Investor Update 2017 2016 - 2020 Value & Resilience - Repsol

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Update 2017

2016 – 2020 Value & Resilience

©

Disclaimer ALL RIGHTS ARE RESERVED © REPSOL, S.A. 2017 Repsol, S.A. is the exclusive owner of this document. No part of this document may be reproduced (including photocopying), stored, duplicated, copied, distributed or introduced into a retrieval system of any nature or transmitted in any form or by any means without the prior written permission of Repsol, S.A. This document does not constitute an offer or invitation to purchase or subscribe shares, in accordance with the provisions of the Royal Legislative Decree 4/2015 of the 23rd of October approving the recast text of the law on the securities market and its implementing regulations. In addition, this document does not constitute an offer of purchase, sale or exchange, nor a request for an offer of purchase, sale or exchange of securities in any other jurisdiction. This document mentions resources which do not constitute proved reserves and will be recognized as such when they comply with the formal conditions required by the system “SPE/WPC/AAPG/SPEE Petroleum Resources Management System” (SPE-PRMS) (SPE – Society of Pretroleum Engineers). This document contains statements that Repsol believes constitute forward-looking statements which may include statements regarding the intent, belief, or current expectations of Repsol and its management, including statements with respect to trends affecting Repsol’s financial condition, financial ratios, results of operations, business, strategy, geographic concentration, production volume and reserves, capital expenditures, costs savings, investments and dividend payout policies. These forward-looking statements may also include assumptions regarding future economic and other conditions, such as future crude oil and other prices, refining and marketing margins and exchange rates and are generally identified by the words “expects”, “anticipates”, “forecasts”, “believes”, estimates”, “notices” and similar expressions. These statements are not guarantees of future performance, prices, margins, exchange rates or other events and are subject to material risks, uncertainties, changes and other factors which may be beyond Repsol’s control or may be difficult to predict. Within those risks are those factors and circumstances described in the filings made by Repsol and its affiliates with the Comisión Nacional del Mercado de Valores in Spain and with any other supervisory authority of those markets where the securities issued by Repsol and/or its affiliates are listed. This document mentions resources which do not constitut e proved reserves and will be recognized as such when they comply with the formal conditions required by the system “SPE/WPC/AAPG/SPEE Petroleum Resources Management System” (SPE-PRMS) (SPE – Society of Pretroleum Engineers). Repsol does not undertake to publicly update or revise these forward-looking statements even if experience or future changes make it clear that the projected performance, conditions or events expressed or implied therein will not be realized. In October 2015, the European Securities Markets Authority (ESMA) published the Guidelines on Alternative Performance Measures (APM), of mandatory application for the regulated information to be published from 3 July 2016. Information and disclosures related to APM used on the present document are included in Appendix I “Alternative Performance Measures” of the Management Report for the full year 2016. ©. 2

2016-2020

Value & Resilience

1. Company overview and strategy

2. Upstream

3. Downstream

4. Gas Natural Fenosa

5. Financing

6. 2017 Outlook

3

3

Company overview

and strategy 1

4

4

Key messages 9M 2017

Company overview and strategy

Continued delivery on strategic objectives

Bn€ ~6.5 ~6.5 (X) 1.1 ~1.1

4.8

Strong EBITDA CCS generation Net Debt/EBITDA in line with projections

(1)

Upstream Downstream

Kboe/d 685-690 USD/Bbl 6.8

~680 6.4

688

Production volumes in line with guidance Refining margin indicator in line with

expectations

2017 Budget 9M17 actual 2017 guidance

(1) Refinining Margin Indicator 5

Key messages Q3 2017

Company overview and strategy

Upstream

Production: Exploration program:

Q3 17 = 693Kboe/d 3% increase YoY 3 exploratory wells completed (1 positive)

Libya ~25 Kboe/d in the quarter As of 30th Sept. 8 exploratory and 1 appraisal in progress

