Digital Business Transformation - Germany 2019 Quadrant Report - T-Systems

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Digital Business A research report

Transformation comparing provider

strengths, challenges

Germany 2019 and competitive

differentiators

Quadrant

Report

November 2018

ISG Provider Lens™ Quadrant Report | November 2018 Section Name

About this Report

Information Services Group, Inc. is solely responsible for the content of this report. ISG Provider Lens™ delivers leading-edge and actionable research studies, reports

and consulting services focused on technology and service providers’ strength and

Unless otherwise cited, all content, including illustrations, research, conclusions, weaknesses and how they are positioned relative to their peers in the market. These

assertions and positions contained in this report were developed by and are the sole reports provide influential insights accessed by our large pool of advisors who are

property of Information Services Group, Inc. actively advising outsourcing deals as well as large numbers of ISG enterprise clients

who are potential outsourcers.

The research and analysis presented in this report includes research from the ISG

Provider Lens™ program, ongoing ISG Research programs, interviews with ISG advisors, For more information about our studies, please email ISGLens@isg-one.com,

briefings with services providers and analysis of publicly available market information call +49 (0) 561-50697537, or visit ISG Provider Lens™ under ISG Provider Lens™.

from multiple sources. The data collected for this report represents information that

was current as of 30.09. 2018. ISG recognizes that many mergers and acquisitions have

taken place since that time but those changes are not reflected in this report.

The lead authors for this report is Heiko Henkes, Oliver Nickels and Wolfgang Heinhaus.

The editor is Jürgen Brettel. ISG Research™ provides subscription research, advisory consulting and executive

event services focused on market trends and disruptive technologies driving change

in business computing. ISG Research™ delivers guidance that helps businesses

accelerate growth and create more value.

For more information about ISG Research™ subscriptions, please email

contact@isg-one.com, call +49 (0) 561-50697537 or visit research.isg-one.com.

2

© 2018 Information Services Group, Inc. All Rights Reserved.

1 Executive Summary

5 Introduction

21 Enabling the Digital Customer Journey

© 2018 Information Services Group, Inc. All rights reserved.

25 Digital Enterprise Operations – Large Accounts Reproduction of this publication in any form without prior

permission is strictly prohibited. Information contained in this

29 Digital Transformational Platforms (PaaS)

report is based on the best available and reliable resources.

33 Digital Transformational Services (aaS) Opinions expressed in this report reflect ISG’s judgment at the

time of this report and are subject to change without notice.

37 Blockchain as A Service

ISG has no liability for omissions, errors or completeness of

42 Methodology information in this report. ISG Research™ and ISG Provider Lens™

are trademarks of Information Services Group, Inc.

ISG Provider Lens™ Quadrant Report | November 2018 Section Name

Executive Summary

Executive

EXECUTIVE Summary

SUMMARY

While digital transformation has been one of the hottest topics of discussion among architecture and infrastructures. Digital transformation of functions includes automation,

enterprises, consultancies, research companies and academics for as long as a decade, it artificial intelligence (AI) and cognitive technologies, coupled with feedback and analytical

is inherently difficult to fully understand the scope, breadth of reach and potential impacts capabilities that can be applied in both the real world (such as production facilities,

of the digital transformation across the enterprise. Digital transformation comprises many customer contact centers, retail environments and other customer interaction points,

technological topics, business coverage areas, organizational functions and business including mobile) and in the virtual world by automating the response and interaction with

processes. And while these digital transformational areas are being analyzed, the overall clients, partners and governments.

Internet of Things (IoT) and information and communication technology (ICT)-enabled world

The following points provide a framework of key characteristics of digital services,

is increasingly evolving, which is rapidly causing exponential change.

including their differentiation from less digitalized services:

Enterprises are by necessity evaluating means to increase their competitiveness. A large

Digital transformational services combine maximum automation with autonomy,

part of this challenge is not just technological, but also has to do with how to transform

providing multi-platform compatibility.

established processes and traditional management practices. How can companies enjoy a

sufficient degree of flexibility, speed and collaboration across departments and enterprise Service delivery is based on ubiquitous communications and information networks.

boundaries, while enabling them to master their challenges so they can deliver benefits to This includes stationary and mobile networks and low-power wide-area (LPWA)

themselves and their (ever more mobile) customers? networks such as narrowband IoT (NB-IoT). The required always-on connectivity is

ensured through standardized interfaces, automated, software-defined provisioning

Enterprise agility goes far beyond software development agility to define how organizations

and capabilities that are fully based on business- and user (class)-specific SLAs.

can adjust business, development and operations work streams to survive in a constantly

changing competitive environment. This adjustment, and the speed at which it is realized, is Despite a high degree of automation, digital services provide individual variants

relevant and critical for the whole enterprise value stream. (such as efficiency prioritization, dynamic response and provisioning, automated

policy mapping, high security) that are based on an integrated service management

Digital transformation evolves through virtualization of technology and operations

approach. Performance can be adjusted based on information from the digital

while integrating the virtual and physical worlds. From the systems and IT infrastructure

customer journey (for example information gathered by cookies and movement

perspective, "virtual" refers to running on the cloud and includes software-defined

1

© 2018 Information Services Group, Inc. All Rights Reserved.

ISG Provider Lens™ Quadrant Report | November

Juni 2018 2018 Executive Summary

profiles). Service variations and improvements are location- and time-independent and networks or cloud ecosystems, are also used to automatically detect and anonymize

are performed based on preferences, user class or other influencing factors. anomalies and translate them into patterns or best practices.

Service performance can be guaranteed, independent of utilization rates and based on Self-healing mechanisms, reporting and forecasting models are used to detect and

automated and predictive system provisioning tools. contain problems and resolve them, if possible. To trace and improve forecasts or to

automate methods, results and reports are stored and shared with involved parties

Container technologies or other digital transformational architectures (such as SDN)

according to the DevOps model to improve the quality of a service.

support a large variety of infrastructure types and workload platform independence

within a software-defined operations environment. Previously separate IT areas, such The highly modular service or microservice is provisioned ad hoc and provides an API-

as servers, storage, networks or non-IT devices plus information and applications, are controlled data model that classifies and handles device and personal data, information

now managed based on an SDN approach. and applications. If necessary, management is done via command line or code and is

ensured via standardized interfaces. Graphical user interfaces (GUIs) are optional. If GUIs

Service billing is done through multiple channels (for example credit card, PayPal and

are implemented, they are available natively for the device and/or platform (framework)

similar approaches, mobile wallets and cryptocurrencies).

to ensure ease of use for inexperienced end users.

