Microinsurance Product Pool - public Overview and assessment of Allianz microinsurance products

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Microinsurance

Product Pool

Overview and assessment

of Allianz microinsurance products

Allianz SE

Oct 2014

public

Introduction

This microinsurance product pool lists the microinsurance products of Allianz Group that

currently provide insurance cover to low-income people in emerging markets and

developing countries. Products launched since June 2013 which still have less than 1,000

inforce (active) policies are not included.

Two non-microinsurance products are included at the end to show why some Allianz

products are not considered microinsurance although they also serve low-income people.

This initiative supports the “Transparency” value of our Allianz microinsurance values:

Allianz Microinsurance Values1

Passion Quality Fairness Transparency

e.g. product pool

Information on each product is presented in three sections:

A. Product specifications Gives a high-level explanation how the product looks like

(distribution, benefits, pricing)

2

B. Product assessment Matches the product against the Allianz

microinsurance definition and assessment tool.

This includes

1. Knock-out criteria: “Can we call this product micro?”, and

2. Qualitative criteria: “How well does the product fulfill our

microinsurance values?”2

C. Product brochures where available

We will update this product pool every April/May and October as new microinsurance

products are launched and existing products are modified or taken off market. We try to list

products from the moment that over 1,000 inforce (active) policies are first reached until the

last policy matures. However, there is no duty to update (see disclaimer).

Contact

Martin Hintz +49 89 3800-18401 Is this really the latest?

See our microinsurance website for the

© Allianz SE 2014

Microinsurance E-mail:

Allianz SE martin.hintz@allianz.com most recent reports and publications

1) To learn more about the Allianz microinsurance values please see our latest microinsurance business updates.

2) The product assessment shows how well the products is intended to serve low-income families in compliance with our

microinsurance values (“as planned”). It does not verify how products and distribution look on the ground (“as is”).

Example: Allianz may have produced product brochures although for various logistical reasons they do not reach the

insured. The assessment is also no indicator for actual business success. 2

Knock-out Qualitative criteria:

Overview1 criteria: "Can "How well aligned with our

we call it micro?" microinsurance values?"

A B C D 1 2 3 4 5 6 7

Insurance principles

Dev. Country or EM

Low-income focus

No subsidies >50%

Strong Risk Mgmt

Other benefits

Customers involved

Voluntary

Customer education

Product simplicity

Low transaction costs

Quality

rank Details

Product avg. on

# Country Company Name c1-c7 page

Allianz Family + + + +

1 Colombia

Colombia Term Life + -

+ + +

+ + 1.4 5

Allianz Home + + + +

2 Colombia

Colombia Business + -

+ + +

+ + 1.4 7

Allianz Life + + + +

3 Colombia

Colombia & Maternity + -

+ + +

+ + 1.4 9

Ivory Allianz Mobile + + + + +

4 Coast Africa Funeral + - -

+ + + +

1.4 11

Bajaj Life + + + + +

5 India

Allianz Life Savings + - -

+ + + +

1.3 15

Allianz Credit Life + + +

update 6 Indonesia

Life Plus + - + + +

+ +

1.3 17

Ivory Allianz Funeral + + + +

7 Coast Africa Insurance + - -

+

+

+ +

1.3 21

Allianz Scratch- + + +

8 Indonesia

General card PA2 - + -

+ + +

+ 1.1 25

Allianz Motorcycle + + +

9 Malaysia

General + PA2 + - -

+ +

- + 1.0 29

West + + +

10 Africa & Allianz Africa Credit Life + -

+

- -

+ +

1.0 33

Egypt

West + +

11 Africa

Allianz Africa Crop Index + -

+

- + + + 1.0 35

Savings- + +

12 Burkina Allianz Africa

Life + - - + -

+ +

0.9 39

Bajaj Allianz Cattle & + +

13 India

General Livestock + - - +

+

- + 0.9 41

Bajaj Allianz + +

14 India

General

PA Plus + -

+ +

- - + 0.9 43

© Allianz SE 2014

1) See our website for a full explanation of our assessment methodology

2) PA: Personal Accident

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success 3

Knock-out Qualitative criteria:

Overview1 criteria: "Can "How well aligned with our

we call it micro?" microinsurance values?"

A B C D 1 2 3 4 5 6 7

Insurance principles

Dev. Country or EM

Low-income focus

No subsidies >50%

Strong Risk Mgmt

Other benefits

Customers involved

Voluntary

Customer education

Product simplicity

Low transaction costs

Quality

rank Details

Product avg. on

# Country Company

Name c1-c7 page

Bajaj Group + +

15 India

Allianz Life Term Life + - - - +

+ +

0.9 45

Bajaj Allianz Personal +

16 India

General Accident + - -

+

- - + 0.6 47

Phased out products Knock-out Qualitative criteria:

Quality

since last update May 2014 criteria: "Can "How well aligned with our

rank

we call it micro?" microinsurance values?"

Product avg. Reason for

# Country Company Name A B C D 1 2 3 4 5 6 7 c1-c7 phase out

Distribution

Allianz PA2 & + + + + +

1 Colombia

Colombia Dental + +

-

+ + + +

1.6 contract

ended

Phased out

Mada- Allianz + + due to low

3 gascar Africa

Mobile PA2 - - -

+

-

+

+ 0.7 product

quality

Non-qualifying products Knock-out Qualitative criteria:

Quality

due to failing on criteria A - D criteria: "Can "How well aligned with our

rank Details

we call it micro?" microinsurance values?"

Product avg. on

# Country Company Name A B C D 1 2 3 4 5 6 7 c1-c7 page

not

1

Ivory

Coast

Allianz

Africa

Mobile

Savings micro

49

not

2 Malaysia

Allianz Life

+ General

Life & PA2 micro

53

Non-qualification means that a product has failed to meet any of the four basic criteria A – D of the Allianz

Group microinsurance definition, although they may still address needs of low-income people. Sample

© Allianz SE 2014

cases are shown here to better illustrate conditions under which this may happen.

1) See our website for a full explanation of our assessment methodology

2) PA: Personal Accident

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success 4

1. Colombia: Family Term Life

A. Product Specifications

Product name “Seguro de Vida” (Life Insurance)

(generic or marketing name)

Product type Term Life

(e.g. term life, endowment, motorcycle)

Company name Allianz Colombia

Country Colombia

Distribution partner type Microfinance Institution (MFI)

(e.g. MFIs, banks, coops, retailers)

Launch date 1 July 2012

(and stop date if any)

1-sentence product description Voluntary Group Term Life Insurance that provides life insurance cover

to the group’s members (and optional their partners) plus additional

funeral cover to the insured group members and up to 4 freely chosen

close relatives

Group or individual product Group

Voluntary opt-in, opt-out or Voluntary opt-in

compulsory

Covered risks & Death due to any cause of insured (i.e. group member and optional –

benefits / sum insured against additional premium – the partner): COP 3mn to COP 15mn

depending on chosen premium plan (~ USD 1,600 to 8,000)

Funeral benefit to member and 4 freely chosen close relatives (which

can include the partner): up to maximum COP 3mn (~ USD 1,600) for

all premium plans. Benefit expires after 2 death cases

Maximum sum assured per person: COP 30mn (~ USD 16,000), e.g. if

a client has multiple policies of this product

Premium range Minimum COP 9,960 per month (~ USD 5.50) for minimum benefits for

(min, max) single insured and 4 relatives

Maximum COP 42,068 per month (~ USD 23.00) for maximum benefits

for insured, partner and 4 relatives

Avg. premium / year COP 122,880 (USD ~ 68.00)

(annualize if necessary)

Other comments The product is only available to active clients of the MFI, i.e. those who

have an active credit and/or savings account with that MFI

90 days waiting period for minor pre-existing conditions

180 days waiting period for major pre-existing conditions (e.g. cancer)

and suicide

© Allianz SE 2014

>> back to Overview 5

1. Colombia: Family Term Life

B. Product Assessment1

Product: Seguro de Vida Ranking2 Rationale / Comments

A Insurance principles applied Fully applied

Developing country or emerging Colombia is an emerging market according to S&P

B

market

and a developing country according to World Bank

The MFI distributor targets low-income families, i.e. strata

Great majority of insured people

1 - 3 of the 6-step Colombian socioeconomic stratification.