Startup of Juniper (T&T), ramp up of Flyndre and MonArb in 2017 program: 17 wells (15 exploratory & 2 appraisal)

the UK and Lapa and Sapinhoa in Brazil

Downstream

Refining: Petrochemicals:

Strong perfomance EBIT ~180M€ in line with record

Refining margin indicator 7.0 USD/Bbl in Q3 17 levels in early 2016

Planned maintainance for the year completed in 1H17: Marketing:

Higher volumes and margins in Service Stations

3Q17 Utilization of the distillation units = 99%

FCF:

3Q17 Utilization of the conversion units = 104% Generation above 2 Bn€

Corporate and others

Synergies and efficiencies: Corporation:

2017 target €2.1 Bn Q3 17 Net debt €6,972 Mn€

(1)

Accelerated delivery of 2018 target Net Debt / EBITDA (x) = 1.1

Capex: Objective Credit rating BBB stable

~3 Bn€ without impacting production volumes

(1) Estimated FY 2017 6

Through the value chain and across the globe

Company overview and strategy

Upstream main Both

projects

Our shareholders

Core businesses:

Upstream and

Downstream

~700 kboepd ~1 Million bpd refining

production capacity

~2.4 billion boe

20% stake in GNF

proved reserves (*)

(*) As at 31/12/2016 7

2016 - A year of strategic progress

Company overview and strategy

Group FCF breakeven Divestments

$/Bbl ~50 • 10% stake in GNF € 1.9 Bn

~42

̴ 60 • Piped LPG € 0.7 Bn

Target ~40

̴ 43 • Tangguh € 0.3 Bn

• TSP € 0.1 Bn

• Others (eg: LPG Ecuador and Peru) € 0.6 Bn

TOTAL CASH RECEIVED € 3.6 Bn

Net Debt Key Metrics

€Bn 2015 2016

14.00

€11.9 Bn EBITDA CCS (Bn€) 5.1 5.0

11.00

Brent price ($/Bbl) 52.4 43.7

€8.1 Bn

8.00

€ 3.8 Bn HH ($/MBtu)

Refining margin

2.7 2.5

5.00

Indicator($/Bbl) 8.5 6.3

2.00 Exchange rate ($/€) 1.11 1.11

2015 1Q16 2Q16 3Q16 4Q16 8

2016 to 2020: Value and Resilience

Company overview and strategy

Challenge: a volatile, uncertain and complex environment

Strategic Plan 2016-2020 Long term value capture

Portfolio

Value • Keep financial and operating

Management

discipline: synergies and efficiencies

• Shift from growth to value

• Capex flexibility delivery • Consolidate and extract the current

• Portfolio rationalization • Competitive and sustainable value of our assets

shareholder remuneration

• Manage portfolio to capture maximum

value

Efficiency Resilience

• Review of projects with a long-term

• Integrated model pay back

• Synergies and • Self-financing strategy even

company-wide in a stress scenario • Be ready to diversify/adapt traditional

Efficiency Program • FCF breakeven reduction businesses

Transformation Program

9

Delivery on commitments

Company overview and strategy

COMMITMENT 2016&2017 DELIVERY

0.3B€ impact in 2018 In 2016 0.3B€ already achieved

Synergies

New target of 0.4B€

Efficiencies (Opex & Capex)

IMPLEMENTATION

0.8B€ in 2016; 1.8B€ in 2018 2016: 1,3B€; 2017 1.8B€

Capex flexibility ̴3.9 B€ average per annum 2016: 3.2B€; 2017 3.0B€

3.1B€ by 2017 (*)

Portfolio Management Already divested 5.1 B€

6.2B€ by 2020

(**)

Reduce FCF Breakeven $40 /Bbl Brent ~$42/Bbl Brent targeting $40/Bbl

Financial strength Maintain investment grade BBB stable rating achieved

Ahead of plan On target

(*) It includes cash proceeds and benefits (**) Organinc breakeven (divestments not included) 10Efficiencies and Synergies Update

