Pension Provider Report 2018 - Thomsons Online Benefits

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Thomsons Online Benefits Pension Provider Report 2018

Contents

Introduction 3

The future of financial wellness enhanced 4

by connectivity

A shrinking provider market 7

About this report 10

Mercer Workplace Savings 14

Aegon 16

Aviva 22

Legal & General 28

Royal London 33

Scottish Widows 36

Standard Life 43

Appendix 1: NMG – Broad market opinion 50

(adviser sentiment)

Appendix 2: High level statistics 50

Appendix 3: Thomsons Online Benefits service 52

statistics

Appendix 4: DarwinTM fund range 53

Appendix 5: Default fund performance 53

Appendix 6: Access to savings 54

Appendix 7: Quick comparison 54

2 | Pension Provider Report 2018

Introduction

Neil Atkinson

Head of Proposition

Welcome to the 2018 Pension Provider Report, our annual

review of the UK group pension provider market.

Typically, workplace pension provision is the largest benefit spend for our clients. With

this in mind, to ensure we deliver the best possible pension solution for our clients, we

are constantly evaluating the market on your behalf.

This report is the culmination of our client provider review activity throughout the

year and applies multiple objective data sources, coupled with our own operational

experience, to provide you with the best quality summary of how providers stack

up. Crucially, this report gives our readers an opportunity to understand our view on

provider propositions, their service quality and approach to technology. In addition,

we look into the rise of data analytics, the explosion of fintech companies offering

financial wellness solutions and the opportunities that technology and partnerships

present to deliver better financial outcomes for employers and their people.

Following our acquisition by Mercer in December 2016, it’s been a privilege to share

and collaborate with the wider team at Mercer to increase the value we bring to our

Thomsons consulting clients. As we look forward to summer and beyond, we’ll be

building out our suite of products and services. This includes developments in the

advised services space, deeper and more enhanced DarwinTM provider connectivity as

well as building out Darwin enhancements, particularly with our Retirement Planner,

where members can look forward to a consumer-grade member experience and a

new-and-improved investment risk modeller. Furthermore, we are in talks with a

host of new and exciting third party providers of financial wellness solutions to deliver

an updated proposition, ensuring that we enable our clients to deliver the very best

solutions for their people.

In the meantime, we hope you enjoy this year’s report! If you have any questions

or feedback please get in touch with your usual Thomsons contact or email us at

connect@thomsons.com.

One last thing, if you want to keep up-to-date with our latest articles, webinars,

podcasts and videos why not follow us on LinkedIn and Twitter?

Click here to follow us on LinkedIn

Click here to follow us on Twitter

Pension Provider Report 2018 | 3

The Future of Financial Wellness Enhanced by Connectivity Neil Atkinson Head of Proposition, Thomsons Online Benefits Technology underpins everything we do at Thomsons. That’s why adopting our award- winning software Darwin is a prerequisite to taking our pension governance consulting services. This is because we believe, and indeed can prove, that higher employee engagement and pension contribution rates are achieved through delivering workplace pensions through technology. If you’ve read our annual provider review before, you’ll know that the extent to which we can connect with pension providers to ensure an enhanced member experience impacts our overall assessment. It’s much the same with financial wellness. This section of the report aims to help you better understand the rapidly evolving financial wellness landscape; and hear how we’re engaging with the provider market to deliver great solutions to employees and help our clients boost their employee value proposition. We believe scalable digital solutions, delivered through Darwin, will ultimately help people make better financial decisions. Aside from salary, the amount employers spend on workplace pensions is likely to be their single largest benefit cost. Whilst we proudly evangelise the benefits of saving into a workplace pension, we also recognise that employee needs vary hugely, even within generational segments. More and more people are feeling more immediate financial stress as they aim to make ends meet month-to-month. This stress can also be put down to struggling to service expensive debt, not knowing how to save and reacting to the perceived complexities of their own financial situation with inaction. In today’s always-on society, it’s easy for people to put personal finances into the ‘do it later’ pile, rather than engaging with it and making positive decisions. In short, financial matters don’t really ‘come alive’ for most people. However, the market is reacting with a clutch of emerging providers, mostly in the fintech space, seeking to engage users with simple products, engaging interfaces, transparent charging structures and lean operating models. These providers tend to be agile and their propositions focused on customers’ self-serving. Big financial institutions are investing heavily and taking stakes in many of the emerging platforms such as Legal & General (L&G) and Salary Finance, Unum and Smarterly, Goldman Sachs and Neyber, and Aviva and Wealthify. Additionally, providers such as Aviva are taking this digital revolution very seriously in their own right, and bringing R&D in-house by setting up incubator-style entities staffed by industry outsiders and data scientists. Emergent new providers are on the whole, product-focused. Entrepreneurial in spirit; fintechs see a niche or specific customer need and then build a product around it. Product-led solutions work up to a point, and deliver value to customers where demand exists, or where it’s created by nudges, engagement or communications. There’s a role in the workplace for product hosting and provider introduction, but also just as much a role for engagement, education and promoting self-awareness to empower people to make better decisions. This is evidenced by point-solution providers expanding into financial education in order to round out their propositions. However, these bolt-on education modules are often seen as accompaniments to the main product and no matter how personalised, are premised on users seeking the information out, reading it and acting on it. 4 | Pension Provider Report 2018

Education and engagement is the mainstay of how employers communicate to their

people; and rightly so. Comms can be targeted, personalised, branded appropriately and

span different media. However, there’s a different way of looking at financial wellness

which has quietly been gaining traction over the last 5 or so years; account aggregation.

Our own Employee Benefits Watch 2018 research highlights how Millennials want

easier access to their benefits via SSO, integrating multiple provider platforms in a single

place, interacting via apps on mobile devices, and using interactive tools.

