Pemex and the Mexican Economy - March 8, 2019 by Deborah Watkins of LM Capital Group - Advisor Perspectives

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Pemex and the Mexican Economy

March 8, 2019

by Deborah Watkins

of LM Capital Group

Executive Summary

Pemex is a state-owned company that manages all of Mexico’s oil and gas sector. The majority of its oil

fields are located onshore or in shallow waters, yielding low extraction costs. Yet the company is

extremely inefficient and heavily indebted. Both production and proven reserves of oil are declining and

the company consistently loses money.

In response to Pemex’s worsening situation the government of former President Enrique Peña Nieto

introduced energy reforms which were approved by the Mexican Congress in 2013. The energy

reforms opened up the oil sector to foreign and private investment in the form of joint ventures. The

goal was for private companies to provide financing, share production costs, and transfer technical and

management skills to Pemex. However, the new President Manuel Lopez Obrador (AMLO) does not

have a favorable view of the energy reforms. He has a nationalistic vision for Mexico’s oil and gas

sector and would like to limit foreign and private sector involvement in the industry.

Fitch Ratings Inc. recently downgraded Pemex debt to one notch above junk. The ratings company

explained that the key driver for the downgrade is Pemex’s heavy tax burden, which represents a

significant share of the company’s cashflow. This tax burden has translated into low investment and

ballooning debt, rising 36% between 2014 and 2018 to reach $106 billion USD. Other factors also

contribute to Pemex’s poor bottom line numbers: substantial unfunded pension liabilities, dwindling

production due to low investment, corruption, fuel theft, as well as a bloated and inefficient corporate

culture.

In an attempt to stave off further credit rating downgrades, the government unveiled a bailout package

on February 15, 2019 of $5.5 billion USD. Markets were underwhelmed, and although Pemex bond

prices fell and the peso weakened, a major sell off was avoided in part through government

assurances that it would increase the financial support if necessary.

Pemex is crucial for the Mexican economy. Although energy’s contribution to GDP and its share of total

oil and gas exports are not very high (5% and 6% respectively in 2017) the company is very important

for three reasons: (1) there is heavy government reliance on Pemex for budget revenues (2) it is the

source of all oil and gas in Mexico and (3) it is a significant source of foreign exchange receipts. A

financial crisis in Pemex could result in a disruption to the supply of oil in the country; this could put a

Page 1, ©2019 Advisor Perspectives, Inc. All rights reserved.

serious drag on the economy. It could also jeopardize an important source of government revenue.

The strong link between Pemex and the Mexican economy means that a financial crisis at Pemex could

hurt Mexico’s sovereign credit rating. Thus far, investors and ratings agencies have not allowed for a

meaningful spillover. The Peso did weaken 0.5% against the dollar on February 15, following the

announcement of a lower than expected bailout package; however, it recovered by the end of the day.

And perhaps even more telling, Mexico was able to sell $2 billion in sovereign debt in mid-January,

2019. [11] This new debt was well-received and came with a coupon which is only slightly higher than

the rate on Mexico’s January, 2018 debt issuance.

Pemex’s future will depend on the government fully understanding the delicate situation of the

company. The decision of whether to continue to allow foreign and private sector involvement in the oil

industry will be of particular importance given the limited financial resources the government has

pledged in order to bolster Pemex.

LM Capital client accounts currently hold Pemex bonds. This analysis thus begs the question: why

does LM Capital hold Pemex bonds? As a matter of fact, what makes us different from other managers

is the ability to combine financial analysis with the understanding of what drives those results, both in

terms of politics and of the people that run the companies in which we invest. An institution’s credit risk

reflects both its ability to pay and its willingness to pay. Pemex’s special status, combined with the very

low cost of production, gives the company and the government many different levers that allow interest

and principal to be paid in a timely manner. We believe that Lopez Obrador knows he will be measured

by what happens in Pemex, as an easy way to judge if his policies are successful, so he will do what is

necessary to ensure its success.

