MERDEKA GENERATION - FINANCIAL PLANNING FOR THE - Advice by MoneyOwl

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FINANCIAL

PLANNING

FOR THE

MERDEKA

GENERATION

Author

MoneyOwl Solutions Team

CONTENTS SYNOPSIS 3 CHAPTER 1 YOUR HOME 4 CHAPTER 2 SHOULD YOU RETIRE NOW? 8 CHAPTER 3 CPF PAYOUTS- YOUR SAFE RETIREMENT INCOME FLOOR 11 CHAPTER 4 ADDITIONAL INCOME IN RETIREMENT 15 CHAPTER 5 A MEDICAL SAFETY NET 20 CHAPTER 6 ESTATE DISTRIBUTION 28

SYNOPSIS

We all know someone from the Merdeka Generation perhaps a parent, neighbour,

colleague or even yourself. Born in the 1950s, each has a story to tell - stories of how one

lived through the independence struggle of the nation, joined the workforce early and

experienced serving National Service as one of the earliest batches. These are men and

women who contributed to the early nation building of Singapore.

As a tribute to our nation builders, MoneyOwl has put together this e-book to help you

better prepare for retirement. A common worry you may have is retirement adequacy,

i.e. whether there is enough money for living expenses and medical needs in your golden

years. The question of “enough” is a subjective one and is dependent on your financial

situation and expectation. However, regardless of your expectation, a good retirement plan

should provide you with these 3 Must-Haves:

$

A home to stay in Monthly retirement Medical safety net

income for life

In this e-book, we will explore each of these Must-Haves, as well as highlight the planning

considerations you may face. In line with MoneyOwl social mission to help the man on

the street achieve greater financial security to live fulfilling lives, we consciously integrate

national schemes into our planning approach. Hence we will also discuss national schemes

like CPF LIFE, MediShield Life, ElderShield/CareShield Life, Lease Buyback Scheme and

how they can support your retirement needs. We wrap up with how you can distribute

your estate to your loved ones according to your wishes upon demise. This is an important

step as it will end your financial journey on a good note.

1

CHAPTER 1 | YOUR HOME 5

YOUR HOME

1.1 A FULLY PAID HOME One option is to monetise your property, i.e.

unlocking it to supplement your retirement

needs. There are a few ways to go about

We all need a place to stay, a place we call it and the ultimate decision boils down to

home, where lives and memories are built. personal preference.

All thanks to our housing policy, most

households here (more than 90%) owns

a property.

1.2 MONETISE BY RENTING

A 3-room flat in Toa Payoh in the 1970's

was only around $8,000. Even with one's

OUT SPARE ROOM OR

meagre salary, he/she will be able to WHOLE FLAT

fully repay the home loan quite easily.

Some, however, continue to upgrade their Do you have a spare bedroom or have

houses and added more to their loans alternative accommodation arrangement

in the process. The guess is most of the such as staying with your children? If so,

Merdeka Generation would have repaid renting out the excess space for income is

their mortgages by now, but if for some not a bad idea. Renting out excess space

reasons one has not, the immediate goal rewards them with the extra money to

is to review the finances and try to pay it enjoy their retirement. A spare room can

off as soon as possible in preparation for typically fetch about $600 to $1,200 in

retirement. There is psychological bliss, a rental income depending on location

peace of mind, from being debt-free. and condition.

What if there are difficulties in clearing the The benefits of this option include keeping

loan? Or if one is caught in an asset-rich, your property (and your neighbours),

cash-poor dilemma? What should you do? receiving rental income and continuing

to participate in the appreciation of your

There are no easy answers but suffice to property value.

say that you need to review your assets,

optimise your savings, CPF and estimate

how much is needed for your retirement.

We will cover more of that in the

next chapter.

CHAPTER 1 | YOUR HOME 6

1.3 MONETISE BY Besides receiving extra money from down-

sizing, you could also save on running cost

DOWN-SIZING from lower conservancy charges, property

tax and lower upkeep of a smaller unit.

But what if you do not wish to share your

property with others? Or find that the

current house is now too big to upkeep 1.4 MONETISE BY LEASE

as your children or family members have

moved out. In such cases, perhaps down- BUYBACK SCHEME (LBS)

sizing or right-sizing is a consideration. This

option allows you own the entire unit, albeit Finally, what if you prefer to age in place,

a smaller one, but with extra money from because you love the neighbourhood or you

the exercise. just cannot accept the idea of renting out

your rooms? In that case, there is the Lease

One affordable option of a smaller flat is the Buyback Scheme (LBS).

2-room flexi unit from HDB. You can select

how long a lease you need. The shorter the In LBS, you are essentially selling the tail-

lease, the smaller the property price. end lease of your flat back to the HDB for

money. In this way, the lease of your flat

Seniors who are aged 55 and above can is now shortened. There are conditions

take up a lease of between 15 and 45 years on the sales proceeds, which requires one

as long as it must cover the age of the use the money to first do a top up into

applicants up to 95 or more. your CPF Retirement Account (RA); any

remaining balance would then be available

Such a flat is quite attractively priced. for cash spending. The whole idea of the

According to HDB as of April 2018, such top-up is for you to join CPF LIFE which will

a flat is priced around $150,000 in the then provide a stream of income for your

matured estate and $90,000 in the non- retirement for life.

matured estate for a 40-year lease1. These

flats are getting quite popular in recent Perhaps the following example from HDB

years and HDB has been ramping up supply website2 can help us understand how the

of such units to meet demand. LBS works.

How can Mr & Mrs Lim unlock the

value of their flat with the Lease

Buyback Scheme?

Couple profile

Mr & Mrs Lim both 65 years old

Joint owners of fully paid 5-room flat

CPF

RA

Flat value: $520,000 Mr Lim $20,000

Lease left: 65 years Mrs Lim $5,000

1. Source: HDB data dated 24 Apr 2018, https://www.hdb.gov.sg/cs/infoweb/various-options-for-seniors-to-monetise-hdb-flats

2. Source: http://www.hdb.gov.sg/cs/infoweb/img/top-up-worked-example.jpg

CHAPTER 1 | YOUR HOME 7

In this example, Mr & Mrs Lim, both age 65, own a fully paid 5-room flat, valued at

$520,000 with a remaining lease of 65 years. Their CPF-RA savings stand at $20,000

and $5,000 respectively. With such low CPF savings, their combined CPF LIFE payout

(assuming Standard plan) is about $1603 monthly. This is obviously insufficient for their

retirement needs if that is all they have.

