MACROECONOMIC PROJECTIONS FOR SPAIN 2022-2024 - ÁNGEL GAVILÁN Director General Economics, Statistics and Research - Banco de ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MACROECONOMIC PROJECTIONS FOR SPAIN 2022-2024 ÁNGEL GAVILÁN Director General Economics, Statistics and Research Madrid 5 April 2022 DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA

CONTENTS

1. Overview

2. Developments in economic activity in the short term

3. Economic projections for the Spanish economy for 2022-2024

4. Main risks and sensitivity exercises

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 2

ÍNDICE

1. Overview

2. Developments in economic activity in the short term

3. Projections for the Spanish economy for 2022-2024

4. Main risks and sensitivity exercises

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 3

THE SPANISH ECONOMIC OUTLOOK IN THE SHORT AND MEDIUM TERM IS HEAVILY INFLUENCED BY THE

RUSSIAN INVASION OF UKRAINE

• National Accounts: data better than expected

Until the outbreak of the armed conflict in

• The Omicron variant had a smaller impact on activity than

Ukraine: activity posted upside surprises, as

previous waves of the pandemic

did inflation

• Initial signs of an easing of bottlenecks

• Sharp rise in commodity prices

The war in Ukraine: a considerable negative

• Sanctions against Russia and decline in trade flows

shock when the recovery from the health crisis

• Negative impact on agents’ confidence and financial

was still incomplete

dynamics

New macroeconomic projections: the • GDP is revised downwards in 2022 and 2023, and upwards

extraordinary uncertainty as to the duration in 2024

and intensity of the conflict makes it • Inflation is revised sharply upwards in 2022, although a

impossible to assess its precise implications gradual moderation is projected in the medium term

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 4

CONTENTS

1. Overview

2. Developments in economic activity in the short term

3. Projections for the Spanish economy for 2022-2024

4. Main risks and sensitivity exercises

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 5POSITIVE SURPRISES IN NATIONAL ACCOUNTS DATA WITH RESPECT TO THE BANCO DE ESPAÑA’S DECEMBER

PROJECTIONS

REAL GDP (quarter-on-quarter rates) QUARTER-ON-QUARTER GDP GROWTH (%) AND QUARTER-ON-QUARTER RATES

CONTRIBUTIONS (pp)

% and pp %

%

3.0 3.0 8 7.2

2.6

2.5 6

2.2 4.6 4.5

2.0 2.2

2.0 4

1.6

2.0

1.5 2 1.4 1.3

1.1 1.1 1.6

1.0 0

1.2 1.2

0.5 1.0 -2 -1.6 -1.5

1.0

0.0 -4

0.3

-0.5 -6

-0.5

-0.6

-1.0 0.0 -8

Mar-21 Jun-21 Sep-21 Dec-21 GDP Domestic demand Net external Private Gov. Invest. Housing Other Exports Imports

demand cons. cons. in capital invest. constr.

goods Invest.

3.0 1.6 2.2 1.2 1.2 0.3 1.0

2.0

1.0

0.0 BANCO DE ESPAÑA PROJECTIONS DEC-21 QNA 2021 Q4

GDP Domestic demand Net external demand

SOURCES: Banco de España and INE.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 6THE SPREAD OF THE OMICRON VARIANT AT THE END OF 2021 AND BEGINNING OF 2022 AFFECTED ACTIVITY

DEVELOPMENTS, BUT THE HIGH VACCINATION RATE LIMITED ITS IMPACT

COVID-19 IN SPAIN FULLY VACCINATED POPULATION INTERNATIONAL AIR PASSENGERS BY COUNTRY

(percentages of figures for same dates in 2019)

New cases per 100,000 New deaths per 100,000 % total population

inhabitants (14-day total) Percentage of levels in 2019

inhabitants (14-day total) 100

4,500 25 90

90 82.7

4,000 80

20 80 67.9

3,500 70 67.7

70 62.9

3,000 60

15 60 50

2,500

50 40

2,000

10 40 30

1,500

30 20

1,000 5 20 10

500

10 0

Nov-21

Apr-21

Mar-21

Jul-21

May-21

Jan-21

Jan-22

Oct-21

Feb-21

Feb-22

Dec-21

Sep-21

Aug-21

Jun-21

0 0 0

SPAIN FRANCE GERMANY FRANCE UNITED KINGDOM ITALY

14- DAY CUMULATIVE INCIDENCE

ITALY GERMANY

UNITED KINGDOM

14 DAY CUMULATIVE DEATHS (right hand scale)

SOURCES: Our World in Data and AENA.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 7IN THE FINAL STRETCH OF 2021 AND EARLY 2022, THERE WERE SIGNS OF MODERATION IN THE BOTTLENECKS.

THE WAR AND THE FRESH OUTBREAKS OF COVID-19 IN CHINA HAVE REVERSED THIS TREND

MARITIME TRANSPORT

COVID-19 at

SUPPLIERS’ DELIVERY TIMES INCIDENCE OF COVID-19 IN CHINA

End of Suez

z-scores Canal Chinese ports Index

blockage Daily new cases

5 70

8,000

4 60

7,000

3 50

More 6,000

2 congestion 40

5,000

1 30

4,000

0 20

3,000

-1 10 Increase in delivery times

-2 2,000

0

-3 1,000

ene.-21 abr.-21 jul.-21 oct.-21 ene.-22

0

2020 2021 2022

SPAIN GERMANY FRANCE ITALY

COMPOSITE INDICATOR OF MARITIME TRAFFIC

COMPOSITE INDICATOR OF TRANSPORT PRICES

SOURCES: IHS Markit, Johns Hopkins University and Banco de España.

