Info Produits - ABN AMRO Investment ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

23-05-2016

18/03/2020

Info Produits

Product Info

Fusion – absorption de Neuflize Europe Expansion dans

ABN AMRO Pzena US Equities: update following the Coronavirus crisis

ABN AMRO Euro Smaller Companies Equities

COVID-19 CRISIS MANAGEMENT AT PZENA

AND INVESTMENT UPDATE

Committed to offer full transparency and risk management solutions to their clients, ABN AMRO Investment

Solutions asked its delegated portfolio manager Pzena about their thoughts on the stock market’s reaction to

the coronavirus and the main impact on the ABN AMRO Pzena US Equities fund regarding performances and

turnover.

With the aim of sharing as much information as possible with you in a timely manner, we gathered the write up

from Pzena as well as some Q&A from last week, as follows:

1. “Investing in Value Stocks in the Face of Coronavirus”

2. “Evaluating Opportunity During Extreme Volatility: Oil Price Collapse”

3. Q&A

1. Investing in Value Stocks in the Face of Coronavirus

Uncertainty about the coronavirus’ economic impact on the world economy has wreaked havoc on financial markets.

Certain of slowing growth, investors fear even worse – a global pandemic that tips the world into severe recession. This

has created a flight to perceived safety (i.e., utilities, REITs and government bonds) and away from economically sensitive

equities, which are highly represented within value stocks today, without consideration of an economic recovery once the

coronavirus crisis abates.

Although this knee-jerk reaction may be understandable, is it rational? Especially since over the last two years, cyclical

stocks have already massively underperformed and appeared cheap even before the coronavirus came on the scene.

We sought to answer this question by looking at how bad the earnings of cyclical stocks could be in a severe economic

downturn. As a guide, we looked at the 2007-2009 global financial crisis (GFC) which was the worst economic downturn

in recent history. During that period, the earnings of cyclical stocks fell by about half from peak to trough.

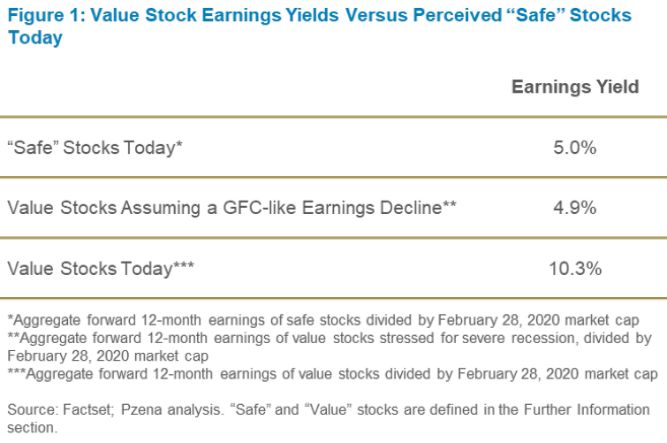

If that happened again (and there are no current signs of financial crisis, by the way), what would the earnings yield be if

we bought cheap cyclical stocks today? The answer is that the earnings yield, using the worst recession in memory, is

comparable to the current earnings yield on “safe” stocks (Figure 1). Furthermore, earnings of the cyclical stocks

rebounded quickly from that point, as companies took remedial actions and the economy improved, as we might expect

following the current crisis.

Product Info: Insights from Pzena on US portfolio – 18/03/2020. Professional investors only.