Company overview and strategy

Pre-tax cash savings

COMMITMENT DELIVERY ESTIMATED

// 2016 BUDGET // // 2016 // // 2017 //

Synergies €0.2 B €0.3 B €0.3 B

Upstream Opex &

Capex efficiency €0.6 B €0.8 B €1.2 B

Downstream

profit improvement €0.2 B €0.3 B €0.4 B

and efficiency

Corporation right-

sizing

€0.1 B €0.2 B €0.2 B

€1.1 B €1.6 B €2.1 B

2018 target accelerated into 2017

11Resilience in the lower part of the cycle

Company overview and strategy

2015 2016

Upstream 2015 2016 2015 2016

Brent price ($/Bbl) 52.4 43.7 Refining margin

Break (*)

Even($/Bbl)

̴ 94 ̴ 61 Indicator ($/Bbl) 8.5 6.3

HH ($/MBtu) 2.7 2.5

EBITDA CCS (Billion €) 5.1

5.0

2016 • Upstream: Lower cash

3.8

2015 breakeven.

3.2

• Downstream: Strong

2.1 integrated margin.

1.6

• Group FCF breakeven

after dividend and

> -0.3 -0.2 interest reduced to

$42/Bbl.

Corporate &

Upstream Downstream

Others Repsol

12

(*) Includes Talisman Energy Inc. figures since 8th of May 2015. Excludes any 2015 Upstream disposal.Portfolio management

Company overview and strategy

Completed

10 % Stake GNF Piped LPG Alaska dilution

Eagle Ford-Gudrun 10 % Stake CLH UK wind power

LPG Peru & Ecuador Exploratory licences Canada Brynhild Norway

….Latest transactions

Tangguh Ogan Komering

TSP

TOTAL DIVESTED 5.1 B€13Self-financed SP 2016-2020 - 40% net cash delivered

Company overview and strategy

Cash movements 2016-2020 (*) Sensitivities 5 years accumulated

2016 3.8 -0.3 3.6 -3.2 4.0 Adj. Net

Contribution Bn€ FCF Income

1.5 1.3

Bn€ Brent +/- $5/bbl

~6 ~21

-1.5 -1.3

~29 ~4

Adj. Net

Bn€ FCF Income

0.8 0.6

HH +/- $0.5/MBtu

-0.8 -0.6

~10

Adj. Net

Bn€ FCF Income

Refining marging 0.8 1.1

+/- $1/bbl

-0.9 -1.1

Cash for

Operating cash Financial

Divestments Investments dividend and

flow post tax expenses

debt

(*) Stress price scenario considered: Brent ($/Bbl) 2016: 40; 2017: 40; 2018: 50; 2019: 50; 2020: 50; HH ($/MBtu) 2016: 2.6; 2017:2.6; 2018-2019-2020:3.5

Note 1: This figure does not consider non-cash debt movements such as exchange rate effect and other effects 14UPSTREAM 2

