Investor Presentation | March 2016 - Hannon Armstrong

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Presentation | March 2016

Forward Looking Statements

2

Some of the information contained herein are forward-looking statements and within the meaning of Section 27A of the Securities

Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. When used herein, words such as

"believe," "expect," "anticipate," "estimate," "plan," "continue," "intend," "should," "may," "target," or similar expressions, are intended

to identify such forward-looking statements. Forward-looking statements are subject to significant risks and uncertainties. Investors are

cautioned against placing undue reliance on such statements. Actual results may differ materially from those set forth in the forward-

looking statements. Factors that could cause actual results to differ materially from those described in the forward-looking statements

include those discussed under the caption "Risk Factors" included in our Annual Report on Form 10-K for our fiscal year ended Dec.

31, 2015, which was filed with the U.S. Securities and Exchange Commission (SEC), as well as in other reports that we file with the

SEC.

Forward-looking statements are based on beliefs, assumptions and expectations as of February 25, 2016. We project annualized

Core Earnings growth in the range of 14% to 19% per diluted share for 2016 and continued double-digit Core Earnings growth for

2017. This guidance reflects the Company's estimates of (i) yield on its existing Portfolio; (ii) yield on incremental Portfolio

investments, inclusive of the Company's existing pipeline; (iii) amount, timing, and costs of debt and equity capital to fund new

investments; and (iv) changes in costs and expenses reflective of the Company's forecasted operations. All guidance is based on

current expectations of future economic conditions, the dynamics of the markets in which it operates and the judgment of the

Company's management team. We disclaim any obligation to publicly release the results of any revisions to these forward-looking

statements reflecting new estimates, events or circumstances after the date of this presentation.

2

Hannon Armstrong: Q4 & FY 2015 Highlights

• $0.25 Core EPS for Q4 2015

3

• 12% annual Core EPS Growth to $1.04/share

• 15% increase in dividend to $0.30/share in Q4, for yield of 6.9%1

• $340 million closed in Q4 and $935 million for FY 2015

• 6.2% balance sheet yield as of 12/31/15, up from 6.0% at 9/30/15

• ~$400 million in capital raised with equity offering and new non-recourse debt in Q4 2015

• 2.1:1 leverage, up from 1.9:1

• 71% fixed rate debt target achieved Core Earnings Per Share

$1.40 $1.18 to $1.24

Target Asset Classes $1.20

$1.04

$1.00 $0.93

14-19%

Efficiency $0.80 Growth

Target

$0.60

$0.43

Wind $0.40

$0.20

Solar $-

2013A 2014A 2015A 2016E

1 Source: Bloomberg – Based on HASI closing share price of $17.28 on 2/24/16 3

Market Update – Macro Conditions

Headline Risk Near Term Impact 2016-2017 Impact

4

Re-priced several Q4 transactions, caused

• Market volatility Better economics, margins

delays, impacting Q4 CE

• Falling oil and natural gas Oil, zero Oil, zero. Natural gas affects merchant

prices Natural gas, limited pricing; we protect with preferred flips

Fixed out 71% of rates, increased Q4 interest

• Rising interest rates Stronger balance sheet

expense

• Falling interest rates Wider spreads for new business Forward yield up to 6.2%

• Stress on banks Diversified bank partners in Q4 Creates more lending opportunities

Minimal, ~10% exposure; underwrite to

• YieldCo sell-off Equity is no longer ‘cheaper’ than debt

project not the YieldCo1

October raise was timely; Increased leverage

• Closed equity markets 2016 plan requires less equity than 2015

to 2.1:1

• SCOTUS stay of the CPP Minimal Minimal; our driver is economics not policy

• Exposure to Nevada resi-solar None Resi-solar is less of a focus

• 2016 Elections None Minimal

Headline Risks taken together cause us to widen range of 2016 guidance

1 Based on transactions held by a YieldCo or intended to be dropped down to a YieldCo; Excludes residential solar portfolio 4

Increased Market Volatility Reinforces our Investment Thesis…

Distributed Solar Efficiency

Residential Commercial Industrial

Regulated Utility

Utility Scale Solar Utility Scale Wind

Power Purchase Agreement

Regulated Utility Investors

…Best Risk-Adjusted Returns are in the Senior or Preferred Position.