a) An increase in the indicators denotes greater congestion in sea ports. The composite indicator of maritime traffic is the main component of the indicators of container traffic in the Suez Canal and of

wait times at four US and Chinese ports. The composite indicator of transport prices is the main component of prices of Baltic Dry Index, Harpex Global and container traffic between Asia and the

United States and between Asia and Europe.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 8COMMODITY PRICES REMAINED ON AN UPWARD PATH OVER THE QUARTER, SURGING AT THE START OF THE

ARMED CONFLICT IN UKRAINE, BUT MODERATING RECENTLY

OIL PRICES MIBGAS INDEX FOR SPAIN (a) COMMODITY PRICES (S&P)

$ per barrel €/MWh 04/01/21 = 100

150 250 260

140

230

130 200

120 200

150

110

170

100

100

90 140

80 50

110

70

60 0 80

TOTAL AGRICULTURE ENERGY METALS

SOURCES: Refinitiv and Mibgas.

(a) The MIBGAS index is the weighted average price for all gas transactions carried out on the same day at all the Trading Sessions for Spain.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 9IN RECENT MONTHS INFLATION HAS CONTINUED TO ACCELERATE, MAINLY OWING TO ENERGY AND FOOD, BUT

ALSO TO THE INCREASE IN UNDERLYING INFLATION

HEADLINE HICP UNDERLYING INFLATION MEASURES OVERALL INDEX EXCLUDING ENERGY AND FOOD

(percentage of items in each growth range)

% y-o-y and pp % y-o-y

10 4,0 %

9 3,5 100

8

3,0

7

2,5 80

6

5 2,0

4 60

1,5

3

2 1,0

1 40

0,5

0

0,0

-1 20

-2 -0,5

-3 -1,0

2019 2020 2021 2022 2019 2020 2021 2022 0

Jan-19

Apr-19

Oct-19

Jan-20

Apr-20

Oct-20

Jan-21

Apr-21

Oct-21

Jan-22

Jul-19

Jul-20

Jul-21

ENERGY (excl. electricity) ELECTRICITY HICP EXCL. ENERGY AND FOOD

UNDERLYING EXCL. TOURISM AND CLOTHING

HICP EXCL. ENERY AND FOOD FOOD TRIMMED MEAN AT 10%

HICP TRIMMED MEAN AT 30%

MEDIAN 4

SOURCES: INE, Eurostat and Banco de España. Latest observation: February 2022 (March 2022 flash estimate for the HICP).

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 10HIGH VOLATILITY IN THE FINANCIAL MARKETS, OWING TO THE WAR AND THE CHANGES IN EXPECTATIONS OF

THE MONETARY POLICY RESPONSE TO INFLATION, ALTHOUGH WITHOUT HIGHLY DISRUPTIVE EPISODES

STOCK MARKET INDICES SOVEREIGN SPREADS IN THE EURO AREA INTEREST RATES ON 10-YEAR SOVEREIGN DEBT

31.12.2021 = 100 pp %

104 180 2,4

Ukraine invasion

160

100 2,0

140

1,6

96 120

1,2

100

92

80 0,8

88 60 0,4

40

84 0,0

20

-0,4

80 0

Jan-21

Feb-21

Apr-21

Jul-21

Aug-21

Sep-21

Dec-21

Oct-21

Nov-21

Jan-22

Feb-22

Mar-21

Mar-22

Jun-21

May-21

Jan-22 Feb-22 Mar-22

-0,8

Dec-21

Apr-21

Jan-21

Feb-21

Jul-21

Aug-21

Sep-21

Nov-21

Oct-21

Jan-22

Feb-22

Mar-21

Mar-22

May-21

Jun-21

S&P 500 EURO STOXX 50 FTSE 250 IBEX 35

ITALY PORTUGAL FRANCE SPAIN

GERMANY UNITED STATES

SPAIN UNITED KINGDOM

SOURCE: Refinitiv Datastream. Latest observation: March 31.

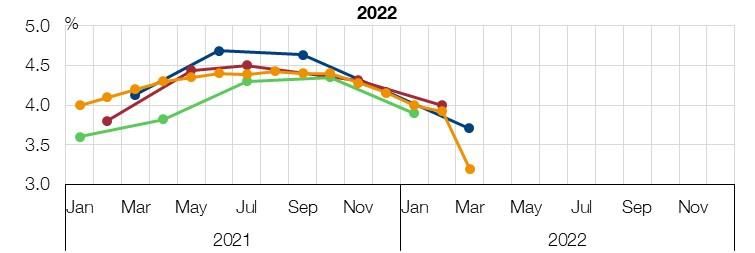

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 11FINANCING TERMS AND CONDITIONS TIGHTENED SLIGHTLY, IN A SETTING IN WHICH NEW LENDING TO

ENTERPRISES AND TO HOUSEHOLDS FOR HOUSE PURCHASE SHOWED GREATER MOMENTUM

FINANCING COSTS BLS: CHANGE IN CREDIT STANDARDS (a) NEW LENDING

% %

3,0 7,5 %

50

2019 average = 100

2,5 7,0 180

40

160

TIGHTENING

2,0 6,5

30

1,5 6,0 140

20

1,0 5,5 120

10

0,5 5,0 100

0 80

0,0 4,5

-10 60

-0,5 4,0

EASING

-20 40

-1,0 3,5

2019 2020 2021 2022

-30 20

HOUSE PURCHASE 2019 2020 2021 2022 2020 2021 2022

12M EURIBOR HOUSE PURCHASE HOUSE PURCHASE

NFCs, UP TO €1 MILLION FORECAST

CONSUMER CREDIT AND OTHER LENDING CONSUMER CREDIT

NFCs, OVER €1 MILLION FORECAST NFCs, UP TO €1 MILLION

LONG-TERM DEBT SECURITIES SMEs

FORECAST NFCs, OVER €1 MILLION

CONSUMER CREDIT (r-h scale) LARGE FIRMS SOLE PROPRIETORS

FORECAST

GROSS ISSUANCE OF DEBT SECURITIES

SOURCES: Banco de España and Refinitiv Datastream. Latest observation: February (financing costs and new lending), March (EURIBOR) and 2021 Q4 (credit standards).