Aggregation gives users this experience and adoption is poised to accelerate in the wake

of the European Payment Service Directive (PSD2). For the sake of clarity, Open

Banking is the UK version of PSD2. The difference is that whereas PSD2 requires

banks to open up their data to third parties, Open Banking dictates that they do so in a

standard format.

Open Banking allows people to be more in control of their own financial information.

It stemmed from a UK government investigation which highlighted a lack of choice for

consumers and a lack of competition on the part of banks. Nine UK banks and building

societies are now required to make certain data accessible to other approved companies

in a standardised, straightforward and secure way, following explicit consent from the

consumer (although at the time of writing only four have released their API data). The

process is underpinned by a set of security protocols to ensure the safety of this data.

What this means in practice is an increasingly emergent set of fintech companies mining

this rich vein of data for the benefit of consumers.

Account aggregators are important because they’re not focused on individual product

needs, rather bringing together a customer’s entire financial position and net worth in

one place. They allow a user’s own banking data to be served directly to them within

the confines of an aggregator application, which is approved by the FCA if they’re

using Open Banking. So think forensic line-by-line details of all banking transactions

from multiple accounts. This can then split automatically into different spend areas and

give user’s a detailed position of what they spend their money on. Within a workplace

context, data on your workplace pension can be also be fed into these apps via standard

API technology from the benefit platform or provider.

The ‘so what’ is that detailed spending habits can be used to help individuals plan better,

save more, and highlight better financial decisions. The technology does the hard work

and the user sees everything in one place.

A central aggregator solution like this is a good place to start for financial wellness as the

model works on a subscription basis, so charging is transparent. Crucially, it is provider

agnostic and its central tenet is a user’s own highly specific financial circumstances and

not a provider imperative.

Are you wondering how a 10% pay rise will affect your financial life? Let the algorithm

model it for you. Are you wondering if you can replace the 10-year-old car on the drive

and keep saving at your current rate? Are you keen to cut down on monthly spending to

save for a wedding and know what the impact might be in 5 years’ time? See how much

you spend on your morning coffee or your broadband and get an idea of how much you

could save. Or how about this: The app knows your postcode, knows how much your

house is worth through Zoopla or Land Registry data, what your mortgage balance is and

monthly re-payments are, and knows you can get a better deal by re-broking.

The existing product-led nature of many solutions will reach a glass ceiling in terms of

uptake as they only address existing needs. Account aggregation will create demand

through actual personalisation, where consumers hold power over their own data and

are no longer restricted by large financial institutions using data advantage purely for

Pension Provider Report 2018 | 5

commercial benefit. This may in turn stimulate point-solution providers further once personalised needs are identified for saving, lending or protection. Aggregation is here, and has been for some time. But it’s Open Banking, PSD2 and the normalisation of personal data being shared, underpinned by proper security protocols, which will really shake the market up. These are some of the providers we are working with, or are currently in talks with, to provide our clients and their people with market-leading solutions through Darwin. 6 | Pension Provider Report 2018

A shrinking provider market

Kevin Brendling

Senior Pensions Technical Consultant, Thomsons Online Benefits

There is no doubt that the corporate pension provider market is shrinking; the

important question is why, and what does this mean for our clients and members?

It will come as no surprise that this question cannot be answered by a single response.

But, certainly some responsibility lies with the introduction of the charging cap.

Controversial? Perhaps, but the mandatory decrease from the existing 1% stakeholder

rules to 0.75% in 2015 was brought about largely by tabloid pressure, with pensions an

easy target for generating headlines.

Whilst there were of course some schemes applying excessive charges, most

contract-based schemes were already delivering low charges for members, due to

the introduction of the stakeholder cap in 2001. However, the new cap ushered in

a period of renewed competition and wafer-thin margins for providers, as it became

necessary to undercut the cap to win business.

Despite all the talk about delivering value and not driving down to the lowest cost

solution, the pressure for every scheme review to deliver a lower charge for members,

is perhaps causing more harm than good. After all, what was wrong with a 1% charge?

For those invested in a scheme default fund, that left 99% of the fund with no charge

applied and while a drop of 25 basis points would deliver some limited improvement to

member outcomes, it manifested a much more significant fall in income for providers

administering the products. The knock-on effect has arguably led to compromises in

other areas (e.g. default fund design).

Fast-forward a couple of years and we’ve lost the Friends Life and Zurich brands.

More recently, Standard Life has felt the need to outsource its administration of

workplace pensions to Phoenix. The danger now is that we end up with a smaller and

less competitive market, with providers overstretching to win business and having to

wait many years before they turn a profit - clearly this scenario presents some risks.

Phoenix itself is akin to a vacuum for failed pension providers and life companies. In

recent years the closed book provider has bought AXA Wealth, Royal & Sun Alliance,

Scottish Mutual and a host of other businesses.

Other key contributors to a shrinking market are the loss of annuity business (a

direct side-effect of the introduction of pension freedoms) and the low interest rate

environment that followed the 2008 financial crisis. Low interest rates, and more

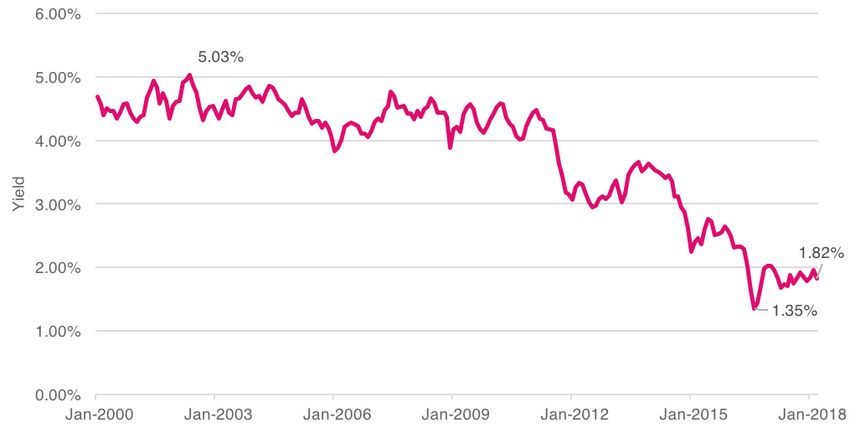

specifically quantitative easing, have led to lower yields on fixed interest assets. This

has made it more difficult for the insurance industry (which predominantly invests in

fixed interest assets – Fig 1) to cover its liabilities and annuity rates have also fallen as

a result.

