IMPACT BONDS: WHERE NEXT? - IRP-HSG

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

IMPACT BONDS: WHERE NEXT?

EVALUATING IMPACT FOR EFFECTIVE PHILANTHROPY –

WORKSHOP SUSTAINABLE FINANCE & IMPACT INVESTING

HSG CENTER FOR EVALUATION AND DEVELOPMENT – 15 JANUARY 2020

Dr Maximilian Martin, Global Head of Philanthropy, Lombard Odier Group

2017: The world’s first “Humanitarian Impact Bond” launched

to transform financing of aid in conflict-hit countries

Please see important information at the end of the document

2 · Philanthropy Services· January 2020

For illustrative purposes only.

Sources: ICRC

Context: Impact bonds – the first decade State of the market: lots of innovation, limited scale Please see important information at the end of the document 3 · Philanthropy Services· January 2020

Addressing key impact bond challenges

Action items to move from pilots to a fully functioning market

Social Impact Bonds vs Green Bonds Key challenges of impact bond market

• Low volume – Small-scale projects face several obstacles when

Impact bonds Green bonds searching for financing. As this market is still in its infancy with a limited

proven track record, many governments are cautious about engaging in

the market. On a broader level, questions have been raised about the

176 launched 4,343 green bonds availability of monetizable and easily measurable socially desirable

since 2010 in 2018 used for outcomes that would be suitable for SIB projects.

buildings, transport

• High transaction costs - Within the SIB market, transaction costs are

& energy alone dominated by the costs incurred for intermediary services and technical

assistance, evaluation, and legal fees. Further, deal development

USD 418 USD 168 ranged from six months to three years. Given the nascent and relatively

ad-hoc nature of the SIB market, these transaction costs are

million raised billion in 2018 considered to be extremely high and prohibitive for further scaling.

only (USD 521

bn since 2007) • Availability of capital - The availability of private entities willing to

invest capital in SIBs remains limited. The reasons include: 1) lack of

investment vehicles and credible financial intermediaries that can be

738’671* na trusted to direct capital flows, 2) minimizing the uncertainty of future

lives touched payments is difficult, 3) pay-outs can occur over extended time periods,

4) few entities are willing to play the role of market maker.

Sources: Climate Bond Initiative, “Green Bonds – the state of the market 2018”, https://www.climatebonds.net/files/reports/cbi_gbm_final_032019_web.pdf; Statista

;*: Estimate from Social Finance 2017

Please see important information at the end of the document

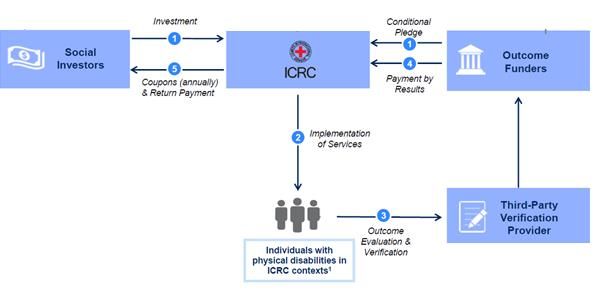

4 · Philanthropy Services· January 2020The Program for Humanitarian Impact Investment

Mechanics & learnings

• PHII Investment Agreement between the ICRC

and the social investors

• Payment by results agreements between

outcome funders and the ICRC

• Verification agreement between Philanthropy

Advisors and the ICRC

• Escrow agreement between UBS, the ICRC, and

the social investors

• ICRC will play the role of the social provider

delivering the social intervention

• Outcome metric: Staff Efficiency Ratios (SER) of

PRP centres versus SER of baseline centres, in

addition to number of beneficiaries reached

1. Conflict-affected countries and other situations of violence.

*Schematic representation based on publicly available information.

