

faltered in 2010/11, prompting another

As herds are liquidated this will increase

agricultural commodity rally. The coming

supplies in the short term and depress prices.

decline in world grain and oilseed stocks

In the medium/longer term this will maintain

reinforces the longer term trend of

upward pressure on food prices as meat

consumption surpassing production,

and dairy supplies contract.

with production only outpacing supply

Figure 1.4: Combined world stocks-to-use for wheat, rice, corn Figure 1.5: Combined world stocks-to-use for wheat, rice, corn

and soybeans began to decline in 1999/2000 and soybeans improved following 2007/08, but are forecast

to decline for the third consecutive year in 2012/13

34 2,400 120

32 2,300 110

days of use (world stocks)

30 2,200 100

million tonnes

28 2,100 90

percent

26 2,000 80

24 1,900 70

22 1,800 60

20 1,700 50

18 1,600 40

00/01

10/11

99/00

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

11/12

12/13f

07/08

08/09

09/10

10/11

11/12

12/13f

Stocks/use Consumption (RHS) Production (RHS) Corn Soybeans Rice Wheat Combined

Source: FAO, Rabobank, 2012 Source: USDA, Rabobank, 20126 | Rabobank Re-entering Agflation

Low growth, lower oil prices and weaker that the share of global demand reduction

consumer confidence levels are all likely to will be proportionally larger in the Middle

lessen the impact of higher food prices this East, North Africa and Asia, where demand

time around. Persistent economic output is more elastic and where lower incomes

gaps relative to pre-2008 levels have recently drive consumers to reduce animal protein

contained, and will likely continue to contain and milk consumption in favour of staple

inflationary pressures. This is an important grains (see Figure 1.7).

difference compared to 2007/08 as there was

Higher prices will stall the long-term trend

no output gap in that period and broadly

towards higher animal protein diets in

based inflationary pressures drove food prices

developing economies. Rabobank expects

higher. The US dollar—the currency commonly

the developing world—with its high demand

used for pricing world grains—has depreciated

elasticity, especially to meat—to ration import

11 percent since its peak in late 2008, which

demand of grains, oilseeds and meat most

also helps to alleviate the food price pressures

heavily, leading consumption growth to slow

of the first half of 2012 in importing nations.

and even recede for a period as prices rise.

Crude oil prices are lower than in 2008,

Ultimately, the extent of this season’s price

reducing bullish pressure on input costs such

hikes for corn and soybeans is likely to reduce

as fertiliser and fuel, which are highly related

meat consumption growth in the coming

to energy prices, and therefore alleviating

years, moving counter to the longer term

some pressure on agricultural commodity

trend of increasing animal protein

prices (see Figure 1.6). Despite this, some

consumption. This is a form of demand

pressure remains, with a mild US economic

rationing—as on a calorie-for-calorie basis

recovery underway, strong emerging market

meat and dairy products require multiples

growth, and geopolitical tensions in the

of grain inputs used in direct grain

Middle East inducing average prices of over

consumption—and will reduce pressure

USD 110 per barrel for Brent crude oil over

on global grain and oilseed balance sheets.

the last 12 months. If economic growth picks

up and oil prices rise, there could be further Meat demand reduction in the Middle East

bullish pressure on agricultural commodity and North Africa is likely to cut grain imports

prices in 2013. 9 percent YOY in 2012/13. Meat price elasticity

in these regions averages -0.5, in line with

Regional eff ects: Asia, the M iddle E ast Asia, but likely understates the true sensitivity

and N or th Africa to slo w demand to price increases due to high income, small

Rabobank expects that emerging market population states such as Kuwait. However,

demand for animal proteins will be most reduction in grain import demand in some

affected by higher food prices. Although high countries (Morocco is one such case) will be

prices will be felt chiefly in the meat and dairy limited by post-Arab spring wariness as

sectors, and although the developed world higher prices for staple grains are commonly

consumes a disproportionate share of these considered a key catalyst for the kind of

products, food makes up a smaller share of unrest seen in recent years. In order to limit

developed world budgets with consumers the risk of another period of widespread

less responsive to price changes. This means social unrest, governments in these regions

Figure 1.6: Agricultural commodity prices and energy prices

remain strongly correlated

600 160

550 140

500

120

450

index value

100

USD/barrel

400

350 80

300 60

250

40

200

150 20

100 0

2000

2002

2004

2006

2008

2010

2012

Brent Crude Oil S&P Agri Index (RHS)

Source: Bloomberg, Rabobank, 2012Section 1 The price of food will increase further | 7

Figure 1.7: Meat price elasticity of demand is highest in the developing world where meat comprises a larger share of household budgets