In recent years, nine annuity providers have pulled out of the market (or merged

with others) and there now remains just six.1 The impact of these factors is a more

challenging environment for insurance companies, which also tend to be pension

providers.

1. https://corporate-adviser.com/annuity-market-shrinks-canada-life-buys-retirement-advantage/

Pension Provider Report 2018 | 7

It’s not clear whether these factors have driven insurers to change their business

strategy away from insurance to more sustainable approaches, or whether this would

have happened regardless - driven by technological change. However, it is clear that a

transition is in place:

• Aviva, the UK’s largest insurer is heavily investing in technology to become a

digital leader and it is successfully generating profit by hosting multiple products

(and multi-buy discounts) on its platform.

• Scottish Widows’ purchase of Zurich's UK pensions and savings business gives it

greater scale and better product diversification. This is part of a wider platform

plan for Lloyds Banking Group and its customers.

• The merger between Standard Life and Aberdeen again delivers scale, but the

deal with Phoenix allows it to offload a capital-intensive business, as it seeks to

become one of the largest asset managers.

Whilst all three of these major pension providers are changing and adapting to market

conditions in different ways, there is one primary goal – assets under management.

All are looking to establish the best ways to attract and retain more, and the great

accumulation tool is the platform. The end-game being a platform that delivers

multiple financial products in one place. Essentially, providers are looking to create

their own version of Darwin!

Figure 1: Asset allocation of UK insurers2

2. http://www.genre.com/knowledge/publications/iipc1611-en.html

8 | Pension Provider Report 2018

Figure 2: Reducing yields on long-dated gilts3

All are looking to establish

the best ways to attract and

retain more, and the great

accumulation tool is the

platform. The end-game

being a platform that delivers

multiple financial products

in one place. Essentially,

providers are looking to

create their own version of

Darwin!

3. Debt Management Office (DMO)

Pension Provider Report 2018 | 9About this report

Kevin Brendling

Senior Pensions Technical Consultant

Before delving into the main body of the report, which contains our analysis of each

provider on our panel, it would be beneficial to understand the member journey within

a scheme delivered through Darwin. This is important as it drives the metrics that we Most providers on our panel

review in this report. now offer contract-based

(GPP) and trust (Master

Darwin delivers an award-winning member experience for retirement savings, Trust) products. Legislative

including auto-enrolment assessment, retirement tools and a total reward outlook changes means that these

that enables members to view all of their benefits in one place. As a result, the pension products are now very

provider (usually a UK insurance company) acts primarily as an asset manager and similar, as are the terms

retirement income facilitator. offered by the providers.

Therefore, our review focuses on the key elements of responsibility for providers For the majority of our

within this symbiotic arrangement and includes the following: existing clients, our view

is that a GPP with our

• Background governance service, run

through Darwin, delivers the

• Proposition best overall solution.

• Connectivity to Darwin and service Whilst there will be scenarios

when a Master Trust is more

• Investment: Default options appropriate (and we do

consider both), this report

• Retirement journey focuses primarily on the

GPP market.

• Development potential

Background

You may be reading this report to gain more insight into the strengths and weaknesses

of your current provider or you may be considering whether to conduct a market

review. We therefore aim to provide you with some detailed background about the

provider’s past and relevant details about the direction of travel.

For example, there may have been some recent merger and acquisition activity, or

perhaps the prospect of changes in ownership. Such changes can be positive for

members, but can also be disruptive and unsettling.

Given that pension providers may also be part of a much larger global group, there

may also be some insights into the wider successes, or otherwise, of the group. A

notable example would be the release of financial results for 2017 or the outcomes of

an Investment Governance Committee (IGC) review.

Proposition

This section covers the core components of the provider’s product(s) – what it does

and how it compares to our view of what is required.

10 | Pension Provider Report 2018Most providers on our panel are now able to offer access to Group Personal Pensions

(GPPs), Group Self-Invested Personal Pensions (GSIPPs), Master Trusts and Own

Trusts. Following legislative changes, these products are broadly similar with regard to

the experience delivered to members, but our consulting team can advise clients on

the most suitable product to meet their needs.

One of the aims of providers in recent years has been to position themselves to be

able to offer this suite of products. Typically, as far as our panel is concerned, this has

been achieved by acquisition rather than the launch of new products. This is important

to note, as behind the scenes there is the need to achieve system integration and

some products have better reputations for service and connectivity than others.

Connectivity to Darwin and service

This of course is of critical importance, as better connectivity equals better member

experience. In addition, service levels are also heavily dependent upon a provider’s

technological capabilities and whilst some are excelling in this area, others are falling

behind in the development race.

The best providers deliver live fund value feeds into Darwin, along with notifications

of changes to member fund choice retirement ages. They will also deliver certain

governance data fields in a useable member format, rather than more simplistic

scheme-level brochures.

Furthermore, the best providers will deliver excellent relationship support, with fast

turnaround times, along with the highest attention to compliance, processes and best

practice.

Given that one of the providers’ key functions is to collect and invest the

contributions, the system capabilities for contribution uploads, new joiner uploads

and leaver notifications bears considerable scrutiny by our administration team. These

views are shared in detail within the appendices.

