Macroeconomic Outlook 2021: 21, It was a very good year - AXA Investment Managers

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

For professional clients only

2 December 2020

Research & Strategy Insights

Macroeconomic Outlook

2021: 21, It was a very good

year…

From the Core Investment

Macro Research team

With contribution from:

Chris Iggo – AXA IM Core Investments CIO

Romain Cabasson – Solution Portfolio Managers, AXA IM Core Multi-Assets

Alessandro Tentori – CIO AXA IM Italy

Table of contents

Macro outlook – Looking beyond the winter 3

By Gilles Moec

Investment outlook 2021 – A brighter future is possible 5

By Chris Iggo

US – A year of rebound, but recovery must wait 7

By David Page

Eurozone – It’s not over yet 9

By Apolline Menut

UK – Winter outbreak and Brexit to delay 2021 recovery 11

By David Page

Once the pandemic is over, Japan may leverage on some tailwinds 12

By Hugo Le Damany

China – Back to normal 13

By Aidan Yao

Emerging Markets – Tomorrow is another day 15

By Irina Topa-Serry

Foreign Exchange – Growth expectations to drive currencies in 2021 17

By Romain Cabasson

Cross asset – Correlation regime 17

By Gregory Venizelos

Rates – modest performance likely in 2021 19

By Alessandro Tentori

Credit – hard to imagine anything but a calmer 2021 21

By Gregory Venizelos

Equities – Show me what you got 23

By Varun Ghotgalkar

Forecast summary 25

Calendar of 2021 events 26

Abbreviation glossary 27

2

Macro outlook – Looking beyond the winter

By Gilles Moec

We now know that a “V-shape” recovery did not materialise.

Key points We never believed in it in the first place because, even in the

absence of the “second wave”, our view always was that

• The good news of the vaccines insures us against after the spectacular rebound upon reopening, lagged

indefinite “lockdown/reopening” cycles, but we do demand-side impairments, channelled through the labour

not expect a proper rebound for the world economy market and firms’ financial position, would slow GDP growth.

before the second half of 2021. We note that even China, which so far has avoided a “second

• To deal with the unavoidable GDP contraction in wave”, private consumption is still “below trend”.

Europe and this US this winter, and fuel the ensuing

recovery, more policy support is need. Central banks Does this mean we are in a “W” shape trajectory? Yes, but

are doing their part. Fiscal policy may be more only with a shallow second leg. The best analogy we can think

hesitant. of is the Greek letter μ. Four factors will make the winter

contraction less painful:

Choose your horizon - First, large swathes of the world economy are not

affected by the pandemic at this stage. When Europe

Our level of optimism at this juncture is dependent on the went into its first lockdown, Chinese activity had not yet

time horizon. We now know for certain that we are not normalised. At this stage there is no sign that we need to

sentenced to and endless repetition of lockdown/reopening brace ourselves for a second wave there. World demand

cycles. Uncertainty on the roll-over of the vaccine is high but, should hold better. This is good news for an export-reliant

in our baseline, “herd immunity” would be reached in most region such as the Euro area.

developed economies around the middle of 2021, allowing a

permanent restoration of supply conditions. However, we - Second, even where the second wave is in full swing,

still need to brace ourselves for some challenging months lockdowns are less stringent. Our forecasts assume that

ahead, with a relapse in GDP which is already well underway the impact of Covid-suppressing measures and

in Europe as we write, and which is looming in the US. behavioural changes on activity will be roughly half of

what it was at the last peak and so far, this seems to be

Of course, we could choose to look through the next three to confirmed by the message from real-time indicators such

six months as a mere bad dream. This is what equity markets as Google activity reports. Lockdowns are also at this

are largely doing. An issue though is that the quality of the stage expected to be much shorter.

rebound from the second half of 2021 onward will be to

some extent dependent on the depth of the ongoing - Third, businesses are much better prepared than during

recession and the quantum of policy protection governments the first wave. They have been able to test their capacity

and central banks will offer. Some decisions need to be made for mass remote-working, and where on-site activity is

urgently. permitted, sanitary protocols are already in place.

We are convinced that central banks will be successful in - Fourth, the first wave came with a brief but intense

creating the right conditions for massive fiscal support. Some financial turmoil, which added to the generic sense of

political/institutional issues may however impair uncertainty. Now that central banks have demonstrated

governments’ capacity to take advantage of this favourable their capacity to rein in volatility, financial institutions,

environment. Thinking about how an “exit strategy” from corporates and households should feel more secure.

extraordinary policy support could shape up would in fact

help governments and central banks make their decisions But symmetrically we expect the ensuing rebound to be

now. This could be the “big debate” of the end of 2021. shallower than what was observed last summer.

Governments will have learned from their mistakes last

The μ shape recovery spring upon reopening too fast, not least because lockdowns

will end in wintertime when pressure on healthcare capacity

Coming up with intuitive descriptions for the trajectory of is high. Lockdowns are likely to give way to easier restrictions,

economic growth in the current pandemic has become a not outright reopening. In the US, the federal level has little

cottage industry. Let’s start with two shapes which have direct impact on how Covid-suppressing measures are

become impossible, or at least very unlikely. implemented on the ground, but it can “nudge” the local

authorities. Joe Biden is likely to take a more hands-on

3

approach than his predecessor. In our baseline, governments its Pandemic Emergency Purchase Programme until the end

won’t take the risk of a “third wave” until vaccination ensures of 2021 at least. The Fed is clearly in a similar mindset,

“herd immunity” around the middle of the year. judging by Jay Powell’s repeated calls for more fiscal action.

