Quarterly Meeting 3rd quarter 2018 - PROFESSIONALS ONLY - Carmignac ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

P R O F E S S I O N A L S O N LY Quarterly Meeting 3rd quarter 2018

Didier Saint-Georges

Managing Director,

Member of the Investment Committee

PROFESSIONALS ONLY 2

US Equity Markets:

Sector Performances Since the Beginning of the Year

S&P 500 Index 9,0%

Technology 19,5%

Consumer discretionary 19,5%

Healthcare 15,2%

Energy 5,2%

Industrials 3,3%

Utilities 0,0%

Real Estate -1,0%

Finance -1,2%

Communication -3,3%

Materials -4,2%

Consumer staples -5,5%

Source: Carmignac, Bloomberg, 28/09/2018

PROFESSIONALS ONLY 3

Chinese Equity Markets:

Sector Performances Since the Beginning of the Year

-14,7% Shanghai Shenzhen CSI 300 Index

1,0% Healthcare

-2,9% Energy

-4,7% Utilities

-7,4% Consumer staples

-11,6% Finance

-18,8% Consumer discretionary

-20,4% Materials

-20,9% Industrials

-26,6% Technology

-31,5% Telecoms

Source: Carmignac, Bloomberg, 28/09/2018

PROFESSIONALS ONLY 4

Carmignac Patrimoine:

Performance Attribution Since the Beginning of the Year (%)

Net performance: -4.01%

4.1% LONG TERM CONVICTIONS

US EQUITIES, HIGH VISIBILITY STOCKS

0.2% CREDIT

TRUMP COLLATERAL EFFECTS

-5.5% (DOLLAR, EMERGING, COMMODITIES,

GOLD, CHINESE TECH)

-1.7% OTHER

Source: Carmignac, 28/09/2018

Performance shown on the graph are gross figures and do not include fees

PROFESSIONALS ONLY 5 Past performance is not a reliable indicator of future performance.

Performance of our Fund Range During the Third Quarter

EQUITY range PATRIMOINE range FIXED INCOME range

C. Investissement C. Patrimoine C. Portfolio Unconstrained

-2.61% -2.79% Global Bond

Global -0.51%

C. Investissement Latitude C. Portfolio Capital Plus

-2.66% +0.02%

C. Portfolio Grande Europe C. Long-Short C. Sécurité

-0.44% European Equities -0.41%

Europe -0.50%

C. Euro-Entrepreneurs

+0.37%

C. Emergents C. Portfolio Emerging Patrimoine

-3.72% -3.28%

Emerging

C. Portfolio

Emerging Discovery

+0.76%

C. Portfolio

Thematic Commodities

-3.33%

Source: Carmignac, 28/09/2018

Past performance is not a reliable indicator of future performance.

Performance is shown net of fees (excluding any entry charges payable to the distributor).

All the fund performances shown are those of A EUR accumulation units

A green icon represents positive Fund performance relative to the reference indicator, while an amber icon

represents negative Fund performance

PROFESSIONALS ONLY 6 relative to the reference indicator.

Frédéric Leroux

Global Fund Manager,

Head of Cross Asset Team

PROFESSIONALS ONLY 7

America First! But at What Cost?

PROFESSIONALS ONLY 8

United States: The Economic Policy « Miracle »

United States: consumption United States: investment

9% Investment outlook over 6 months (Fed

surveys), 4 months advanced

Household revenue growth

7%

expectations

5%

3%

1%

-1% Libor 3-month

real rate

Non-residential

-3%

investments (yoy %)

-5%

Source: Carmignac, Datastream, 09/2018

PROFESSIONALS ONLY 9United States: An Unusual Timing in the Economic Cycle for

a Fiscal Stimulus

Fiscal stimuli & Output gap

4,0

Economic Output Gap Trump tax plan

2,0

recovery act

1981

0,0

-2,0

Fiscal reform Bush tax cut Bush tax

-4,0 1986 2001 cut 2003

-6,0 American

recovery

Recession periods

act 2009

-8,0

Source: Carmignac, 09/2018

PROFESSIONALS ONLY 10United States:

Growth Robustness is Having its First Effects on Inflation

United States: inflation United States: wage pressure

Inflation

(Core PCE*, %yoy) Wage growth

(Atlanta Fed)

Prime age employment/

Leading indicator on inflation population ratio (4-months

(computed by the New York advanced)

Fed)

Source: Carmignac, Datastream, 09/2018

*The Core PCE Price Index is a consumer price index that excludes food and energy

PROFESSIONALS ONLY 11United States:

Overheating Risks are Threatening Wealth Effects

United States: company profitability United States: housing market

21% Existing home

sales

19%

Gross margins

17%

15%

13%

11%

9%

Household

7% Net margins confidence on

5% housing market

3%

Source: Carmignac, 09/2018

PROFESSIONALS ONLY 12It’s Getting Late Mr. Powell

Taylor rule US credit growth

8% US non financial

corporate debt growth

6% (%yoy)

Taylor rule*

4%

2%

0%

-2%

Fed’s fund rates

-4% adjusted to its balance Banking credit

sheet conditions

-6%

*Taylor’s rule is a proposed guideline for how central banks, such as the Federal Reserve, should alter

interest rates in response to changes in economic conditions.

