The institutionalisation of Bitcoin - 17 December 2020 - Mercury Redstone

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

17 December 2020

The institutionalisation of Bitcoin

Verbier

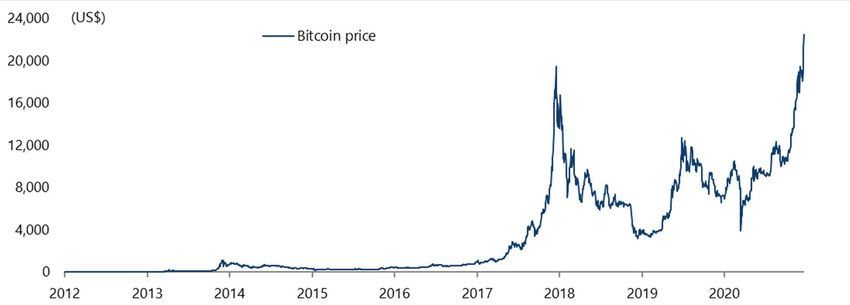

If 2020 has been the year of Covid-19, it has also been the year of Bitcoin. Indeed it is the year when Bitcoin

has come of age.

This report is intended for kurt.martinson@locustwood.com. Unauthorized distribution prohibited.

GREED & fear is not only talking about price performance, though clearly that has been impressive with Bitcoin

up 474% from the March low and 214% year to date (see Exhibit 1), including a 9.2% gain yesterday while

GREED & fear was writing this! Rather what GREED & fear means is that this is the year Bitcoin has become

investible for institutions with custodian arrangements available and with prominent investors and indeed

institutional investors declaring that they have bought it. In this respect, Bitcoin has now become part of the

system with opportunities also for retail investors to buy into it via quoted vehicles, be it the Greyscale Bitcoin

Trust in America or the recently launched VanEck Vectors Bitcoin ETN traded on the Frankfurt exchange.

Exhibit 1: Bitcoin price

Source: Bloomberg

This is important since, before such arrangements were in place, there was always the risk that Bitcoin

accounts could be hacked. The other risk, of course, was that Bitcoin would be declared illegal because it was

used for nefarious purposes, such as illegal narcotic transactions. Still an asleep GREED & fear has only just

been made aware by a friend of the most remarkable development in this area, though it happened four

months ago. That was the announcements in mid-August and September by the Nasdaq-listed MicroStrategy,

a business intelligence software company, that it had invested in the Bitcoin equivalent of US$425m

(US$250m in August and US$175m in September), amounting to almost 100% of its own treasury funds, to

hold on its balance sheet. The aim is to make Bitcoin “the primary treasury reserve asset on an ongoing basis”,

along with cash and short-term investments, according to the company’s official US Securities and Exchange

Commission (SEC) approved Form 8-K. MicroStrategy invested a further US$50m in Bitcoin in early December,

with a cumulative holding of 40,824 Bitcoins.

Please see analyst certifications, important disclosure information, and information regarding the status

of non-US analysts at the end of this report. 1

*Jefferies Hong Kong Limited

This marks a watershed moment in GREED & fear’s view since the auditors approved MicroStrategy putting

Bitcoin on its balance sheet as did the SEC. Now it is true that the far more famous Square also announced in

October that it was investing US$50m in Bitcoin but that only amounted to 1% of the Silicon Valley company’s

assets. Such a small investment probably did not even have to be reported but in MicroStrategy’s case that

was certainly not the case.

GREED & fear must admit to never having heard of MicroStrategy previously. But the company seems to have

been investing in technology and software for 31 years. Since announcing its investment in Bitcoin, the

company’s market capitalisation has risen by 131% to US$2.77bn (see Exhibit 2) and the value of its Bitcoin

holding has almost doubled to US$917m. Intrigued by the motivation behind this investment, GREED & fear

decided to do something GREED & fear seldom does. That was to listen to a “podcast” featuring an interview

with the highly articulate CEO and co-founder of MicroStrategy, Michael Saylor. He is, by the way, no fast

money operator since he has been a public company CEO for 22 years since MicroStrategy’s listing in 1998.

Exhibit 2: MicroStrategy market cap

3,500 (US$m)

MicroStrategy market cap

3,000

2,500

2,000

1,500

1,000

500

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20

Source: Bloomberg

The most amazing revelation is that he only started to look at Bitcoin in 2019, which is a lot later than GREED

& fear. He made the decision to invest the company’s funds in Bitcoin as a store of value in the spring after

seeing the monetisation triggered by the Federal Reserve’s extreme policy response to Covid-19, and then was

able to convince his fellow directors and get the lawyers and auditors to execute the process in a period of

only ten weeks.

Saylor views Bitcoin as the “ideal Treasury reserve asset”. But, more worryingly to people like GREED & fear

who own gold, Saylor argues that Bitcoin is “destroying gold’s value proposition” because Bitcoin has

“dematerialised gold”. GREED & fear has to admit that this argument has some real merit. GREED & fear has

commented before on several occasions that ownership of gold and Bitcoin are not mutually exclusive and

appeal to different generations (i.e. boomers and millennials). But gold bugs have to face up to the real risk

that risk averse capital, which would have otherwise gone to gold to hedge the obvious ongoing fiat paper

currency debasement in the G7 world, will now go to Bitcoin. In fact that process has already begun.

Meanwhile the brutal fact is that since the policies of extreme currency debasement began in America, which

GREED & fear will take from the commencement of quanto easing under Billyboy in late 2008, Bitcoin has

outperformed gold by 177,000-fold (see Exhibit 3). It is also the case that the supply of Bitcoin is shrinking,

under the quantitative tightening dynamic, which is certainly not the case with gold.

17 December 2020 2

Please see important disclosure information at the end of this report.

