Hibernia REIT plc Company update July / August 2014

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Hibernia REIT plc Company update July / August 2014

DISCLAIMER

This presentation (hereinafter "this document") has been prepared by Hibernia REIT plc (the "Company") and WK Nowlan REIT

Management Limited ("WNRML"), the Company’s investment manager, for information purposes only.

This document has been prepared in good faith but the information contained in it has not been independently verified and

does not purport to be comprehensive. The Company is not undertaking any obligation to provide any additional information or

to update this document or to correct any inaccuracies that become apparent. This document is neither a prospectus nor an

offer nor an invitation to apply for securities. The information contained in this document is subject to material updating,

completion, revision, amendment and verification. This document does not constitute or form a part of any offer for sale or

solicitation of any offer to buy or subscribe for any securities. Any prospective investor must make its own investigation and

assessments and consult with its own adviser concerning any evaluation of the Company and its prospects.

No representation or warranty, express or implied, is given by or on behalf of the Company, its group companies, WNRML or

any of their respective shareholders, directors, officers, employees, advisers, agents or any other persons as to the accuracy,

completeness, fairness or sufficiency of the information, projections, forecasts or opinions contained in this presentation. In

particular, the market data in this document has been sourced from third parties. Save in the case of fraud, no liability is

accepted for any errors, omissions or inaccuracies in any of the information or opinions in this document.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of terms

such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue", "target" or "believe" (or the

negatives thereof) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events

or results or actual performance of the Company may differ materially from those reflected or contemplated in such forward-

looking statements. No representation or warranty is made as to the achievement or reasonableness of, and no reliance should

be placed on, such forward-looking statements. There is no guarantee that the Company will generate a particular rate of

return.

The Company has not been, and will not be, registered under the US Investment Company Act of 1940, as amended, and

investors are not entitled to the benefit of that Act. This Presentation is available only to persons who are (1) both Qualified

Institutional Buyers as defined in Rule 144A under the US Securities Act of 1933, as amended, as well as Qualified Purchasers

within the meaning of section 2(a)(51) of the US Investment Company Act of 1940, as amended, or (2) outside the United

States and not US persons as defined in Regulation S under the US Securities Act of 1933, as amended.

2

Agenda

Operating and financial highlights

Market update

Acquisitions

Conclusion and outlook

3

OPERATING AND FINANCIAL HIGHLIGHTS

Overview

Highly active period since full year results to 31 March 2014

– Completed eight acquisitions, totalling €267m, primarily of Dublin CBD offices

– Three new hires including CFO, bringing management team to 12

– Support from the wider WKN team of 33 people

Portfolio taking shape

– Have invested €336m, over 90% of net proceeds raised in December 2013, with a further €63m

committed

– Summary of portfolio statistics

– 76% (by cost) in Dublin CBD offices, remainder between residential and logistics, all within

Dublin

– Portfolio NIY 4.1% (4.7% post rent free periods / abatements)

– Strong reversionary potential: weighted average contracted rents for offices of €33 per sq. ft.

– Development project at Wyckham Point and development opportunities at Windmill Lane and

Gateway sites

Outlook

– Very high level of transaction volumes in Dublin office market currently and NAMA to accelerate

portfolio sell-down

– Management are finding attractive acquisition opportunities within the Dublin office market,

particularly in off-market and loan spaces

– Hibernia is considering various funding options: in first instance seeking to put in place debt

4

OPERATING AND FINANCIAL HIGHLIGHTS

Our strategy has not changed since our IPO

Investment criteria Target property types and locations

Balanced portfolio of property types Majority in Grade A or Grade B office buildings that can

be acquired close to or below replacement cost

− Principally institutional quality, well located, income Appropriate allocation to

producing commercial property − Retail assets with low tenant risk e.g. in Dublin’s prime

shopping districts that have historically performed well

− Up to 30% of portfolio allocated to “value-added” − Industrial assets in prime locations close to good

properties e.g. requiring refurbishment or tenanting transport links and leased to strong tenant covenants

− Prime Dublin residential, infill residential schemes in

− Full scale development not envisaged other than in close proximity to public transportation and within 6 miles

special circumstances of limited risk and not above 15% of CBD

of portfolio

Primarily Dublin CBD and Greater Dublin area Illustrative targeted portfolio breakdown

Lot sizes – typically €10m–€50m

Targeting Total Shareholder Return of 10-15% p.a.