Smart contracts that are based on coded specifications and requirements and can

be used to control and check contractual relationships automatically are also gaining

Based on a maximum degree of standardization and the use of open-source technology,

services may be published in community directories such as GitHub. Services are

relevance. Depending on the contract, usage is based on rules from a variable (on-

optimized and versioned to ensure code transparency and integration into additional

demand scaling) or rigid usage agreement. The agreement always contains reserved

digital ecosystems, platforms and industry- or user-specific innovations.

instances to ensure the availability of immediate additional performance that is not

included in the contract. Blockchain is entering the field to enable such scenarios and Increasingly, a service is produced within decentralized, globally scaling ecosystems with

can be considered as a disruptive service, for automated contracts and in other areas. complementary business partners and offerings. Users of such services can become

providers, or “prosumers,” and contribute their own data or content. Ultimately,

Product-specific support is mostly personalized, based on conversational user

they become part of the value or supply chain. Chaining individual services into new

interfaces (CUIs), chatbots and natural language processing (NLP). Image recognition

(mash-up) services, based on theoretically infinite numbers of third-party services that

elements and even artificial or cognitive intelligence, based on integrated neural

can be accessed by heterogeneous and unknown customers, serves as the basis for

2

© 2018 Information Services Group, Inc. All Rights Reserved.

ISG Provider Lens™ Quadrant Report | November 2018 Executive Summary

exponential growth, innovations and the success of niche products (long-tail marketing) Market Segment “Digital Product Creation & Continuous Delivery”

and non-linear business models. This kind of business model is currently used by

It is one thing to know about the right timing in the sales process, and quite a different

hyperscale companies such as Facebook, Amazon, Apple, Netflix and Google, who are

thing to be able to deliver the required product in time and in the right quality. To align

collectively referred to as FAANG.

sales, product development and delivery teams accordingly, it is important to establish an

This is the ultimate challenge. From the business model to the portfolio and customer, innovation management that accounts for all stakeholders and their requirements, while

employee and partner relationship management – the digital transformation is challenging ensuring a maximum degree of agility. The silver bullet to build up an agile enterprise is

all certainties. Therefore, the biggest question for IT users is what kind of opportunities to involve DevOps methodologies into the whole process organization. There are not only

and risks are waiting for them on their digitization journey. And the next question is: What technical, but also business-related development issues which must be clarified accordingly,

consulting houses, service providers and IT companies can provide the support required for instance concerning the entry into non-linear business models or the modification of

in the B2B sector? ISG divides the market into five segments that build upon each other to current license models. This ISG study combines all these transformation topics in the

analyze the market and identify those providers who are among the current market leaders “digital product creation & continuous delivery” segment. For ISG current leaders in this

and the strongest competitors of these leaders. market are Atos, Capgemini, codecentric, Cognizant and DXC.

Market Segment “Digital Customer Journey” Market Segment “Digital Transformational Platforms (PaaS)”

Understanding the customer journey is key to ensure successful transformation. On the technological level, as-a-service portals are the method of choice to provision the

Companies need to understand the customer relation life cycle to make personalized offers required IT services to the lines of business. The required infrastructure and respective

at an optimum point in time to differentiate themselves from the competition. This is a key providers are described in the “digital transformational platforms (PaaS)” category of this

challenge, and ISG examines which IT providers, strategy consultants and service providers study. The focus is on companies with a high degree of automation for provisioning and

have the required competencies within this “digital customer journey” segment. For ISG, the using their IT platforms. Cloud computing is the basis and can be enhanced and refined

following eight providers are currently leading the market: Accenture, Atos, Capgemini, CGI, through comprehensive partner ecosystems. These solutions consist of a technology mix

DXC Technology, IBM iX, Publicis.Sapient and UDG. and are embedded in web platforms and marketplaces. Market leaders in Germany are

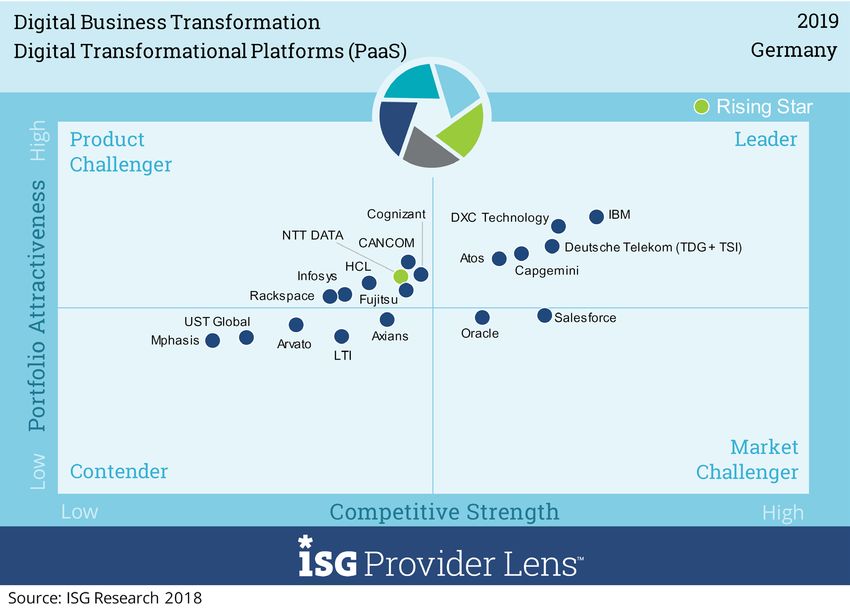

Atos, Capgemini, Deutsche Telekom (TDG and TSI), DXC and IBM.

3

© 2018 Information Services Group, Inc. All Rights Reserved.