a. Indicator = percentage of banks that have tightened their credit standards considerably × 1 + percentage of banks that have tightened their credit standards somewhat × 1/2 – percentage of banks that

have eased their credit standards somewhat × 1/2 – percentage of banks that have eased their credit standards considerably × 1.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 12THE WAR INTERRUPTED THE IMPROVEMENT OBSERVED AT THE BEGINNING OF THE QUARTER IN THE

CONFIDENCE INDICATORS

PURCHASING MANAGERS’ INDEXES CONFIDENCE INDICATORS

Index Index

Index

70 40 120

65 30 115

60

20 110

55

50 10 105

45

0 100

40

35 -10 95

30 -20 90

25

20 -30 85

15 -40 80

10

5 -50 75

0 -60 70

CONSUMERS

INDUSTRY

MANUFACTURING PMI. OUTPUT

SERVICES

SERVICES PMI. ACTIVITY

ECONOMIC SENTIMENT INDICATOR (r-h scale)

SOURCES: IHS Markit and European Commission.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 13EMPLOYMENT CONTINUED TO GROW IN Q1, ALTHOUGH AT A LOWER RATE THAN IN PREVIOUS QUARTERS

CHANGE IN TOTAL AND ACTUAL SOCIAL SECURITY REGISTRATIONS QUARTERLY CHANGE IN ACTUAL SOCIAL SECURITY

AND IN FURLOUGHED EMPLOYEES VERSUS FEBRUARY 2020 (a) REGISTRATIONS AND CONTRIBUTION OF TOTAL REGISTRATIONS

AND OF FURLOUGHED EMPLOYEES (a)

% %

5 3,0

0 2,5

-5 2,0

-10 1,5

-15 1,0

-20 0,5

-25 0,0

Aug-20

Sep-20

Dec-20

Aug-21

Sep-21

Dec-21

Mar-20

Feb-21

Mar-21

Feb-22

Mar-22

Jun-20

Jun-21

May-20

May-21

Nov-20

Nov-21

Jan-21

Jan-22

Apr-20

Jul-20

Oct-20

Apr-21

Jul-21

Oct-21 -0,5

2020 Q4 2021 Q1 2021 Q2 2021 Q3 2021 Q4 2022 Q1

FURLOUGHED EMPLOYEES (ERTE)

FURLOUGHED EMPLOYEES (ERTE)

TOTAL SOCIAL SECURITY REGISTRATIONS

TOTAL SOCIAL SECURITY REGISTRATIONS

EFFECTIVE SOCIAL SECURITY REGISTRATIONS

EFFECTIVE SOCIAL SECURITY REGISTRATIONS

SOURCES: Ministerio de Inclusión, Seguridad Social y Migraciones and Banco de España. Latest observation: March 2022.

a) Seasonally adjusted series.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 14FIRMS EXPECTED THEIR TURNOVER TO SHRINK IN 2022 Q1

TURNOVER. QUARTERLY CHANGE (a) EMPLOYMENT. QUARTERLY CHANGE (a)

0,4 0,4

0,3 0,3

0,2 0,2

0,1 0,1

0,0 0,0

-0,1 -0,1

-0,2 -0,2

-0,3 -0,3

-0,4 -0,4

-0,5 -0,5

-0,6 -0,6

2020 Q4 2021 Q1 2021 Q2 2021 Q3 2021 Q4 2022 Q1 2020 Q4 2021 Q1 2021 Q2 2021 Q3 2021 Q4 2022 Q1

Nov-20 wave Feb-21 wave May-21 Aug-21 waveNov-21 wave Feb/Mar-22 Nov-20 Feb-21 May-21 Aug-21 Nov-21 Feb/Mar-22

wave wave wave wave wave wave wave wave

SOURCE: Banco de España (EBAE).

a) Index calculated as steep decrease = -2, slight decrease = -1, stable = 0, slight increase = 1, steep increase = 2.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 15GDP GROWTH FORECAST FOR Q1

QUARTER-ON-QUARTER GDP GROWTH (%)

%

3,0

2,6

2,5

2,2

2,0

1,5

1,1

1,0 0,9

0,5

0,0

-0,5

-0,5

-1,0

2021 Q1 2021 Q2 2021 Q3 2021 Q4 2022 Q1

SOURCES: Banco de España and INE.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 16CONTENTS

1. Overview

2. Developments in economic activity in the short term

3. Projections for the Spanish economy for 2022-2024

4. Main risks and sensitivity exercises

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 17THE ARMED CONFLICT IN UKRAINE AFFECTS THE OUTLOOK FOR GROWTH AND INFLATION, THROUGH VARIOUS

