Impact of COVID-19 on Insurers - Special Series on COVID-19

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

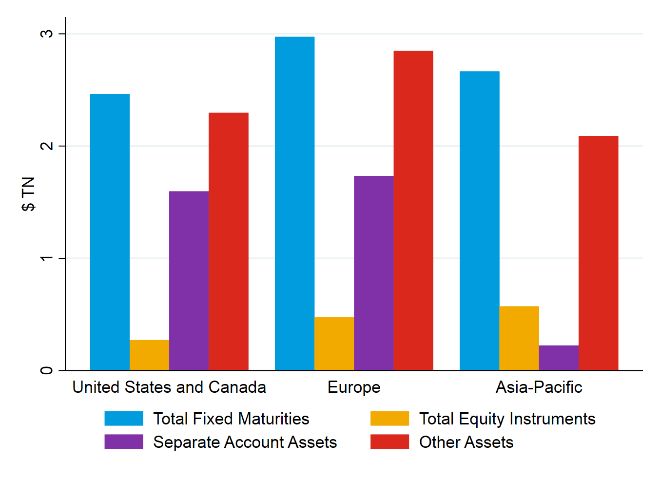

Special Series on COVID-19 The Special Series notes are produced by IMF experts to help members address the economic effects of COVID-19. The views expressed in these notes are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management. May 18, 2020 Impact of COVID-19 on Insurers Divya Kirti and Mu Yang Shin 1 The grim impact of COVID-19—extensive financial dislocations across asset classes and potentially large increases in morbidity and mortality—could be challenging for insurers. Life insurers could be hit particularly hard. Should mortality reach levels seen in large past pandemics such as the Spanish flu, payouts would be significant relative to capital for life insurers. Widespread asset-rating downgrades and persistently low interest rates would add to the difficult environment. In a scenario with widespread bond rating downgrades, regulators should closely monitor and reassess linkages to rating actions within supervisory frameworks, while enhancing supervision for insurers with risky holdings. However, any changes would need to be designed carefully to avoid relaxation in the overall level of capital requirements. Central banks looking to preserve credit supply should account for changes in insurer risk appetite, which could take place well before capital levels approach regulatory thresholds. Financial stability assessments should examine the implications of the pandemic for insurers. I. STYLIZED FACTS ABOUT INSURERS Insurers are important financial intermediaries, holding about $20 trillion in assets across North America, Europe, and Asia-Pacific (Figure 1) and more than $33 trillion globally (FSB 2020). Life insurers need to manage risk transfer over long horizons, as their liabilities commit them to payouts decades ahead. In contrast, property and casualty (P&C) and health insurers aim to match payouts and premiums within relatively short periods and can reprice contracts more frequently. Consequently, life insurers tend to hold more long-term fixed- income investments than other insurers. Like other financial intermediaries, insurers tend to be much more levered than nonfinancial corporations. 2 1 For more information, contact DKirti@imf.org. 2 Equity finances roughly 15 percent, 10 percent, and 7 percent of insurers’ assets in North America, Asia-Pacific, and Europe, respectively. IMF | Research |1

FIGURE 1. Stylized Facts on Global Insurers by Region

A. Total assets B. Asset class breakdown

Sources: S&P Global Market Intelligence and IMF staff analysis.

Note: This figure and subsequent figures use data as of end-2019, unless otherwise noted.

II. IMPACT OF COVID-19 ON INSURERS

COVID-19 will affect insurers both directly, via health shocks (increases in mortality and morbidity), and

indirectly, via financial shocks (lower equity prices, higher credit spreads, widespread downgrades, and lower

short-term and long-term interest rates including due to quantitative easing). The financial impact of recent

epidemics has been far larger than the direct health impact. Insurance regulators have taken a flexible approach

to prudential regulation (see a complementary note by the IMF Monetary and Capital Markets department

“Regulatory and Supervisory Response to Deal with Coronavirus Impact: The Insurance Sector”). 3

Insurers’ exposure to these shocks varies by line of business. For example, life insurers have longer-term

liabilities, and hence large liability duration exposure. These long-term liabilities also permit longer-term

investment horizons, potentially supporting financial stability (Chodorow-Reich, Ghent and Haddad 2020, IAIS

2019). The impact of market movements on regulatory requirements also varies across jurisdictions.