Very high (-.50 to -0.65)

High (-.45 to -0.50)

Medium (-.40 to -0.45)

Moderate (-.25 to -0.40)

Low (-.25 to -0.35)

No information available

Source: USDA, Rabobank, 2011

may choose to keep domestic prices imports will remain supported with the

artificially low. Large hard-currency reserves, region maintaining a share of nearly a third

generally derived from oil export revenue, of global wheat imports (see Figure 1.8).

provide additional support for government

Asian demand is also expected to decline as

purchases. Despite this, Rabobank expects the

increasing prices interact with high animal

regions to import under 78 million tonnes of

protein demand elasticity, with much of the

grain in 2012/13—the lowest amount since

region lacking protectionist policies. Although

2007/08. Imports would be even lower, but

the region may move to adopt more

base import demand has been increased due

protectionist measures (see pages 9 to 11)

to lower yields in 2011/12 in grain producing

we believe that higher food prices will

areas of North Africa. Although feed grain

ultimately lower animal protein consumption,

demand is likely to fall, we expect that staple

and therefore reduce meat imports.

Figure 1.8: The Middle East and North African regions rely heavily on grain and oilseed imports,

comprising a third of global wheat trade

Tunisia Syria

Afghanistan

Morocco Israel Iraq Iran

Jordan

Kuwait

Algeria

Libya Egypt

Saudi Arabia

Oman

Yemen

Share of global wheat trade8 | Rabobank Re-entering Agflation

Meat price elasticity averages -0.52 in South of the recent rally is expected to be more

Korea, Vietnam, Malaysia and Indonesia. Even benign, with the recent rally in international

if governments undertake protectionist prices seeing them gain (but not meet)

measures to encourage imports, as mooted higher Chinese prices (see Figure 1.9).

by South Korea in early August, we expect

Domestic inflationary pressure will also

that animal protein imports (chiefly those

be alleviated by falling asset prices as the

from the US) will fall as the US domestic

Shanghai Composite Equity Index, down

animal protein sector is squeezed by higher

14 percent from its May 2012 peak, is

costs. In this way, we see much of the decline

correlated, with a nine-month lag, to

in US feed demand, and subsequent meat

food price inflation (see Figure 1.10). This

production, ultimately falling on Asian

relationship between equity prices and food

consumption—tempering the recent trend

price inflation suggests that wealth effects

of rapidly increasing US meat exports into

may drive part of Chinese households’

this region.

consumption behaviour. Lower perceived

Demand rationing is expected to be limited wealth may therefore temper growth in

in China, the world’s largest net importer of per capita meat consumption.

food, with net imports of grains and oilseeds

Demand from developed net importing areas

increasing to new record highs in 2012/13.

is generally unresponsive to changes in food

This will see net imports jump 19 percent to

prices. Europe and Japan are the second and

89 million tonnes in the 2012/13 marketing

third largest importers of global grains and

year, with soybean imports the chief driver of

oilseeds, respectively. They are also the only

demand—although corn and wheat imports

developed economies included in the world’s

are also expected to increase. Soybean

top 30 importers. Demand for grains in these

imports, of which China imports 70 percent

countries is so inelastic that responsiveness

of world trade, are expected to be 62 million

to price changes is statistically zero—though

tonnes in 2012/13, a 4 percent increase YOY.

higher meat elasticity is expected to result

Despite higher prices, it is the government

in some reductions in animal protein

rather than consumers that will face

consumption. Despite low price elasticity, we

international markets, muting the

expect demand in Japan and Europe will slow

transmission of higher prices to the Chinese

marginally, with importing end users acting

consumer. The Chinese government’s ability

to protect profits through stock drawdowns,

to act quickly was exemplified by the

but otherwise ultimately able to pass higher

21 August announcement that China will

prices through to the consumer. However,

redistribute commercial importers’ unused

longer term consequences of food price

2012 quotas for wheat, corn, rice, sugar and

inflation may be particularly visible in Europe,

cotton (there is no soybean quota). This

potentially increasing pressure on

signals the Chinese government’s desire

governments to repeal bans on growing

for imports to continue. Chinese domestic

genetically modified (GM) crops or to reverse

prices for corn and soybean have been above

biofuel mandates. Stagnating economic

USD 8.00/bu and USD 16.00/bu, respectively,

growth provides additional support for this

since early 2011. Therefore, the price shock

Figure 1.9: Chinese soybean prices have long been higher than Figure 1.10: China’s food prices are closely correlated to the

those in the US (and internationally) with the recent rally performance of financial assets, such as the Shanghai

seeing the margin decrease Composite Equity Index presented below

850 7,000 30

750 6,000 25

20

650 5,000

USD/tonne

15

550 4,000

percent

index

10

450 3,000

5

350 2,000

0

250 1,000 -5

150 0 -10

2005

2006

2007

2008

2009

2010

2011

2006

2007

2008

2009

2010

2011

2012

Dalian Soybeans CBOT Soybeans Shanghai Composite CPI - Food (RHS)