CHANNELS

• Increase in the price of these inputs and higher consumer price inflation

Commodities channel

• Possible supply problems

• Deterioration in global economic outlook

Trade channel

• Worsening of global value chain bottlenecks

• Postponement of consumption and investment decisions of households

Confidence/uncertainty channel and firms

• Tightening of financing conditions

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 18COMMODITIES CHANNEL: ALTHOUGH SPAIN’S RELIANCE ON RUSSIAN ENERGY IS NOT HIGH, IT HAS ALWAYS

BEEN PARTICULARLY VULNERABLE TO ENERGY SHOCKS

CHANGES IN PURCHASING POWER OWING TO

CHANGES IN ENERGY PRICES (b)

%

2

1

0

-1

-2

-3

-4

-5

Mar-19

Mar-20

Mar-21

May-19

May-20

May-21

Sep-19

Sep-20

Sep-21

Jan-19

Jan-20

Jan-21

Jan-22

Nov-19

Nov-20

Nov-21

Jul-19

Jul-20

Jul-21

EURO AREA SPAIN

SOURCES: INE, Eurostat and Banco de España.

a) Simulations based on the NiGEM model with rational expectations and exogenous monetary policy.

b) The indicator proxies the change in households’ purchasing power stemming from changes in the price of energy if their gross disposable income were to grow at the same pace as the HICP.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 19TRADE CHANNEL: SPAIN’S DIRECT EXPOSURE TO RUSSIA IS MODEST, BUT GLOBAL ECONOMIC ACTIVITY IS

ALREADY HIGHLY INTERCONNECTED. POSSIBLE WORSENING OF BOTTLENECKS

EURO AREA GDP GROWTH FORECASTS

WORLD GDP GROWTH FORECASTS

SOURCES: ECB, European Commission, IMF, Consensus Forecast and Banco de España (EBAE).

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 20CONFIDENCE/UNCERTAINTY CHANNEL: CONFIDENCE AND UNCERTAINTY INDICATORS HAVE DETERIORATED

SINCE THE START OF THE WAR, WHICH NORMALLY HAMPERS GROWTH

DENSI (CONFIDENCE) EPU (UNCERTAINTY) CONSUMER CONFIDENCE AND GDP

change change

0.0 1.8 Index %

10 10

1.6

8

-0.5 1.4 0 6

1.2 -10 4

-1.0 2

1.0

-20 0

0.8 -2

-1.5 -30

0.6 -4

0.4 -40 -6

-2.0

-8

0.2

-50 -10

ene-10

jul-10

ene-11

jul-11

ene-12

jul-12

ene-13

jul-13

ene-14

jul-14

ene-15

jul-15

ene-16

jul-16

ene-17

jul-17

ene-18

jul-18

ene-19

jul-19

ene-20

jul-20

ene-21

jul-21

ene-22

-2.5 0.0

-0.2

-3.0 -0.4

1 7 13 19 25 31 37 43 49 1 7 13 19 25 31 37 43 49 GDP. YEAR-ON-YEAR RATES (right-hand scale)

days since the start of each crisis days since the start of each crisis CONSUMER CONFIDENCE

UKRAINE CRISIS FINANCIAL CRISIS DEBT CRISIS COVID-19 CRISIS

SOURCES: Banco de España, GPR, EPU, Refinitiv, Factiva, INE and European Commission.

The DENSI and EPU indicators are built on the “economic sentiment” and “economic policy uncertainty” contained in articles published in the main Spanish newspapers. The DENSI takes into account the

difference between the number of articles containing terms that may be associated with a potential improvement and that referring to a potential worsening of economic activity in the short term, while the

EPU is based on the number of articles about the uncertainty surrounding economic policies.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 21THE WAR IN UKRAINE HAS UNLEASHED A NEW NEGATIVE SHOCK WHILE WE HAVE YET TO COMPLETE THE

RECOVERY FOLLOWING THE HEALTH CRISIS…

REAL GDP PERCENTAGE OF VULNERABLE FIRMS BASED ON THE NET DEBT / (GROSS

OPERATING PROFIT + FINANCIAL REVENUE) RATIO (a) (b)

2019 Q4 = 100 %

35

105

30

100 100,2

25

96,2

95

20

90

15

85

10

80 5

75 0

Dec-19 Dec-20 Dec-21 2019 2020 2021 2019 2020 2021 2019 2020 2021 2019 2020 2021

Total firms Sectors severely Sectors moderately Sectors largely

EURO AREA GERMANY FRANCE ITALY SPAIN affected by the health affected by the health unaffected by the

crisis crisis health crisis

SOURCES: INE and Banco de España.

a. The most vulnerable firms are defined as those whose Net financial debt / (Gross operating profit + Financial revenue) ratio is greater than 10 or which have positive net financial debt and zero or

negative earnings.

b. Sectors are defined as severely affected by the COVID-19 crisis if their sales fell by more than 15% in 2020; as moderately affected if their sales fell between 9% and 15%; other sectors are deemed to

be largely unaffected.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 22-1,6

-1,2

-0,8

-0,4

-2,0

0,0

0,4

0,8

1,2

1,6

2,0

%

Land transport

Fishing and aquaculture

Air transport

Manuf. of motor vehicles

Water transport

Wood and cork

Food, bev. and tob.

SOURCES: INE and Banco de España.

Pharmaceutical products

Electrical equipment

Construction

Agriculture

Accomm. and food serv. act.

Paper and graphic arts

DEVIATION FROM NOMINAL GVA IN 2023

Other non-metalic min.

Rubber and plastics

Water, sew., waste man.

Telecommunications

Other transport equipment

Arts, ent. and rec.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA

Furn., rep. of mach. and equip.

Public admin. and defence

Trade; rep. of motor veh.

Computer prog. and related act.