———————————————————————————————————

Petroleos Mexicanos (Pemex) is a state-owned company that manages the oil and gas sector in

Mexico. It is a vertically integrated company participating in every stage of the oil exploration and

distribution process. It is Mexico’s largest company but it has serious structural and financial

weaknesses. It is inefficient, is heavily indebted, and has suffered a decline in both production and

proven reserves.

Pemex Overview

Pemex was created in 1938 when President Lazaro Cardenas nationalized the oil industry. In the

1960s the government started using Pemex for social and economic goals unrelated to oil. From

nationalization until the 2013 energy reforms, Pemex operated as a monopoly, having the exclusive

right to manage all petroleum activities in Mexico.

In response to declining production and Pemex’s growing debt, the government approved energy

reforms in 2013. The reforms amended the constitution in order to allow foreign and private investment

in the long-protected petroleum sector.

Pemex has the lowest production costs in Latin America.[16] Its competitive pre-tax cost structure is

Page 2, ©2019 Advisor Perspectives, Inc. All rights reserved.

due to the profile of Mexico’s oil fields. Over 90% of Mexico’s oil fields are located onshore or in

shallow waters. These types of oil fields are much easier to drill than offshore fields, allowing Pemex to

keep its production costs low and enjoy higher margins than its peers.[1]

Pemex’s annual budget is incorporated into the government’s budget and then submitted to the

Mexican Congress for approval. The Mexican government, which relies on transfers from Pemex to

fund a substantial portion of its own budget, has historically discouraged Pemex from retaining

earnings. Instead the government imposes a heavy tax burden on the company and provides incentives

for Pemex to employ a large number of workers. This limits long-term investment. The low levels of

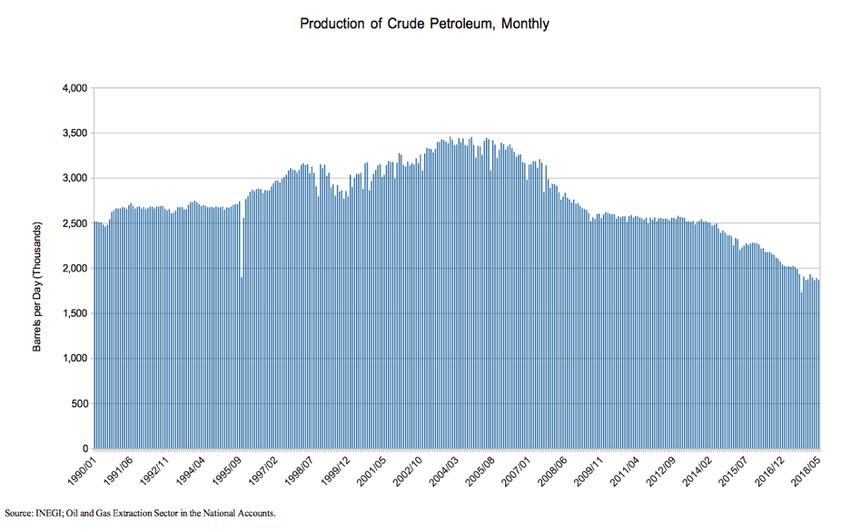

investment have resulted in a steady decline in oil production. Daily production of oil has declined 50%