Life insurers provide protection for both mortality and longevity risk. 4 Joint provision of both types of protection

can help insurers manage risk. In a pandemic with significant mortality, life insurance claims rise immediately,

whereas expected future payments on life-contingent annuities fall. These risks can therefore offset each other

from a long-term solvency perspective, although large life insurance claims may have a meaningful short-term

impact. Moreover, annuities typically pay out account values upon death prior to annuitization. Although the

majority of variable annuities do not offer guaranteed returns, some insurers do provide guarantees and face

pressure from falling equity prices and higher volatility. 5 Run risk is generally perceived to be lower than for

banks; most withdrawals trigger large surrender charges, repricing of mortality risk, or adverse tax

consequences (Figure 2, Paulson and others 2014), although nontraditional liabilities such as institutional

3 The European Insurance and Occupational Pensions Authority (EIOPA) issued a statement noting that Solvency II allows for flexibility on supervisory

interventions in extreme situations, including measures to extend the recovery period of affected insurers. Regulators in the United Kingdom and Italy have

added flexibility on the valuation of insurance liabilities. The US National Association of Insurance Commissioners (NAIC) and state regulators have relaxed

announcing standards to include delayed payments of premiums in admitted assets.

4 Life insurance policies generally do not include “pandemic” exclusions. Capital requirement regimes use pandemic scenarios as inputs.

5 Variable annuity providers have seen their stock prices fall by as much as 50–70 percent in the first quarter of 2020 (Koijen and Yogo 2020). The cost of

hedging via equity derivatives rise with market volatility.

IMF | Research |2

borrowing, borrowing from Federal Home Loan Banks, and securities lending have increased in recent years

(Foley-Fisher, Narajabad, and Verani 2019).

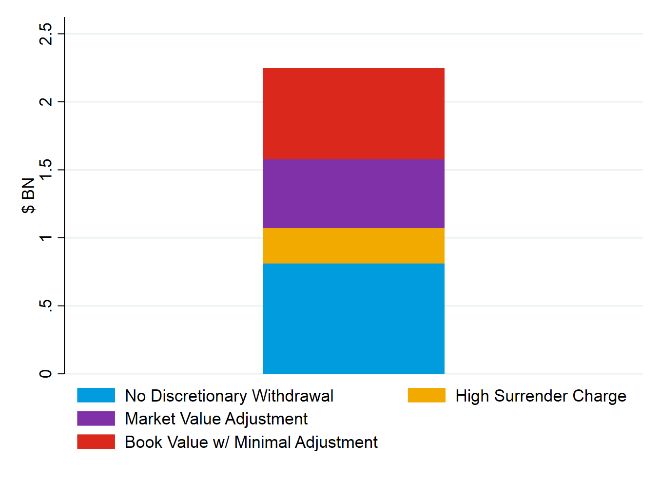

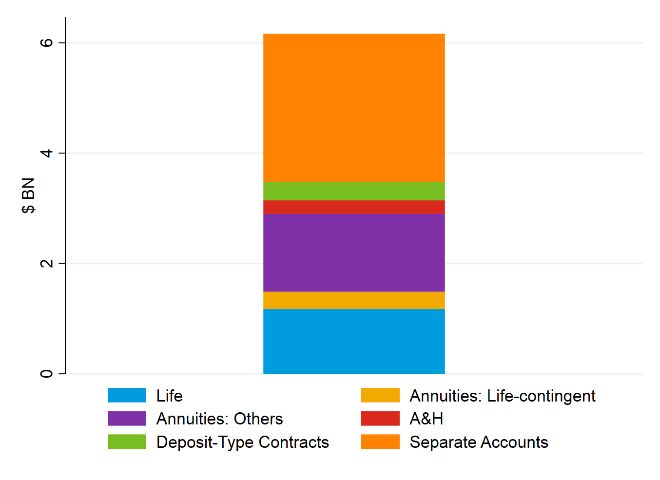

FIGURE 2. Liabilities of US Life Insurers

A. All liabilities B. Annuities by withdrawal characteristics

Sources: S&P Global Market Intelligence; and IMF staff analysis.

Note: Panel A shows the breakdown of the US life insurance industry’s aggregate reserves by type. Life-contingent annuities include immediate and annuitized

policies. Other annuities are still in the build-up phase. Panel A shows liabilities net of reinsurance. Panel B shows the breakdown of annuities by withdrawal

characteristics. Panel B shows liabilities before reinsurance.

Life insurers are large holders of corporate and sovereign bonds, and hence are important nonbank sources of

credit to the economy. 6 In the United States, insurers hold assets on a comparable scale to banks. To the extent

that insurers are hit hard by this crisis, their risk appetite may be curtailed, affecting credit supply to the broader

economy. Insurers hit hard by the global financial crisis (GFC) pulled back from risk taking (Kirti 2019).

Regulatory treatment, which can be an important determinant of the response to market stress, varies by

jurisdiction. US life insurers are generally not required to mark bonds to market for the purpose of determining

regulatory capital. 7 European insurers are required to mark assets and liabilities to market under Solvency II.

Capital requirements for US insurers are tied to regulatory risk categorization of assets. For most asset classes,

regulatory risk categories are a function of credit ratings. US life insurers’ holdings are somewhat skewed

toward bonds only one or two rating notches above regulatory thresholds for significantly higher risk weights

(Figure 3, Becker and Ivashina 2015). Risk weights for junk bonds are more than triple those for investment

grade bonds. Downgraded bonds tend to be sold by insurers facing capital pressure (Ellul, Jotikasthira, and

Lundblad 2011).