C or assets from low-income This can also be seen by the low maximum loan amount of

segment

their micro-credit segment of COP 2.3mn (~ USD 1,300)

No government subsidies of

D

more than 50%

No government subsidies

The product protects several family members against death

Significant contribution to risk which is a significant risk. Coverage includes pre-existing

1

management of end customers

++ conditions which allows for the inclusion of more vulnerable

people (subject to waiting periods).

End-customer receives other

2 tangible benefits (e.g. discounts, - None

lottery etc.)

Workshops were done by the MFI in selected branches to

End-customers involved in garner input for the product design, especially as previous

3

product development

++ life insurance offers had not found wide acceptance among

customers

Voluntary opt-in (++),

4 voluntary opt-out (+) ++ Fully voluntary for existing customers of the MFI

or compulsory (-)

Simple brochures are provided, and – because many

customers are not fully literate - the bank’s staff also gives

Customer education and

5

feedback mechanisms in place

++ verbal explanations. Customers receive insurance

certificates, have access to a 24/7 hotline and to a special

claim help desk

Simple product without health declaration. Several plan

Simple product specifications

options exist, so the distinction of which family member has

6 (e.g. pre-underwritten, few + what level of coverage takes time to understand. Certain

exclusions)

waiting periods and exclusions exist.

Monthly batch processing from MFI to insurer, sales are

Strong measures to ensure low done complementary on top of other products (credit,

7

transaction costs

+ savings). A claim help desk and a bank agent help desk

achieve streamlining of the service processes

Overall ranking3 1.4

© Allianz SE 2014

C. Product Brochure: not available

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success >> back to Overview 6

2. Colombia: Home Business

A. Product Specifications

Product name “Seguro de Hogar” (Home insurance)

(generic or marketing name)

Product type Property

(e.g. term life, endowment, motorcycle)

Company name Allianz Colombia

Country Colombia

Distribution partner type Microfinance Institution (MFI)

(e.g. MFIs, banks, coops, retailers)

Launch date 1 July 2012

(and stop date if any)

1-sentence product description Voluntary Group Property insurance that covers private homes,

including those used for home-based business, against damage to the

building and its content arising from various risks such as fire,

lightening, flooding, windstorm, civil commotion etc.

Group or individual product Group

Voluntary opt-in, opt-out or Voluntary opt-in

compulsory

Covered risks & Costs of repair or replacement (but not improvement) of home and

benefits / sum insured home content damages due to below risks are covered as follows for

Plan 1/Plan 2 respectively

A: Fire, lightening, explosion, windstorm (incl. related rains and floods),

falling trees, falling aircraft and vehicle crashes: up to COP 20mn/15mn

(~ USD 11,000/8,000)

B: Water damage, flooding, avalanche and landslides: up to COP

5mn/3mn (~ USD 2,500/1,600)

C: Violent strikes, civil commotion and malicious acts by 3rd parties: up

to COP 10mn/7.5mn (~ USD 5,000/ 4,000)

D: Actions to contain damage, actions of public authorities and debris

removal: up to COP 2mn/1.5mn (~ USD 1,100/800)

Max. sum insured from all risks per home over the entire life of the

policy is COP 20mn (~ USD 11,000), i.e. should the accumulated

damages exceed that amount, the excess is not covered and coverage

will end

Premium range Minimum (Plan 2): COP 4,995 (~ USD 2.75) per month

(min, max) Maximum (Plan 1): COP 6,660 (~ USD 3.60) per month

Avg. premium / year COP 67,200 (~ USD 37.00)

(annualize if necessary)

Other comments The product is only available to active clients of the MFI, i.e. those who

have an active credit and/or savings account with that MFI

© Allianz SE 2014

Earthquake risk is not covered, as this is not considered important by

customers and would significantly increase the premium

A deductible of 10% applies to risks B and C above; risks A and D do

not have a deductible

>> back to Overview 7

2. Colombia: Home Business

B. Product Assessment1

Product: Seguro de Hogar Ranking2 Rationale / Comments

A Insurance principles applied Fully applied

Developing country or emerging Colombia is an emerging market according to S&P

B

market

and a developing country according to World Bank

The MFI distributor targets low-income families, i.e. strata

Great majority of insured people

1 - 3 of the 6-step Colombian socioeconomic stratification.

C or assets from low-income This can also be seen by the low maximum loan amount of

segment

their micro-credit segment of COP 2.3mn (~ USD 1,300)

No government subsidies of

D

more than 50%

No government subsidies

Several serious risks to home property are covered. The

Significant contribution to risk sums insured are high enough to allow micro-

1

management of end customers

++ entrepreneurs to quickly get back on their feet and resume

their home-run businesses after a claim.

End-customer receives other

2 tangible benefits (e.g. discounts, - None

lottery etc.)

The product was developed based on strong customer

End-customers involved in demand to cater to the insurance needs of small

3

product development

++ entrepreneurs that borrow from the MFI and often run their

business out of their private homes

Voluntary opt-in (++),

4 voluntary opt-out (+) ++ Fully voluntary for existing customers of the MFI

or compulsory (-)

Simple brochures are provided, and – because many

customers are not fully literate - the bank’s staff also gives

Customer education and

5

feedback mechanisms in place

++ verbal explanations. Customers receive insurance

certificates, have access to a 24/7 hotline and to a special

claim help desk

For a property product, design and policy wording are kept

Simple product specifications

relatively simple, with only 2 available coverage plans. Still,

6 (e.g. pre-underwritten, few + time is needed to explain the exact covered risks, the

exclusions)

deductibles and the claim procedure.