Although the depth of a future recession is impossible to predict, it is important to note that the 2007-2009 recession followed a period of economic excess, particularly in the housing and financial markets, whereas it is hard to identify significant areas of the economy that are above normal today. One might therefore expect a recession, should it occur, to be shallower than the 2007-2009 one that started in an overheated economy. We would stress that at Pzena, researching and analyzing individual companies is what drives our investment decisions. Our focus at Pzena is always on constructing concentrated portfolios of businesses that we believe offer downside protection and significant upside potential, thus exposing portfolios to outcomes skewed in our favor. Our focus is not on short-term stock price volatility – in fact, that is what creates opportunity. Our focus is on the long-term and avoiding permanent impairment of capital along the way. A critical part of our investment process is to identify businesses that have the financial and operating flexibility to weather a severe downturn before we invest, as we never know when a downturn may occur. In light of fears in the market, we wanted to briefly highlight the compelling valuations we are seeing and the analysis we have conducted to gain comfort that the probability of permanent impairment in these holdings is remote. Below we discuss our five largest portfolio holdings and our largest sector exposure – financials. General Electric Our analysis of General Electric focuses on its power segment and the components of its health care and aviation aftermarket businesses that are subject to short-cycle demand fluctuations. Revenues in GE’s health care and aviation aftermarket businesses proved resilient during the 2007-2009 recession, each experiencing top-line declines of approximately 10%. GE’s aviation segment held up better than might be expected, mainly due to aftermarket services on aircraft engines. We applied operating margins from the worst cyclical year of the past 20 for each business and assumed no contribution from the power segment. Even in this downside case we expect GE to be profitable with positive free cash flow, which does not include the benefit of working capital reductions beyond those already expected in 2020. Ford is an iconic brand with a diversified production and revenue base across five major regions around the global. We believe Ford has been taking the right steps to fortify its business in an ongoing restructuring that has demonstrated progress in anticipation of a downturn. The company has $22.3 billion of cash and $35.4 billion in available liquidity through its cash and line of credit that would allow the company to maintain operations in the event of a recession. Industry-wide supply chain issues notwithstanding, Ford’s trading at 6.6x our normal earnings estimate and 6.0x 2020 earnings with a 10.1% free cash flow yield. Consider that this company is holding the equivalent of 84% of its market cap in cash on its balance sheet, and the stock’s trading below book value (at 0.9x). Put simply, we believe Ford’s valuation offers a healthy margin of safety along with an 8.6% dividend yield. Lear is a designer and manufacturer of seating and e-systems servicing global automobile manufacturers of both internal combustion engines and electric vehicles. As the number-two supplier of seating in an industry that largely functions as a duopoly, Lear is well-positioned with a more premium product (at higher margins) and a healthier balance sheet than its number-one competitor. Lear has delivered steady organic growth in its core business and has a growth engine in its more profitable e-systems segment, which serves the increasing demand for electrification. Furthermore, the company’s asset-light, just-in-time production model allows it to downshift its production in the event of slowing demand. With cash on its balance sheet that’s roughly 23% of its overall market cap, very low leverage of just 0.2x net debt-to-operating earnings, and a stock that’s priced at 8.0x our estimate of normal earnings, we believe Lear has significant downside protection with meaningful upside potential. Oilfield Services: The crude oil market has been reacting to the threat of a protracted global economic slowdown (which would affect oil demand) as a result of the coronavirus. As it pertains to oil & gas services companies, lower oil prices could theoretically result in reduced capital expenditure (CapEx) spending by E&Ps, which is a proxy for oil service revenue. That being said, outside of US shale companies, most international oil companies (IOCs) and national oil companies (NOCs) have longer term time horizons for capital budgeting (3-5 years), so short term oil price volatility should not have a material impact on capital expenditures. Halliburton is a diversified oil services company with both US and international operations thattrades at just over 5x our normal earnings estimate. During and after the precipitous drop incrude oil prices in 2015/2016, Halliburton tooksteps to substantially right-size its operational footprint and take costs out of the business, resulting in a much leaner and more operationally efficient company. The vast improvement in the company’s cost structure means that it is now better suited to weather a potential downturn than it was pre-2015. The significant operating leverage generated during the 2015/2016 downturn also means that Halliburton is poised to benefit considerably from an improving revenue outlook. Also, Halliburton has been gaining share in the international oil services markets over the past few years. Being that IOCs & Product Info: Insights from Pzena on US portfolio – 18/03/2020. Professional investors only.