The majority of weighting in this category is applied from the views of our own

administration team, as this experience has the greatest impact on member

experience. However, in order to provide an element of balance to this view and to

ensure that we not overlook wider market considerations, we work with our trusted

partner, NMG Consulting.

NMG provides a specialist and global view on the asset management, wealth,

insurance and reinsurance markets. The application of proprietary research enables

NMG to produce considered opinions that are in turn used by financial institutions to

help shape strategy and influence change. For our purposes, the view of key metrics

across the pension industry are very valuable and some of these insights are shared in

the appendices.

Investment options

In our experience, typically around 90% of members invest in the scheme default

fund. Whilst details of the self-select range of each provider are included in the

appendices, our report focusses on the default investment options.

Pension Provider Report 2018 | 11The introduction of auto-enrolment in 2012, and ‘retirement freedoms’ legislation in 2015, initiated a reassessment of the best way forward for default fund solutions for Defined Contribution (DC) schemes. These levers for change were also accompanied by concerns over low annuity rates and the risks to members of investing in a heavy concentration of annuity-hedging long gilt assets, which had become very volatile, relative to long-term trends. These factors were addressed by a greater focus on multi-asset funds, as opposed to 100% equity or equity/bond mixes. These newer funds aimed to deliver greater diversification to help protect from significant equity market falls. All of the providers on our panel have now adopted these principles, which carry through into the pre- retirement and at-retirement phases. Typically the newer lifestyle profiles are termed flexible, drawdown or universal, although annuity-targeted options are still available for schemes that wish to use them. These lifestyles are now 3-5 years old and are now more comparable, due to a longer performance history. However, whilst some are true ‘multi-asset’ funds (e.g. Mercer Growth Fund, L&G MAF), others are less diversified than might be expected, investing primarily in equities with a small holding in bonds. This is especially the case in the growth phase, which to some extent is a reflection of market conditions. In recent years, certain bond assets have delivered remarkable returns, relative to their long-term trends, which has enabled greater diversification whilst still delivering double-digit returns. However, as interest rates start to creep up from the abnormal lows of recent years, bond returns have started to decline and we’re seeing some managers shift to an underweight positon in credit and an overweight position in equities. Whilst this is logical, it does make diversification more challenging, especially in the growth phase. Our analysis explores the pros and cons of each default solution, with a risk/return comparison provided in the appendices. Retirement journey When members reach the point of withdrawal, it is important that the provider can both facilitate their requirements and support the decision-making process. Since 2015, members have enjoyed much greater freedom in how they manage their income in retirement, but they also need to make a decision between taking an annuity or remaining invested whilst withdrawing an income. Not an easy choice, especially where advice is not readily available. Beyond this primary decision, lies the choice about how much income to draw and the very real concern about taking too much, too soon. In addition, not all providers will facilitate a direct withdrawal from the plan and members will be required to transfer out and navigate different charging structures and other restrictions. The best providers offer a lot of support, from concise case studies to online chat and full telephone support. In addition, some will enable members to retain their scheme annual management charge (AMC), will apply no additional charges or restrictions and will allow the whole process to be transacted online. 12 | Pension Provider Report 2018

Some will insist on a transfer into a separate product. This can be viewed as a

disadvantage, given the need to endure a transfer process and the application of a

different charging structure (often a sliding-scale based on the value of the assets

held). However, on the other side of the coin, members gain access to a specialist

income withdrawal product, with complementary investment options. Furthermore,

from a governance perspective (assuming a member transfers all their assets into the

new plan), the employer is relieved of responsibility.

Where the average age of a scheme is relatively high, there is plenty of food for

thought under this category.

Development potential

In essence, a strong financial position delivers the ability for a provider to invest in

its proposition, increase scale and ultimately increase assets under management. In

principle, this should also deliver a better member experience, providing that market

competition is not constrained by the emergence of a small number of supersized

participants.

A strong financial position should also mean that a provider makes strategic

acquisitions, rather than being acquired. Whilst of course this is not a given, it can be

an indicator of future stability.

Alongside our own industry experience, we apply input from world-renowned credit

ratings agency Moody’s. Whilst Moody’s produces financial strength ratings, the key

information is delivered within its published research, which includes influential metrics

such as distribution and diversification strengths, credit strengths and weakness,

product strengths and weaknesses, potential for cash generation and risks to ratings.

Within this section, we share our view on the market and each provider’s development

potential.

Star rating and Thomsons Online Benefits (Thomsons)

comment

We purposely do not rank our panel of providers, as we value the specific needs of

each of our clients and some providers will be a perfect fit for some and not for others.

However, we also recognise the value of delivering some form of assessment and the

need to identify areas for improvement. To this end, each provider section contains a

star rating (out of five) on the first page.

Finally, we share our summary view under Thomsons comment, which really is our ‘if

you read nothing else, read this.’

Pension Provider Report 2018 | 13Mercer workplace savings

Neil Atkinson

Head of Pensions, Thomsons Online Benefits

Within the larger corporate DC space, master trusts have steadily been gathering

momentum, indeed our 2017 Provider Report drew attention to their rise in

prominence and the subsequent Royal Assent of the Pension Schemes Bill cemented A key point of differentiation

their place in the future of DC. for MWS is the investment

management. This differs

As Thomsons Online Benefits is now part of the Mercer group our clients have access from more traditional

to a range of services including Mercer Workplace Savings (MWS) and the Mercer provider selection exercises

Master Trust. where the investment

proposition is embedded

As highlighted in the previous section of this report, most Thomsons consulting within the provider, with

clients use a contract-based governance structure and are satisfied with this set-up. clients typically adopting off-

However, trust clients seeking to outsource governance may well wish to consider the the-shelf default funds.

Mercer Master Trust.

Launched in 2011 and now with more than £10bn under management, the MWS

proposition provides an end-to-end workplace pension and savings solution which

covers provider selection, investment solutions and governance, operational

governance and a retirement income service.