Monthly batch processing from MFI to insurer. No on-site

Strong measures to ensure low claim inspection needed. A claim help desk and a bank

7

transaction costs

+ agent help desk achieve streamlining of the service

processes

Overall ranking3 1.4

© Allianz SE 2014

C. Product Brochure: not available

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success >> back to Overview 8

3. Colombia: Life & Maternity

A. Product Specifications

Product name “Voy Seguro” (I go safely)

(generic or marketing name)

Product type Term Life

(e.g. term life, endowment, motorcycle)

Company name Allianz Colombia

Country Colombia

Distribution partner type Microfinance Institution (MFI)

(e.g. MFIs, banks, coops, retailers)

Launch date 1 November 2012

(and stop date if any)

1-sentence product description Voluntary Group Term Life Insurance that also provides maternity

benefits to the insured or partner during pregnancy and after birth

Group or individual product Group

Voluntary opt-in, opt-out or Voluntary opt-in

compulsory

Covered risks & Death of the insured due to any cause: COP 4mn basic life benefit +

benefits / sum insured COP 600k for food basket + COP 500k funeral assistance, i.e. total

death benefits of COP 5.1mn (~ USD 2,800)

Maternity benefits for insured or partner: COP 400k at 6 months into

pregnancy and COP 200k after birth, i.e. total maternity benefits of COP

600k (~ USD 330)

Maximum sum assured per person: COP 32mn (~ USD 18,000), e.g. if

a client holds multiple policies of this product

Premium range COP 4,990 per month (~ USD 2.75)

(min, max) One standard plan only; no other premium and benefit options

Avg. premium / year COP 59,880 (~ USD 33.00)

(annualize if necessary)

Other comments The product is only available to active micro-loan clients of the MFI (the

MFI offers no savings services)

The food basket and funeral assistance benefits are usually paid out as

a cash lump sum together with the basic life insurance benefit

90 days waiting period for pregnancy and minor pre-existing conditions

180 days waiting period for major pre-existing conditions (e.g. cancer)

and suicide

© Allianz SE 2014

>> back to Overview 9

3. Colombia: Life & Maternity

B. Product Assessment1

Product: Voy Seguro Ranking2 Rationale / Comments

A Insurance principles applied Fully applied

Developing country or emerging Colombia is an emerging market according to S&P and a

B

market

developing country according to World Bank

The MFI distributor targets low-income families, i.e. strata

Great majority of insured people

1 - 3 of the 6-step Colombian socioeconomic stratification.

C or assets from low-income This can also be seen by the low average loan amount of

segment

their borrowers of COP 2mn (~ USD 1,100)

No government subsidies of

D

more than 50%

No government subsidies

Death is a significant risk and coverage includes pre-

Significant contribution to risk existing conditions (subject to waiting periods). Moreover,

1

management of end customers

++ maternity expenses are a very frequent risk even if the

related policy benefits are not high.

End-customer receives other

2 tangible benefits (e.g. discounts, - None

lottery etc.)

Focus Group Discussions with the MFI customers have

strongly influenced the product, for example that the larger

End-customers involved in

3

product development

++ part of the maternity benefits is already paid out at 6

months pregnancy. This allows the expectant mothers to

prepare in time for the delivery and post-natal phase.

Voluntary opt-in (++),

voluntary opt-out (+) Fully voluntary option that can be added to the MFIs credit

4 ++ offering

or compulsory (-)

Customers receive verbal explanations from the bank’s

Customer education and staff. Brochures are not used as customers are often semi-

5

feedback mechanisms in place

++ literate. Customers receive insurance certificates, have

access to a 24/7 hotline and to a special claim help desk

Simple product specifications Simple, easy to understand product design with only one

6 (e.g. pre-underwritten, few + available standard plan. No health declaration required.

exclusions) However, certain waiting periods and exclusions exist.

Monthly batch processing from MFI to insurer, sales are

Strong measures to ensure low done complementary on top of other products (credit,

7

transaction costs

+ savings). A claim help desk and a bank agent

help desk achieve streamlining of the service processes

Overall ranking3 1.4

© Allianz SE 2014

C. Product Brochure: not available

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

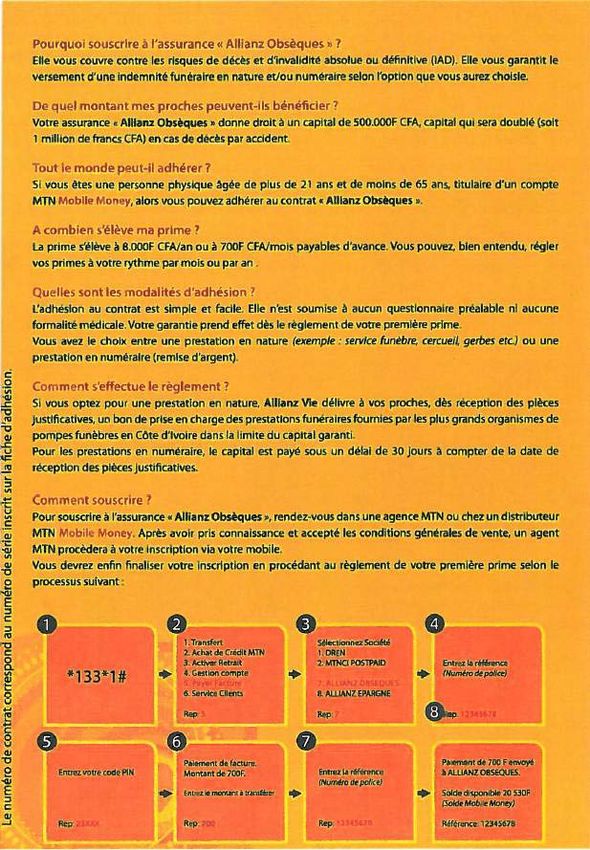

microinsurance values, not an indicator for actual business success >> back to Overview 104. Ivory Coast: Mobile Funeral

