Global Investment Weekly 2019.03.11 - CTBC Private Banking

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global Investment Weekly

2019.03.11

Market Calendar, 2019/3

W1(3/1-3/8) W2(3/10-3/15) W3(3/17-3/22) W4(3/24-3/29)

Composite PMIs(1) UK Parliament Vote US NAHB Housing US 4Q18GDP(28)

RBA Meeting(5) (12~15) Market Index(18) IFO Expectation(25)

Euro zone BOJ Meeting (15) Germany ZEW(19) US Durable Goods

DM 4Q18GDP(7) US NFIB Small EU/JP PMI(21) Orders(26)

ECB Meeting(7) Business FOMC Meeting(21) Brexit Deadline(29)

Japan 4Q18GDP(8) Optimism(12) BOE Meeting(21)

US Nonfarm EU27 New Car Germany PMI(22)

Payroll(8) Registrations(15) EU Summit(21~22)

US Consumer

Confidence(15)

BOT Meeting(20)

China Social Taiwan Export

EM Financing(10) Orders(20) SARB Meeting(28)

China Retail Sales BCB Meeting(20)

And Industrial CBC Meeting(21)

Output(10) CBR Meeting(22)

S ector

S ur pr ise

E vent

Market NPC/CPPCC Commentary

Topic And Equity/FI/FX Strategy

Source: Compiled by CTBC Bank, 2019/3/8

1

Investment Strategy Summary

With Market Realizing Positive News, Cautious On Retracement

NPC/CPPCC: 2019 Policy Target No Surprises

Market China-A: Limited Room In Short-term But Not Pessimistic

Topics CNH: Close To PBOC Satisfactory Level, Pressure To Weaken

China Bond Strategy: Supply Concern And Rising Defaults

ECB: ECB Turning Dovish

EUR: EUR Weakness In 1H19 Unlikely To Change

Policy

EU Rates: Outlook Concern/Event Risk, Downgrade

Change Germany/UK Rates

BOJ: Unlikely To Change In Mar, Apr Meeting Crucial

Investment US Strategy: 2800 Breakthrough Requires Positive News

Strategy Energy: Geopolitics Affects 2019 Oil Price And Energy Sector

Source: Compiled by CTBC Bank, 2019/3/8

2

Agenda

Part I Macro and Market Review

Part II Short-Term Focus and Strategy

3

Macro Review

Economic Data Release Review(3/1-3/7)

Macro Data: Fed Beige Book indicated 10 of the 12 regions expanded moderately with tight labor market. In addition,

ADP employment reached 183k, comparable to nonfarm payroll forecast (190k) due to release on 3/8, showing US

overall economic growth though slowed but still keep up with some momentum. Only some indicators exhibited positive

signs in EU, unlikely to reverse the current Euro Zone economic plight. Take Feb PMI as example, Manufacturing PMI

released early of the month fell to contraction zone of 49.3 but with services sector recovery, the composite PMI rose to

51.9 with leading indicator new orders and new export orders remaining weak. ECB 3/7 meeting focus: 1. maintaining

rate but downgrade growth and inflation forecasts with 2019/2020 GDP growth downgraded to 1.1% and 1.3% from

1.7%, 2. New quarterly TLTRO from 2019/9 to 2021/3 with each duration of 2 years to maintain benign bank lending.

Release Date Country Economic Data Period Consensus Actual Prior

03/01/2019 23:00 US ISM Manufacturing Feb 55.8 54.2 56.6

03/01/2019 23:00 US U. Of Mich. Sentiment Feb F 95.9 93.8 95.5

03/01/2019 17:00 EC Markit Euro Zone Manufacturing PMI Feb F 49.2 49.3 49.2

03/01/2019 16:55 GE Markit/BME Germany Manufacturing PMI Feb F 47.6 47.6 47.6

03/05/2019 17:00 EC Markit Euro Zone Services PMI Feb F 52.3 52.8 52.3

03/05/2019 17:00 EC Markit Euro Zone Composite PMI Feb F 51.4 51.9 51.4

03/05/2019 23:00 US ISM Non-manufacturing Index Feb 57.4 59.7 56.7

03/05/2019 11:30 AU RBA Cash Rate Target Mar 5 1.50% 1.50% 1.50%

03/06/2019 21:15 US ADP Employment Change Feb 190k 183k 213k

U.S. Federal Reserve Releases Beige

03/07/2019 03:00 US Book

03/07/2019 20:45 EC Euro Zone Main Refinancing Rate Mar 7 0.00% 0.00% 0.00%

Source: Bloomberg, Compiled by CTBC Bank, 2019/3/7

4

Market Review

Without Further Positive Events, Equity Retraced Under Selling Pressure

Country: Most markets fell in the past week with only Chinese equities relatively stronger with the support of

NPC/CPPCC policies. Though there is no reason to be pessimistic in the short-term, profit taking activity surged without

further positive news.