Calibrating the speed of the recovery in the second half of Will these calls be heard? While we don’t doubt fiscal policy

the year is difficult. In a “rosy” scenario, households would will remain accommodative in the US and Europe in 2021,

quickly catch-up on spending and the bulk of the savings there is a wide margin of uncertainty on the quantum of such

overhang accumulated in 2020 would find its way back to actions. In the US, if the Democrats win the two remaining

consumption. In a similar fashion, firms would immediately Senatorial races on 5 January 2021, their fiscal stimulus

step up their investment effort. We are more circumspect. To programme of 10% of GDP will be in play. If they don’t, they

some extent, the recent rise in savings is an artefact. In many will have to find a compromise with the Republicans who

advanced economies income has been propped up by a currently hold to their $500bn red line (2.5% of GDP). $500bn

massive fiscal stimulus (particularly in the US where the is no small change. It would be enough to avoid a “cliff” for

CARES act injected 10% of GDP in the economy). In October emergency unemployment benefits and channel enough

2020, US personal income fell on the month as the fiscal push federal money into local authorities to avoid a mandatory

is fading. In Europe, the true state of the labour market is fiscal tightening of 1.5% of GDP in this layer of government.

much worse than what the usual indicators would suggest: In our baseline, the fiscal push would stretch to $1tn – the

many workers remain on their firms’ payrolls thanks to Republicans reacting to the winter GDP contraction – but the

generous part-time unemployment benefit schemes. They level of uncertainty is high. Moreover, the longer-term fiscal

keep workers attached to their employers which is a good boost that Biden campaigned on would be highly unlikely to

thing to prepare the recovery, but (i) this does not help the materialise without Democrat control of the Senate.

“newcomers” to the labour market and (ii) there could be a

“backlash” when the schemes are wound down. On the In Europe, the Next Generation pact should allow for

business side, decision-makers will have to factor in the steep significant fiscal support, even if it will roll out only slowly

elevation in corporate debt in 2020 as well as ongoing over the coming years. It may become more effective in

uncertainty around the likely strength of demand. prolonging the recovery into 2022 than in kickstarting it in

2021, but political difficulties continue to impair its roll-out

We also need to be realistic about world demand. During the (as we write, we still don’t know if a deal will be struck with

Great Recession of 2008/2009 China accepted to act as an Hungary and Poland, unblocking the EU budget). In general,

engine of global growth by over-stimulating domestic some European governments seem to remain cautious with

demand. While the Chinese economy has normalised nicely the quantum of fiscal support, except for Germany which is

in 2020, Beijing has remained prudent with its policy-mix. We making full use of its massive room for manoeuvre.

think western exporters should count on solid, rather than

stellar Chinese demand in 2021. Governments with shakier debt sustainability conditions do

not want to count too much on permanent ECB forbearance,

Calibrating policy support probably rightly so. There is a debate to have on how

cooperation between fiscal and monetary policy could

The impact of monetary policy on the economy through the continue beyond the pandemic emergency. Governments

traditional channels has probably exhausted by now (interest need to be convinced that the central bank will take its time

rates were already low to start with) and the extension of QE to normalise its stance so that they are not forced into

in the spring of 2020 to new asset classes (e.g. corporate recovery-killing crash fiscal retrenchment. Symmetrically, the

bonds in the US, commercial paper for both the Fed and the central bank needs to be reasonably confident governments

ECB) had more to do with nipping the financial turmoil in the will engage in fiscal consolidation when the economy is on a

bud than about stimulating the economy per se. sounder footing. This calls for an overhaul of the European

fiscal surveillance framework. There might be some volatile

However, monetary policy remains crucial because it is what moments in late 2021 when the market questions the ECB’s

makes fiscal policy possible, free from any market-made policy beyond PEPP.

tightening in financial conditions. This was expressed in no

ambiguous terms by Christine Lagarde in her policy speech at We note that in some EMs, the room for manoeuvre on

the ECB’s annual conference: “While fiscal policy is active in accommodation is scarce, with inflation surging in a few

supporting the economy, monetary policy has to minimise any cases (Turkey, India, Mexico to a lesser extent). However, this

“crowding-out” effects that might create negative spill overs is not a general feature. We are broadly constructive on EM,

for households and firms. Otherwise, increasing fiscal where GDP would grow by 5.5% in 2021, more than

interventions could put upward pressure on market interest offsetting the 2.9% loss of 2020. In the developed world, a

rates and crowd out private investors, with a detrimental significant “GDP deficit” would remain, the rebound of 4.6%

effect on private demand”. This is akin to “implicit yield not offsetting the 5.9% contraction of 2020.

control”. We expect the ECB to extend in duration and size of

4

Investment outlook 2021 – A brighter future is possible

By Chris Iggo

the on-hold super-easy monetary policy, and the potential for

Key points expectations of growth and inflation. There may be scope for

higher levels of government borrowing to push yields up.

• Policy support and hope for a vaccine enabled a Many anticipate higher yields, given where they presently

defensive bull market to develop post-March 2020 are, and the potential for a reversal of the past year’s moves.

• A broader-based cyclical rally in risk assets should However, forecasts of higher bond yields have been subject

come in the wake of vaccine deployment in 2021 to systematic errors for some time. Without inflation,

• An end to the pandemic, ongoing policy support and investors really should mull over whether central banks will

a focus on green investment should all contribute to want higher long-term real yields.

a brighter outlook. Equities should benefit.

• Fixed income returns will likely remain constrained at Since the middle of 2020 global bond returns have been flat -

low levels of yield and credit spread. What happens and given the backdrop of low yields, alongside the fact that

to yields will be important for all markets in 2021. credit spreads are almost back to pre-crisis levels, returns

from fixed income strategies will be challenged. Higher

underlying yields would make it even more challenging.

Follow policy – and the science Either central banks continue to repress yields and volatility

in bond markets, allowing only modest returns, or – in a more

For investors, there are vital lessons to be learned from the positive economic environment – markets start to price in a

past year. The first really echoes the experience of the “tapering” of monetary support. Under such a scenario,

2008/2009 global financial crisis – namely when the going returns could be negative. This would also impact credit and

gets tough, policymakers show up. Since it became clear how equity returns too, as was the case in 2018.

severe the impact of the pandemic was going to be,

monetary and fiscal policy has underwritten the global Emerging market debt, high yield and loans may be more

economy, and by extension, financial asset prices. interesting to yield-hunting investors. High yield and loans

Importantly, this is continuing, and from a long-term offer more protection against any upward shift in risk-free

perspective the benefits of aggressive policy support rates and credit concerns should alleviate in a recovery. Of

massively outweigh the costs. Concerns over rising budget course, 2021 will be challenging from a growth point of view,

deficits, debt and bloated central bank balance sheets should just as the environment was after the previous financial crisis.

be judged against the fact that policy continues to limit the But these credit-intensive assets still performed well back

risk of devastating wealth destruction, mass unemployment then. Emerging market bonds witnessed significant inflows

and an outright depression. towards the end of 2020 and should be a beneficiary of the

impact of vaccines, even if the distribution to populations in

Another lesson is to pay attention to the science. The fragility developing markets may be somewhat fragmented.