5

Our Strategy Stays The Same, While Our Client List Expands

Originate

Programmatic

Assets with Positive

GHG Profile

Internally managed • Sustainability Report

•

• Average Experienced Team Competitive Cost of Card

management tenure Capital • Sustainable Yield℠

is 13 years Bonds with

CarbonCount™

• Deep industry

experience since

late 1980s

Core Purpose: Generate superior risk-adjusted returns using finance to enable

GHG reducing assets to be adopted at scale.

6

Clean Energy Financing Opportunity Continues to Grow

Our Three Large Markets Are Getting Larger1 Hannon’s Financing Complements

Transaction Industry Incumbents

Size

Utility Market With PTC extension

Commercial Life Insurance

Banks Companies

With ITC extension

Wind

Solar Private

Equity

Hannon

DG Solar

Hannon

Efficiency

Retail Market

Tenor

• Flexibility in deal size and tenor

Hannon Competitive Advantages: • Low cost of capital

• Clear-eyed view of risk and return

1

7

Illustrative; not to scale

Pipeline is Strong, Giving Us More and Better Investment Choices

Pipeline on the Right Side of the Climate Change Line 1

12-Month Pipeline >$2.5 Billion… Significant GHG Reductions in Q4….

Removing

305,690

Solar Metric Tons

14%

of GHGs

reduced

annually

from Q4 ‘15 148 thousand

investments

Wind Metric Tons

Efficiency

19% >$2.5b 67%

of Coal

…and Meaningful Differences in Impact

by Asset Class and Geography

2

MT of GHG/$1,000

of Investment

1.5

…and PTC/ITC extension should 1

increase Wind and Solar Pipeline. 0.5

0

Efficiency Wind Solar

1Estimatedcarbon savings are calculated using the estimated kilowatt hours (“kWh”), gallons of fuel oil, million British thermal units (“MMBtus”) of natural gas and gallons of water

saved as appropriate, for each project. The energy savings are converted into an estimate of metric tons of CO2 equivalent emissions based upon the project’s location and the

corresponding emissions factor data from the U.S. Government and International Energy Administration. Portfolios of projects are represented on an aggregate basis. 8

Summary Financial Data

Results, Unaudited Q4 Q4 FY FY

($ in millions)

Notes

2015 2014 2015 2014

Investment income, core $ 17.9 $ 11.7 $ 62.5 $ 32.8 Grew YoY portfolio from $0.9b to $1.3b

Other Investment Revenue 2.6 3.8 10.7 15.2

Core Total Revenue 20.5 15.5 73.2 48.0 32% Increase Q4’14 to Q4’15

Investment interest expense (7.4) (5.5) (26.4) (16.7) 71% Fixed-rate debt

Core Total Revenue, net 13.1 10.0 46.8 31.3

Higher SG&A due to growth in

Other expenses, core (3.6) (2.9) (13.2) (11.0) the business

Core Earnings 9.5 7.1 33.51 20.3

Core Earnings/Share $0.25 $0.27 $1.04 $0.93 12% Core YoY EPS Growth

1 After subtracting $0.1 million of cash taxes paid

Balance Sheet Portfolio2

Quarterly Transaction Volume Fluctuates

Wind Efficiency ≈4.4%

37% 31% Yield Due to the Nature of the Assets

≈6.9% ≈6.2% ($ in millions)