NOCs’ CapEx spending is much less elastic in response to shortterm demand shocks (most IOCs and NOCs which are majority-owned by national governments, take a longer term view of oil prices), Halliburton’s improving international presence means it’s also better positioned from a revenue standpoint in a potential downturn. National Oilwell Varco (NOV) is a manufacturer and supplier of capital equipment to the upstream oil and gas industry. NOV currently trades around 6x our normal earnings estimate, and management’s aggressive pursuit of cost initiatives have resulted in improved operating margins across all segments. NOV’s main advantage is that it operates as an asset- light business, which offers greater flexibility in responding to different macro situations. Specifically, NOV benefits from being able to better manage working capital and adjust CapEx quickly to a changing environment (CapEx is currently running well below depreciation). This shows up in the cash flow statements, as we expect NOV to be able to generate $100mm of FCF even in a 2015/2016-like environment, offering significant downside protection. Financials: Our largest sector exposure is to financials (approximately 38% of the portfolio). We recognize the leveraged nature of most financials business models and inherent wider range of outcomes. For this reason, we have built a portfolio of financials that are diverse in business models (banks, as well as other financials) and balance sheet risks. Over the last decade global banks have worked to rehabilitate their balance sheets, tightening lending standards to improve asset quality and restricting payouts to rebuild capital. Banks have significantly improved their capital ratios, with average Common Equity Tier-1 (CET-1) above 13% today, up from 7% in 2007. In the meantime, they have also consolidated, wound down or sold non-core businesses, slashed non-performing loans (NPLs) and aggressively cut costs. The increase in capital ratios and lowered risk profile should provide significant support to bank balance sheets during an economic downturn. Therefore, even in the event of credit losses in-line with the GFC, we expect an earnings downturn for our bank holdings, but not a capital/solvency event unlike the GFC. In this environment, research and selectivity are key. We focus on financials that have strong market positions, are well capitalized and benefit from resilient business models. Below we highlight the top three financial holdings (Citigroup, Capital One, and American International Group) in our portfolio. Citigroup is a leading global trade bankanchored around a dominant banking franchise and a top tier consumer & commercial bank, as well as a leading investment banking franchise. From a long-term perspective we are comfortable with this exposure while acknowledging the current environment is potentially stressful for the bank. While Citigroup suffered during the GFC due to significant North American subprime losses, today the company stands in a very different capital position and we don’t see significant excesses in its business lines. We are stress testing Citigroup by more than tripling loan losses and assuming a 100 basis point decline in interest rates. In this scenario we believe Citigroup would still be profitable, with no material impact to its capital position. Capital One is a bank with a strong credit card franchise that has a well-established history of profitable credit underwriting that has carried it successfully through difficult credit cycles. In a stressed scenario that would see a more than doubling of loan losses to levels approaching the GFC and a 100 basis-point decline in interest rates, we still believe earnings will remain positive and see no deterioration in capital. American International Group, Inc. is a US-based multi-line Insurer. Since the global financial crisis, the company successfully cleaned up its balance sheet and the Life Insurance segment.The new management team is getting back to basics, building off AIG’s industry leading positions in Specialty Insurance and High Net Worth Personal Lines, fixing the struggling commercial portfolio, and bringing the company back to peer levels of profitability. While the company was at the center of the GFC, its business model has changed markedly, as it exited higher risk businesses such as capital markets. We believe that even though earnings will turn down in our stressed scenario (which includes cutting ROE in the life business to 2009 levels), they should remain positive, and the company should suffer no material deterioration in its capital position. In the current market environment, we acknowledge that the range of outcomes related to the coronavirus is wide. We are closely monitoring uncertainties and continue to vigorously assess any potential impact to the normal and stressed earnings estimates for our portfolio holdings. Our focus at Pzena is always on constructing concentrated portfolios of businesses that we believe offer downside protection and significant upside potential, thus exposing portfolios to outcomes skewed in our favor. The environment prior to the outbreak of the coronavirus offered a wide variety of these opportunities, which has only been enhanced by the market correction. Source: Pzena analysis and figures. “Safe” stocks comprise the Communication Services, Consumer Staples, Real Estate, and Utilities sectors within the Russell 1000 Index. “Value” stocks are the cheapest quintile of stocks based on Pzena’s estimates of their price-to-normal valuations, measured on an equally weighted basis, within the universe (~1,000 largest US companies). Written on March 6, 2020 Product Info: Insights from Pzena on US portfolio – 18/03/2020. Professional investors only.