ISG Provider Lens™ Quadrant Report | November

Juni 2018 2018 Executive Summary

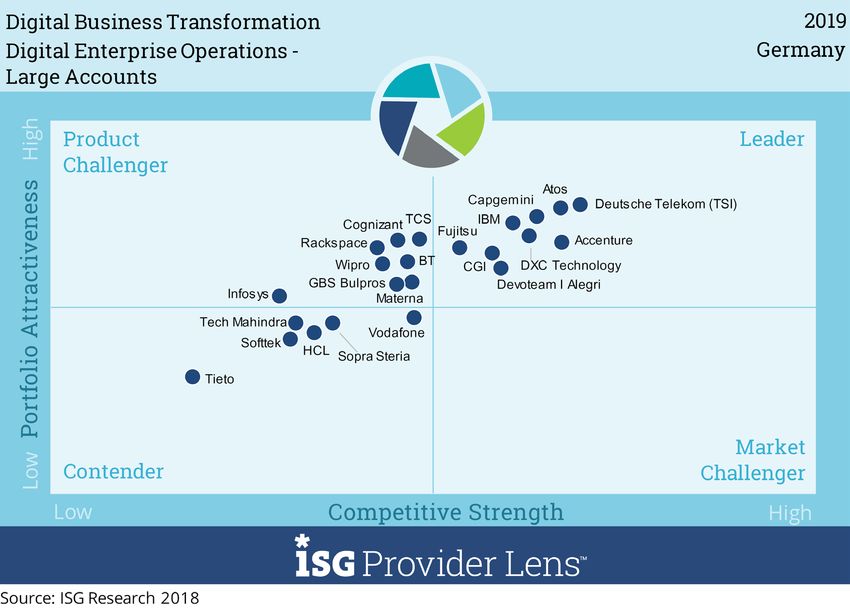

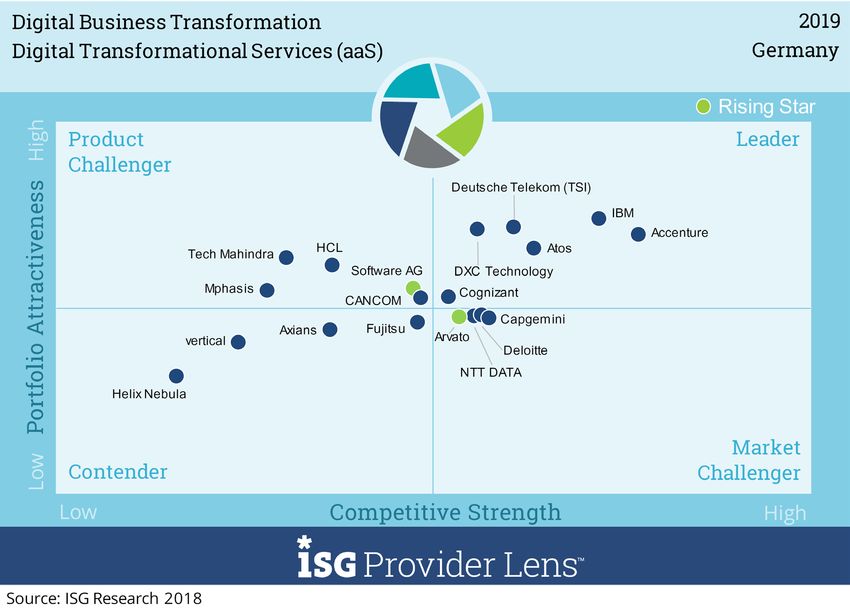

Market Segment “Digital Transformational Services (aaS)” enterprise operations providers for midmarket businesses include All for One Steeb, Arvato

Systems, Axians IT Solution, CANCOM, Deutsche Telekom (TDG) and PlusServer. Leading

Digital transformation “as a service” offerings combine heterogeneous IT services into

digital enterprise operations providers for the large accounts segment are Accenture, Atos,

an intelligent complete solution. Individual components can be used independently and

Capgemini, CGI, Deutsche Telekom (TSI), Devoteam | Alegri, DXC, Fujitsu and IBM.

in combination, depending on customers’ requirements. Normally, such offerings are

based on self-service elements provisioned and managed through dashboards. Payment Market Segment “Blockchain as a Service” (as Managed Service)

is done based on pay-as-you-go (PAYG) models or reserved resources as agreed within

A special focus within this study is on the blockchain market, since this segment bears

an enterprise agreement. Increasingly, companies are looking for XaaS solution platforms

highly disruptive potentials. Blockchain is a mature technology to control and automate

that map industry characteristics and end-user roles, for instance, solutions for sales, HR

any kind of digital transactions. This is an interesting option for all use cases that require a

or production management. Within the “digital transformational services (aaS)” segment

decentralized (distributed) ledger, for instance, Internet of Things where billions of IoT-en-

ISG analyzes and evaluates service providers who have a focus on provisioning out-of-

abled devices have the potential to communicate with each other. From a B2B perspective,

the-box platforms or easy-to adapt (open/modular) solutions, either individual parts of

many of these distributed instances can be integrated into the value creation process to

the whole service chain, such as ERP, CRM or mobile apps/IoT integration, or individual

perform transactions. This requires secure authentication and sufficient documentation

ITaaS platforms that can be used to flexibly map customer-specific management and

of related transactions for these devices. Blockchain is suitable like no other technology

control requirements. Current leaders within this market segment include Accenture, Atos,

to perform such tasks. As of to date, blockchain providers are leveraging aaS offerings

Cognizant, DXC, Deutsche Telekom and IBM.

from multiple public clouds and by Linux Foundation, Hyperledger and R3 Corda. Leading

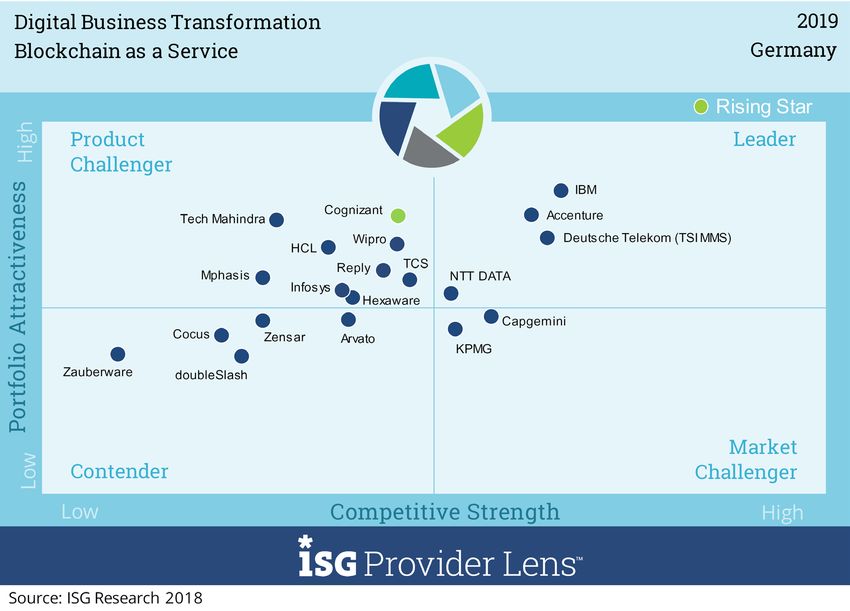

Market Segment „Digital Enterprise Operations” “blockchain as a service” providers are Accenture, Deutsche Telekom, IBM and NTT DATA.