A. Product Specifications

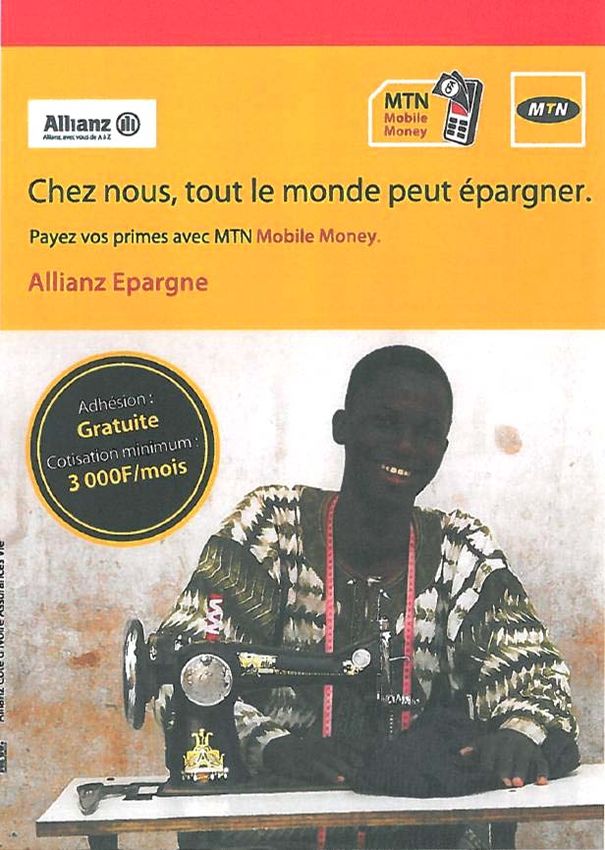

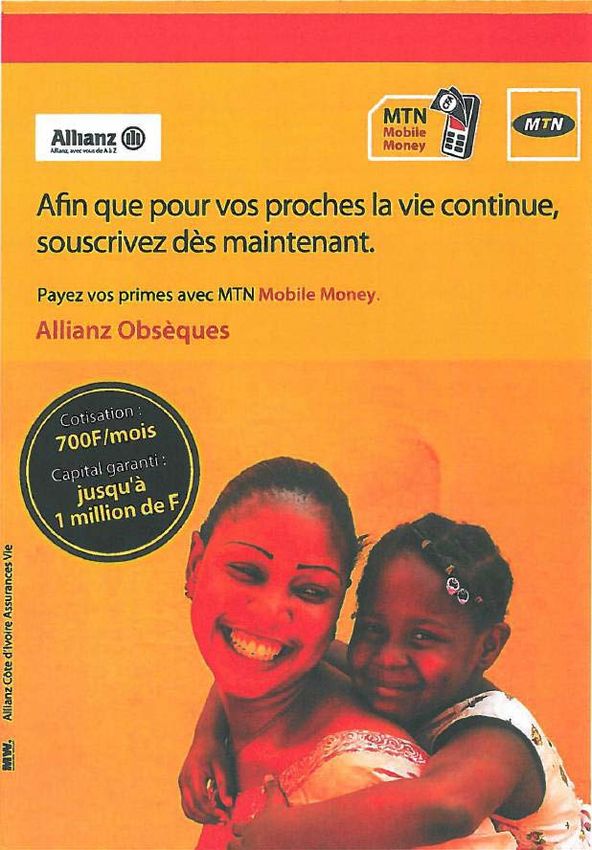

Product name “Allianz Obsèques”

(generic or marketing name)

Product type Term life insurance

(e.g. term life, endowment, motorcycle)

Company name Allianz Côte d’Ivoire Assurance Vie

Country Ivory Coast

Distribution partner type Telecommunication company

(e.g. MFIs, banks, coops, retailers)

Launch date 1 June 2012

(and stop date if any)

1-sentence product description Voluntary group life insurance for “mobile money” account holders

of the partnering telecommunication company; coverage includes

protection against death due to all causes and total permanent disability

Group or individual product Group

Voluntary opt-in, opt-out or Voluntary opt-in

compulsory

Covered risks & Natural death or total permanent disability:

benefits / sum insured FCFA 500,000 (~ USD 900)

Accidental death: FCFA 1,000,000 (~ USD 1,800)

Part of the death benefit (up to 100%) can be chosen as direct

payment to a designated funeral home to cover funeral expenses

(i.e. “in kind” benefit)

Premium range FCFA 8,000 (~ USD 14) for yearly or FCFA700 (~ USD 1.3)

(min, max) for monthly payment; premiums are automatically deducted

from “mobile money” account

Avg. premium / year FCFA 8,400 (~ USD 15), based on the fact that most insured

(annualize if necessary) choose the monthly premium payment option

Other comments Age limits are 21 to 65, with disability coverage expiring at age 61

Enrollment still happens by physical form filling at the telco’s outlets, but

premium payment is only possible through mobile money

Multiple enrollments are not allowed

© Allianz SE 2014

>> back to Overview 114. Ivory Coast: Mobile Funeral

B. Product Assessment1

Allianz

Product: Ranking2 Rationale / Comments

Obsèques

A Insurance principles applied Fully applied

Developing country or emerging Ivory Coast, after 10 years of civil war and a political crisis

B

market

in 2011, is more still very much a developing country

Great majority of insured people The vast majority of the population of Ivory Coast is low

C or assets from low-income income and the low sums insured also only appeal to low-

segment income segments

No government subsidies of

D

more than 50%

No government subsidies

Death is a significant risk for low-income families in Ivory

Significant contribution to risk Coast. Optional direct payment of a part of the benefit to

1

management of end customers

++ funeral homes helps to insure “proper” payout usage.

The “payout to annual premium ratio” of 60 is decent

End-customer receives other

2 tangible benefits (e.g. discounts, - None

lottery etc.)

End-customers involved in

3

product development

- No

Voluntary opt-in (++),

voluntary opt-out (+) Fully voluntary. Moreover, the monthly premium payment

4 ++ option allows for cash-flow friendly payment

or compulsory (-)

Customers receive a physical insurance certificate,

Customer education and

5

feedback mechanisms in place

++ additional information via SMS and have access to a 8/5

hotline of the insurer

Simple product specifications

Policy terms and exclusions are much simplified.

6 (e.g. pre-underwritten, few ++ No health underwriting and waiting period

exclusions)

Strong measures to ensure low Premium collection through auto-debit from “mobile money”

7

transaction costs

++ accounts is very efficient

Overall ranking3 1.4

© Allianz SE 2014

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success >> back to Overview 124. Ivory Coast: Mobile Funeral

C. Product Brochure

© Allianz SE 2014

Front

>> back to Overview 134. Ivory Coast: Mobile Funeral

C. Product Brochure

© Allianz SE 2014

Back

>> back to Overview 145. India: Life + Savings

A. Product Specifications

Product name Sarve Shakti Suraksha (SSS)

(generic or marketing name)

Product type 5-year term life insurance with systematic savings incorporated

(e.g. term life, endowment, motorcycle)

Company name Bajaj Allianz Life Insurance Company Limited

Country India

Distribution partner type Non-bank Microfinance Institutions (MFIs),

(e.g. MFIs, banks, coops, retailers) Regional Rural Banks, Banking Correspondents,

Customer Support Centers, Cooperatives

Launch date Launch date: April 2008

(and stop date if any) Stop date: effective August 2013, this product has been closed for the

issuance of new group policies, due to regulatory changes

New members could still enroll under existing group policies until latest

July 2014

Now completely closed for new business and phasing out over the

next 5 years until 2019

1-sentence product description A combination of term insurance and systematic savings benefits

designed to provide risk protection as well as alternative savings

opportunities

The product term is 5 years

Group or individual product Group Insurance

Voluntary opt-in, opt-out or Voluntary opt-in

compulsory

Covered risks & Sum Insured: Minimum INR 2500 (~ USD 50), no limit on maximum

benefits / sum insured coverage (Subject to underwriting limits)

Risks covered: Natural and accidental death + disability

Premium range Minimum INR 500 (~ USD 10) per annum

(min, max) no limit on maximum premium

Avg. premium / year INR 1,750 (~ USD 35)

(annualize if necessary)

Other comments The product has won numerous awards, including the Skoch Award for

Financial Inclusion 2011 & 2012

© Allianz SE 2014

>> back to Overview 155. India: Life + Savings

B. Product Assessment1

Sarve Shakti

Product: Ranking2 Rationale / Comments

Suraksha (SSS)

A Insurance principles applied Fully applied

Developing country or emerging India is an emerging market according to S&P

B

market and a developing country according to World Bank

Great majority of insured people

Majority of the premiums collected for this product

C or assets from low-income are under INR 2,000 (~ USD 40) per year

segment

No government subsidies of All premiums are paid by the customer.

D

more than 50% There is no premium subsidy

SSS offers life coverage and a savings feature but

Significant contribution to risk claims and especially savings balances are relatively

1

management of end customers

+ small, even for low-income Indians. Moreover, in case

of RBBs outstanding loan balances are deducted first

End-customer receives other

2 tangible benefits (e.g. discounts, - None

lottery etc.)

End-customers involved in

3

product development

- No

Voluntary opt-in (++), It is a voluntary opt-in. In some cases premium amounts

voluntary opt-out (+) are also bundled with the loan installments to make the

4 ++ product affordable. However, there is no compulsion

or compulsory (-)

from the distribution partner’s side at any point in time

Allianz hotline printed on every brochure and policy

Customer education and

5

feedback mechanisms in place

++ document. A systematic “Value for the Customer”

education initiative has been put in place, too

Simple product specifications Guaranteed issuance except where questions on

6 (e.g. pre-underwritten, few ++ the health declaration are marked as affirmative.

exclusions) Only exclusion: Suicide not covered in year 1

The delivery channel fully integrates the product

Strong measures to ensure low into existing business processes.

