Take Solutions Ltd. Initiating Coverage - Embracing change, TAKE a leap towards growth !! - Axis Direct

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Initiating Coverage

Take Solutions Ltd.

Embracing change, TAKE a leap towards growth !!

19 Dec 2018

19 Dec 2018 Company Report

BUY

Target Price: 178

CMP : Rs. 136

Potential Upside : 31%

MARKET DATA

No. of Shares : 14.79Cr.

Market Cap : 2011Cr

Take Solutions

Free Float : 727 Cr

Avg. daily vol (6mth) : 13970

52-w High / Low : Rs127/308

Bloomberg : TAKE:IN

Life Sciences Outsourcing

Promoter holding : 66.8%

Embracing change, TAKE a leap towards growth !!

Price performance

200

160

120

80

Dec-17 Mar-18 Jun-18 Sep-18 Dec-18

BSE Sensex Take Solutions

Financial Summary Shareholding pattern

Y/E Sales EBITDA PAT EPS Change RoCE DPS Sep-18 Q-o-Q Change Jun-18

P/E (x) RoE (%)

March (Rs Cr) (Rs Cr) (Rs Cr) (Rs) (%) (%) (Rs) Promoters 66.8 0.00 66.8

FY17 1345 262 146 11.2 6.9 - 19.1 20.7 1.0 FPIs 13.78 1.00 12.78

FY18 1587 306 160 12.2 9.3 - 14.1 16.9 1.5 MFs / AIF 1.44 (0.04) 1.48

FY19E 1996 397 214 14.6 19.4 9.2 14.9 18.5 1.5 Banks / FIs 0.2 0.02 0.17

FY20E 2404 474 264 17.8 22.0 7.5 15.6 19.8 2.0 Public 7.52 (0.49) 8.01

FY21E 2941 574 331 23.6 32.9 5.7 17.5 22.1 3.0 Others 10.27 (0.49) 10.76

Source: Company, Axis Securities CMP as on 18 Dec 2018

Kumar Nihal – Manager - Research | kumar.nihal@axissecurities.in | (+91 22 4267 1747) 2

19 Dec 2018 Company Report

Take Solutions Ltd.

Investment Rationale Sector: Life Sciences Outsourcing

Incorporated in 2000, Take Solutions Limited(TSL) is a globally recognized technology service provider with distinct expertise across

Life Sciences (LS) and select niches in Supply Chain Management (SCM). In the fast-growing Life Sciences space, TSL offers services

ranging from Clinical Trials for innovative drugs, Bioavailability and bioequivalence (BA-BE) studies for generics drugs, regulatory

submissions and post marketing safety monitoring (Pharmocovigilance) backed by IP-based technology expertise. Headquartered in

Chennai, India with a global footprint spanning America, Europe and the APAC, TSL brings together the capabilities of a full-service

CRO (Contract Research Organization), a technology-led Life Sciences services provider, and expertise in analytics and data

sciences under its Life Sciences brand Navitas Life Sciences. TSL serves 9 out of top 10 Pharma Companies. It is represented by

1500+ professionals across 16 offices in 7 countries.

We estimate revenue to grow at CAGR of 23% over FY18-FY21E and PAT to grow at CAGR of 30% over FY18-FY21E driven by:

Growth trajectory in Life Sciences segment following restructuring of TSL and focus on developing niche in Life

Sciences via domain expertise

Huge gamut of opportunity lying in Clinical business as development spending for R&D in the phase I - IV during

CY18 is estimated to be $93bn (~39% being outsourced)

Take Solutions

growth would be Frequent changes in regulatory requirements leading to 11.5% CAGR over CY17-21E in regulatory submissions

driven by being outsourced

End-to-end BA & BE services to fast track in achieving client’s first to market strategy with its state-of-the art

USFDA compliant facilities in Manipal, Mangaluru, Bengaluru and Chennai

Focus on expansion with organic as well as inorganic growth, tangible assets addition is expected to be

Rs 200 Cr by FY20

We initiate coverage with “BUY” rating with a target price of Rs 178 i.e. 31% upside (implies 10x FY20E)

3

19 Dec 2018 Company Report

Take Solutions Ltd.

Investment Rationale Sector: Life Sciences Outsourcing

Large addressable market Robust revenue growth Patent expiry to drive Clinical Trials

The global Life Sciences R&D TSL has grown at strong CQGR of Global drug sales at risk is expected

expenditure is growing at 3.1% 8%+ for the last 12 quarters led by to be $ 251 bn over CY18-24 due

CAGR and expected to reach $204 growing LS vertical (91% of Q2FY19 to patents expiration. Pharma

bn by CY24. R&D spend for the revenue). Management expects 22- companies are increasing R&D

CY18 is estimated to be $172 bn. In 24% annual revenue growth in this spend to replenish the sales and

this gamut, development spending in segment for next two financial years bring new patent drug, thereby

the phase I to IV stands at $93bn as which would be slightly offset by de- increasing the need for Clinical

per Industry Standard Research growth in SCM as TSL has Trials. Expiry of patent drugs and

(ISR), the business presence of TSL is strategically exited two parts of SCM government’s thrust for cost efficient

in outsourcing space which is ~39% business and are in talks for getting drug would generate demand for

of development spending i.e. $36 suitable deals for its last part, post BA-BE studies to bring more generic

bn for CY18 Joseph

and estimated to reach which it will be 100% LS business

Joseph Josephbuilt the credentials to

drugs. TSL has

at $44bnHeading

by CY21, representing a Heading

with strong EBITDA margin of ~20%. Heading

help generics client achieve first to

large addressable market for TSL. TSL’s order book for Q2FY18 stood market strategy with its state-of-the

at $ 228 Mn, a growth of 48.5 % art USFDA compliant facilities at

YoY, pipeline visibility is expected to multiple locations.

be more than double the order book

which may get reflected in order

book in the next 3-4 months.

4

19 Dec 2018 Company Report

Take Solutions Ltd.