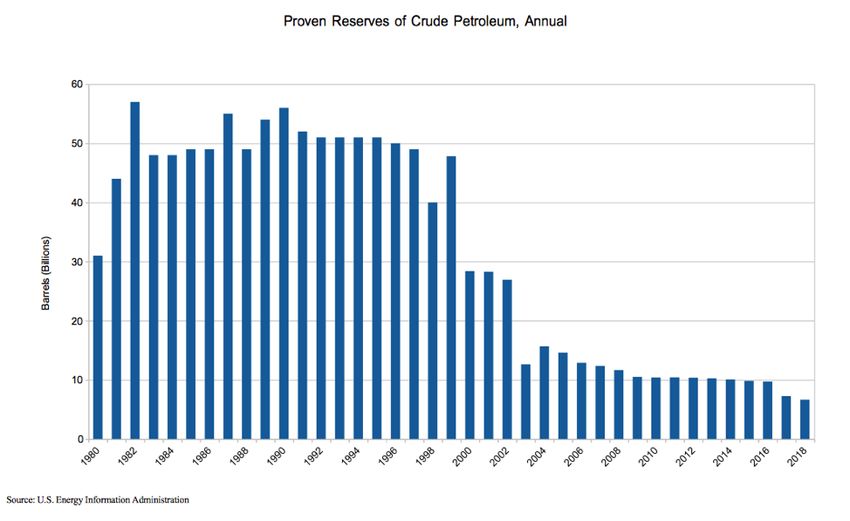

since its peak in 2004, dropping from 3.4 million barrels per day (bpd) to 1.73 million bpd in 2018.[12]

Proven reserves, though still substantial, are now less than a third of what they were twenty years

ago.[3]

The company has done little to stem this decline, and has actually cut investment in recent years.

Between 2014-2018 Pemex steadily reduced capital expenditures from $27 billion a year to $11

billion.[25] These expenditures fund the exploration and production of crude oil as well as the

technology that could make existing fields yield more output. This limits the amount that can be

dedicated to the exploration of new oil fields or to the acquisition of technology to raise output at

existing fields.

Figure 1. Production of Crude Petroleum

Page 3, ©2019 Advisor Perspectives, Inc. All rights reserved.

Source for Figure 1 [14]

Figure 2. Proven Reserves of Crude Petroleum, Annual

Page 4, ©2019 Advisor Perspectives, Inc. All rights reserved.Source for Figure 2 [9]

Insufficient investment also means that Mexico’s six refineries have not received necessary

maintenance or upgrades. They are outdated and ill-equipped to process the heavy mix of crude oil that

Mexico produces.[6] Instead, Mexico exports its crude oil to U.S. Gulf Coast refineries which process

the crude into gasoline and diesel and then ship it back to Mexico or other countries. Despite being a

significant producer of crude oil, Mexico imports over two-thirds of the processed gasoline and diesel it

uses.[8]

One of the goals of the 2013 energy reforms was to address declining production. However, President

Manuel Lopez Obrador who took office in December, 2018 has been vocal about his desire to block the

energy reform. He subscribes to a nationalistic view of the oil and gas sector and would like to see

Mexico become self-sufficient in energy.

Pemex’s Credit Rating Downgrade

AMLO has committed to provide financial support to Pemex in order to bolster the troubled company.

Yet recent announcements with monetary pledges have left investors and ratings agencies

unimpressed. They are left wondering whether the government fully understands the severity of

Pemex’s financial troubles.

Page 5, ©2019 Advisor Perspectives, Inc. All rights reserved.On January 25, 2019 Fitch Ratings Inc. downgraded Pemex’s credit rating from ‘BBB+’ to ‘BBB-‘. This

put the company’s credit rating only slightly above a junk bond rating. In its downgrade announcement,

the ratings company explained that the key driver for the downgrade was Pemex’s heavy tax burden,

which represents a significant share of the company’s cash flow.

The downgrade in Pemex’s credit rating came one day after the government had pledged financial

support to bolster Pemex. This pledge of a $25 billion Peso capital injection and $11 billion Peso in

reduced taxes in 2019, was meant to quell investor fears about Pemex’s weak financial position. Yet it

clearly was insufficient to convince the ratings agency that the downgrade was not necessary.