7

transaction costs

++ Collection is often aligned with loan repayment.

Other operational tasks are also outsourced

Overall ranking3 1.3

© Allianz SE 2014

C. Product Brochure: not available

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

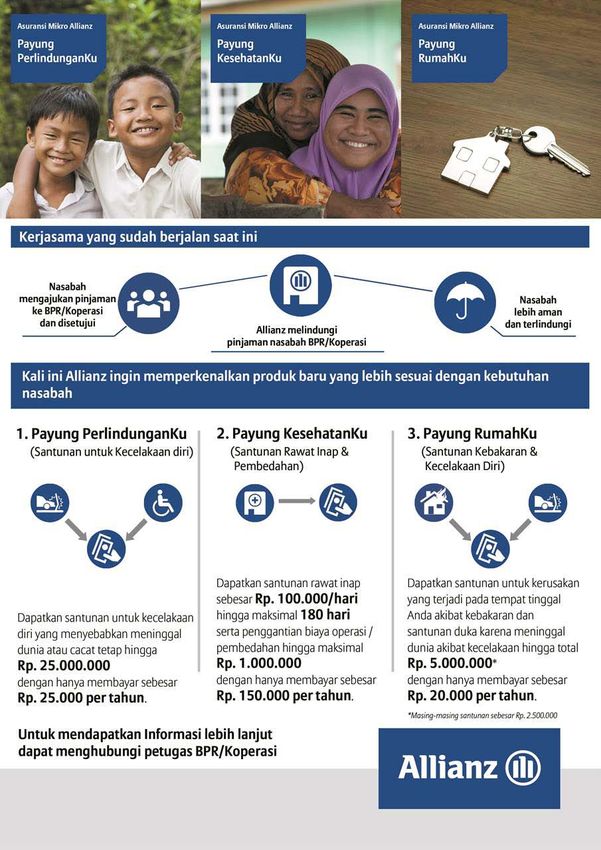

microinsurance values, not an indicator for actual business success >> back to Overview 166. Indonesia: Credit Life Plus (additional brochure added, see page 20)

A. Product Specifications

Product name Payung Keluarga (Family Umbrella)

(generic or marketing name)

Product type Term Life (attached to credit accounts), with riders

(e.g. term life, endowment, motorcycle)

Company name Allianz Indonesia

Country Indonesia

Distribution partner type Banks, MFIs

(e.g. MFIs, banks, coops, retailers)

Launch date 1 Sep 2006 for base product

(and stop date if any) 27 Nov 2013 for riders

1-sentence product description Compulsory group credit life coverage (conventional or takaful) with

flexible benefits and voluntary add-on riders

Group or individual product Group

Voluntary opt-in, opt-out or Compulsory for base product (with benefit package pre-configured by

compulsory MFI), and voluntary for add-on riders

Covered risks & Base Product:

benefits / sum insured Risk: Death of debtor and spouse (optional)

Benefit: Outstanding loan balance, or original loan amount

Additional “funeral” benefit of up to 2x original loan (optional)

Loans: IDR 0 – max. 200mn (~ USD 0 - 20,000)

Riders (since Dec-2013):

Personal Accident for accidental death and total or partial

permanent disability, with benefits of up to IDR 25,000,000

(~ USD 2,500) - pro-rated for partial disability

Home Insurance for fire; with relocation benefits up to IDR

5,000,000 (~ USD 500) and additional accidental death benefit

of up to IDR 5,000,000 (~ USD 500)

Hospital Cash; with daily lumpsum of up to IDR 250,000

(~ USD 25) from 1st day of hospitalization, for max. 180 days,

and max. IDR 2,500,000 (~ USD 250) of surgery benefits

Premium range Base Product:

(min, max) IDR 100 to 1mn (~ USD 0.1 – 110), depending on loan amount,

tenor & benefits

Riders (annualized premium, as coverage runs as long at the loans):

Personal Accident: IDR 8,000 – 20,000 (~ USD 0.8 – 2)

Home Insurance: IDR 5,000 – 30,000 (~ USD 0.5 – 3)

Hospital Cash: IDR 100,000 – 250,000 (~ USD 10 – 25)

Avg. premium / year Base Product: IDR 12,000 (~ USD 1.3)

(annualize if necessary) Riders: n.a.

© Allianz SE 2014

Other comments Base product is modular, with theoretically 54 different

benefit configurations for MFIs to choose from

Additional resources Case Study: How Allianz Indonesia reached over 1 million with

microinsurance (Allianz 2013)

>> back to Overview 176. Indonesia: Credit Life Plus

B. Product Assessment1

Payung

Product: Ranking2 Rationale / Comments

Keluarga

A Insurance principles applied Applied

Developing country or emerging Indonesia is an emerging market according to S&P

B

market and a developing country according to World Bank

Great majority of insured people 98% of insured loans are under IDR 5mn (~ USD 550).

C or assets from low-income This serves as a reliable proxy for „majority low income“

segment customers

No government subsidies of

D

more than 50% No government subsidies

Death of a breadwinner is a significant risk to low-income

families in Indonesia. Although most loans are covered for

Significant contribution to risk

1

management of end customers

++ the outstanding balance only, 20% of them also carry some

cash payout to the families. Voluntary riders add further

flexibility to customers to manage various other risks.

End-customer receives other

2 tangible benefits (e.g. discounts, - None

lottery etc.)

Extensive market research was done to understand the

End-customers involved in target market. Life risk was only the top4 identified

3

product development

+ customer risk. The voluntary hospital cash rider, though,

addresses the top1 identified customer risk of sickness.

Voluntary opt-in (++), The base credit life cover is compulsory for customers as

4 voluntary opt-out (+) + per the MFIs benefit configuration. However, the additional

or compulsory (-) riders can be taken by customers on voluntary basis.

Brochures are provided by some MFIs. Other MFIs

distribute member cards instead. MFI staff is also equipped

Customer education and

5

feedback mechanisms in place

+ with flip-charts to explain the product on the spot. Direct

helpline and Allianz address are not provided, except for

the rider products. No systematic feedback collection.

Simple product specifications Free coverage limit up to IDR 10mn (~ USD 1,100).