Exhibit 3: Bitcoin price/gold price

16 Bitcoin price / Gold price

14

12

10

8

6

4

2

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Bloomberg

This does not mean that GREED & fear is going to give up on gold. And the yellow metal should rally again if

the Fed stays doveish in the face of the dramatic cyclical recovery that is coming on the other side of the

pandemic, in line with GREED & fear’s base case. But GREED & fear is now going to do what GREED & fear

should already have done since owning Bitcoin was first recommended here back in June 2019 (see GREED

& fear - The dollar spasm, 27 June 2019), and since it became evident that institutional acceptable ways of

owning Bitcoin were becoming available. That is to introduce an investment in Bitcoin in GREED & fear’s long-

only global portfolio for US dollar-denominated pension funds, established at the end of 3Q02. The 50%

weighting in physical gold bullion in the portfolio will be reduced for the first time in several years by five

percentage points with the money invested in Bitcoin (see Exhibit 4). If there is a big drawdown in bitcoin from

the current level, after yesterday’s historic breakout above the US$20,000 level, the intention will be to add to

this position.

Meanwhile there is no need for GREED & fear to apologise for the original investment in gold when this portfolio

was launched at the end of 3Q02. It was made at the price level of US$323/oz.

Exhibit 4: Recommended long-only asset allocation for US-dollar-based pension funds

Weight (%) Investment type

45% Physical gold bullion

30% Asia ex-Japan equities, weighted according to the long-only thematic portfolio

20% Unhedged gold mining stocks

5% Bitcoin

Source: Jefferies

Returning to the more mundane subject of Federal Reserve mumbo jumbo, the latest Fed FOMC meeting on

Wednesday indicated a slightly less doveish outlook as a consequence of the vaccine news. But GREED & fear

is only talking about at the margin. The 2% inflation target is still projected not to be reached until 2023 while

most Fed governors assume shot-term rates will remain near zero for at least three more years.

GREED & fear repeats the point that by far the most important issue for financial markets in 2021 is how the

Fed responds when presented with evidence of cyclical recovery, as pent up demand is unleashed on the other

side of the pandemic. GREED & fear’s base case is that the Fed remains doveish even if only because the

system cannot afford higher rates. But it will be hard for Pivot to admit to this. The goal of the Fed’s new

forward guidance is seemingly to avoid the kind of market backlash that occurred in 2013, according to a Wall

17 December 2020 3

Please see important disclosure information at the end of this report.

Street Journal article today (“Fed Reinforces Stimulus Will Be Open-Ended to Spur Recovery”, 17 December

2020). So far as GREED & fear is concerned, any hint of tapering will lead to a taper convulsion, not a tantrum.

Investors everywhere need to understand this.

Back in Asia, sentiment amongst foreign investors towards Korea turned much more positive this quarter as

the focus turned to owning cyclicals. This was reflected in foreigners turning largescale net buyers of equities

after having been net sellers for the preceding six quarters. Foreigners have bought a net W4.1tn worth of

Korean equities so far this quarter, after selling a net W34tn in the previous six quarters (see Exhibit 5). The

ironic point to GREED & fear is that foreigners entered the market after retail investors had been active buyers

all year, a point which has been highlighted in recent months by Peter Kim, investment strategist at Jefferies’

new Korea research partner, KB Securities. Domestic retail investors bought a net W58.8tn in the first three

quarters of 2020 and a further W5.4tn so far in 4Q20 (see Exhibit 6).

Exhibit 5: Quarterly foreign net buying of Korean stocks

10 (Won tn) Foreign net buying of Korean stocks

5

0

(5)

(10)

(15)

(20)

Sep-16

Sep-17

Sep-18

Sep-19

Sep-20

Jun-16

Jun-17

Jun-18

Jun-19

Jun-20

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

Source: Bloomberg

Exhibit 6: Domestic retail investors' net buying of Korean equities

30 (Won tn) Domestic retail investors' net buying of Korean stocks

25

20

15

10

5

0

(5)

(10)

Sep-16

Sep-17

Sep-18

Sep-19

Sep-20

Jun-16

Jun-17

Jun-18

Jun-19

Jun-20

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

Source: Bloomberg

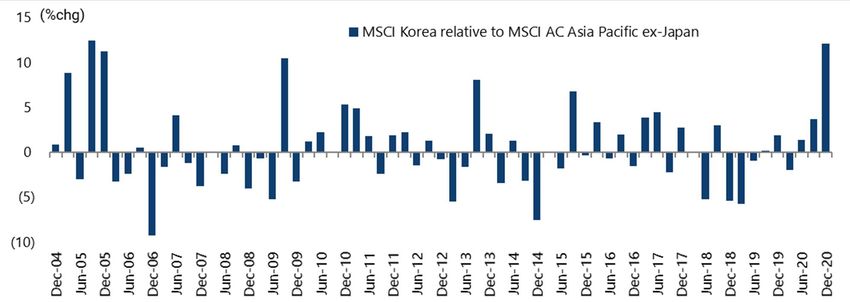

The result of the renewed foreign enthusiasm is that Korea is at present the best performing market in Asia

Pacific ex-Japan year-to-date, a performance also helped by a 6.9% appreciation of the won against the US

dollar this quarter. The MSCI Korea has risen by 30.3% in US dollar terms so far this quarter and is up 35.5%

year-to-date, compared with a 16.2% gain quarter-to-date and a 17.2% gain year-to-date in the MSCI AC Asia

17 December 2020 4

Please see important disclosure information at the end of this report.

Pacific ex-Japan Index. This is Korea’s biggest outperformance against the rest of the region in a quarter since

3Q05 (see Exhibit 7).

Exhibit 7: MSCI Korea relative performance against the MSCI AC Asia Pacific ex-Japan

Source: Datastream

The above is a reminder that Korea remains extremely geared to the external cycle despite all the negative

focus in recent years amongst investors, as well as GREED & fear, on the socialist redistribution policies of the

Minjoo Government elected in May 2017. It is also the case that these policies no longer look so extreme given

the policies implemented in the G7 world in response to the pandemic. As for the cyclical gearing, exports

have started to turn up. Total exports rose by 4.1% YoY in November, while exports to China rose by 1.2% YoY

(see Exhibit 8).