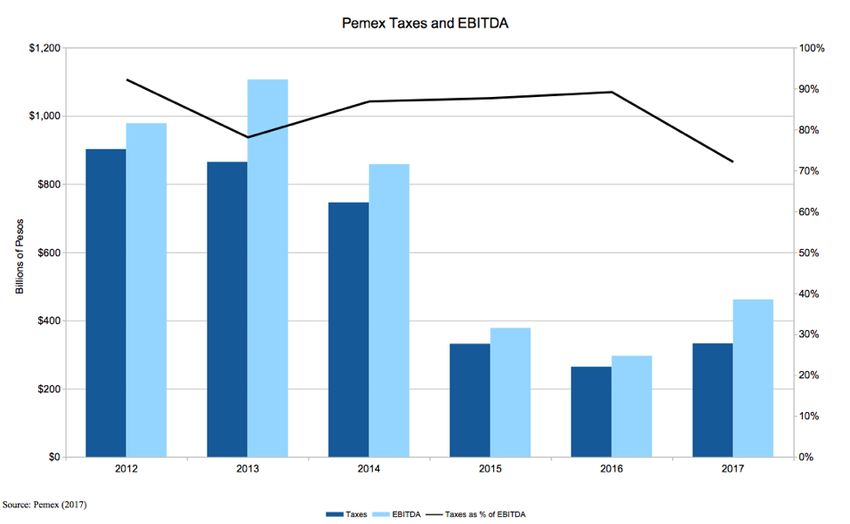

For years Pemex has been overtaxed. The company has historically paid 50-60% of its revenues in the

form of royalties and duties. Since the 2013 energy reforms, Pemex’s tax burden has been steadily

decreasing. Nevertheless, during the last five years transfers to the government represented 45% of

revenues. This still represents over 80% of EBITDA [7] and is a substantially higher tax burden than its

direct peers Petrobras or Ecopetrol.[17]

Figure 3. Pemex Taxes and EBITDA

Source for Figure 3 [24]

In addition to its heavy tax burden, Pemex’s pension liabilities also hurt its bottom line. The generous

Page 6, ©2019 Advisor Perspectives, Inc. All rights reserved.defined benefit plan has amounted to $66 billion USD.[18] Corruption, fuel theft and a bloated

workforce also contribute to Pemex’s lack of profitability, as do the inefficiencies stemming from

Pemex’s excessive vertical integration. Beyond participating at every stage of the oil production and

distribution process, the company provides, healthcare, schools and daycare to its employees.

Low profitability and decreasing output have forced the company to take on substantial leverage.

Pemex is the most indebted of the major oil companies. Its debt has ballooned to $106 billion USD in

2018, a 36% increase since 2014. The grand majority of this debt (over 80%) is denominated in US

dollars and is coming due shortly.[7] Nearly $30 billion USD of Pemex’s debt will come due in the next

three years and $5.3 billion USD must be paid by May, 2019.[17]

In its announcement of Pemex’s credit rating downgrade, Fitch made it clear that Pemex’s credit profile

is in fact commensurate with a ‘CCC’ rating which would classify the Pemex bonds as junk bonds.

Four factors stopped the ratings agency from punishing Pemex with a stronger downgrade: (1) its

competitive pre-tax structure, (2) substantial hydrocarbon reserves, (3) its control of the domestic

market and (4) the fact that the company is state-owned. Although the Pemex bonds do not have an

explicit guarantee from the government, Fitch “continues to expect the government to ensure Pemex

maintains a robust liquidity position to service debt”.[8]

The Mexican government immediately responded to the Fitch credit downgrade by announcing that

they would commit additional funds to bolster Pemex. On February 15, 2019 the government

announced a bailout package amounting to $5.5 billion USD per year. The package has four

components:

A capital injection of $1.3 billion USD

A reduction in the tax burden of $800 million USD

A transfer from SHCP of $1.8 billion USD

Savings from stemming fuel theft of $1.6 billion USD

The bailout package amounts to only 5% of Pemex’s outstanding debt. This may be enough to avoid a

crisis in the short term, but will not be sufficient to solve Pemex’s structural problems, low production

and its unreasonably high tax burden.