Please see important information at the end of the document

5 · Philanthropy Services· January 2020

For illustrative purposes only.Key investment features

Creating a compelling proposition

Programme outline CHF 18.6 million equivalent at the commencement date, supported by outcome funders’ pledges in 5 years,

will be used to finance an increase in the capacity of (by construction) and the efficiency of (by process re-

engineering) the delivery of prostheses, orthoses, and wheelchairs (mobility devices), and related

physiotherapy, to improve the socio-economic circumstances of people with physical disabilities in:

• Mali

• Nigeria, and

• the DRC

Outcome funders Governments of Belgium, Switzerland, Italy, and the UK, as well as the “La Caixa” Banking Foundation

Cornerstone investor An institutional investor from the insurance industry, New Reinsurance Company

Operation duration The full 5 years from the commencement date

Investor total return • 2% coupon for the first 4 years, in addition to

• A return payment based on the success of the programme operations at the end of year 5, net of coupon

already paid

Return payment The return payment is based on the impact the programme has had on the efficiency of delivery of mobility

devices to beneficiaries. It is calculated and verified by a verification provider, and compared to an average

historical SER of comparable ICRC centres. If the ICRC is more efficient, a return of up to 7% IRR is due on

completion of programme operations at the end of 5 years. If the ICRC is less efficient, then investors could

lose up to 40% of principal.

Escrow bank UBS AG Zurich

Verification provider Philanthropy Advisors

Please see important information at the end of the document

6 · Philanthropy Services· January 2020

For illustrative purposes only.Value proposition

A strategic approach to solving important bottlenecks

• It is the first time an established aid organisation in the humanitarian space

with a large budget (>CHF 1.5 billion) has looked to impact investors to

help fund its work on such a scale;

• Government funding often has a time horizon of 1-2 years. It rarely reaches • Channel additional resources – EUR 22m of five-

beyond the electoral cycle. Providing financing certainty for a longer year funding to provide much needed humanitarian

period of time, in this case five years, not only allows the construction of services to people in conflict affected countries

new centres, but also permits actors to take a strategic perspective, aiming construction and operation of three centres in Africa;

for much higher expectations of efficiency;

• Test and implement new efficiency initiatives –

• The project funds three new centres. However, the ICRC has been social impact expected to reach far beyond the three

operating 139 rehabilitation projects in 34 countries since 1979, helping centres;

almost 330,000 people. The ultimate impact therefore reaches much further.

• Successful co-operation of different European

The three centres will be piloting the next generation of physical

parties (governments, humanitarian actors and

rehabilitation service delivery. Next to the immediate impact on the

private investors) to bring about potentially game-

thousands of beneficiaries served, the PHII is financing the innovation of a

changing improvement of services and a new

core programme, to take it to the next level;

financing model in the humanitarian space, inspired

by social impact bonds.

• While this private loan belongs to the family of social impact bonds because

it links a social outcome (physical rehabilitation) to a financial return, it is the

scale, effectiveness and potential impact of this project that makes it

stand out, in addition to the different financial structure.

Please see important information at the end of the document

7 · Philanthropy Services· January 2020

For illustrative purposes only.The Staff Efficiency Ratio (SER)

Measuring impact

Number of mobility devices delivered (adjusted)

SER =

Number of staff involved in mobility device delivery (adjusted)

SER calculation methodology

(# of Prostheses x 1 ) + (# of Orthoses x 0.74 ) + (# of Wheelchairs x 0.90 )

((# of trained P&Os x 1 ) + (# of P&Os without training x 0.75 ) + (# of bench workers x 0.50 )) x working hours ratio

The formula is designed to make physical rehabilitation centres comparable to each other and to prevent

perverse incentives.

Each type of mobility device is given a different weight to account for the different labour time requirements to

manufacture them. As a result, there is no incentive to produce the least time-intensive device to improve the SER in a way

detrimental to the beneficiaries’ best interest.

Different categories of rehabilitation professionals are given different weights according to their level of education

(assuming that better trained professionals work more efficiently). This avoids penalising centres that are staffed with less

qualified supporting staff (i.e., bench workers), because of an exogenous lack of trained prosthetists and orthotists in the region

where a centre operates.