(pre-taxation) with a substantial income element when fully

invested

Ability to enter joint ventures

Gearing not to exceed 50% of portfolio (Irish REIT Office Retail Industrial Residential

limit) and not expected to exceed 40% of portfolio at

time of borrowing

5

OPERATING AND FINANCIAL HIGHLIGHTS

Summary of acquisitions to date

Since commencing operations in January 2014, have deployed €336m (over 90% of net IPO proceeds) and have a further

€63m committed

Acquisitions to date

Acquisition Initial Acquisition Acquisition

Name Location completion date investment Type Net initial yield type structure

Dorville Portfolio (key Dundrum, 28‐Feb‐14 €67m Primarily n/a Off‐market Loan

asset: Wyckham Point) Dublin 16 Residential

New Century House Mayor Street, 01‐May‐14 €47m Office c.6%(1) Off‐market Property

Dublin 1

Gateway Site Newlands Cross, 07‐May‐14 €10.1m Industrial c.5%(2) On‐market Property

Dublin 22

Montague House and Hatch Street Upper 16‐May‐14 €18.3m(3) Office c.8% Off‐market Loan

Hardwicke House and Adelaide Road,

Dublin 2

Chancery Building and Chancery Lane, 30‐Jun‐14 €16m Office c.7% Off‐market Loan

Chancery Apartments Dublin 8

Notes

(1) Once rent abatement period ends in September 2015

(2) Gross initial yield

(3) Hibernia REIT has the right to take full ownership for an incremental €41.75m

6

OPERATING AND FINANCIAL HIGHLIGHTS

Summary of acquisitions to date (cont’d)

Acquisitions to date

Acquisition Initial Acquisition Acquisition

Name Location completion date investment Type Net initial yield type structure

Hanover Building Hanover Quay, 16‐Jun‐14 €20.2m Office c.7% Off‐market Loan

Dublin 2

Windmill Lane Windmill Lane, 13‐Jun‐14 €7.5m Development site n/a Off‐market Property

Dublin 2

Observatory Sir John Rogerson’s 16‐Jul‐14 €51.5m Office c.4%(1) On‐market Property

Quay,

Dublin 2

Guild House and Guild Street, 18‐Jul‐14 €90.8m Office c.7% Off‐market Property

Commerzbank House Dublin 1

Total €328m

Total including acquisition costs €336m

Since commencing operations in January 2014, have deployed €336m (over 90% of net IPO proceeds) and have a

further €63m committed

Notes

(1) Once rent free periods end in 2015 and 2016

7

Agenda

Operating and financial highlights

Market update

Acquisitions

Conclusion and outlook

8

MARKET UPDATE

Irish economic backdrop supportive of

continued recovery in property market

Domestic demand to contribute to growth in 2014 Employment growth has picked up

10%

2% 6%

8%

4%

6% 1%

4% 2%

2% 0%

0%

0%

% YoY

-1% -2%

-2%

-4%

-4% -2%

Data

-6% released -6%

-8% -3% since IPO

-8%

-10%

-4% -10%

-12%

Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1 2014

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014f 2015f

Domestic demand GDP Quarterly (LHS) Annual (RHS)

Source: CSO, Goodbody Source: CSO

PMIs are well into positive territory Consumer confidence has risen since the end of the bailout

65 100

90

60

80

55

70

Index

50 60

Data 50 Data

released released

45

since IPO 40 since IPO

40 30

May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May Jan May Sep Jan May Sep Jan May Sep Jan May Sep Jan May Sep Jan May Sep Jan May

11 11 11 11 12 12 12 12 12 12 13 13 13 13 13 13 14 14 14 08 08 08 09 09 09 10 10 10 11 11 11 12 12 12 13 13 13 14 14

Services Manufacturing Composite

Source: Bloomberg, Markit Source: Factset

9

MARKET UPDATE

Commercial property market recovering

strongly, particularly office sector

Commercial property is continuing its recovery Capital values are currently at c.1999 levels

