Portfolio and Market Review 1st Quarter 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Portfolio and Market Review

1st Quarter 2021

1 Oak Court, North Leigh Business Park, Nursery Road, North Leigh, Oxfordshire OX29 6SW

T: 01865 208000 | E: info@mathewscomfort.co.uk | www.mathewscomfort.co.uk

FIN A NCIA L

Mathews Comfort Financial Services Ltd, Authorised and Regulated by the Financial Conduct Authority, PL A NN I NG

Company Registration Number 2187209, Registered in England and Wales.

Index funds DO care about ESG

When powerful vested interests feel threatened by inconvenient evidence they often respond in the same

way. Instead of challenging it head-on with counter-evidence of their own, they seek to undermine it by

spreading and perpetuating myths.

The tobacco industry spent billions obscuring the facts of the health effects of smoking over several

decades. The fossil fuel industry responded in the same way to growing evidence of climate change.

Existential Crisis

Today, active fund management is facing a similarly existential crisis as a result of the rise of passive

investing, which helps to explain the steady stream of myths we read about index funds. We are told, for

example, that indexing makes markets unstable, that it threatens market efficiency and even capitalism itself

— none of which is true.

Another myth doing the rounds in recent years is the notion put forward in an open -editorial in the Wall

Street Journal in June 2017, that passive investors don’t care about corporate governance. Indexers,

the argument goes, are only interested in financial returns, and managers of index funds have little or no

incentive to hold company boards to account on issues like excessive corporate pay, staff welfare, social

justice and the environment.

But is it true? Once again, there’s another side of the story which we rarely hear.

Stronger Incentive

Think about it: index funds should, in theory, have a stronger incentive to monitor the firms in their portfolios

than active managers, who can simply sell out of their positions if they disagree with management. Index

funds, by definition, are in it for the long term. If the company’s stock is on the underlying index, they have

no choice but to engage with the board. It is, moreover, in their interests to do so in order to compete with

active funds that have discretion over their holdings.

But what about in practice? Do index funds challenge company boards on ESG issues? There have been

several academic studies on this subject over the years, and most show that managers of passive funds are

just as likely as their active counterparts to hold boards to account — if not more so.

F I N A N C I A L PL A N N I N G

Academic Studies

In a 2016 study called Passive Investors, Not Passive Owners, Ian Appel, Todd Gormley and Donald Keim

found that index ownership at a firm is associated with more independent directors, the removal of takeover

defences and more equal voting rights.

The same authors revisited the subject with another paper, published in 2018. In it they established a

link between increased index ownership and greater use of proxy fights by activists, as well as a higher

likelihood that an activist obtains representation on the board of the target firm.

In March 2020, Joseph Farizo from the University of Richmond in Virginia published an in-depth study

on the voting records of both passive and active funds. Farizo concluded that the evidence “dispels the

concern that index funds, at least in the aggregate, completely disregard voting responsibilities by either

always siding with management”.

Passive Funds Have More Clout

In October 2020, the Faculty of Law at the University of Oxford published a paper by Adrian Aycum Corum

from Cornell University and Andrey and Nadya Malenko from the University of Michigan called Corporate

Governance in the Presence of Active and Passive Delegated Investment. Although the findings were

less clear-cut than those of the other papers mentioned here, they nevertheless dispelled the idea that

passive funds are bad for governance simply because their fees are lower, leading to smaller budgets for

governance oversight.

The authors wrote:

“While passive fund growth indeed decreases fund fees, it may nevertheless be beneficial for governance.

The reason is that fund fees do not decrease in isolation: lower fees are accompanied by higher AUM,

allowing funds to take larger stakes in their portfolio companies. These larger stakes, in turn, give funds

stronger incentives to engage.”

In other words, the growth of indexing has given passive managers more clout when it comes to ESG, and

we are pleased to see providers such as Vanguard, beefing improving up their ESG resources in Europe

and the US.

Conclusion

In summary, the claim that index funds present a danger to governance because they adopt a hands-off

approach, allowing management to act as it wants to, is another myth created by the fund industry. It wants

and needs investors to believe it, but it simply isn’t true.

Index funds care just as much about ESG as active funds do, and arguably more so.