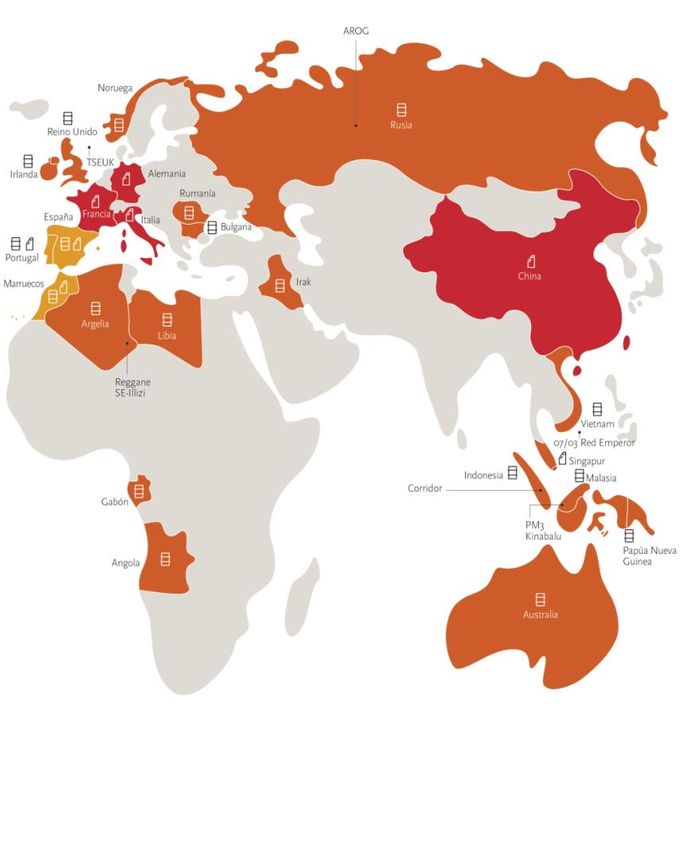

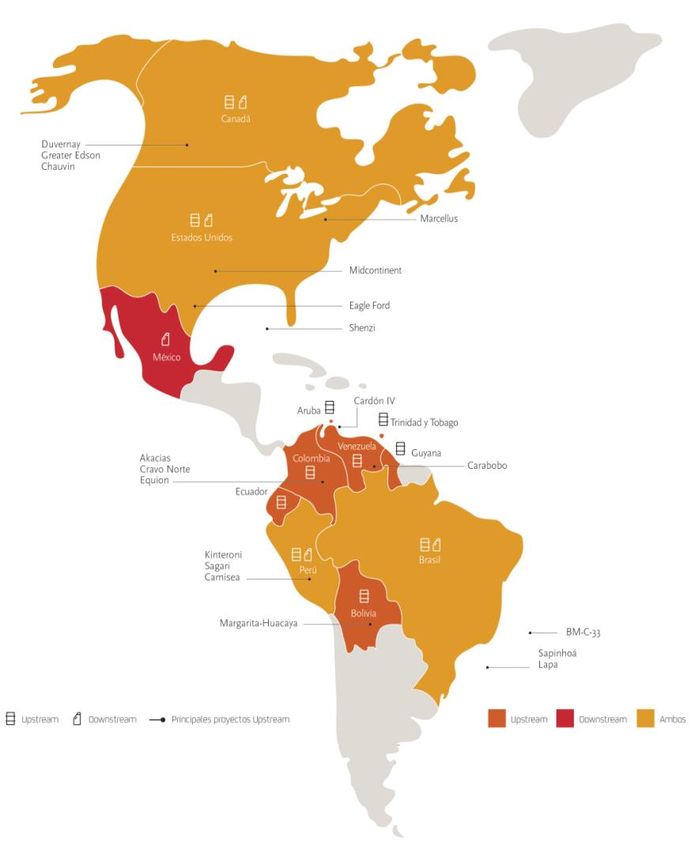

153 core regions in the portfolio

Upstream

North America: Growth

Production 2016: ~182 kboepd

Operatorship: ~79%

SouthEast Asia: FCF & Growth

Gas production (2016): 71% Production 2016: ~98 kboepd

• Unconventional portfolio Operatorship: ~37%

• Operatorship Gas production (2016): 77%

• Valuable midstream positions • Self-financed growth

• Relationship with governments/NOCs

Latin America: FCF • High potential exploration blocks

Production 2016: ~302 kboepd

Operatorship: ~20%

Gas production (2016): 70%

• Regional scale

• Exploration track record

• Cultural fit

2016 2017E

(*)

NOTE: Europe, Africa & Brazil:

Production (Kboepd) 690 685-690

Production 2016 ~ 108 kboepd

1P Reserves (Mboe) 2,382

(**) (***)