Investment Rationale Sector: Life Sciences Outsourcing

Domain Expertise Expansion

TSL has deep domain expertise in TSL’s focus is in on expanding Clinical

the LS segment with respect to sites and Lab infrastructure such as

consulting, technology (own as well investment in Liquid chromatography–

as third-party software mass spectrometry (LCMS) to serve

implementation) and outsourcing the growing demand from Life

services. A total of 30+ Sciences companies. Total tangible

experienced executives at senior asset addition is expected to be Rs

position were brought on board this 200 crore by FY20. Technology &

year. TSL has always relied on a automation is the differentiating factor

technology-driven approach and for the company and they are

investing on developing Intellectual

workforce include domain experts in

Joseph property. The

Josephexpansion plan would

clinical trials and drug development

Heading include Heading

organic growth via

process comprising Medical

investments as well as inorganic

doctors, PhDs or Bio-statisticians.

growth via acquisition. TSL is in talks

This results in higher quality work

for acquisition in North America

and sticky revenues which region, funding for which would be

differentiates TSL from a BPO done by internal accruals and is

company which relies on low-cost expected to be completed by the end

labour. of FY19.

5

19 Dec 2018 Company Report

Take Solutions Ltd.

Global Life Sciences Industry Outlook Sector: Life Sciences Outsourcing

Worldwide total prescription drug sales 2011-2024

1200

1000

800 828

785

In $ bn

749

600 706

631 663

576 583 608

590 572 569 581 565

400

200 216 240 262

138 151 169 192

77 82 88 94 100 112 125

66 67 70 76 78 80 81 84 89 95 100 104 109 114

0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Source: EvaluatePharma Generics Orphan Presciption (exc. Generics)

Worldwide prescription drug sales

Worldwide prescription drug sales are expected to be US$1.2

New Molecule entities (NMEs) FDA approvals in

trillion in CY24.Global sales are forecast to grow at 6.4% CAGR 55

2017, rebounding from 27 in 2016

over CY17-24. This growth is in contrast to the 1.2 % CAGR in

CY11-17 Additional sales in 2024 from orphan drugs

$124bn

(commercially undeveloped)

With the arrival of the fourth industrial revolution, the life sciences

sector continues to embark on a transformative technology journey

2017-2024 CAGR for oncology

Companies, today, are preparing for the future by embracing +12%

Key (tumours studies/treatment))

these technologies and building a patient-centric culture. Strategic Drivers

alliances and new operating models are also contributing to $5bn Additional sales in 2024 from advanced therapies

overall growth in the sector

6

19 Dec 2018 Company Report

Take Solutions Ltd.

Growing R&D spend Sector: Life Sciences Outsourcing

Global pharma R&D to grow at 3.1% CAGR over CY17-24 NMEs approvals indicating increase in productivity

250 25% 60 35

21%

19% 17%

200 20% 50 30

25

150 15% 40

In $ bn

20

In $ bn

100 10% 30

15

20

50 5% 10

199

129

137

136

138

159

165

172

177

183

188

144

149

204

194

10 5

29

37

26

35

38

28

25

31

35

26

35

44

35

51

56

55

0 0%

0 0

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Global Pharma R&D spend (LHS) R&D as % of drug sales (RHS) New Molecule Entities(NMEs) USA sales 5yrs Post Launch ($bn)

(LHS) (RHS)

Worldwide pharmaceutical R&D spend totalled $165bn in 2017 Following the drop in CY16 NME approvals, CY17 suggests a

representing an increase of +3.9% on the previous year return to form in industry R&D productivity

Worldwide pharmaceutical and biotech R&D is forecast to grow at R&D value creation seems to be at an all-time high with total USA

3.1% CAGR over CY17-24, slightly lower than the 3.6% CAGR sales 5 years post launch for products approved in CY17 reaching $

over CY10-17. Total R&D spend is expected to reach US$204 33.2 bn

billion in CY24, compared to US$165 billion in CY17 Significant innovation is coming from small niche companies focused

The industry is increasingly looking towards employing big data on discovering new drugs. Less than 25% of drugs discovered are

and predictive analytics to improve R&D efficiency brought to market by the big pharmaceutical companies

Source: EvaluatePharma, Axis Securities

719 Dec 2018 Company Report

Take Solutions Ltd.

Technology accelerating R&D Sector: Life Sciences Outsourcing

The use of big data for evidence generation could vastly improve the speed and outcomes of clinical

development. Artificial Intelligence, real-world evidence (RWE), and robotic and cognitive automation are

expected to bring transformational change to R&D. These emerging technologies can improve study design,

physician and patient recruitment, and in-trial decision making as well as increase efficiency and accuracy in

repetitiveoftasks

Application RWE all the way through to regulatory filings.

in R&D

Support evidence generation across a product lifecycle

Understand

Help understand the burden of the disease, illuminate any unmet needs & provide

rare diseases epidemiological data

Reduce the cost and time it takes to execute a trial

Serving as a control

Demonstrate improvements in outcomes that are of interest to health plans and health

arm in clinical trial care providers

Supporting Compare before and after drug treatment data with clinical trial data to determine

label expansion any other potential indications

Expediting patent Ability to better track and connect with patients, allowing patient enrollment to occur

enrolment at the point of care

Expediting the development Potential to expedite assessment when there is no time or opportunity to conduct a

of life-saving treatments randomized clinical trial

819 Dec 2018 Company Report

Take Solutions Ltd.

Growing need for Outsourcing Sector: Life Sciences Outsourcing

Clinical Services Outsourced Vs In-house ratio 2017 Advantages of Outsourcing to Life Sciences Company

100%

(Sponsor)

18% 20% 0%

80% 40% 38% 28%

55% 55% 45%

60% Increased management bandwidth:

60%

100% To focus on core activities

40% 82% 80% 72%

60% 62% 55%

20% 40% 45% 45%

0% Reduced cost of drug development:

To remain competitive in the market

Lab Services

PDS

Regulatory

Late Stage CT

Stage CT

Trial Supplies

Staffing

management

Clinical

Biostatistics

Clinical

Affairs

Early

Central

Clinical

IT

Data

Reduced time to market:

Enables quick turn around time

Outsourced In-house

Source: PAREXEL biopharmaceutical sourcebook 2016/17

Outsourcing to take larger pie in increasing drug development market Growing Outsourcing Market Size

50

43.9

Safety (PV): 13.8 % CAGR 45 41.1

38.8

$ 1.94 bn (CY17) to $ 3.25 bn (CY21) 40 36.8

34.3

$ 34 bn 35 31.6

Regulatory: 11.5 % CAGR

(2017) $ 2.76 bn (CY17) to $ 4.2 bn (CY21) 30

in $ bn

25

Clinical: 5.2 % CAGR $ 44 bn

$ 29.7 bn (CY17) to $ 36.3 bn (CY21) 20

Clinical Trial (2021)

15

Regulatory Submission 10

PV 5

0

CY16 CY17 CY18 CY19 CY20 CY21

Source: ISR, Axis Securities Source: ISR, Axis Securities

919 Dec 2018 Company Report

Take Solutions Ltd.