Cognizant has been positioned as Rising Star.

Digital enterprise operations providers build up and run intelligent, IT-based infrastructures,

platforms and networks that can be used to integrate customers’ whole value chain by

combining their traditional operational excellence and managed services know-how with

business process and industry know-how to address their target customers. Leading digital

4

ISG2018

© Confidential

Information

© 2018

Services

Information

Group, Inc.

Services

All Rights

Group,

Reserved.

Inc. All Rights Reserved.

ISG Provider Lens™ Quadrant Report | November 2018

Introduction

Introduction

Definition

Simplified illustration The digital transformation megatrend is a top priority on corporate agendas. The

delivery of digital transformational solutions coupled with corporate agility is

Digital Business Transformation fully supported by advisors and researchers that are concentrating upon future-

oriented business models. The focus is on enabling businesses to efficiently

Digital Enterprise Digital Enterprise address individual customer expectations and requirements, rapidly, with

Realizing the Enabling the Digital

Operations Operations

Digital Ambition Customer Journey minimal unplanned cost, effort or disruption for the enterprise, thus increasing

- Midmarket - Large Accounts

the corporation’s competitiveness. This requires companies to move to a digital

Digital Digital Digital transformational technology and process level as soon as possible and then

Enabling Digital

Transformational Transformational Product Creation & strive for continuous change – both internally and externally. This study covers

Transformation

Platforms (PaaS) Services (aaS) Continuous Delivery three overriding aspects of the digital transformation. The general aspects and

the specific quadrants covered within each one are presented below.

Disruptive Services Blockchain as a Service 1. Realizing the Digital Ambition, comprised of two quadrants: Enabling the

Customer Journey, Digital Enterprise Operations.

Source: ISG 2018 2. Enabling Digital Transformation: PaaS, XaaS, Digital Product Creation and

Customization, Digital Continuous Delivery.

3. Disruptive Services: Blockchain.

5

© 2018 Information Services Group, Inc. All Rights Reserved.

ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Definition (cont.)

Enabling the Digital Customer Journey

A customer journey comprises the individual cycles experienced by clients before and IT vendors, strategy advisors and service providers such as IBM, Accenture and Deloitte continue

during the decision-making process for buying or using a product or service as well to take over marketing agencies and are building up their internal competencies to strengthen

as their product or service experience after having purchased the product/service. their presence in the marketing departments, while marketing agencies are strongly enhancing

Digital technologies can be used to allow for a completely new customer experience. their digital and IT technology competencies.

This category comprises agencies and service providers that have specialized

in comprehensive portfolios of digital go-to-market/business strategies, brand

communications, creative service, design and experience offerings. Providers need to

understand but must not be limited to their own underlying technology and solutions.

Instead, they should ensure an integrated strategy and a clear roadmap of the digital

customer journey offering for enterprise SMB and customers.

6

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Definition (cont.)

Digital Enterprise Operations

This segment covers the digitization of the processes of a typical large-scale These implementations are often considered “initial” or “starter” steps in the journey from

organization – using an ecosystem of components, technical platforms, processes traditional or current operations, towards cloud-based operations which map onto the enterprise

and system integration and capable of either using PaaS, or in-house operations/ inspirational “Customer Journey” plans. They are in many cases considered initial iterations and

DC or aaS operations and main DC functions in a managed and integrated (end to replaceable by more customized / comprehensive PaaS and/or XaaS offerings as the enterprise

end) manner, including DevOps tools and improvement to all operational and rapid becomes more mature in its aspirations and further along its strategic roadmap of the overall

provisioning process. digital transformation process, tempered by business and customer feedback, usage patterns and

new requirements based on this initial operating offering.

Digital enterprise operations providers help customers operate smart, IT-based

infrastructures, platforms and networks that connect sales, service and partners

across the whole value chain. This market segment combines traditional operational

excellence, including highly sophisticated technology, with managed services know-how

and an in-depth understanding of customers’ business and industry-specific challenges.

7

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Definition (cont.)

Digital Transformational Platforms (PaaS)

This segment evaluates PaaS integrated multi-tenant platform solutions offered Solutions consist of a technological mix, including hybrids, of in-house developments and best-of-

to enterprises by System Integrators and vendors acting in an SI role. Focus is on breed solutions by leading product and platform-as-a-service providers and are embedded in web

companies that deliver a high degree of automation meaning solutions that are either platforms and cloud marketplaces. These marketplaces create networking effects, integrate and

ready to use “out of the box” (pre-build) or that need customization by the SI (and distribute additional solutions, and integrate third-party products or services.

partners) whereby the solution is designed for ease of customer tailoring/modification

Many systems integrators are established players in this segment. Reasons for this include their

(open / modular / customizable). Data center managed service, IaaS or hybrid cloud

histories of being involved with integration of technological advances of cloud management

management is optional, as clients may have already selected other providers for

& orchestration and event processing services, coupled with their ecosystems of internal and

infrastructure management. Cloud computing is the foundation and the philosophy

partner offerings and adaptation capabilities.

behind these platforms that can be enhanced and refined, based on an extensive

partner ecosystem.

8

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Definition (cont.)