Source: USDA, Bloomberg, 2012 Source: NBSC, Bloomberg, Rabobank, 2012Section 1 The price of food will increase further | 9

hypothesis as cost conscious consumers are developing nations—a figure which expands

more likely to react to higher meat prices, to 27 percent once fish and dairy

increasing the popularity of policies that consumption are included—which means

increase grain production and reduce prices. an increase in commodity prices will have a

larger impact on household budgets in these

Rising feed costs will have a substantial

regions compared to developed countries.

impact on the US livestock industry but

With food comprising such a large share

domestic meat consumption will be less

of spending, especially in Asia, increases

affected. The US has the lowest meat price

in food prices could possibly have knock-

elasticity in the world, with consumption

on effects in demand growth of other

least likely to drop in response to higher

commodities and consumer spending

prices. However, the effects on the US

more broadly (see Figure 1.12).

livestock complex will be extensive and,

despite inelastic domestic demand, meat

Free mar kets ar e out the windo w

product exports are likely to fall. The US

when f ood pr ices ar e on the table

became a net exporter of animal protein in

Increases in commodity stockpiling and

2006, with rapid increases in Asian demand

other interventionist measures, such as export

driving exports up by 14 percent per annum

bans, are a distinct possibility in 2012/13

since (see Figure 1.11). Relatively inelastic

as governments react to protect domestic

demand in the US should see this trend

consumers from increasing world food prices.

reversed in 2013, with meat imports rising

Rabobank sees Asian and Middle Eastern

while exports fall as other countries are

countries as the most likely first movers, with

unable to afford the higher prices that US

large foreign currency reserves and large

exporters will demand. This trend could be

portions of household expenditure exposed

exacerbated by increases in grain stockpiling

to food prices encouraging early action to

as other nations protect domestic industries

protect social order (see Figure 1.13).

and consumption, supporting US grain and

Increased government intervention will likely

oilseed exports while slowing the animal

add to increasing world commodity and

protein export complex.

food prices with domestic stockpiles meaning

Ultimately, we expect that the effects of that a larger portion of already low global

higher global prices will be contingent upon stocks sits idle. We expect that localised

the political sensitivity of higher price moves efforts to increase stockpiles would be

as well as the size of government foreign counterproductive at the global level, with

reserves. We believe that many of the largest those countries least able (or willing) to pay

importing countries will be able to stabilise higher prices likely to see greater moves

domestic prices by implementing domestic in domestic food price inflation. This is a

procurement programmes, which could vicious circle, with governments committing

offset the effects of higher global prices to domestic stockpiling and other

and cushion domestic consumption. interventionist measures earlier than

Grains, oilseeds and meat make up at least usual—recognising the risk of being left

20 percent of discretionary income in out as exportable stocks decline further.

Figure 1.11: US pork, veal and beef exports should come under Figure 1.12: Food comprises a much larger share of consumer

pressure as Asian importers reduce demand due to budget in Asia than in higher income countries,

higher prices such as the US Exports

production

4 25 50

3.5 45 Imports

23 40

3

35

21

million tonnes

million tonnes

2.5 30

percent

2 19 25

1.5 20

17 15

1

10

15

.5 5

0 13 0

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

Philippines

India - CPI

Vietnam

Indonesia

Thailand

China

Malaysia

Hong Kong

Taiwan

Singapore

Korea

US

Imports Exports Production (RHS)

Source: USDA, Rabobank, 2012 Source: Bloomberg, Rabobank, 201110 | Rabobank Re-entering Agflation

Figure 1.13: Higher food prices had significant geopolitical consequences in 2008 as riots occurred in many regions

Food riots, 2007-2008

Source: USDA, Rabobank, 2011

Russian export bans may not be imposed, but • A Mexican entity purchased the fourth-

we expect the effects to be similar, with largest single order of corn ever from the

demand for exports in the Black Sea region US. A chicken import tariff was introduced

outstripping available supplies for export. in response to reported US dumping of

These pressures have risen again due to chicken legs and thighs.

intense drought crippling Black Sea wheat

• South Korea is currently considering

production. Grain export bans, emanating

whether to introduce a domestic

from the Black Sea region—led by Russia—

purchasing regime for grains and oilseeds.