Sector: Weak outlook data of major countries and delay of ECB rate hike led to resurgence of market concern on

corporate outlook. Cyclical sectors such as Financial, Industrial and Resource fell this week while real estate, utilities,

telecom and consumer staple were relatively resilient as US 10-yr treasury yield consolidated around 2.6%. Healthcare

lost the MTD gains as US FDA head resigned and Democrats proposed Medicare-for-all in the House of Reps.

Global Equity Index Change Global Sector Index Change

Source: Bloomberg, past month is for 2018/2/4~2019/3/6, past week is for 2019/2/28~2019/3/6.

Sector indices based on Morgan Stanley Capital International (MSCI) global 11 sectors. 5

Market Review

ECB Easing Caused Market Concern Over Economy

FI: Financial market volatility caused DM bonds yield spread to widen. ECB policy expectation supported the

performance of EU HYBs but weakening EUR dragged the return of EU HYBs in dollar terms. EM bonds were also

pressurized by the concern over slowing global economic growth. Though local currency bond index yield did not

change much in the past week, FX loss had adverse impact on total return. China government report was positive to

the Chinese equity market rally so Asian HYBs and Asian bonds outperformed.

FX: ECB was more dovish than market expected, hitting EUR 1% weaker. European currencies such as GBP and CHF

depreciated as well. With rising market concern over future economic outlook, volatile currencies such as ZAR and

LatAm currencies depreciated significantly.

Global Bond Index Change Global FX Change (Against USD)

Source: Bloomberg, past month is for 2018/2/4~2019/3/6, past week is for 2019/2/28~2019/3/6

Note: Bonds take BAML Bond Index price change in the period. FX is against USD. 6

NPC/CPPCC

NPC/CPPCC 2019 Policies And Targets In Line With Expectation

2019 Government Work Report, Fiscal Policy At Focus: In 2019/3/5 NPC, Primer Li downgraded China 2019 GDP

growth target to 6%~6.5% in the government work report, in line with market expectation. We think 2019 6% would be the

bottom line for economic growth. Monetary policy removed ‘neutral’ but stressed no liquidity flooding and skewing focus to

SME. Fiscal policy was at focus of the report with deficit widening to 2.8%, slightly lower than we expected. But LGFV

would increase ¥800B to boost infrastructure investment. VAT and Social Security cut of ¥ 2trillion would alleviate corporate

burden. Employment was the focus of authority this year with more subsidies for hiring retrenched workers.

Focus After 3/15 Meetings Conclusion: Authority 2019 policy focus was in line with market expectation, alleviating

downward pressure with mainly fiscal policy and moderately monetary ease. The combination could improve outlook with

limited scope and long time. Votes of Foreign Investment and Intellectual Property Right bills next week might fuel positive

progress of Sino-US trade talk. Tech Board would be online soon as another milestone of 2019 capital market reform.

2019 Key China Policies And Targets

2017 2018 2019

Proactive, Tax Cut Policy/Target

Fiscal Target Actual Target Actual Target

GDP 6.5% 6.8% 6.5% 6.6% 6~6.5%

CPI 3% 1.6% 3.0% 2.1% 3.0%

Monetary Balanced Reasonable

M2 12% 8.1% 8.1%

Growth Match Nominal

Reasonable GDP Growth

New Social Funding 12% 12% 9.8%

Focus Employment Growth

Investment(%) - 7.2% - 5.9% -

Consumption(%) - 10.2% - 9.0% -

Downgrade 2019 Economic Growth to 6% ~6.5%

Industrial Production(%) - 6.6% - 6.2% -

Stable to Stable to Higher

Trade Growth(%) Recovery 14.2% 9.8%

Better Quality

Fiscal Deficit(trillion¥) 2.38 2.38 2.38 3.08 2.76

Deficit/GDP(%) 3.0% 2.9% 2.6% 3.4% 2.8%

New Urban Employment 11mil 13.51mil 11mil 13.61mil 11mil

Source: Compiled by CTBC Bank, 2019/03/07

7

China Equity Strategy

Limited Short-term Room For SHCOMP But Not To Be Pessimistic

Cooling Trade War, SHCOMP Recouped Losses:

SHCOMP lost over 20% since trade war from April 18. As

Strong Performance During NPC/CPPCC

Sino-US trade talk restarted and global liquidity eased, Past 10-yr Performance During NPC/CPPCC

NPC/CPPCC Period(3/3-3/15)

SHCOMP has rebounded more than 20% to 3000-3100

pts with the hope of government stimulus policies.