Suppose they decide to participate in LBS, this is how it works:

• Sell off 35 years of their flat’s lease to HDB for $219,300

• Sales proceeds to top-up their respective CPF-RA up to the

Basic Retirement Sum of $88,000

• $151,000 is required to do the top up; ($88,000 – $20,000 + $88,000 – $5,000)

• Net proceeds left after CPF top-up is $68,300 ($219,300 – $151,000)

• Receive a $5,000 LBS Cash Bonus, since the CPF top up is more than $60,000

Total value unlocked by Mr & Mrs Lim

LBS CPF LIFE Payout LBS

Cash Proceeds (per month, for life) Cash Bonus

$68,300 $1,000 $5,000

Based on $151,000 top-up to

the couple's CPF RA account

Mr & Mrs Lim both 65 years old, retains their flat with 30 years of lease remaining.

Benefits of LBS

The couple could now receive a lump sum cash payout of $73,300(LBS cash proceeds

$68,300 + LBS cash bonus $5,000) and a monthly income stream from CPF LIFE of $1,000.

Not bad considering that before this, the couple could only enjoy about $160 monthly from

their CPF LIFE.

The key drawback of LBS is the once in the scheme, you are not allowed to sell the flat in

the open market or rent out the whole flat. In other words, you are not able to participate in

the potential appreciation of the property value.

What if you outlived the lease period, e.g., beyond age 95? HDB assures you that in such

a situation, you will not be left without a home. HDB will review your circumstances on

a case-by-case basis taking in factors such as family support, health conditions and

financial status and work out an appropriate housing arrangement with you.

For more info on LBS, please check out

https://www.hdb.gov.sg/cs/infoweb/residential/living-in-an-hdb-flat/for-our-seniors/

lease-buyback-scheme

Source: This amount is estimated from the CPF LIFE Estimator. Mr Lim is estimated to receive $$126 to $133 monthly and $29 to $31 monthly for Mrs Lim.

2 SHOULD YOU RETIRE NOW

2

CHAPTER 2 | SHOULD YOU RETIRE NOW 9

SHOULD YOU

RETIRE NOW?

The second Must-Have in retirement is a monthly

retirement income for life to cover our expenses.

It is no coincidence that those belonging to expectancy of 84 years – that is as long as

the Merdeka Generation are at one of the half our economically productive years!

important milestones of their retirement

planning – crossing the statutory retirement In 2018, more than 53% of those aged 60

age of 62, CPF payout eligibility age of to 69 are employed.4 Some may continue

between 63-65 and re-employment age working due to lack of choice, but perhaps

of 67. many do so to remain physically, mentally

and socially active. If you have ever taken

But before we talk about retirement income, a gap year in your work, you would realise

let us talk about whether one should seek how quickly one runs out of things to do

to retire in his or her 60s. after a few months and the emotional and

psychological complexities of that.

You’ve worked and saved hard for most

part of your life and finally, retirement is Indeed, what is often underestimated is the

in view. But retirement is not a destination emotional journey of a retiree.

but rather another phase of your life. According to the New Retirement

Retirement can stretch for as long as 15- Mindscape II study (Ameriprise Financial

20 years in view of today’s average life Inc), there are six stages in this journey:

IMAGINATION HESITATION ANTICIPATION REALISATION REORIENTATION RECONCILIATION

6 to 15 years prior 3 to 5 years prior 2 years prior Retirement day and 2 to 15 years after 16 years or more after

to Retirement Day the year following

3. Based on MOM’s Labour Force Survey, 2018 (Table 4)

CHAPTER 2 | SHOULD YOU RETIRE NOW 10

As a member of the Merdeka Generation, What this means is that your employer

you may be either in the Imagination can choose to terminate your employment

stage, where you might feel unprepared without compensation when you turn 62

for retirement or the Hesitation stage, years old. But in view of our tight labour

when you are actively seeking advice and market, decreasing fertility rate and

the ability to cover your healthcare costs increasing life expectancy (60 is the new

becomes a particularly important concern 50), the Re-employment Act was passed

for you. This is also why the Merdeka in 2012. With this in place, your employer

General Package focuses on help for will need to offer you (subject to eligibility

medical expenses, the coverage of which criteria) re-employment beyond 62 years

is our third Must-Have, of which we will old, on an annual basis, up to age 67. There

write more in a future part of this series. are also recent policy changes to increase

Or, you might be in Anticipation, which is CPF contribution rates and an additional

the happiest stage of the six stages. A few 1% interest rate is now paid on CPF

might have just retired and the Realisation savings for workers aged 55 and above.

or feeling of being a little let down can be

hard, the most difficult being the loss of In addition, the government also announced

income, and this emotional stage improves that the Tripartite Workgroup on Older

only upon some Reorientation. Workers will be looking into further

changes to the CPF contribution rates. As

Retirement is thus not all sun, sand announced in Budget 2019, the Workfare

and laughter, emotionally or otherwise. Income Supplement Scheme will also

Retirement can only be truly fulfilling if be enhanced from 2020. The qualifying

you are active and doing something that income cap will be raised to $2,300 and the

is of meaning to you. Financially also, you maximum annual payouts will be increased

need to consider if you would benefit from by $400. So, if you continue to work, you

delaying retirement. As you are your Most can potentially get up to $4,000 per year in

Important Financial Asset , don’t discount income supplements.

how you can still contribute to your own

well-being monetarily or otherwise. With Nonetheless, whether you choose to

the $100 top up to your PAssion Silver Card continue working, knowing that you have

from the Merdeka Generation Package, a retirement plan in place will provide you

don’t miss out on the various courses and with a peace of mind. Based on a recent

activities that you can sign up for at your survey of baby boomers, the top three

local community centre. sources of retirement income are CPF

(78%), savings/investments (55%) and

The Government has been improving the work (37%)5. We will explore these

infrastructure to help those who are able sources of retirement income in our next

and willing, to work longer. The statutory few chapters.

retirement age in Singapore is 62 years old.

Example of sources of income

Payout

Work

Savings/

Investment

CPF

Age

4. Manulife 3-Gen Survey, Nov 20183CPF PAYOUTS: YOUR SAFE RETIREMENT INCOME FLOOR

3

CHAPTER 3 | CPF PAYOUTS: YOUR SAFE RETIREMENT INCOME FLOOR 12

CPF PAYOUTS:

YOUR SAFE RETIREMENT

INCOME FLOOR

In this third chapter, we explore how CPF, specifically,

CPF LIFE forms the foundation of your retirement

plan by providing you with a stream of income for life.

A retirement income that covers daily expenses is the

second Must-Have in retirement, alongside a home to

stay in and a medical safety net.

The age at which you can start your CPF monthly payout is based on your year of birth.

Year born 1950 - 51 1952 - 53 1954 and after

Payout eligibility age 63 64 65

Arriving at the Payout Eligibility Age comes with a list of decisions. These are:

• Should I join CPF LIFE if I am on the Retirement Sum Scheme?

• Should I start my CPF LIFE payouts now?

• Should I make a lump sum withdrawal from my Retirement Account (RA)?