PROFESSIONALS ONLY 13 Source: Carmignac, Bloomberg, 09/2018The United States and

the Rest of the World

PROFESSIONALS ONLY 14The Tightening Continues

Annual change in the main central banks’ balance sheets ($Bn)

$Bn

Projections

2 300

2 000

1 700

1 400

1 100

800

500

200

-100

-400

-700

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

FED ECB BOJ Total

Source: Carmignac, Bloomberg, 09/2018

PROFESSIONALS ONLY 15Monetary Tightening and Repatriation Create

a Biased Situation in Favour of the United States

$Bn $Bn

400

US Share buybacks

0

Foreign earnings

-400 retained abroad

Cash Repatriation

(1-year rolling)

-800

Source: Carmignac, 09/2018

PROFESSIONALS ONLY 16Emerging World

PROFESSIONALS ONLY 17China: The Protectionist Threat is Weakening an Economy

with an already Feeble Domestic Demand

China: consumption and investment growth

Retail sales

(%yoy)

Urban Fixed Asset

Investments (%yoy)

Source: Carmignac, Datastream, 08/2018

PROFESSIONALS ONLY 18China:

A Rate-Cut Stimulus Would Exacerbate Capital Outflows

But other ways exist

China: international dynamics China: capital outflows

$Bn

5%

China-US 5-year swap differential

4%

3% Current account,

in % of GDP

2%

1%

0% Capital outflows

Net foreign direct investments,

-1% in % of GDP

Source: Carmignac, Bloomberg, 09/2018

PROFESSIONALS ONLY 19Eurozone

PROFESSIONALS ONLY 20Eurozone:

ECB Stuck Between Inflation and Decelerating Growth

Eurozone: GDP growth (quarterly) Eurozone: inflationary pressure

Real GDP 5%

1% Labor cost Index

4%

0%

3%

-1% GDP leading indicator

(proprietary model) Regressed on

2%

unemployment and

hiring intentions

-2% (proprietary model)

1%

Source: Carmignac, 09/2018

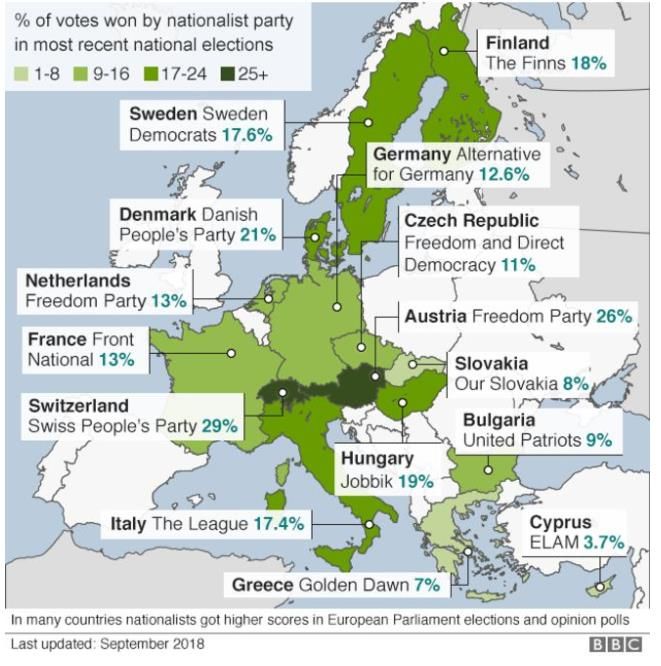

PROFESSIONALS ONLY 21Europe: An Economic Slowdown in 2019

Would Reinforce Political Risks for Markets

Rise of nationalism in Europe

Source: BBC, 09/2018

PROFESSIONALS ONLY 22Investment Strategy PROFESSIONALS ONLY 23

Investment Strategy: Same Reasons, Same Effects

10-year US rates US: relative performance vs the rest of the world

3,5%

150

MSCI USA

3,0% 140

130

2,5%

120

2,0% 110

1,5% 100

MSCI World ex-USA

90

1,0%

80

01/16 10/16 07/17 04/18

Source: Carmignac, Bloomberg

Left: 12/10/2018

PROFESSIONALS ONLY 24 Right: 28/09/2018Investment Strategy: Towards an Interest Rate Regime Shift

10-year US rates

16%

14%

12%

10%

8%

6%

4%

2%

0%

Source: Carmignac, Bloomberg, 12/10/2018

PROFESSIONALS ONLY 25Biggest Losers: Leveraged Cyclical Stocks

Sentiment towards global earnings

Both cyclical and leveraged: this cycle’s biggest losers

peaked in January

Number of stocks upgraded / Number downgraded

Weekly Earnings Revision Ratio (ERR)

3-week Rolling Average ERR 110

105 MSCI World

100

95

Average Earnings

Revision Ratio

90 Basket of leveraged cyclical

stocks

85

80

Source: Carmignac,

Left: 09/2018

PROFESSIONALS ONLY 26 Right: 19/10/2018Equity Markets: Similarities with the 60’s

60’s: S&P500 – EPS* growth

29%

United States: 60’s

18%

110 9% 13% 15% 11% 11%

8% 9% 7%

8% 2% 1% 5% 1%

100 S&P 500

7%

(LHS)

6% -9%

90 -10%

US 10-year yield (RHS) 5% -18%

60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75

80 4%

3% US corporate profits and output gap

70

2%

Inflation 1%

60

(CPI)- RHS 0%

50 -1%

Source :

Non-financial corporate profits Left: Bloomberg, 10/2018

Top: Bloomberg, 31/03/1969

Output gap, 12-month advanced Bottom: Carmignac, 09/2018

PROFESSIONALS ONLY 27 EPS: earnings per share“Nifty Fifty”: a Bubble?