of our way of life has been exposed by a pandemic, which in

hindsight, we were woefully unprepared for. The success or

The outlook is equity-friendly

otherwise in managing the crisis has been determined by our

understanding and application of epidemiology and virology

The outlook remains equity-friendly. Policy support and

research. Sadly, policymakers have not always followed the

investor faith in a scientific solution to the pandemic have

science, and arguably, there have been human and economic

been the twin pillars of market performance since last March.

costs which potentially could have been avoided. It also

Growth has resumed and should continue while interest

means that the legacy of the pandemic will persist beyond

rates will remain low. There is upside in consumer spending

the good news on vaccine developments. Lost jobs and

and industrial production in many economies. Sectors

businesses, as well as changes in how people live, work and

trashed by the pandemic will have the opportunity to recover

interact will be the legacies of 2020. But so ultimately will be

over the next 12 to 24 months. Life won’t be a bed of roses

the successes of economic policy and the development of

though. Equity markets are likely to reflect numerous trends,

vaccines in record time.

and not just the progress of global GDP shifting back towards

what would have been its trend level.

For the coming year, changing expectations of the shape and

strength of the recovery will be important in influencing

Some of these trends are clear. The evolution from a

returns and volatility. What we can count on is that interest

defensive, to a more cyclical bull market, has had a couple of

rates will remain extremely low, and therefore companies

false starts. What has stifled it so far is the ongoing damaging

and governments alike will continue to enjoy low-cost

impact of the pandemic on activity – pushing the next leg of

funding. What happens to bond yields will be determined by

5

the cyclical recovery back. There is also the lack of conviction identifying best-in-class companies across sectors that are

that inflation and rates will move higher and that cyclical developing credible strategic plans to lower their carbon

earnings will experience an above-trend trajectory, even if footprint. But the world needs to follow science-based

these are necessary for a more broad-based bull market. As targets and focus on the technologies which will make the

we are not convinced that inflation will move higher and biggest impact on lowering the cost curve of the energy

await convincing signals from higher yields, support needs to transition. Hydrogen as a green fuel, carbon capture and

come from earnings. The consensus for 2021 is for strong storage, and new ways of transporting and storing green

growth in earnings-per-share relative to the recession of energy are all areas that need investment but can also

2020. Yet, now, the level of projected earnings for the end of provide profitable opportunities for the key players.

next year is not much higher than it was at the end of 2019.

As 2020 draws to a close, the news on the pandemic and the Exhibit 1: Carbon price still too low

global economy – ahead of a vaccine next year – is worrying.

Investors need to be given reasons to be more confident that

earnings will eventually rebound robustly next year and into

2022 – and we do generally expect that to occur. However,

the story needs to include a recovery in earnings in cyclical

sectors and those most impacted by the pandemic. The

timeline of when sectors such as airline travel and hotel

occupancy will return to normal levels remains unclear. Here

is where deployment of vaccines is critical in putting the

world on a recovery path to economic normality. The

industrial cycle also needs to continue to strengthen to push

Source: Bloomberg and AXA IM Research, as of 19 November 2020

up the general level of corporate earnings.

Public investment needs to sit alongside the marshalling of

There are two other big themes for equities. One is the private capital. There are grounds for optimism here. The

continued impact of digitalisation and automation across incoming Joe Biden-led Democrat Administration in the US

many walks of life. The pandemic has clearly identified this. will take a very different approach to climate relative to the

Online communication, consumption, education and outgoing government. Domestically this will include a focus

entertainment is replacing many traditional economic on areas such as electronic vehicles and de-carbonising

activities with implications for small and large businesses energy. In Europe, a significant amount of the European

alike. The large providers of online services and the Union’s recovery fund and budget will be dedicated to green

technology that supports them will, in all likelihood, continue investments. There are interesting developments in countries

to deliver superior growth. They will also continue to be a like Saudi Arabia, and of course, China, which is aiming to

magnet for regulatory and political attention. However, the become carbon neutral by 2060. Ideally, we might see more

investment case remains strong. international cooperation on things like establishing a global

price for carbon. While there are numerous carbon pricing

The other theme is related to the energy transition. This year schemes around the world, they are fragmented and mostly

has seen increased awareness of the need to rapidly reduce don’t reflect a carbon price that is high enough to accelerate

carbon emissions. The private sector – corporates, banks, and the shift away from fossil fuels. The carbon price should rise

asset owners and managers – are making big contributions quite substantially over time, and the existence of financial

and there will be intense focus on governments at the United products based on exchange-traded futures for carbon now

Nations COP26 meeting in Glasgow, which is now set to take provide investors the opportunity to hedge or offset their

place in November 2021. In the field of investing, the hard-to-reduce carbon exposures (Exhibit 1).

proliferation of environmental, social and governance factors

i.e. ESG, and impact funds, is unlikely to be halted. More A sustainable economy is one that can deliver wealth and

interesting, however, is that the technologies being growth. Reducing climate risks and lowering the cost of

developed around the energy transition can give a boost to energy over time are essential for driving productivity and

the earnings of traditional industrial companies. The biggest reducing inequality. As investors, we need to continue

manufacturers and users of green hydrogen, for example, sit putting governments and companies to task by insisting on

in the materials and industrials sectors. allocating capital on the grounds of sustainability. For

markets, long-term growth is dependent on the continued

Achieving carbon neutrality requires trillions of dollars of shifting of the frontiers. Going forward, climate change

investment over the coming years. The key is to mitigate the mitigation could prove as powerful for corporate earnings

cost of transition through technological progress and this and equity investors, as digitalisation has been over the last

provides plenty of investment opportunities. These include two decades.

the ongoing development of renewable energy sources and

6

US – A year of rebound, but recovery must wait

By David Page

widespread coverage is only likely to lift activity across H2

Key points 2021. A broad rise in mobility to pre-COVID-19 levels could

boost growth materially from mid-2021. Yet we pencil in a

• Uncertainty will persist into 2021, over a winter virus more cautious gain as households face resource constraints

outbreak, policy gridlock after the US election and – and firms’ spending may be limited by high levels of debt.

more positively – the roll-out of a vaccine

• We forecast strong growth of 4.8% in 2021 and 3.7% Exhibit 2: Virus on the rise again

in 2022, following this year’s expected 3.4% fall

• Yet this would only achieve ‘recovery’ by end-2023

• The Federal Reserve is likely to remain the only

reliable source of policy support. Rates should remain

on hold until 2024, but quantitative easing tapering

could begin early in 2022

•

Who knew?

