Managing Risk In The Oil Industry: Credit And Supply Chain Management

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Managing Risk In The Oil Industry: Credit

And Supply Chain Management

Polish Risk Association

Warsaw, June 4, 2014

Gustavo Tella, CFA, FRM

Head of EMEA Business Development

S&P Capital IQ

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ.

Not for distribution to the public. Copyright © 2014 by Standard & Poor’s Financial Services LLC (S&P). All rights reserved.

Topics

• Best Practices For Assessing The Health Of Your Supply Chain

• Assessing Supply Chain Risk: PKN Case Study

• Supplier Credit Surveillance

• Finding potential substitutes

– Example: TOTAL Nigeria PLC

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

2

Best Practices For Assessing The Health Of Your Supply Chain

Qualitative Framework

• How do my suppliers perform relative to each other?

• What is the credit health of my suppliers?

• Can I identify “at risk” suppliers?

– Can I assess the credit quality of each supplier?

– The Impact to my revenue as part of a “critical factor”?

– Operational dependability in terms of uniqueness and disruption

– Can I measure the operational risk to my supply chain when there are limited substitutes?

• Can I monitor suppliers for early warning signals of credit deterioration?

• Do we have a consistent and transparent framework for our supply chain?

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

3

Supply Chain Management

A Major Focus

“The market is quick to punish companies that report supply chain disruptions. On average, affected companies’

share prices dropped 9 percent below a benchmark group during the two-day announcement period (i.e., the day

before and the day of the announcement).”

Source: PWC’s “From Vulnerable to Valuable: How Integrity Can Transform a Supply Chain”

“Oil and gas companies’ supply chains are playing an increasingly vital role […] from steel and drill bits to

transportation and catering – [it] is required to meet global oil and gas production demand.”

Source: Oil & Gas’s “The future of the supply chain”

“Supplier relationships and performance management are increasingly important. Managing supply risks and

reducing avoidable costs require close integration and visibility into suppliers’ operations, even more so when

suppliers are immature or constrained..”

Source: Ernst & Young’s “Supply Chain Management in Shale Environment”

“We’ve moved from everybody can do their own thing in supply chain to a much more centralized or centre-led

approach in our industry—learning from other industries […] We must keep that focus.”

Source: Head of Procurement Supply Chain at BP

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

4The Problem: Analysis Beyond The Rated Universe

The Coverage/Accuracy Tradeoff

RATED UNIVERSE

• Credit analysis driven by

qualitative and quantitative

inputs

PUBLIC UNRATED UNIVERSE

• Credit analysis driven by Accuracy

fundamentals-based relative

analysis Coverage

• Supplemented by absolute

measures

PRIVATE UNRATED UNIVERSE

• Credit analysis driven by user

inputs to models

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

5Assessing Supply Chain Risk: PKN Case Study

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

6Fundamentals Based Peer Analysis:

Supplier Credit Assessment

PKN Suppliers

Industry: Oil and Gas Refining

• 54 suppliers globally: 47 unrated, 7 rated by Standard & Poor’s Rating Services

• Unrated companies have limited information compared to rated, therefore they

need to be assessed in a different manner and from a different prospective:

– Monitoring changes in suppliers’ financial strength and credit quality

– Relative peer analysis of PKN’s suppliers

– Credit Scoring Models, Stress Testing, and Probability of Default evaluation highlights the level

of risk in PKN’s supply chain

For illustrative purposes only.

S&P Capital IQ, as well as its products and services are analytically and editorially separate and independent from Standard & Poor’s Ratings Services

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

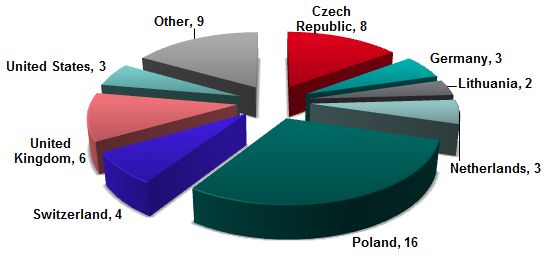

7Break Down Of PKN’s Suppliers

Industry & Geographic Concentrations

• 29* out of a total of 54 companies from PKN’s suppliers have a probability of default and a

score, compared to 7 companies rated by Standard & Poor’s Ratings Services

• Geographic breakdown of PKN’s suppliers

shows a large proportion are based in the

Poland (16 companies)

* 8 companies are not scored due to insufficient data. Source: S&P Capital IQ. As of 1 April 2013.