During the GFC, mortgage-backed securities (MBS) suffered mass rating downgrades. Risk classification of

MBS was therefore modified in a manner that incentivized US insurers to mark bonds to market (reducing both

actual and required capital) and likely prevented fire sales (Hanley and Nikolova 2020). 8 However, the change in

regulatory treatment was permanent, not temporary, and dramatically altered the capital treatment of MBS

(Becker, Opp, and Saidi 2020). It also applied to new purchases of MBS. US insurers have been

6 Fixed-income investments account for a large share of life insurers’ assets, except for equities held in segregated accounts backing pass-through policies

(variable annuity or unit-linked policies).

7 US life insurers generally do not need to mark bonds to market, unless they deem the losses to be “other than temporary.” Some state regulators can require

marking to market (Ellul and others 2015).

8 Risk categorization of MBS was previously based on credit ratings, as is still the case for corporate bonds. Risk categories for MBS are now linked to modeled

expected losses relative to book value.

IMF | Research |3

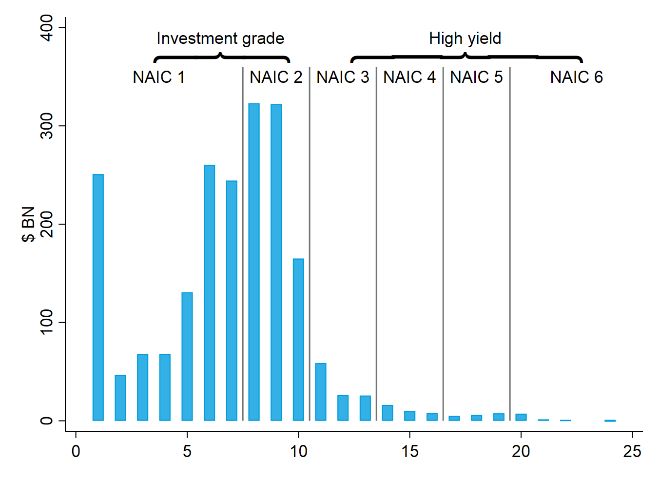

disproportionate purchasers of newly issued junk MBS in recent years (Becker, Opp, and Saidi 2020), and private equity-backed insurers have actively added risky MBS to their portfolios (Kirti and Sarin 2020). FIGURE 3. General Account Bond Holdings of US Life Insurers by Rating and Regulatory Category Sources: S&P Global Market Intelligence; and IMF staff analysis. Note: This figure shows the distribution of credit ratings within general account bond holdings converted to a numeric scale of 1–25 with lower values corresponding to better ratings. Credit ratings are computed as the median of Fitch, Moody’s, and S&P ratings as of April 30, 2020. If only two ratings are available, the lower rating (higher number) is used. General account assets back liabilities excluding pass-through policies such as variable annuities, for which assets are held in segregated accounts. In a scenario with widespread downgrades of corporate bonds or collateralized loan obligations (CLOs), changes that decouple capital treatment from ratings may help safeguard financial stability. However, any changes would need to be designed carefully to avoid relaxation in the overall level of capital requirements or other unintended consequences. Such changes should be considered only after all supervisory measures have been taken (see a complementary note by the IMF Monetary and Capital Markets department “Regulatory and Supervisory Response to Deal with Coronavirus Impact: The Insurance Sector”). Lower interest rates across tenors will also have a significant impact on life insurers. Long-term liabilities mean that life insurers have high liability duration. Life insurers may face a trade-off between obtaining asset duration to offset this liability exposure and boosting returns. Lower long-term rates may therefore impact insurers’ willingness to take on credit risk. More broadly, insurers’ portfolio choices tend to amplify changes to long-term rates including changes induced through quantitative easing (Domanski, Shin, and Sushko 2017, Koijen, Koulischer, Nguyen, and Yogo 2020). P&C insurers provide protection against various kinds of losses to property and business, typically via short- term contracts that are repriced comparatively frequently. Consequently, they hold a larger share of assets than life insurers in equities and are likely to be affected by equity market turmoil. A large exposure for many P&C insurers pertains to motor vehicle insurance. In an environment with lockdowns and reduced traffic accidents, claims are likely to fall. However, insurers are also seeing demands to return “excess” premiums. P&C insurers also provide business-interruption protection. These policies are generally thought to include coverage language or exclusions that would prevent coverage for losses resulting from pandemics. However, insurers are facing heavy pressure (via litigation, legislative discussions, and lobbying) in several jurisdictions to include the current shock in coverage. In a scenario where the current shock is deemed to be covered, P&C insurers would face very large claims. Health insurers may see higher claims due to increased costs and may need to bear a higher share of costs due to policy initiatives. On the other hand, some governments are stepping in with plans to cover costs themselves, and procedures unrelated to COVID-19 may fall. US legislative efforts to date seem more focused on hospitals IMF | Research |4