The working hours ratio adjusts for differences in centres’ working hours (as if they all worked a 40-hour week). This

avoids creating distortions among centres which have quite different modus operandi depending on the country/region.

Please see important information at the end of the document

8 · Philanthropy Services· January 2020

For illustrative purposes only.Feasibility and implementation

Key factors for consideration derived from other impact fund projects

Focus - Identify a programme of strategic importance to your organisation that has the potential

to be taken to the next level.

Participation - Launch an ambitious internal brainstorming and readiness assessment effort to

consider how alternative funding mechanisms could provide the capital needed for a future

iteration of that core programme.

Impact measurement - Develop a set of metrics that can track the programme’s results at a

reasonable cost and establish a base of empirical evidence.

Senior engagement - Make sure senior leaders are willing and able to devote the attention

required for this effort to succeed.

External support - Enlist funders close to the organisation and make them part of a joint

“moonshot” innovation effort.

Timeline - Recognise that innovative financing efforts may take time—and give yourself the time

needed, and the budget.

Source: Martin (2017), “The Next Phase of Innovative Financing,” Stanford Social Innovation Review

Please see important information at the end of the document

9 · Philanthropy Services· January 2020

For illustrative purposes only.Looking back to look ahead: A preliminary evaluation

Praise vs. criticism

Praise Criticism

By making private investment available to social programmes, Х Too early to have definitive evidence SIBs are delivering on

SIBs were expected to bring innovation, more money, and their promise.2

better outcomes for society’s most disadvantaged people. Х Most SIBs are low risk and high return - instead of funding

De-risking programs for governments should allow a bigger innovative programmes, private capital is backing social

variety of social programmes. programmes with a proven track record.2

Provides a way to generate more funding for social policy Х SIBs require direct attribution of outcomes, their focus is

while also proving attractive to investors. 1 narrowed to a single programme when we should be thinking

Relatively new financial solution, yet high level of interest and more holistically about how to address complex social

latent demand. problems. 2

To evolve, improve reporting, outcome measurement and Х The need to return profits in a timely fashion to investors can

structuring in the years to come. deter a comprehensive program evaluation that leads to

At its core, pay for success includes a number of possible program improvement. 2

fundamentally value creating elements, including data- Х Privately negotiated, customised arrangements are not easily

informed decision-making, adaptive governance structures, amenable to standardisation, transparency, or liquidity, which

and active performance management. curbs their potential to scale. 3

Sources: 1: Financial Times, “Table: the top global social impact bonds”, 4 Dec. 2018. https://www.ft.com/content/99b49376-eea6-11e8-89c8-d36339d835c0

2:Stanford Social Innovation Review, “The Downside of Social Impact Bonds”, 31 May 2019. https://ssir.org/articles/entry/the_downside_of_social_impact_bonds

3:Stanford Social Innovation Review, “Social Impact Bonds: What’s in a Name?”, 12 Oct. 2016. https://ssir.org/articles/entry/social_impact_bonds_whats_in_a_name