• Which CPF LIFE plan should I choose?

To answer these questions, it would be useful to have a gauge of what percentage of your

retirement needs would be funded by your CPF savings and consequently, how much you

may need to supplement with other income sources.

At MoneyOwl, we advocate that all retirement plans comprise an annuity as a base. An

annuity is a stream of income that pays for life and hedges against longevity risk, i.e., the

risk of outliving one’s assets. CPF LIFE is the best annuity in the Singapore market, all else

being equal, in terms of payout versus capital, return and risk. It is thus well placed to form

the Safe Retirement Income Floor for all Singaporeans. This Safe Retirement Income Floor

is a “die die must have” level of income to fund a basic level of retirement lifestyle.CHAPTER 3 | CPF PAYOUTS: YOUR SAFE RETIREMENT INCOME FLOOR 13

Based on the Household Expenditure If you do not own a property, you should

Survey 2012/13, we know that a retiree have the Full Retirement Sum (FRS) that

household in the second quintile of is double of BRS, because the need to

expenditure spends on average $518 rent a room on top of paying for basic

per month in 2013 on food, transport necessities can cause monthly expenses in

and other goods and services excluding retirement to double. For those whose Safe

accommodation. This is enough to Retirement Income Floor is even higher,

support a basic standard of living there is the option of topping up your RA to

(excluding rental of a place to stay) and is the Enhanced Retirement Sum (ERS) which

the basis on which the Basic Retirement provides an even higher level of payout.

Sum (BRS) under CPF LIFE is set – the BRS

provides for a payout under CPF LIFE that For CPF members who turn 55 in year

is close to $518 in 2013 dollars, adjusted 2019 (who are not Merdeka generation),

for inflation. This is also the reason why the current BRS, FRS and ERS are $88,000,

you can choose to set aside the BRS $176,000 and $264,000 respectively. In 10

only if you own a property as the payout years’ time, these would provide payouts

corresponding to BRS assumes you do not that are, in today’s dollars, roughly $600+,

need to rent a place to stay. $1,100+ and $1,600+.

For Merdeka Generation members who turn 65 this year and start their payouts, the

amount you need to have in your RA to generate a corresponding monthly income today is

shown in the table below:

Monthly lifetime payout

$600 $1,100 $1,600

from 65 years old

RA balance required at $100,000 - $200,000 - $300,000 -

65 years old $110,000 $210,000 $310,000

*Payout figures are estimates, based on the CPF LIFE Standard Plan and computed as of 2019. If you choose

to top up to your RA, the top up limit is the current Enhanced Retirement Sum less your RA savings excluding

interest earned and government grants.

You can use the CPF LIFE Payout Estimator on the CPF website for your own projection

based on your current RA balances.

Now that you have a sense of how much your CPF savings will contribute to your

retirement income, we can start to address these questions.

3.1 SHOULD I JOIN CPF LIFE IF I AM ON THE RETIREMENT

SUM SCHEME?

Before CPF LIFE, CPF members receive their monthly payouts from the savings in their

Retirement Account until it is depleted under the Retirement Sum Scheme (RSS). With

Singaporeans living longer, the risk of retirees outliving their savings is becoming very real.

Hence, CPF LIFE, our national annuity plan, was introduced in 2009 and made mandatory

in 2013 to protect against this longevity risk. If you are born 1958 or later and have at least

$60,000 in your RA when you turn 65 years old, you will be placed on CPF LIFE instead of

the RSS.

If you are on the RSS, you can also choose to join CPF LIFE before your 80th birthday. The

question is, should you? Ideally, you should have a retirement plan that pays you for life

because the last thing you want is to go back to work when you are in your 80s or hope

that your children can support you when they are already in their 60s. It would be better to

age with dignity with assurance of a lifelong income. Nonetheless, there are scenarios that

CPF LIFE is not suitable, i.e., very old members or those with very low RA balances, as you

may end up with a very small monthly payout that is not meaningful. In comparison, the

RSS gives a minimum payout of $250 per month.CHAPTER 3 | CPF PAYOUTS: YOUR SAFE RETIREMENT INCOME FLOOR 14

3.2 SHOULD I START MY CPF Based on a current payout of $600 a month,

making a 20% withdrawal will reduce your

LIFE PAYOUTS NOW? payout to $490 per month on the Standard

plan. It is important to decide if the reduction

Since 2016, you can choose to defer your of the monthly payout is worthwhile and

payout start age up to 70 years old. For would lend to a more meaningful life. In

every year you defer, your monthly payout addition, you don’t have to withdraw the

will increase by 6 – 7% more. For example, 20% in a lump sum, it can be done so in

if your payout is $600 per month if you start parts and even after your Payout Eligibility

at 65 years old, delaying the payout till 70 Age. So, if you don’t have immediate use for

years old will increase it to about $800 per the money, why not treat this as some sort

month for life. If you are still working or have of emergency funds instead?

other sources of income, this is one way for

you to increase your payouts without having

to put more money in your CPF.

3.4 WHICH CPF LIFE PLAN

SHOULD I CHOOSE?

3.3 SHOULD I MAKE A LUMP

There are currently 3 CPF LIFE plans you

SUM WITHDRAWAL AT can choose from – the Standard, Basic or

PAYOUT ELIGIBILITY AGE? Escalating plan, each catering to those with

different priorities. For those who want to

If you were born after 1957, you have enjoy the highest payout, Standard plan is

the option to make an unconditional for you. For those who are more concerned

withdrawal of up to 20% of your RA with leaving behind a legacy, Basic plan

balances (excluding top-ups and grants) could be more suitable. Lastly, if you are

when you reach your Payout Eligibility Age. concerned about rising cost of living, you

While such a withdrawal option provides can also consider the Escalating plan which

you with flexibility to fulfil some lifelong starts with a lower payout but increases by

wish upon retirement, the effect of this 2% per year.

withdrawal reduces your monthly payout.

Here is a comparison of the payouts across the three plans.

Standard Basic Escalating

$680 @ 65

Based on $150,000 in RA at

$860 $780 $830 @ 75

age 65 years old

$1010 @ 85

*Payout figures are estimates, based on a male member and computed as of 2019.

All CPF LIFE plans comes with a bequest feature, which means the monies used to join

CPF LIFE which was not paid out to you in monthly payouts by the time you pass on,

will be returned to your loved ones. The payouts, while stable, are not guaranteed as it is

subject to changes in CPF interest rates6 and mortality experiences.

Perhaps the easiest way to decide between the three plans is to check if the $100 per

month difference in payout between the plans is important to you, as the main objective in

any annuity is to provide an income stream. If yes, you may want to consider the Standard

plan to maximise your payouts today or the Escalating plan to maximise your payouts

in future. If no, the Basic plan could be more suitable as it would leave behind a larger

bequest for your beneficiaries.