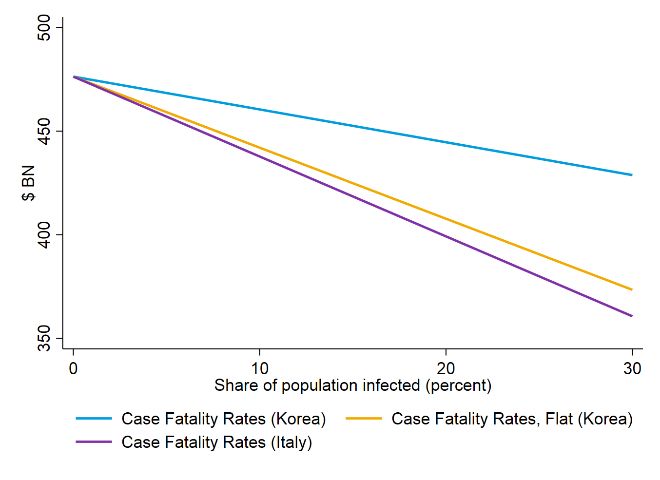

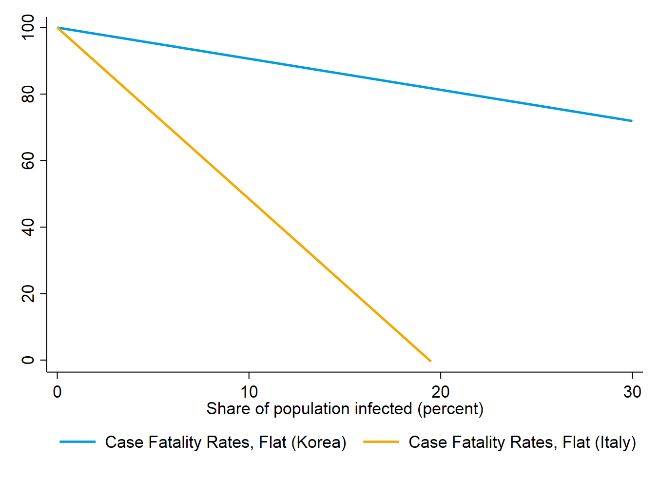

and providers than on health insurers. Growth in new business may slow across countries with slower economic growth, or in the United States, with higher unemployment. Reinsurers may bear concentrated pandemic risk, and the reinsurance market for mortality risk is generally viewed to be highly concentrated. Reinsurers could face significant new claims. Catastrophe reinsurance prices generally rise after large shocks (Froot 2001); the same may happen for mortality reinsurance. III. POTENTIAL TRANSMISSION CHANNELS TO OTHER SECTORS If insurers are hit hard, risk appetite may be impaired. This would effectively reduce credit supply to riskier borrowers, who may see spreads and the cost of new external finance rise. As insurers are an important source of credit to the economy, policymakers working to preserve credit supply to the economy should account for any changes to insurers’ risk appetite. Downgraded bonds may see fire sales, particularly if downgrades are widespread, although selling distressed assets would potentially trigger recognition of losses that permanently impair RBC ratios, which would disincentivize fire sales. IV. IMPACT ON US LIFE INSURERS This section presents estimates of the impact of COVID-19 on capitalization levels for US life insurers, considering both the direct pandemic shock and the indirect financial shock, using insurer-level data. Pandemic Shock Outflows due to life insurance claims that reduce actual capital This note bases key assumptions (share of population with coverage and average size of policy by age group, and extent to which mortality may be lower conditional on coverage) on a report prepared by the SOA (2007) and applies case fatality rates by age group as experienced in Korea (a more benign scenario) or Italy (a more severe scenario with limited health care capacity) as of April 30, 2020. This analysis makes several simplifying assumptions: mortality rates are assumed to be fixed within age group, reinsurance (including affiliate reinsurance) is assumed to be fully paid, and participating life contracts are not analyzed. 9 Annuities are also not analyzed: this ignores both death benefits payable on annuities in the buildup phase (80 percent of US annuity reserves) and reductions in ongoing payments on immediate and annuitized annuities. Although the pandemic appears to be tapering in Europe and even the United States as of mid-May 2020, it is currently difficult to exclude further waves of infections. Figure 4 shows the impact on US life insurers as a share of capital given the share of the population affected by COVID-19. Insurers, regulators, and industry observers typically use an excess death ratio of 1.5 per 1,000 as a standard pandemic stress test scenario. In the United States, this would imply about 500,000 deaths (more than 8 percent of the population affected at case fatality rates seen in Korea), larger than current estimates of the potential death toll released by US authorities. In such a scenario, losses would be about $26 billion, or about 5.5 percent of current industry capital. 10 Should the 9 Uncertainty about the mortality rate from COVID-19 remains very large. Current case fatality rates may overestimate mortality as all cases may not have been detected. Mortality rates may also be even lower within age groups for holders of life insurance policies than is assumed here—mortality rates from flu and pneumonia are lower in US counties with higher incomes (SOA 2020). On the other hand, some deaths due to COVID-19 may have been incorrectly attributed to other causes. Mortality rates from other causes may increase with stress and loss of access to medical treatment. The US Centers for Disease Control and Prevention report that excess deaths from all causes have risen markedly since late March 2020. Affiliate reinsurance may not be fully paid (Koijen and Yogo 2016). Media reports indicate that some life insurers have significantly raised prices for mortality coverage due to the mortality impact of COVID-19 and the new market environment. 10 This note provides estimates net of reinsurance, assuming reinsurance claims are fully paid. The 2015 US Financial Sector Assessment Program (IMF 2015) reported estimated losses of $20–25 billion, gross of reinsurance, in a standard pandemic scenario. IMF | Research |5