1,600 600

1,400 580

1,200 560

Capital value index

Capital value index

1,000 540

520

800

500

600

480 Data

400

released

460

200 since IPO

440

0

420

1977

1981

1984

1986

1988

1990

1992

1994

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

Source: Jones Lang LaSalle Source: Jones Lang LaSalle

Quarterly change in capital values by sector Quarterly change in rents by sector

7% 8%

Data Data

6%

released 6% released

5% since IPO since IPO

4% 4%

3%

2%

2%

Quarterly change

Quarterly change

0%

1%

0% -2%

-1%

-4%

-2%

-3% -6%

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014

Retail Office Industrial Retail Office Industrial

Source: IPD Source: IPD

10MARKET UPDATE

Dublin residential market also showing

strong growth from depressed levels

Residential prices now growing across the country Average residential property prices

30% 500,000

450,000

20%

400,000

350,000

10%

300,000

% YoY

250,000

0%

200,000

-10% 150,000

100,000

Data Data

-20% released released

since IPO 50,000 since IPO

0

-30%

Jan 07 Jan 08 Jan 09 Jan 10 Jan 11 Jan 12 Jan 13 Jan 14

Dublin ex Dublin Dublin ex Dublin

Source: CSO Source: ptsb/ESRI, CSO, Goodbody

11MARKET UPDATE

Rental market: Dublin office dynamics

Number of Grade A vacant buildings in Dublin IFSC, 2 and 4 Vacant space by geography and quality

10 IFSC 5,000 Grade A

Dublin 2 Grade B

9

Dublin 4 Grade C

8 2 4,000

7

Thousands (sq.ft.)

6 3,000

3

5

4

2,000

7

3 Only 1 building of >50,000 sq. ft.

2

currently vacant, down from 5 at end of

1 Q2 2013

2 4

1 1,000

1 2 2

1 1

0

0 - 9,999 10,000 - 20,000 - 30,000 - 40,000 - 50,000 - 60,000 - 70,000 - 80,000 - 90,000 - 100,000 - 150,000 0

sq.ft. 19,999 29,999 39,999 49,999 59,999 69,999 79,999 89,999 99,999 149,999 sq.ft.+

sq.ft. sq.ft. sq.ft. sq.ft. sq.ft. sq.ft. sq.ft. sq.ft. sq.ft. sq.ft IFSC Dublin 2 Dublin 4 Rest of Dublin

Dublin City

Source: Jones Lang LaSalle Source: Jones Lang LaSalle

Q2 take-up of 0.42m sq. ft. brings the year to date take up to 1.02m sq. ft.

Total take up for 2014 expected to be in line with 2013’s total of 1.92 million sq. ft.

Currently 1.3 million sq. ft. of active requirements in the market

Prime quoted rents in the city centre have increased to €45 per sq. ft. with rents in excess of €40 per sq. ft. being achieved

Evidence of longer leases of 20 – 25 years is more common in the market with first break options at year 10 in the city centre

CBRE forecasting prime rents at c.€60psf by 2020(1)

Source: Jones Lang LaSalle Dublin Office Market Report Q2 2014, (1) CBRE Outlook 2014

12MARKET UPDATE

Rental market: Dublin office dynamics (cont’d)

Dublin office take-up expected to be c.2m sq.ft. in 2014 Dublin geographic take-up

3.0 100%

90%

2.5 36%

80% 44% 41%

48%

2.0 70%

60%

Million sq.ft.

1.5

50%

1.0 40%

30% 59% 64%

0.5 52% 56%

20%

0.0 10%

0%

H1 2014

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2011 2012 2013 H1 2014

Forecast Take Up 20 Year Average City Centre Suburbs

Source: Jones Lang LaSalle Source: Jones Lang LaSalle

Vacancy reducing and very limited new supply Q2 2014 Dublin take-up by sector

40 5.0

30 4.0

Suburbs 373,697 sq.ft.

3.0

20

Million sq.ft.

2.0

10 1.0

0 0.0 CBD 650,649 sq.ft.

Q4 2001

Q4 2002

Q4 2003

Q4 2004

Q4 2005

Q4 2006

Q4 2007

Q4 2008

Q4 2009

Q4 2010

Q4 2011

Q4 2012

Q4 2013

Q2 2014

TMT Transport and Storage

Insurance and Pension Funds Banking and Fin.