(*) Post disposals of ̴17 Kboepd from TSP and Tangguh in 2016 RRR (%) 124 ̴100

(**) Organic (***) Long term average 162016 Upstream Results

Upstream

RESERVES PRODUCTION (**)

kboepd

690

800 +23%

2015 700

2014 2016

600

+57% 559

1P Reserves (Mboe) 1,539 2,373 2,382 500

400 355

300

(*) 200

RRR (%) 118 159 124 100

0

2014 2015 2016

(*) Organic RRR (**) It includes Talisman since the 8th of May of 2015

(***)

EBITDA PROJECTS

M€

+29%

2,500

2,072 • Ramp-up Cardón IV (Venezuela)

2,000

1,611

1,500

• Ramp-up of Sapinhoá (Brazil)

1,000 • First oil of Lapa (Brazil)

500

0

• Production restarted in Libya

2015 1Q16 2Q16 3Q16 2016

(***) Cumulative 17Assets & Projects

Upstream

// Exploration //

AMERICA

GoM Contingent resources

NORTH

Duvernay Marcellus Eagle Ford

/Midcontinent

(Canada) (USA) (USA) (USA)

• Unconventional North America

WI: ~31% in basin

WI: 100% WI: ~89% and 37% in JV WI: 28%/~11% • Brazil: Campos-33, Sagitario

• Russia: Karabashky

• Colombia: CPO9 & Niscota

• Alaska: Colville High

AMERICA

Kinteroni + Akacias

LATIN

M. -Huacaya Carabobo – AEP Cardon IV • GOM: Leon and Buckskin

Sagari (Colombia)

(Bolivia) (Venezuela) (Venezuela)

(Peru) • Indonesia: Sakakemang

WI: 45%

• Vietnam: Red Emperor extension

WI: 37.5% WI: 11% WI: 50% WI: 53.8%

• Kurdistan

• PNG: GAP

Europe, Africa

MonArb / Prospective resources

& Brazil

El-Sharara Reggane Flyndre Cawdor

Sapinhoa Lapa

(Libya) (Algeria) (UK) • Brazil: Santos Basin & Espirito Santo

WI: 15% WI: 15% NC115-WI: 20% WI: 29,25%

WI: 30% • Colombia: RC11, RC12 & Tayrona

NC186-WI:16% Redevelopment • Unconventional North America

• GOM

• Peru

SOUTHEAST

• Guyana

PM3,Kinabalu C. & J. Merang Red Emperor

ASIA

(Vietnam)

• Angola

(Malaysia) (Indonesia)

• Romania

WI:35% PM3 WI: 36% C / WI: 46.8% • Portugal

WI: 60% K 25% JM

• Norway

• Indonesia

• Malaysia

• Vietnam

“As is” organic portfolio potential of more than 900 kboepd • PNG

• Bulgaria

First production 2017 Ramping up in 2017

18Capex optimization

Upstream

Organic RRR (%)

Average 2017-2020

118% 159% 124% ̴100%

Bn$

8

7

6

5

4

3

2

1

0

2014 2015 2016 2017 2018-2020

Exploration Capex Development Capex Average Capex 2018-2020

19Efficiency program: delivering our target

Upstream

~400

M€

~1,200 2017

Original

~350 Target

850 M€

2016 ~50

Original

Target (*)

~800

550 M€

2016 Savings already New Savings 2017 Savings

achieved in to be Target

2016 impacting achieved in (accelerated

in 2017 2017 from 2018)

Note: Excluding synergies

* It does not include ~ 200 M€ of one off 203 Downstream

21Sustainable cash flow generator

DOWNSTREAM

Downstream

Refining Petrochemicals

̴1 million barrels of CORUÑA All three sites are

refining capacity per BILBAO managed as a single

day. petrochemical hub

TARRAGONA

Top quartile position among Chemical sites and crackers

European peers along the cycle. strategically located to supply

Southern Europe and

La Pampilla

63 % FCC equivalent. Mediterranean markets.