6 (e.g. pre-underwritten, few ++ Only 2 exclusions: Suicide and insurance related crime

exclusions) (+ age limit 17-60)

Product, distribution and collection are fully integrated

Strong measures to ensure low

7

transaction costs

++ with MFI micro loans, including for riders. Most of the data

entry and claims handling is also “outsourced” to the MFIs

© Allianz SE 2014

Overall ranking3 1.3

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success >> back to Overview 186. Indonesia: Credit Life Plus

C. Product Brochure – Compulory base product

Member Card as alternative to brochure

Front

Back

© Allianz SE 2014

>> back to Overview 196. Indonesia: Credit Life Plus

C. Product Brochure – Voluntary add-on riders (NEW)

© Allianz SE 2014

207. Ivory Coast: Funeral Insurance

A. Product Specifications

Product name Assurance Obséques (Funeral Insurance)

(generic or marketing name)

Product type Funeral Insurance

(e.g. term life, endowment, motorcycle)

Company name Allianz Ivory Coast

Country Ivory Coast

Distribution partner type Microfinance Institutions (MFIs)

(e.g. MFIs, banks, coops, retailers)

Launch date October 2009

(and stop date if any)

1-sentence product description Payment of a lump sum in case of death due to any cause, with variable

options (accidental death, education grant for children, family

coverage); exact offering may vary per MFI

Group or individual product Group

Voluntary opt-in, opt-out or Voluntary opt-in

compulsory

Covered risks & Death: lump sum from XOF 300,000 to 2,000,000 (~ USD 600 – 4,000),

benefits / sum insured depending on selected benefit plan

With some MFIs,

spouse, children, and parents can be selectively added to

coverage

the death benefit is doubled in case of accidental death

the insured can choose to have approx. 60% of the death

benefit paid directly to an undertaker

a supplementary education rider can be added, which provides

additional XOF 250,000 to 500,000 for 4 to 6 months as school

fees payment (depending upon chosen option)

Premium range From XOF 5,000 to 92,000 (~ USD 10 – 195) per year

(min, max) An additional XOF 1,000 (~ USD 2) one time subscription fee is

charged

Avg. premium / year XOF 22,000 (~ USD 45)

(annualize if necessary)

Other comments None

© Allianz SE 2014

>> back to Overview 217. Ivory Coast: Funeral Insurance

B. Product Assessment1

Assurance

Product: Ranking2 Rationale / Comments

Obséques

A Insurance principles applied Fully applied

Developing country or emerging Ivory Coast, after 10 years of civil war and a political crisis

B

market

in 2011, is more still very much a developing country

Great majority of insured people The customers of the MFI distribution partners are low-

C or assets from low-income medium segment, with at least 80% of the insured

segment belonging to the 60% of population with the lowest incomes

No government subsidies of

D

more than 50%

Premiums are not subsidized

Funerals are a significant expense in Ivory Coast, and the

product significantly contributes to covering these. Family

Significant contribution to risk

1

management of end customers

++ and parents can be covered as well at very competitive

pricing. The possibility to add an education rider gives

further options to customize the product to customer needs.

End-customer receives other No tangible other benefits. But with some MFIs the insured

2 tangible benefits (e.g. discounts, - has the option that part of the payout is paid to the

lottery etc.) undertaker to ensure a proper funeral, no matter what

End-customers involved in

3

product development

- No customer studies

Voluntary opt-in (++),

4 voluntary opt-out (+) ++ 100% voluntary

or compulsory (-)

Simple language brochures are provided. Some MFIs also

Customer education and

5

feedback mechanisms in place

+ give Allianz contact details on their brochures. No service

hotline and systematic collection of customer feedback.

Simple product specifications

Simple base product, with simple add-on options (e.g.

6 (e.g. pre-underwritten, few ++ education rider), no medical selection

exclusions)

The MFIs takes charge of distribution, subscription, data

Strong measures to ensure low

7

transaction costs

++ and premiums collection, and parts of the claims process.

This significantly lowers costs

Overall ranking3 1.3

© Allianz SE 2014

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success >> back to Overview 227. Ivory Coast: Funeral Insurance

C. Product Brochure – MFI1

Outside

© Allianz SE 2014

Inside

>> back to Overview 237. Ivory Coast: Funeral Insurance

C. Product Brochure – MFI2

Front

Back

© Allianz SE 2014

>> back to Overview 248. Indonesia: Scratch-Card Personal Accident

A. Product Specifications

Product name • Kartu ProteksiKU (“My Protection Card”)

(generic or marketing name)

Product type • Personal Accident

(e.g. term life, endowment, motorcycle)

Company name • Allianz General Indonesia

Country • Indonesia

Distribution partner type • MFIs (Micro Finance Institutions)

(e.g. MFIs, banks, coops, retailers)

Launch date • 2011 (for microinsurance channel: 1-Oct-2012)

(and stop date if any)

1-sentence product description • Personal Accident insurance in form of credit-card sized pre-paid

voucher; instant activation and coverage confirmation via SMS

Group or individual product • Individual

Voluntary opt-in, opt-out or • Voluntary opt-in

compulsory

Covered risks & • Death caused by accident: IDR 25mn (~ USD 2,750)

benefits / sum insured • Total permanent disability caused by accident: maximum IDR 25mn (~

USD 2,750) depending on degree of physical disability

Premium range • All vouchers cost IDR 27,500 (~ USD 3.0) and are valid for one year

(min, max)

Avg. premium / year • IDR 27,500 per year (~ USD 3.00)

(annualize if necessary)

Other comments • The product is also sold through other channels, e.g. tied agents.

However, this assessment focuses only on the microinsurance

segment, i.e. distribution through MFIs. Business figures are only

reported from this channel.

© Allianz SE 2014

>> back to Overview 258. Indonesia: Scratch-Card Personal Accident

B. Product Assessment1

Product: Kartu Proteksiku Ranking2 Rationale / Comments

A Insurance principles applied Fully applied

Developing country or emerging Indonesia is an emerging market according to S&P and a

B

market developing country according to World Bank

Product is distributed through MFIs that focus on low-

Great majority of insured people

income customers. As the product is voluntary, some

C or assets from low-income insured may actually be better off, but the majority can still

segment

be considered low-income in the Indonesian context.

No government subsidies of

D

more than 50% No government subsidies

Personal Accident sold to the general public, i.e. not to a

Significant contribution to risk special high risk group (e.g. construction workers), does

1

management of end customers

- not contribute significantly to risk management of low-

income people as the likelihood of a claim is very low

End-customer receives other The exceptionally high payout-to-premium ratio of 920/1

2 tangible benefits (e.g. discounts, + (USD 2,750 coverage for 3.00 premium) qualifies as a

lottery etc.) “tangible other benefit”.

End-customers involved in

3

product development

- No

Voluntary opt-in (++),

4 voluntary opt-out (+) ++ Fully voluntary

or compulsory (-)

Customer receives full policy wording as booklet and a

Customer education and

5

feedback mechanisms in place

++ handy insurance card to be put in wallet, including Allianz

service number and address.

Simple product specifications Simple product format (voucher), automatic acceptance via

6 (e.g. pre-underwritten, few ++ SMS with no exclusions except age limit. Booklet with full

exclusions) policy wording is a bit lengthy.

SMS activation and single premium payment minimize

Strong measures to ensure low

7

transaction costs

+ distribution and collection costs. Claim settlement is

traditional. No integrated IT system.