Health and social work

Publishing; cin., TV and radio

Metal prod, exc. mach. and equip

Comp., electr. and opt. prod.

a) Sectors severely affected by the COVID-19 crisis are defined as those whose turnover fell by more than 15% in 2020.

…. AND WILL AGAIN HAVE A HIGHLY UNEVEN IMPACT BY SECTOR

Manuf. of mach. and equip.

Prof. Sci. and tech. act.

Stor. and support act. for transp.

Other services

Admin. act. and anc. serv.

IMPACT OF A 25% INCREASE IN ENERGY PRICES ON NOMINAL GVA IN 2023

Education

Textiles, leather and footwear

Postal and courier act.

Financial and insurance serv.

Real estate act.

Mining of metal ores

Metallurgy

DEVIATION FROM NOMINAL GVA IN 2023 AND SECTOR SEVERELY AFFECTED BY COVID-19 (a)

Chemicals industry

Coke and refined petroleum

Mining support services

Elect., gas, steam, a/c supply

%

Extract. of petr. and natural gas

Right-hand scale

0

4

8

-8

-4

12

16

20

-16

-12

-20

23MACROECONOMIC PROJECTIONS 2022-2024

APRIL 2022 DIFFERENCE VIS-À-VIS

PROJECTIONS (a) DECEMBER PROJECTIONS

Annual rate of change (%), unless otherwise indicated 2020 2021 2022 2023 2024 2022 2023 2024

GDP -10.8 5.1 4.5 2.9 2.5 -0.9 -1.0 0.7

Harmonised index of consumer prices (HICP) -0.3 3.0 7.5 2.0 1.6 3.8 0.8 0.0

HICP excluding energy and food 0.5 0.6 2.8 1.8 1.7 1.0 0.4 0.1

Unemployment rate (% of labour force). Annual average 15.5 14.8 13.5 13.2 12.8 -0.7 0.3 0.4

General government net lending (+)/net borrowing (-) (% of GDP) -10.3 -6.9 -5.0 -5.2 -4.7 -0.2 -1.2 -1.4

General government debt (% of GDP) 120.0 118.4 112.6 112.8 113.5 -3.1 -0.9 0.0

SOURCES: Banco de España and INE.

a) Projections cut-off date: 31 March 2022.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 24GDP GROWTH IS REVISED DOWN IN 2022 AND 2023, AND UP IN 2024

GROSS DOMESTIC PRODUCT In the baseline scenario, under which there is no

(chained volume index)

2019 Q4 = 100 escalation in the armed conflict in Ukraine, the

110 war would have its largest adverse impact on

105

activity in Q2

100

95

The conflict does not prompt an appreciable

90 deterioration of potential growth: at the end of

the projections horizon, economic growth stands

85

at similar rates to those forecast in December

80

75

2019 Q4 2020 Q4 2021 Q4 2022 Q4 2023 Q4 2024 Q44

The Spanish economy’s return to pre-pandemic

APRIL 2022 DECEMBER 2021 TREND DECEMBER 2019 GDP levels is pushed back to 2023 Q3

SOURCES: Banco de España and INE.

Latest observation: 2021 Q4.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 25FACTORS BEHIND THE REVISION OF THE GDP GROWTH PATH

CHANGES IN THE GDP FORECAST IN 2022

% y-o-y and pp 2021 2022 2023 2024 % and pp

8

December 2021 forecast 4.5 5.4 3.9 1.8

7

0,2

New National Accounts data 0.6 0.8 0.0 0.0 6 0,7

0,8 6,2

5,7 0,6

5 5,4 5,4 0,5

Fiscal measures 0.0 0.2 -0.2 0.0 5,2 0,2

4 4,7 4,5 4,5

External markets and bottlenecks 0.0 -0.5 -0.3 0.1

3

Energy and inflation dynamics 0.0 -0.7 -0.7 0.5 2

Confidence and uncertainty 0.0 -0.6 0.1 0.1 1

0

Financial factors and other elements 0.0 -0.2 0.2 0.1

Accounts data

and uncertainty

December 2021

April 2022

Fiscal measures

External markets

and other elements

inflation dynamics

and bottlenecks

New National

forecast

Financial factors

Confidence

Energy and

forecast

April 2022 forecast 5.1 4.5 2.9 2.5

SOURCE: Banco de España.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 26A VERY SIGNIFICANT PORTION OF THIS GROWTH MUST BE DRIVEN BY IMPLEMENTATION OF INVESTMENT

PROJECTS UNDER THE NGEU PROGRAMME

CUMULATIVE VOLUME OF PUBLISHED RRF TENDERS (a) NGEU SPENDING ASSUMPTIONS EFFECT OF NGEU ON GDP LEVEL

(b) (RRF AND REACT-EU)

€m €m % deviation vs counterfactual

25.000 30000 2,0

25000

20.000

1,5

20000

15.000

15000 1,0

10.000

10000

0,5

5.000

5000

0 0 0,0

2021 2022 2023 2024 2021 2022 2023 2024

2,0

1,5

1,0

Tender start date 0,5

0,0

BANCO DE ESPAÑA -Dec.21 BANCO DE ESPAÑA - Apr.22

2021 2022 2023 2024

25.000 END DATE AFTER 2022

€m

-25.000 END DATE DURING 2022

END DATE DURING 2021

Tender start date

SOURCES: https://planderecuperacion.gob.es, 2022 Budgetary Plan, 2021-2024 Draft Budget, IGAE and Banco de España.

(a) Not including tenders in “forthcoming” status, those agreed without being publicised, those relating to Government guarantees or those identified as REACT-EU.