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

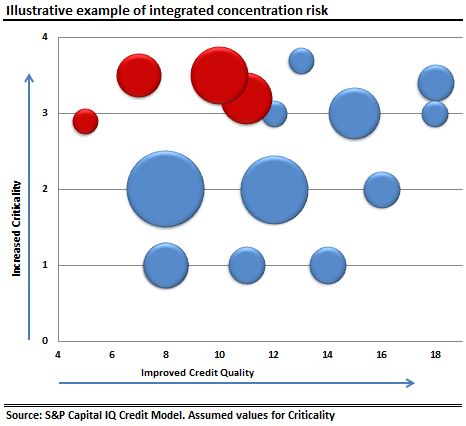

8PKN’s Suppliers: Rated Vs Unrated Universe

• The number of suppliers with a credit rating is limited

• Additional credit scoring models are needed to determine current credit assessment of suppliers

Potential

concentration risk at

the lower end of the

scale with a greater

number of

counterparties as

non-investment

grade scores.

Source: S&P Capital IQ’s PD Fundamental. As of 15 May 2014.

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

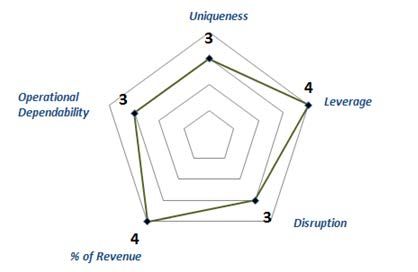

9Criticality Of Suppliers – PKN Supplier Example

Position Of Suppliers In Oil & Gas Equipment & Services Industry

• Important to reduce exposure to risky/volatile suppliers.

• PKN can monitor performance of its suppliers and reduce deals with the most risky ones.

• Suppliers with low credit quality and high criticality pose a greater risk as they are crucial

to PKN’s operations, regardless of credit quality

Criticality scale assesses revenue dependence and

operational reliance from 1 (low) to 4 (High)

Source: S&P Capital IQ. Both graphs are for illustrative purposes only.

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

10Relative Peer Analysis For Critical Suppliers

A Fundamental Credit Health Ranking Of PKN’s Suppliers

•Suppliers are ranked based on a number of Operational, Solvency and Liquidity metrics

•The largest group of companies in the lower quartile of PKN’s supply chain are from Oil & Gas

Equipment & Services

•Depending on PKN’s exposure to these particular suppliers, further in-depth analysis may be

required

Source: S&P Capital IQ’s Credit Health Panel on the Global Credit Portal. As of 13 May 2014.

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

11A Holistic View Of PKN’s Supply Chain

Monitoring Suppliers Credit Performance

• Surveillance template enables analysis of entire portfolio of PKN’s suppliers

• Combine proprietary data (such as criticality), auto populate financials, and conduct analysis

on the broad portfolio

Source: S&P Capital IQ. As of 15 May 2014.

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

12Supplier Credit Surveillance

Example: TOTAL Nigeria PLC

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

13A Telling Picture: Comparing TOTAL Nigeria PLC

GICS: Global Industry Classification Standard

• Analysis using Credit Health Panel shows that TOTAL Nigeria PLC was not only one of the lowest ranked suppliers

when compared to all of PKN’s suppliers, it is also one of the lowest ranked amongst a group of its 41 GICS peers

globally

• TOTAL Nigeria PLC is placed in the 3rd lowest quartile when ranked against global peers

• It also utilizes more debt given its financial leverage ratio of 52% compared to the group average of 34%

• Its Current Ratio is also the bottom quartile (0.89x) against its global peer group average of 1.41x

*Management Rate of Return: EBIT / (Net Property, Plant and Equipment + Net Working Capital).