Overall ranking3 1.1

© Allianz SE 2014

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success >> back to Overview 268. Indonesia: Scratch-Card Personal Accident

C. Policy Document

Policy booklet (cover)

© Allianz SE 2014

Policy booklet (first inside page)

>> back to Overview 278. Indonesia: Scratch-Card Personal Accident

C. Policy Document

Insurance card (front)

© Allianz SE 2014

Insurance card (back)

>> back to Overview 289. Malaysia: Motorcycle + PA

A. Product Specifications

Product name Motorcycle & Personal Acccident

(generic or marketing name)

Product type Motorcycle & Personal Accident

(e.g. term life, endowment, motorcycle)

Company name Allianz General Malaysia

Country Malaysia

Distribution partner type Postal Service

(e.g. MFIs, banks, coops, retailers)

Launch date 1 July 2011

(and stop date if any)

1-sentence product description Motorcycle coverage for third-party liability and

(optional) loss and damage to due to accident

+ Personal Accident as semi-bundled extra offer

Group or individual product Individual

Voluntary opt-in, opt-out or Voluntary opt-in

compulsory

Covered risks & Motorcycle loss & damage: maximum current

benefits / sum insured market value of motorcycle

PA: Death due to accident: MYR 5,000 (~ USD 1,600)

PA: Total permanent diability or dismemberment:

MYR 5,000 (~ USD 1,600)

PA: Bereavement benefit: MYR 500 (~ USD 160)

Premium range for Motorcylce: n.a.; for PA: MYR 15 (~ USD 5) per year

(min, max)

Avg. premium / year For Motorcycle: MYR 100 (~ USD 33)

(annualize if necessary) For PA: MYR 15 (~ USD 5)

Other comments Motorcycle premiums vary per brand and engine volume

Product is also marketed by tied agents at different premiums

(excluded here)

Third-party liability cover is a statutory requirement for motorcycles in

Malaysia. Additional motorcycle cover and personal accident cover are

voluntary

© Allianz SE 2014

>> back to Overview 299. Malaysia: Motorcycle + PA

B. Product Assessment1

Motorcycle

Product: Ranking2 Rationale / Comments

& PA

A Insurance principles applied Applied

Developing country or emerging Malaysia is an emerging market according to S&P

B

market and a developing country according to World Bank

Great majority of insured people

Customer base of postal service is generally

C or assets from low-income low-income, especially for insurance sales

segment

No government subsidies of

D

more than 50% No government subsidies

Motorcycle coverage is comparable in importance to

Significant contribution to risk car coverage in developed markets. It is a statutory

1

management of end customers

++ requirement in Malaysia. PA is sensible for motorcyclist as

a high risk group

End-customer receives other

2 tangible benefits (e.g. discounts, - None

lottery etc.)

End-customers involved in

3

product development

- No

Voluntary opt-in (++), Several options to choose from: Third-Party liability only (a

4 voluntary opt-out (+) ++ statutory requirement), comprehensive (TPL + loss &

or compulsory (-) damage) and on-top Personal Accident cover

Brochures and policy documents are provided,

Customer education and

5

feedback mechanisms in place

++ including an Allianz customer service hotline. Coverage

is widely used and well known in Malaysia.

Simple product specifications Motorcycle policy wording is quite lenghty, the same

6 (e.g. pre-underwritten, few - as for all other distribution channels (e.g. tied agents),

exclusions) and the same as for car insurance

Distribution through low-cost Malaysian postal service

Strong measures to ensure low

7

transaction costs

+ allows somewhat lower distribution and operational

costs (e.g. vis-à-vis tied agents)

Overall ranking3 1.0

© Allianz SE 2014

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success >> back to Overview 309. Malaysia: Motorcycle + PA

C. Product Brochure

Outside

Personal Accident only. No brochure for Motorcycle component.

© Allianz SE 2014

>> back to Overview 319. Malaysia: Motorcycle + PA

C. Product Brochure

Inside

Personal Accident only. No brochure for Motorcycle component.

© Allianz SE 2014

>> back to Overview 3210. West Africa & Egypt: Credit Life

A. Product Specifications

Product name • Assurance Décès Emprunteur (Life Insurance for Entrepreneurs)

(generic or marketing name)

Product type • Term Life (attached to credit accounts)

(e.g. term life, endowment, motorcycle)

Company name • Allianz Africa and local subsidiaries

Country • Cameroon, Burkina Faso, Egypt, Ivory Coast, Madagascar, Senegal

Distribution partner type • Microfinance Institutions (MFIs)

(e.g. MFIs, banks, coops, retailers)

Launch date • 13-Jan-2008

(and stop date if any)

1-sentence product description • In case of death of the loan taker due to all causes or in case of total

permanent disability of the loan taker due to accident, Allianz repays

100% of the initial loan amount

Group or individual product • Group

Voluntary opt-in, opt-out or • Compulsory

compulsory

Covered risks & • Death of the loan taker due to all causes

benefits / sum insured • Death of spouse (as voluntary add-on, Senegal only)

• Total permanent disability of the loan taker due to accident (medically

certified)

• Sum Insured: 100% of the initial loan amount from which:

• The MFI receives the outstanding loan balance

• The micro-entrepreneur’s family receives the difference

between the initial loan amount and the outstanding loan

balance

Premium range • Avg. 0.6% of loan amount (depending on risk characteristics of the

(min, max) insured group)

Avg. premium / year • USD 3 per loan

(annualize if necessary) • loans run for an average of 12 months with an avg. loan size USD 540

Other comments • Developed and distributed in cooperation with

Planet Guarantee (except Cameroon and

Ivory Coast)

© Allianz SE 2014

>> back to Overview 3310. West Africa & Egypt: Credit Life

B. Product Assessment1

Assurance Décès

Product: Ranking2 Rationale / Comments

Emprunteur

A Insurance principles applied Applied

Burkina Faso, Cameroon, Egypt, Ivory Coast, Madagascar

Developing country or emerging

B

market and Senegal are all developing countries according to

World Bank

The vast majority of insured are low income micro-

Great majority of insured people

entrepreneurs. This can be seen from their average loan

C or assets from low-income size of USD 540 (data from Cameroon and Ivory Coast not

segment

included)

No government subsidies of

D

more than 50% No government subsidies

Death is a significant risk and there is a direct payout to the

Significant contribution to risk family (after deduction of the loan balance). Coverage of

1

management of end customers

+ HIV+ or diabetic entrepreneurs facilitates their access to

credit. Accidental disability risk is less significant

End-customer receives other

2 tangible benefits (e.g. discounts, - None

lottery etc.)

A market and demand study was done. Product design and

End-customers involved in

3

product development

++ education materials were pilot tested with micro-

entrepreneurs

Voluntary opt-in (++),

voluntary opt-out (+) The product is compulsory for the credits of all MFI

4 - partners

or compulsory (-)

The MFI’s credit officers are trained to orally explain the

Customer education and product to their clients, but no local language material for

5

feedback mechanisms in place

- the customer. Regular exchange on customer complaints

between MFIs and the broker (Planet Guarantee)

Simple product specifications No pre-underwriting. Only 3 exclusions (suicide, radiation,

6 (e.g. pre-underwritten, few ++ war). No medical exclusions. Simplified disability definition

exclusions) and easy claims documentation

The mandatory underwriting-free group insurance

Strong measures to ensure low approach lowers transaction costs. Most processes are