滬指平均漲幅(%) 上漲機率(%, 右)

8 80

Outlook And Liquidity Critical: China deleveraged last 7 70

year when oil price surged and EM countries hiked to 6 60

curb inflation, tightening onshore and offshore liquidity. 5 50

4 40

This round of liquidity fueled rally was against the weak 3 30

outlook. Whether equity falls to reflect fundamentals or 2 20

easy money boosting outlook would depend on PBOC. 1 10

0 0

Limited room in short-term but not to be pessimistic.

前五個交易日 前三個交易日 兩會期間 後三個交易日 後五個交易日

A Share Recouped Loss Since Trade War A Share Rebound Diverged From AUD

SHCOMP SHCOMP vs. AUD

3600

3500

3/22 Trump 上證指數 澳幣兌美元

3400 3800 0.8

Signed 301 MOU

3300 3600 2016-2019 Correlation 0.79 0.8

3200

3100 3400 0.8

3000 3200 0.8

2900 6/15 USTR released

2800 $50B tariff final list

3000 0.8

2700 9/24 10% tariff on $200B +24% 2800 0.7

2600 goods, to rise to 25% on 1/1 2600 0.7

2500 12/2 G20 Trump-Xi agreed 90-

day delay of 25% tariff 1/7 US team visited China

2400 to restart negotiation

2400 0.7

2018/1 2018/3 2018/5 2018/7 2018/9 2018/11 2019/1 2019/3 1/1/2016 1/1/2017 1/1/2018 1/1/2019

Source: (Bottom)Bloomberg, 2019/3/5, (Top)Datapay, Sina Finance, Compiled by CTBC Bank

8

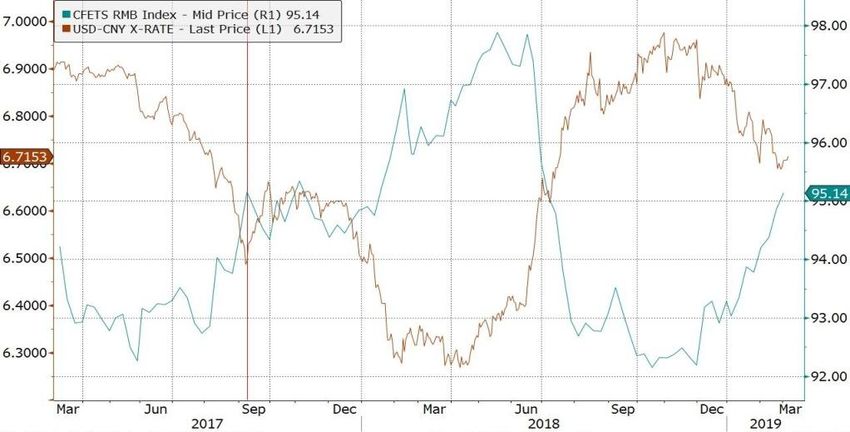

CNH Strategy

No Competitive Devaluation, Less Likely To Touch 7, Limited Upside

USD/CNH Weak Outlook For Depreciation But Sino-US Deal

Limited It: NPC/CPPCC stimulus largely met market

Upward Downward 2Q19 6.85

expectation but took time to realize. Manufacturing PMI

Deviated Realized Quant Voluntary was still in the contraction so CNH would still weaken

Reason: Sino-US negotiation accelerated. Market after positive trade news. But Sino-US MOU might

expects the MOU might be signed by the end of March, contain FX content and China reiterated not to conduct

earlier than prior consensus. The MOU is also likely to competitive devaluation. CNH is unlikely to reach 7.

include currency related contents. The base case is to

promise no competitive devaluation of CNY. Compared CNY Close To PBOC Satisfactory Level: In the rally

to qualitative items such as intellectual property rights, of early 2017, PBOC removed forward margin when

foreign market entry barrier, forced technological CFETS RMB index reached 95 and USD/CNY in 6.6-

transfer and hidden subsidies, FX and commodity 6.7 range, exiting intervention. CNY is currently at this

purchase would be priority implementation items. Weak

level so room for further appreciation would be limited.

outlook points to depreciation but at lesser extent.