What if you do not manage to actively take any of the above decisions? Have no fear. If

you do nothing, you will by default start your payout when you turn 70 years old on the

CPF LIFE Standard plan. This combination will give you the highest payout for life based on

your RA balances.

5. Interest on your Special, Medisave and Retirement Accounts is either the current floor rate of 4% p.a. or the 12-month average yield of 10-year Singapore Government

Securities (10YSGS) plus 1%, whichever is higher. The floor rate of 4% is reviewed annually by the government. Current(2019) average yield of the 10YSGS plus 1% is 3.38%.4 ADDITIONAL INCOME IN RETIREMENT

4

CHAPTER 4 | ADDITIONAL INCOME IN RETIREMENT 16

ADDITIONAL

INCOME IN

RETIREMENT

Strategies a Merdeka Generation senior can employ in

building a second layer of retirement income.

THE 5 RISKS FACED BY RETIREES

Retirement planning for retirees is more complicated than for accumulators because of the

combination of 5 risks that retirees need to deal with:

1. Longevity risk – living too long

2. Inflation risk – things becoming more expensive

3. Investing risk – assets value rise and fall

4. Over-spending risk – unsustainable spending

5. Healthcare risk – huge medical expenses

The combination of these risks poses a conundrum for retirees. While an annuity like CPF

LIFE takes care of longevity risk to some extent, rising costs (inflation risk) mean that

a much bigger retirement fund is required to maintain your current standard of living.

Leaving your money in the bank to earn fixed deposit interest rates is unlikely (going/

able) to support your retirement spending and hence there is a need to invest for higher

returns on your savings. However, investing carries risk (investing risk) and too much

volatility on your investment might become uncomfortable for retirees to accept. At the

same time, if left unchecked, excessive spending (over-spending risk) especially in the early

years of retirement could deplete their savings faster. Finally, as we age, our medical cost

(healthcare risk) increases and this will put further strain on the retirement funds.

A good retirement plan needs to try and reconcile these 5 risks for the retiree.

Here are some instruments you can consider using to build an additional layer of retirement

income, on top of CPF payouts:CHAPTER 4 | ADDITIONAL INCOME IN RETIREMENT 17

4.1 INVEST IN SUITABLE LOW-COST, WELL-DIVERSIFIED,

MARKET-BASED PORTFOLIOS TO STRETCH YOUR

SAVINGS, WHILE SETTING WITHDRAWAL RULES

Contrary to popular intuition, you can still invest in markets during your retirement years.

Your investment decision should be a combination of the need to take risk (what return you

need), your ability to take risk and your willingness to do so.

The need to take risk includes your need for income and your need to overcome longevity

and inflation risks. As for your ability to take risk, consider your financial situation, such

as whether you have an emergency fund and the time horizons that are relevant to you.

Given that an average retirement can span 15 to 20 years today, you certainly have the

time horizon to invest at least a portion of your savings that you do not immediately need.

However, you need to be willing to accept some volatility because staying invested is key

to capturing market return.

Unless you have a large enough pool of capital to be able to spend only the return, you

should also set a retirement withdrawal rule at between 2.5% to 4.0% of initial invested

capital, to help mitigate the negative impact of sequence of returns risk in investing. This is

the risk of experiencing negative market returns at the beginning of your drawdown, such

that you would deplete your capital base quickly if you are drawing down a fixed amount

(or an amount that is adjusted for inflation yearly), compared to a situation in which the

returns are positive at the start of your drawdown period. Alternatively, you can bucket

your investments according to different time horizons and invest later “buckets” into higher

risk portfolios earlier “buckets” into low-risk instruments.

Sequence of returns matter in retirement

ACCUMULATOR RETIREE

No withdrawals / Starting value: $100,000 5% annual withdrawal of starting value

($684,848) inflation-adjusted

Annual Portfolio A Annual Portfolio B Annual Portfolio A Annual Portfolio B

Age Age

Return Year-End Value Return Year-End Value Return Year-End Value Return Year-End Value

41 -12% $87,695 29% $129,491 66 -12% $566,337 29% $852,571

42 -21% $69,426 18% $152,281 67 -21% $413,086 18% $967,355

43 -14% $59,707 25% $189,590 68 -14% $318,927 25% $1,168,029

44 22% $72,984 -6% $178,404 69 22% $352,432 -6% $1,061,698

45 10% $80,136 15% $204,272 70 10% $348,431 15% $1,177,105

46 4% $83,595 8% $221,183 71 4% $323,772 8% $1,234,855

47 11% $92,707 27% $281,124 72 11% $318,176 27% $1,525,614

48 3% $95,210 -2% $274,939 73 3% $284,653 -2% $1,452,871

49 -3% $92,155 15% $315,355 74 -3% $232,143 15% $1,623,066

50 21% $111,507 19% $375,272 75 21% $236,215 19% $1,886,771

51 17% $130,129 33% $498,737 76 17% $194,417 33% $2,461,500

52 5% $137,026 11% $554,097 77 5% $194,417 11% $2,687,327

53 -10% $123,597 -10% $499,795 78 -10% $126,543 -10% $2,375,148

54 11% $137,316 5% $526,284 79 11% $90,304 5% $2,450,746

55 33% $182,493 17% $614,174 80 33% $68,219 17% $2,808,226

56 19% $217,167 21% $743,150 81 19% $27,833 21% $3,344,606

57 15% $249,091 -3% $719,305 82 15% $0 -3% $3,182,338

58 -2% $243,611 3% $738,726 83 -2% $0 3% $3,211,664

59 27% $309,629 11% $819,247 84 27% $0 11% $3,503,440

60 8% $335,262 4% $854,602 85 8% $0 4% $3,594,592

61 15% $383,875 10% $938,354 86 15% $0 10% $3,885,017

62 -6% $361,226 22% $1,147,022 87 -6% $0 22% $4,685,527

63 25% $449,727 -14% $986,439 88 25% $0 -14% $3,963,710

64 18% $528,878 -21% $780,941 89 18% $0 -21% $3,070,398

65 29% $684,848 -12% $684,848 90 29% $0 -12% $2,622,984

8% $684,848 8% $684,848 8% $0 8% $2,622,984

No difference Big differenceCHAPTER 4 | ADDITIONAL INCOME IN RETIREMENT 18

To compare 4.2 CONSIDER RETIREMENT Retirement income plans provide a monthly

payout over a fixed period. The payout

the different INCOME PRODUCTS comprises both a guaranteed and non-

retirement

guaranteed portion depending on the

income plans in For those who prefer not to make portfolio performance of the underlying fund. It is

the market, try investments, you may wish to consider important to take note that a portion of

MoneyOwl’s retirement income products offered by local the return is not guaranteed. Compared

Insurance insurers. When CPF LIFE was introduced, to portfolio investments, Retirement

Robo. it effectively killed off the private annuities income products generally present less

market as it was close to impossible to visible volatility as the payouts depend on

match the returns, all else being equal. the insurer’s ability to make the different

Nevertheless, the insurance companies threshold of investment returns in the

have reinvented this product range as insurance fund. In terms of disadvantages,

retirement income products which now you may find the capital outlay large

offer themselves as a complement to CPF relative to the return.