2. Evaluating Opportunity During Extreme Volatility: Oil Price Collapse

Oil prices collapsed after Saudi Arabia declared a price war on oil in response to Russia’s refusal to get on board with the

Saudi’s efforts to direct OPEC and other oil producers to cut production and stabilize oil prices. The result of the Saudi

declaration is the opposite of stability; sharply declining oil prices, and uncertainty about the future and energy sector

share prices, reflecting something akin to the early 2016 oil price environment after prices had fallen from over $100 to

the $30s (Figure 1).

We entered 2020 with expectations of substantial increases to non-

OPEC supply as new projects started up in the North Sea and

Brazil, and US Shale continues to generate production growth.

However, the coronavirus outbreak and the disruption it is causing

to the global economy is acting as a demand shock and is now

expected to depress oil demand for at least the first two quarters of

2020. Along with the expected oversupply in 2020, the market had

been optimistic about OPEC and Russia agreeing to cut supply in

the short term to balance the market. When the OPEC+ talks

collapsed, and Saudi Arabia indicated that it would drop prices and

raise volumes unilaterally, the market was faced with a

simultaneous demand and supply shock which led to the current

collapse.

Clearly, the price of oil is likely to be very weak in the near term

which will have a material impact on the earnings of the oil sector

in the short term. We are resetting our oil price assumptions lower for the near term as the oil market tries to find a new

equilibrium. However, a prolonged price war is not in the interest of any market participant including Saudi Arabia and

Russia. We expect that a new equilibrium will be found as the current low oil prices are not high enough to meet the

budgetary needs of the oil producers nor the economic requirements that support the necessary level of reserve

replenishment. So, we expect oil prices to recover. Nevertheless, we are also evaluating a ‘bear case scenario’ where

lower oil prices persist for longer, so we can better assess the range of outcomes for our energy sector investments.

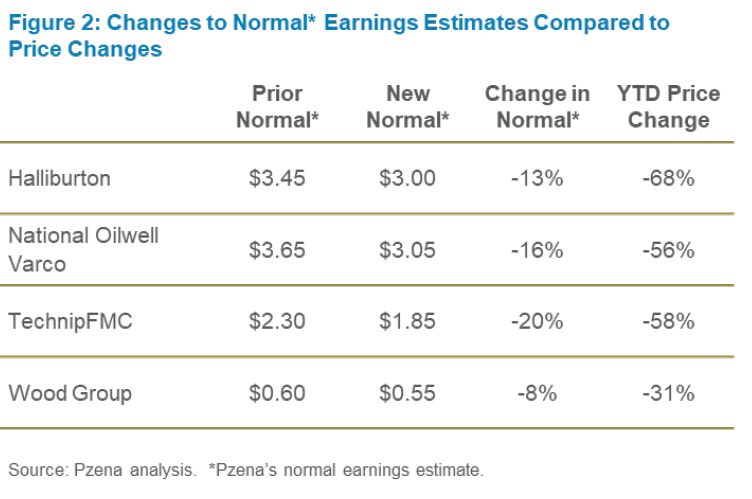

Because of lower oil prices and the economic effects from the coronavirus, the earnings and cash flow of our holdings will

be lower in the near term. This reduction in the interim cashflow will have an impact on the normal EPS estimates of our

holdings. However, the stock price reaction is much worse than the reduction in normal earnings (see Figure 2) and our

holdings are now materially cheaper on our key valuation metric:

Current Price/Normal EPS. We further believe there is minimal

risk of our holdings facing balance sheet pressure as we expect

them to generate cash even in the bear-case scenario.

Our starting point for updating our normal earnings estimates

typically begins with two basic questions:

1. What is the impact of the new information on our estimate of

normal earnings?

2. Has the new information caused a change in our assessment

of the range of outcomes and particularly the “worst-case

scenario?”

First a bit of history about our energy exposure. Our portfolio positioning in the energy sector has shifted over the past

several years. Following the collapse in oil prices that began in 2014 and bottomed in 2016, we focused our exposure

predominantly on the major oil companies, as their valuations had collapsed along with oil prices.