Sino-US MOU To Include Currency Clause CNY Close To Level PBOC Satisfactory With

Policy Possible Measures

Remove FX

Trade Deficit China promises to purchase more US goods

Forward

Margin USD/CNY(L)

Tech China to stop ‘Made In China 2025’ subsidy, remove

forced technology transfer, protect intellectual property

rights, stop cyber theft

Market Entry China to remove entry restriction on US investments, CFETS RMB Index(R)

lower tariff and remove non-tariff barriers

Assessment Quarterly review with tariff threat

Currency China promises not conduct competitive devaluation

Source: (Bottom Left)Bloomberg Economics, 2019/2/27, Compiled by CTBC Bank, 2019/3/7, (Bottom Right)Bloomberg, 2019/3/6

9China Bond Strategy

Increased Supply Negative To Bonds, Cautious On Rising Default Pressure

Fiscal Easing Negative To Lowering Chinese Bond Yield: In light of slowing economic growth, government work

report mentioned ‘to reinforce and improve efficiency of proactive fiscal policy’, forecasting ¥2.76 trillion fiscal deficit in

2019. Though fiscal deficit at 2.8% is lower than the international safe level of 3%, but still higher than 2.6% of 2017

while LGFV bonds would increase ¥ 2.15 trillion. Though monetary easing policy target remains, widening fiscal deficit

concern and increasing issuance size would limit the downside room for yield. Strength of corporate bonds in the past

was mainly from the falling benchmark rates, less from narrowing spread. Unless SMEs could obtain liquidity more

easily from the financial system, the corporate bond performance would be adversely affected.

Corporate Bond Defaults, High Credit Risk: Chinese defaults did not improve. As China has downgraded economic

growth while monetary easing failed to deliver, bond defaults have spread from private companies to LGFVs with

Qinghai Investment USD bond delaying interest payment, triggering market concern of local government supports.

Chinese default size reached ¥14.7B YTD. Bloomberg data showed ¥200B bonds to be repaid this year with Mar/Apr as

the peak of repayment for lower rating bonds. High rating policy or quasi-sovereign bonds were still preferred.

Widening Fiscal Deficit Raised Concerns First 2 Months Default Size At Historical High

Source: (R)Bloomberg, 2019/3/5, (L)China Ministry Of Finance, Compiled by CTBC Bank, 2019/3/7

10Agenda

Part I Macro and Market Review

Part II Short-Term Focus and Strategy

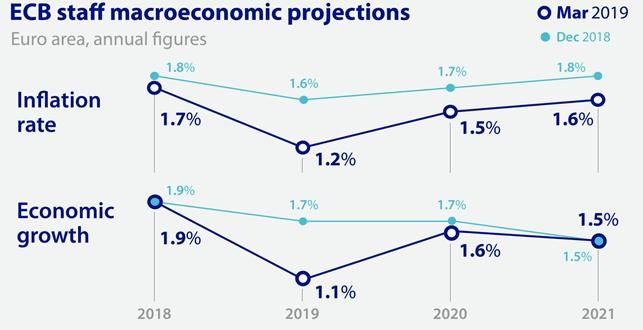

11ECB

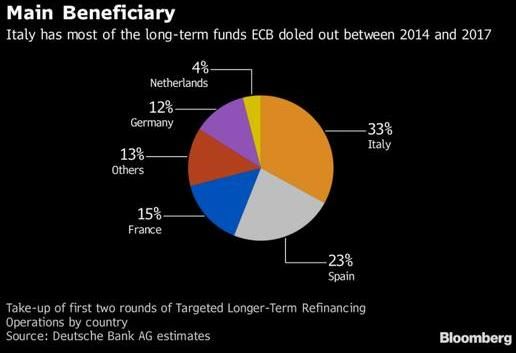

Highly Dovish ECB To Delay Rate Hike And Start New TLTRO

ECB Meeting Pessimistic About Growth This Year: The meeting held rate unchanged but downgraded economic

growth and inflation forecasts with 2019/2020 GDP growth rate downgraded to 1.1% and 1.3% respectively, and stated

economic growth outlook still faced downside risk. In terms of forward guidance, it expects to maintain the low rate

unchanged until ‘at least through the end of 2019’ (‘at least through the summer of 2019’ in prior meeting). Reinvestment

was consistent with the prior meeting citing it would persist until a fairly long period after first rate hike.

Provide Banking Liquidity, Boost Current Easing Policy: Implement quarterly TLTRO with each duration of 2 years,

starting fro 2019/9 to 2021/3 to maintain the good lending environment. TLTRO between 2014 and 2017 would gradually

mature after 2020/6. Without new round of low rate loans to banks, Italy and Spain financial institutions would be hit the

most. As Draghi said, short-term Euro zone outlook was worse than expected so ECB stayed cautious to ‘increase the

resilience of economy’, clearly turning dovish.