Exhibit 8: Korea export growth

40 (%YoY, 3mma)

Korean exports Exports to China

30

20

10

0

(10)

(20)

(30)

Oct-11

Oct-12

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Oct-19

Oct-20

Apr-11

Apr-12

Apr-13

Apr-14

Apr-15

Apr-16

Apr-17

Apr-18

Apr-19

Apr-20

Jul-11

Jul-12

Jul-13

Jul-14

Jul-15

Jul-16

Jul-17

Jul-18

Jul-19

Jul-20

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jan-20

Source: CEIC Data

Traditionally Korea was a geared play on the OECD cycle. But this has changed significantly in recent years as

the share of exports going to emerging markets has increased dramatically. Emerging markets accounted for

62% of total Korean exports in 2019, up from 40% in 2000. By contrast, G7’s share of Korean exports has

declined from 43% to 24% over the same period (see Exhibit 9). China and Vietnam, for example, now account

for a combined 34% of Korean exports, compared with 13.5% for America (see Exhibit 10). This is a positive

dynamic, not a negative one, given the growing contribution of China and the emerging world to global growth.

Still the rally, and the retail contribution to that rally, means that Korea is no longer as cheap as it traditionally

has been. The MSCI Korea now trades on 13.4x 2021 consensus earnings based on 42% forecast earnings

17 December 2020 5

Please see important disclosure information at the end of this report.

growth (see Exhibit 11). It is also worth noting the renewed decline in RoE in recent years though this should

be bottoming out. The Kospi ROE fell from 9.7% in 2017 to 4.3% in 2019 and is projected to rise to 11.5% in

2021, according to Bloomberg (see Exhibit 12).

Exhibit 9: Share of Korean exports (Emerging markets vs G7)

65% Exports to emerging markets Exports to G7

60%

55%

50%

45%

40%

35%

30%

25%

20%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: CEIC Data

Exhibit 10: China, Vietnam and US shares of Korean exports

50%

USA China Vietnam

40%

30%

20%

10%

0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: CEIC Data

Exhibit 11: MSCI Korea 12m forward PE

14 (X) MSCI Korea 12m forward PE

13

12

11

10

9

8

7

6

5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Datastream, IBES

17 December 2020 6

Please see important disclosure information at the end of this report.Exhibit 12: Kospi ROE

16 (%)

Kospi ROE

14

12

10

8

6

4

2

0

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Source: Bloomberg

Exhibit 13: Cumulative net inflows into Korea investment funds investing offshore

160 (Won tn)

140

120 Cumulative net inflows into Korean investment funds investing offshore

100

80

60

40

20

0

(20)

(40)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Korea Financial Investment Association (KOFIA)

Meanwhile the won’s recent strength, and the domestic stock market boom, has slowed down the previous

boom in investing in offshore markets discussed here a year ago (see GREED & fear - Kim and the appeal of

boring, 12 December 2019). Net offshore investment by Korean investment funds has totaled W21tn so far in

2020, compared with W45tn in 2019 and W24tn in 2018 (see Exhibit 13). The total amount invested by such

funds offshore is now W206tn (US$189bn). Still gung ho Korean retail investors have also bought a net

US$19bn worth of foreign stocks so far in 2020, of which US$16.8bn was in US stocks (see Exhibit 14). This

compares with net buying of “only” US$2.5bn of foreign stocks in 2019.

Finally, on Covid, Korea has so far continued to avoid complete lockdowns as the number of cases has

fluctuated, though of late there has been a notable deterioration. The 7-day average daily Covid case count

has surged from a low of 69 in early October to a record 908 on Wednesday, with the daily case count

exceeding 1,000 over the past two days. While the 7-day average daily death count has also risen from 1 in

late October to 10, with a record 22 deaths on Wednesday (see Exhibit 15). Still, total confirmed cases and

deaths are running at “only” 907 and 12 per 1m of population respectively.

17 December 2020 7

Please see important disclosure information at the end of this report.Exhibit 14: Korea retail investors net buying of foreign stocks

3,500 (US$m)

3,000

Other foreign stocks US stocks

2,500

2,000

1,500

1,000

500

0

-500

-1,000

May-11

Sep-11

May-12

Sep-12

May-13

Sep-13

May-14

Sep-14

May-15

Sep-15

May-16

Sep-16

May-17

Sep-17

May-18

Sep-18

May-19

Sep-19

May-20

Sep-20

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jan-20

Source: Korea Securities Depository

Exhibit 15: Korea Covid-19 7-day average daily new cases and deaths

1000 12

Korea daily new cases, 7dma Daily deaths, 7dma (RHS)

10

800

8

600

6

400

4

200

2

0 0

23-Apr

21-May

12-Mar

26-Mar

19-Nov

13-Feb

27-Feb

8-Oct

18-Jun

16-Jul

30-Jul

3-Dec

9-Apr

30-Jan

7-May

13-Aug

27-Aug

2-Jul

5-Nov

10-Sep

24-Sep

22-Oct

4-Jun

Source: Korea Centers for Disease Control & Prevention

Exhibit 16: Philippines 7-day average daily Covid new cases and deaths

Source: Department of Health

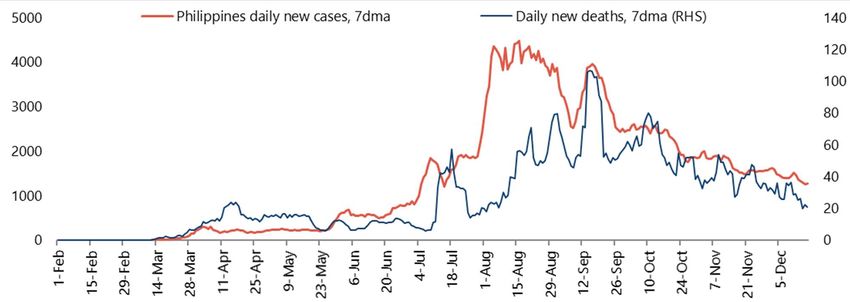

Elsewhere in Asia, it is interesting to note that the Covid cases are down significantly in the Philippines and

now look to be well past the peak. The 7-day average daily Covid case count has declined by 72% from the

peak of 4,477 in mid-August to 1,272, while the 7-day average daily Covid death count has fallen by 80% from