Occupied Stock Vacant Stock Under Construction Other

Source: Jones Lang LaSalle Source: Jones Lang LaSalle

13MARKET UPDATE

Investment market: volumes of transactions

picking up sharply

5,000

4,500

4,000

3,500

3,000

€ millions

2,500

2,000

1,500 Ø €1,152m

1,000

500

0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total Investment Volumes Loan Sales Forecast Direct & Loan 12 year average

Note: Excludes IBRC loan sales of €9.3bn nominal value

H1 direct property sales of €1.7bn have already achieved 90% of total volume for 2013, when €1.9bn was transacted

Large supply pipeline in H2 2014, with NAMA, Bank of Ireland and Ulster Bank expected to be the most significant sellers

Source: Jones Lang LaSalle

14MARKET UPDATE

Irish property market recovery leading to

increased disposals by NAMA in Ireland

NAMA’s Irish disposals continue to increase… …as focus shifts away from London back towards Ireland

Cumulative Irish Disposals by NAMA (€m) Irish Disposals as a % of NAMA total

3,000

2,500

2,000

50%

1,500

1,000

22%

500 13%

0

Q1'10 Q3'10 Q1'11 Q3'11 Q1'12 Q3'12 Q1'13 Q3'13 Q1'14 2012 2013 2014 YTD July

“ To date in 2014, our (total) sales are over €5bn. 50% of that has come from Irish sales

”

Frank Daly, NAMA Chairman, 4 July 2014

Senior figures within NAMA and the Irish government are suggesting that the rate of Irish disposals is likely to increase

“ New redemption target of 80% (of NAMA senior debt) by 2016

Michael Noonan, Minister of Finance, 16 July 2014

” “ We currently estimate that we will need to sell about €6bn in Irish

assets over the period from 2014 to 2016

”

Brendan McDonagh, NAMA CEO, 29 May 2014

Sales of NAMA-owned assets in Ireland have accelerated in recent months and this trend looks set to continue

Source: NAMA, Investec, press reports

15MARKET UPDATE

NAMA’s portfolio well suited to Hibernia’s

investment proposition

NAMA loans: split by geography (Dec-13) NAMA loans in Dublin: split by type (Dec-13)

Hotel & Other

Leisure 3%

5%

Rest of World

10%

Office

Land

Rest of 24%

13%

Britain

12%

Dublin 43% of

€19.6bn(1) 38% NAMA’s total €7.5bn(2)

portfolio is

London Dublin based

18% Development

15% Retail

18%

64% of

DCB Industrial NAMA’s

Cork 5% Residential

20% 2% Dublin assets

Rest of 6%

in Hibernia

Ireland

target sectors

4%

Limerick

Northern

1% Galway Ireland

2% 4%

Within the Dublin area, commercial office space and

A significant portion of NAMA’s portfolio is in central

other Hibernia investment priorities make up the

Dublin and the adjacent commuter belt

majority of assets

DCB = Dublin Commuter Belt

Source: NAMA, Investec

Note: Split of AuM in NAMA portfolio as of 31-Dec-2013

(1) NAMA carrying value of loans (total portfolio) as at 31-Dec-13

(2) NAMA carrying value of loans in Dublin as at 31-Dec-13

16MARKET UPDATE

Investment market: availability of assets

Total value of commercial property transactions has increased significantly since IPO

NAMA See prior slides

Acceleration of sales expected to hit new target of redeeming 80% of senior debt (a cumulative €24 billion) by 2016

Banks IBRC: The Residential Mortgage loan sale, completed on 6 June 2014, resulted in the disposal of 64% of IBRC’s

Residential Mortgage book

Ulster Bank: Disposal of £9bn in Irish investment and development loans kicked off in February 2014 with €850m sale

process for portfolio of commercial loans

Permanent TSB: To sell commercial loan book of €2.6bn

Domestic banks: continue to make selective loan sales

Other Private equity funds, active over last 18 months in Ireland, have become increasingly active in other EU markets and

some are exploring opportunities to exit Irish assets particularly where project management expertise is required

JV opportunities – NAMA has confirmed it will engage in JV opportunities with suitable partners, as have some PE

funds, and these opportunities will most likely emerge where project management expertise is required

JLL forecasting direct property and commercial loan transactions totalling €4bn in 2014(1)