PUERTOLLANO

Logistic flexibility to enhance

5 refineries optimized as a single CARTAGENA Peru

competitive feedstock imports at

operation system.

Tarragona and Sines.

Oil pipeline Repsol Oil pipelines CLH

Marketing LPG Trading and G&P

4,715 service stations One of the leading retail distributors of G&P: transportation,

throughout Spain, Portugal, Peru, LPG in the world, ranking first in Spain marketing, trading and

and Italy. and is of the leading companies in regasification of liquefied

Portugal. natural gas.

3,501 service stations in Spain → 70% have a

strong link to the company and 29% directly We distribute LPG in bottles, in bulk and

managed . Trading & Transport: trading and supply of

AutoGas.

crude oil and products

Objective to generate FCF ̴ €1.7B per annum (average 2016-2020)

222016 Downstream Results

Downstream

European Integrated Margin of R&M EBITDA CCS (*)

Industry peer group Repsol position

M€

($/Bbl)

12

4,000 3,788 3,173

10 3,400

8

6 2,800

4

2 2,200

0

-2 1,600

-4

-6 1,000

-8

2014 2015 1Q16 2Q16 3Q16 2016 400

Source: Company filings. 2015 1Q16 2Q16 3Q16 4Q16

Peers : Repsol, Cepsa, Eni, Galp, OMV, MOL, Total, PKN Orlen, Hellenic Petroleum, Saras and Neste Oil * Cumulative

FCF Integrated Model

Operating Cash

Flow €2.2Bn • Top quartile position among European

Divestments €1.2Bn peers.

Capex -€0.7Bn • Fully-invested assets

Free Cash Flow €2.7Bn

232016-2020 Downstream strategy

Downstream

Maximizing value and cash generation leveraged on fully invested assets

European Integrated Margin of R&M Average investments

Industry peer group maximum margin

Repsol position

Industry peer group minimum margin

Downstream resilience reinforced by the integration of commercial and

industrial businesses

Note: Integrated R&M margin calculated as CCS/LIFO-Adjusted operating profit from the R&M segment divided by the total volume of crude processed (excludes

petrochemicals business) of a 10-member peer group.

Based on annual reports and Repsol’s estimates. Source: Company filings.

Peer group :Repsol, Cepsa, Eni, Galp, OMV, MOL, Total, PKN Orlen, Hellenic Petroleum, Saras and Neste Oil.

24Repsol’s refining margin indicator

Downstream

$/Bbl 8

6.3 6.4

6 0.4 0.7

0.7

3.2 3.0

3.0

4

2.7

2

2.7 2.7

0

2016 Refining Margin Indicator Estimated Refining Margin

Indicator 2017-2020

Base Repsol Crack Index Additional margin from projects pre-SP Efficiency and margin improvement program

25Gas Natural

4 Fenosa

26Gas Natural Fenosa

Rationale

10% stake sold 20% remaining stake

Liquid investment provides

€1.9Bn proceeds

financial optionality

Executed with no discount to

market price at 19€/share

8.6% above GNF’s unaffected

Strong profitability

performance through

dividend stream

market price of €17.5/share 1

7.8x EV/EBITDA 2016E Strategic stake in a leading

gas & power company

above comparable trading

multiples

Window into role of gas and

renewables in energy mix

27

(1) 6 months volume weighted average share priceFINANCING 5

Financial Strategic Plan 2016-2020

Financing

Sound track record

Resilient Plan with stronger Conservative

in managing adverse

business profile financial policy

conditions

Commitment to reduce debt and maintain investment grade

The three Rating Agencies, Standard & Poor’s, Moody’s and Fitch have upgraded

and confirmed the rating BBB stable , Baa2 stable and BBB stable respectively.