LIFE, especially if you have already hit the

CPF top-up limit.

Retirement income plans

Yearly income payouts

Non-guaranteed

amount

Guaranteed

amount

Payout age Retirement years Age

4.3 PARK YOUR LIQUID FUNDS IN SINGAPORE SAVINGS

BONDS (SSB)

Singapore Savings Bonds are more savings than investment instruments. For retirees (or

anyone, actually), they can be a very good place to park your liquid funds. They are flexible

alternatives to fixed deposit accounts, but without penalty for redemption. These bonds

are backed by the Singapore government and principal is guaranteed.

The SSB has a full tenure of 10 years and its interest is tied to that of Singapore

Government Securities (SGS). You get a coupon every 6 months. You receive less interest

at the start, but the interest steps up over time. The coupons and effective interest rates

you will receive are all announced prior to your investment. If you hold your SSB for the

full 10 years, your return will match the average 10-year SGS yield the month before your

investment.

The difference between SSBs and SGS is that you have the flexibility to redeem the bond

at any time, with a maximum waiting period of one month, without price risks. You always

get back your full principal even if you sell before the 10 years is up. In this regard, SSBs

are unlike Singapore Government Securities (SGS), which have to be sold on the secondary

market if you want to redeem them early. The price at which you can sell the SGS is

dependent on market factors. If the interest on newer issues of SGS has gone up, buyers

will ask for a lower price to compensate for the opportunity cost. If market forces move

the other way, the price of SGS can go up as well. Not so for SSBs. You get back what you

invested, no more, no less, and of course you keep the coupons you have already clipped.

In terms of overall return, an investor who holds an SSB for a given number of years wouldCHAPTER 4 | ADDITIONAL INCOME IN RETIREMENT 19

have an average return similar to that of an SGS of the same tenure. You even know what

this return is ahead of time!

SSBs deal with the risk of investing loss (given that they are not really a traditional

investment), but not inflation or other risks faced by retirees. They can complement your

retirement plan in two ways. The first is to receive the coupons, but these are not high. The

coupon rate for March 2019 issues are 1.95% in the first 12 months and step up to 2.55%

for a 10-year period. Assuming you buy into $100,000 worth of these SSBs and hold it till

maturity, you can expect to receive an average of just under $1,100 in coupons every 6

months. The second way is to draw down your SSBs by redeeming them gradually over set

time intervals or when you have unforeseen emergencies.

INTEREST FOR $100,000 INVESTED IN MARCH 2019 SSB

2550

2480

25000 2390

2300

2200

2130

2050

1950 1950 1970

Annual Interest ($)

2000

1500

1000

500

0

1 2 3 4 5 6 7 8 9 10

Years

You can buy SSBs through one of our three local banks – DBS/POSB, OCBC or UOB, via

the ATM or internet banking. You will need either a CDP account or an SRS account and

there is an administrative charge of $2 per application. The minimum investment amount

is $500, capped at a maximum holding level of $200,000. In months when the SSBs are

oversubscribed, you may not get your full allocation.

4.4 OTHER SOURCES OF INCOME

In an earlier chapter, we had talked about monetising your home for additional income

in retirement. In the event of severe disability in retirement, there may be payouts from

ElderShield or the upcoming CareShield Life to help in long-term care expenses, in addition

to what you may have from CPF LIFE/ Retirement Sum Scheme and investments.

We will cover this in our next chapter.

The saying goes that the journey of thousand miles begins with a single step.

So does a 20, 25 or 30-year retirement. We’ve listed down several ways you can

supplement your income for a more secure and purposeful retirement.

We hope you are encouraged to take them.5 A MEDICAL SAFETY NET

5

CHAPTER 5 | A MEDICAL SAFETY NET 21

A MEDICAL

SAFETY NET

The third Must-Have for Retirement – a strong healthcare

safety net that takes care of your healthcare needs.

Ageing is inescapable and as we age, our body’s healing ability declines significantly,

especially in the silver years. We become more susceptible to illnesses and injuries which

may eventually lead to some forms of disability. The Ministry of Health (MOH) estimated

that one in two healthy Singaporeans age 65 could become severely disabled in their

lifetime and may need long-term care. Furthermore, 3 in 10 severely disabled persons

remain disabled for 10 years or more. With rising medical costs and longer life expectancy,

it is no wonder that healthcare cost is an increasing concern among the seniors.

The cost of healthcare can come from 3 areas;

Outpatient treatments Hospitalisation Long-term care

Retirees should have a strong medical safety net in the form of savings and medical

insurance that can support their healthcare needs without compromising their standard

of living.

With the generous benefits under the Merdeka Generation Package, Merdeka Generation

seniors can now be more assured of their healthcare funding. Let us look at how Merdeka

Generation seniors can manage their healthcare funding in the following areas.CHAPTER 5 | A MEDICAL SAFETY NET 22

5.1 FIRST SAFETY NET – OUTPATIENT TREATMENTS

These are treatments for common ailments (e.g. cough and colds), dental care as well

as chronic conditions like hypertension and diabetes. The cost of treatment at GPs or

even specialist clinics are generally manageable but the on-going follow-ups for chronic

conditions can be a burden.

There are affordable options. Pioneer Generation (PG) and Singaporeans with low to

middle-income can enjoy subsidies at clinics participating in the Community Health

Assist Scheme (CHAS). With Budget 2019, this scheme is now extended to all Merdeka

Generation Singaporeans regardless of income:

• Special CHAS subsidies at CHAS GP and dental clinics, which are higher than CHAS

Blue subsidies (the more subsidised of the two CHAS tiers, for persons whose per

capital household income isCHAPTER 5 | A MEDICAL SAFETY NET 23

Age next MediShield Estimated MediShield Life Premium (2019 rates) after existing

birthday Life Premium subsidy based on household income and additional 5/10%

before subsidy discount for the Merdeka Generation

Lower income8 Lower middle Upper middle High income11

income9 income10

61-65 755 453 491 528 717

66-70 815 489 530 570 774

71-73 885 531 576 620 841

74-75 975 585 634 682 926

76-78 1130 565 622 678 1017

79-80 1175 588 647 706 1058

81-83 1250 625 688 750 1125

84-85 1430 715 787 858 1287

The table above is applicable for Singaporeans living in residences with an Annual Value of $13,000 or less, which covers all persons living in

HDB flats.7

The overall discount on the MediShield Life premium for the Merdeka Generation is quite

significant especially for the lower income. You can estimate your MediShield Life premium

by using the Premium Calculator on MOH’s website12 (before the 5%/10% Merdeka

Generation premium discount).