(b) Tenders published on the RTRP website to 29/03/2022 and on a cumulative monthly basis.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 27INFLATION IS REVISED UP SHARPLY IN 2022, BUT IS PROJECTED TO MODERATE GRADUALLY OVER THE MEDIUM

TERM

HEADLINE HICP HICP EXCLUDING FOOD AND ENERGY

% y-o-y % y-o-y

10,0 3,5

3,0

8,0

2,5

6,0 2,0

1,5

4,0

1,0

2,0 0,5

0,0

0,0

-0,5

-2,0 -1,0

2019 2020 2021 2022 2023 2024 2019 2020 2021 2022 2023 2024

20,0

0,0

-20,0 APRIL 2022 DECEMBER 2021

SOURCES: Banco de España and INE.

Latest observation: February 2022.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 28MEASURES APPROVED IN ROYAL DECREE-LAW 6/2022 OF 29 MARCH 2022 DIRECTLY AFFECTING INFLATION

An extraordinary and temporary rebate (between 1 April and 30 June 2022) on the retail price of fuel

A 36% reduction in energy system-related charges with respect to March (55% with respect to August 2021) until 31

December 2022

An extension until 30 June 2022 of the suspension of the tax on electricity generation and of the reduced rates for

VAT on electricity (10%) and the excise duty on electricity (0,5%)

An extension of the cap on the April and July 2022 revisions of the regulated rate for small natural gas consumers (to

a maximum increase of 5% for retail consumers)

A 2% cap on rent increases from 1 April to 30 June

A reduction of between 0.5 pp and 0.8 pp in the average inflation rate for 2022 (compared with a scenario of

no measures)

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 29HOUSEHOLDS ARE EXPECTED TO RESORT TO A GREATER EXTENT TO THEIR ACCUMULATED SAVINGS, BUT

THIS WILL NOT PREVENT A SLOWER RECOVERY IN REAL CONSUMPTION OWING TO HIGH INFLATION

PRIVATE CONSUMPTION SAVING RATE

(volume chain-linked index)

% of GDI (a)

2019 Q4 = 100

16

110

105

14

100

12

95

90 10

85

8

80

6

75

70 4

2019 Q4 2020 Q4 2021 Q4 2022 Q4 2023 Q4 2024 Q4 2019 2020 2021 2022 2023 2024

24

APRIL

4 2022 DECEMBER 2021 2015-2019 AVERAGE

2019 2020 2021 2022 2023 2024

SOURCES: Banco de España and INE.

Latest observation: 2021 Q4.

a) Gross disposable income.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 30IN 2021 THE GENERAL GOVERNMENT BUDGET BALANCE WAS BETTER THAN EXPECTED DUE TO SOUND

REVENUE PERFORMANCE, BUT IT IS REVISED DOWN FOR 2022-2024

GENERAL GOVERNMENT BALANCE GENERAL GOVERNMENT REVENUE AND CHANGES IN THE PUBLIC DEFICIT FORECAST

EXPENSES (a) FOR 2022 SINCE DECEMBER

% of GDP

% y-o-y % of GDP

-2 20 5,1

5,0

15

-4 4,9

10 4,8

-6 0,6

4,7

5 0,3

4,6

-8 5,0

0 4,5

4,8 0,1

4,4

-10

-5

4,3

4,4

4,2

-12 -10

2019 2020 2021 2022 2023 2024 Jan-20 Jul-20 Jan-21 Jul-21 Jan-22

4,1

Dec. 2021 close Macro Measures Apr.

Forecast Forecast

DECEMBER 2021 APRIL 2022 APE 2021-24 REVENUE EXPENSES

SOURCES: SPU 2021-2024, IGAE and Banco de España.

a) Relating to the general government aggregate, excluding local government and transfers between tiers of government.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 31CONTENTS

1. Overview

2. Developments in economic activity in the short term

3. Projections for the Spanish economy for 2022-2024

4. Main risks and sensitivity exercises

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 32AN EXTRAORDINARILY UNCERTAIN SCENARIO: MAIN SOURCES OF UNCERTAINTY

Duration and severity of the

war in Ukraine and persistence Indirect and second-round Take-up and economic impact

of the possible geopolitical effects on inflation of the European NGEU funds

fall-out

Energy prices Household consumption and

Course of the pandemic

recourse to stock of savings

Impact of worldwide monetary

Possible energy and fiscal

Bottlenecks in global policy normalisation on

policy measures in Spain and

production and supply chains financial markets and financing

the European Union

conditions

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 33IN SUCH AN UNCERTAIN SETTING, SEVERAL HYPOTHETICAL SCENARIOS ARE CONSIDERED THAT ILLUSTRATE

THE CONSIDERABLE SENSITIVITY OF THE PROJECTIONS TO VARIOUS KEY ASSUMPTIONS

SENSITIVITY EXERCISES CAUTIONS

What if the high energy prices prove more • The counterfactual scenarios considered

persistent than expected? include assumptions which, albeit plausible, are

less likely to arise than those envisaged in the

baseline scenario

What if trade with Russia is suspended?

• The estimated impacts should be interpreted

with caution, as it is not possible to accurately

assess the economic response to relatively

extreme assumptions

What if significant second-round effects

arise?

• The sensitivity exercises considered are

interconnected, so the impacts are not

What if household consumption is more cumulative

buoyant?