Jan. 1973 Oct. 2018

« Nifty Fifty » « Nifty Fifty 2.0 »

42 21,5

average P/E

Today’s "Nifty

S&P500 P/E 19 16,8 S&P 500 Nasdaq

fifty“

10-year U.S. rates 6.9% 3.19%

Growth expectations (%)

2019 EPS* Growth 10.5% 10.1% 16.0%

Jan. 1973 : « Nifty Fifty » - P/E

Walt Disney 82 Profitability/Leverage

Intel. Flavors & Frag 78,2 Return on equity 31.4% 19.2% 20.4%

McDonald’s 72,5 Net debt to EBITDA 0.2 1.1 0.3

Baxter Intl. 71,8

Avon Products 68,3 Examples of “Nifty Fifty 2.0” stocks

Johnson & Johnson 65,2

Xerox 51,7 Mastercard

Coca Cola 50,2

Alphabet

Eli Lilly 49,8

Celgene

Booking

Merck & Co. 48,4

Tencent

Procter & Gamble 43,5

Costco

American Express 39,5

Becton-Dickinson

Source: Carmignac, Bloomberg, 10/2018

EPS = earnings per share

PROFESSIONALS ONLY 28Investment Strategy

P ER FOR MANCE RISK

DRIVERS MANAGEMENT

US Equity exposure Avoid leveraged cyclical stocks

Growth, non-cyclical, non leveraged stocks Specific hedges

Negative modified duration to core

interest rates

Emerging markets opportunities

Source: Carmignac, 28/09/2018

Portfolio composition may vary over time.

PROFESSIONALS ONLY 29Carmignac Patrimoine:

Highly Selective Performance Drivers

Portfolio construction

CREDIT 17%

NORTH AMERICA PERIPH. SOVEREIGN

22% (ex. energy & gold) DEBT 9%

CORE

4% ENERGY SOVEREIGN

DEBT 4%

10% EMERGING EMERGING

DEBT 3%

9% EUROPE CASH/CASH

EQUIVALENT 20%

2% GOLD

Currency exposure

Equities Modified duration*

USD 0% 100%

Exposure 0% 50%

EUR 0% 100%

Investment 0% 50% YEN 0% 100%

Source: Carmignac

Top: 28/09/2018

Bottom: 14/10/2018

PROFESSIONALS ONLY 30 *Modified duration is computed at the fixed income component level and not at the fund’s level.

Portfolio composition may vary over time.Rose Ouahba

Head of Fixed Income

Keith Ney

Fixed Income Fund manager

PROFESSIONALS ONLY 311) The Federal Reserve Determined to

Pursue its Monetary Policy Tightening

PROFESSIONALS ONLY 32Solid Growth Implies Higher Inflation

United States: Inflation and Output gap

2% 2,5%

3-year rolling US inflation* (annual change) Output gap

1,5% 1,5%

0,5%

1%

-0,5%

0,5% -1,5%

0% -2,5%

-0,5% -3,5%

-4,5%

-1%

-5,5%

-1,5% -6,5%

-2% -7,5%

Source: Bloomberg, Carmignac, 31/08/2018

*US PCE : US Personal Consumption Expenditure Index is a US consumer price index

PROFESSIONALS ONLY 33Real Yields Have Adjusted Upward

US 30-year yields and breakeven

2,5% 5%

30-year US real yields (left) 4,5%

2%

4%

30-year US nominal yields (right)

1,5% 3,5%

3%

1% 2,5%

2%

0,5%

1,5%

US 30-year breakeven (right)

0% 1%

Source: Bloomberg, 18/10/2018

PROFESSIONALS ONLY 34Fed Projections Are Not Yet Priced In by Markets

Fed funds projections by the Fed and the market

3,6%

3,4% 3,375

3,2%

3,125

3% 2,92 2,96

2,8% 2,92

2,875

2,6%

2,4% 2,38

2,375

2,2% Markets Fed Median

2%

1,8%

2018 2019 2020 Terminal

Source: Carmignac, 18/10/2019

PROFESSIONALS ONLY 35The Fed is Reducing its Balance Sheet

Fed –– Inflows

Fed Inflows annual

annual change

change Who

Who is

is buying

buying thethe US

US Debt?

Debt?