Digital Transformational Services (aaS) Digital Product Creation & Continuous Delivery

This segment evaluates “cloud first” aaS service providers that are focused upon “Digital product creation“ covers the creation of new digital products from ground up for

Digital Transformation with “out of the box” solutions or easy to customize solutions enterprises and is closely related to the “digital continuous delivery” paradigm, where the goal is

(open/modular) specific for enterprise needs. The Provider can manage the solution/ to deliver code updates, while ensuring continuous releasability.

service end to end if required. This may be individually focused parts of the entire DT

The basic difference, compared to the old world of product development, is the inherent focus

enterprise service chain (e.g. ERP, CRM or mobile apps/IoT integration, microservice/

on creating modular service components for the enterprise business or adapting existing but

API integration and provision, maintenance) or may be individual ITaaS platforms with

outmoded service components.

a high degree of technical complexity to meet specific customer requirements for

centralized control and high flexibility. Digital continuous delivery enables companies to increase the speed and efficiency of their

development projects while ensuring high-quality services or software. Providers of continuous

Solutions may consist of a technological mix, including hybrids, of in-house

development and innovation services may either offer co-creation or shared workspace services

developments and best-of-breed solutions by leading product and platform-as-a-

or just partial services where a team or only a management and control function remains in the

service providers and are embedded in web platforms and cloud marketplaces which

customer’s company.

provide networking effects and integrate and distribute the platform provider’s as well

as third-party products or services.

9

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Definition (cont.)

Blockchain as a Service

While blockchain is often associated with Bitcoin and other cryptocurrencies, the be used to perform peer-to-peer contracts. Blockchain is a decentral, open and cryptographic

blockchain technology can be applied to many other use cases. Bitcoin is merely the technology which allows economic agents to trust each other and perform peer-to-peer

first and most well-known use case. Blockchain implies many “independent” instances transactions; medium-to-long-term, this will eliminate the need for intermediaries accordingly.

which are based on decentralized, independent transaction automation to verify and Ultimately, blockchain also is an encryption and authentication technology to be used by service

quickly confirm a transaction. The blockchain principle is based on instances (blocks or providers in proofs of concept (POCs) and managed services operations models. Blockchain aaS

miners) that are connected (“chained”). Bitcoin is a “distributed ledger” (DL) technology, implies close partnerships with blockchain technology providers such as the top hyperscale public

i.e., a distributed database is available which grants the members of a network shared cloud providers AWS, Microsoft, Google or IBM who provide various building blocks to set up and

write, read and store permissions. Blockchain networks can be private, with restricted use this technology at the push of a button.

membership like an intranet, or public. For instance, a public Ethereum blockchain can

10

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Provider Classifications

The ISG Provider Lens™ quadrants were created using an evaluation matrix containing

four segments, where the providers are positioned accordingly.

Leader Product Market Contender

Challenger Challenger

The “leaders” among the vendors/ The “product challengers” offer a “Market challengers” are also “Contenders” are still lacking mature

providers have a highly attractive product and service portfolio that very competitive, but there is still products and services or sufficient

product and service offering and a provides an above-average cover- significant portfolio potential and depth and breadth of their offering,

very strong market and competitive age of corporate requirements, but they clearly lag behind the “leaders”. while also showing some strengths

position; they fulfill all requirements are not able to provide the same Often, the market challengers and improvement potentials in their

for successful market cultivation. resources and strengths as the are established vendors that market cultivation efforts. These

They can be regarded as opinion leaders regarding the individual are somewhat slow to address vendors are often generalists or

leaders, providing strategic market cultivation categories. Often, new trends, due to their size and niche players.

impulses to the market. They also this is due to the respective vendor’s company structure, and have

ensure innovative strength size or their weak footprint within therefore still some potential to

and stability. the respective target segment. optimize their portfolio and increase

their attractiveness.

11

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Provider Classifications (cont.)

Each ISG Provider Lens™ quadrant may include a service provider(s) who ISG believes has

a strong potential to move into the leader’s quadrant.

Rising Star Not In

Rising Stars are mostly product challengers with high future potential. This service provider or vendor was not included in this

When receiving the “Rising Star” award, such companies have a promis- quadrant as ISG could not obtain enough information to

ing portfolio, including the required roadmap and an adequate focus on position them. This omission does not imply that the

key market trends and customer requirements. Also, the “Rising Star” has service provider or vendor does not provide this service.

an excellent management and understanding of the local market. This

award is only given to vendors or service providers that have made ex-

treme progress towards their goals within the last 12 months and are on

a good way to reach the leader quadrant within the next 12-24 months,

due to their above-average impact and innovative strength.

12

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Digital Business Transformation - Quadrant Provider Listing 1 of 7

Enabling the Digital Enterprise Digital Enterprise Digital Digital Digital Product

Blockchain as a

Digital Customer Operations - Operations - Transformational Transformation Creation &

Service

Journey Midmarket Large Accounts Platforms (PaaS) Services (aaS) Continuous Delivery

Accenture 4 Leader 4 Not in 4 Leader 4 Not in 4 Leader 4 Not in 4 Leader

All for One Steeb 4 Not in 4 Leader 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Arvato 4 Product Challenger 4 Leader 4 Not in 4 Contender 4 Rising Star 4 Not in 4 Contender

Atos 4 Leader 4 Not in 4 Leader 4 Leader 4 Leader 4 Leader 4 Not in

Axians 4 Not in 4 Leader 4 Not in 4 Contender 4 Contender 4 Not in 4 Not in

BCG 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Bechtle 4 Not in 4 Market Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

BT 4 Not in 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in

CA 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Contender 4 Not in

CANCOM 4 Contender 4 Leader 4 Not in 4 Product Challenger 4 Product Challenger 4 Not in 4 Not in

Capgemini 4 Leader 4 Not in 4 Leader 4 Leader 4 Market Challenger 4 Leader 4 Market Challenger

13

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Digital Business Transformation - Quadrant Provider Listing 2 of 7

Enabling the Digital Enterprise Digital Enterprise Digital Digital Digital Product

Blockchain as a

Digital Customer Operations - Operations - Transformational Transformation Creation &

Service

Journey Midmarket Large Accounts Platforms (PaaS) Services (aaS) Continuous Delivery

CGI 4 Leader 4 Not in 4 Leader 4 Not in 4 Not in 4 Not in 4 Not in

Claranet 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Cocus 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Contender

codecentric 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Leader 4 Not in

Cognizant 4 Product Challenger 4 Not in 4 Product Challenger 4 Product Challenger 4 Leader 4 Leader 4 Rising Star