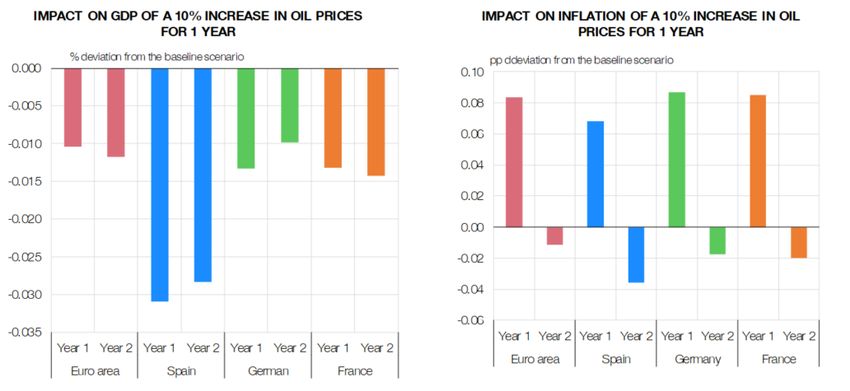

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 34WHAT IF THE HIGH ENERGY PRICES PROVE MORE PERSISTENT?

A future energy price trajectory is considered that holds steady around the highest level recorded since the

start of the war in Ukraine (observed in mid-March)

ENERGY PRICE SHOCK (INCREASE COMPARED DIFFERENCES VIS-À-VIS THE BASELINE SCENARIO (IN PP)

WITH FEBRUARY 2020)

INFLATION GDP

%

80

0,5 0,0

70

60

0,4 -0,1

50

40 0,3 -0,2

30

20 0,2 -0,3

10

0,1 -0,4

0

2021 Q1 2022 Q1 2023 Q1 2024 Q1

0,0 -0,5

BASELINE

CENTER SCENARIO

STAGE ADVERSE STAGE

ADVERSE SCENARIO 2022 2023 2024 2022 2023 2024

SOURCES: Banco de España and INE.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 35WHAT IF TRADE WITH RUSSIA IS SUSPENDED?

The suspension of all bilateral trade between Russia and the European Union, including trade in energy

commodities, is considered

DIFFERENCES VIS-À-VIS THE BASELINE SCENARIO in 2022 (IN PP)

IMPACT ON GDP IMPACT ON INFLATION

pp pp

0,0 1,6

-0,2 1,4

1,2

-0,4

1,0

-0,6

0,8

-0,8

0,6

-1,0

0,4

-1,2 0,2

-1,4 0,0

Low substitutability Medium High substitutability Low substitutability Medium substitutability High substitutability

substitutability

SOURCE: Banco de España.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 36WHAT IF SIGNIFICANT SECOND-ROUND EFFECTS ARISE? (1/3)

So far, wage settlements have increased only slightly, so workers are losing purchasing power

WAGE RISES AND WORKERS AFFECTED IN 2022

WAGE RISES BY DATE OF SIGNING OF AGREEMENT INFLATION INDEXATION CLAUSES

Persons % total % y-o-y

3,0 % 1.200.000 80 7

70 6

2,5 1.000.000

5

60

2,0 800.000 4

50

3

1,5 600.000 40

2

30

1,0 400.000 1

20

0

0,5 200.000

10 -1

0,0 0 0 -2

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2015 2016 2017 2018 2019 2020 2021 2022 2020 2020 2020 2020 2021 2021 2021 2021 2022

(to Feb) Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

INDEXATION CLAUSES CPI (Dec t-1) (right-hand scale)

TOTAL REVISED NEW 0%-2% 2%-3% 3%-5% >5%

SOURCES: Ministerio de Trabajo y Economía Social and Banco de España.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 37WHAT IF SIGNIFICANT SECOND-ROUND EFFECTS ARISE? (2/3)

For the time being, firms do not appear to be fully passing their rising input costs through to the price of their

products: profit margins are narrowing

CHANGES IN FIRMS’ TRADE MARGINS IN 2021 Q4 (b) SHARE OF EMPLOYMENT OF FIRMS WITH

Difference with respect to 2020 Q4 NEGATIVE PROFITABILITY (c)

QUARTERLY EVOLUTION OF PRICES pp % pp

1,4 2 35 14

1,2

1 30 12

1,0

0 25 10

0,8

0,6 -1 20 8

0,4 -2 15 6

0,2

-3 10 4

0,0

-4 5 2

-0,2

-0,4 -5 0 0

2020 Q4 2021 Q1 2021 Q2 2021 Q3 2021 Q4 2022 Q1 Total Of which:Of which: 2019 2020 2021 2022 2023

industry Minerals Other

Nov-20 Feb-21 May-21 Aug-21 Nov-21 Feb/mar-22 and manufac.

round round round round round round metals industries IMPACT OF COVID-19. Change in 2020 (right-hand scale)

Total Industry Trade Information Other

IMPACT OF RISING ENERGY PRICES (right-hand scale)

PRICE OF INPUTS PRICE OF OUTPUTS firms and hospitality and

comms

DECEMBER 2021 SCENARIO

SOURCE: Banco de España (EBAE and CBQ). DECEMBER 2021 SCENARIO, WITH RISING ENERGY PRICES

a) Index calculated as Significant decrease = -2; Slight decrease = -1; Stability = 0; Slight increase = 1; Significant increase = 2

b) The trade margin is defined as the ratio of GVA to output.

c) 2019 employment. A 22% rise in energy prices has been assumed for 2022, with an additional 3% in 2023.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 38WHAT IF SIGNIFICANT SECOND-ROUND EFFECTS ARISE? (3/3)

Meanwhile, a scenario is envisaged in which business owners and workers look to increase their prices and

wages in order to neutralise the initial impact of the energy shock on their income, triggering second-round

effects on prices and wages

DIFFERENCES WITH RESPECT TO THE BASELINE SCENARIO (IN PP)

HICP GDP EMPLOYMENT

3,0 0,0 0,0

-0,2 -0,2

2,0

-0,4 -0,4

1,0

-0,6 -0,6

0,0 -0,8 -0,8

2022 2023 2024 2022 2023 2024 2022 2023 2024

SOURCES: Banco de España and INE

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 39WHAT IS HOUSEHOLD CONSUMPTION IS MORE BUOYANT?