Yield

Yield Other

2%

Q4 ’14 Q1 ’15 Q2 ‘15 Q3 ’15 Q4 ’15

≈8.5%

Yield Volume $375 $104 $350 $140 $340

Solar

30%

9

2 Represents forward looking unlevered return on assets yield as of December 31, 2015

Portfolio / Credit Quality1

Commercial

Commercial Non- Subtotal,

Investment Investment Debt and Real Equity Method

Government Grade Grade Estate Investments Total

($ in millions)

Financing receivables $ 401 $ 383 $ — $ 784 $ — $ 784

Financing receivables held-for-sale 60 — — 60 — 60

Investments — 16 13 29 — 29

Real estate — 156 — 156 — 156

Equity method investments — — — — 319 319

Total $ 461 $ 555 $ 13 $ 1,029 $ 319 $ 1,348

% of Debt & Real Estate portfolio 45% 54% 1% 100% N/A N/A

Average remaining balance/transaction $ 12 $ 9 $ 13 $ 10 $ 27 $ 12

Diversified Portfolio,

High Credit Quality

With Over 105 Transactions

1 See Supplemental Financial Information on Slide 14 for footnotes 10Positioned for Higher Interest Rates

Assets ($ in millions)

Financing receivables & investments $ 873 • 59% of portfolio is fixed-rate debt

investments

Real estate 156 • Remaining 41% consists of floating rate

Strong debt, equity method investments and real

Equity method investments 319 Portfolio estate

• New assets originated at current rates

Cash 43 • Asset side of B/S similar to a bond ladder

Other 79

Total Assets $ 1,470

Liabilities and Equity

• 71% Fixed debt; target is 50 – 70%

Credit facility $ 247 • 2.1 to 1 Leverage; target is 2.5 to 1

Conservative • 25 bps increase in LIBOR would increase

Nonrecourse debt 563 Leverage quarterly interest expense by $0.2

million, or less than $0.01 per share

Other nonrecourse debt 101

Other 127

Total Liabilities 1,038

Total Equity 432 • Hannon Employees: ≈6%

High Quality • Institutional Ownership: >70%

Total Liabilities and Equity $ 1,470 Shareholders1 • Public Float: ≈94%

On average over the last three years, approximately 80% of dividends treated as return of capital

due to available tax attributes

1 Bloomberg data as of 2/25/16; Management calculations 11Capitalization Strategy

• Diversify lenders and expand both on balance sheet and off balance sheet financing

• Maintain fixed rate range of 50% to 70% and leverage target of 2.5 to 1

• Raise additional equity, when required, 20161

through ATM and follow-ons

20151

Fixed-Rate Debt

Fixed-Rate Debt

$650m Total

20141

BAML Facility

Fixed-Rate Debt $1.5b Capacity

BAML Facility

20131 $320m Total

$1.5b Capacity

Equity

Fixed-Rate Debt Potential 2016 issuance

$260m Total BAML Facility

$1.35b Capacity

BAML Facility

$700m Capacity

Equity Equity

$478m total $478m total

Equity

Equity $296m total

$167m Raised at IPO

1

12

Illustrative; not to scaleHannon Armstrong: Different by Design

• Long-term cash flows provide stable dividend

Yield • Preferred returns minimize commodity, resource variability

• Over 105 Investments

Portfolio • Multiple customer segments and technologies

Good • Industry leader in environmental disclosure

Governance • Internally managed, LTIP aligned with shareholders

13Supplemental Financial Data

EXPLANATORY NOTES

Non-GAAP Financial Measures

Core Earnings

Core Total Revenue, Core Total Investment Revenue, net of investment interest expense and provision, Core Other Expenses, net and Core Earnings ("Core Financial Metrics") are non-GAAP financial measures. Core Total Revenue reflects the wind equity investments

adjusted to an effective interest method and the-add back of non-cash real estate intangible amortization and the provision for credit losses, if any.