COMLINE 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Comparex 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Data One 4 Not in 4 Market Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Deloitte 4 Not in 4 Not in 4 Not in 4 Not in 4 Market Challenger 4 Market Challenger 4 Not in

Deloitte Digital 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

denkwerk 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

14

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Digital Business Transformation - Quadrant Provider Listing 3 of 7

Enabling the Digital Enterprise Digital Enterprise Digital Digital Digital Product

Blockchain as a

Digital Customer Operations - Operations - Transformational Transformation Creation &

Service

Journey Midmarket Large Accounts Platforms (PaaS) Services (aaS) Continuous Delivery

Deutsche Telekom (MMS) 4 Rising Star 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Deutsche Telekom (TDG + TSI) 4 Not in 4 Not in 4 Not in 4 Leader 4 Not in 4 Not in 4 Not in

Deutsche Telekom (TDG) 4 Not in 4 Leader 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Deutsche Telekom (TSI) 4 Not in 4 Not in 4 Leader 4 Not in 4 Leader 4 Not in 4 Not in

Deutsche Telekom (TSI MMS) 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Leader

Devoteam I Alegri 4 Not in 4 Not in 4 Leader 4 Not in 4 Not in 4 Not in 4 Not in

Dimension Data 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

direkt gruppe 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

doubleSlash 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Contender

DXC Technology 4 Leader 4 Not in 4 Leader 4 Leader 4 Leader 4 Leader 4 Not in

FIT 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

15

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Digital Business Transformation - Quadrant Provider Listing 4 of 7

Enabling the Digital Enterprise Digital Enterprise Digital Digital Digital Product

Blockchain as a

Digital Customer Operations - Operations - Transformational Transformation Creation &

Service

Journey Midmarket Large Accounts Platforms (PaaS) Services (aaS) Continuous Delivery

Fujitsu 4 Product Challenger 4 Not in 4 Leader 4 Product Challenger 4 Contender 4 Not in 4 Not in

GBS Bulpro 4 Not in 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in

HCL 4 Not in 4 Not in 4 Contender 4 Product Challenger 4 Product Challenger 4 Product Challenger 4 Product Challenger

Helix Nebula 4 Not in 4 Not in 4 Not in 4 Not in 4 Contender 4 Not in 4 Not in

Hexaware 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Contender 4 Product Challenger

Horváth & Partner 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

IBM 4 Not in 4 Not in 4 Leader 4 Leader 4 Leader 4 Leader 4 Leader

IBM iX 4 Leader 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Infosys 4 Product Challenger 4 Not in 4 Product Challenger 4 Product Challenger 4 Not in 4 Product Challenger 4 Product Challenger

inovex 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

KPMG 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Market Challenger

16

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Digital Business Transformation - Quadrant Provider Listing 5 of 7

Enabling the Digital Enterprise Digital Enterprise Digital Digital Digital Product

Blockchain as a

Digital Customer Operations - Operations - Transformational Transformation Creation &

Service

Journey Midmarket Large Accounts Platforms (PaaS) Services (aaS) Continuous Delivery

LTI 4 Not in 4 Not in 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in

Materna 4 Not in 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in

Mindtree 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Product Challenger 4 Not in

Mphasis 4 Contender 4 Not in 4 Not in 4 Contender 4 Product Challenger 4 Product Challenger 4 Product Challenger

mVISE 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

NTT DATA 4 Not in 4 Not in 4 Not in 4 Rising Star 4 Market Challenger 4 Not in 4 Leader

OIO 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Contender 4 Not in

Oracle 4 Not in 4 Not in 4 Not in 4 Market Challenger 4 Not in 4 Not in 4 Not in

PlusServer 4 Not in 4 Leader 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Publicis.Sapient 4 Leader 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

QSC 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

17

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Digital Business Transformation - Quadrant Provider Listing 6 of 7

Enabling the Digital Enterprise Digital Enterprise Digital Digital Digital Product

Blockchain as a

Digital Customer Operations - Operations - Transformational Transformation Creation &

Service

Journey Midmarket Large Accounts Platforms (PaaS) Services (aaS) Continuous Delivery

Rackspace 4 Not in 4 Not in 4 Product Challenger 4 Product Challenger 4 Not in 4 Not in 4 Not in

Ratiokontakt 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Reply 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Product Challenger

Salesforce 4 Not in 4 Not in 4 Not in 4 Market Challenger 4 Not in 4 Not in 4 Not in

SHE 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Softtek 4 Not in 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in

Software AG 4 Not in 4 Not in 4 Not in 4 Not in 4 Rising Star 4 Not in 4 Not in

Sopra Steria 4 Not in 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in

TCS 4 Not in 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Product Challenger 4 Product Challenger

Wipro 4 Product Challenger 4 Not in 4 Contender 4 Not in 4 Product Challenger 4 Rising Star 4 Product Challenger

tecRacer 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

18

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Introduction

Digital Business Transformation - Quadrant Provider Listing 7 of 7

Enabling the Digital Enterprise Digital Enterprise Digital Digital Digital Product

Blockchain as a

Digital Customer Operations - Operations - Transformational Transformation Creation &

Service

Journey Midmarket Large Accounts Platforms (PaaS) Services (aaS) Continuous Delivery

Tieto 4 Not in 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in

UDG 4 Leader 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

Unisys 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

UST Global 4 Not in 4 Not in 4 Not in 4 Market Challenger 4 Not in 4 Not in 4 Not in

Valtech 4 Product Challenger 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in

vertical 4 Not in 4 Not in 4 Not in 4 Not in 4 Contender 4 Not in 4 Not in

Vodafone 4 Not in 4 Not in 4 Contender 4 Not in 4 Not in 4 Not in 4 Not in

Wipro 4 Not in 4 Not in 4 Product Challenger 4 Not in 4 Not in 4 Product Challenger 4 Product Challenger

Zauberware 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Contender

Zensar 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Not in 4 Contender

19

© 2018 Information Services Group, Inc. All Rights Reserved.Digital Business Transformation Quadrants

ISG Provider Lens™ Quadrant Report | November 2018

SOCIAL

ENABLINGENTERPRISE NET-

THE DIGITAL CUSTOMER

WORKING

JOURNEY SUITES

Definition

A customer journey comprises the individual cycles experienced by

clients before and during the decision-making process for buying or

using a product or service as well as their product or service experience

after having purchased the product/service. Digital technologies can be

used to allow for a completely new customer experience. This category

comprises agencies and service providers that have specialized in

comprehensive portfolios of digital go-to-market/business strategies,

brand communications, creative service, design and experience

offerings. Providers need to understand but must not be limited to

their own underlying technology and solutions. Instead, they should

ensure an integrated strategy and a clear roadmap of the digital

customer journey offering for enterprise SMB and customers.