F I N A N C I A L PL A N N I N G

Asset Class Return

After numerous lockdowns and false starts in 2020, the widespread rollout of the COVID-19 vaccine has

given real hope that economies will soon be able to fully re-open. The International Monetary Fund (IMF)

revised its projections of world economic growth in 2021 up to 6%, an increase of 0.5% from its predictions

in January. This is the fastest rate of global economic growth since 1980 and is in stark contrast to the

reduction in global output of 3.3% in 2020, the worst since the Great Depression.1

Figure 1 – Asset Class Performance (GBP Returns)

2

Source: FE Fundinfo (2021)

1

IMF (2021)

2

Global Bonds: Bloomberg Barclays Global Aggregate, UK Gov Bond: Bloomberg Barclays Global Aggregate UK Government

Float Adjusted, UK Equities: FTSE All Share, Global Property: FTSE EPRA Nareit Global, Emerging Markets Equity: MSCI

Emerging Markets, EU Equities (ex-UK): MSCI Europe ex UK, Japanese Equities: MSCI Japan, US Equities: MSCI USA, Global

Value Equities: MSCI World Small Value, Global Equities: FTSE Global All Cap, UK Inflation (RPI): UK Retail Price Index. F I N A N C I A L PL A N N I N G

As in the previous quarter, the change of leadership in Washington was a dominant theme. Once

inaugurated, President Biden wasted no time in announcing the American Rescue Plan, a $1.9 trillion

stimulus package. This was signed into law in March. Shortly afterwards, the President announced his

intention to spend an additional $2 trillion to rejuvenate the USA’s infrastructure via the American Jobs

Plan. US equity markets, as to be expected, reacted favourably and the S&P 500 increased by 7.4% over

the quarter. With this additional support and increasingly positive outlook for the US economy, the IMF

3

amended its predictions of US economic growth from 5.1% to 6.4% for 2021.

China together with the USA are seen to be driving the global recovery. China was the first country to

encounter the virus, first to shut down and the first to re-open. The Chinese economy is expected to grow by

4

8.4% this year despite the continuing trade war with the USA. For another quarter, China again failed to fulfil

its commitments to increase imports of US goods, as outlined in the “Phase One” agreement signed back in

January 2020. There were hopes that changes in the Whitehouse would result in a more cordial relationship

between the two nations. However, the first call between President Biden and his Chinese counterpart Xi

Jinping in February were reported to be tense. Later in March, angry exchanges between the two nations

during high level talks played out in front of the world’s media. As the quarter drew to a close the US

reaffirmed its position that it had no immediate plans to lift tariffs introduced but did express a willingness to

engage in further trade talks.

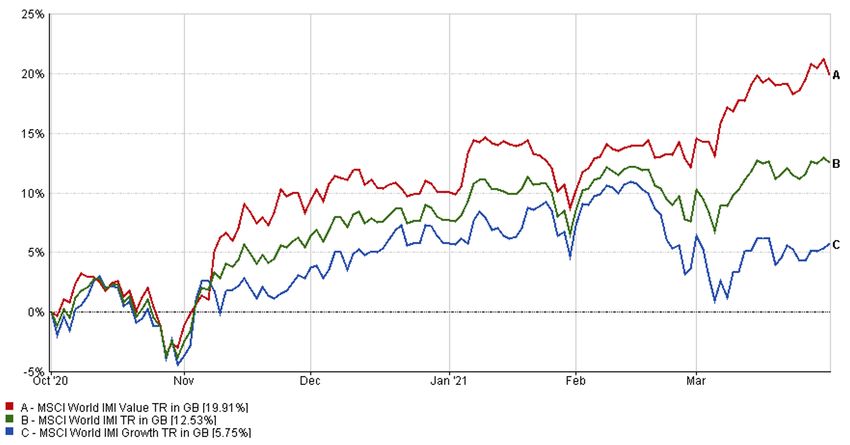

The first quarter of 2021 saw a continued resurgence in value stocks, giving further hope to long embattled

value investors that the initial upswing in value stocks observed in the last quarter of 2020 was here to stay.

Value investing is a strategy whereby investors seek to identify stocks that are currently undervalued by the

market. The intention is to buy these “cheap”, value stocks and profit from their eventual increase in price.