Is MediShield Life adequate for you?

MSHL is catered for those who will stay at Class B2 or C wards at restructured hospitals.

These are heavily subsidised wards with basic amenities and no flexibility to choose your

preferred doctors.

Those who prefer amenities such as air-conditioning, attached TVs and toilets or choice of

own doctors, may upgrade to an Integrated Shield Plan (IP) for:

• Restructured hospital in B1 ward

• Restructured hospital in A ward

• Private hospitals

WITH IP NO IP

Private hospitals A/B1 ward

Interestingly, more than 6 in 10 people in Singapore own an IP and about half of them are

catered for private hospitals. With rising IP premiums, some may find it no

longer affordable.

6. Refer here for subsidies rate for Permanent Residents and those living in larger properties. https://www.moh.gov.sg/MediShield-life/medishield-life-premiums-

and-subsidies/premium-subsidy-tables

7. Lower-income refers to individuals with a household monthly income per person of $1,100 or less.

8. Lower-middle-income refers to individuals with a household monthly income per person of $1,101 to $1,800.

9. Upper-middle-income refers to individuals with a household monthly income per person of $1,801 to $2,600.

10. High-income refers to individuals with a household monthly income per person of more than $2,600.

11. https://www.moh.gov.sg/MediShield-life/medishield-life-premiums-and-subsidies/medishield-life-premium-calculator#CHAPTER 5 | A MEDICAL SAFETY NET 24

Upgrading or downgrading your IP

Before making changes to your MediShield Life or IP, you should consider the following.

A F FOR DA B I L I T Y

The premium for MSHL/IP increases over time. Consider the current and future premium.

Age next MediShield Life Premium range of IPs in the market

birthday Premium (MSHL premium + Additional Insurer premium)

Restructured Restructured Restructured Private hospitals

B2/C ward B1 ward A ward

61-65 755 1063 - 1235 1229 - 1528 1874 - 2712

66-70 815 1292 - 1534 1727 - 2102 2639 - 3589

71-73 885 1610 - 2036 2163 - 2691 3337 - 4635

74-75 975 1834 - 2316 2519 - 3082 3744 - 5376

76-78 1130 2156 - 3042 2877 - 3868 4602 - 6503

79-80 1175 2337 - 3099 3132 - 4143 4924 - 7166

81-83 1250 2525 - 3800 3443 - 4974 5237 - 7780

84-85 1430 2897 - 4001 3884 - 5216 6176 - 8579

(Source: MOH website. The range of premium pertains to IP plans currently available for purchase. The premium does not include any plan

rider.) The MediShield Life Premiums shown above are before any subsidy given based on household income as well as the 5%/10% premium

discount for the Merdeka Generation (refer to the previous table for reference). With these subsidy and discount, the IP premium will be lower

than reflected above.

Note that you can pay the MediShield Life premium fully using Medisave.

Compare IP

For IP, you can only use Medisave to pay the additional insurer premium up to these caps:

plans here:

• $300 if you are 40 years old or younger on your next birthday.

https://www.

• $600 if you are 41 to 70 years old on your next birthday.

moneyowl.com.

• $900 if you are 71 years or older on your next birthday

sg/#/direct

If you must upgrade or downgrade your IP, the golden rule is to make changes within

the current insurer. If you switch to a different insurance company, the new insurer could

impose exclusion on pre-existing conditions that you may have. What this means is that

you cannot make any claims on the IP that is related to the excluded pre-existing condition.

5.3 THIRD SAFETY NET – LONG-TERM CARE

Many will require long-term care due to severe disability in old age. A person is severely

disabled if he or she is unable to perform at least 3 Activities of Daily Living (ADLs)

independently, namely, feeding, dressing, toileting, washing, mobility and transferring.

When it happens, caregiving is needed.CHAPTER 5 | A MEDICAL SAFETY NET 25

ElderShield was launched in 2002 to address the financial concern of long-term care.

Being a non-compulsory scheme, a significant number of people chose to opt-out

especially when it first started. The benefits of ElderShield are kept low for affordability.

Monthly payouts are either $300 for up to 5 years or $400 for up to 6 years.

Read our

CareShield Life

commentary From 2020, CareShield Life (an improvement from ElderShield) will be launched. Not only

on CareShield does it provide higher payouts of at least $600 (which increases till age 67 or when a claim

Life here is made, whichever earlier), the payouts are for life as long as severe disability persists.

https://advice. Severe disability can be due to a physical injury, illness or even severe mental impairment.

moneyowl.

com.sg/a- Merdeka Generation seniors who are not severely disabled can join CareShield Life in

singaporeans- 2021. To encourage Merdeka Generation seniors to join CareShield Life, an additional

help- participation incentive of $1,500 is given to join the scheme. This is on top of a previously

singaporeans- announced $2,500 sum, making it a total of $4,000 discount to offset CareShield Life

scheme/ premium. This is in addition to current means-tested premium subsidies.

Your CareShield Life premium is dependent on several factors including your age, gender,

citizenship, monthly per capita household income, residential property and whether you

are currently on ElderShield plan or not.

Estimated CareShield Life Premium Table for selected Merdeka Generation ages

(currently with ElderShield 300 and staying in an HDB flat)

Additional total premiums payable for 10 years - Male

Age Without SC - With all subsidy and incentives^ PR - With subsidy

subsidies

$0 - $1101 - $1801 - Above $0 - $1101 - $1801 - Above

$1100 $1800 $2600 $2601 $1100 $1800 $2600 $2601

62 7313 1374 1697 2020 3313 6344 6505 6667 7313

67 7490 1594 1910 2226 3490 6542 6700 6858 7490

Additional total premiums payable for 10 years - Female

Age Without SC - With all subsidy and incentives^ PR - With subsidy

subsidies

$0 - $1101 - $1801 - Above $0 - $1101 - $1801 - Above

$1100 $1800 $2600 $2601 $1100 $1800 $2600 $2601

62 9699 3125 3554 3983 5699 8412 8627 8841 9699

67 10,200 3608 4040 4472 6200 8904 9120 9336 10,200

Source: MOH website ^

Incentives include both Participation Incentive and Additional Participation Incentive for MG

For a male, age 62, Singaporean, whose monthly per capita household income falls within

the $1,101 to $1,800 range, his CareShield Life premium is estimated at $1,697 after

subsidy and incentives for ten years. This works out to less than $170 per year.

Premium without subsidy is estimated at $7,313, or about $731 per year.