Source: S&P Capital IQ’s Credit Health Panel on the Global Credit Portal. As of May 14nd, 2014.

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

14PD Fundamental

A Quantitative Creditworthiness Assessment – TOTAL Nigeria PLC

• TOTAL Nigeria PLC is in the

bottom quartile in terms of

its PD (Fundamental)

• It has been in the in the

bottom quartile since the

end of 2009

Source: S&P Capital IQ’s Fundamental PD. As of 14 May 2014.. For illustration purposes only.

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

15Finding Potential Alternatives

African Oil & Gas Refining

• We shortlisted 14 Oil & Gas Refining & Marketing companies operating in Africa by:

– Screening for companies in Africa within the O&G Refining and Marketing industry with Total Assets > 0

• TOTAL Nigeria PLC is still at the below average quartile relative to its industry/geographic peers

• Credit Health Panel shows that, for example, Engen Botswana Ltd. has a better quantitative score and its

placed at the top of the this peer group

Source: S&P Capital IQ. As of May 14th, 2014. For illustrative purposes only.

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

16Monitoring Your Supply Chain Exposure

Moving From Relative To Absolute Analysis

• Applying holistic approach to evaluate supplier exposure and pockets of risk concentrations enables risk

managers to conduct due diligence more effectively

• We look for alternatives to TOTAL Nigeria PLC based on key fundamental metrics such as interest coverage

and Operating Income/Revenue

• Engen Botswana Ltd. is at the top of the table in terms operating income to revenues and the second highest

interest coverage ratios of the group

• Societe Anonyme Marocaine de I’Industr has the highest total assets amongst this group, but the lowest

operating income/revenue and interest coverage. It’s gearing is 79%

• Criticality Factor should also be assessed in the final decision making process

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

17Summary And Uses Of PKN’s Supply Chain Risk Management

• Out of PKN’s 54 Global Suppliers, only 7 are currently rated. This requires using

other risk assessment metrics to evaluate financial strength of suppliers

• Using quantitatively driven models such as Fundamental Probability of Default, we

extend the coverage to 29 companies with quantitative credit metrics.

• Relative peer analysis identifies TOTAL Nigeria PLC which is placed at the bottom

of PKN’s suppliers and below average within its own global industry group

• For this case example, we assume that Total Nigeria PLC is a critical supplier for

PKN’s Supply Chain Operations.

• Looking for potential alternatives, we shortlisted 14 African Oil & Gas Refining &

Marketing companies and focus on top quadrant in relative analysis, before we

perform an absolute analysis.

• We identify Engen Botswana Ltd as a potential replacement for TOTAL Nigeria PLC

Permission to reprint or distribute any content from this presentation requires the prior written approval of S&P Capital IQ. Not for distribution to the public.

18www.spcapitaliq-credit.com

Copyright © 2014 by Standard & Poor’s Financial Services LLC (S&P). All rights reserved. No content (including ratings, valuations, credit-related analyses and data, model, software or other application or output therefrom) or

any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s

Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P, its affiliates, and any third-party providers, as well as their directors, officers,

shareholders, employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions, regardless of the

cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR

IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR

DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be

liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and

opportunity costs) in connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact or recommendations to purchase, hold, or sell any

securities or to make any investment decisions. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and

experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P’s opinions and analyses do not address the suitability of any security. S&P does not act

as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due diligence or

independent verification of any information it receives.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P may have information that is

not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non–public information received in connection with each analytical process.

S&P may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and analyses. S&P's

public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributed through other

means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at www.standardandpoors.com/usratingsfees.

19

STANDARD Permission

& POOR’S, S&P, CAPITALtoIQ

reprint or distribute

and GLOBAL anyPORTAL

CREDIT content from this presentation

are registered requires

trademarks the prior

of Standard written

& Poor’s approval

Financial of S&P

Services Capital IQ. Not for distribution to the public.

LLC.You can also read