Please see important information at the end of the document

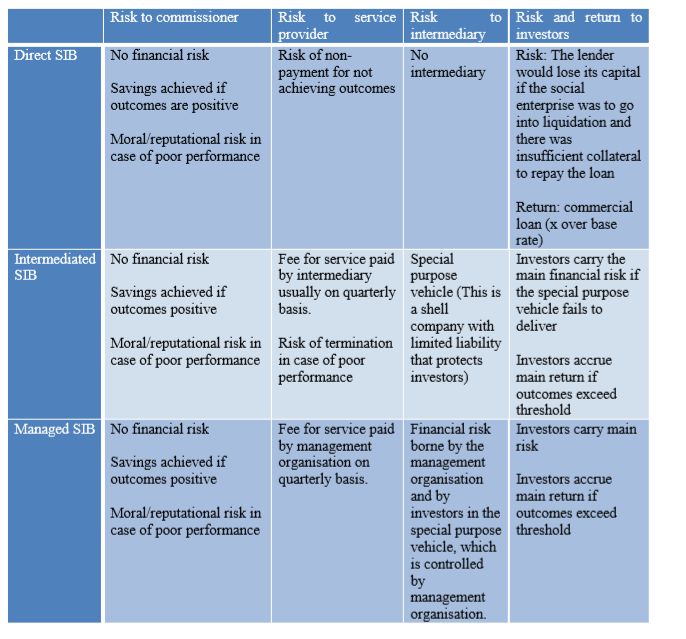

10 · Philanthropy Services· January 2020Backup impact bonds risk distribution Table summarising SIB stakeholder risks Sources: OECD, Social Impact Bonds: State of Play and Lessons Learnt, 2016. https://www.oecd.org/cfe/leed/SIBs-State-Play-Lessons-Final.pdf Please see important information at the end of the document 11 · Philanthropy Services· January 2020