7

transaction costs

++ outsourced to the MFIs and the broker (Planet Guarantee)

which operate on lower costs than Allianz

Overall ranking3 1.0

© Allianz SE 2014

C. Product Brochure: not available

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

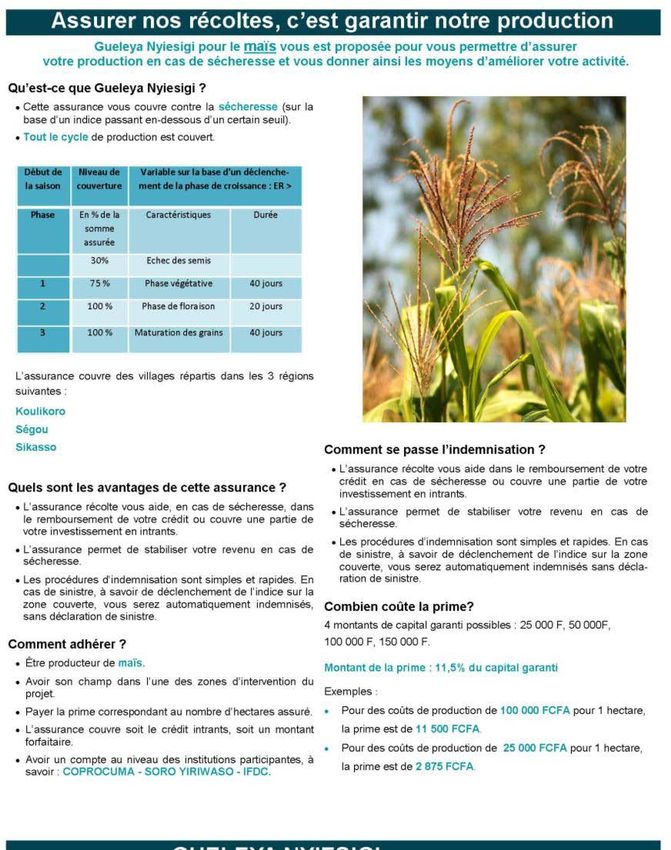

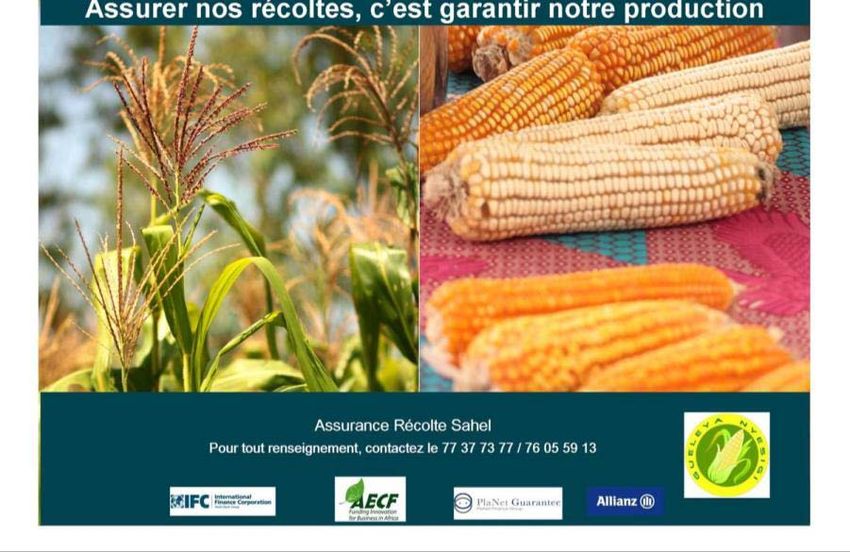

microinsurance values, not an indicator for actual business success >> back to Overview 3411. West Africa: Crop Index

A. Product Specifications

Product name Assurance Récolte Sahel (Sahel Harvest Insurance)

(generic or marketing name)

Product type Index insurance

(e.g. term life, endowment, motorcycle)

Company name Allianz Africa and local subsidiaries

Country Burkina Faso and Mali

Distribution partner type Microfinance Institutions (MFIs), banks, agricultural cooperatives and

(e.g. MFIs, banks, coops, retailers) agro-dealer networks

Launch date 1 June 2011

(and stop date if any)

1-sentence product description Covers outstanding loans of smallholder farmers; claims are triggered

automatically if the rainfall is insufficient for proper growth of the

farmers’ crops (corn or cotton)

Group or individual product Group

Voluntary opt-in, opt-out or Compulsory

compulsory

Covered risks & If evapotranspiration index1 below 54 – 58% (depending on crop and

benefits / sum insured region), i.e. total crop failure: Full coverage of outstanding loan amount

If evapotranspiration index* between approx 65% and 54 – 58%, i.e.

partial crop failure: Partial coverage of outstanding loan amount

Premium range 10 – 12% of loan amount, depending on crop and region

(min, max)

Avg. premium / year USD 27 per loan; avg. loan size is USD 235 (avg. loan duration: 3.5

(annualize if necessary) months)

Annualization not applicable because planting season only lasts 3.5

months

Other comments Only sold in a 4 - 6 weeks sales window before planting season

Expansion to more markets and crops types is planned

100% of the risk is reinsured by international reinsurance partners

Developed and distributed in cooperation with

Planet Guarantee

© Allianz SE 2014

1) Evapotranspiration is the sum of evaporation of water from plants and soil.

This index is independently measured by third parties using satellite data. >> back to Overview 3511. West Africa: Crop Index

B. Product Assessment1

Assurance Récolte

Product: Ranking2 Rationale / Comments

Sahel

Applied. The risk of insufficient rainfall in the insured areas

A Insurance principles applied is high. This is why the premium rate is also relatively high

at around 10-12%

Developing country or emerging Burkina Faso, Mali and Senegal are developing countries

B

market according to World Bank

Great majority of insured people The vast majority of insured are low income farmers. This

C or assets from low-income can be seen from their small farm sizes (avg. 1.3 ha) and

segment their low avg. loan size of USD 235

No government subsidies. However, an initial grant by

No government subsidies of

D

more than 50% AGRA (Alliance for a Green Revolution in Africa) helped

with product development and piloting

Low rainfall is a great risk for farmers. Outstanding loans

Significant contribution to risk

1

management of end customers

++ are hard to repay when harvests fail. The product

addresses this and eases access to credit

End-customer receives other

2 tangible benefits (e.g. discounts, - None

lottery etc.)

Extensive market and demand study before product

End-customers involved in

3

product development

++ development. Product and education materials were pilot

tested with a small number of farmers.

Voluntary opt-in (++), Although the product can be offered on a voluntary basis,

4 voluntary opt-out (+) - virtually all current distribution partners have made

or compulsory (-) coverage mandatory for their agro-loans

Intensive training of distribution channels and their field

Customer education and representatives. Raising of awareness through posters,

5

feedback mechanisms in place

+ radio, film. However, no access to a hotline or systematic

feedback mechanism

No underwriting and no exclusions. Conceptually, the index

Simple product specifications

is straightforward. But the exact technical definition and

6 (e.g. pre-underwritten, few + measurement method is complex. The product therefore

exclusions)

requires in-depth explanation

The (mandatory) group insurance approach lowers

transaction costs. The claims process is simplified by the

Strong measures to ensure low

7

transaction costs

+ index as it allows automatic triggering of claims.

Reinsurance coverage is essential and needs to be

administered

© Allianz SE 2014

Overall ranking3 1.0

1) See our website for a full explanation of our assessment methodology

2) For knock-out criteria A-D: or ; for criteria 1 – 7: “-” (0), “+” (1) or “++” (2)

3) Average of criteria 1 – 7. Minimum 0.0, maximum 2.0.

Note: A high ranking is only an indicator for compliance with Allianz’

microinsurance values, not an indicator for actual business success >> back to Overview 3611. West Africa: Crop Index

C. Product Brochure

© Allianz SE 2014

Flyer examples

>> back to Overview 3711. West Africa: Crop Index

C. Product Brochure

Inside

Personal Accident only. No brochure for Motorcycle component.

© Allianz SE 2014

Product brochure from Mali

>> back to Overview 38You can also read