ECB Downgraded Growth And Inflation Forecast Italy And Spain To Benefit From New TLTRO

Source: (L)ECB, 2019/3/7, (R)Bloomberg, 2018/11/3

12EUR Strategy

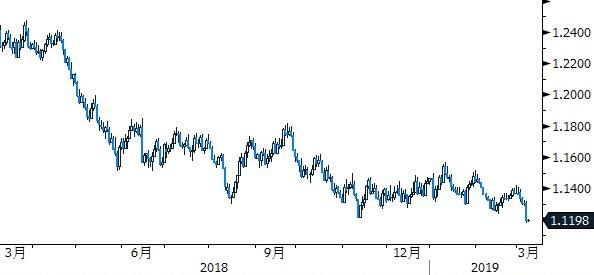

ECB More Dovish Than Expected, EUR To Maintain Weakness In 1H19

EUR Plunged After ECB Meeting: ECB was more dovish than market expected. Though we previously believe EUR to

consolidate at low in 1H19, but 1% depreciation of EUR after meeting was still weaker than our expectation. As EUR is the

heaviest weighted currency in DXY(57%), it boosted DXY to close at 97.67, rising to Dec high intraday.

EUR To Maintain Weakness In 1H19: ECB new round of TLTRO was within market expectation. It was mainly to solve

interbank credit and liquidity issue instead of massive easing. According to Goldman Sachs analysis, monetary easing

would be negative to EUR but credit improving policy would actually be positive to EUR. The real reason for EUR plunge

was a more dovish ECB than market expected. Besides amending to keep the low rate ‘at least through the summer of

2019’ to ‘at least through the end of 2019’ in the forward guidance, more importantly ECB slashed economic growth

forecast with 2019 from 1.7% to 1.1% and large downgrade in 2020. Economic outlook concerns increased financial

market volatility, leading EUR to breach the lower end of consolidation range. Without real improvement in global economy,

we hold 1H19 EUR weakness, USD strength. 2H19 EUR recovery relies on the effect of China/Eurozone stimulus policy.

EUR Breached Range Low After ECB Meeting Weak EUR Not From TLTRO But Outlook Concern

Monetary Easing Improving Credit

Impact On EUR Policy Impact

On EUR

Source: (L)Bloomberg, 2019/3/8, (R)Goldman Sachs, 2019/2/28

13Rate Strategy

Outlook Concern And Delayed Rate Hike, Cut Germany 10Y Yield Target

Euro Zone PMI Deteriorated: Fed composite PMI final

Germany 10-yr Treasury Yield

rose to 51.9 but manufacturing fell to 49.3. New orders

Upward Downward 1Q19 0.30% and new export orders were both underperforming in

Deviation Realized Quant Voluntary manufacturing, but improvement in employment index

could help Euro Zone to avoid recession.

Reason: ECB has set the dovish tone. As weak

manufacturing is one of the three major risks, PMI fell Outlook Risks Downward, Rate Hike Delay: Draghi

below 50 indicated it would take time to confirm outlook mentioned three major risks and stated relevant outlook

bottoming out. Germany treasury yield was still under

factors could ‘stay in a longer time’. Conclusion:

pressure in the short-term so we downgrade 1Q19 and

2Q19 target price to 0.30% and 0.35% respectively. maintain the low rate until end of 2019 and implement

TLTRO. Major countries’ treasury yield fell significantly.

Improved Employment Bright Spot In Feb PMI Slowing Outlook Not Recession, Cautious ECB

Source: (L)IHS Markit, 2019/2/1, (R)Bloomberg, 2018/7/21~2019/3/7

14Rate Strategy

BOE Turned Dovish, Benchmark Yield Would Be At Low

BOE Turned Dovish, Yield Cliff Fell: BOE governor

GILT 10-yr Yield Carney stated the “fog of Brexit” was creating a series

Upward Downward 1Q19 1.35% of tensions in the economy so BOE downgraded

Deviation Realized Quant Voluntary 2019/2020 GDP growth forecast to 1.2% and 1.5%,

lowest in 10 years, widely interpreted as a dovish BOE.

Reason: BOE turned dovish so investors further

delayed the expected rate hike, depressing treasury Falling Inflation: Due to falling oil price in 4Q, Jan

yield. Brexit vote was extended to 3/12, increasing the inflation fell to 1.8%, first time in 2 years to fall below

risk of no deal Brexit shock. Considering outlook and BOE’s 2% target. In the N6M, with lower energy price

inflation stable, we downgrade 1Q19/2Q19 target to

and weaker pound, inflation might not hit BOE target of

1.35%.

average 2.2% set last year.