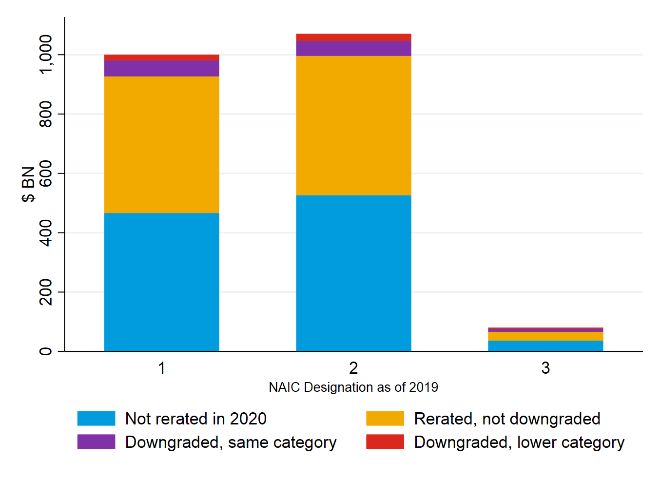

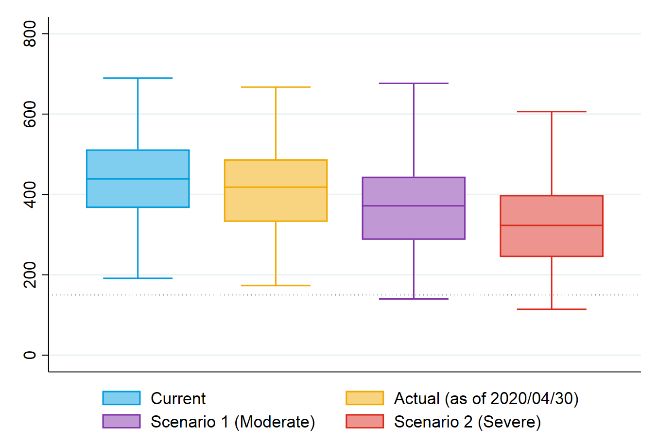

pandemic prove challenging to control (with treatment and vaccines remaining elusive), an extreme scenario in which 30 percent of the population is affected (more comparable to the 1918 Spanish flu) could become relevant. In such a scenario, losses would be more than $90 billion—nearly 20 percent of current capital. Such a scenario would likely unfold over multiple years, giving insurers additional time to accumulate new net premium income. FIGURE 4. Impact of Potential Mortality Claims on US Life Insurer Regulatory Capital Sources: S&P Global Market Intelligence; and IMF staff analysis. Note: This figure shows the US life insurance industry’s aggregate capital net of pretax excess claims as a function of the share of population infected. Estimates are based on the age-group-specific number of policyholders and average face amount in force used by SOA (2007), adjusted to match the current US population and stock of life insurance in force net of reinsurance as of end 2019 (close to $20 trillion). Case fatality rates by age group as of April 30, 2020, are from the Italian National Institute of Health and the Korean Ministry of Health and Welfare. Case fatality rates are assumed to be 23 percent lower for the insured population as in the severe scenario used by SOA (2007). For comparison, Figure 4 also shows the implications of assuming flat mortality and coverage patterns across age groups. There are two offsetting forces: first, COVID-19 is particularly deadly for older people, and second, life insurance coverage and amounts peak prior to retirement. With the two combined, using flat mortality and coverage patterns overstate the impact on capital. Financial Shock Rating downgrades that increase required capital Despite unprecedented policy responses from monetary and fiscal authorities, many corporate issuers may face rating downgrades due to the widespread economic fallout from COVID-19. If downgrades move assets into higher-risk regulatory categories, capital requirements would increase. This analysis focuses on the impact of rating downgrades on required capital. Marking to market and realizing losses would reduce actual capital (which is not incorporated here). Note that European insurers are required to mark assets to market under Solvency II. 11 This analysis uses bond-level holdings data for all US life insurers as of the fourth quarter of 2019, along with bond ratings (and downgrades) as of April 30. Meaningful shares of bonds held have already been downgraded across regulatory categories ($59 billion of bond holdings have been downgraded across categories, while nearly $170 billion have been downgraded at least one rating notch). Figure 5 shows corporate bond holdings broken down by recent rating actions. The analysis also considers two scenarios: a moderate scenario in which 50 percent of bonds (by value) one notch away from regulatory thresholds are downgraded into the next 11 For levered balance sheets, marking assets to market has an amplified impact on equity. For example, suppose that fixed-income with observable market prices accounts for 70 percent of assets, with equity financing 10 percent of assets. Even a 5 percent reduction in the value of the fixed-income assets then reduces equity by one-third. IMF | Research |6