MWS utilises a select panel of market-leading providers which is reviewed periodically,

a process which Thomsons pension specialists have recently been part of. On a client-

by-client basis, a detailed selection project is undertaken to ensure their needs are

adequately met by the most suitable provider. This ‘best of breed’ approach provides

choice and competition between market-leading administration providers for the

benefit of clients and their people.

The panel members are governed by strict contractual service level agreements

(SLAs), which carry pre-agreed financial penalties payable to employers for non-

compliance; these SLAs are monitored by Mercer on a monthly and quarterly basis.

This structure promotes operational excellence for all participating employers and

their members.

A key point of differentiation for MWS is the investment management. This differs

from more traditional provider selection exercises where the investment proposition

is embedded within the provider, with clients typically adopting off-the-shelf default

funds. With MWS, clients buy into Mercer’s best investment thinking called Mercer

SmartPath™, with the proprietary fund constructs plugging into any of the three

panel-providers’ platforms.

The Mercer SmartPath™ framework delivers an investment strategy for each of the

three at-retirement options of cash, drawdown or annuity. This open architecture

approach utilises the asset allocation and fund selection of Mercer’s global manager

research expertise. The Mercer Growth Fund, the fund used within the growth phase

of the lifestyle strategies, has produced average returns of 7.8% p.a. (gross of fees)

over the three years to 31st March 2018 and has delivered competitive risk-adjusted

returns relative to its competitors.

14 | Pension Provider Report 2018Mercer

At the end of a member’s career the Retirement Income Service provides integrated,

personalised support for retirees, giving them the ability to confidently take decisions

and act on them. The service has been designed to work with retirees by offering a

comprehensive range of services, including education and learning through online

capabilities and telephone support, plus a suite of advised services.

MWS is a packaged DC-trust solution and as our integration with Mercer deepens

we continue to build greater connectivity between the MWS panel providers, and

the Darwin platform. In doing so we can deliver all the great member experience

and employer governance familiar to our own group personal pension (GPP) clients,

backed up by a market-leading master trust and Mercer’s own investment solution.

Pension Provider Report 2018 | 15Aegon

Kevin Brendling

Senior Pensions Technical Consultant

Background

There is no doubting the ambition of Aegon to be a dominant force in the UK

pensions market, but there’s also the sense that it doesn’t always know how it wants to

achieve this. In recent years Aegon has introduced its At Retirement Choices (ARC)

platform, which is essentially a GSIPP with ISA and General Investment Account

bolted on. Tagged onto this was RetireReady – a genuine differentiator. Key Points

RetireReady is a more innovative product that seeks to help pension members • Aegon identified as one

understand their choices when it comes to readiness for retirement and to understand of nine systemically

their access to savings. Members are led through a number of questions and important global

presented with a score that gives them a measure of how prepared they are for their insurers, with AUM of

desired retirement lifestyle. €318bn.

This is a great retirement tool, but its future appears under threat with Aegon • ARC is a platform

announcing a review. Why? Well, apparently this product may not fit with Aegon’s leader in the UK.

strategy which now appears to have returned to a reliance on intermediaries, as However, the GPP

opposed to seeking customers via more direct routes. systems and service

do not measure up to

Cue puzzled expression! When ARC was launched, there was the feeling that peers.

intermediaries were very much not what Aegon was looking for, to the extent that

ARC was certainly not built with an outward-looking agenda. To explain, ARC has • Plenty of potential,

been built in quite a rigid way, which makes it difficult to relate to third-party software but the short-term

and third-party requirements. One such example has been the unwillingness to supply challenge will be to

data to the advisers of members, which has left members in no man’s land. retain its GPP schemes.

However, it seems that Aegon has made something of a U-turn, which is welcome

news. Furthermore, the acquisition of Cofund’s investment platform (£77bn of assets)

and BlackRock’s Compass platform (£12bn of assets) has given Aegon a broader suite

of products to go to market with.

Proposition

Aegon offers the four primary group pension products, with the majority of members

(957,000) using its GPP and Trust products:

• ARC (Platform, predominantly used for its GSIPP)

• GPP (Group Personal Pension)

• Compass (Platform, offering GPP, Trust, Master Trust)

To date, our experiences with ARC have been mixed. From a member perspective,

it’s modern user interface (UI) and digital capabilities are a definite plus but from a

governance perspective it has been more challenging, as ARC was built as a direct-to-

customer platform. However, the governance reporting aspects have improved over

time, and member-level data is now downloadable in a more useable format (whilst

static scheme-level only reports, remain the default option under the GPP).

16 | Pension Provider Report 2018Aegon

For the non-typical pension member that requires a large range of funds, ARC scores

highly for volume. There are around 4,800 investment choices available and the

site is reasonably easy to navigate, delivering 20 metrics in one view. These include

independent performance ratings, full charging detail, yields and dealing times. ARC

could certainly not be accused of withholding details, but then again there is a lot of

information to view on one screen and when scrolling down the titles disappear!

The GPP is our most heavily used Aegon product and (as we have reported in the

past) it feels like a product that is being overshadowed by ARC. A bit harsh? Maybe,

but the GPP continues to be the product on our panel that we experience the most

issues with and, whilst we have been assured that the GPP is not a dead product and

continues to be invested in, it appears to only receive minor upgrades.

For example, until last year members could only take a single withdrawal from their

plan. In 2018 members can now take two withdrawals, but on ARC it is possible to

utilise monthly drawdown. The feeling (and this is pure speculation) is that it would be

too big a job to migrate all schemes from the GPP product to ARC and therefore the

GPP must be kept on a pacemaker until this becomes a feasible option.