(in billion $)

(in billion $) (in billion $)

(in billion $)

0 2000

-3 US Bonds ex-T-bills net Issuance

-50

Fed

-100 1500

Rest of world

-150

-200 1000

-250

-300 500

-350

-400 -357 0

-391

-450

-500 -467 -500

2017 2018 2019 2020

Sources:

Left: Federal Reserve, October 2018

PROFESSIONALS ONLY 36 Right: Bloomberg, 15/10/2018US Long-Term Yields, Adjusted from FX Risk, Are Not Attractive

10-year yields in core countries after FX hedging Japanese investment in foreign bonds

for a Japanese investor (government and credit)

0,95%

0,9%

France

0,6% 0,55%

United-States (RHS)

0,3% Germany

0,15%

0,08%

0,0%

10 yr US 10 yr JPY 10 yr DE 10 yr FR

Source: Carmignac, Natwest, 18/10/2018

PROFESSIONALS ONLY 37How Equity Markets will Accommodate to a Higher Yield

Environment?

United States: real yields and equity/bond correlation

80%

2,20%

10-year US real yields – Neutral Equity/Bond weekly correlation 60%

1,60% Rate (52 weeks rolling) 40%

1,00% 20%

0,40% 0%

-20%

-0,20%

-40%

-0,80%

-60%

-1,40% -80%

-2,00% -100%

Correlation calculations based on assets weeklyperformance

Source: Carmignac, 30/09/2018

PROFESSIONALS ONLY 38Divergence Between US Growth and Rest of the World

Manufacturing PMI Index

65

60 United States

55 Eurozone

50 Emerging Markets

45

40

07 08 09 10 11 12 13 14 15 16 17 18

Sources: Bloomberg, 30/09/2018

PROFESSIONALS ONLY 39Time to Come Back on Emerging Market Debt?

EM FX EM Local Debt EM External Debt

95 7,5% +143 bps

+57 bps in 2018

90 in 2018

6,5%

7,0%

85

80 -11%

In 2018 6,5%

75 5,5%

70

6,0%

65

60 5,5% 4,5%

08/13 08/15 08/17 09/13 09/15 09/17 09/13 09/15 09/17

Source : Bloomberg, 19/10/2018

PROFESSIONALS ONLY 40Carmignac Patrimoine: US Positioning

MODIFIED DURATION

-174 bp

CURRENCY EXPOSURE

EUR 45.4%

USD 39.4%

Modified duration is rebased on the fixed income portion and not at the Fund’s level.

Portfolio may vary over time

PROFESSIONALS ONLY 41 Source: Carmignac, 19/10/20182) Europe: Surviving Financial Repression

PROFESSIONALS ONLY 42Financial Repression: Nowhere to Hide

October 2018

4

7-10yr IT

5-7yr IT

3

3-5yr IT

2 1-3yr IT

Yield

7-10yr SP

1 5-7yr SP

3-5yr SP 7-10yr FR 7-10yr GER

5-7yr FR

0 6m IT 1-3yr SP 3-5yr FR 5-7yr GER

Deposit rate 6m SP 3-5yr GER

1-3yr FR

6m FR 1-3yr GER

-1 6m GER

0 1 2 3 4 5 6 7 8 9 10

Effective Duration

Source: Bloomberg, 15/10/2018

PROFESSIONALS ONLY 43Eurozone Growth Stabilization Above

Potential Drives Continued Wage Inflation

Eurozone: growth Eurozone: wage inflation

5,0%

Model (uer-Nairu,

1% hiring intentions )

4,0%

Labor cost

index

0% 3,0%

Real GDP QoQ% 2,0%

-1%

1,0% Model (uer-Nairu, hiring

Model intent, part-time )

-2% 0,0%

Source: Carmignac, 09/2018

PROFESSIONALS ONLY 44Post-QE Supply Should Put Pressure on Rates

70 1,2%

60 1%

EMU Supply (ex-ECB) in 10yr equivalent

50 0,8%

40 0,6%

Bn€

30 0,4%

20 0,2%

10yr German rate yield

10 0%

0 -0,2%

Source: Citi Research, 18/10/2018

EMU: Economic and monetary union

PROFESSIONALS ONLY 45Not Enough Priced-in « Through Summer »

EONIA curve (in basis points)

20

10

0

20 bp-hike priced for Feb-20

-10

-20 10 bp-hike priced for Sept-19

-30

-40

Source: Bloomberg, 18/10/2018

PROFESSIONALS ONLY 46Bund Safe Haven Premium Ought to Reverse

0,2% 0,8%

Eonia 2y1m 0,7%

0,1%

0,6%

0%

0,5%

-0,1%

0,4%

-0,2%

0,3%

-0,3%

0,2%

-0,4% 10yr German Sovereign Bond Yield

0,1%

-0,5% 0%

Source: Bloomberg, 18/10/2018

PROFESSIONALS ONLY 47Real Yields Hit All-Time Low Negative in May

10y German yield versus 10y Eurozone inflation

4%

10y German real yield 10y German yield 10y EUR inflation

3%

2%

1%

0%

-1%

-2%

Source: Bloomberg, 18/10/2018

PROFESSIONALS ONLY 48Benchmark Duration Risk at All-Time High

Effective Duration - BAML Euro Government Index

7,5

7

6,5 YTM: 0.97%

6

5,5 YTM: 4.89%

5

4,5

4

Source: BAML All Maturity All Euro Government Index as at 05/10/2018

YTM: Yield to maturity

PROFESSIONALS ONLY 49Italian Budget Likely to be Rejected by the Commission

Budget deficit (in % of GDP) Government debt / GDP

1% 134%

Government projections – Parliamentary budget office

0,5% April 2018 132%

0%

Government

-0,5% 130%

projections –

-1% October 2018

128%

-1,5%

-2% 126%

-2,5% 124%

Government projections – Government projections –

-3% October 2018 April 2018

122%

-3,5% Initial draft

-4% 120%

2014 2015 2016 2017 2018 2019 2020 2021 2014 2015 2016 2017 2018 2019 2020 2021

Source: Bloomberg, European Commission, Government of Italy, Parliamentary budget office, 18/10/2018