BOE Slashed GDP Forecast GILT 10-yr Yield Fell After Dovish BOE

Brexit Uncertainty

Triggered BOE to

Slash The GDP

Growth Forecast

For 2019/2020

Source: (L)Goldman Sachs, 2019/2/7, (R)Bloomberg, 2018/8/24~2019/3/7Rate Strategy

South Africa Inflation Surprisingly Fell, SARB Rate Hike Unlikely

Jan Inflation Surprisingly Fell Below 4.5% Target:

SARB Policy Rate Jan inflation fell from prior 4.5% to 4%, much lower than

Upward Downward 1Q19 6.75% market consensus of 4.3%, mainly due to food and

Deviation Realized Quant Voluntary transportation price slide. Fuel prices such as crude oil

have fallen to ease inflationary pressure.

Reason: Expect weak oil price would lower petroleum

price in SA to 10-month low. Without major depreciation Weak Outlook Does Not Support Rate Hike: As

in ZAR, import price inflation was contained. SARB leading indicator has fallen slightly, South Africa outlook

would be less concern about inflation so we downgrade was not very optimistic. With 2019 budget bailout of

the rate target to remove the prior one hike expected.

Eskom ruled out other infrastructure investment and

We think SARB would maintain 6.75% unchanged.

electricity shortage due to strike, outlook was dim.

Recent Low Inflation Hit Mar Rate Hike Chance Leading Indicator Fell, Uncertain Outlook

110

Transportation Price 108 Leading

Fall led Dec CPI

YOY to go lower 106

104

102

100

98

96

94

92

2016/10/1

2016/12/1

2017/10/1

2017/12/1

2018/10/1

2016/2/1

2017/4/1

2018/6/1

2016/4/1

2016/6/1

2016/8/1

2017/2/1

2017/6/1

2017/8/1

2018/2/1

2018/4/1

2018/8/1

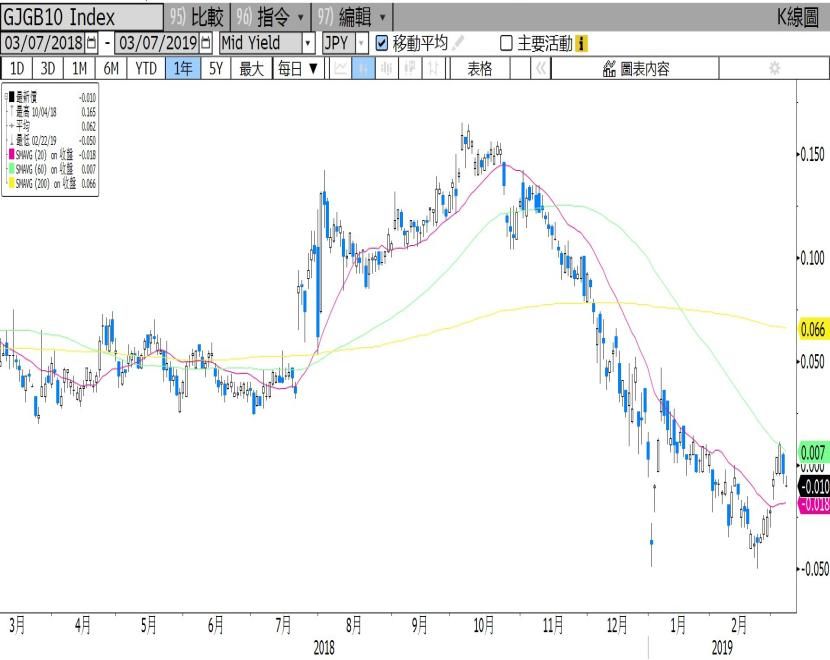

Source: (L)JP Morgan, 2019/2/23, (R)Bloomberg, 2016/2~2018/12BOJ

Hardly Any Move In Mar BOJ, Apr Meeting Crucial

Japan Manufacturing Outlook Still Unclear: Japan Jan export fell 5.3% MOM, the largest fall since Sep 18. Jan industrial

production fell 4.3% while Feb manufacturing PMI fell to 48.9. Though Japan manufacturing momentum continues to be

weak, domestic related outlook was relatively stable with Fed services PMI returning to 52.3.

Hardly Any Move In Mar BOJ, Apr Meeting Crucial: Considering the mixed Japan outlook and current levels of JPY and

10-yr JGB yield, we think BOJ Mar meeting would not have large changes. But Apr BOJ meeting would be more important

as BOJ would release yearly economic outlook forecast up to 2021. If global outlook does not improve with major central

banks continue to be dovish, we think BOJ might change its attitude towards easing. Though the benchmark rate is likely to

be held, BOJ might increase the bond purchase program to lower the yield.