In 2022-2024, a scenario has been envisaged in which households may use two thirds of the savings they

have built up since the onset of the pandemic (only one third in the baseline scenario)

DIFFERENCES WITH RESPECT TO THE BASELINE SCENARIO (IN PP)

SAVINGS RATE GDP EMPLOYMENT

0,0 0,5 0,5

-0,2

0,4 0,4

-0,4

0,3 0,3

-0,6

0,2 0,2

-0,8

0,1 0,1

-1,0

-1,2 0,0 0,0

2022 2023 2024 2022 2023 2024 2022 2023 2024

SOURCES: Banco de España and INE

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 40APPENDIX DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 41

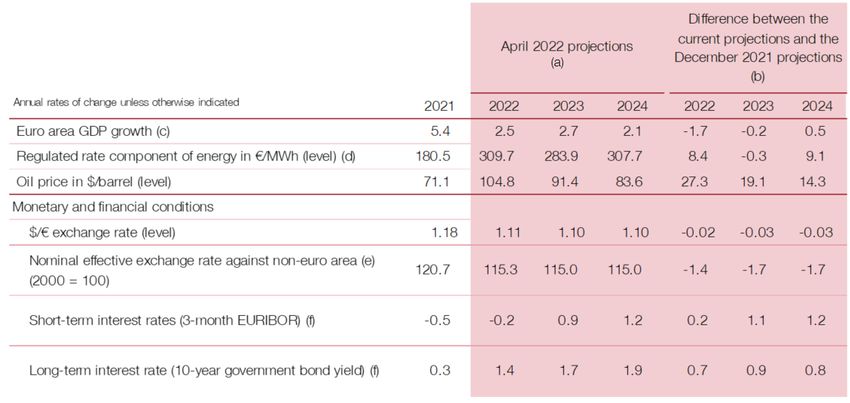

ASSUMPTIONS ON THE INTERNATIONAL ENVIRONMENT AND MONETARY AND FINANCIAL CONDITIONS

SOURCES: Banco de España and ECB.

a. Cut-off date for assumptions: 31 March 2022. The figures expressed as levels are annual averages. The figures expressed as rates are calculated based on the relevant annual averages.

b. The differences are expressed as rates for euro area GDP, as levels for electricity and oil prices and the $/€ exchange rate, as percentages for the effective nominal exchange rate and as percentage points for interest rates.

c. Obtained from the ECB staff macroeconomic projections for the euro area, March 2022.

d. Regulated rate for small electricity consumers.

e. A positive percentage change in the nominal effective exchange rate denotes an appreciation of the euro.

f. For the projection period, the figures in the table are technical assumptions, prepared following the Eurosystem's methodology. These assumptions are based on futures market prices or approximations thereto, and should not be

interpreted as a Eurosystem prediction as to how these variables will trend.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 42MACROECONOMIC PROJECTIONS (2022-2024)

December 2021

April 2022 projections (a)

projections

2020 2021 2022 2023 2024 2022 2023 2024

GDP -10.8 5.1 4.5 2.9 2.5 5.4 3.9 1.8

Private consumption -12.0 4.6 4.5 3.9 2.4 5.1 5.2 2.2

Government consumption 3.3 3.1 -0.3 0.8 1.2 -0.2 0.7 1.5

Gross fixed capital formation -9.5 4.3 4.5 2.1 2.5 7.8 3.7 2.1

Exports of goods and services -20.1 14.7 12.0 3.8 3.7 9.1 4.6 3.1

Imports of goods and services -15.2 13.9 9.0 3.3 2.9 6.5 4.8 3.7

Domestic demand (contribution to growth) -8.6 4.6 3.3 2.7 2.1 4.4 3.9 1.9

Net external demand (contribution to growth) -2.2 0.5 1.2 0.2 0.4 1.0 0.0 -0.1

Nominal GDP -9.8 7.4 9.1 4.8 4.3 8.1 5.6 3.6

GDP deflator 1.1 2.2 4.4 1.9 1.7 2.5 1.7 1.7

Harmonised index of consumer prices (HICP) -0.3 3.0 7.5 2.0 1.6 3.7 1.2 1.5

HICP excluding energy and food 0.5 0.6 2.8 1.8 1.7 1.8 1.4 1.6

Employment (hours) -10.6 7.0 1.9 2.0 1.6 3.8 2.8 1.3

Unemployment rate (% of labour force).

15.5 14.8 13.5 13.2 12.8 14.2 12.9 12.4

Annual average

Net lending (+)/net borrowing (-) of the nation (% of GDP) 1.2 1.9 2.7 3.3 3.2 2.9 2.7 2.1

General government net lending (+)/net borrowing (-) (% of GDP) -10.3 -6.9 -5.0 -5.2 -4.7 -4.8 -4.0 -3.4

General government debt (% of GDP) 120.0 118.4 112.6 112.8 113.5 115.7 113.7 113.5

SOURCES: Banco de España and INE. Latest QNA data published: 2021 Q4

a) Projections cut-off date: 31 March 2022.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH – BANCO DE ESPAÑA 43You can also read