Information importante Le présent document de marketing a été préparé par Lombard Odier (Europe) S.A., un établissement de crédit Odier (Europe) S.A. au Luxembourg et de chacune de ses succursales opérant dans les territoires suivants : agréé et réglementé par la Commission de Surveillance du Secteur Financier (CSSF) au Luxembourg. La Belgique : Lombard Odier (Europe) S.A. Luxembourg · Succursale de Belgique ; France: Lombard Odier (Europe) publication de document de marketing a été approuvée par chacune de ses succursales opérant dans les territoires S.A. · Succursale en France ; Italie : Lombard Odier (Europe) S.A. · Succursale in Italia ; Espagne : Lombard Odier mentionnés au bas de cette page (ci-après « Lombard Odier »). Il n’est pas destiné à être distribué, publié ou utilisé (Europe) S.A. · Sucursal en España ; et Royaume-Uni : Lombard Odier (Europe) S.A. • UK Branch. Avis aux dans une juridiction où une telle distribution, publication ou utilisation serait interdite, et ne s’adresse pas aux investisseurs au Royaume-Uni : Lombard Odier (Europe) S.A. • UK Branch est autorisée au Royaume-Unit par la personnes ou entités auxquelles il serait illégal d’adresser un tel document de marketing. Le présent document de Prudential Regulatrions Authority (PRA) et soumise à une réglementation limitée par la Financial Conduct Authority marketing est fourni à titre d’information uniquement et ne saurait constituer une offre ou une recommandation de (FCA) et la Prudential Regulation Authority (PRA). Vous pouvez obtenir, sur demande, auprès de notre banque souscrire, d’acheter, de vendre ou de conserver un quelconque titre ou instrument financier. Il reflète les opinions plus de détails sur la portée de notre agrément et de notre réglementation par la PRA ainsi que sur la de Lombard Odier à la date de sa publication. Ces opinions et les informations exprimées dans le présent réglementation par la FCA. La réglementation britannique sur la protection des clients privés au Royaume- document ne prennent pas en compte la situation, les objectifs ou les besoins spécifiques de chaque personne. Uni et les indemnisations définies dans le cadre du Financial Services Compensation Scheme ne Aucune garantie n’est donnée qu’un investissement soit approprié ou convienne aux circonstances individuelles, ni s’appliquent pas aux investissements ou aux services fournis par une personne à l’étranger (« overseas qu’un investissement ou une stratégie constituent un conseil en investissement personnalisé pour un investisseur. person »). Par ailleurs, la publication du présent document de marketing a également été approuvé pour utilisation Le traitement fiscal dépend de la situation individuelle de chaque client et est susceptible d’évoluer avec le temps. par les entités suivantes domiciliées au sein de l’Union européenne : Gibraltar : Lombard Odier & Cie (Gibraltar) Lombard Odier ne fournit pas de conseils fiscaux. Il vous incombe par conséquent de vérifier les informations Limited, une société agréée et réglementée par la Commission des services financiers de Gibraltar (FSC) pour susmentionnées et toutes les autres informations fournies dans les documents de marketing ou de consulter vos exercer des activités de services bancaires et de services d’investissement ; Espagne : Lombard Odier Gestión conseillers fiscaux externes à cet égard. Certains produits et services de placement, y compris le dépôt, peuvent (España) SGIIC., S.A., une société de gestion d’investissements agréée et réglementée par la Comisión Nacional être soumis à des restrictions juridiques ou peuvent ne pas être disponibles dans le monde entier sans restrictions. del Mercado de Valores (CNMV), Espagne. Les informations et les analyses contenues dans le présent document sont basées sur des sources considérées Etats-Unis : Ni ce document ni aucune copie de ce dernier ne peuvent être envoyés, emmenés ou distribués aux comme fiables. Lombard Odier fait tout son possible pour garantir l’actualité, l’exactitude, l’exhaustivité desdites Etats-Unis ou remis à une US-Person. informations. Néanmoins, toutes les informations, opinions et indications de prix peuvent être modifiées sans Le présent document de marketing ne peut être reproduit (en totalité ou en partie), transmis, modifié ou utilisé à des préavis. fins publiques ou commerciales sans l’autorisation écrite et préalable de Lombard Odier. Tout investissement est exposé à une diversité de risques. Avant d’effectuer une quelconque transaction, il est Information importante sur la protection des données: Lorsque vous recevez cette communication marketing, conseillé à l’investisseur de vérifier minutieusement si elle est adaptée à sa situation personnelle et, si nécessaire, nous pouvons traiter vos données personnelles à des fins de marketing direct. Nous vous informons par la présente d’obtenir un avis professionnel indépendant quant aux risques et aux conséquences juridiques, réglementaires, que vous avez le droit de vous opposer à tout moment au traitement de vos données personnelles à des fins de fiscales, comptables ainsi qu’en matière de crédit. marketing, ce qui inclut le profilage dans la mesure où il est lié à un tel marketing direct. Si vous souhaitez vous Les performances passées n’offrent aucune garantie quant aux résultats courants ou futurs et il se peut que opposer au traitement de vos données personnelles à cet égard, veuillez vous adresser au responsable de la l’investisseur récupère un montant inférieur à celui initialement investi. La valeur de tout investissement dans une protection des données du Groupe : Banque Lombard Odier & Cie S.A., Group Data Protection Officer, 11, Rue de monnaie autre que la monnaie de base d’un portefeuille est exposée au risque de change. Les taux peuvent varier la Corraterie, 1204 Genève, Suisse. Courriel : group-dataprotection@lombardodier.com. Membres de l'UE : Pour et affecter défavorablement la valeur de l’investissement quand ce dernier est réalisé et converti dans la monnaie de plus amples informations sur la politique de protection des données en ce qui concerne le règlement général de de base de l’investisseur. La liquidité d’un investissement dépend de l’offre et de la demande. Certains produits l'UE sur la protection des données (GDPR), qui s'applique à Lombard Odier (Europe) S.A. et à ses succursales, peuvent ne pas disposer d’un marché secondaire bien établi où s’avérer difficiles à valoriser dans des conditions de Lombard Odier & Cie (Gibraltar) Limited et Lombard Odier Gestión (España) S.G.I.I.C., S.A.U., veuillez consulter le marché extrêmes, ce qui peut se traduire par une volatilité de leur cours et rendre difficile la détermination d’un prix site www.lombardodier.com/privacy-policy. pour la vente de l’actif. © 2019 Lombard Odier (Europe) S.A. – Tous droits réservés. Ref. LOESA-GM-fr-052018. Membres de l’UE : La publication du présent document de marketing a été approuvé pour utilisation par Lombard Please see important information at the end of the document 12 · Philanthropy Services· January 2020

Please see important information at the end of the document 13 · Philanthropy Services· January 2020

You can also read