In our 2020 Outlook, we warned of recession in 2021 and the

Federal Reserve (Fed) easing policy by end-2020. We did not

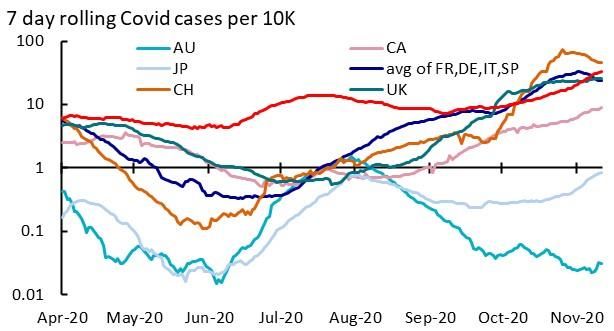

Source: Johns Hopkins and AXA IM Research, Nov 20

envisage a global pandemic, the sharpest quarterly

contraction in GDP on US records and the Fed expanding its 46th POTUS – transition delay, divided Congress?

balance sheet faster than after the financial crisis of 2008-09.

November’s election left Joe Biden set to become the 46th

Looking ahead to 2021 and 2022, we are mindful of the still

President on 20 January. While President Donald Trump has

significant uncertainties that persist. These include an

pursued a number of legal challenges, none have proved

acceleration of new virus cases in the US and Europe as the

substantial and only served to delay transition. Yet the new

winter approaches, and more encouragingly, the prospect of

President still faces an uncertain Congress. The House of

mass vaccination throughout 2021. It also includes more

Representatives remains in Democrat control. The Senate

mundane uncertainties, such as how new US President Joe

outcome is uncertain, with ‘run-off’ ballots to decide the two

Biden will manage the likely challenge of a mixed Congress.

Georgia seats to be held on 5 January. If the Democrats win

both they would draw level in the Senate, handing a casting

The economics of COVID-19 vote pass to Vice President Kamala Harris and gaining

majority control. In our view, this is unlikely.

As 2020 has taught us, the path of the virus is both

unpredictable and damaging. The US’s initial Q2 contributed President-elect Biden thus looks most likely to face a divided

to a 31.9% (annualised) contraction in GDP, the steepest on Congress, creating material policy-making uncertainty. Biden

record. Exhibit 2 shows the virus is re-emerging as the US is a seasoned politician with experience of crafting bipartisan

heads into winter. We fear a worse outbreak than over the support. However, US politics has become more fractious and

summer, but less disruptive than the initial outbreak. All-in-all partisan and the experiences of Presidents Trump and

we have lowered our outlook for Q4 2020 and Q1 2021 to Obama working with a divided Congress are not encouraging.

6.1% and -2.4% (annualised) respectively. We fear political gridlock that is likely to impact the economy.

Government appointments may take longer. Further short-

2021 looks likely to be the year of mass vaccination against term emergency stimulus is expected to be delayed further

the coronavirus. Yet deployment at scale is challenging and and smaller – we assume $1-1.5tn in Q1 2021. And most of

demand uncertain, with one survey suggesting that a third of Biden’s progressive manifesto is unlikely to be enacted,

the US public would not get inoculated. We assume that a leaving the US economy bereft of significant long-term fiscal

vaccine is made available to emergency workers and support and remaining reliant on easy monetary conditions.

vulnerable groups in Q1, with wider dissemination beginning

in Q2 and broadly completed before next winter. The Fast growth, but much ground to make up

economic boost this would deliver is uncertain. Reduced

susceptibility amongst the vulnerable would lower the need

The near-term outlook will be dependent on the virus and

for broader restrictions, boosting activity in H1 2021. More

short-term stimulus. While the virus should dampen

7

spending over the coming months, the ongoing delay to 2022. PCE inflation – the Fed’s preferred measure – is likely

additional fiscal support is resulting in falling household to remain somewhat lower and we forecast 1.5% and 1.9%

incomes. The saving rate, in decline since April, was a still for 2021 and 2022 respectively.

elevated 14.3% in September, but we expect it to fall steadily

to close this year to under 11%. Without additional stimulus The Fed’s broad shoulders

in Q1, falling incomes are likely to constrain consumer

spending and growth from early next year. With only gradual economic recovery, ongoing policy support

will be needed, and our baseline electoral view suggests this

Beyond a challenging start to the year, we are hopeful for is more likely to be monetary than fiscal. In the near-term,

2021. Fresh fiscal stimulus and the gradual mass roll-out of a fresh virus risks – or paradoxically market overreaction to

vaccine should underpin spending and hiring. We forecast vaccine hopes – could spur the Fed to additional action, such

growth of 4.6% in 2021, (the market consensus is 3.8%1), as buying more assets, buying longer maturities, or injecting

slowing to 3.7% in 2022 (consensus 2.9%) as a gridlocked more liquidity. However, on balance we consider the Fed

government fails to enact long-term fiscal support. most likely to continue to accumulate assets at the

extraordinary pace of $120bn per month (Exhibit 4).

Exhibit 3: Level of US GDP

Exhibit 4: Fed’s balance sheet to continue to support

Source: Bureau of Economic Analysis (BEA) and AXA IM Research, Nov 2020

Although we forecast the fastest consecutive growth rates Source: Bloomberg and AXA IM Research, Nov 19

for over 20 years, this follows an expected fall of 3.4% in

2020. Exhibit 3 illustrates the impact on the level of activity. The Fed has also made changes to its reaction function,

We do not forecast the US regaining its previous trend even shifting to an average inflation target, and introducing

as we look out to 2023. That said, the 2016 to 2019 trend forward guidance based on full employment-consistent

likely exceeded long-term economic potential. We expect the labour conditions and PCE inflation at target and expected to

US to close its output gap by the end of 2023. overshoot. It remains to be seen how the Fed will interpret

these conditions, with broad scope for discretion. However,

This persistent shortfall should leave labour market with the output gap expected to close only by end-2023, we

conditions loose over the coming two years. Unemployment do not consider PCE inflation likely to be above target much

has recovered quicker than we anticipated, standing at 6.9% before then, while our current labour market projections

in October, although we fear little progress over the coming suggest full employment conditions only in 2024. As such, we

months. Moreover, economic participation remains 1.7ppt do not expect a change in the Fed Funds Rate until 2024.