Take Solutions Sector: Life Sciences Outsourcing

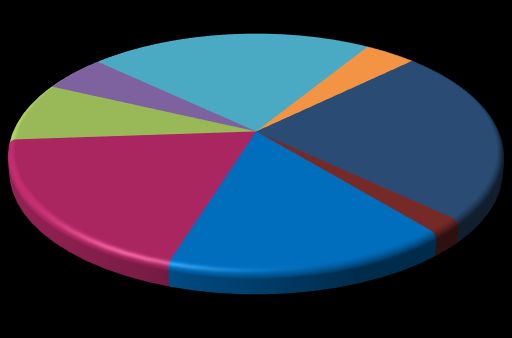

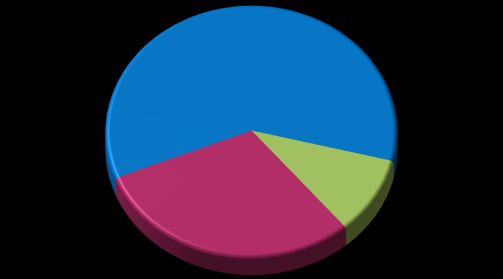

Introduction Shareholding (Sep-18)

Incepted in 2000, Take Solutions Limited (TSL) delivers domain- 7.52% 10.27%

0.2%

intensive, technology-led services in Life Sciences Industry(91%, 1.44%

Q2FY19) and Supply Chain Management(9%)

13.78%

Life Sciences: The company offers IP-based solutions in clinical, 66.8%

regulatory, safety and consulting processes to global Life

sciences companies across multiple therapeutic areas. Global

clients include large and small innovator biopharmaceutical

companies as well as generics manufacturers. TSL brings Promoters FPIs MFs / AIF Banks / FIs Public Others

together the capabilities of a full-service Contract Research Source: Company, Axis Securities

Organisation (CRO), a technology-led Life Sciences services Revenue Concentration by Segments

provider, and expertise in analytics and data sciences under its 100%

17% 12%

Life Sciences brand Navitas Life Sciences across North 29% 23%

80% 39%

America, Europe, Asia, and South America region.

60%

Supply Chain Management: TSL focuses on niches in 88%

40% 77% 83%

71%

engineering services, and supply chain collaboration. However 61%

20%

Company has decided to exit this business to focus on its

0%

expertise as niche service provider for Life Sciences.

FY14 FY15 FY16 FY17 FY18

Life Sciences Supply Chain Management

Source: Company, Axis Securities

1019 Dec 2018 Company Report

Take Solutions Ltd.

Global presence: 16 offices in 7 countries Sector: Life Sciences Outsourcing

Revenue contribution by region over FY16-18

FY16 FY17 FY18 FY16 FY17 FY18 FY16 FY17 FY18

74 % 79.3% 80.1% 9% 7.4% 6.5% 17% 13.3% 13.4%

01 America Europe 02 03 Asia Pacific

USA HQ: Princeton, NJ Europe HQ: Frankfurt, Germany APAC HQ: Chennai, India

Clinical, Regulatory & Safety consulting Major trial operations centre in Germany Clinical Operations (Incl. Generics) in

and technology centers. and sites through Europe in UK, Sweden, Bangalore, Chennai, Mangalore and

Trial operations through strategic Germany, Poland, Denmark, Russia and Manipal Regulatory & Safety operations

partnerships other locations hub in Chennai & Bengaluru

LATAM Delivery Centre: Bogota,

Columbia Regulatory & Safety support

across 9+ countries in region

Source: Company, Axis Securities

1119 Dec 2018 Company Report

Take Solutions Ltd.

Management Expertise & Industry Recognition Sector: Life Sciences Outsourcing

Mr. Ram Yeleswarapu Industry Recognition, Awards & Accolades

- A widely acknowledged industry thought leader, Ram Yeleswarapu co- - The Company’s domain centricity was recognized in the form of a

founded the organization’s Life Sciences business and has been a key

contributor to its growth. He leverages deep domain expertise from listing as ‘Leader’ in the prestigious IDC MarketScape: Drug Safety

over 25years of industry experience with large global pharmaceutical Services 2018 Vendor Assessment as one of only eight vendors

organizations

selected based on the MarketScape’s stringent research and due

Mr. Srinivasan HR diligence process.

- Gartner recognized TSL amongst Top 20 Global Solution Providers in

- Founder of TSL. He brings over 3 decades of leadership and has held

its Market Guide for Track-and-Trace and Serialization Software

significant leadership positions in organizations including the Shriram

Group, Sembcorp Logistics and Temasek Capital Providers for Life Sciences Companies

- Award-winning talent management practices continued to receive

Mr. D.V. Ravi accolades in the form of the Best Employer Brand for the second

- Co-founder of TSL. He is also the Managing Director of Shriram consecutive year at the World HRD Congress 2018, where it also

Capital, a financial services conglomerate with USD15 Billion AUM. ranked 3rd in the Times Ascent presents Dream Companies to Work For

His portfolio of expertise includes key areas of Corporate Strategy,

Finance and Leadership Development. He has an exemplary track category

record of value creation across several enterprises - Earned a place in the Great Place to Work global listing, the global

authority on building, sustaining and recognizing exemplary workplace

Mrs. Subhasri Sriram

culture and best practices

- Has over 25 years of experience in Financial Services and has served - ISO 9001:2015 for Quality management systems, ISO 27001:2013

in key leadership positions in the Shriram Group. She was the CFO of

for Information Security Management, NABL (ISO 15189:2012)

the USD2.4 Billion Shriram City Union Finance. She has expertise in

setting up strong governance systems and transparent processes. She accreditation for clinical laboratory

was recognized as one of the most influential CFOs in India by

Chartered Institute of Management Accountants in 2016

Source: Company, Axis Securities

1219 Dec 2018 Company Report

Take Solutions Ltd.