PROFESSIONALS ONLY 50Italian Downgrade to High Yield Largely Priced

10-years rates vs ratings matrix (average rating)

4,5%

Greece

4%

Italy

3,5%

3%

2,5%

2% Spain Portugal

1,5%

1%

0,5% France

Germany

0%

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB-

BBB- BB+

BB+ BB BB- B+

Source: Bloomberg, 22/10/2018

PROFESSIONALS ONLY 51Greece: Imbalances Have Corrected

Greece: Current account & budget deficit

4%

Current account (in %) Reforms rebuilt competitiveness

0%

Growth and surplus beating Commission

-4% estimates

Large cash reserve reduces funding risk

-8%

Yields penalized by Italian and EM contagion

-12%

Budget deficit (in %)

-16%

Sources: IMF, ECB, Bloomberg, 30/09/2018

PROFESSIONALS ONLY 52European CLOs Remain Misunderstood

AAA CLO Spread vs % of loss-making tranches

iTraxx Main index (A-/BBB+) over the past 20 years

180

Global CLOs

160

Spread (basis points)

140 Baa

EMEA ABS,CMBS & RMBS

120 Aaa

100 US CMBS

80

60 Global CDOs (ex CLOs)

40

20 Global Structure Finance

0

US Sub-prime RMBS

EUR CLO 2.0, AAA Markit iTraxx Europe Main 0% 20% 40% 60% 80% 100%

Sources:

Left: Bloomberg, Citi Global Markets, 18/10/2018

PROFESSIONALS ONLY 53 Right: Goldman Sachs, November 2015Portfolio Construction

PROFESSIONALS ONLY 54Keith Ney

Carmignac Sécurité Fixed Income

Fund Manager

MODIFIED DURATION KEY FIGURES

-296 bp

Total -3 +4 Cash, T-Bills and bonds < 1

year maturity 33%

Core rates YTM 0.73%

Non-core rates

Average maturity 3.61 years

Credit

Portfolio may vary overtime

Source: Carmignac, 19/10/2018

PROFESSIONALS ONLY 55Rose Ouahba

Carmignac Patrimoine Head of

Fixed Income

MODIFIED DURATION CURRENCY EXPOSURE

-384 bp

Total -4 +10 EUR 45,4%

USD 39,4%

JPY 5,4%

Core rates GBP 4,6%

Non core rates

Asia (ex. Japan) 3,1%

EMEA 1,6%

EM rates AUD & CAD 0,3%

Latin America 2,0%

Credit

EQUITY EXPOSURE

0% 50%

Modified duration is rebased on the fixed income portion and not at the Fund’s level.

Portfolio may vary over time

PROFESSIONALS ONLY 56 Source: Carmignac, 19/10/2018David Older

Head of Equities

Haiyan Li

Analyst

PROFESSIONALS ONLY 57Carmignac Patrimoine’s Equity Philosophy Remains Unchanged

ACTIVE MANAGEMENT CONVICTION-DRIVEN RISK MANAGEMENT

So What Has Changed?

INVESTMENT BOTTOMS UP DRIVEN CONVICTIONS

PROCESS

RISK TOP-DOWN INPUT RISK / REWARD DISCIPLINE

MANAGEMENT

PROFESSIONALS ONLY 58Global Equity Investment Strategy

PROFESSIONALS ONLY 59Stock Picking is Key in the Current Environment

Tech accounted for 98% of the S&P 500’s total return in H1 2018

Relative performance of the US Sectors’ contribution to the FAANG stocks contribution to the

& World ex-US¹ indices S&P 500’s H1 2018 total return S&P 500’s H1 2018 total return

150 3,00% 4,00%

MSCI USA S&P total return: 2.65% 3.38%

3,50%

140 2,50%

3,00% S&P total return: 2.65%

2,00%

130 2,50%

1,50% 2,00%

120

1,00% 1,50%

110

0,50% 1,00%

100 0,50%

MSCI World ex-USA 0,00%

0,00%

90 -0,50%

-0,50%

80 -1,00% -1,00% -0.73%

Staples

Real Estate

Cons. Disc.