have historically been a threat to grain price

stability, although recent comments by the • China’s soybean purchases show little to

Russian government suggest bans are no sign of slowing down, with 12 million

unlikely in the near term. We expect that if tonnes of the 2012/13 US soybean crop

export bans are not imposed by Russia, sold—a 14 percent increase in new crop

internal Black Sea region trade will grow to sales compared to this point in 2011.

see Kazakhstani wheat moved into Russia in

• Iran—a country that is usually self-

early 2013 to offset the rapid pace of Russian

sufficient in wheat, importing only

exports seen in Q3 2012. This will have an

0.5 million tonnes in 2010/11—has

effect similar to an export ban: reducing the

reportedly transacted several sales of over

available Black Sea region surplus, albeit with

1 million tonnes of wheat from both

lower near-term price volatility. This solution

Pakistan and India, and purchases of rice

still means the market has to adjust to lower

and corn could follow, placing further

wheat supplies but delays the impact—

pressure on global grain and oilseed

kicking the can further down the road.

balance sheets.

Rabobank has been monitoring several

• Indonesia is repealing import tariffs on

events that could be the beginning of a

soybeans to protect domestic tofu

trend towards larger government purchases

processors, and has announced plans to

in 2013.

increase grain stockpiles.Section 1 The price of food will increase further | 11

Expectations of further increases in food

prices and high supply uncertainty will see

competition for world food inventories

increase, resulting in reduced stocks in major

exporting countries. China and India have

increased their shares of global stocks in

the past five seasons in order to combat high

domestic prices (see Figure 1.14). The

increasing shares of China and India have

come at the expense of US inventories; the US

is forecast to have 11 percent of global stocks

in 2012/13, down from 20 percent in 2005/06.

As the scale of damage to the US corn and

soybean crops becomes more apparent,

Rabobank expects there will be a renewed

tendency to increase domestic stockpiles in

China, but this will be constrained by the low

supply. As US stocks have continually fallen

since 2005/06, and are now at pipeline levels

for most grains and oilseeds, further increases

in US exports to support stockbuilding

in China are not possible. Chinese imports

will have to originate from further afield,

increasing competition and disrupting

traditional trading partnerships. Other

countries will therefore have to outbid

incremental Chinese demand, placing

further pressure on agricultural commodity

prices. Given the high prices and low

availability of exportable supply, we

anticipate the Chinese share of global

stocks will fall in coming seasons as their

strategic reserves are drawn down.

Figure 1.14: The share of wheat, rice, corn and soybean stocks held

by the world’s largest countries has declined since 1999/2000

100

90

80

global stocks (percent)

70

60

50

40

30

20

10

0

00/01

10/11

97/98

98/99

99/00

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

11/12

12/13

China India US Other

Source: USDA, Rabobank, 2012Section 2 Global agricultural prices spike, again | 13

2 Global agricultural prices spike, again

Global grain and oilseed prices are currently Many comparisons have been made to the

experiencing their third major rally in only devastating drought of 1988, when corn

five years as a combination of adverse production fell 31 percent YOY. However,

weather and robust demand keeps global according to heat and precipitation records,

stocks at record low levels (see Figure 2.1). the damage to this year’s crop may be even

As often occurs in major agricultural price more severe. June to August precipitation and

rallies, the trigger in 2012 has been a heat in the central US, where most of the US

weather-induced supply shock. This has row crops are produced, is likely to result in

been supported by a sustained period of the least favourable growing conditions seen

strengthening agricultural commodity since the Dust Bowl (peaking in 1936), and

demand; all the while, inventory levels have the third worst in over a century. Our crop

been unable to be replenished. Over the past modelling indicates that there may still be a

five seasons, low grain and oilseed stocks considerable downside from current official

have left the market without any buffer to production forecasts, which reflects our bias

adverse growing conditions. This is a short- that prices are unlikely to have reached a high

term versus long-term problem, with the at this stage of the season. The market may

short-term supply response thus far unable still need to price in further reductions to

to meet the requirements of longer term output as well as a risk premium associated

demand for feed grains to supply the animal with the coming South American crops.

protein consumption growth in emerging

Production setbacks this season have not

market economies and the rapid acceleration

been limited to the US, with a number of key

in world biofuel demand experienced over

regions suffering adverse seasonal conditions

the past decade. Given the inability for prices

in 2012. Widespread droughts in South

to incentivise a sufficient supply response

America and Russia together with a sub-par

during these recent price rallies, we expect

Indian monsoon, disease issues in China and

the 2012 price reaction will need to be

some dry conditions in Western Australia,

strong and sustained.