17 December 2020 8

Please see important disclosure information at the end of this report.107 in mid-September to 21 (see Exhibit 16). The number of active cases also peaked at 83,109 in mid-August

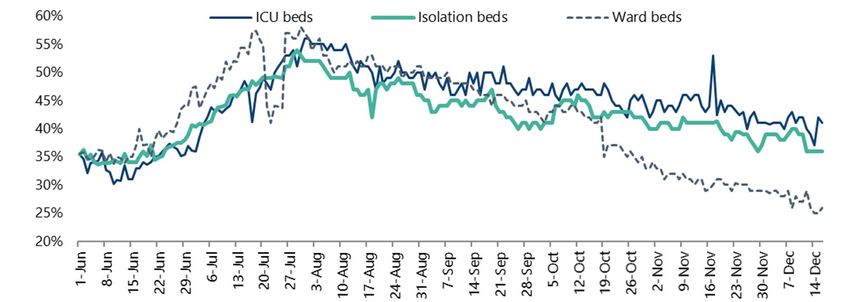

and has since declined by 69% to 25,695. While hospitalisation rates are also way down. Nationwide ward bed,

ICU bed and isolation bed occupancy rates have declined from 58%, 56% and 54% in late July to 26%, 41% and

36% respectively (see Exhibit 17).

But, despite all this, the Philippines is ending 2020 still in various forms of lockdowns, most particularly Metro

Manila where public transport is still only operating at around 40% of capacity.

Exhibit 17: Philippines hospital bed occupancy rates for Covid-19

Source: Department of Health

The impact of the extended lockdowns continues to show up in the labour market. The national adult jobless

rate was still a horrifying 39.5% in September, though down from the peak of 45.5% in July, according to Social

Weather Stations (see Exhibit 18). The economic consequences of the lockdown also continue to be reflected

in third quarter data with real GDP declining by 11.5% YoY, though that was an improvement from the second

quarter which saw the biggest YoY decline (16.9%) since the quarterly data series began in 1981 (see Exhibit

19).

Exhibit 18: Philippines adult jobless rate

50 (%) Philippines SWS adult jobless rate

40

30

20

10

0

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Note: % of the adult labour force without a job at present and looking for a job. Source: Social Weather Stations

17 December 2020 9

Please see important disclosure information at the end of this report.Exhibit 19: Philippines real GDP growth

15 (%YoY)

Real GDP growth

10

5

0

(5)

(10)

(15)

(20)

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Source: CEIC Data, Philippines Statistics Authority

Exhibit 20: Philippines fiscal balance as % of GDP

2 (%GDP)

0

(2)

(4)

(6)

(8)

(10)

2020F

2021F

2022F

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Source: CEIC Data, Bureau of Treasury, Development Budget Coordination Committee (DBCC)

As elsewhere, the Philippines has engaged in aggressive fiscal easing this year with a forecast fiscal deficit

of P1.4tn or 7.6% of GDP this year, the highest since 1985 (see Exhibit 20). But the real dramatic shift has

been in monetary policy where Bangko Sentral ng Pilipinas (BSP) has gone unorthodox, in terms of

implementing both quantitative easing and what Jefferies’ Philippine research partner Regis Partners calls

“direct monetisation”. The BSP’s direct purchases of government securities under repo agreements rose from

P300bn in March to P540bn in October and is expected to rise to P850bn in 2021, while the central bank has

since March bought an additional P1tn worth of Treasuries in the open market as of August, the latest data

available (see Exhibit 21).

The central bank effectively funded about 77-81% of the issuance of Treasury bonds in the first eight months

of 2020, according to Regis. The central bank has also said it will keep up its bond buying programme for at

least the next two years.

17 December 2020 10

Please see important disclosure information at the end of this report.Exhibit 21: BSP holdings of domestic securities (open market operations) and govt securities under repo agreements

3,000 (P bn)

2,500 Domestic Securities Gov't Secs Under Repo Agreement

2,000

1,500

1,000

500

0

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Oct-20E Jan-21E

Source: Bangko Sentral ng Pilipinas (BSP), Regis Partners

As for conventional monetary policy, the central bank has since February cut the overnight reverse repurchase

rate by 200bp to 2.0%, including a 25bp cut in November following a pause since July. It has also cut the

reserve requirement ratio by 200bp in late March to 12% and is authorised by the monetary board to cut a total

of 400bp in 2020. But no more RRR cut has been announced since then. The central bank kept its policy

unchanged in today’s monetary policy meeting.

The move to unorthodox monetary policy has been positive for the stock market, sending a clear message to

domestic fund managers to switch out of bonds and cash. Philippine M1 growth and M3 growth were 22.4%

YoY and 11.8% YoY respectively in October (see Exhibit 22). The result is that the stock market has rallied

sharply so far this quarter without foreign net buying. The PSEi Index has risen by 24.5% so far in 4Q20, while

foreigners have sold a net US$425m over the same period (see Exhibit 23).

This divergence is almost unprecedented for the Philippines. It in part reflects domestic equity funds

dramatically reducing their cash holdings during the second half of 2020. The estimated cash levels of local

funds have declined from 11.2% in May to 6.3% in October, according to Regis (see Exhibit 24).