Our equity method investments in the wind projects are structured using typical wind partnership "flip" structures where we, along with other institutional investors, if any, receive a pre-negotiated preferred return consisting of priority distributions from the project cash

flows along with tax attributes. Once this preferred return is achieved, the partnership flips and the wind energy company, which operates the project, receives the majority of the cash flows through its equity interests with the institutional investors retaining an ongoing

residual interest. Given this structure, we negotiated our purchase price of our wind investments based on our assessment of the expected cash flows from each investment discounted back to net present value based on a discount rate that represented an expected yield

on the investment. This is similar to how we value the expected cash flows in financing receivables. Under U.S. GAAP, we are required to account for these investments utilizing the hypothetical liquidation at book value method ("HLBV"), in which we recognize income or

loss based on the change in the amount each partner would receive if the assets were liquidated at book value, in this case, at the end of the immediately preceding quarter after adjusting for any distributions or contributions made during such quarter. As HLBV

incorporates non-cash items, such as depreciation, and because we are entitled to receive a preferred return of cash flows on our investments independent of how profits and losses are allocated, the HLBV allocation does not, in our opinion, reflect the economics of our

investments. As a result, and in an attempt to treat these investments in a manner similar to our other investments and our initial valuation, in calculating our Core Total Revenue for the above periods, we adjusted the income we receive from these investments as if we

were recognizing income or loss based on an effective interest methodology. Generally, under this methodology income is recognized over the life of the asset using a constant effective yield. The initial constant effective yield we selected is equal to the discount rates

we used in making our investment decisions. On at least a quarterly basis, we will review and, if appropriate, adjust the discount rates and the income or loss we receive from these investments for purposes of calculating our Core Total Revenue in future periods, as

necessary, to reflect changes in both actual cash flows received and our estimates of the future cash flows from the projects. Our allocation of profits and losses is projected to change in 2019 in our transactions with JPMorgan Chase & Co. ("JPMorgan"), which is

expected to result in an increase of the amount of HLBV profits or losses allocated to us. In June 2015, JPMorgan and one of the project holding companies entered into an agreement regarding the treatment of certain tax matters that had the impact of reducing our

expected future cash flows from that holding company. As a result of this agreement, JPMorgan paid us approximately $3 million, which effectively reduced our investment in that entity. In accordance with the methodology described above, we have calculated a new

constant effective yield based upon the reduced investment amount and the reduction in expected future cash flows. We used this new effective yield, which is not materially different from our initial constant effective yield, beginning with the quarter ended September

30, 2015.

We have borrowed approximately $234 million on a nonrecourse basis using our equity method investments as collateral. Included in our U.S. GAAP investment interest expense for the year ended December 31, 2015, was approximately $7 million of interest

expense related to these nonrecourse loans. For the year ended December 31, 2015, we collected cash distributions from our wind investments of approximately $25 million (in addition to the $3 million payment), of which $13 million represents our Core Earnings

adjustment for these investments based upon the effective yield methodology discussed above.

Core Other Expenses, net reflects the add back of non-cash equity-based compensation, amortization of intangible assets, GAAP HLBV income or loss on our equity method investments, and business acquisition costs, if any. Core Earnings represent earnings utilizing the

adjustments for Core Total Revenue and Core Other Expenses, net and adjusting for any non-cash taxes and the minority interest. Our Core Financial Metrics are also adjusted to exclude one-time events pursuant to changes in GAAP and certain other non-cash charges,

if any, as approved by a majority of our independent directors.

We believe that the Core Financial Metrics provide additional measures of our core operating performance by eliminating the impact of certain non-cash income and expenses and facilitating a comparison of our financial results to those of other comparable REITs with

fewer or no non-cash charges and a comparison of our operating results from period to period. Our management uses Core Financial Metrics in this way. We believe that our investors also use our Core Financial Metrics or a comparable supplemental performance

measure to evaluate and compare our performance to our peers, and as such, we believe that the disclosure of our Core Financial Metrics is useful to our investors.