Evolution from Supply Chain to Life Sciences Sector: Life Sciences Outsourcing

Successfully exited from

two SCM units, a 100%

TAKE Solutions was

owned unit in the US and a

founded in Chennai,

Middle East Joint venture

India as a software

Acquired UK-based WCI Consulting Group, a with the WJ Towell Group

products company

Acquired Ecron

leading patient safety and compliance advisor to the in Oman

focused on Supply Acunova, a full-

Chain Management Life Sciences industry service CRO with TSL would be 100% Life

Launched SafetyReady to increase the efficiency of Clinical & BA/BE Sciences Outsourcing

Inaugurated North

Oracle Argus Safety Suite for Life Sciences capabilities Company post its exit from

American headquarters

its APA engineering Joint

at Princeton, New Recognized as a Leader in IDC MarketScape: 100th pharmaRea- Venture

Jersey, USA Worldwide Life Sciences R&D IT Outsourcing 2011 dy customer win

2000-04 2007-10 2011-14 2015 2016 2017 2018

Acquired OnSphere Corporation, North Carolina, USA, Launched cdsnet, a proprietary Consolidated Life Sciences businesses under the

an IP-driven leader in regulatory compliance for Life industry network on Clinical Data brand Navitas Life Sciences to provide full

Sciences Strategy services across Clinical, Regulatory and Safety

Launched OneSCM, a multi-tenant SaaS platform to Launched India’s first propriety Launched Labeling Assessment Express to

improve enterprise supplier management industry network on improve End-to-End labeling for Life Sciences

pharmacovigilance, pvindia

Acquired ClearOrbit, a Supply Chain Management Celebrated the landmark 15th year of proprietary

software company in Austin, Texas, USA Life Sciences industry network forums

Registered a successful IPO and listed on BSE & NSE

1319 Dec 2018 Company Report

Take Solutions Ltd.

Life Sciences drug development landscape Sector: Life Sciences Outsourcing

Manufacturing: Approved drugs

Mfg.

are mass produced & sold to the

Regulatory Submission

public

Safety of drug in monitored

Safety Monitoring

and reported regularly as

long as drug is in the market

Safety Monitoring: The molecule is

monitored and adverse events are

reported at each stage ~ 1/10000 identified

compounds are approved

Human Trials

Regulatory Submission: The

findings are submitted to the Phase I 10s Volunteers

CT

regulator for approval at each Phase II 100s Patients

stage Phase III & IV 1000s Patients

Animal Trials

CT

Clinical Trials (CT): The molecule

is tested for its safety & efficacy

Research

Basic Research: Molecule

formulation is identified to combat

a disease

1419 Dec 2018 Company Report

Take Solutions Ltd.

Role of Take Solution in Life Sciences business Sector: Life Sciences Outsourcing

Take Solutions’ Business presence

Manufacturing: Approved drugs

Mfg.

are mass produced & sold to the

public

Regulatory Submission

Safety Monitoring

Industry Growth

Size 2021

2017 (CAGR%)

Safety Monitoring: The molecule is Safety

monitored and adverse events are $1.9bn $3.2bn (13.8)

monitoring

reported at each stage

Regulatory

$2.8bn $4.3bn(11.5)

submissions

Regulatory Submission: The Clinical

$29.7bn $36.4bn (6%)

Trial

findings are submitted to the

CT

regulator for approval at each

stage

CT

Clinical Trials (CT): The molecule

is tested for its safety & efficacy

Research

Basic Research: Molecule

formulation is identified to combat

a disease

Source: ISR, Axis Securities

1519 Dec 2018 Company Report

Take Solutions Ltd.

Take Solution Service Mix Sector: Life Sciences Outsourcing

TSL Revenue breakup (FY18) Supply Chain Management (SCM)

TSL started as a software products company focused on Supply

Chain Management (SCM). SCM lacked differentiation despite

presenting growth and better pricing was difficult to come by, so

TSL strategically decided to exit this business. SCM contributed

59% 29% 12% to the FY18 revenues which has come down to 9% for

12% 88%

H1FY19 and is expected to be phased out by end FY19

11%

SCM business has three parts and TSL have successfully exited from

two of them and are in the process of a finding a suitable

transaction for the third one

Regulatory & PV Clinical

Life Sciences Supply Chain Management

Nets & Consulting

Life Sciences (LS)

Source: Company, Axis Securities Clinical Trial services Regulatory Offerings Safety Services /PV

TSL moving towards 100% Life Sciences

Strategic clinical Regulatory consulting Strategic Safety

100% consulting Global submission Consulting

17% 17% 14% 13% 12% 9% 9% 9% Full service Clinical management and Safety Industry

80% trials report publishing Networks

60% Medical Imaging Medical writing End-to-End

87% 88% 91% 91% 91% Services License maintenance Pharmacovigilance

40% 83% 83% 86%

Bioavalibility & for marketed product (PV) Services

20% Bioequivalence Application Pharmacovigilance

Studies management services Technology

0%

Biologics & Industry networks:

Q3FY17

Q4FY17

Q1FY18

Q2FY18

Q3FY18

Q4FY18

Q1FY19

Q2FY19

Biosimilars Studies CCDS, labeling, and

Non-interventional artwork

Studies

Clinical data Sevices

Life Sciences Supply Chain Management

One Clinical platform

Source: Company, Axis Securities

1619 Dec 2018 Company Report

Take Solutions Ltd.

Extensive Expertise in Life Sciences Sector: Life Sciences Outsourcing

250+ 8% All 20+ Non- 10 Unique

350+ Validated Submission interventional proprietary Life

Clinical Bioanalytical to USFDA Studies Sciences Industry

Trials Methods in 2017 annually networks

1000+ 120,000+ 300+ Safety 7% of all Biosimilars 120 members

BABE Lab Submissions with Consulting studies in India in in Network

Studies 0 refusal to file Engagements 2017 forums

Life Sciences driving the growth: 8%+ CAQR growth for last 12 quarters

TSL has always relied on a

250 221 OneClinical technology-driven approach

190 and workforce include domain

200

151 pharmaREADY experts in clinical trials and

141 141

In USD Mn

150 134 drug development process,

Unique comprising Medical doctors,

traceREADY

100 64 64 67 technology PhDs or Bio-statisticians. This

47 50 55

50 IPs labelREADY results in higher quality work

driving Life and sticky revenues which

0 affiliateREADY differentiates TSL from a BPO

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19 Sciences company which relies on low-

safetyREADY cost labour

LS order book LS revenue

Source: Company, Axis Securities

1719 Dec 2018 Company Report

Take Solutions Ltd.