have all negatively impacted world grain and

The primary catalyst of the current oilseed production this season. We estimate

agricultural price rally has been devastating that this season’s adverse weather has slashed

droughts in the US, South America and Russia, over 165 million tonnes from the global grain

which have slashed grain and oilseed and oilseed balance sheet. Taken together

production expectations. US corn production with already tight stock levels coming into

is now forecast to fall 29 percent below the season, this underscores the need for a

initial USDA expectations, a 14 percent relatively unprecedented amount of demand

decline YOY and the lowest level in nine rationing in the global grains and oilseeds

years, despite record plantings this season. sector. Global corn consumption is likely to14 | Rabobank Re-entering Agflation

Figure 2.1: Wheat, corn and soybean prices are experiencing

their third major price rally in five years—setting records for

soybeans and corn

18

16

14

12

USD/bushel

10

8

6

4

2

0

2011

2003

2004

2005

2006

2007

2008

2009

2010

2012

CBOT Wheat CBOT Corn CBOT Soybeans

Source: Bloomberg, Rabobank, 2012

decline YOY for the first time in 17 years. However, we still expect prices to remain

However, total global grain use is likely to above long-run average levels, unless there

exceed production for the seventh time is a major demand shock in the market, such

in 14 years. as a major policy change (e.g. biofuels) or a

global recession.

Agricultur al commo dit y pr ices

The scale of the production setbacks this

to remain high f or some time y et

season will underscore the need for an almost

Record high agricultural commodity

unprecedented amount of demand rationing.

prices will be required over the next 12 to

We believe that this will be a much more

24 months in order to cut demand and

difficult task than current livestock and

encourage a production response from

ethanol production margins would suggest.

the world’s farmers next season. We expect

Entrenched demand, feedback effects from

agricultural commodity prices will peak

animal protein price increases, hedged

somewhere between Q4 2012 and Q1 2013

production margins within the hog and

as new crop prospects in Brazil and Argentina

cattle sectors and the US ethanol mandate

are showing signs of trend line yields being

(Renewable Fuel Standard-RFS) will likely

achieved for corn and soybeans. Beyond this

mean that elevated agricultural commodity

period, we anticipate an easing in prices if

prices will be required for the entire

seasonal conditions normalise and world

marketing year and beyond in order to

inventory levels can recover (see Figure 2.2).

sufficiently limit both US and global use.

Figur e 2.2: Rabobank quar terly a verage gr ain and oilseed pr ice forecasts

Q4’09 Q1’10 Q2’10 Q3’10 Q4’10 Q1’11 Q2’11 Q3’11 Q4’11 Q1’12 Q2’12 Q3’12 Q4’12 Q1’13 Q2’13

Wheat (CBO T) USc/bu 522 496 467 653 707 786 745 690 615 643 642 860 880 900 920

Wheat (Matif ) EUR/tonne 129 125 132 200 225 252 233 199 186 210 212 255 261 267 273

Corn USc/bu 386 370 355 422 562 670 731 696 620 641 617 790 800 810 820

Soybeans USc/bu 1,002 955 957 1,035 1,245 1,379 1,361 1,356 1,175 1,272 1,426 1,725 1,685 1,600 1,450

Soy oil USc/lb 38.1 38.6 38.1 40.2 51.0 57.0 57.2 55.7 50.6 52.9 52.2 53.0 52.5 52.0 51.0

Soymeal USD/ton 306 278 281 305 338 367 353 352 302 339 413 510 490 420 375

Palm oil MYR/tonne 2,309 2,577 2,527 2,650 3,293 3,675 3,362 3,097 3,016 3,219 3,245 2,850 2,900 3,000 3,100

Source: Bloomberg, Rabobank, 2012Section 2 Global agricultural prices spike, again | 15

Several key factors are likely to support commodity prices are needed to encourage

US domestic demand, reducing world export improved production in South America, the

availability and supporting prices into Black Sea region and the US in the short term.

2012/13 and beyond as global grain and High fertiliser prices, which are linked with

oilseed stocks decline more than expected: stubbornly high energy prices, remain a

key cost of production for agricultural

• US broiler egg sets are up 1 percent YOY,

commodities (see Figure 2.3). Other rising

and chick placements are flat YOY as of

production costs, such as improved seed

8 September.

technology and rising land rents, will also

• The US pork industry had the opportunity prove to be increasing hurdles to farmer

to use futures markets to lock in profit profitability, and will require higher prices

margins for 2012, which would likely as an incentive to invest in expanded

shield margins from rising feed costs production. Additionally, the bulk of potential

until 2013. acreage gains are in countries with high

political risks, causing a larger risk premium

• US consumers are able (and historically

to be associated with the investments

willing) to pay high prices for animal

required. Despite these opportunities to

protein. The USDA estimates that the US

build production, it is unlikely that inventories

has the most inelastic meat demand of

will be substantially rebuilt in only one

any country.