Exhibit 22: Philippine M3 growth and M1 growth

40 (%YoY)

M3 growth M1 growth

35

30

25

20

15

10

5

0

May-10

Sep-10

May-11

Sep-11

May-12

Sep-12

May-13

Sep-13

May-14

Sep-14

May-15

Sep-15

May-16

Sep-16

May-17

Sep-17

May-18

Sep-18

May-19

Sep-19

May-20

Sep-20

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jan-20

Source: CEIC Data, BSP

17 December 2020 11

Please see important disclosure information at the end of this report.Exhibit 23: Cumulative foreign net buying of Philippine stocks

Source: Bloomberg, Philippine Stock Exchange

Exhibit 24: Estimated local fund cash levels (% to NAV, AUM-weighted)

12%

10%

8%

6%

4%

2%

0%

Feb-17

Feb-18

Feb-19

Feb-20

Aug-17

Aug-18

Aug-19

Aug-20

Oct-17

Oct-18

Oct-19

Oct-20

Apr-17

Apr-18

Apr-19

Apr-20

Jun-17

Jun-18

Jun-19

Jun-20

Dec-16

Dec-17

Dec-18

Dec-19

Source: Various funds' fact sheets, REGIS estimates

From a valuation standpoint, the stock market is on 18x 12-month forward earnings based on the PSEi

universe. This is based on Regis’ assumption of a 90% return to normal by the end of 2021 in terms of

economic activity. A potential positive is that a pending tax bill, if implemented, will reduce the corporate

income tax rate from 30% to 25% retroactively to July 2020. If this occurs, it will increase the forecast earnings

growth by about 5-7 percentage points from the current Regis forecast of 34% in 2021.

If this is all positive, the risk next year for foreign investors is that the currency takes the pressure as a result

of the aggressive monetary easing. This risk will increase if rising commodity prices, particularly a rising oil

price, cause a rise in inflation at a time when domestic purchasing power is under pressure from the lack of

employment.

Still the peso has so far remained remarkably stable against a weak US dollar, though in a sign of vulnerability

it has begun to underperform other Asian currencies since mid-August. The peso has underperformed the

Bloomberg Asia Dollar Index by 3.5% since mid-August (see Exhibit 25). GREED & fear would certainly not have

a weighting in the peso or in Philippine bonds in an Asian currency or bond fund.

One explanation for the currency’s resilience of late has been evidence of capital inflow, as reflected in the net

errors and omissions item (or so-called net unclassified items) on the balance of payments. Net errors and

omissions rose from an outflow of US$2.83bn in 2018 to an inflow of US$3.88bn in 2019 and US$2.06bn in

17 December 2020 12

Please see important disclosure information at the end of this report.the first three quarters of 2020 though, significantly to GREED & fear, they fell to an outflow of US$709m in

3Q20 (see Exhibit 26). The most plausible explanation for this previous capital inflow remains mainland

Chinese money related to the offshore gaming boom, as previously discussed here (see GREED & fear - Asean

blues, 6 August 2020).

Exhibit 25: Peso performance relative to Bloomberg Asia Dollar Index

6 (%YTD)

4

2

0

(2)

Peso against US$

(4) Bloomberg Asia Dollar Index

Peso relative to Asia Dollar Index

(6)

May-20

Sep-20

Aug-20

Oct-20

Jun-20

Nov-20

Jul-20

Mar-20

Apr-20

Jan-20

Dec-20

Feb-20

Source: Bloomberg

Exhibit 26: Philippines balance of payments: Net unclassified items

8 (US$bn)

Net unclassified items Annualised

6

4

2

0

(2)

(4)

(6)

(8)

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: BSP

Still it now looks to GREED & fear as if the offshore gaming boom has peaked amidst growing anecdotal

evidence that Philippine offshore gaming operators (POGOs) are leaving, a trend which is already causing a

negative impact on both residential prices and commercial rents. Office rents have declined by 10-15% since

peaking in 1Q20, while residential condo prices are down 5-20% over the same period (see Exhibits 27 and

28).

There are two reasons. The first is a crackdown on POGOs from China. The second is that the Rodrigo Duterte

government imposed a 5% tax on turnover (i.e. the amount bet) in September.

17 December 2020 13

Please see important disclosure information at the end of this report.Exhibit 27: Philippines office spot rents

1,800 (P/sqm/month) Makati Premium Makati Grade A Ortigas Grade A BGC Grade A

1,600

1,400

1,200

1,000

800

600

400

1Q13 1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20

Source: Colliers, Regis Partners

Exhibit 28: Philippines residential condo prices

350,000 (P/sqm) Makati Premium Rockwell Premium Bonifacio Premium

300,000

250,000

200,000

150,000

100,000

1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20

Source: Colliers, Regis Partners

The other risk to the peso is that it is simply not cheap. The real effective exchange rate has appreciated by

15.5% since February 2018 and is up 57% since 2004 (see Exhibit 29). Meanwhile a positive for the currency

and, more importantly, for an economy whose biggest export remains people, is that the remittances from

overseas workers have been much less badly hit by the pandemic than earlier feared. After an initial 19.3%

YoY collapse in cash remittances in US dollar terms in May which was the biggest monthly YoY decline since

January 2001, it is a positive surprise that remittance were only down 0.9% YoY in US dollar terms in the first

ten month of 2020 and were up 2.9% YoY in October (see Exhibit 30). Similarly, BPO revenues have also held

up better than expected with the feedback that BPOs continue to take up new space.

17 December 2020 14

Please see important disclosure information at the end of this report.Exhibit 29: Philippines real effective exchange rate

(2010=100) Philippines real effective exchange rate

120

110

100

90

80

70

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: BIS

Exhibit 30: Philippines overseas workers cash remittances %YoY

50 (%YoY)

Overseas workers cash remittances %YoY

40

30

20

10

0

-10

-20

-30

-40

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: CEIC Data, BSP

Meanwhile it is worth noting, in the context of the anticipated cyclical rebound in 2021, that the Philippines

had enjoyed an already extended eight-year-long investment cycle and related credit cycle prior to the

pandemic; though investment momentum has slowed in recent quarters. The annualised gross fixed capital

formation to GDP ratio has fallen from a 35-year high of 27.4% in 1Q19 to 23.1% in 3Q20 (see Exhibit 31).