Indeed, markets appeared to be underwhelmed by the announced bailout measures. Pemex’s bond

prices fell and the Mexican currency weakened in response to the February 15 announcement. Yet the

weakening was measured, in large part because of the government’s pledge that Pemex would not

take on any more debt in 2019 and that the government would increase its financial support to Pemex

if these initial bailout measures proved to be insufficient.

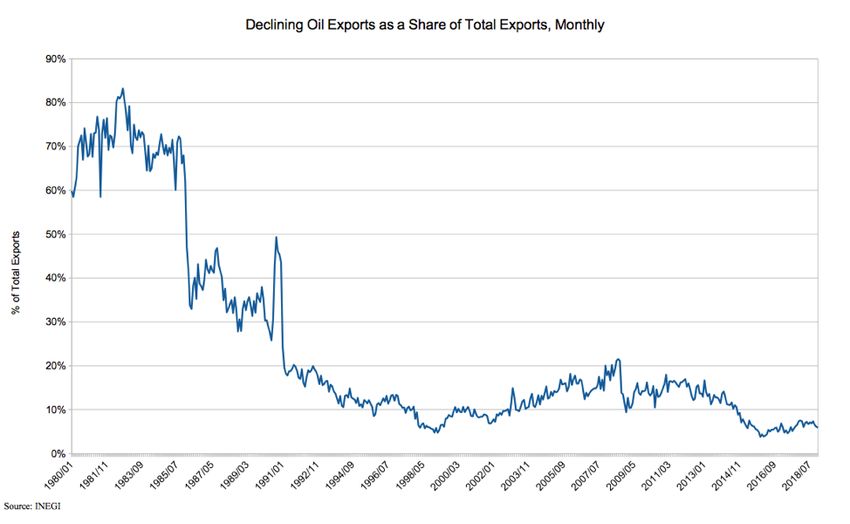

The Relationship between Pemex and the Mexican Economy

When looking at aggregate numbers, the contribution of the oil and gas sector to the economy is

relatively low. The sector contributed less than 5% to GDP in 2017. This value has been steadily

declining in recent years. Further, oil and gas only represent 6% of Mexico’s total exports. Declining oil

extraction and lower prices have been the main drivers of the decline.

Page 7, ©2019 Advisor Perspectives, Inc. All rights reserved.Nonetheless, Pemex is Mexico’s largest company and is strategically important to the overall economy

for three primary reasons: (1) its monopoly on the distribution of gas, (2) as a source of foreign

exchange and (3) its contribution to public finances.

Figure 4. Declining Contribution of the Oil Sector to GDP, Quarterly

Source for Figure 4 [14]

Figure 5. Declining Oil Exports as a Share of Total Exports, Monthly

Page 8, ©2019 Advisor Perspectives, Inc. All rights reserved.Source for Figure 5 [14]

Fuel Distribution

Pemex distributes all of the gasoline and diesel within Mexico, supplying 10,000 service stations

throughout the country.[7] A financial crisis in Pemex could result in a disruption of fuel distribution in

the country with negative consequences for the economy.

The country experienced the impact of a disruption in fuel supply in mid-January, 2019 following

AMLO’s attempts to stem fuel theft from Pemex. The fuel shortages caused miles-long lines at petrol

stations and left many businesses stalling. This is expected to to have a negative impact on first Q1

2019 growth figures.

Government Budget

Public finances rely heavily on transfers from Pemex, in part because Mexico’s non-oil tax collection is

among the lowest in Latin America. Historically, Pemex transfers to the government have represented

30-35% of government revenue.