At present we do not have any schemes with the Compass products and therefore

cannot comment on these. However, we are interested to see what Compass can

offer, relative to the GPP, and look forward to seeing how this will work when Aegon

completes the new front end that will serve both ARC and Compass.

One final point to be made concerning Aegon’s proposition is the disappointing

news that the Secured Retirement Income (SRI) option has been removed (from

1st March). SRI was an innovative attempt to bridge the gap between drawdown

and annuity and offered savers a guaranteed minimum level of retirement income,

regardless of whether the original investment ran out.

Unsurprisingly this guarantee came at extra cost, but one which many were prepared

to pay with £1bn of sales since launch three years ago. The removal of the SRI

coincides with the sale of Aegon Ireland (which sold the guaranteed products) to

AGER Bermuda. Aegon has said that it may resurrect SRI if perceived demand

increases in future. We hope that it will, or that another provider may step in to

provide better flexibility for members.

Connectivity to Darwin and service/administration

We have a good level of connectivity between Aegon and Darwin for the GPP. This

includes the update of fund values, but Aegon does not provide updates on changes

to fund choices and retirement ages. Whilst the majority of members (c. 90%) invest

in the scheme default fund, and retirement ages are not regularly changed, the

responsibility falls upon Aegon members to update their information on Darwin and

the member experience can clearly be improved here.

Alternatively, as providers continue to embrace single sign-on (SSO) capability,

members will be able to seamlessly access the provider site for these elements.

However, whilst Aegon is developing SSO to enable ARC to connect to third party

portals, this project is currently on hold and connectivity to ARC remains very limited.

On the servicing side, there is room for improvement and with a renewed focus on

Pension Provider Report 2018 | 17Aegon the intermediary market it will be interesting to see whether this filters through to the GPP side. Our impression is that the back-office systems are buckling under sustained pressure and timescales for the supply of governance data are fund updates among other things are routinely missed. This view is backed by NMG’s summary of the market, where Aegon received the lowest score on our panel for operations. There have been two notable issues over the last couple of years, where contributions have not been applied on time and where fund charge rebates have not been applied, despite sitting in Aegon’s bank account. This raises some important questions about the provider’s compliance capabilities and processes, and why these issues were left undetected. Having said this, Aegon have quickly put the most recent matter right and our new Aegon Client Service Manager has been proactive in bringing the right people together to deliver a resolution. This action has restored some confidence in the provider’s ability to deliver a good level of service but we will need to see sustained action on this front before full confidence is restored. Investment: default options The relationship between Aegon and BlackRock is a long-standing one, with the asset manager supplying Aegon’s internal fund range. It is no surprise then that Aegon’s Workplace Target fund range (default options) are predominantly invested in passive BlackRock funds. Being the world’s largest asset manager provides BlackRock with tremendous opportunities to deliver economies of scale, hence the low-cost of its passive range, which makes it a go-to manager for default funds. However, the issue of historic pricing with these funds (which results in a time- lag between the fund and its benchmark) remains a source of consternation and ultimately this can be misleading for governance committees and members alike. The Workplace Targets are simplistic instruments (and merely a rebrand of many existing options), but they do offer choice and are neatly arranged into risk-rated, retirement-targeted solutions with the option to apply active management and ethical iterations where required. Alternatively, the default-default, so to speak, is the Aegon Default Equity and Bond Lifestyle Fund. Where an average-risk, multi-manager and flexible retirement option is required, Aegon offers its Universal Balanced Collection (Flexible Target). This option initially invests in the UBC, a fund which in the past has borne scrutiny over its performance, which has lagged behind the competition. However, the fund performed more in-line with its peers in 2017. Beyond this multi-manager option, the majority of which is still passively managed via the underlying Balanced Passive fund, there is nothing especially ground-breaking – nothing to push the boundaries of an evolving investment market. The Workplace Target range continues to feel like a low-cost solution, rather than a high-value approach. When other providers can offer active fund management (not that this is necessarily 18 | Pension Provider Report 2018

Aegon

better) at no extra cost, funds that track non-market cap weighted indices, ESG

options and investment into futures contracts, the Aegon cupboard looks a little light

on inspiration.

A further frustration with the Workplace Targets range is the de-risking phase, which

predominantly relies upon Aegon’s target-dated Multi-Asset Fund (MAF). Whilst

we support the use of a multi-asset approach as members approach retirement, this

is essentially quite a traditional equity/bond fund with a long-term strategic asset

allocation. Again, it seems that cost may be the key factor driving decisions.

There are two matters of concern here, the first being that the asset allocation does

not appear to undergo any formal review, or at least if it does this is not published via

the IGC or other channels. The second issue is the lack of transparency. Aegon’s view

is that this is an ‘internal fund’ and therefore it does not publish factsheets for the fund

and does not provide a benchmark for performance, or indeed any coverage within the

IGC report.

Our view is that a default investment approach should be clear about its aims and

objectives (as per the Department of Work and Pensions - DWP - guidelines) and

that members, along with scheme advisers, should have barrier-free access to the

performance of this fund. We have asked Aegon to review its position on this matter

and would hope to see this quickly addressed.

Our hope is that greater scale, and the need to re-engage with intermediaries, may

help to drive change and deliver a stronger default investment range.

Retirement journey

When members are ready to start accessing their retirement pot, they are directed

to the RetireReady site. This provides some excellent tools for members, which can

help them plan for retirement. This includes features such as the retirement needs

calculator, which enables members to assign monthly values to treats, restaurants

and holidays. In addition, the retirement planner enables members to model different

methods of drawing an income.

The site benefits from Aegon’s investment in digital and provides members with an

informative and engaging online experience. Furthermore, if additional help is required

or members just wish to speak to someone, they can contact Aegon Assist.

With regard to actually making withdrawals, this has to be transacted via the product

invested in and it is far better for members to be on the ARC platform, as opposed to

the GPP.