As for credit growth, total banking system loan growth was only 0.8% YoY in October, down from 10.8% YoY

in March (see Exhibit 32). Still there remains room for credit expansion since the gross loan-to-deposit ratio

of the banking system is only 74%, though up from 63% in late 2013. Meanwhile, inflation remains, for now at

least, within the central bank’s target range of 2-4%. Headline CPI inflation was 3.3% YoY in November while

core CPI inflation was 3.2% YoY (see Exhibit 33).

17 December 2020 15

Please see important disclosure information at the end of this report.Exhibit 31: Philippines annualised gross fixed capital formation as % of nominal GDP

28 (%) Annualised gross fixed capital formation as % of nominal GDP

26

24

22

20

18

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: CEIC Data

Exhibit 32: Philippines banking system loan growth

20 (%YoY)

Philippines banking system loan growth

15

10

5

0

Aug-18

Aug-19

Aug-20

May-18

Oct-18

May-19

Oct-19

May-20

Oct-20

Jun-18

Nov-18

Jun-19

Nov-19

Jun-20

Sep-18

Sep-19

Sep-20

Mar-18

Jul-18

Mar-19

Jul-19

Mar-20

Jul-20

Apr-18

Apr-19

Apr-20

Jan-18

Feb-18

Dec-18

Jan-19

Feb-19

Dec-19

Jan-20

Feb-20

Source: BSP

Exhibit 33: Philippines CPI inflation and BSP policy rate

12 (%) BSP key overnight RRP rate Core CPI inflation CPI inflation

10

8

6

4

2

0

(2)

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: CEIC Data, BSP

17 December 2020 16

Please see important disclosure information at the end of this report.Analyst Certification:

I, Christopher Wood, certify that all of the views expressed in this research report accurately reflect my personal views about the

subject security(ies) and subject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly,

related to the specific recommendations or views expressed in this research report.

Registration of non-US analysts: Christopher Wood is employed by Jefferies Hong Kong Limited, a non-US affiliate of Jefferies LLC

and is not registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies LLC,

a FINRA member firm, and therefore may not be subject to the FINRA Rule 2241 and restrictions on communications with a subject

company, public appearances and trading securities held by a research analyst.

As is the case with all Jefferies employees, the analyst(s) responsible for the coverage of the financial instruments discussed in

this report receives compensation based in part on the overall performance of the firm, including investment banking income. We

seek to update our research as appropriate, but various regulations may prevent us from doing so. Aside from certain industry

reports published on a periodic basis, the large majority of reports are published at irregular intervals as appropriate in the analyst's

judgement.

Investment Recommendation Record

(Article 3(1)e and Article 7 of MAR)

Recommendation Published December 17, 2020 , 09:05 ET.

Recommendation Distributed December 17, 2020 , 09:05 ET.

Explanation of Jefferies Ratings

Buy - Describes securities that we expect to provide a total return (price appreciation plus yield) of 15% or more within a 12-month

period.

Hold - Describes securities that we expect to provide a total return (price appreciation plus yield) of plus 15% or minus 10% within

a 12-month period.

Underperform - Describes securities that we expect to provide a total return (price appreciation plus yield) of minus 10% or less

within a 12-month period.

The expected total return (price appreciation plus yield) for Buy rated securities with an average security price consistently below

$10 is 20% or more within a 12-month period as these companies are typically more volatile than the overall stock market. For Hold

rated securities with an average security price consistently below $10, the expected total return (price appreciation plus yield) is

plus or minus 20% within a 12-month period. For Underperform rated securities with an average security price consistently below

$10, the expected total return (price appreciation plus yield) is minus 20% or less within a 12-month period.

NR - The investment rating and price target have been temporarily suspended. Such suspensions are in compliance with applicable

regulations and/or Jefferies policies.

CS - Coverage Suspended. Jefferies has suspended coverage of this company.

NC - Not covered. Jefferies does not cover this company.

Restricted - Describes issuers where, in conjunction with Jefferies engagement in certain transactions, company policy or applicable

securities regulations prohibit certain types of communications, including investment recommendations.

Monitor - Describes securities whose company fundamentals and financials are being monitored, and for which no financial

projections or opinions on the investment merits of the company are provided.

Valuation Methodology

Jefferies' methodology for assigning ratings may include the following: market capitalization, maturity, growth/value, volatility and

expected total return over the next 12 months. The price targets are based on several methodologies, which may include, but are

not restricted to, analyses of market risk, growth rate, revenue stream, discounted cash flow (DCF), EBITDA, EPS, cash flow (CF),

free cash flow (FCF), EV/EBITDA, P/E, PE/growth, P/CF, P/FCF, premium (discount)/average group EV/EBITDA, premium (discount)/

average group P/E, sum of the parts, net asset value, dividend returns, and return on equity (ROE) over the next 12 months.

Jefferies Franchise Picks

Jefferies Franchise Picks include stock selections from among the best stock ideas from our equity analysts over a 12 month

period. Stock selection is based on fundamental analysis and may take into account other factors such as analyst conviction,

differentiated analysis, a favorable risk/reward ratio and investment themes that Jefferies analysts are recommending. Jefferies

Franchise Picks will include only Buy rated stocks and the number can vary depending on analyst recommendations for inclusion.

17Stocks will be added as new opportunities arise and removed when the reason for inclusion changes, the stock has met its desired

return, if it is no longer rated Buy and/or if it triggers a stop loss. Stocks having 120 day volatility in the bottom quartile of S&P

stocks will continue to have a 15% stop loss, and the remainder will have a 20% stop. Franchise Picks are not intended to represent

a recommended portfolio of stocks and is not sector based, but we may note where we believe a Pick falls within an investment

style such as growth or value.

Risks which may impede the achievement of our Price Target

This report was prepared for general circulation and does not provide investment recommendations specific to individual investors.