IT vendors, strategy advisors and service providers such as IBM,

Accenture and Deloitte continue to take over marketing agencies

and are building up their internal competencies to strengthen their

presence in the marketing departments, while marketing agencies are

strongly enhancing their digital and IT technology competencies.

21

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Enabling the Digital Customer Journey

ENABLING THE DIGITAL CUSTOMER

JOURNEY

Observations

More and more providers understand the relevance of the digital of them very extensively – to meet their clients’ needs. United Digital Group (UDG) as the remaining

customer journey as an integral part of the digital enterprise traditional marketing agency in the leader quadrant has sold parts of its business and seems to lose

transformation. Many (especially traditional IT) providers have started some of its traction, although still being a leader in this segment. The Rising Star of 2019 is Deutsche

vast efforts to reorganize their business units towards dedicated digital Telekom (T-Systems MMS), having reorganized and now been given a wider scope within the large

customer journey fulfillment organizations, effectively combining T-Systems organization.

marketing and branding skills with technology expertise and lab offerings. Accenture clearly focuses on a holistic digital transformation on the technical and organizational side

Best examples are Capgemini and Publicis, who are looking at the and enjoys an established thought leadership position in this segment. Within the digital customer

business from completely different perspectives but are both creating journey, Accenture's organizational development competencies are combined with SinnerSchrader's

new business units around the digital transformation and the digital branding and marketing technology skills.

customer experience. This year’s evaluation of Publicis therefore includes

Atos has a strong market presence and a very broad technological offering in the DCJ space. Atos

both SapientRazorfish and Pixelpark, combining them within an overall takes a holistic approach to the digital customer journey, including touchpoints, transactions,

Publicis.Sapient division integration into existing systems and customer behavior analysis.

Clear market leaders are IBM iX, especially with their long-term strategy Capgemini is reorganizing its digital business into one business line, Capgemini Invent, with approx.

and their ability to effectively integrate their Watson AI functionality into 6,000 employees, in 10 studios and 30 offices worldwide. Capgemini Invent includes strategy and

the digital customer journey, and Publicis.Sapient who combines vast transformation consulting, creative design, emerging technologies and data analytics/AI.

creative marketing and branding skills with deep technology expertise and With "CGI Innovation as a Service", CGI has a full-service offering for setting up a structured,

an extraordinary market presence. Capgemini, CGI, Atos and DXC are all consolidated innovation management in the company. CGI understands the digital customer journey

technology powerhouses that have reorganized their businesses – some as part of a larger digital transformation process and includes agile development processes, data

analytics and advanced cybersecurity services.

22

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Enabling the Digital Customer Journey

ENABLING THE DIGITAL CUSTOMER

JOURNEY

Observations (cont.)

DXC Technology pursues a holistic approach to the digital customer UDG's portfolio includes strategy & change management, data & insights, marketing campaigns

journey, from user experience (UX) through value proposition/business & content, sites & portals and learning & development. UDG services a broad base of renowned

modelling and service design to the development of touchpoints. DXC international customer, including very good German references. However, the overall strategic

uses established methods such as Design Thinking and Business Model direction of UDG is quite unclear.

Generation.

T-Systems MMS as the Rising Start 2019 clearly focusses on digital business processes and the

As an agency and design studio network, IBM iX serves customers of impact of digital technology on brands, products and services. With their Digital Innovation Lab

various sizes worldwide. IBM has a strong focus on cloud computing and individual transformation workshops they offer joint development of tangible innovations

and is a leader in artificial intelligence and data analytics. IBM and prototypes already within strategy sessions.

integrates their Watson AI capabilities featuring campaign automation,

personalization functionalities, market insights, cognitive tagging and

even contextual data like weather data.

Publicis.Sapient is represented by SapientRazorfish, the largest

German digital agency, being also active worldwide, and Publicis

Pixelpark. Highly interesting projects in the digital environment are

conducted both with large and midmarket customers and at any level

of complexity, testifying the leading role and understanding of the

customer requirements of a digital customer journey.

23

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Rising Star: Enabling the Digital Customer Journey

RISING STAR: DEUTSCHE TELEKOM (MMS)

Overview Caution

Within their daughter company T-Systems, Deutsche Telekom offers T-Systems Multimedia Solutions (MMS) Although being part of T-Systems’ Digital Solution unit, the digital customer journey

for digital business consulting, including the design and development of a digital customer journey. T-Systems team of T-Systems MMS is still rather small and focusing on organic growth, which

MMS, with about 1,900 employees and an extended team of about 700 employees that cover customer journey might limit their growth capabilities, due to the shortage of experts such software

and customer experience solutions, is part of the new T-Systems “Digital Solutions” portfolio unit, with a total of engineers or UX developers in the work market.

4,800 employees approx. and a clear focus on the DACH region.

With the background of Deutsche Telekom and T-Systems, T-Systems MMS can provide the full scope of

business digitization services, from strategic development to the development of a technological infrastructure.

Strengths

T-Systems MMS as the Rising Start 2019 clearly focusses on digital business processes and the impact of digital

technology on brands, products and services. With their Digital Innovation Lab and individual transformation

workshops they offer joint development of tangible innovations and prototypes already within strategy

sessions. This approach, together with their packaged consultancy and workshop offering, are clear advantages

to win the conservative German midmarket.

T-Systems MMS provides partnerships with leading technology manufacturers. Dedicated teams specialize e.g.

on IBM Watson AI, on data analytics and customer experience solutions. T-Systems MMS prefers to expand their

2019 ISG Provider Lens™ Rising Star

solution offerings with partnerships but has some solutions developed in-house, e.g., semantic analytics and

chatbots. T-Systems MMS offers easy prototyping and

T-Systems MMS has a strong presence in the German midmarket sector as well as within the large packaged offerings – a clear advantage not

enterprise segment. only for the German midmarket.