TSL to leverage opportunity created from Patent Expiration Sector: Life Sciences Outsourcing

Drug Sales at Risk from Patent Expiration Patent drugs: R&D spend to replenish pipelines

80

6%

7% Global sales at risk from expiry of patent drugs is expected to

70 6% be $ 251bn over CY18-24. Global pharma companies are

5% 5%

60 increasing R&D spend for new patent drugs to replenish lost

5%

50

4% sales

4%

In $ bn

40

2% 2% 2%

3% Small niche companies leading the innovation on discovering

30

2% new drugs. Less than 25% of drugs discovered are brought to

20

market by the big pharmaceutical companies

10 1%

39 26 43 23 17 19 17 15 41 15 67 22 27 19

0 0% TSL would leverage on these tailwinds providing full fledged

2018 2019 2020 2021 2022 2023 2024

outsourcing services for faster and cost effective clinical trials to

Total Sales at Risk Expected Sales Lost % Market at Risk sponsor companies

Source: EvaluatePharma, Axis Securities

World-class bioequivalence facilities State-of-the art Generics: Large gamut of opportunity

Bio analytical capabilities

TSL’s would also benefit as patent expiry along with government

48 bed clinical thrust for cost efficient drug would generate demand for BA-BE

Pharmacology Unit

studies

Bioanalytical Lab

Manipal Bioanalytical Lab

Bangalore TSL has the ability to help generics client achieve first to market

strategy with its state-of-the art USFDA compliant facilities at

Mangalore multiple locations

TSL Conducted 7% of All Biosimilars Trials in India in 2017

80 bed clinical Chennai 80 bed clinical

Pharmacology Unit Pharmacology Unit

Source: Company, Axis Securities

1819 Dec 2018 Company Report

Take Solutions Ltd.

Increasing share of Clinical business to continue Sector: Life Sciences Outsourcing

Revenue breakup of Life Sciences business

80% of the outsourcing growth

FY16 FY17 FY18 FY21E opportunity lies within Clinical

business; being highly

27% 29% 60% underpenetrated, entry barriers

5%

15% like multiple regulatory

12% 11% requirements and high domain

knowledge positions TSL to reap

the benefits of growing pie

10%

80% 61% 59% The margins in Clinical business

30%

is healthy at 16-18%, though

lower than regulatory & PV

segments

Regulatory & PV Clinical Nets & Consulting

Clinical business would continue to grow its share in revenue and management plans to have ~60% revenue share from Clinical Trials by FY21E

OneClinical: Patent technology TSL presence across 20+ therapeutic areas to increase further

20% Top Drug sales by growth (2017-24 CAGR)

Optimized eClinical and Analytics Clinical Trials Management Platform

16%

Offers Comprehensive Trial Oversight and Enables Faster Decisions

12%

8%

OneClinical 4%

0%

Reduces Cost of Lower risk of trial quality

Trial by 25% issue by 20%

Owing to lower feet on With early detection and

ground monitoring mitigation

TSL is present in 4 of the top 5 therapy areas by growth

1919 Dec 2018 Company Report

Take Solutions Ltd.

Domain expertise in Regulatory Submissions & Pharmacovigilance (PV) Sector: Life Sciences Outsourcing

Regulatory Submissions and PV are high margin (22-25%) business segments for TSL due to in-depth subject matter expertise, competencies and

technology enabling them being cost efficient

Technology Solutions

Regulatory Submissions Pharmacovigilance

A fully integrated web-based A next generation mobility platform Affiliate compliance, An accelerated solution for

eDMSand eCTD Submissions that enables easy implementation oversight and implementation, upgrade and

with over 150 clients of SOPs and audit readiness with dashboarding tools migration for Oracle’s Argus

accurate data at all times Services Safety suite

Frequent changes in regulatory requirements leading to 11.5% CAGR in Pharmacovigilance Market will register 13%+ CAGR

regulatory submissions being outsourced over CY17-21 to touch $8 billion by CY24

Regulatory Submissions & PV market to continue uptrend Expertise led by qualified personnel mix

Computer Science Engineering

4%

TSL enables almost 50% of the global regulatory submissions 5% 22%

Engineering Graduates

for a top global pharma company and 8% of the total MBA Graduates

regulatory submissions to USFDA (between 2012 and 2017) 8%

24%

were through TSL Others

19% Pharma Graduates

The global pharmacovigilance market is expected to rise 16% Science Engineering Graduates

significantly due to compulsory pharmacovigilance activities 2% Arts & Science Graduates

that are being rigorously implemented

CA's

Source: Company (FY17), Axis Securities

2019 Dec 2018 Company Report

Take Solutions Ltd.

Proprietary Industry Networks developed to be the key differentiator Sector: Life Sciences Outsourcing

TSL has built strong moat for itself through its proprietary networking forums (NETS), a subscription based platforms for senior life sciences

professionals to discuss Industry wide issues. These NETS are difficult to replicate providing TSL’s competitive advantage with respect to access

to over 16 years of industry benchmark data and global client acquisitions

For Heads of Safety of Top 30 Life Sciences companies; invests in thought leadership to help shape future practices

For Heads of Information Technology for PV departments, focused on increasing business value from technology

For Heads of Safety of mid-sized Life Sciences companies with a range of product portfolios including one or more of Pharma,

Biologicals, Consumer, and Medical Devices

For PV leads of Life Sciences companies in the APAC region with Pharma, Consumer, Generics, or mixed portfolios

For Chief Medical Officers; addressing strategic and governance topics within the remit of the CMO

For Labeling Professionals; focused on the full lifecycle of labeling

For Regulatory Information Management(RIM) professionals to develop best practices and leading edge solutions

For Regulatory or Labeling IT Professionals; focused on exploring E2E Labeling technologies to improve processes and

increase business value

For Labeling Leaders of Life Sciences companies with a specific focus on operational aspects of the full lifecycle of E2E

labeling

For Heads of Clinical Operations, focused on sharing best practice to define excellence in delivery of clinical trials

2119 Dec 2018 Company Report

Take Solutions Ltd.