(1) Source: Jones Lang LaSalle

17Agenda

Operating and financial highlights

Market update

Acquisitions

Conclusion and outlook

18ACQUISITIONS

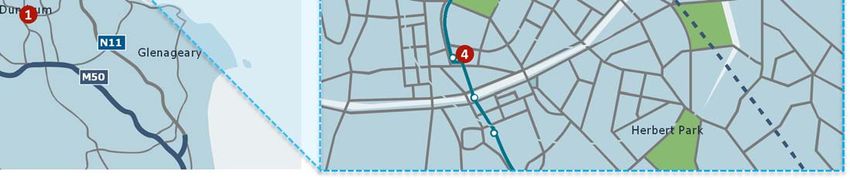

Location of Hibernia acquisitions

Office acquisitions all within CBD; ex-CBD acquisitions both

with good transport links Central Dublin acquisitions

Dublin

The Ward Airport Fairview Park

Croke Park

M1

Portmarnock

N2/M2

Northwest

Business Park M50

Northern

Cross

N3/M3 Ballymun

Sutton

Blanchardstown Beaumont

Kings Inns

Howth

Castleknock Drumcondra Clontarf

North Bull

N4/M4 Phibsborough Island 2 9

Palmerstown Alexandra Basin

Dublin River Liffey

92

8

6

8

54

7 7 6

N81

Ballsbridge

Clondalkin Kimmage 5

3 Ballymount

N7/M7 Blackrock

St. Stephens

Rathfarnham 1 Wyckham Point

Green

M50

Dundrum 2 New Century House

1

Tallaght 3 Gateway Site

N11

4 Glenageary

Montague House and Hardwicke House

4

5 Chancery Building and Chancery Apartments

M50

6 Hanover Building

7 Windmill Lane

8 Observatory

Herbert Park

9 Guild House and Commerzbank House

Source: Google Maps, Visit Dublin, Jones Lang LaSalle

Note: Hibernia acquisitions shown in red.

19ACQUISITIONS

Summary of Dorville portfolio loan acquisition

Off–market acquisition of €67m Dorville loan portfolio from Ulster Bank

Gaining access to a portfolio of 16 assets, principally residential

Hibernia to retain three “core” assets and undertake phased disposal of the other assets

Summary

Core assets Ascribed value

Wyckham Point Residential €30m

Cannon Place Residential €6m

South Dock House Office €5m

€41m

Non core assets Ascribed value

8 residential assets €19m

2 office assets €2m

3 development assets €5m

€26m

20ACQUISITIONS

Wyckham Point

Acquisition type Dundrum, Dublin 16

Acquired as part of €67m Ulster Bank loan portfolio

Off-mkt On-mkt

Apportioned value of c. €30m

Property Loan

Comprises:

Dev. opportunity

– Wyckham Point – 213 partially completed apartments

– Mix of one, two and three bed apartments

Property type

– Excellent amenities incl. 3 acre park with lake, gym, creche

Office

Prime south Dublin residential location

Grade A

– Good transport links

CBD

– close to Dundrum Shopping Centre

Income producing

Value-add space

Retail

Low tenant risk

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Wyckham Point planned timeline to complete

Infill Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016

Good transport

links Stage 1 - Pre Construction

Stage 2 - Construction

Stage 3 - Turn-key fit-out

21ACQUISITIONS

Cannon Place

Acquisition type Herbert Road, Dublin 4

Acquired as part of €67m Ulster Bank loan portfolio

Off-mkt On-mkt

Apportioned value of €6m

Property Loan

Comprises 12 two and three-bed apartments in a 22 unit apartment block

Dev. opportunity

Well-located modern estate

– Walking distance from Sandymount and Ballsbridge villages

Property type

– Close to Lansdowne DART station and the Aviva Stadium

Office

Grade A

CBD

Income producing

Value-add space

Retail

Low tenant risk

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

22ACQUISITIONS

South Dock House

Acquisition type 1st Floor Offices, Hanover Quay, Dublin 2

Acquired as part of €67m Ulster Bank loan portfolio

Off-mkt On-mkt

Apportioned value of c.€5m, equating to €530psf capital value

Property Loan

Asset comprises

Dev. opportunity

– One floor of 8,942 sq ft in three office suites with parking for 9 cars

– Let to 3 tenants (Open Hydro Ireland, Collins Stewart, Guggenheim Partners)