24

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018

SOCIAL ENTERPRISE

DIGITAL ENTERPRISE NET-

OPERATIONS – Digital Enterprise Operations – Large Accounts

WORKING SUITES

LARGE ACCOUNTS

Definition

This segment covers the digitization of the processes of a typical

large-scale organization – using an ecosystem of components, technical

platforms, processes and system integration and capable of either

using PaaS, or in-house operations/DC or aaS operations and main

DC functions in a managed and integrated (end to end) manner,

including DevOps tools and improvement to all operational and rapid

provisioning process.

Digital enterprise operations providers help customers operate

smart, IT-based infrastructures, platforms and networks that connect

sales, service and partners across the whole value chain. This market

segment combines traditional operational excellence, including highly

sophisticated technology, with managed services know-how and an

in-depth understanding of customers’ business and industry-

specific challenges.

25

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Digital Enterprise Operations – Large Accounts

SOCIAL ENTERPRISE

DIGITAL ENTERPRISE NET-

OPERATIONS –

WORKING SUITES

LARGE ACCOUNTS

Definition (cont.) Observations

These implementations are often considered “initial” or “starter” steps in The degree of process digitization among globally active corporations has increased

the journey from traditional or current operations, towards cloud-based significantly. Driven by new business concepts that must be implemented quickly,

operations which map onto the enterprise inspirational “Customer companies are forced to digitize their workflows in order to achieve managed end-to-end

Journey” plans. They are in many cases considered initial iterations and

functions. Managed service providers have got ready accordingly and have added digital

replaceable by more customized / comprehensive PaaS and/or XaaS

enterprise operations services to their offerings, increasingly with an industry-specific

offerings as the enterprise becomes more mature in its aspirations

focus. Service providers’ in-depth industry know-how is an important requirement.

and further along its strategic roadmap of the overall digital

transformation process. Accenture provides an outstanding consulting and integration services portfolio and

comprehensive digital services.

Atos’ offering includes high-class managed services for digital environments. The company

has industry-specific know-how of all industries and great IoT competence. With their global

presence, Atos is an attractive partner for globally active customers.

Capgemini provides a comprehensive digital services offering and is driving automation.

The company has in-depth know-how of all industries and is an adequate partner for

large accounts.

26

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Digital Enterprise Operations – Large Accounts

SOCIAL ENTERPRISE

DIGITAL ENTERPRISE NET-

OPERATIONS –

WORKING SUITES

LARGE ACCOUNTS

Observations (Cont.)

Fujitsu provides a broad digital services portfolio, supported by the OpenStack-based K5

Based on their Unify 360 platform, CGI provides comprehensive

platform, which can be used to integrate all cloud environments as well as traditional

digital solutions. The portfolio comprises an end-to-end solution,

IT landscapes.

from consulting to the going-live of a cloud environment.

IBM is a successful integrator and provides a flexible, scalable platform for managing digital

Deutsche Telekom (TSI) provides attractive and comprehensive digital

enterprise operations services. The offering covers all technologies and the portfolio is

services for large accounts as well as an extensive security portfolio

enhanced continuously.

which is also available as managed service.

Devoteam | Alegri has specific industry know-how of the

manufacturing, automotive and energy sectors and has been a

successful and long-standing provider of digital enterprise operations

services. The provider’s large development team develops and

modifies applications, which can be integrated into the managed

services. DXC Technology is driving their digital process and

automation offering. Based on the multitude of digital services and

the provider’s long-standing managed service experience DXC is an

attractive partner.

27

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018 Digital Enterprise Operations – Large Accounts

DEUTSCHE TELEKOM (TSI)

Overview Caution

Deutsche Telekom’s T-Systems (TSI) subsidiary provides a comprehensive digital enterprise operations portfolio According to press announcements, the provider plans to reduce staff numbers by

for large enterprises. TSI has proven market and industry knowledge and helps customers to transform their 6,000 employees within the next three years. About 4,000 jobs are outsourced and

process landscape into a new digital IT landscape to provide a targeted, customized digital business solution moved abroad into more cost-efficient countries. On the other hand, the provider

which is operated by TSI. Customers benefit from a highly scalable, platform-based cloud environment. is searching for qualified talent to expand and drive the service offering. The future

will show how this reorganization will affect the provider’s market position and

adoption by customers.

Strengths

Comprehensive transformation support. TSI has strong capabilities to provide end-to-end digital

transformation support form one single source, covering all kinds of topics such as cloud computing, data

analytics, Internet of Things, mobile enterprise/business or cybersecurity. More than 7,000 ITIL-certified

employees provide consulting and service integration support. Prince2 is used to conduct complex IT projects.

Digital enterprise operations services. Services are provisioned out of the provider’s own certified data

centers in Germany and comply with German privacy and data protection regulations. The Open Telekom Cloud

(OTC) is the only public cloud offering certified as “Trusted Cloud” by the German Federal Ministry of Economics

2019 ISG Provider Lens™ Leader

and Energy. It can be operated out of customers’ internal and/or hyperscaler data centers. TSI maintains

partnerships with all major cloud service providers. TSI provides comprehensive digital services

Comprehensive security services. The provider has about 1,200 security experts. Products are tested and for large enterprises, combined with in-depth

used within TSI’s own data centers and ensure a high degree of security. This allows TSI to offer integrated ICT industry know-how and market experience.

services and support hybrid IT infrastructures. The offering complies with GDPR.

28

© 2018 Information Services Group, Inc. All Rights Reserved.ISG Provider Lens™ Quadrant Report | November 2018

Digital Transformational Platforms (PaaS)

SOCIAL ENTERPRISE NET-

DIGITAL TRANSFORMATIONAL

WORKING

PLATFORMS SUITES

(PAAS)

Definition

This segment evaluates PaaS integrated multi-tenant platform

solutions offered to enterprises by System Integrators and vendors

acting in an SI role. Focus is on companies that deliver a high

degree of automation meaning solutions that are either ready

to use “out of the box” (pre-build) or that need customization by

the SI (and partners) whereby the solution is designed for ease of

customer tailoring/modification (open / modular / customizable).

Data center managed service, IaaS or hybrid cloud management is

optional, as clients may have already selected other providers for

infrastructure management. Cloud computing is the foundation

and the philosophy behind these platforms that can be enhanced

and refined, based on an extensive partner ecosystem.

29

© 2018 Information Services Group, Inc. All Rights Reserved.You can also read