below its level at the start of 2020. As the economy recovers

in 2021, we expect job growth and participation to rise - Yet the Fed has offered no guidance around its balance sheet

particularly if a vaccine aids recovery in the labour-intensive policy. With an expected softer start to 2021, we expect the

service sector. However, we see unemployment only below Fed to be cautious and continue to provide balance sheet

6% at the end of next year and to average 5.2% in 2022. expansion at the current pace throughout 2021. We would

expect the Fed to warn of reduced operations later next year

Inflation should rise gradually in 2021. It has been firmer than and spend most of 2022 tapering its QE programme, with

expected recently, with demand for goods rising quickly and increases in 2023 only reflecting the gentle rise of Fed

a sharp fall the dollar. While this may reverse a little over the liabilities. However, any materialisation of upside risks on

winter, base effects look set to push CPI inflation to over 2% activity associated with a vaccine could see the Fed bringing

by mid-2021. However, despite rising activity, excess supply forward such a tapering into the second half of next year.

should keep downward pressure on prices. We forecast

inflation to average 1.3% in 2020, 1.8% in 2021 and 2.2% for

1

Bloomberg, Nov 2020.

8

Eurozone – It’s not over yet

By Apolline Menut

Eurozone consumer confidence had plateaued over the summer

Key points and edged down in October even before stringent restrictions

were announced. Although the labour market impact has been

• Good news on the search for a coronavirus vaccine is largely cushioned by short-time working schemes, the number

unlikely to change the macro trajectory before mid- of unemployed has increased by 15% since February and there

2021 – we expect a weak end to 2020 and a shallow are multiple signals of a job-poor recovery: employment fell by

recovery in the first half of next year. 2%yoy in Q3 and firms hiring intentions are down in both the

• But by providing a horizon to normal sanitary services and industry sectors. In this context, precautionary

conditions, it should help governments to opt for savings should remain elevated in the months ahead, capping

more generous stimulus: deficits will remain large. household spending.

• The ECB will make sure it does not really matter:

implicit yield curve control is on the way. This will Exhibit 5: One aspect of internal divergence

require flexibility. Discussions on the limits won’t be

easy though and should be seen in the broader

context of revamping Brussels fiscal rulebook.

•

2020 not ending fast enough

For Eurozone economies, 2020 cannot end soon enough. After a

15.1% decline in the first half of the year and a strong, but partial,

rebound in the Q3, the euro area economy is set to contract again

in Q4 (-4.1%qoq). The autumn lockdowns triggered by the

pandemic’s second wave are less restrictive than in the spring

(schools, the public sector and industry remain open this time), Source: Datastream and AXA IM Research, as of 16/11/20

and so is our assumption of activity hit (-10% in November on

The flipside is that corporates will continue to see demand as

average for the euro area versus around -25% in April). But

a key factor limiting production. Once again, this comes while

the euro area will finish the year 8.3 percentage points (ppt)

activity levels have not fully recovered from the first wave.

below end-2019 levels and with large dispersion across

Even in the less affected industry sector, the capacity

countries. Virus developments, stringency of restrictions,

utilisation rate is still 6% below its pre-crisis level – it has

exposures to the most affected sectors (Exhibit 5) and fiscal

barely improved from a record low in the services sector.

supports vary across countries. For that reason, we see

Despite the help from short-time working schemes, profits

German growth shrinking by “only” 6%yoy in 2020, half of

have been squeezed, credit risks are piling up – banks have

the contraction we expect in Spain, and much better than the

tightened credit standards on corporate loans already and

7.7% decline we project for the euro area as a whole.

expect further tightening in Q4 – and debt has risen sharply.

This is not conducive to stronger investment, even without

A vaccine will boost growth in the second half mentioning the risks of rising bankruptcies. So far, these have

been suppressed by temporary regulatory forbearances, but

We expect a shallow recovery in the first half of 2021. The news demand may not pick up quickly enough to avoid them.

of a vaccine from Pfizer and Moderna is positive, helping dispel

concerns that the lockdown/re-opening pattern and its persistent The broad deployment of a vaccine should allow for a full

damage to trend growth would be permanent. Yet its near-term unwinding of containment measures, leading to some growth

growth impact should be limited in our view – production acceleration in the second half of 2021. A supportive external

and distribution capacity constraints suggest herd immunity environment will add to a significant bounce-back of the domestic

may not be reached before the summer. In the meantime, hospitality sector. Household consumption (precautionary

we think governments will keep in mind a key lesson of the savings to be unleashed) and exports (rising tourism) should fuel

summer experience: in an imperfect testing/tracing the recovery, but an investment rebound is likely to be capped

environment, restrictions must be lifted gradually. by the debt legacy. In Q4 2021, we see euro area private

consumption just 3.2% below its pre-COVID-19 level, but

Despite a potentially positive confidence boost from the investment still 8.1% lower. Overall, the Eurozone should round

vaccine, countries have entered their second wave on a weak off the year with 3.7% annual growth, followed by another solid

footing, having managed only partial repair from the first.

9

4.4% in 2022. Still, the economy would only be back to its these damage control measures to be extended well into Q1

pre-pandemic level at the end of our forecast horizon (Exhibit 6). and could even spur some proper demand stimulus. One

obvious consequence is that 2021 deficits – and debt – will

Exhibit 6: A long time to come back to square one be larger than planned in the Budgets sent to the European

Commission in mid-October. We think the European Central

Bank (ECB) will make sure this has no adverse impact.

The ECB – in it for the long haul

ECB support during the first phase of the pandemic has been

prompt and swift, ensuring easy financing conditions and

reducing fragmentation. More is coming in December to face

the second wave. At the ECB Forum on central banking,

President Christine Lagarde suggested that the Pandemic

Emergency Purchase Programme (PEPP) and the Targeted

Source: Datastream and AXA IM Research, as of 16/11/20 Longer-Term Refinancing Operations (TLTROs) will remain the

tools of choice. We expect a top-up of the PEPP by €500bn

Enabling “last mile” policy support in the first half with an extension until end-2021, with reinvestments until

of 2021 end-2023, and more generous TLTROs, with a longer discount

period until end-2021 at least, and potentially a lower dual rate.