Clients include 9 out of top10 Pharma Companies Sector: Life Sciences Outsourcing

Large Innovators Small/Mid Innovators Generics Others

Generics are bio-pharma companies that Others includes medical devices companies,

Innovators are bio pharma companies that discover new drugs

produce existing drugs after patent expires academia & CROs

Source: Company, Axis Securities

2219 Dec 2018 Company Report

Take Solutions Ltd.

Competitive positioning: No Indian Competitors for LS services Sector: Life Sciences Outsourcing

Leader in IDC market space: Worldwide Life Sciences Technology Peers

R&D BPO Services 2018 Vendor Assessment In terms of Technology TSL has been positioned as leader in

comparison to IT companies by IDC in Life Sciences R&D BPO services

Clinical business Peers

Global CRO peers have EBIT margin of ~12%-15% whereas as TSL

commands ~16-18% margin in its Clinical business enabled by its

patent IP based ‘OneClinical’ near real-time platform enabling faster

decision making and minimizing risks to trial success.

There are no competitors of TSL in India offering full fledged Life

Sciences services

EBIT Margin Comparaison (Global Peers CY17)

24% 18.20%

14.40% 14.80%

16% 11.60% 10.70%

8%

0%

TFS ICON Medpace Parexel Take Solutions

(2016) (2016)

Source: Company, Axis Securities

Global Peers

EPS PE EV/Ebidta RoE EPS

MCAP USD$ Million 1Y Fwd 2Y Fwd 3Y FWD 1Y Fwd 2Y Fwd 3Y FWD 1Y Fwd 2Y Fwd 3Y FWD 1Y Fwd 2Y Fwd 3Y FWD CAGR%

Take Solutions Ltd 277 14.6 17.8 23.6 9.2 7.5 5.7 4.0 2.8 1.8 14.9 15.6 17.4 24.37

IQVIA Holdings Inc 24191 5.52 6.26 7.09 21.65 19.09 16.87 15.43 14.36 13.23 11.83 12.96 15.45 13.28

PRA Health Sciences Inc 6757 4.25 4.91 5.63 24.48 21.18 18.46 17.00 14.99 13.23 26.37 26.83 28.49 15.13

Syneos Health Inc 5153 2.74 3.17 3.63 18.23 15.76 13.76 13.30 12.05 11.02 8.00 9.98 11.88 15.11

Veeva Systems Inc 13238 1.48 1.72 2.00 61.93 53.24 45.77 41.60 34.82 29.15 25.33 20.48 20.35 16.32

Medidata Solutions Inc 4505 1.63 1.84 2.30 45.22 39.99 32.04 28.91 23.58 19.00 18.01 16.77 17.97 18.79

Source: Reuters, Axis Securities

2319 Dec 2018 Company Report

Take Solutions Ltd.

Performance delivery post restructuring Sector: Life Sciences Outsourcing

Revenue (Rs Cr) Growth trajectory led by Life Sciences to continue

4,000

2,941 TSL posted revenue CAGR of 10% over FY11-FY15 as company

3,000 2,404 identified the opportunity in Life Sciences and started building

1,996

In Rs Cr.

1,587 domain expertise

2,000 1,345

816 1,030

1,000 730 TSL started delivering results of restructuring process from Supply

Chain towards Life Sciences by reporting CAGR of 29% over FY15-

0

18 and it is expected to grow at 23% CAGR over FY18-21E

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

EBITDA & PAT (Rs Cr) Robust EBITDA and PAT led by top line growth

600 574

474 EBITDA/PAT were subdued due to low margin SCM business. Post

450 397 transformation into full service LS business, TSL witnessed robust

306 331

In Rs Cr.

300 213

262

214

264 EBITDA/PAT growth of 27%/31% over FY16-18

147 149 120 146 160

150 58 70

We expect growth opportunity provided in Life Sciences to help TSL

0 grow EBITDA/PAT at 23%/30% over FY18-21E. Robust growth to

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E be slightly offset by de-growth in SCM business as a strategic

EBITDA PAT decision of TSL to sell SCM business

EBITDA & PAT margin Premium margins due to domain expertise

18.1% 20.5% 20.7% 19.5% 19.3% 19.9% 19.7% 19.5% TSL commands premium margins led by Regulatory Submissions and

20% PV segments (22%-25%) due to in-depth subject matter expertise,

15% 11.6% 10.9% competencies and technology enabling them being cost efficient

9.6% 10.1% 10.7% 11.0% 11.3%

10% 7.1%

Clinical business margins are comparatively lower to regulatory &

5% PV segments, however, near real time technology enables TSL earn

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E higher margin(16-18%) over its peers. As clinical business

EBITDA Margin(%) PAT Margin (%) segment’s revenue share increases to over 60% by FY21E we

expect muted growth in margins although growth in absolute

Source: Company, Axis Securities amount would be robust

2419 Dec 2018 Company Report

Take Solutions Ltd.

Key Financials Sector: Life Sciences Outsourcing

Healthy return ratios Reducing Client concentration

25% 23%

22% Both ROCE and ROE have 28%

21% 30% 26% While most of the large

20% been maintained at 24%

18% 23% Pharma companies are

20% 17% healthy levels.

25% 22%

20% 19% TSL’s Client, revenue

After a dip due 20% 18%

14% 16% 16% 15% concentration from top

15% 19% 17% incremental gross asset

15% clients is continuously

15% 16% addition for expansion

14% decreasing.

10% 12% impacting asset turnover, 10% TSL winning more clients

ROE has started to indicates diversification

5% improve as benefit of of risk and low

FY15 FY17 FY19E FY21E restructuring begin to dependence on top

occur clientele

Revenue from Top 5

RoE RoCE

Revenue from Top 10

Operating Cash Flows to increase Receivable days in line with Industry*

TSL has generated strong 250

350 operating cash flow and 200 TSL’s gross receivable

funding for expansion 200 days are well in line with

300

would be met by internal 154

No. of days

135 the industry average

250 accruals 150 122 117 TSL does not seek large

Decline in FY17 was due 90 up-front payments for

200 100 78

In Rs Cr

to acquisition of EAL in studies which increases its

150 FY16 and increase in net working capital

50

working capital led by requirement

100

higher DSO & lower DPO 0 The focus of TSL is on

50 days to support clinical building strong customer

segment relationship which would

0 We expect operating CF bear fruits in coming years

of TSL to grow at a CAGR

of 24% over FY18-21E

Source: Company, Axis Securities * Gross receivable days (Without adjusting for customer advances)

2519 Dec 2018 Company Report

Take Solutions Ltd.