Jan Japan Manufacturing data Were Weak Japan 10-yr Treasury Yield At The Low

Japan 10-yr Treasury Yield Returned To

Positive, Expect Consolidation At Low

Source: (L)Nomura, 2005/01~2019/01, (R)Bloomberg, 2018/03~2019/03

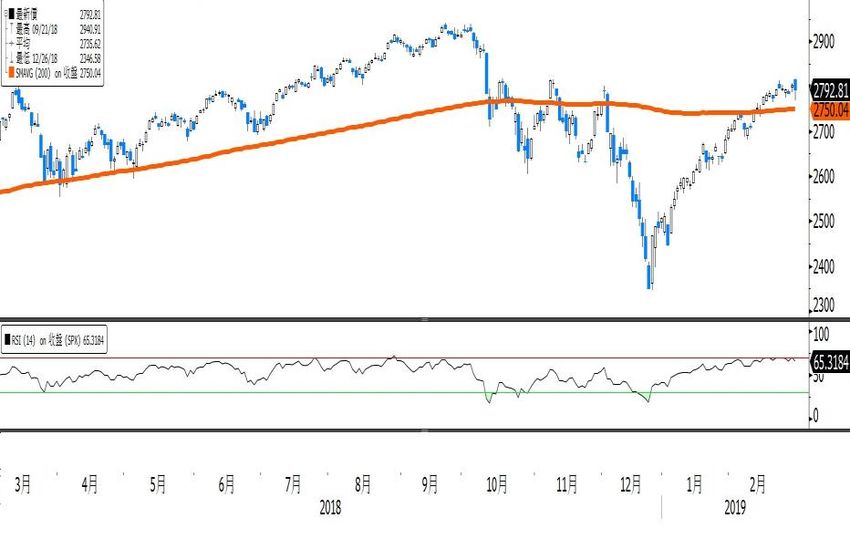

17US Equity Strategy

2800 Resistance Breakthrough Requires Multiple Factors

US Equity Reflected Dovish Fed And Lower Trade Risk: US

US Equity Reflected Dovish Fed/Sino-US Talk

equity has rallied 11% YTD with P/E ratio returning to long-term

average, reflecting the dovish Fed and lower trade risk. Market Monitoring Factors Market Reaction

rumored trade deal to sign on 3/27, expect diminishing impact. Fed Turning Dovish Upward

US Equity Faces 2800 Resistance, Breakthrough Requires

Optimistic Sino-US Talk Upward

Multiple Factors: S&P500 has challenged and failed to break

through 2800 since Aug 18. While it approaches 2800 again, we Corporate Earnings Neutral

think, in the Mar windows period of financial results, further rally Confidence

requires US economy to bottom out, automotive trade deal to US Economy Bottom-out Neutral

progress, Fed to confirm the end of QT. Any of the above news

could trigger market volatility. Fundamental Downward

US Equity Faces 2800 Resistance Hurdle US Equity Fund Outflow YTD

Unit: Mil USD

Resistance: 2800

200DMA

>70 Overbought

RSI (14D)Energy Strategy

Geopolitics Affects 2Q19 Oil Price And Energy Sector

1Q19 Crude Oil Balanced: Saudi planned to further cuts in Mar but Russia planned to accelerate its behind schedule

cuts in end of Mar/Apr while US production and inventory rose. Overall we maintain 1Q19 Brent $66/barrel target.

Expect 2Q19 Oversupply Narrows: 1. Venezuela sanction cuts its output, 2. US oil rig count 1Q19 fell, negative to

upstream equipment sector, delaying 2Q19 US oil production, 3. US to maintain current waiver of Iranian oil in May, 4.

Expect OPEC+ only to respond to Trump oil policy in amending output cut in Jun. With 3Q19 demand recovery, we

expect OPEC+ to shrink output cut with Brent in $60~70/barrel in 2Q19.

Sino-US Deal Increases US Oil/Gas Purchase Benefits Energy Sector In 2H19: Sources of China crude oil import

were dispersed from Russia (15%), Saudi(11%), Iraq and Angola. US crude export average 1900k barrel/day last year

with 250k to China. With rising US oil output and export, if China boosts US purchase, 2H19 premium between Brent

and WTI could reduce from $10 to $6. China LNG import is 60% of total gas import, mainly from Australia, Qatar and

Malaysia totaling 72% and only 4% from US. Higher purchase will benefit US Integrated Energy Producers.