Materials

Utilities

Telecom

Tech

Energy

Industrials

Financials

Health Care

01/16 10/16 07/17 04/18 FAANG Rest of index

¹Base 100 as of the 01/01/2016

Left: Datastream, Kepler Chevreux, September 2018

Past performance is not necessarily indicative of future performance

Middle & right: S&P, BofA Merrill Lynch US Equities & US Quant Strategy, H1 2018

PROFESSIONALS ONLY 60 FAANG: Facebook, Apple, Amazon, Netflix, GoogleEven if we don’t Perceive Overall Tech Valuations as

Over-Stretched, Discipline is Key to Manage Risks

P/E ratio adjusted to growth (PEG ratio)

3.0

2.5

2.0 US Tech Profit taking on high multiple

1.5 S&P 500 growth names

(Amazon, Software companies)

1.0

0.5

0

Enterprise value to sales ratio¹

12,0x

10,0x Increased exposure to lower

Servicenow

8,0x

multiple growth stocks

PTC

(Booking.com, Electronic Arts, Google)

Splunk

6,0x

4,0x

12/16 03/17 06/17 09/17 12/17 03/18 06/18 09/18

¹Blended 12 months

Sources:

LHS: Datastream, IBES, Goldman Sachs Global Investment Research, 28/09/2018

PROFESSIONALS ONLY 61 Portfolio composition may vary over timeCarmignac Patrimoine: Increasing the Flexibility of the Portfolio

Reduction of Remain underweight leveraged Cash increase

Emerging Markets exposure cyclical stocks Figures for Carmignac Investissement²

US & European Financials

End Q1 2018:

Sold domestic 8.9% vs 10.9%

Argentine names for our reference indicator¹

3.1%

Industrials

1.0% vs 5.4%

for our reference indicator¹

Reduced Indian End Q3 2018:

banking exposure Materials ex-gold

1.6% vs 2.5% 6.7%

for our reference indicator¹

¹50% MSCI ACWI (EUR) (net dividends reinvested) + 50% Citigroup WGBI All Maturities (EUR)

²Carmignac Investissement reference indicator: MSCI ACWI (EUR) (net dividends reinvested)

Source: Carmignac, 28/09/2018

Portfolio composition may vary at any time

PROFESSIONALS ONLY 62Finding « Quality » Names Beyond the Tech Sector

Carmignac Patrimoine:

Style Concentration by sector (%)

Increase of our healthcare exposure

Where do we find quality?

6,1%

3,4%

Q2 2018 Q3 2018

Portfolio composition may vary over time

Source: Carmignac, 28/09/2018

PROFESSIONALS ONLY 63Why is the Food Delivery Industry so Attractive?

Investing across geographies

US restaurants

US addressable market % of revenue coming from food ordered

$ Bn online and consumed off premises¹

High Barriers to Entry

11%

Under- Current US online Strong “two-sided” network

$520B restaurant delivery

appreciated effects

6%

addressable $220B

market $13B Total US restaurant Focusing on Industry Leaders

opportunity industry off premise¹

Total US restaurant

industry

2016 2022E

High return business with

Changing consumer habits attractive long term profitability

Asset light “platform”

Leverage on High frequency habit

secular trends Food cooked at home

Low churn

Sources:

Top Left: Wall Street research, Waitr & Landcadia 2018

¹ Including drive through

PROFESSIONALS ONLY 64 Bottom Left: BofA Merrill Lynch, 2015

Right: Carmignac, 28/09/2018Chinese Food Delivery Leader: Meituan Dianping

Favourable dynamics for consumer services industry

650

mln

82%

156

20 million meals delivered per day

2.9 billion meals delivered in 2017

57%

Sizable addressable market (+20% CAGR*) 60%

with low online penetration (12%)

Undisputed online food delivery leader

in China with 59 % market share

10

Diversification into hotel booking services,

already a key player with 31% market share Urbanization Number of cities

Smartphone rate with over 1m

penetration rate population

Number of online

Portfolio composition may vary at any time

payment active users *Chinese local service market size growth

expectations between 2017-2023

Source: Bloomberg, JP Morgan Research,

PROFESSIONALS ONLY 65 company data, 28/09/2018Is it Time to Go Back to Emerging Markets?

Earnings Growth 2018, YoY¹ P/E Ratio (adjusted for seasonal changes)

40

35

30

25 MSCI US

20

15 DM countries

(excl. US)²

10

MSCI EM

5

S&P 500 MSCI EM EuroStoxx 50 06 07 08 09 10 11 12 13 14 15 16 17 18

Subdued EM growth

Tightening USD liquidity (Strong USD + rising rate environment)

Trade tensions

Sources:

LHS: Morgan Stanley, September 2018

¹USD for S&P 500 & MSCI EM , € for the EuroStoxx 50

RHS: Gerard Minack, 31/08/2018

²Price index in USD; Index and earnings per share deflated by U.S. CPI inflation

Based on the profits of the last 12 months in USD

PROFESSIONALS ONLY 66Selective Opportunities among Collateral Victims

of the Trade War

Example with the Quality Chinese Tech names

Performance of US vs Chinese tech sector indices Main Chinese positions of Carmignac Patrimoine¹

2017 MSCI China

200 Tech + 92% Quality: growth and cash flow

Domestic focus

150 Nasdaq

+30%

FCF yield EPS Growth

100

(2018e) (2018-2019e)