Property type

– Annual rent of €312k, average of €35psf

Office

– WAULT of three years

Grade A

CBD

Income producing

Value-add space

Retail

Low tenant risk

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

23ACQUISITIONS

New Century House

Acquisition type Mayor Street, IFSC Dublin 1

Acquisition price €47m: equating to €587psf capital value

Off-mkt On-mkt

Asset comprises

Property Loan

– 80,000 sq ft offices over six storeys with parking for 87 cars

Dev. opportunity

– Let to Bank of Ireland on FRI lease until 2024, with upward-only rent review

in 2019

Property type

– Annual headline rent €2.85m, or €32psf, with rental abatement until

Office October 2015

Grade A – Initial yield (post-abatement period): c.6%

CBD Significant refurbishment work is about to be implemented by the tenant

Income producing

Value-add space

Retail

Low tenant risk

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

24ACQUISITIONS

Gateway Site

Acquisition type Newlands Cross, Naas Road, Dublin 22

Acquisition price: €10.1m

Off-mkt On-mkt

Comprises

Property Loan

– 14.1 acres (5.71 ha) with three large industrial/logistics facilities of 177,960 sq. ft.

Dev. opportunity

– Buildings currently 46% occupied and producing an annual rental income of €517k

or c.€5.5psf

Property type

– Initial yield c.5%

Office

Strategic location adjacent to intersection of Ireland’s two busiest roads and Dublin’s

Grade A light rail system

CBD Significant redevelopment potential

Income producing

Value-add space

Retail

Low tenant risk

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

25ACQUISITIONS

Montague House & Hardwicke House

Acquisition type Hatch Street Upper & Adelaide Road, Dublin 2

Acquisition price: €60m, equating to €692psf capital value

Off-mkt On-mkt

Acquisition from Hardwicke Group in partially deferred transaction structure

Property Loan

– Initial acquisition of €18.25m of loans (giving operational control) with NIY of

Dev. opportunity

7.7%

– Right to take full ownership of the buildings any time up to mid-2016 for

Property type incremental €41.75m

Office Assets comprise

Grade A – 88,483 sq ft of prime Grade A office space in two 5 storey buildings on contiguous

CBD back-to-back sites with 56 basement car parking spaces

Income producing – Both multi-let at avg rent of €30psf (Hardwicke €34psf, Montague €27psf)

Value-add space – WAULT of 7 years

Retail – 100% of rent to be reviewed during or prior to 2018

Low tenant risk

– 28% with break clauses in 2016

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

26ACQUISITIONS

Chancery Building & Chancery Apartments

Acquisition type Chancery Lane, Dublin 8

Acquisition price: €16m

Off-mkt On-mkt

Acquiring loans from Bank of Ireland, giving full ownership of assets

Property Loan

Assets comprise

Dev. opportunity

– a) office building with 33,799 sq. ft. space over 6 stories with 19 parking spaces

– Allocated price of €15m for the offices equates to cap. val. of €445psf

Property type

– Fully let with WAULT of 9 years and 2 years to break

Office

– Average passing rent of €30psf

Grade A – Net initial yield 6.8%

CBD – b) four 2 bed apartments in same building with separate entrance

Income producing – Fully let on 1 year contracts

Value-add space

Retail – Allocated price of €1m for the apartments equates to a net initial yield

Low tenant risk 6.1%

Prime Dublin – c) a small 0.05 acre site with planning consent for a c. 13,900 sq. ft. NIA office

building or a 45 ‘suite’ student accommodation building

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

27ACQUISITIONS

The Hanover Building

Acquisition type Windmill Lane, Dublin 2

Acquisition price: €20.2m, equating to €360psf cap. val. and 7.3% NIY

Off-mkt On-mkt

Asset comprises 5 storey building and 13 underground parking spaces with:

Property Loan

– a) 44,317 sq. ft. of office space on upper floors

Dev. opportunity – Fully let to BNY under leases running to 2026/7 with break clause in 2016

– Average passing rent on office space of €30psf

Property type

– b) 11,614 sq. ft. of retail space on ground floor

Office

– Fully let to Eurospar to 2032 with break clause in 2019

Grade A

– Office and retail income all subject to rent reviews in 2017 and 2018

CBD South Docks area one of most popular office locations in recent years

Income producing

Adjoins the 1 acre Windmill Lane Site acquired in simultaneous transaction from a