Valuation Charts Sector: Life Sciences Outsourcing

PE Band Valuation

350 We estimate TSL to post revenue growth at a CAGR of 23%

300 and profits at CAGR of 30% over FY18-21E. Given the size of

250 TSL’s revenue compared to global peers, its domain expertise

200

In Rs

and the opportunities available, we feel TSL is a small fish in a

150 big pond

100

50

0 We value TSL at 10x FY20E given the growth prospects to

arrive at a target price of Rs 178 (31 % upside). The valuations

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Jul-13

Nov-13

Jul-14

Nov-14

Jul-15

Nov-15

Jul-16

Nov-16

Jul-17

Nov-17

Jul-18

Nov-18

are conservative as TSL is trading at lower valuations compared

to global peer, with coming quarters’ performance at par with

expectations, TSL has the potential to be re-rated at higher

Price 5x 10x 15x 18x multiple

12mth fwd P/E (x) Key Risks and Concerns

20 TSL enjoys patent ‘OneClinical’ technology which enables them

to command premium margins. As competitors comes up with

15 similar technology, it would affect TSL’s USP

10 There are no domestic peers offering full Life Sciences services

but domestic players offering select services are scaling up

5 their services, this along with increasing competition from

global peers would be major challenge for TSL

0

Jul-16

Mar-13

Jul-13

Mar-14

Jul-14

Mar-15

Jul-15

Mar-16

Mar-17

Mar-18

Jul-17

Jul-18

Nov-13

Nov-14

Nov-15

Nov-16

Nov-17

Nov-18

Higher working capital requirements potent risk for TSL

PE Mean Mean+1Stdev Mean-1Stdev

Source: Company, Axis Securities

2619 Dec 2018 Company Report

Take Solutions Ltd.

Financials (Consolidated) Sector: Life Sciences Outsourcing

Profit & Loss (Rs Cr) Balance Sheet (Rs Cr)

YE March FY17 FY18 FY19E FY20E FY21E YE March FY17 FY18 FY19E FY20E FY21E

Net sales 1,345 1,587 1,996 2,404 2,941 Total assets 1,209 1,682 1,933 2,240 2,593

Other operating income 0 0 0 0 0 Net Block 319 349 353 261 170

Total income 1,345 1,587 1,996 2,404 2,941 CWIP 6 1 7 3 3

Cost of revenue 396 457 567 685 841 Goodwill 235 240 240 240 240

Gross margin (%) 70.5% 71.2% 71.6% 71.5% 71.4% Investments 13 13 13 13 13

Other expense 299 377 459 692 850

Wkg. cap. (excl cash) 508 680 836 1,003 1,173

Employee Expense 387 447 573 553 677

Cash / Bank balance 110 341 425 662 937

Operating Profit 262 306 397 474 574

Other income 13 6 22 20 20 Other assets 18 59 59 59 59

PBIDT 275 313 419 494 594 Capital employed 1,209 1,682 1,933 2,240 2,593

Depreciation 87 104 136 146 141

Equity capital 13 15 15 15 15

Interest & Fin Chg. 23 21 23 26 27

Reserves 898 1,314 1,529 1,792 2,141

E/o income / (Expense) 0 0 0 0 0

Pre-tax profit 165 188 260 321 425 Pref. Share Capital 0 0 0 0 0

Tax provision 19 28 44 58 77 Minority Interests 42 8 8 8 8

(-) Minority Interests 3 (1) 0 0 0 Borrowings (Short term

221 308 334 375 376

& Long term)

Associates 0 0 0 0 0

Def tax Liabilities 23 34 43 46 49

Adjusted PAT 143 160 216 263 349

Reported PAT 143 160 216 263 349 Other Liabilities 12 4 4 4 4

Source: Company, Axis Securities

2719 Dec 2018 Company Report

Take Solutions Ltd.

Financials (Consolidated) Sector: Life Sciences Outsourcing

Cash Flow (Rs Cr) Ratio Analysis (%)

YE March FY17 FY18 FY19E FY20E FY21E YE March FY17 FY18 FY19E FY20E FY21E

Sales growth 30.5 18.0 25.7 20.4 22.4

Sources 343 496 313 358 434

OPM 19.5 19.3 19.9 19.7 19.5

Cash profit 256 285 375 436 517

Oper. profit growth 22.9 16.9 29.6 19.2 21.1

(-) Dividends 16 27 27 35 49 COGS / Net sales 29.5 28.8 28.4 28.5 28.6

Retained earnings 240 257 347 401 468 Overheads/Net sales 22.3 23.8 23.0 28.8 28.9

Depreciation / G. block 21.7 19.3 20.0 20.0 18.0

Issue of equity 1.1 1.5 0.0 0.0 0.0

Effective interest rate 8.4 7.9 7.3 7.4 7.3

Change in Oth. Reserves 175 218 0.0 0.0 0.0

Borrowings (19) 6 (20) (20) (10) Net wkg.cap / Net sales 0.30 0.37 0.38 0.38 0.37

Others (54) 14 (15) (23) (24) Net sales / Gr block (x) 3.3 2.9 2.9 3.3 3.8

RoCE 20.7 16.9 18.5 19.8 22.1

Debt / equity (x) 0.24 0.23 0.22 0.21 0.17

Applications 343 496 313 358 434

Effective tax rate 11.4 15.0 17.0 18.0 18.0

Capital expenditure 134 157 146 50 50 RoE 19.1 14.1 14.9 15.5 17.4

Investments (12) 50 0 0 0 Payout ratio (Div/NP) 10.7 17.2 12.7 13.3 13.9

EPS (Rs.) 11.2 12.2 14.6 17.8 23.6

Net current assets 270 39 111 106 158

EPS Growth 6.9 9.3 19.4 22.0 32.6

Change in cash (18) 231 56 202 226

CEPS (Rs.) 18.1 17.8 23.7 27.7 33.1

Others (32) 20 0 0 0 DPS (Rs.) 1.0 1.5 1.5 2.0 3.0

Source: Company, Axis Securities

2819 Dec 2018 Company Report

Take Solutions Ltd.