Under ARC, members can set-up full drawdown functionality, take ad-hoc lump sums

or seek to purchase an annuity. However, it should be noted that Drawdown access

is charged at £75pa and whilst this is not unusual, other providers on our panel do not

charge for this.

Under the GPP, however, members can only make two partial withdrawals per year,

which could hardly be termed ‘embracing pension freedoms.’ This is symptomatic

of trying to make an old product learn new tricks and it is clear that Aegon are

constrained here.

Pension Provider Report 2018 | 19Aegon Development potential Aegon has made two notable acquisitions in recent years, with the addition of the Cofunds and BlackRock platforms. These purchases have bolstered Aegon’s member numbers, but also its assets under management and suite of products. Given that Chief Executive, Adrian Grice, is billing Aegon as a back-book platform consolidator, further purchases are likely to follow. However, it seems unlikely that anything on a similar scale will happen anytime soon (given the disruption this would cause) and Aegon is already incurring considerable costs as it works to integrate the Cofunds and BlackRock Compass platforms. These costs were recently reported to be around £94m4 and Aegon is apparently in talks with Fintech company (FNZ) about the Cofunds integration. FNZ appears to be winning a lot of platforming business at present, but there are concerns that it may be over-stretching itself in the process. In our experience, these platforms also tend to be a little less flexible than others (e.g. with regard to the refund of contributions in the first month opt-out window and the management of fund options), although it is not clear how much of this is driven by the provider. The plan is to deliver a new front end for both ARC and Compass and presumably some retirement tools to replace what is offered under RetireReady. We would hope to see some form of enhanced RetireReady solution applied and look forward to seeing what Aegon delivers. Digital development costs are rumoured to be around £20m for this year and this may seem small in comparison to what other providers are investing. However, given that Aegon already has a digital solution in place, it could be argued that it doesn’t need to match the spending of some of its peers. Having said this, the GPP would benefit from such much-needed investment to improve functionality, although this seems unlikely to transpire on any significant scale. Furthermore, the restructuring costs that Aegon is currently absorbing will of course constrain the potential for investment in this product. Aegon’s financial position is a little more arduous to comprehend than with some of its rivals, given that it is a Dutch company with a UK operation. Moody’s awarded an A3 long-term issuer rating to the Aegon Group (Aegon N.V.) in 2009 and this level has been maintained, which is a couple of notches lower than some of the other providers on our panel. However, its rating outlook was changed from negative to stable in December 2017, in recognition of its good level of geographic diversification and the successful offset of lost earnings, following the sale of its annuity business in 2016. This action coincides with Moody’s wider view that economic growth, financial stability and underwriting discipline are offsetting the challenges of the low interest rate environment for the European insurance industry. Moody’s also notes that the G20 Financial Stability Board has identified Aegon as one of nine systemically important global insurers, which reflects the overall scale of the group (€318bn AUM at 31.12.17). This should enable it to stand on its own two feet and in time to increase its profitability.5 4. https://corporate-adviser.com/annuity-market-shrinks-canada-life-buys-retirement-advantage/ 5. http://www.genre.com/knowledge/publications/iipc1611-en.html 20 | Pension Provider Report 2018

Aegon

The ability of Aegon UK to increase its profitability and to continue to invest in its

products, will depend on its success in growing its platform and increasing assets

under management. The BlackRock and Cofunds acquisitions increased assests under

management (AUM) from £9bn in Q2 2016 to over £100bn and Moody’s asserts

that Aegon has been the leader in the UK platform segment. The Edinburgh based

platform will be keen to maintain this position and further increase its AUM, but

the challenge will be to complete this integration whilst maintaining a high level of

customer service. It is this aspect that has come under scrutiny in recent years.

TOB comment

So, as a pension provider, Aegon is a bit of a mixed bag at present. On one hand, the

GPP product has seen better days and some of the compliance-related issues are of

significant concern. The alternative is ARC and this certainly provides a better user

experience in some areas, but most schemes are still on the GPP and cannot simply

be lifted and dropped onto ARC. Instead a formal transfer process would be required

and at present ARC does not have contract-enquiry and therefore cannot connect

with Darwin.

The next wave of connectivity software (APIs) could solve this problem and Aegon

may pull something out of the bag to replace RetireReady. However, the development

spend for now will clearly be focussed on integrating Compass and Cofunds.

There is plenty of potential here, but at present it looks to be a wait and see for Aegon.

In the meantime, the biggest challenge will be to try and retain its GPP schemes, by

moving these onto ARC.

Pension Provider Report 2018 | 21Aviva

Kevin Brendling

Senior Pensions Technical Consultant

Background

There’s a tangible buzz around Aviva at present. Driven forwards by CEO Mark

Wilson, Aviva is becoming increasingly profitable and is fast transitioning from a UK-

based insurance company to a global fintech.

This embracing of all things digital, is setting it apart from the competition and the

commitment to deliver customer service rated in the top 10 for UK businesses is an

incredibly positive ambition.

The ‘99 in 3’ plan is a prime example of this intent. In principle, Aviva aims to Key Points

deliver 99% of customer requests in no more than three days from start to finish.

Furthermore, this commitment would not allow the clock to be stopped to make this • Early investment in

target easier. digital and data analytics

is reaping rewards for

‘Ask it never’ is another bold concept that demonstrates Aviva is not paying lip- Aviva, with exciting

service to customer experience, but instead is applying data analytics to revolutionise enhancements to

experience. As the television ads demonstrate, customers are no longer being member experience due

burdened with the need to supply intricate or difficult-to-locate details, when Aviva throughout 2018.

can obtain this from official sources. Where such details can only be provided by the

customer, Aviva will only request the information once and this will be available at • Renewed commitment

renewal stage and for additional product purchases. to digital spend -

£100m-pa.