If we think the vaccine boost to growth will be limited in the

near term, we nonetheless believe it will have a strong and But beyond the short-term monetary policy hints, Lagarde

early impact on economic policies. The perspective of seized the opportunity of the ECB Forum to explicitly unveil a

restoring normal conditions at some point in the second half strategic shift, which to some extent pre-empts the conclusions

of 2021 should make policymakers more generous with their of the review which has barely started (and where we expect

stimulus. Indeed, if the first half of the year is the “last mile”, symmetric inflation target and some implicit form of average

then fiscal authorities should be less worried about the risks inflation targeting). By saying that “monetary policy has to

of an endless drift in public debt and take the risk of minimise any ‘crowding-out’ effects” of fiscal policy, she is de

providing more support in the months ahead. facto engaging the ECB in an implicit yield curve control. This

means that a relaxed approach to the ECB limits should be

This would be particularly relevant for Spain, which has here to stay. Indeed, the central bank can hardly tell

adopted a slightly more hesitant fiscal approach so far. governments “we have your back” and then withdraw

Indeed, fiscal stimulus in 2020 has been broadly similar support because their holdings of sovereign bonds have

across countries at around 4.5 to 5.5% of GDP, but the GDP reached a certain level. In the near term, this has only limited

loss, as discussed above, has not – meaning that Germany implications – flexibility is embedded in PEPP, and an

has done relatively more, and moved earlier, than Spain to extension until end-2021 seems (almost) a done deal.

repair its economy. For 2021, Spain is betting heavily on the

Next Generation EU package funds (€27bn), but disbursement Yet things might get a bit bumpy towards the end of 2021. By

will not happen before the second part of the year and will that time, as per our baseline the euro area will no longer be

only peak in 2024. On a side note, we remain constructive on in a proper “state of emergency”. Maintaining PEPP beyond

the resolution of the rule of law standoff: the economic – and such point would be difficult to justify. True, inflation would

probably geopolitical – pain for Poland and Hungary would be still be below target at 1.5% as per the ECB’s latest forecasts –

too significant for them to actually veto the EU budget. artificially boosted by upward base effects due to the reversal of

the German Value-Added Tax rate cut. This alone would mean

Germany, France and Italy did not wait for the vaccine to the monetary policy stance will have to remain accommodative.

boost their fiscal responses. Renewed lockdown pushed Fiscal policy will also probably need to remain supportive, as

France to shift its fiscal cliffs, extending short-time work and output gaps would still be significantly negative. This should call

state loans guarantees schemes. In addition, the quantum of for boosting the ECB’s “ordinary” quantitative easing programme,

help to enterprises has increased. Germany announced a the Asset Purchase Programme (APP). A fiscally-supportive

€10bn support package to pay 70 to 75% of revenue losses to German government (with general elections in September

businesses directly affected by the November lockdown and 2021) and the Recovery and Resilience Fund – which offers

an extension of the bridge-funding fixed-cost grants for another pool from which the ECB will be able to buy – might

business until mid-2021. In France, eligibility for the solidarity help to buy time before the APP limits bind. Still, the market

fund payments has been eased and payments are being more may question the credibility of APP if the ECB fails to explicitly

generous than in the spring. The same is true in Italy, with a tackle the “limits” issue. Cooperation between monetary and

€8bn package. We believe the vaccine will make it easier for fiscal policy needs mutual trust, and that’s why discussions in

Brussels on the fiscal rulebook will be key to monitor.

10UK – Winter outbreak and Brexit to delay 2021 recovery

By David Page

The UK will complete Brexit this year. At the time of writing,

Key points the UK and EU were yet to agree a post-transition trade deal,

although we expect one soon. This would avoid further

• The virus has left a 10% hole in UK output – and a separation costs and allow wider agreements, including

winter outbreak and Brexit disruption could dampen equivalence for some financial services. Yet any agreement

any rebound over the coming quarters would be a bare-bones deal and estimates suggest that even

• An easing of restrictions and a vaccine should lift a comprehensive deal would cost the UK 4.9ppt of GDP,

growth by 4.6% in 2021 and 6.5% in 2022 compared to 7.6ppt in the event of no deal2. Around 5% of

• Policy support will remain important. We expect a British business reports being fully prepared for new trading

fiscal stimulus package next year and more QE from conditions3. We expect disruption at ports to block exports,

the Bank of England, although on balance we do not build inventory and curtail production. The UK exports

expect negative interest rates around 9.5% of GDP in goods to the EU in a normal year, so

costs could be high. A ‘no deal’ outcome would be worse and

could lower GDP growth by a further 1ppt in 2021.

Pandemic leaves devastating gap

We are cautious in our outlook for growth in early 2021 and

The pandemic saw GDP contract by 19.8% in Q2 – the sharpest pencil in a 4.6% rise for the year as a whole – the fastest

quarterly fall on record and one of the worst worldwide. since 1997 – but this would still leave GDP 4% lower than

Despite a 15.5% rebound in Q3, output remained 9.7% below end-2019. A vaccine in H2 2021 should help recovery in 2022,

its end-2019 level. The return to national lockdown in Q4 – when we forecast 6.5% growth, leading activity to regain

albeit shorter and less intense than before – looks likely to end-2019 levels by end-2022. With supply capacity still rising,

see a further drop in GDP by year-end. We forecast GDP at - even then we would forecast excess supply. However,

11.2% in 2020. Exhibit 7 illustrates how this compares with permanent losses associated with Brexit and scarring from

previous recessions. the pandemic should see the output gap close in 2024.

Exhibit 7: GDP comparison with prior recessions Spare capacity is likely to be most obvious in the labour

market. The furlough scheme has supported the economy

and unemployment has only risen to 4.8% to date. However,

it has also disguised the amount of labour market slack and

with the scheme extended until March, this will continue into

next year. For now, we expect unemployment to reach 7.5%

around mid-2021 and retreat to 5% by end-2022.

The extension of the furlough scheme and other support

measures will be key to ensuring a pick-up post-lockdown.

Yet to drive recovery, a medium-term package of growth-

enhancing measures is likely to be necessary. We expect a

material fiscal easing in next year’s Budget. Yet with a deficit

Source: National Statistics, AXA IM Research, Nov 2020 approaching 20% of GDP and debt exceeding 100%, the

Treasury will also consider longer-term consolidation.