season, with consecutive seasons of

• Despite the US ethanol mandate, use favourable conditions and increased

is likely to prove inelastic even if the plantings required to alleviate the pressures

mandate is relaxed as oxygenate of low inventory levels within the global

requirements and strong blending grains and oilseeds complex.

margins above USD 0.60 per gallon

Weather risks remain, with intensifying

support demand.

concerns in Russia, India and Western

• Declining corn use for ethanol Australia, supporting wheat prices

production also detracts one-third of and limiting the amount of wheat-for-corn

a bushel of distillers dried grains (DDG) substitution in global feed rations. Wheat

feed for every bushel used for ethanol— substitution in feed rations has been a major

intensifying soymeal and corn use in feed mitigating factor to short corn supplies in

rations. We expect there to be a loss of the past 12 months. However, weather risks

4.5 million tonnes YOY of high protein are threatening production in major wheat

DDGs production in the 2012/13 producing regions, namely Russia, where

marketing year. wheat production is now forecast to fall

30 percent YOY, albeit from record high

The incremental cost of increasing

levels. Given the magnitude of the wheat

agricultural output, which is vital to rebuilding

production shortfall in Russia, there are

global buffer stocks, is growing larger and

lower estimates of available export surpluses.

supporting higher equilibrium agricultural

Restrictions on exports are likely to come

commodity prices. Higher agricultural

either in the form of a ban or Russia importing

Figure 2.3: Despite lower oil prices than in 2008, cost of US corn Figure 2.4: Substantial threats to rebuilding stocks from

production remained higher as land rental and seed prices current levels remain, with rice yields likely to deteriorate

rose strongly if El Niño eventuates

700 3 24

600 2 18

500 1 12

USD/acre

0 6

percent

400

index

300 -1 0

200 -2 -6

100 -3 -12

0 -4 -18

2000/01

2010/11

1990/91

1995/96

2005/06

2011

2012f

2013f

2005

2006

2007

2008

2009

2010

Seed Fertiliser and chemicals

Fuel, lube, and electricity Land rental equivalent Other Rice yield Southern Oscilation Index (RHS)

Source: USDA, Bloomberg, Rabobank, 2011 Source: BOM, USDA, Bloomberg, Rabobank, 201216 | Rabobank Re-entering Agflation

Kazakhstani wheat, removing Black Sea weather-risk premiums during early phases

region wheat from the international market. of the growing season. This will be especially

evident during the first half of the calendar

A strengthening El Niño pattern threatens to

year when Northern Hemisphere summer

erode non-US seaborne grain supplies as the

row crops are being planted.

Australian East Coast growing areas often

experience drought during El Niño periods.

Specula tiv e influenc e has diminished

The risk of lower Australian East Coast

The recent rally in global grain and oilseed

production this season seems relatively minor

prices has been predominantly driven by

as precipitation to date has been sufficient,

fundamentals. The speculative positions in

although a lack of moisture on the West Coast

corn, the most heavily traded agricultural

still stands to reduce production from last

futures market have been lower than the

year’s record crop. El Niño would also place

previous price rally in 2010/11. A possible

pressure on global rice balance sheets with

reason for this is the uncertain macro

global yields historically correlated to the

environment this time around, due to

Southern Oscillation Index as dryness

economic troubles in the EU and slowing US

hampers planting (see Figure 2.4). These

growth, which has created a more cautionary

ongoing production risks are another

environment. However, there has been a

factor that will likely keep global grain and

significant inflow of investor money as the

oilseed prices at elevated levels over the

severity of the US drought became clear.

next year due to the need for increased

weather risk premiums. Managed money has doubled its net long

position in the agricultural complex, growing

Longer term agricultural commodity prices

from 430,160 contracts to 811,152 contracts

are expected to be supported by the

since mid-June, but down from 2010 peaks

increased number of extreme weather events

(see Figures 2.6 and 2.7). Over half of the

which continue to hamper inventory building.

increase has come from position building

Extreme weather reduces the ability of global

CBOT Corn contracts with managed

growers to respond to increased demand,

money net long positions rising from

with heat stress during critical summer

260,154 contracts to 323,629 contracts over

periods offsetting higher planted acreage

the period. This inflow of long positions may

and increasing pre-harvest abandonment.