Since 2014 this reliance has been declining due to dwindling oil production, lower oil prices and the

introduction of the tax and energy reforms. These reforms explicitly strove to reduce the government

Page 9, ©2019 Advisor Perspectives, Inc. All rights reserved.reliance on oil and gas production. In 2017 Pemex’s royalties, tax, duties and other payments to the

government amounted to 17.6% of the government’s annual budget.[16] The recently approved budget

for 2019 projects that oil revenue will account for 20% of government revenue.[2]

Foreign Exchange Receipts

Until 2014, oil exports were Mexico’s primary source of foreign exchange. Although it has dropped to

second place behind remittances, it is still one of the primary contributors of U.S. dollars to the

Mexican economy. In 2017 remittances, exports of petroleum and tourism contributed $28.8 billion,

$21.9 billion and $21.3 billion USD respectively to the Mexican economy.[13,20,21] Manufacturing

would dwarf these numbers; however, it is generally considered too broad of an industry to be counted

as a single source of foreign exchange.

The drop in oil prices during late 2014 as well as improvements in systems for tracking transfers

between Mexico and the U.S. have all contributed to the demotion of oil exports from a primary to

secondary source of foreign exchange.

Mexico’s Sovereign Rating

Given Pemex’s importance to the Mexican economy and to the government budget, a concern is that a

crisis at Pemex could spill over into Mexico’s sovereign credit rating.

Despite investor fears over Pemex’s precarious situation, in mid-January the AMLO administration was

able to raise $2 billion USD from global markets. These were 10-year USD denominated bonds with a

4.5% coupon - only slightly higher than the 3.5% coupon rate on debt Mexico issued in January

2018.[19]

The strong reception received by this issuance can be in large part interpreted as a vote of confidence

in AMLO’s promises of prudent fiscal management. This was recently bolstered by the seriousness of

his administration’s 2019 budget. The budget was generally considered to be conservative and

responsible. It will not increase the fiscal deficit which currently stands at 2.5% of GDP. It also will not

increase the debt and it promises a primary surplus equal to 1.0% of GDP. The budget also came with

a heavy cut in administrative expenses in favor of public investment.

AMLO may also have garnered goodwill when he chose to buy back $1.8 billion USD of $6 billion USD

airport bonds after his controversial decision to cancel the construction of a new airport in Mexico City

that was one-third complete. By avoiding a messy default, he is likely to have signaled to the market

that despite his left-leaning rhetoric he will ensure the government meets its obligations.

Conclusion

Pemex’s most immediate problem is its massive debt. The decrease in government reliance on Pemex

since 2014 is a positive trend. Yet such a drastic reduction in recent years means the government may

be limited in its ability to make drastic cuts to its reliance on Pemex in the near future while following

through on its budgetary promises.

Page 10, ©2019 Advisor Perspectives, Inc. All rights reserved.Given the limited financial resources the government can reasonably expect to extend to Pemex this

year, it will be particularly important that AMLO does not continue to insist on blocking foreign

investment in joint ventures.

The Mexican oil and gas industry would strongly benefit from the financing and technical expertise that

multinational oil companies could bring to joint ventures. This may go against the President’s

nationalistic view of the industry, but it would provide a clean way for the government to support Pemex

without having to make drastic changes to the government budget and risk Mexico’s credit rating.

In short, this would be a great opportunity to show investors that AMLO deserves the goodwill that

financial markets seem have been affording him in recent weeks.

LM Capital client accounts currently hold Pemex bonds. This analysis begs the question: why does LM

Capital hold Pemex bonds? What makes us different from other managers is the ability to combine

financial analysis with the understanding of what drives those results, both in terms of politics and of

the people that run the companies in which we invest.

The Pemex bonds are a holding in spite of their huge debt and mediocre management for the following

reasons:

They are a SOE (state-owned-enterprise), and a default would destroy the credit of Mexico,

which has to refinance 40 billion dollars in the next two years.

Pemex doesn’t have to pay for the crude it sells and, therefore, has huge operating profits

Taxation for Pemex is not consistent with the tax code for other companies. The government

uses it to finance other expenses and can, if it has to do so, lower Pemex’s taxes it to maintain

them as a viable entity.

Pemex is now in the world’s spotlight, and the government will make it its poster child in the fight

against corruption.