2Q19 Oil Price Affected By US, OPEC+ US Waiver Of Iranian Oil Scenario Analysis

Maintain If Brent is above $65/barrel in early May, US is

Current likely to maintain the current waiver, 2Q19 Brent

Waiver target would be $66/barrel

Cut If Iran oil export reduces 150k-250k barrels/day,

Waiver oil price could rise $2/barrel

Total If Iran oil export reduces 500k barrels/day, oil

Ban price could rise $5/barrel

Source: Bloomberg, 2019/3/6, Compiled by CTBC Bank, 2019/3/6

19Target Price

Target Price – Rates/FI

Source: Compiled by CTBC Bank, 2019/3/8 : TP Adjustment

20Target Price

Target Price - Equity

Source: Compiled by CTBC Bank, 2019/3/8 : TP Adjustment

21Target Price

Target Price – FX/Commodity

Source: Compiled by CTBC Bank, 2019/3/8 : TP Adjustment

22GENERAL DISCLAIMERS:

1. This document and the investments and/or products referred to herein are for information only and do not have regard to your specific investment objectives, financial situation or particular needs.

2. This document and the investments and/or products referred to herein should not be construed as any recommendation for you to enter into the investment briefly described above and this document must

be read with CTBC’s General Terms and Conditions including without limitation Risks Disclosure Statements, Supplemental Terms and Conditions and such terms and conditions specified by CTBC from time to

time.

3. You are advised to exercise caution in relation to this document. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice from a licensed or

exempt financial adviser before making your commitment to invest in the investments and/or products referred to herein.

4. If you choose not to seek advice from a licensed or exempt financial adviser or such other independent professional, you should carefully consider whether investment in the investments and/or products

referred to herein is suitable and appropriate for you taking into consideration the risks and associated risks.

5. The final terms and conditions of the proposed investment in the investments and/or products referred to herein will have to be set out in full in the definitive trade confirmation between CTBC and you.

6. CTBC does not guarantee the accuracy or completeness of any information contained herein or otherwise provided by CTBC at any time. All of the information here may change at any time without notice.

7. CTBC is not responsible for any loss or damage suffered arising from this document.

8. CTBC may act as principal or agent in similar transactions or in transactions with respect to the instruments underlying the transaction.

9. Until such time you appoint CTBC, CTBC is not acting in the capacity of your financial adviser or fiduciary.

10. Investments involve risks. Past performance figures, predictions or projections are not necessarily indicative of future or likely performance. Actual performance may differ from the projections in this

document.

11. Any references to a company, financial product etc is used for illustrative purpose and does not represent our recommendation in any way.

12. Any scenario analysis is provided for illustrative purpose only and is no indication as to future performance and it does not reflect a complete analysis of all possible scenarios that may arise under an actual

transaction. All opinions and estimates given in the scenarios are illustrative and do not represent actual transactions.

13. The information in this document must not be reproduced or shared without our written agreement.

14. This document does not identify all the risks or material considerations that may be associated with you entering into of the transaction and the transaction period you wish to consider.

15. This document does not and is not intended to predict actual results and no assurances whatsoever are given with respect thereto. It does not present all possible outcomes or takes into consideration all

factors that may affect or influence the transaction.

16. This document is based on CTBC’s understanding that you have inter alia sufficient knowledge, experience and access to professional advice to make your own evaluation and choices of the merits and risks

of such investments and you are not relying on the CTBC nor any of our representatives or affiliates for information, advice or recommendations of any sort whatsoever.

17. You should have determined without relying on CTBC or any of our representatives or affiliates for information, advice or recommendations of any sort whatsoever, the economic risks and merits as well as

the legal tax and accounting aspects and consequences of the transaction and that you are able to fully assume such risks.

18. CTBC accepts no responsibility or liability whatsoever for any loss of whatsoever nature suffered by you arising from the use of this document or reliance on the information contained herein.

19. CTBC may have alliances with product providers for which CTBC may receive a fee and product providers may also receive fees from your investments.

20. The following exemptions under the Financial Advisers Regulations apply to the CTBC and its representatives:

(1) Regulation 33(1) – Exemption from complying with section 25 of the Financial Advisers Act (“FAA”) when making a recommendation in respect of (a) any designated investment product (within

the meaning of section 25(6) of the FAA) to an accredited investor; (b) any designated investment product (within the meaning of section 25(6) of the FAA) that is a capital market product, to an

expert investor;

(2) Regulation 34(1) – Exemption from complying with section 27 of the FAA when making a recommendation in respect of (a) any investment product to an accredited investor; (b) any capital

markets product to an expert investor or (c) any Government securities;

(3) Regulations 36(1) and (2) – Exemption from complying with sections 25, 26, 27, 28, 29, 32, 34 and 36 of the FAA when providing any financial advisory service to any person outside of Singapore

who is (a) an individual and (i) not a citizen of Singapore; (ii) not a permanent resident of Singapore; and (iii) not wholly or partly dependant on a citizen or permanent resident of Singapore; or (b)

in any other case , a person with no commercial or physical presence in Singapore.

23You can also read