have helped sustain the upward momentum

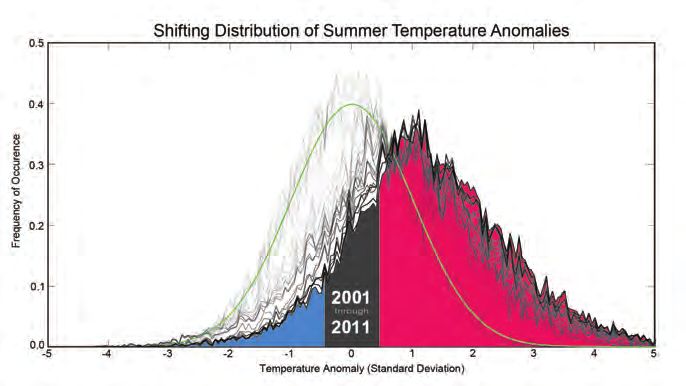

Heat stress risks were recently highlighted

of prices. However, the direction and for

in a multi-decade study by NASA showing

the most part, the magnitude of the price

mean summer temperatures and volatility

move needed have been the result of

increasing uniformly since the 1960s

fundamentally driven events this season.

(see Figure 2.5). Price shocks as a result of

low grain and oilseed stocks will likely Evidence from recent rallies demonstrates

continue to be exacerbated by adverse differing outcomes with speculators

weather. Subsequently, we expect commodity withdrawing 92 percent of their net long

prices in futures markets to reflect increased positions following the 2007/08 peak, and

Figure 2.5: Changing temperature anomalies, as observed by NASA, show volatility has been

increasing; the flattening of this distribution shows that a wider range of extreme temperatures is

now occurring compared to past decades

Reference years 1951 to 1980

Source: NASA/Goddard Space Flight Center GISS and Scientific Visualization Studio, Rabobank, 2012Section 2 Global agricultural prices spike, again | 17

prices falling 47 percent over the same evident in reduced ethanol production in

period. However, the next largest drawdown the US and then, as hedge coverage declines

in net long positions, -73 percent in 2011, into Q1 2013, in the North American animal

saw prices fall 26 percent, suggesting that protein sector. Ethanol production will remain

fundamentals following this period required a feature in the US, although it will decrease

still higher prices than speculators were for the first time in 17 years in 2012/13. There

willing to bet on. If fundamental data are indicators that this decrease may begin

continues to deteriorate, and demand soon, with current ethanol production margins

for agricultural commodities proves as near the worst in the industry’s history.

entrenched as we forecast, speculative net

World feed consumption demand is nearly

longs in the agricultural complex should

impervious to price shocks in the short term,

continue to rise, surpassing record levels set

with global demand rising in 36 out of the

in September 2010. Further supporting the

last 47 years and only declining 5 percent YOY

fundamental, rather than speculative, backing

on two occasions in the 1974/75 and 1988/89

of the 2012 rally is that much of the gain in

marketing years (see Figures 2.8 and 2.9).

prices pre-dated the speculative increases.

This remains the most difficult portion of

This is in sharp contrast to 2008.

the balance sheet to forecast as strategic

geopolitical decisions, including stockpiling,

Demand r ationing t o hit biofuels and

tariffs and export bans, will determine how

animal pr otein industr ies

much strain is placed on major grain and

Demand rationing for grains and oilseeds use

oilseed exporting nations—the largest of

is expected to be strongest in the US ethanol

which is still the US. Rabobank expects

industry, where corn use is expected to

combined global soybean and corn trade of

fall 11 percent YOY in the 2012/13 season.

191 million tonnes in 2012/13, up 4 percent

Although US ethanol and short-term animal

YOY, spurred by Chinese soybean demand.

protein production are both relatively

This will place further pressure on the US

inelastic, the scale of the US drought will

internal stock situation and, ultimately, prices

require significant demand destruction across

for consumers. This will especially be the

both industries, in order to contain shortages

case if government stockpiling increases

in feed grains. Importantly, we see declines

and low demand elasticity means larger price

in ethanol use happening within the bounds

increases are needed in the US as a result.

of the ethanol mandate, dictated by the

needs of gasoline refineries, with further Diminished US soybean production and

declines possible (but not likely) whether or subsequent evidence of inelastic Chinese

not the mandate is waived in the near term. demand suggest higher prices are needed

Global corn and soymeal use for animal feed to ration demand in 2013. Prices for soymeal

is forecast to decline over 6 percent from and soy oil have also risen, maintaining crush

initial 2012/13 USDA estimates in May, margins, and driving import demand for

although it is still set to rise 1 percent from China. Soymeal is seen as the limiting factor

2011/12 levels. Rabobank expects that in the oilseeds complex, demonstrated by its

demand rationing will initially be most 69 percent outperformance of soy oil YTD.