As such, the financial instruments discussed in this report may not be suitable for all investors and investors must make their own

investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors

as they deem necessary. Past performance of the financial instruments recommended in this report should not be taken as an

indication or guarantee of future results. The price, value of, and income from, any of the financial instruments mentioned in this

report can rise as well as fall and may be affected by changes in economic, financial and political factors. If a financial instrument

is denominated in a currency other than the investor's home currency, a change in exchange rates may adversely affect the price of,

value of, or income derived from the financial instrument described in this report. In addition, investors in securities such as ADRs,

whose values are affected by the currency of the underlying security, effectively assume currency risk.

Distribution of Ratings

Distribution of Ratings

IB Serv./Past12 Mos. JIL Mkt Serv./Past12 Mos.

Count Percent Count Percent Count Percent

BUY 1530 58.06% 138 9.02% 14 0.92%

HOLD 970 36.81% 25 2.58% 6 0.62%

UNDERPERFORM 135 5.12% 2 1.48% 1 0.74%

18Other Important Disclosures

Jefferies does business and seeks to do business with companies covered in its research reports, and expects to receive or intends

to seek compensation for investment banking services among other activities from such companies. As a result, investors should

be aware that Jefferies may have a conflict of interest that could affect the objectivity of this report. Investors should consider this

report as only a single factor in making their investment decision.

Jefferies Equity Research refers to research reports produced by analysts employed by one of the following Jefferies Group LLC

("Jefferies") group companies:

United States: Jefferies LLC which is an SEC registered broker-dealer and a member of FINRA (and distributed by Jefferies Research

Services, LLC, an SEC registered Investment Adviser, to clients paying separately for such research).

United Kingdom: Jefferies International Limited, which is authorized and regulated by the Financial Conduct Authority; registered in

England and Wales No. 1978621; registered office: 100 Bishopsgate, London EC2N 4JL; telephone +44 (0)20 7029 8000; facsimile

+44 (0)20 7029 8010.

Hong Kong: Jefferies Hong Kong Limited, which is licensed by the Securities and Futures Commission of Hong Kong with CE number

ATS546; located at Suite 2201, 22nd Floor, Cheung Kong Center, 2 Queen's Road Central, Hong Kong.

Singapore: Jefferies Singapore Limited, which is licensed by the Monetary Authority of Singapore; located at 80 Raffles Place

#15-20, UOB Plaza 2, Singapore 048624, telephone: +65 6551 3950.

Japan: Jefferies (Japan) Limited, Tokyo Branch, which is a securities company registered by the Financial Services Agency of Japan

and is a member of the Japan Securities Dealers Association; located at Tokyo Midtown Hibiya 30F Hibiya Mitsui Tower, 1-1-2

Yurakucho, Chiyoda-ku, Tokyo 100-0006; telephone +813 5251 6100; facsimile +813 5251 6101.

India: Jefferies India Private Limited (CIN - U74140MH2007PTC200509), licensed by the Securities and Exchange Board of India

for: Stock Broker (NSE & BSE) INZ000243033, Research Analyst INH000000701 and Merchant Banker INM000011443, located at

42/43, 2 North Avenue, Maker Maxity, Bandra-Kurla Complex, Bandra (East), Mumbai 400 051, India; Tel +91 22 4356 6000.

Australia: Jefferies (Australia) Securities Pty Limited (ACN 610 977 074), which holds an Australian financial services license (AFSL

487263) and is located at Level 22, 60 Martin Place, Sydney NSW 2000; telephone +61 2 9364 2800.

This report was prepared by personnel who are associated with Jefferies (Jefferies International Limited, Jefferies Hong Kong

Limited, Jefferies Singapore Limited, Jefferies (Japan) Limited, Tokyo Branch, Jefferies India Private Limited), Jefferies (Australia)

Pty Ltd; or by personnel who are associated with both Jefferies LLC and Jefferies Research Services LLC ("JRS"). Jefferies LLC is

a US registered broker-dealer and is affiliated with JRS, which is a US registered investment adviser. JRS does not create tailored

or personalized research and all research provided by JRS is impersonal. If you are paying separately for this research, it is being

provided to you by JRS. Otherwise, it is being provided by Jefferies LLC. Jefferies LLC, JRS, and their affiliates are collectively

referred to below as "Jefferies". Jefferies may seek to do business with companies covered in this research report. As a result,

investors should be aware that Jefferies may have a conflict of interest that could affect the objectivity of this report. Investors

should consider this report as only one of many factors in making their investment decisions. Specific conflict of interest and other

disclosures that are required by FINRA and other rules are set forth in this disclosure section.

***

If you are receiving this report from a non-US Jefferies entity, please note the following: Unless prohibited by the provisions of

Regulation S of the U.S. Securities Act of 1933, as amended, this material is distributed in the United States by Jefferies LLC, which

accepts responsibility for its contents in accordance with the provisions of Rule 15a-6 under the US Securities Exchange Act of

1934, as amended. Transactions by or on behalf of any US person may only be effected through Jefferies LLC. In the United Kingdom

and European Economic Area this report is issued and/or approved for distribution by Jefferies International Limited ("JIL”) and is

intended for use only by persons who have, or have been assessed as having, suitable professional experience and expertise, or by

persons to whom it can be otherwise lawfully distributed.

JIL allows its analysts to undertake private consultancy work. JIL’s conflicts management policy sets out the arrangements JIL

employs to manage any potential conflicts of interest that may arise as a result of such consultancy work. Jefferies LLC, JIL and

their affiliates, may make a market or provide liquidity in the financial instruments referred to in this report; and where they do make

a market, such activity is disclosed specifically in this report under “company specific disclosures”.