It is this application of data science that is driving change and Aviva appears to

be leading the pack here. Data aggregation presents the opportunity to better • Robust GPP product,

understand customers’ needs and having started this process early, it now has all of its superior connectivity

data (including legacy products) in one place. This enables the provider to drill down to to Darwin, excellent

a much more granular level and to better personalise member experience. service and support.

The decision to ring fence the digital part of the business and to create a non- • Plans to deliver market-

insurance culture, attracting the right people, is now reaping rewards. Furthermore, leading personalised

Aviva is demonstrating the value of ‘platform’ by employing a multi-discount strategy. default fund.

This approach assisted in driving up new business values in 2017 (+25%), which is

generating cash for greater investment in digital.

In a fast-shrinking market, it is vitally important that providers can attract and retain

assets. Those that manage this successfully can then apply more favourable economies

of scale and deliver higher levels of investment into their propositions. Ultimately, this

should equate to better member experience.

Of course, while this all sounds great, Aviva still has to deliver on its ambitious

targets and must do so consistently. However, if successful, this provider could really

dominate the GPP market in the UK for years to come!

22 | Pension Provider Report 2018Aviva

Proposition

Aviva continues to offer a Master Trust and three contract-based products:

• Designer (GPP)

• NGP (GPP)

• MyMoney (GSIPP)

Whilst a Master Trust will be a suitable product for some (e.g. when coming from

a historically trust-based environment), the majority of our clients have been best

served by contract-based products. However, given that there is now little tangible

difference between Master Trust and GPP, and charges are broadly similar, there is

more scope to utilise Master Trust, where appropriate

For now, our focus remains on contract and the Designer and NGP products, which

are primarily designed to accommodate medium sized schemes (500 to 1,000

members) with a heavy reliance upon the default investment strategy.

In contrast, MyMoney is designed to accommodate larger schemes, where a

significant proportion of members are likely to require access to a wider range of

investment options, requiring the functionality to make regular trades. This product

sits on the FNZ platform, which is less flexible in its connectivity with Darwin, relative

to some other platforms. However, we do have SSO with MyMoney, which provides

a seamless transition from Darwin to the product, and this feature enhances member

experience.

All three products are accessible through the MyAviva app, which in itself is a strong

part of the overall proposition, unrivalled by the other providers on our panel. With

fingerprint login already in use, and facial recognition technology recently introduced,

upgrades to functionality are now coming thick and fast.

Whilst it was initially expected that NGP would migrate to Designer, it is intended

that the three products will continue to operate on a stand-alone basis. This decision

is officially based upon the view that each has its own merits and where Designer and

MyMoney are concerned, we would agree.

However, in our experience, Designer GPP is a stronger product than NGP and

offers a wider and arguably better fund range, along with more sophisticated default

investment options. This view is backed by NMG, as the NGP product consistently

generates lower market feedback scores.

The suspicion is that migrating NGP to Designer would be a considerable project and

one that Aviva may not wish to undertake at present. Having said this, the good news

for NGP members (and indeed MyMoney members) is that the default fund (the

MyFuture Investment Programme) will be undergoing a much-needed makeover.

MyFuture is a relatively simple, and low-cost default investment solution that relies

on a number of underlying BlackRock passive funds. In contrast to the Future Focus

options available through Designer, it is less sophisticated, less diversified and more

constrained in its asset allocation.

This is no great surprise, given that Future Focus is managed by Aviva Investors and

the refresh of MyFuture will be a welcomed result for ex-Friends Life members.

Pension Provider Report 2018 | 23Aviva Since our last review, Aviva has introduced integrated drawdown to both Designer and NGP, which allows members to withdraw directly from their plan. This is good news and brings both products in-line with MyMoney, which already delivered this access. One aspect that we have been asking Aviva to improve upon is the retirement journey for members. Currently this works on a paper-based process, which is out of kilter with Aviva’s commitment to digital. It also slows the timescales for members to acquire their money, as they must wait for the pack to arrive, complete the paperwork and return it for processing. Thankfully, Aviva has now created an online journey, which includes an interactive online retirement pack, with all the options available to select online. This is due for release in Q2/Q3. Service/administration and connectivity to Darwin Whilst much of the technological advances are still to filter through, our experience of Aviva continues to be excellent for the Aviva Designer GPP product and we anticipate greater parity with NGP and MyMoney in future. We have full connectivity between Aviva and Darwin on Designer GPP, and via SSO with MyMoney, and have an excellent working relationship with Aviva. The Aviva team are supportive, proactive and deliver to a consistently high standard. Furthermore, the Designer GPP is a very robust product and the software and processes for managing our clients’ monthly submissions are dependable. Essentially members can use Darwin to understand their pension scheme, change contributions and model their retirement income. Later this year, it is anticipated that they will then be able to SSO into MyAviva and into the relevant product to make fund switches. Beneath each product sits Appian, a US-based low-code platform that operates as a workflow system. This allows Aviva flexibility in how it delivers customer service, as it maps tasks to the correctly skilled person whether the enquiry is generated by phone or email. It is also important to note (as with some other providers) that call centre staff are not pressured to complete phone calls within a certain time, with the focus firmly placed upon first time resolution. As highlighted earlier, Aviva is taking this commitment to customer service one important step further, with ‘ask it never.’ A prime example of this is in the case of death claims, where the executor of a will is required to provide a death certificate to many organisations simultaneously. Aviva have linked up to the death certificate register and therefore no longer need to ask for this (for fund values under £50,000). It is no surprise then that NMG’s survey of market opinions shows a significant improvement in sentiment towards Aviva, with scores up in every category, relative to last year. Furthermore, of the providers connected to Darwin, Aviva’s Designer GPP is rated highest in three of the four core categories. This view is mirrored by our colleagues, who have also reported that Aviva’s processing of individual pension policies is extremely proficient. 24 | Pension Provider Report 2018

You can also read