category, along with 25 percent of bonds two notches away; and a severe scenario with double these downgrade rates. US capital requirements are a nonlinear function of several components, one of which moves linearly with the ratings-based composition of bond holdings. This analysis estimates a lower bound for the impact on total capital requirements based on Kirti and Sarin (2020). FIGURE 5. US Life Insurer Bond Holdings by Recent Rating Actions Sources: S&P Global Market Intelligence; and IMF staff analysis. Note: This figure shows the dollar value of corporate bond holdings by recent rating actions. Rerated refers to bonds which have been rerated by at least one of Fitch, Moody’s, or S&P in 2020. Downgraded bonds are broken down by whether they remain in the same National Association of Insurance Commissioners risk category. Figure 6 shows how risk-based capital (RBC) ratios (the ratio of actual capital held to required capital) would be affected under different scenarios. US insurers must submit corrective action plans if their RBC ratio is below 150 percent and has a negative trend, or breaches 100 percent, and can be placed under regulatory control if their RBC ratio falls below 50 percent. 12 Regulators view excess capitalization beyond these minimum thresholds as “desirable in the business of insurance” (see the NAIC’s Model RBC Law). The median RBC ratio is above 400 percent, with some insurers already below 200 percent. The severe downgrade scenario would significantly lower RBC ratios and bring some insurers close to company action thresholds. FIGURE 6. Impact of Potential Bond Downgrades on US Life Insurer RBC Ratios Sources: S&P Global Market Intelligence; and IMF staff analysis. Note: This figure shows the distribution of RBC ratios for (1) the current level (as reported in 2019), (2) the actual level (accounting for actual downgrades to date), (3) the moderate scenario (half of 1-rating-notch-above and quarter of 2-rating-notches-above corporate bonds are downgraded), and (4) the severe scenario (all of 1-rating-notch-above and half of 2-rating-notches-above corporate bonds are downgraded). The RBC ratio is total adjusted capital divided by two 12 These thresholds apply to an RBC ratio defined as total adjusted capital (TAC) divided by company action level (CAL) RBC. CAL RBC is two times authorized control level (ACL) RBC. IMF | Research |7

times authorized control level (required) capital. The figure is restricted to insurers with assets of more than $5 billion. Observations outside the 10th and 90th

percentiles are not shown.

Joint Impact of Pandemic and Downgrades

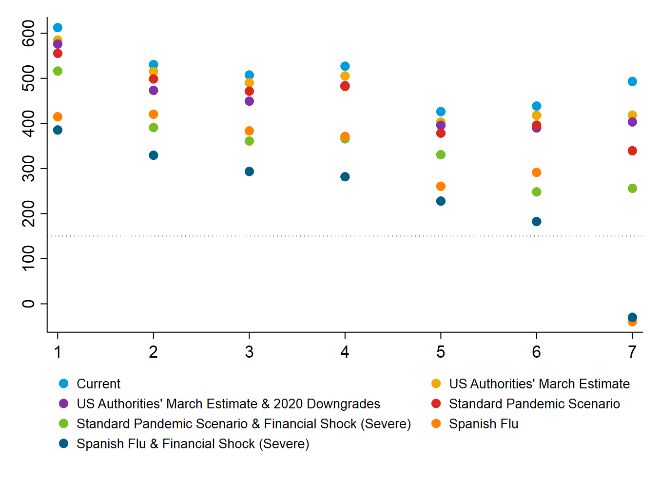

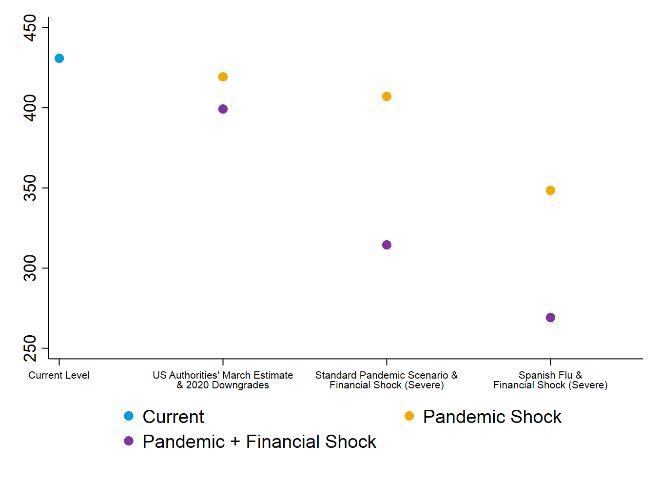

Figure 7 illustrates the joint impact of the health and financial shocks. Given the level of uncertainty surrounding