Commitment to maintain shareholder compensation

in line with current company level

29Net Debt Evolution

Financing

€Bn

12 3.2 0.5

10

8

(3.8) (3.6)

6 11.9

Breakeven at $42 per barrel

4 8.1

2

0

Net Debt 31st Operating Cash Capex Dividends Paid Divestments Net Debt 31st

Dec 2015 Flow & Others Dec 2016

Targeting FCF Breakeven at $40/Bbl

30Strong liquidity position

Financing

(Billion €) (Billion €)

14

12.2

14.0

12

12.0

Term deposits w/ 10 9.8

immed.availab. ** 9.2 1.9 x

10.0

7.7

7.9

Operating 8

committed 0.2 8.0

Credit Lines

0.4 0.2

6.0

Structural 6 2.3 6.0 2.7

committed

Credit Lines

4.2

4.0

4

4.8 4.1

Cash & 2.1 2.0

4.8

Equivalents 2

2.1 2.1 2.4 0.0

1.7 1.9

1.3

0.6

Liquidity as of Short term debt

0 September 2017 September 2017 *

Liquidity as of 2017 * 2018 * 2019 2020 2021 2022 >2023

September 2017

Liquidity covers Liquidity exceeds 1.9x

long term debt maturities beyond mid 2020. short term maturities

(*) Short term debt excludes interest and derivatives € 0.16 billion.

(**) Deposits classified as financial investment in the accounting although they have an immediate availability.

31Sources of liquidity as of 30th Sep 2017

Financing

63%

(Million €)

14.0

Cash and Equivalents 4,830

12.0

Total Unused Committed Credit Lines 2,698

10.0

Term deposits w/ immediate availability (1) 200

Total Liquidity Available 8.0

7,728 0.2

Long term Short term 6.0 2.7 12.2

(Million €) Structural Operating TOTAL 4.0 7.7

Committed Credit Lines 2,327 396 2,723

2.0 4.8

85% 15% 100%

Used 0 (25) (25)

0.0

Cash and Undrawn Credit Term deposits w/ Liquidity 3Q2017 Gross debt

Available 2,327 370 2,698 equivalents Lines immed.availab. * 30 Sept 2017 **

86% 14% 100%

Available Structural credit lines

Strong liquidity position represents

represent 86% from total committed

63% gross debt

credit lines

(*) Deposits classified as financial investment in the accounting although they have an immediate availability.

(**) Gross debt excludes interests and derivatives € 0.16 million

32Delivery of Commitments

Financing

• Piped Gas Business, Offshore Wind, TSP, Tangguh

Divestments

• E&P portfolio management: Alaska, Norway

GNF monetization • Sale of 10% participation in GNF

• Repsol dividend reduction

Dividend

• Scrip dividend

Synergies and

Efficiencies

• Efficiencies and synergies accelerated

Debt reduction and • Net Debt/EBITDA of 1.1x

maintenance of IG • Rated BBB stable by the three rating agencies

Maintenance of investment grade is fundamental to our long term strategy

33Industry

Context

2017 OUTLOOK

6

34Outlook for 2017

2017 Outlook

Our assumptions

(*)

2017B 9M17 2017B 9M17

Brent price ($/Bbl) 55.0 51.8 Refining Margin ($/Bbl) 6.4 6.8

HH ($/MBtu) 3.2 3.2 Exchange rate ($/€) 1.05 1.11

Guidance

(***)

2017B 9M17 2017E 2017B 9M17

Production (KBoepd) ̴ 680 688 685-690 (**)

FCF BE ($/Bbl) ̴ 40 ̴ 40

Capex (Bn€) 3.2-3.6 1.8 ̴ 3.0

ND/EBITDA (x) 1.1 1.1

Synergies and 2.1 ̴ 1.8 2.1

Efficiencies (Bn€)

(*) Budget (**) Long term objective (***) Estimated 35Investor Update 2017

2016 – 2020 Value & Resilience

©You can also read