For full details on CareShield Life and estimate your premium using the CareShield Life

Premium Calculator, you can refer to https://www.moh.gov.sg/careshieldlife/about-

careshield-life.

12. https://www.moh.gov.sg/careshieldlife/about-careshield-life/careshield-life-premium-calculator

13. If you have ever opted out and re-joined ElderShield, have a single or 10-year ElderShield premium payment plan or have a paid-up policy, your personalised

premiums will be available closer to 2021.CHAPTER 5 | A MEDICAL SAFETY NET 26

Those who opted out of ElderShield can either wait till 2021 to sign up for CareShield Life

or get immediate coverage by first applying for ElderShield provided they are not older

than 64 and are not severely disabled.

Should I switch from ElderShield to CareShield Life?

Monthly payouts of $300 to $400 under ElderShield are insufficient to meet long-term

care cost, especially as severe disability is likely to last longer than the 5-6 years after

occurrence.

While you may have income from CPF LIFE payouts, it can be a strain to pay for long-term

care costs out of these payouts.

Long-term care options include staying in a nursing home, being looked after by a helper or

family member at home, or a combination of day care and homecare. The cost can easily

range from $1,000 to over $3,000 per month before subsidies. Even after means-tested

subsidies and CareShield Life payouts of $600, there will still be a cost that has to be borne

out of one’s retirement income.

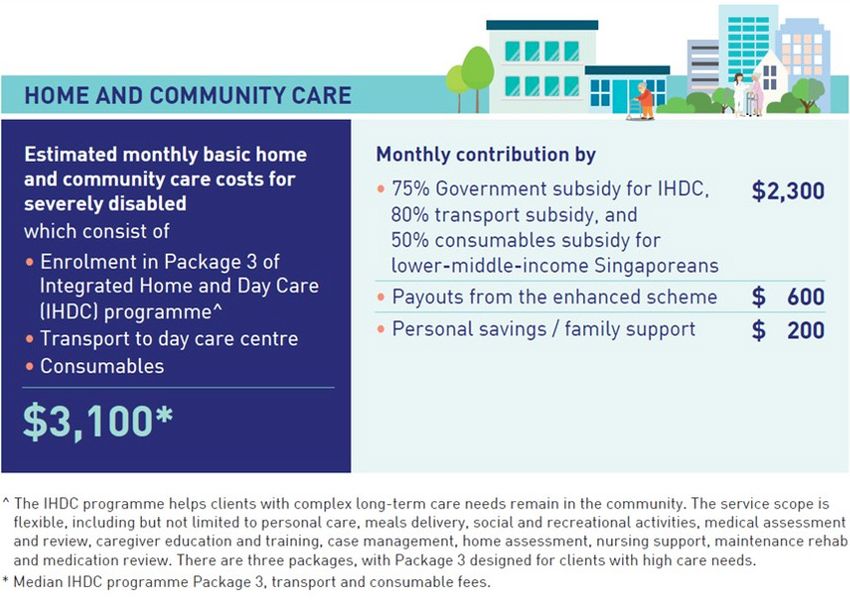

5.3 ESTIMATED COSTS OF LONG-TERM CARE OPTIONS

FOR LOWER-MIDDLE-INCOME SINGAPOREANS AFTER

SUBSIDY AND CARESHIELD LIFE PAYOUTS

Source: ElderShield Review Committee Report, 25 May 2018CHAPTER 5 | A MEDICAL SAFETY NET 27

Source: ElderShield Review Committee Report, 25 May 2018

Given the high probability of severe disability, the duration of disability should it happen

Compare and the strain of long-term care costs on the family, Merdeka Generation seniors who are

long-term care not yet severely disabled should consider joining CareShield Life early to take advantage

plans here of the Participation Incentives, if they are able to afford the premiums. This will provide a

https://www. better safety net for long-term care.

moneyowl.com.

sg/#/direct You can further enhance the payouts by adding a supplementary Long-Term Care Plan (or

ElderShield Supplement) from a private insurer.6 ESTATE DISTRIBUTION

6

CHAPTER 6 | ESTATE DISTRIBUTION 29

ESTATE

DISTRIBUTION

In this sixth and final chapter in the Merdeka

Generation series, we will be exploring estate

planning – one of the most important aspects of

financial planning that may often be overlooked by

seniors and younger people alike. Indeed, everyone

needs to plan ahead and take actions while they

still have mental capacity, as one never knows

when something may happen. For seniors in the

Merdeka Generation, there may be a heightened

sense of urgency as one starts to age.

Estate planning concerns the loved ones left behind upon your eventual passing, how you

can provide them with your hard-earned assets – leaving a legacy for your family and

loved ones, a final act of love.

So, what happens to our assets when we pass on? How would these assets be distributed

and who gets what? These are important questions that should be decided by none other

than you – the owner of your assets – and distributed in accordance with your wishes.

Without proper planning, we could be leaving a financial mess for our loved ones to pick

up after our passing.

Distribution of assets upon death – or estate distribution – need not be difficult. A better

understanding of the estate rules governing common assets such as property, CPF

savings, life insurance, and the benefits of having a will, and taking action thereafter, can

ensure that our assets will go to our intended beneficiaries without unnecessary hassle.CHAPTER 6 | ESTATE DISTRIBUTION 30

6.1 HOME PROPERTY

How your share of the property gets transferred upon death depends on how it is being

held, whether joint-tenancy or tenancy-in-common.

Most How your property will be distributed upon death

properties are

held under When one of the joint tenants dies, the decease's interest

Joint-tenancy

joint-tenancy. in the property will automatically be transferred to the

(Most common)

You can find remaining surviving owners.

out your

property Each tenant holds a separate and distinct share of the

ownership property and can transfer his or her share of the property

Tenancy-in-common

status here. to others via a will or, in the absence of a will, according to

Intestate Succession Act.

Take, for example, Mr and Mrs Tan who are joint-tenants of a property, and if, say, Mr Tan

passes on, the surviving spouse (Mrs. Tan) will inherit and become the sole owner of the

property. As the property is under joint-tenancy, Mr Tan cannot create a will to distribute

away his share. However, if the property is held under tenancy-in-common, Mr Tan could

write a will to distribute away his share to others.

What if yours is a HDB flat?

HDB flat can only be retained if the beneficiaries fulfil certain eligibility criteria including

Singapore Citizenship or Singapore Permanent Residency and are at least 21 years of age;

otherwise, it must be sold.

6.2 CPF SAVINGS

You should make a CPF nomination to specify how your CPF savings should be distributed.

In the absence of a CPF nomination, your CPF savings will be transferred to the Public

Trustee’s Office for distribution to your family under the Intestate Succession Act or the

Inheritance Certificate (for Muslims).

Your CPF savings cannot be distributed via a will.