We predict a rebound in 2021. With lockdown ending in

December, 2021 should see an initial strong rebound, but we

The Bank of England (BoE) will also provide support.

are mindful of risks. While there are glimmers of hope that

Following a further £150bn of QE in November, the BoE

new virus cases are slowing, restrictions will not be fully

forecasts inflation at 2% from mid-2021. We consider only a

removed in December and renewed deterioration is possible

brief rebound and inflation to average 1.5% in 2022. Further

in January. We expect mass vaccination from around mid-

stimulus looks necessary to return inflation to target. We

2021, offering the prospect of an economic boost later in the

expect more QE, with a further £75bn in Q2 2021, extending

year. While distribution prospects are daunting, demand for a

purchases into 2022. Yet we doubt the merits of negative

vaccine appears high. Earlier inoculation of vulnerable and

rates and do not expect the BoE to experiment with them as

essential workers should also provide economic protection

the foundations for recovery take shape from mid-2021.

against a renewed pick-up in virus cases.

2 3

“EU Exit: Long-term economic analysis”, HM Treasury, Nov 2018 Monetary Policy Report, Bank of England, Nov 2020,

11Once the pandemic is over, Japan may leverage on some tailwinds

By Hugo Le Damany

substantially. On the other, Japan is likely to accelerate into

Key points digitalisation with a ¥15tn plan included in the 1st supplementary

budget, while 2021 budget should contain tax incentives. In

• Japan hasn’t been as badly exposed to COVID-19 as addition, PM Suga would like to endow Japan with a plan to reach

other countries and significant support from the carbon neutrality by 2050. It is too soon for concrete figures, but

government and the Bank of Japan make it more the country may see large stimulus in sectors such as energy,

resilient. Some restrictions may return in the coming transport and housing. On trade, we also expect a gradual

weeks, but it should be less strict than in April recovery over the coming quarters with the global economy

• Private consumption is crucial for the outlook, a high likely shifting into an expansionary phase. The greatest risk

saving rate, job market resilience and large demand could be another virus-related supply-chain disruption in the US.

stimulus should underpin this outlook

• After a -5.5% contraction in 2020, we believe GDP Overall, we expect GDP will rebound by 3% in 2021 and 2% in

should rebound by +3% in 2021 and +2% in 2021 2022 (Exhibit 8). Despite positive headlines, GDP isn’t

• expected to return to its pre-crisis level before Q2 2022.

Assuming Japan’s potential growth continues at around 0.5%,

Pandemic management remains crucial this would be 0.6ppt below potential at that time.

The short-term outlook remains constrained by the evolution

of the pandemic. Japan has been resilient so far and currently

Exhibit 8: GDP growth and contributions

only 15% of intensive care unit is occupied nationwide. The

number of new cases is rising but we believe Japan will be

able to cope with a resurgence of the pandemic without

having to impose strict restrictions. Large and coordinated

support from the government and the Bank of Japan (BoJ)

has been, and will remain, crucial4. For the time being, retail

sales are getting back to pre-crisis levels, but the service

sector is still suffering, while industrial production has

recovered only half of its loss. In addition, following the

strong recovery in China and bigger auto demand in the US,

exports currently stand at -5% of 2019’s level.

Source: Cabinet Office and AXA IM Research, as of 18/11/2020

Private consumption is likely to drive Japan’s recovery. Last year’s

sales tax hike and the pandemic have distorted consumer Falling inflation could increase BoJ discomfort

behaviour, but some tailwinds may facilitate the rebound.

In the short term, CPI inflation should weaken further,

Income has been largely preserved thanks to various fiscal

depressed by a sharp decrease in the output gap and the

support from the Employment Adjustment Subsidy Programme

impact of some measures such as the “Go to” campaign, and

as well as cash handouts to households and SMEs5.

a likely lowering of mobile phone charges. Consequently, CPI

Consequently, both precautionary and forced savings have

should decline to -0.2% in 2021 and only rise to 0.1% in 2022.

risen, pushing the saving rate to an unprecedented 25% of

disposable income. The job market has also been resilient

In this context, the BoJ will face additional calls for more

with unemployment rising by only 0.6 percentage points (ppt) to

accommodative policy. There is still leeway on its special

3%, while job offers per applicant remains at one. Finally, a

programme to support corporate financing and we believe that

third supplementary budget of ¥7tn is likely to stimulate

this should be extended until Q3 2021, as long as the demand

demand in Q1 2021. The “Go to” campaign, offering discounts

exists. In parallel, the BoJ will continue to flexibly adjust its JGB

on domestic travel should be extended through 2021 and

purchases, facilitating the additional issuance by the government.

cash handouts should be granted to low income households.

The BoJ will be keen to avoid taking rates deeper into negative

territory, considering the possibility of further stress on the

In terms of investment, the outlook is more mixed. On one side,

financial system. Finally, if the yen appreciates beyond the

the capital stock has not been destroyed and production –

implicit ¥100/USD threshold, the BoJ may face a difficult decision.

related investments should be muted until demand accelerates

4 Le Damany, H., “Japan’s COVID-19 response: Crisis met with strong economic 5 Le Damany, H., “COVID-19, economic stimulus and monetary policy... How is Japan

package, but is it enough?” – June 2020 responding to the crisis?“ – May 2020

12China – Back to normal

By Aidan Yao

developing COVID-19 vaccines. It has three treatments in

Key points phase three clinical trials, with the general expectation that

at least one will be made available by the end of this year,

• Normalising virus conditions, official policies and the before a mass rollout in 2021. A safe and effective vaccine

natural economy will shape the 2021-2022 outlook will help to further boost public confidence against the virus

• After effectively containing the virus, any lingering and accelerate social and economic normalisation.

impact of COVID-19 will likely come from offshore

• Reviving natural growth will take over from policy Given China’s advanced position in fighting the pandemic, we

easing to drive the economy further to normality think that any further impact of COVID-19 will likely come

more from offshore than within the country. As many of its

trading partners are still mired in the pandemic and having to

Rollercoaster ride coming to an end re-engage in lockdowns, China could face reduced demand

for its regular exports in the near-term. However, demand for

2020 will go down in history as one of the most challenging medical-related products will likely remain strong, as will

years for the global economy since the Second World War. A shipments of electronic goods due to a large number of

major public health crisis, triggered by a deadly infectious people continuing to work from home. Surging sales of these

virus, quickly turned into economic disaster as governments products, which make up 31% of total exports in 2019, have

around the world took drastic measures to restrict social helped to save China from a severe export contraction.