the impact of the pandemic a range of scenarios should be considered. Panel A shows an indicative aggregate

RBC ratio in three increasingly severe scenarios in addition to the current level: (1) the upper end of a mortality

scenario presented by US authorities in late March (240,000 deaths) along with rating downgrades as of April

30; (2) deaths in a standard pandemic stress test scenario (1.5 excess deaths per 1,000, or about 500,000

deaths) combined with the severe financial shock scenario; and (3) deaths in line with Spanish flu (using excess

deaths in the US reported by Barro, Ursúa, and Weng 2020) combined with the severe financial shock scenario

(1.7 million deaths).

Panel B shows the impact for the largest US life insurers by net life insurance in force for the same set of

scenarios. Under severe joint shock scenarios, capital levels for large insurers would approach, and in the case

of one insurer breach, regulatory thresholds.

FIGURE 7. Joint Impact of Health and Financial Shock on US Life Insurer RBC Ratios

A. Aggregate B. Large life insurers

Sources: S&P Global Market Intelligence; and IMF staff analysis.

Note: Panel A shows the current aggregate risk-based capital (RBC) ratio and the joint impact under three scenarios: (1) US authorities’ upper end March

estimate of 240,000 deaths combined with the actual downgrades in 2020; (2) excess deaths of 1.5 per 1,000 as in a standard pandemic stress test scenario;

(3) excess deaths of 5.2 per 1,000 as experienced in the United States during the Spanish flu (Barro, Ursúa, and Weng 2020) combined with the severe

financial shock scenario. For each scenario, age-group-specific case fatality rates in Korea are used to convert excess deaths to the share of population

infected, assuming infection rates are constant across age groups. The share of population that would need to be affected to reach these scenarios is roughly 4

percent, 8.5 percent, and 29 percent, respectively. Panel B shows RBC ratios for the largest life insurers by net life insurance in force with assets of more than

$50 billion for the same scenarios. The RBC ratio is total adjusted capital divided by two times authorized control level (required) capital.

Risk appetite may be curtailed well before capital reaches regulatory thresholds (Keeley 1990, Kirti 2019).

Insurers rely on strong financial strength ratings to attract new business. In normal market conditions, RBC

ratios below 300 percent are associated with drastically lower ratings (Figure 8).

IMF | Research |8

FIGURE 8. Interquartile Range of RBC Ratios for US Life Insurers by AM Best Rating Sources: S&P Global Market Intelligence; and IMF staff analysis. Note: Risk-based capital (RBC) ratios for this figure are capped at 600 percent. The RBC ratio is total adjusted capital divided by two times authorized control level (required) capital. V. IMPACT ON GLOBAL REINSURERS Two large global reinsurers, Swiss Re and Munich Re, disclosed expected losses in a “1-in-200-year” pandemic scenario (typically associated with the standard 1.5 excess deaths per 1,000 scenario) in annual reports covering 2019. Both report a global pandemic to be a central risk. Figure 9 shows that the impact as a fraction of current capital held could be large if a substantial share of the population is affected, assuming the impact scales linearly, with no re-pricing or reduction of exposure to mortality risk. 13 FIGURE 9. Impact of Potential Mortality Claims on Large Reinsurers’ Regulatory Capital (Percent of Current Level) Sources: Company annual reports; and IMF staff analysis. Note: These figures show the level of regulatory capital as a function of the share of population infected. Swiss Re and Munich Re reported a potential loss of $3.1 billion and €1.4 billion, respectively, in a 1-in-200-year pandemic scenario. These estimates, which are assumed to have been calculated based on 1.5 excess deaths per 1,000, are linearly scaled as a function of the share of population infected under two flat case fatality rates in Italy and Korea. 13 This simplifying assumption ignores the presence of reinsurance contracts that cap reinsurer exposure (overestimating the impact on reinsurers) or only apply for sufficiently large losses on covered policies (underestimating the impact on reinsurers). IMF | Research |9

VI. KEY TAKEAWAYS

COVID-19 could have meaningful impact on insurers due to extensive financial dislocations across asset

classes and in, an extreme scenario, potentially large increases in morbidity and mortality. Life insurers with

high exposures to morbidity and mortality could be hit particularly hard if the pandemic proves difficult to control.