12/16 02/17 04/17 06/17 08/17 10/17

2018

6% 29%

120

Nasdaq

110 +9% 5% 68%

100

90 4% 25%

80 MSCI China

Tech -25%

70

12/17 02/18 04/18 06/18 08/18 FCF yield: Free Cash Flow yield

EPS: Earnings Per Share

Portfolio composition may vary at any time

Past performance is not necessarily indicative of future performance

¹As of the 30/06/2018

PROFESSIONALS ONLY 67 Source: Carmignac, Bloomberg, 12/10/2018Carmignac Patrimoine: Equity Breakdown

Sector Breakdown¹ Geographic Breakdown²

TECHNOLOGY INDUSTRIALS &

MATERIALS UNITED STATES

4.2%

17.2%

4.3%

25.6%

CONSUMER ENERGY EMERGING EUROPE

9.3% 4.3% MARKETS³

8.8% 8.9%

FINANCIALS HEALTHCARE

Performance drivers

6.1% 6.1% • Quality names

• Reduced EM exposure

• Favor US stocks

Source: Carmignac, 28/09/2018

Portfolio composition may vary at any time

¹Excluding telecommunications 1,6% vs 1,3% beginning 2018 & utilities 0% vs 0,4% beginning 2018

²missing Canada: 3,1%/3,8% beginning of 2018

PROFESSIONALS ONLY 68 ³excluding Russia: 0,70%/ 0,50% beginning of 2018Main Risks of Carmignac Patrimoine

Equity

The Fund may be affected by stock price variations, the scale of which is dependent on

external factors, stock trading volumes or market capitalization.

Interest rate

Interest rate risk results in a decline in the net asset value in the event of changes in

interest rates.

Credit

Credit risk is the risk that the issuer may default.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 69Main Risks of Carmignac Investissement Latitude

Equity

The Fund may be affected by stock price variations, the scale of which is dependent on

external factors, stock trading volumes or market capitalization.

Interest rate

Interest rate risk results in a decline in the net asset value in the event of changes in

interest rates.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Discretionary management

Anticipations of financial market changes made by the Management Company have a direct

effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 70Main Risks of

Carmignac Portfolio Emerging Patrimoine

Equity

The Fund may be affected by stock price variations, the scale of which is dependent on

external factors, stock trading volumes or market capitalization.

Interest rate

Interest rate risk results in a decline in the net asset value in the event of changes in

interest rates.

Credit

Credit risk is the risk that the issuer may default.

Emerging markets

Operating conditions and supervision in "emerging" markets may deviate from the

standards prevailing on the large international exchanges and have an impact on prices of

listed instruments in which the Fund may invest.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 71Main Risks of Carmignac Euro-Patrimoine

Equity

The Fund may be affected by stock price variations, the scale of which is dependent on

external factors, stock trading volumes or market capitalization.

Credit

Credit risk is the risk that the issuer may default.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Discretionary management

Anticipations of financial market changes made by the Management Company have a direct

effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 72Main Risks of Carmignac Sécurité

Interest rate

Interest rate risk results in a decline in the net asset value in the event of changes in

interest rates.

Credit

Credit risk is the risk that the issuer may default.

Risk of capital loss

The portfolio does not guarantee or protect the capital invested. Capital loss occurs when

a unit is sold at a lower price than that paid at the time of purchase.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 73Main Risks of Carmignac Portfolio

Unconstrained Global Bond

Interest rate

Interest rate risk results in a decline in the net asset value in the event of changes in

interest rates.

Credit

Credit risk is the risk that the issuer may default.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Discretionary management

Anticipations of financial market changes made by the Management Company have a direct

effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 74Main Risks of Carmignac Portfolio Capital Plus

Interest rate

Interest rate risk results in a decline in the net asset value in the event of changes in

interest rates.

Credit

Credit risk is the risk that the issuer may default.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Equity

The Fund may be affected by stock price variations, the scale of which is dependent on

external factors, stock trading volumes or market capitalization.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 75Main Risks of Carmignac Investissement

Equity

The Fund may be affected by stock price variations, the scale of which is dependent

on external factors, stock trading volumes or market capitalization.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Interest rate

Interest rate risk results in a decline in the net asset value in the event of changes in

interest rates.

Discretionary management

Anticipations of financial market changes made by the Management Company have a direct

effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 76Main Risks of Carmignac Emergents

Equity

The Fund may be affected by stock price variations, the scale of which is dependent

on external factors, stock trading volumes or market capitalization.

Emerging markets

Operating conditions and supervision in "emerging" markets may deviate from the

standards prevailing on the large international exchanges and have an impact on prices of

listed instruments in which the Fund may invest.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Discretionary management

Anticipations of financial market changes made by the Management Company have a direct

effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 77Main Risks of

Carmignac Portfolio Emerging Discovery

Equity

The Fund may be affected by stock price variations, the scale of which is dependent

on external factors, stock trading volumes or market capitalization.

Emerging markets

Operating conditions and supervision in "emerging" markets may deviate from the

standards prevailing on the large international exchanges and have an impact on prices of

listed instruments in which the Fund may invest.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Liquidity

Temporary market distortions may have an impact on the pricing conditions under which the

Fund might be caused to liquidate, initiate or modify its positions.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 78Main Risks of Carmignac Portfolio Commodities

Equity

The Fund may be affected by stock price variations, the scale of which is dependent

on external factors, stock trading volumes or market capitalization.