Figure 2.6: Net long positions by managed money in the Figure 2.7: Speculative net longs have been relatively more

agricultural complex have increased to levels seen in 2007/08 concentrated in the grain and oilseed complex during the

but are below 2010/11 highs current agricultural commodity rally

1,400 600 1,400

1,200 550 1,200

thousand contracts

500 1,000

thousand contracts

1,000

450 800

index

800

400 600

600

350 400

400 200

300

200 250 0

0 200 -200

Jun 10

Jun 11

Jun 12

Jun 06

Jun 07

Jun 08

Jun 09

2011

2006

2007

2008

2009

2010

2012

Managed money net length S&P GS agri commodity Index (RHS) Grains and oilseeds Soft commodities Livestock

Source: CFTC, Liffe, Rabobank, 2012 Source: CFTC, Liffe, Rabobank, 201218 | Rabobank Re-entering Agflation

Figure 2.8: Global feed use in the grains and oilseeds complex Figure 2.9: History suggests that significant, and recurrent, price

has increased in 36 out of the past 47 marketing years despite increases are required to significantly ration global feed demand

escalating prices

450 900 20 80

400

800 15 60

350

300 700 10 40

million tonnes

USD/tonne

percent

percent

250

600 5 20

200

150 500 0 0

100

400 -5 -20

50

0 300 -10 -40

70/71

90/91

66/67

74/75

78/79

82/83

86/87

94/95

98/99

02/03

06/07

12/13

80/81

00/01

64/65

68/69

72/73

76/77

84/85

88/89

92/93

96/97

04/05

08/09

12/13

Feed price Feed use (RHS) Change in feed use Change in average price (RHS)

Source: USDA, Bloomberg, Rabobank, 2012 Source: USDA, Bloomberg, Rabobank, 2012

We expect that higher prices for downstream would only be feasible if the RFS mandate

soy products (at the consumer level) are were repealed, something that we are not

inevitable in open markets, with adjustments expecting at this point.

to US production likely to see the US domestic

As corn production losses cannot be

crush fall 175 million bushels YOY to

completely taken out of US ethanol

1,530 million bushels in 2012/13. China’s

demand, we expect US livestock corn feed

soybean imports continue to grow, reaching

to be reduced by 400 million bushels YOY

5.87 million tonnes in July 2012, up

to 4,150 million bushels in 2012/13. The US

10 percent from July 2011 before declining

government introduced a USD 383 million

2 percent YOY in August to 4.42 million tonnes.

drought relief package, mainly for the

We expect that near record-high prices need

livestock industry, which amounts to less than

to be sustained as supplies in Brazil, Argentina

46 million bushels of corn at current prices.

and the US dwindle into early 2013.

While demonstrating the scope of support

We believe that US refinery demand for behind the livestock industry, this is equal to

ethanol, the only feasible oxygenate only 1 percent of the industry’s corn use in

for gasoline in the short term, could push the 2011/12 marketing year. This will have

ethanol prices above current gasoline little-to-no effect on the scale of demand

prices. Ethanol margins averaged negative rationing undertaken in 2012/13. Although,

USD 0.06 per gallon over the month as will be discussed on page 19, many

during August, with production falling livestock producers have hedges currently

to 820,000 bushels per day, which, if held in place, the strength of market pressures is

constant during the 2012/13 marketing year, extraordinary, with US livestock herds likely

would imply corn ethanol use of 4,500 million to be liquidated at an accelerating pace in

bushels—in line with Rabobank forecasts. 1H 2013. Near record-low hog margins of

The potential reductions in corn demand negative USD 60 per head should begin to

for ethanol, initially the most elastic form reduce production in the US pork industry,

of demand due to excess oxygenation with other countries following in lock-step

of gasoline in the last two years, will see as lower margins shift the supply of animal

production fall 500 million bushels short protein to a lower base (see Figure 2.10).

of the 5 billion bushels implied by the RFS

mandate. In the short term, a 20 percent Second or der impac ts—the k nock-on

fall in ethanol production would require an eff ects

extra 200,000 barrels per day of oil imports, Rabobank believes that the new records

increasing pressure on retail gasoline prices. being set in grain and oilseed prices will have

Longer term, should negative blending long-tailed effects on a number of F&A supply

economics at the refinery level be sustained, chains. Short term, we will see significant

the relatively abundant supply of natural pressure on quickly processed parts of the

gas-derived oxygenate substitutes could global grains and oilseeds complex, such as

be supported and would pose a threat milling, brewing and ethanol. Longer term,

to the sustainability of the conventional and most importantly, sustained higher prices

biofuels industry in the US. However, this and lags in animal protein herd adjustmentsYou can also read