Mortality rates in severe scenarios could trigger large payouts relative to capital. Widespread asset-rating

downgrades and persistently low interest rates would add to the difficult environment. Financial stability

assessments should therefore examine the implications of the pandemic for insurers. In a scenario with

widespread bond rating downgrades, regulators should closely monitor and, as appropriate after all supervisory

measures have been taken, reassess linkages to rating actions within supervisory frameworks, while enhancing

supervision for insurers with risky holdings. Authorities looking to preserve credit supply should account for

changes in insurer risk appetite.

REFERENCES

Barro, R. J., J. F. Ursúa, and J. Weng. 2020. “The Coronavirus and the Great Influenza Pandemic: Lessons from the “Spanish Flu” for the

Coronavirus’s Potential Effects on Mortality and Economic Activity.” NBER Working Paper No. 26866, National Bureau of

Economic Research, Cambridge, MA.

Becker, B., and Ivashina, V. 2015. “Reaching for Yield in the Bond Market.” The Journal of Finance 70 (5): 1863–902.

Becker, B., M. Opp, and F. Saidi. 2020. “Regulatory Forbearance in the US Insurance Industry: The Effects of Eliminating Capital

Requirements.” CEPR Discussion Paper No. DP14373, Centre for Economic Policy Research, London.

Chodorow-Reich, G., A. Ghent, and V. Haddad. 2020. “Asset Insulators.”

Domanski, D., H. S. Shin, and V. Sushko. 2017. “The Hunt for Duration: Not Waving But Drowning?” IMF Economic Review 65 (1): 113–53.

Ellul, A., C. Jotikasthira, and C. T. Lundblad. 2011. “Regulatory Pressure and Fire Sales in the Corporate Bond Market.” Journal of Financial

Economics 101 (3): 596–620.

Ellul, A., C. Jotikasthira, C. T. Lundblad, and Y. Wang. 2015. “Is Historical Cost Accounting a Panacea? Market Stress, Incentive Distortions,

And Gains Trading.” The Journal of Finance 70 (6): 2489–538.

Financial Stability Board (FSB). 2020. Global Monitoring Report on Non-Bank Financial Intermediation 2019. Basel.

Foley-Fisher, N., B. Narajabad, and S. Verani. 2019. “Assessing the Size of the Risks Posed by Life Insurers’ Nontraditional Liabilities.”

FEDS Notes. Board of Governors of the Federal Reserve System, Washington, DC, May 21.

Froot, K.A. 2001. “The Market for Catastrophe Risk: A Clinical Examination.” Journal of Financial Economics 60 (2-3): 529–71.

Hanley, K. W., and S. S. Nikolova. 2020. “Rethinking the Use of Credit Ratings in Capital Regulations: Evidence from the Insurance

Industry.” Review of Corporate Finance Studies, forthcoming.

International Association of Insurance Supervisors (IAIS). 2019. Holistic Framework for Systemic Risk in the Insurance Sector. Basel.

International Monetary Fund (IMF). 2015. “United States, Financial Sector Assessment Program, Stress Testing—Technical Note.” IMF

Country Report 15/173. Washington, DC.

Keeley, M.C. 1990. “Deposit Insurance, Risk, and Market Power in Banking.” The American Economic Review 80 (5): 1183–200.

Kirti, D. 2019. “When Gambling for Resurrection is Too Risky.” IMF Working Paper 17/180, International Monetary Fund, Washington, DC.

Kirti, D., and N. Sarin. 2020. “Private Equity Value Creation in Finance: Evidence from Life Insurance.” Institute for Law & Economics

Research Paper 20-17, University of Pennsylvania, Philadelphia.

Koijen, R.S., and M. Yogo. 2016. “Shadow Insurance.” Econometrica 84 (3): 1265–87.

———. 2020. “The Fragility of Market Risk Insurance.” Becker Friedman Institute Working Paper No. 2018-09, University of Chicago,

Chicago.

Koijen, R. S., F. Koulischer, B. Nguyen, and M. Yogo. 2020. “Inspecting the Mechanism of Quantitative Easing in the Euro Area.” Becker

Friedman Institute for Economics Working Paper No. 2019-100, University of Chicago, Chicago.

IMF | Research | 10Paulson, A., T. Plestis, R. Rosen, R. McMenamin, and Z. Mohey‐Deen. 2014. “Assessing the Vulnerability of the US Life Insurance

Industry.” In Modernizing Insurance Regulation 61–83, Hoboken, NJ: John Wiley & Sons.

Society of Actuaries (SOA). 2007. “Potential Impact of Pandemic Influenza on the U.S. Life Insurance Industry.” Research Projects—Life

Insurance, Schaumburg, IL.

———. 2020. “Impact of COVID-19.” Society of Actuaries Research Brief. Schaumburg, IL.

IMF | Research | 11You can also read