As the oil price rose from the mid-$20s in 2016 back up to the mid-$70s in 2018, we started shifting most of the exposure

in the portfolio from the majors into the oil service companies. Oil companies had delayed capital expenditure programs

for several years and our holdings in the majors had appreciated nearly to fair value. This brings us to our current

circumstances. With oil prices collapsing nearly in half from the $60s into the $30s in a matter of the last few weeks, we

are engaged in intensive earnings estimate reviews.

Product Info: Insights from Pzena on US portfolio – 18/03/2020. Professional investors only.As you can see from the table above, our estimates of normal earnings have modestly declined for this sample of our

energy positions given the current reality. This is because the near-term cashflows will be weaker and in some cases, we

have forced the companies to de-lever (in our models) by issuing equity at the current depressed stock prices. While we

have no doubt that the near-term impact will be significant for some of our companies, we do not believe there is a logical

argument that the companies will not continue to earn at rates similar to our original estimates over the next five years or

so. But what about the downside exposure? In this case there are some moving parts; particularly balance sheets and

cash flow estimates. So, we are using the following assumptions to develop a disaster-scenario:

1. Average Brent Oil price of around $45 in 2020 and 2021. This is similar to the average price of Brent in 2016 of

$45.18

2. Substantial contraction in activity as the oil producers reduce their reserves by 4% in 2020 and 3.5% in 2021. As

reference, the maximum reserve decline in any year to date has been 2.2%

3. Peak in Oil demand in 2028 and a slow decline thereafter

Given these assumptions, our EBITDA and free cash flow estimates in the disaster outcome are outlined in Figure 3.

We are taking the opportunity provided by the stock price collapse to add to our positions in Halliburton and Wood Group

while maintaining our positions in our other Oil Service holdings. While we would prefer never to have to face the reality

of sharp sudden declines in the market, these declines provide the fuel for value investors. There is a sense of panic in

the recent selling as thoughtful analysis and judgment have been set aside while fear drives investment decisions.

Thoughtful analysis and judgment are at the foundation of our

investment process. We re-evaluate our investments as if we are

not already invested anytime new and significant information

becomes available. Most investors react from a sense of regret

when the market moves against their positions. For us, we view

these moments as opportunities to rethink anew our investments,

consider whether we have missed something, or whether the long-

term is intact while the short term faces a dislocation. We believe

this current environment driven by coronavirus fears and oil price

roulette played by the major energy players is a rare investment

opportunity. Short term thinking is driving the market and we are

acting as we always do, as long-term focused value investors.

Source: Pzena analysis and figures.

Written on March 10, 2020

3. Additional Q&A

What’s the Net Debt/Ebitda of the fund versus Benchmark? What’s are the most levered companies and

why does the team think there are solid businesses than can easily go through a recession?

The Net Debt / EBITDA of the portfolio is 2.0x, versus 2.9x for the benchmark. If you include National Oilwell Varco whose

ratio is above 26x due to cyclically low EBITDA, the ratio for the portfolio moves up to 3.5x. At these debt levels, we don’t

view the portfolio as highly levered, though we do own some levered companies. When we think about the leverage of

the portfolio, the financials (approximately 34% of the portfolio) are top of mind, as we recognize the leveraged nature of

most financials business models and inherent wider range of outcomes. For this reason, we have built a portfolio of

financials that are diverse in business models (banks, as well as other financials) and balance sheet risks.

Over the last decade global banks have worked to rehabilitate their balance sheets, tightening lending standards to

improve asset quality and restricting payouts to rebuild capital. Banks have significantly improved their capital ratios, with

average Common Equity Tier-1 (CET-1) above 13% today, up from 7% in 2007. In the meantime, they have also

consolidated, wound down or sold noncore businesses, slashed non-performing loans (NPLs) and aggressively cut costs.

The increase in capital ratios and lowered risk profile should provide significant support to bank balance sheets during an

Product Info: Insights from Pzena on US portfolio – 18/03/2020. Professional investors only.economic downturn. Therefore, even in the event of credit losses in-line with the GFC, we expect an earnings downturn

for our bank holdings, but not a capital / solvency event unlike the GFC.