Disclaimer Sector: Life Sciences Outsourcing

Disclosures:

The following Disclosures are being made in compliance with the SEBI Research Analyst Regulations 2014 (herein after referred to as the Regulations).

1. Axis Securities Ltd. (ASL) is a SEBI Registered Research Analyst having registration no. INH000000297. ASL, the Research Entity (RE) as defined in the Regulations, is engaged in the business of

providing Stock broking services, Depository participant services & distribution of various financial products. ASL is a subsidiary company of Axis Bank Ltd. Axis Bank Ltd. is a listed public

company and one of India’s largest private sector bank and has its various subsidiaries engaged in businesses of Asset management, NBFC, Merchant Banking, Trusteeship, Venture Capital,

Stock Broking, the details in respect of which are available on www.axisbank.com.

2. ASL is registered with the Securities & Exchange Board of India (SEBI) for its stock broking & Depository participant business activities and with the Association of Mutual Funds of India (AMFI) for

distribution of financial products and also registered with IRDA as a corporate agent for insurance business activity.

3. ASL has no material adverse disciplinary history as on the date of publication of this report.

4. I/We, Kumar Nihal – Manager, Research, MBA (Finance), author/s and the name/s subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect

my/our views about the subject issuer(s) or securities. I/We (Research Analyst) also certify that no part of my/our compensation was, is, or will be directly or indirectly related to the specific

recommendation(s) or view(s) in this report. I/we or my/our relative or ASL does not have any financial interest in the subject company. Also I/we or my/our relative or ASL or its Associates may

have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Since associates of ASL are

engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this

report. I/we or my/our relative or ASL or its associate does not have any material conflict of interest. I/we have not served as director / officer, etc. in the subject company in the last 12-month

period.

Any holding in stock – No

5. ASL has not received any compensation from the subject company in the past twelve months. ASL has not been engaged in market making activity for the subject company.

6. In the last 12-month period ending on the last day of the month immediately preceding the date of publication of this research report, ASL or any of its associates may have:

i. Received compensation for investment banking, merchant banking or stock broking services or for any other services from the subject company of this research report and / or;

ii. Managed or co-managed public offering of the securities from the subject company of this research report and / or;

iii. Received compensation for products or services other than investment banking, merchant banking or stock broking services from the subject company of this research report;

ASL or any of its associates have not received compensation or other benefits from the subject company of this research report or any other third-party in connection with this report.

Term& Conditions:

This report has been prepared by ASL and is meant for sole use by the recipient and not for circulation. The report and information contained herein is strictly confidential and may not be altered in

any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ASL. The report is based on the

facts, figures and information that are considered true, correct, reliable and accurate. The intent of this report is not recommendatory in nature. The information is obtained from publicly available

media or other sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy,

completeness or correctness. All such information and opinions are subject to change without notice. The report is prepared solely for informational purpose and does not constitute an offer document

or solicitation of offer to buy or sell or subscribe for securities or other financial instruments for the clients. Though disseminated to all the customers simultaneously, not all customers may receive this

report at the same time. ASL will not treat recipients as customers by virtue of their receiving this report.

2919 Dec 2018 Company Report

Take Solutions Ltd.

Disclaimer Sector: Life Sciences Outsourcing

DEFINITION OF RATINGS

Ratings Expected absolute returns over 12-18 months

BUY More than 10%

HOLD Between 10% and -10%

SELL Less than -10%

NOT RATED We have forward looking estimates for the stock but we refrain from assigning valuation and recommendation

UNDER REVIEW We will revisit our recommendation, valuation and estimates on the stock following recent events

NO STANCE We do not have any forward looking estimates, valuation or recommendation for the stock

Disclaimer:

Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to the recipient’s specific circumstances.

The securities and strategies discussed and opinions expressed, if any, in this report may not be suitable for all investors, who must make their own investment decisions, based on their own

investment objectives, financial positions and needs of specific recipient.

This report may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this report should make such investigations as it deems necessary to arrive at

an independent evaluation of an investment in the securities of companies referred to in this report (including the merits and risks involved), and should consult its own advisors to determine the merits

and risks of such an investment. Certain transactions, including those involving futures, options and other derivatives as well as non-investment grade securities involve substantial risk and are not

suitable for all investors. ASL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any

action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or

income, etc. Past performance is not necessarily a guide to future performance. Investors are advice necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document

to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and

may be subject to change without notice.

ASL and its affiliated companies, their directors and employees may; (a) from time to time, have long or short position(s) in, and buy or sell the securities of the company(ies) mentioned herein or (b)

be engaged in any other transaction involving such securities or earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or

act as an advisor or investment banker, lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information

and opinions. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting this document.

ASL and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, the recipients of this report should be aware that ASL

may have a potential conflict of interest that may affect the objectivity of this report. Compensation of Research Analysts is not based on any specific merchant banking, investment banking or

brokerage service transactions. ASL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither this report nor any copy of it may be taken or transmitted into the United State (to U.S. Persons), Canada, or Japan or distributed, directly or indirectly, in the United States or Canada or

distributed or redistributed in Japan or to any resident thereof. If this report is inadvertently sent or has reached any individual in such country, especially, USA, the same may be ignored and brought

to the attention of the sender. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other

jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ASL to any registration or licensing requirement within such

jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors.

The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The

Company reserves the right to make modifications and alternations to this document as may be required from time to time without any prior notice. The views expressed are those of the analyst(s)

and the Company may or may not subscribe to all the views expressed therein.

Copyright in this document vests with Axis Securities Limited.

Axis Securities Limited, Corporate office: Unit No. 2, Phoenix Market City, 15, LBS Road, Near Kamani Junction, Kurla (west), Mumbai-400070, Tel No. – 18002100808/022-61480808, Regd.

off.- Axis House, 8th Floor, Wadia International Centre, Pandurang Budhkar Marg, Worli, Mumbai – 400 025. Compliance Officer: Anand Shaha, Email: compliance.officer@axisdirect.in, Tel No:

022-42671582.

30You can also read