Commodities

Changes in commodity prices and the volatility of the sector may cause the net asset

value to fall.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Discretionary management

Anticipations of financial market changes made by the Management Company have a direct

effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 79Main Risks of Carmignac Portfolio Grande Europe

Equity

The Fund may be affected by stock price variations, the scale of which is dependent on

external factors, stock trading volumes or market capitalization.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Discretionary management

Anticipations of financial market changes made by the Management Company have a

direct effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 80Main Risks of Carmignac Euro-Entrepreneurs

Equity

The Fund may be affected by stock price variations, the scale of which is dependent

on external factors, stock trading volumes or market capitalization.

Currency

Currency risk is linked to exposure to a currency other than the Fund’s valuation currency,

either through direct investment or the use of forward financial instruments.

Liquidity

Temporary market distortions may have an impact on the pricing conditions under which

the Fund might be caused to liquidate, initiate or modify its positions.

Discretionary management

Anticipations of financial market changes made by the Management Company have a direct

effect on the Fund's performance, which depends on the stocks selected.

The Fund presents a risk of loss of capital.

PROFESSIONALS ONLY 81DISCLAIMER

This document is intended for professional clients. This document may not be reproduced, in whole or in part, without prior authorisation from the management company.

This document does not constitute a subscription offer, nor does it constitute investment advice. The information contained in this document may be partial information, and may be

modified without prior notice. Past performance is not necessarily indicative of future performance. Performances are net of fees (excluding possible entrance fees charged by the

distributor). Reference to certain securities and financial instruments is for illustrative purposes to highlight stocks that are or have been included in the portfolios of funds in the

Carmignac range. This is not intended to promote direct investment in those instruments, nor does it constitute investment advice. The Management Company is not subject to

prohibition on trading in these instruments prior to issuing any communication. The portfolios of Carmignac funds may change without previous notice. Copyright: The data published in

this presentation are the exclusive property of their owners, as mentioned on each page. The reference to a ranking or prize, is no guarantee of the future results of the UCIS or the

manager. Morningstar Rating™: © 2017 Morningstar, Inc. All Rights Reserved. The information contained herein: is proprietary to Morningstar and/or its content providers; may not be

copied or distributed; and is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any

use of this information. Carmignac Portfolio refers to the sub-funds of Carmignac Portfolio SICAV, an investment company under Luxembourg law, conforming to the UCITS Directive.

The Funds are common funds in contractual form (FCP) conforming to the UCITS Directive under French law. Access to the Funds may be subject to restrictions with regard to certain

persons or countries. The Funds may not be offered or sold, directly or indirectly, for the benefit or on behalf of a "U.S. person", according to the definition of the US Regulation S and/or

FATCA. The Funds present a risk of loss of capital. The risks, fees and ongoing charges are described in the KIIDs (Key Investor Information Document). The Funds' respective

prospectuses, KIIDs and annual reports are available at www.carmignac.com, or upon request to the Management Company. The KIIDs must be made available to the subscriber prior to

subscription. The investor should read the KIID for further information. • United Kingdom: The Funds' respective prospectuses, KIIDs, NAV and annual reports are available in English at

www.carmignac.co.uk, upon request to the Management Company, or for the French Funds, at the offices of the Facilities Agent at BNP PARIBAS SECURITIES SERVICES, operating through

its branch in London: 55 Moorgate, London EC2R. This material was prepared by Carmignac Gestion and/or Carmignac Gestion Luxembourg and is being distributed in the UK by

Carmignac Gestion Luxembourg UK Branch (Registered in England and Wales with number FC031103, CSSF agreement of 10/06/2013). The KIIDs must be made available to the subscriber

prior to subscription. Belgium: This document is intended for professional clients and has not been submitted for FSMA validation. The prospectuses, KIIDs, the net asset values and the

latest (semi-) annual management reports may be obtained, free of charge, in French or in Dutch, from the management company (tel. +352 46 70 60 1). These documents may also be

obtained via the website www.carmignac.be or from Caceis Belgium S.A., the financial service provider in Belgium, at the following address: avenue du port, 86c b320, B-1000 Brussels.

Switzerland: The Fund’s respective prospectuses, KIIDs and annual reports are available at www.carmignac.ch, or through our representative in Switzerland, CACEIS (Switzerland) SA,

Route de Signy 35, CH-1260 Nyon. Non contractual document, completion achieved on 22/10/2018.

CARMIGNAC GESTION – 24, place Vendôme - F - 75001 Paris – Tel: (+33) 01 42 86 53 35

Investment management company approved by the AMF. Public limited company with share capital of € 15,000,000 – RCS Paris B 349 501 676

CARMIGNAC GESTION LUXEMBOURG – City Link - 7, rue de la Chapelle - L-1325 Luxembourg - Tel: (+352) 46 70 60 1 – Subsidiary of Carmignac Gestion.

Investment fund management company approved by the CSSF. Public limited company with share capital of € 23,000,000 – RC Luxembourg B67549

PROFESSIONALS ONLY 82You can also read