mobility and close large portions of economies. At the initial

epicentre of the pandemic, China implemented the strictest However, if instead the virus outlook improves following the

lockdown of all and saw its economy suffer from a sudden introduction of a vaccine, normal exports look set to be

stop. Fortunately, the sacrifice was not in vain. The draconian buoyed by recovering global demand, albeit at the expense

response proved effective in containing the virus and the of lower sales of pandemic-related goods. China’s well-

pandemic quickly eased. A swift restart of the economy, diversified production base has therefore created a “hedge”

propelled by significant policy easing, has led to a powerful for its exports against various paths of the pandemic.

rebound in economic activities, which is set to make China

the only major economy to record positive full-year growth in Besides the virus, we expect the US-China trade tensions to

2020. de-escalate under a Biden administration, with no more tariff

increases next year. However, the bar for rolling back existing

Looking ahead, the 2021 macro outlook will likely feature a tariffs is also high and will likely require China to make

further normalisation of the economy, the pandemic and concessions in other areas, such as technology, where

official policies. Some of these normalisations – a firmer competition for leadership will remain intense.

control of the virus and restoring organic growth engines –

will add to our growth forecast, while normalising policies Exhibit 9: Economy regains lost ground

that lead to reduced stimulus will subtract from it. We will

examine each in turn.

COVID can still hurt via trade

As the dominant economic driver of 2020, the coronavirus

pandemic has not yet been contained globally. Europe is

currently in the midst of a second wave of the pandemic,

while the US is confronting a virus resurgence without ever

exiting the first wave. China has fared much better in keeping

the pandemic under control. While there have been some

small “aftershocks” since the initial outbreak, the

comprehensive official and public responses – consisting of Source: Bloomberg, CEIC and AXA IM Research, as of 12/11/2020

rapid detention, efficient trace and tracking, widespread

testing, strict quarantine, and sometimes mandatory mask- Policy normalisation to shape growth outlook

wearing and social distancing – have proven effective in

keeping infection numbers significantly below those in the US While the pandemic was responsible for the initial

and Europe. In addition, China is leading the race in contraction in the economy, the subsequent rebound would

13not been possible without Beijing’s forceful interventions. Importantly, the most recent leg of this recovery has

Powerful monetary and fiscal stimuli were deployed to keep occurred despite reduced policy easing by the PBoC and

businesses afloat and employees on payroll during the height slower growth in infrastructure investment. These are signs

of the COVID-19 crisis. Once the pandemic was brought that natural, rather than policy-driven, growth has started to

under control, policy easing also played a vital role in take over as the dominant force behind the recovery.

facilitating factory reopening and work resumption. Despite

being less expansionary than that of many others, China’s Despite the impressive headline performance, it is important

stimulus seems to have worked better because its economic to note that China’s recovery has been uneven across the

rescue came after an effective containment of the virus. different sectors. Exhibit 10 shows that while exports and

industrial outputs have been quick to get back on their feet,

As economic order is gradually restored, Beijing has started private consumption has lagged behind due to a sluggish

to exit its ultra-accommodative policies. The People’s Bank of labour market and limited official support to shore up

China (PBoC) has turned more prudent with liquidity household purchasing power. Encouragingly, both job market

injections lately and refrained from using high-profile policy conditions and consumer spending have improved in recent

tools, such as reserve requirement ratio and interest rate months. A further normalisation in these activities is

cuts. This, coupled with better economic data, has led to a expected to create a more balanced macro base from which

rise in onshore bond yields back to their pre-COVID levels. Beijing can neutralise policies over time.

With the price of money back to neutral, the quantity of

money – credit and money supply – is expected to follow suit. Exhibit 10: Recovery is strong but uneven

This should lead to a gradual convergence in credit and

nominal GDP growth in 2021, and a stabilisation in the

aggregate debt ratio as a result. While the PBoC appears in

no hurry to tighten policy due to muted inflation, targeted

risk controls for some sectors, such as property, could be

stepped up against rising financial imbalances.

Fiscal policy is also heading back to normality. Beijing will

likely start by removing some of the emergency measures put

in place during the pandemic, such as lowering the fiscal

deficit back to around 3% of GDP and eliminating central

government special bond issuance. The withdrawal of

stimulus will likely be more gradual and data-dependent than

Source: CEIC and AXA IM Research, as of 12/11/2020

monetary policy, to ensure that some supports remain in

place to buffer the economy against lingering headwinds. Putting all the moving parts together, we expect China’s

annual growth to accelerate meaningfully to 8% in 2021 from

We also note that 2021 will be the first year of China’s 14th 2.3% this year. However, it is worth noting that nearly half of

Five-Year Plan, where a zealous official response to some this increase will be due to base effects. In level terms, GDP is

initiatives – such as new urbanisation, technology upgrades projected to be moderately below the pre-COVID trend at

and supply-chain enhancement – could raise fiscal spending, the end of 2021. This gap is forecast to close in 2022 when

offsetting some of the impact from exiting cyclical stimulus. growth reverts back to its trend rate of 5.5% without the

Overall, we expect the normalisation of monetary and fiscal base effect distortion.

policies to lend less support to the economy in 2021.

Risks are substantial but balanced

Natural growth to take over

Overall, our forecast projects an economy that is on path to

The anticipated withdrawal of policy accommodation will be normality, but not quite getting there until 2022. All three

supported by a restoration of organic economic growth. The macro forces – the virus, policy operation, and the natural

strong rebound in GDP growth since Q1 2020 was an economy – could deviate from our expectations and cause

indication that the economy has started to heal after the upside or downside surprises to the forecast. Given our base

devastating COVID-19 shock. Many third-party indicators, case has already taken into consideration some factors that

such as measures of mobility, traffic congestion, restaurant could slow the economic normalisation process – due to

orders and e-commerce sales, have largely returned to pre- reduced policy support, an uneven domestic recovery and

pandemic levels. Our proprietary economic cycle indicator sub-trend growth in China’s trading partners – the risk profile

has also rebounded strongly from the bottom and suggests around our forecast is therefore broadly balanced. However,

the economy is now within striking distance of trend growth the range of all possible economic outcomes remains wider

(Exhibit 9). than usual, reflecting the still-elevated macro uncertainties.

14You can also read