Value-add space

separate seller

Retail

Low tenant risk

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

28ACQUISITIONS

Windmill Lane Site

Acquisition type Windmill Lane, Dublin 2

Acquisition price: €7.5m

Off-mkt On-mkt

1 acre development site adjoining Hanover Building in South Docks area

Property Loan

Existing planning consent for:

Dev. opportunity – 125,000 sq. ft. (net) office space

– 9,000 sq. ft. retail

Property type

– 15 residential units

Office

Price paid for land equates to €50psf on the net developable space

Grade A

12 month option to a party to invest on a side by side, equal cost basis on the

CBD

redevelopment of the Hanover Building and the Windmill Lane Site

Income producing

Value-add space

Retail

Low tenant risk

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

29ACQUISITIONS

The Observatory Building

Acquisition type Sir John Rogerson’s Quay, Dublin 2

Off-mkt On-mkt

Acquisition price €51.5m

Property Loan Asset comprises

Dev. opportunity – a) 84,000 sq ft office over six storeys with parking for 47 cars

– Allocated price of €49.8m for the offices equates to cap. val. of €590 psf

Property type – 95% let with WAULT of 11 years and 4 years to break

Office – Tenants include Riot Games, Publicis, Morgan Stanley & Realex Payments

Grade A – Low average rent of €26psf

CBD – Annual headline rent of €2.2m, with rent frees on €1.2m ending in 2015 and

Income producing early 2016

Value-add space – Initial yield (post-rent free periods): c.4.1%

Retail – b) Eight partially completed 2 bed “live / work” units and two retail units

Low tenant risk – Allocated price of €1.7m

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

30ACQUISITIONS

Guild & Commerzbank House

Acquisition type Guild Street, IFSC, Dublin 1

Off-mkt On-mkt Acquisition price €90.75m

Property Loan Purchase of two adjoining buildings in the IFSC. The buildings comprise:

Dev. opportunity – 144,250 sq. ft. of office accommodation over five storeys with parking for 148

cars

– Cap. val. of €629 psf

Property type

– 100% let with WAULT of 3 years to break and 11 years to expiry

Office

– Tenants include FBD Holding Ltd, BNY Mellon and Commerz Management

Grade A Services

CBD – Average rent of €39psf

Income producing – Annual headline rent of €6.1m

Value-add space

Retail – Initial yield: 6.6%

Low tenant risk

Prime Dublin

Industrial

Prime location

Good transport

links

Strong covenant

Residential

Infill

Good transport

links

31Agenda

Operating and financial highlights

Market update

Acquisitions

Conclusion and outlook

32CONCLUSION AND OUTLOOK

Conclusion

Highly active period since full year results to 31 March 2014

– Completed eight acquisitions, totaling €267m, primarily of Dublin CBD offices

– Three new hires including CFO, bringing management team to 12

– Support from the wider WKN team of 33 people

Portfolio taking shape

– Have invested €336m, over 90% of net proceeds raised in December 2013, with a further €63m

committed

– Summary of portfolio statistics

– 76% (by cost) in Dublin CBD offices, remainder between residential and logistics, all within

Dublin

– Portfolio NIY 4.1% (4.7% post rent free periods / abatements)

– Strong reversionary potential: weighted average contracted rents for offices of €33 per sq. ft.

– Development project at Wyckham Point and development opportunities at Windmill Lane and

Gateway sites

Outlook

– Very high level of transaction volumes in Dublin office market currently and NAMA to accelerate

portfolio sell-down

– Management are finding attractive acquisition opportunities within the Dublin office market,

particularly in off-market and loan spaces

– Hibernia is considering various funding options: in first instance seeking to put in place debt

33Agenda

Appendix

34APPENDIX

Strong board with mix of property and plc

experience

Hibernia REIT plc Danny Kitchen Stewart Terence Colm Bill Nowlan

Independent Harrington O’Rourke Barrington Non-Executive

Non-Executive Independent Non-Executive Independent Director

Chairman Non-Executive Director Non-Executive

Director Director

Non-Executive Chairman of Non-Executive Director of BWG Non-Executive Director of The Irish Non-Executive Chairman of Aer Previously Head of Property