Our most levered non-financial names are National Oilwell Varco, Newell, JELD-WEN, Ryder, and Haliburton. Beyond

debt levels, we believe debt terms and maturities are important to consider. As part of our research process, we closely

examine company balance sheets. These companies all hold term debt that is covenant free, with no significant maturities

for the next several years. Additionally, our research team stress tested the entire portfolio, which contemplate the most

extreme environments, including: post 9/11 for any travel related companies and for energy names like NOV, the 2016

collapse of the oil market. We believe for the companies in the portfolio these extreme scenarios will result in only earnings

downturns and not material permanent impairment of capital.

Don’t you think Financial names are in danger with low rate environment even if Yield curve is still +0.2%?

We ran a sensitivity analysis on the banks in the portfolio, and for a 100bp move down in rates we would expect a mid-

single digit impact on EPS before mitigation on the cost side. Banks have been operating in a low interest environment

for several years now and have done a good job taking out costs and relying more on fee income. Ultimately, we believe

banks will earn a reasonable return on their deposit base, whether it’s through a normalization in the term structure of

interest rates, or through shifting to fee income.

What’s the view of the team on energy names? Don’t you think with big ESG focus of investors and

current importance of the Environment, the investments cases of energy companies are challenged?

Don’t you think it’s important to select the names with the biggest focus on the environmental

challenges?

We have attached our most current thinking on energy, with specific points on two names in the portfolio, Haliburton and

National Oilwell Varco.

With regards to ESG, for the oil and gas industry overall, we recognize the risk to overall oil demand from a move to de-

carbonize and assess that risk as part of our investment analysis. We believe the demand and oil price assumptions we

are using are, in our judgement, a realistic base case but we also test the resilience of the industry to more severe

scenarios. Even with a move de-carbonize, global oil demand is expected to continue to grow for the next ~10 years.

For the oil majors, roughly 50% of their profits come from natural gas, which we believe is the gateway fuel to a cleaner

environment in the several decade transition away from fossil fuels. The oil majors are also investing to diversify their

businesses, but these investments are relatively modest at this point. We do engage in conversations with the

management teams on the long-term direction of its businesses.

For oil services, the pressure has been two-fold, as they have also faced a slowdown in spending from the oil producers

due to the uncertainty stated above. We do believe that the current drawdown in spending is likely to reverse in the next

few years as the tailwind from the last spending boom exhausts itself and the industry has to spend again to meet market

demand and replace the barrels lost due to natural field declines.

We engage with all companies among our energy holdings on ESG related issues, specifically actions they are taking to

adapt their business models and reduce their carbon footprint.

Source: ABN AMRO Investment Solutions.

Written on March 9, 2020

We will keep monitoring Pzena’s response to the crisis and update you as needed.

AAIS Business development team.

Product Info: Insights from Pzena on US portfolio – 18/03/2020. Professional investors only.ABN AMRO Investment Solutions - AAIS

Société anonyme à Directoire et Conseil de Surveillance

au capital de 4 324 048 Euros

immatriculée au RCS de Paris sous le numéro 410 204 390,

Siège social: 3, avenue Hoche 75008 Paris, France,

Agréée par l'Autorité des Marchés Financiers, en date du 20/09/1999,

en qualité de société de gestion de portefeuilles sous le numéro GP99027

The information included in this document has been prepared by ABN AMRO Investment Solutions (“AAIS”) for

information purposes only and does not constitute a recommendation or investment advice.

The information, opinions and figures were considered to be well-founded or exact on the day they were produced,

they take account of the economic, financial or trading conditions at that time and reflect AAIS’s prevailing view of

the markets and its predictions for the future.

They have no contractual value and are subject to change. Given, therefore, that this analysis is subjective and for

information purposes only, we draw your attention to the fact that the actual changes in economic variables and

financial markets may deviate significantly from the indications provided in this document.

This document may not be reproduced or distributed and is intended only for its original addressees and may not be

used for anything other than its original purpose. It may not be reproduced or distributed, in whole or part, without

the prior written consent of AAIS and AAIS shall not be held responsible for any use made of the document by a third

party.

Product Info: Insights from Pzena on US portfolio – 18/03/2020. Professional investors only.You can also read