The process of disbursement via CPF nomination is swift, and I have personal experience

in this regard. When my father passed on a few years ago, the CPF Board disbursed the

CPF monies to my mum (the nominee) very quickly within 3 weeks because my late father

did a CPF nomination. To my mum, it was not so much the money she inherited, but the

expediency of settling such matters did help to bring about a closure sooner.

What does a CPF Nomination cover?

Not all assets involving CPF are covered by a CPF nomination. Those assets not covered

must be addressed separately.

Cover under CPF Nomination Not covered under CPF Nomination

1. CPF savings* in your Ordinary, Special, 1. Properties bought using your CPF savings

MediSave and Retirement accounts

2. Payouts from Dependants' Protection Scheme (DPS)

2. Unused CPF LIFE premiums,

3. Cash and investments held in the CPF Investment Account

3. Discounted SingTel shares under the CPF Investment Scheme-Ordinary Account (CPFIS-OA)

*CPF savings cannot be included in your Will. They 4. Investments held under the CPF Investment Scheme-Special

also do not form your estate and are protected from Account (CPFIS-SA)

creditor claims on any outstanding debts.

(Source: CPF)CHAPTER 6 | ESTATE DISTRIBUTION 31

What are the different types of CPF Nomination?

Before making a CPF nomination, do note there are 3 types to choose from depending on

your needs.

1. Cash Nomination – this is the default option. In this nomination, your nominees will

receive the CPF savings in cash. Download the form here (URL: https://www.cpf.gov.sg/

Members/Schemes/schemes/other-matters/cpf-nomination-scheme).

2. Enhanced Nomination Scheme Nomination – Your nominees will receive the CPF savings

in their CPF accounts. You can decide to transfer your CPF savings to their:

• MediSave account – for their healthcare needs; or

• Special account – for their retirement needs.

Visit any of the CPF Service Centres to make this nomination.

3. Special Needs Savings Scheme Nomination – this allows parents to nominate their

special needs children to receive the CPF savings on a monthly basis. To make this

nomination, you would need to work with the Special Needs Trust Company (SNTC) and

the CPF Board. More information on this scheme here.

6.3 LIFE INSURANCE POLICIES

If there are no beneficiaries named in your insurance policies, the proceeds can be

distributed by way of a will or, in the absence of a will, by Intestate Succession Act.

With effect from 1 September 2009, you can make a revocable nomination or a trust

nomination on your insurance policies for your beneficiaries.

• A trust nomination – it is irrevocable and is meant to benefit your spouse

and/or children.

• A revocable nomination – can name any person as a nominee and can be revoked

anytime by you.

If there are beneficiaries named in your insurance policies before 1 September 2009,

there could be some potential issues:

• If the named beneficiaries are a spouse and/or children, your policy is now under

Section 73 of the Conveyancing and Law of Property Act, essentially you have

created a statutory trust. This cannot be revoked unless the named beneficiaries

give their consent.

• If the beneficiary is anyone other than spouse or children, there may be issues

regarding its validity. Hence it may be prudent to remove the named beneficiary and

do a revocable nomination or distribute it by way of a will.CHAPTER 6 | ESTATE DISTRIBUTION 32

6.4 HAVING A WILL

Other than most circumstances as explored above, the decease's estate of a non-Muslim

will be distributed either by way of a will or, in its absence, according to the Intestate

Succession Act.

Death without a Will – Intestate Succession

Without a will, the distribution of a decease's estate will follow the priority as set out by

the Intestate Succession Act (ISA).

Deceased dies intestate leaving: Distribution

Spouse Spouse 100%

(No parents or issue*)

Spouse, Issue Spouse 50%

(With or without parents) Issue (To be shared equally) 50%

Issue Issue 100%

(No spouse) (To be shared equally)

Spouse, Parents Spouse 50%

(No issue) Parents (To be shared equally) 50%

Parents Parents 100%

(No spouse or issue) (To be shared equally)

Siblings Siblings 100%

(No spouse, issue or parents) (To be shared equally)

Grandparents Grandparents 100%

(No spouse, issue, parents or siblings) (To be shared equally)

Uncles and Aunts Uncles and Aunts 100%

(No spouse, issue, parents, siblings or (To be shared equally)

grandparents)

None of the above Government 100%

*”issue” – includes children and the descendants of deceased children.

Under the ISA, spouse and children take precedence over parents, siblings and other

family relationships. While it may seem logical with some, such a distribution order can be

problematic, such as:

• A married person with children hopes to leave behind something for his or her parents.

Under ISA, the parents are excluded.

• A single person wishes to provide for both his or her parents and siblings. Siblings are

excluded in this case.

These issues can be easily solved by having a will.

Benefits of a will

With a will, you can decide who your beneficiaries are and how much they get. Equally

important is the control you exercise to choose whom you trust to be your executors,

trustees and guardians. Having a will can also avoid the potential conflicts and disharmony

among loved ones who may dispute how the estate should be distributed. Lastly, the

process of administrating the estate is generally faster with a will than without one.CHAPTER 6 | ESTATE DISTRIBUTION 33

Interestingly, many people do not have a will. Common reasons being the high cost of

writing a will, not knowing how to begin, and perhaps the time is not right.

With MoneyOwl’s online will writing service, which is complimentary with a promotional

code, there is no reason to put off will writing any further. The guided will writing process

will help you draft out your will in no time. Get it printed and signed before two witnesses

(who cannot be a beneficiary or the spouse of a beneficiary) and your will is legally

binding. If you need to make further edits, just come back and use the service again.

Start writing your will here More info on Why Write a Will?

Lasting Power of Attorney (LPA)

Finally, do consider making a Lasting Power of Attorney while you have the mental

capacity to do so. An LPA basically allows you to appoint one or more people [‘donee(s)’]

to manage your personal welfare and property should you (‘donor’) lose mental capacity

one day.

A donee can be appointed to act in 2 broad areas, whether separately or jointly:

• Personal welfare – such as, where and who should donor live with, healthcare matters,

what to wear and eat.

• Property and affairs – such as dealing with the donor’s property, managing bank

accounts, investing and making purchases of equipment for donor’s needs.

To make a LPA, you need to:

• Fill up a form from the Office of Public Guardian. Till 31 August 2020, the LPA

application fee is waived for the more common LPA option (Form 1).

• Engage a certificate issuer to sign as a witness and certify that you understand the

implications of an LPA. A certificate issuer could be an accredited medical practitioner, a

practising lawyer or a registered psychiatrist. The average fee charged by an accredited

practitioner is about $50.

• Send the form and certificate back to the Office of Public Guardian for registration. If

there are no valid objections in the six-week waiting period, your LPA will be registered.

The stamp of the Office of Public Guardian will be impressed on the registered LPA. The

Office of Public Guardian will send it back to you for safekeeping.THANK YOU!

You can also read