Core Earnings does not represent cash generated from operating activities in accordance with GAAP and should not be considered as an alternative to net income (determined in accordance with GAAP), or an indication of our cash flows from operating activities

(determined in accordance with GAAP), a measure of our liquidity or an indication of funds available to fund our cash needs, including our ability to make cash distributions. In addition, our methodology for calculating our Core Financial Metrics may differ from the

methodologies employed by other REITs to calculate the same or similar supplemental performance measures, and accordingly, our reported Core Earnings may not be comparable to the Core Earnings reported by other REITs.

Portfolio/Credit Quality Footnotes

• “Government” – Transactions where the ultimate obligor is the U.S. federal government or state or local governments where the obligors are rated investment grade (either by an independent rating agency or based upon our internal credit analysis). This amount

includes $297 million of U.S. federal government transactions and $164 million of transactions where the ultimate obligors are state or local governments. Transactions may have guaranties of energy savings from third party service providers, the majority of

which are entities rated investment grade by an independent rating agency.

• “Commercial Investment Grade” – Transactions where the projects or the ultimate obligors are commercial entities, including institutions such as hospitals or universities, that have been rated investment grade (either by an independent rating agency or based on

our internal credit analysis). Of this total, $12 million of the transactions have been rated investment grade by an independent rating agency. Commercial investment grade financing receivables include $175 million of internally rated residential solar loans

where the cash flows which support our financing receivables are subordinated to the tax equity investors (whose return is largely derived from the renewable energy tax incentives) and for which we rely on certain tax related indemnities of the publicly traded

residential solar provider.

• “Commercial Non-Investment Grade” – Transactions where the projects or the ultimate obligors are commercial entities, including institutions such as hospitals or universities, that have ratings below investment grade (either by an independent rating agency or using

our internal credit analysis).

• “Equity Method Investment” – Consists of minority ownership interest in operating wind projects in which we earn a preferred return.

• “Real Estate” - Includes the real estate and the lease intangible assets through which we receive scheduled lease payments, typically under long-term triple net lease agreements.

• “Average Remaining Balance” – Excludes 77 transactions each with outstanding balances that are less than $1 million and that in the aggregate total $26 million.

May 2013 14 14Core Earnings

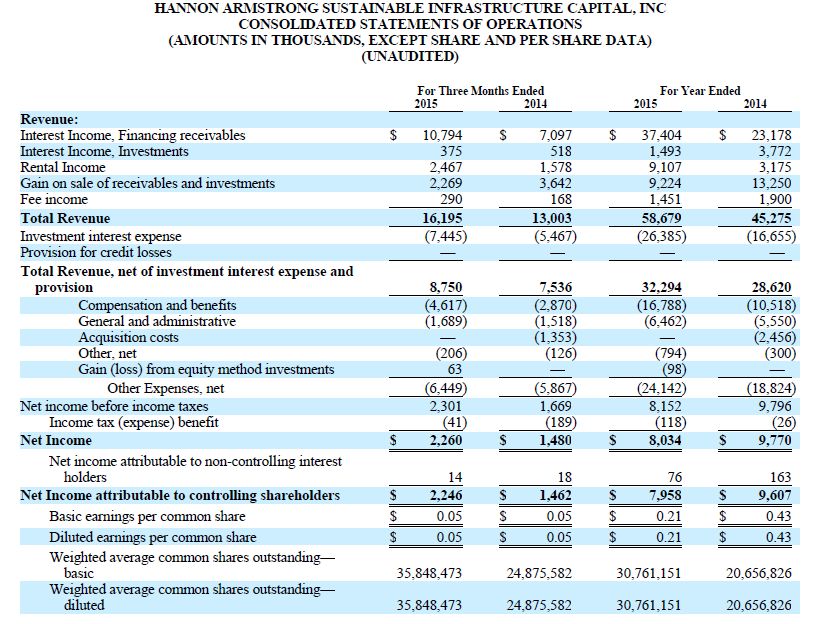

We calculated our Core Earnings and provided a reconciliation of our net income to Core Earnings for the three months and yea

ended December 31, 2015 and 2014, respectively, in the table below:

15Core Adjustments

The table below provides a reconciliation of the GAAP Total Revenue, to Core Total Revenue:

The table below provides a reconciliation of the GAAP Other Expenses, net to Core Other Expenses, net:

16Income Statement

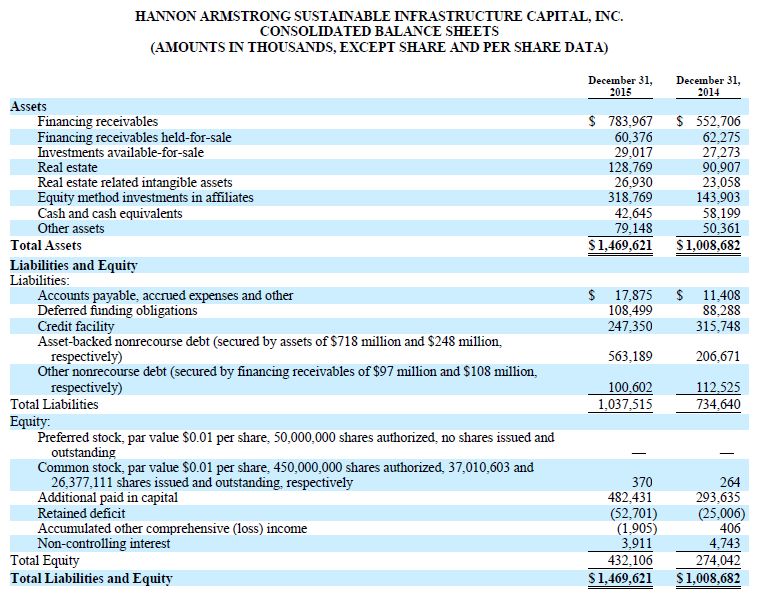

17Balance Sheet

18Energy Efficiency Project Examples

Federal Facilities in the Mid-West $16.7 8,978 Metric Tons

Million Annual Reduction in

14 different energy efficiency CO2 Emissions

improvements implemented in 44

buildings across two federal facilities in

the mid-western U.S.

Mid-Atlantic Public School System $25.0 7,410 Metric Tons

Million Annual Reduction in

17 energy efficiency improvements, CO2 Emissions

including lighting, energy management

systems and HVAC upgrades implemented

in 29 mid-atlantic public schools

V.A. Medical Center $7.7 1,500 Metric Tons

Million Annual Reduction in

6 energy efficiency improvements CO2 Emissions

including, chiller plant upgrades, lighting

upgrades, window film installation, and

steam distribution upgrades at a V.A.

Medical Center in California

19Renewable Energy Project Examples

Residential Solar Leases $86.5 19,459 Metric Tons

Million Annual Reduction in

Hannon Armstrong provided non-recourse CO2 Emissions

debt to SunPower to help finance its

residential solar lease program

Wind Equity Investment $144 87,831 Metric Tons

Million Annual Reduction in

Wind investment covers 10 projects, in CO2 Emissions

five states, representing over 1,200

megawatts (MW) of gross generating

capacity

Solar Land Investment $12.0 1,343 Metric Tons

Million Annual Reduction in

Hannon Armstrong acquires land under CO2 Emissions

60 megawatt solar farm owned by First

Solar in Fresno County, CA. Electrical

output to be sold to Pacific Gas & Electric

under a 20-year Power Purchase

Agreement

20For more information, please visit our website at

www.hannonarmstrong.com

Or contact Investor Relations directly at

410-571-6189

investors@hannonarmstrong.com

Securities are offered by Hannon Armstrong Securities, LLC, a registered broker dealer, member FINRA and SIPC and subsidiary of Hannon Armstrong Sustainable Infrastructure Capital, Inc. 21You can also read