None of the joint ventures created in the Peña Nieto administration under the energy reform rules

have been cancelled.

Lopez Obrador knows he will be measured by what happens in Pemex, as it is an easy way to

judge if his policies are successful; so he will do what is necessary to ensure its success.

Barring dramatic changes, we will continue to hold our positions in Pemex bonds, and we feel the

current yield over 7% amply covers the perceived risk of the issuer not paying interest or principal.

Sources

1. J.P. Morgan. May 5, 2016. “Mexico 101: The 2016 Country Handbook”

2. WSJ. January 11, 2019 “Mexican Finance Officials seek to Boost investor Confidence”

3. Business Week. February 7, 2019 “Mexico’s Pemex Needs More Than Money to turn Itself

Around”

4. Business Week. January 30, 2019 “How two top emerging-market managers ditched Pemex Just

in time.”

Page 11, ©2019 Advisor Perspectives, Inc. All rights reserved.5. Business Week. February 5, 2019 “AMLO’s Pemex Pledge Sparks Rally in Oil-giant’s Battered

Bonds”

6. The Wilson Center’s Mexico Institute. October 25, 2016. “A Look at the Future of the Mexican

petroleum Industry After Energy Reform”

7. Moody’s Corp. October 18, 2018. “Petroleos Mexicanos: New government’s plan to abolish oil

exports and increase fuel sales raises cash flow and foreign exchange risks.”

8. Fitch Ratings Inc. January 30, 2019. “Fitch Downgrades Pemex IDRs to ‘BBB-‘; Outlook

negative.”

9. The U.S. Energy Information Administration. “Mexico Data Overview and Analysis.” Available

online at (https://www.eia.gov/beta/international/country.php?iso=MEX)

10. Mexico Daily News. February 15, 2019 “Government presents 107-billion-peso plan to reduce

Pemex’s debt burden.”

11. Reuters. Feb 15, 2019 “Mexico to Inject $3.6 billion in Pemex, seeks to prevent credit

downgrade.”

12. Financial Times. February 15, 2019 “Mexico Increases Tax Cuts for State Oil Group Pemex.”

13. The United Nations World Tourism Organization. September 13, 2018. “UNWTO Tourism

Highlights 2018 Edition”

14. INEGI Banco de Información Economica. Available online at

(https://www.inegi.org.mx/sistemas/bie/)

15. Reuters. February 21, 2018. “Mexicans abroad sent record $28.8 bln home in 2017”

16. Moody’s Corp. March 30, 2018. “Petroleos Mexicanos: Semiannual Update.”

17. CNBC. December 21, 2018. “Mexico’s Pemex to pay more taxes despite pledge to boost

company.”

18. Financial Times. February 12, 2019. “Doubts Grow Over Mexico’s Rescue Plan for Pemex.”

19. Financial Times. January 14, 2019. “Fuel crisis has `limited impact’ on Mexico’s credit rating for

now: Moody’s.”

20. Ramirez-Cendrero, Juan Manuel; Paz, Jose. November 2016. “Oil Fiscal Regimes and National

Oil Companies: A comparison between Pemex and Petrobras” Energy Policy.

21. Pemex. 2018. “Situación Financiera de Pemex (Consolidado) Periodo 2012-2018”. México DF.

22.Pemex. 2013. “Plan de Negocios 2014–2018”. México DF.

23. Pemex. 2015. “Anuario estadístico 2014. México DF.”

24. Pemex. 2017 "Pemex en Cifras." Available online at

(http://www.pemex.com/ri/herramientas/Documents/PEMEX_Factsheet_e.pdf)

25. WSJ. February 15, 2019 “Mexico Unveils Plan to Support State Oil Company Pemex

Page 12, ©2019 Advisor Perspectives, Inc. All rights reserved.© LM Capital Group

Page 13, ©2019 Advisor Perspectives, Inc. All rights reserved.You can also read