For Canadian investors, this material is intended for use only by professional or institutional investors. None of the investments or

investment services mentioned or described herein is available to other persons or to anyone in Canada who is not a "Designated

Institution" as defined by the Securities Act (Ontario). In Singapore, Jefferies Singapore Limited (“JSL”) is regulated by the Monetary

Authority of Singapore. For investors in the Republic of Singapore, this material is provided by JSL pursuant to Regulation 32C of

the Financial Advisers Regulations. The material contained in this document is intended solely for accredited, expert or institutional

investors, as defined under the Securities and Futures Act (Cap. 289 of Singapore). If there are any matters arising from, or in

19connection with this material, please contact JSL, located at 80 Raffles Place #15-20, UOB Plaza 2, Singapore 048624, telephone:

+65 6551 3950. In Japan, this material is issued and distributed by Jefferies (Japan) Limited to institutional investors only. In Hong

Kong, this report is issued and approved by Jefferies Hong Kong Limited and is intended for use only by professional investors as

defined in the Hong Kong Securities and Futures Ordinance and its subsidiary legislation. In the Republic of China (Taiwan), this

report should not be distributed. The research in relation to this report is conducted outside the People’s Republic of China (“PRC”).

This report does not constitute an offer to sell or the solicitation of an offer to buy any securities in the PRC. PRC investors shall

have the relevant qualifications to invest in such securities and shall be responsible for obtaining all relevant approvals, licenses,

verifications and/or registrations from the relevant governmental authorities themselves. In India, this report is made available

by Jefferies India Private Limited. In Australia, this report is issued and/or approved for distribution by, or on behalf of, Jefferies

(Australia) Securities Pty Ltd. It is directed solely at wholesale clients within the meaning of the Corporations Act 2001 of Australia

(the “Corporations Act”), in connection with their consideration of any investment or investment service that is the subject of this

report. This report may contain general financial product advice. Where this report refers to a particular financial product, you

should obtain a copy of the relevant product disclosure statement or offer document before making any decision in relation to the

product. Recipients of this document in any other jurisdictions should inform themselves about and observe any applicable legal

requirements in relation to the receipt of this document.

This report is not an offer or solicitation of an offer to buy or sell any security or derivative instrument, or to make any investment. Any

opinion or estimate constitutes the preparer's best judgment as of the date of preparation, and is subject to change without notice.

Jefferies assumes no obligation to maintain or update this report based on subsequent information and events. Jefferies, and their

respective officers, directors, and employees, may have long or short positions in, or may buy or sell any of the securities, derivative

instruments or other investments mentioned or described herein, either as agent or as principal for their own account. This material

is provided solely for informational purposes and is not tailored to any recipient, and is not based on, and does not take into account,

the particular investment objectives, portfolio holdings, strategy, financial situation, or needs of any recipient. As such, any advice or

recommendation in this report may not be suitable for a particular recipient. Jefferies assumes recipients of this report are capable

of evaluating the information contained herein and of exercising independent judgment. A recipient of this report should not make

any investment decision without first considering whether any advice or recommendation in this report is suitable for the recipient

based on the recipient’s particular circumstances and, if appropriate or otherwise needed, seeking professional advice, including tax

advice. Jefferies does not perform any suitability or other analysis to check whether an investment decision made by the recipient

based on this report is consistent with a recipient’s investment objectives, portfolio holdings, strategy, financial situation, or needs.

By providing this report, neither JRS nor any other Jefferies entity accepts any authority, discretion, or control over the management

of the recipient’s assets. Any action taken by the recipient of this report, based on the information in the report, is at the recipient’s

sole judgment and risk. The recipient must perform his or her own independent review of any prospective investment. If the recipient

uses the services of Jefferies LLC (or other affiliated broker-dealers), in connection with a purchase or sale of a security that is a

subject of these materials, such broker-dealer may act as principal for its own accounts or as agent for another person. Only JRS

is registered with the SEC as an investment adviser; and therefore neither Jefferies LLC nor any other Jefferies affiliate has any

fiduciary duty in connection with distribution of these reports.

The price and value of the investments referred to herein and the income from them may fluctuate. Past performance is not a guide

to future performance, future returns are not guaranteed, and a loss of original capital may occur. Fluctuations in exchange rates

could have adverse effects on the value or price of, or income derived from, certain investments.

This report may contain forward looking statements that may be affected by inaccurate assumptions or by known or unknown risks,

uncertainties, and other important factors. As a result, the actual results, events, performance or achievements of the financial

product may be materially different from those expressed or implied in such statements.

This report has been prepared independently of any issuer of securities mentioned herein and not as agent of any issuer of securities.

No Equity Research personnel have authority whatsoever to make any representations or warranty on behalf of the issuer(s). Any

comments or statements made herein are those of the Jefferies entity producing this report and may differ from the views of other

Jefferies entities.

This report may contain information obtained from third parties, including ratings from credit ratings agencies such as Standard &

Poor’s. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the

related third party. Jefferies does not guarantee the accuracy, completeness, timeliness or availability of any information, including

ratings, and is not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained

from the use of such content. Third-party content providers give no express or implied warranties, including, but not limited to, any

warranties of merchantability or fitness for a particular purpose or use. Neither Jefferies nor any third-party content provider shall

be liable for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses,

20legal fees, or losses (including lost income or profits and opportunity costs) in connection with any use of their content, including

ratings. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold or sell

securities. They do not address the suitability of securities or the suitability of securities for investment purposes, and should not

be relied on as investment advice.

Jefferies research reports are disseminated and available electronically, and, in some cases, also in printed form. Electronic research

is simultaneously made available to all clients. This report or any portion hereof may not be reprinted, sold or redistributed without

the written consent of Jefferies. Neither Jefferies nor any of its respective directors, officers or employees, is responsible for

guaranteeing the financial success of any investment, or accepts any liability whatsoever for any direct, indirect or consequential

damages or losses arising from any use of this report or its contents. Nothing herein shall be construed to waive any liability Jefferies

has under applicable U.S. federal or state securities laws.

For Important Disclosure information relating to JRS, please see https://adviserinfo.sec.gov/IAPD/Content/Common/

crd_iapd_Brochure.aspx?BRCHR_VRSN_ID=483878 and https://adviserinfo.sec.gov/Firm/292142 or visit our website at https://

javatar.bluematrix.com/sellside/Disclosures.action, or www.jefferies.com, or call 1.888.JEFFERIES.

© 2020 Jefferies Group LLC

21You can also read