Workspace Group plc and Group and Stafford Holdings Times and Chairman of Enterprise Lingus plc and CEO and Director of Investment of Irish Life from 1985

Governance Non-Executive Director of LXB Previously a Partner Jones Lang Ireland Fly Leasing Ltd to 1995, the largest property fund

Retail Properties plc Wootton (now Jones Lang LaSalle) Previously Managing Partner KPMG manager in Ireland. Established

Previously Finance Director of Founding Partner of Harrington Ireland WK Nowlan in 1995, one of the

Green Property plc Bannon Chartered Surveyors largest property asset managers in

Ireland

Breadth of skill set and experience encompassing institutional property management and development in prime

WK Nowlan REIT and value add space, with strong relationships with key decision makers in banking and property

Management

Kevin Nowlan Bill Nowlan Frank Kenny Frank O’Neill Tom Edwards-

Chief Executive Investment Portfolio Chief Operations Moss

Officer Director Management Officer Chief Financial

Director Officer

>20 years of experience in the >40 years of experience advising >35 years of experience in the >20 years of experience in the Previously worked for 9 years at

Irish property market on investment in Irish commercial Irish and US property markets Irish property market Credit Suisse in Investment

Management Previous positions include Senior property Founder and CEO of Willett Previously, manager of WK Nowlan Banking Division with a particular

Portfolio Manager at NAMA, Previously Head of Property Companies LLC, boutique Property Management Division, focus on corporate finance in the

Portfolio Manager at Treasury Investment of Irish Life from 1985 investment company which covering Irish and UK properties real estate sector. He qualified as

Holdings and Assistant Manager at to 1995, the largest property fund managed, developed and/or owned a Chartered Accountant at

Anglo-Irish Bank plc manager in Ireland. Established 2 million sq ft of real estate PricewaterhouseCoopers in 2005

WK Nowlan in 1995, one of the

largest property asset managers in

Ireland

WK Nowlan

Property

WK Nowlan is a property asset management company staffed by 33 professional staff with capacity to execute multiple

transactions simultaneously

The team has a broad mix of skills covering all the key professional aspects of property management and development:

surveyors and valuers, architects, engineers, portfolio managers and financial analysts

Support Capacity to execute multiple transactions simultaneously

Ability to manage complex commercial and residential projects

35APPENDIX

Financial highlights as of 31 March 2014

Financial highlights

31 March 2014 Gateway Site acquired [ ]

Balance sheet €’000 Notes

Loans acquired from Ulster Bank (Wyckham assets)

Loans 68,563 Principally cashfrom

Loans acquired + cash equivalents

Ulster of [ ]assets)

Bank (Wyckham

Current assets 303,337 Principally cash + cash equivalents of €291.7m

Current liabilities (934) Principally accrued acquisition costs and other trade payables

Net assets 370,966

EPRA NAV per share 96.4 cents

Income statement 31 March 2014 Notes

Reflects operating expenses of €1.2m and modest interest income on cash

Net loss (846)

deposits

Basic and diluted loss per share (0.22) cents

Financials reflect the fact most of the acquisitions did not close in the first 90 days of operations

36APPENDIX

Overview of the Irish REIT regime

Summary of Irish REIT regime

Summary of Irish REIT regime

Established Introduced by Finance Act 2013

Legal form Irish incorporated PLC company with an allotted share capital of not less than €38,092

Shareholder requirements No closely held company; 10% threshold for corporate shareholders

Listing requirements Listed on the main market of a stock exchange in an EU Member State

Business restrictions >75% of aggregate income derived from property rental business

>75% of portfolio market value must relate to property rental business

Within 3 years of commencement, the REIT must hold at least 3 separate assets, none of which having a market value >40%

of total portfolio

Irish and non-Irish assets

Authorised sectors: commercial properties, industrial properties, residential properties

Leverage restrictions Profit financing ratio of at least 1.25 : 1

Profit financing ratio = property income plus property finance costs divided by property finance costs

Tax Tax exemption for certain income from property rental business, 12.5% for non property rental income

Tax exemption for capital gains, 33.0% for non property rental assets

Dividend withholding tax of 20.0%

Irish stamp duty of 1.0% apply to the purchase of shares in a REIT

Distribution requirements Property income: 85%

Capital gains: no distribution obligation

Source: European Public Real Estate Association

3738

You can also read