The opposite strategy is that of growth investing, whereby investors attempt to identify firms whose revenue

and earnings will grow faster than the market average.

Figure 2

Source: FE Fundinfo (2021)

3

IMF (2021)

4

IMF (2021) F I N A N C I A L PL A N N I N G

During 2020, with the assistance of governments and central banks, equity markets rebounded quickly.

However, the disparity between the performance of value and growth stocks initially only increased. This

was because of the disproportionate impact that lockdowns had on value stocks, which tend to be more

cyclical in nature, for example energy, retail, and transport. Growth stocks were more resilient, and some for

example, technology stocks, even benefited from the restrictions.

In the last quarter of 2020, investors’ expectations began to change. With the approval of a number of

COVID-19 vaccines together with President-elect Biden’s plan to spend trillion of dollars to revive the US

economy once in office, the prospect of an economic recovery looked promising. Cyclical stocks looked

to benefit more from the developments and hence value stocks began to rise. As 2021 began, the vaccine

rollout globally gathered pace and further US stimulus plans were announced, sustaining the value rally.

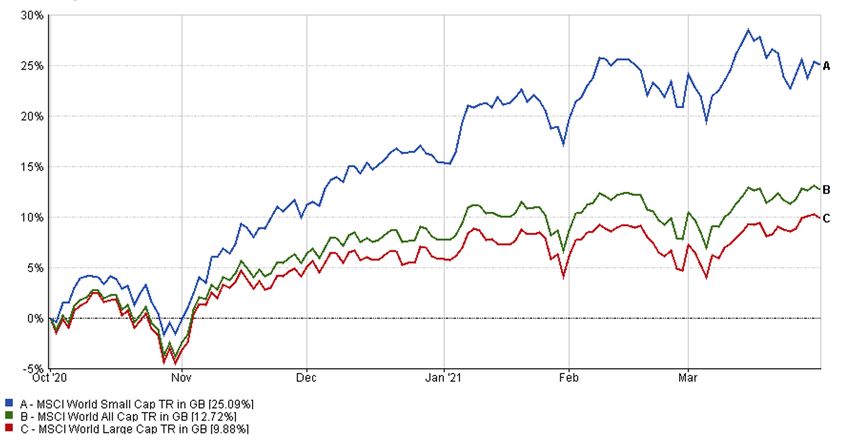

The reversal of fortunes for value stocks were not the only sector of the market to see a rotation in fortune.

Size investors, those looking to invest in small-cap companies, which had also been hit hard by the

pandemic, also continued their upwards momentum, which began in the last quarter.

Akin to value stocks, things started to shift in the last quarter of 2020. Small stocks returns are closely

linked to the performance of the overall economy. With signs that economic recovery could be fast

approaching in the last quarter of 2020, suddenly smaller firms, whose stocks were cheaper, became

an attractive proposition for their potential to deliver higher returns in 2021.

Figure 3

Source: FE Fundinfo (2021)

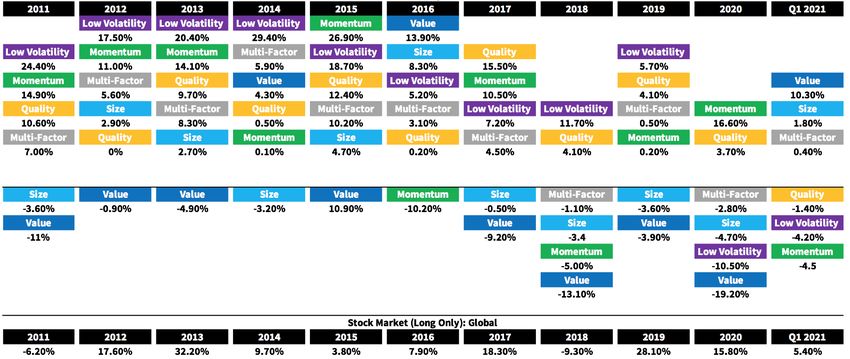

F I N A N C I A L PL A N N I N GA review of the performance of five well known factors strategies over the last ten years reveals the extent

of the rotation to size and value in the first quarter of 2021; the losers of previous years, showing the

cyclical nature of the value factor. Contrastingly, momentum, quality and low volatility have generated

negative returns.

Figure 4 - Factor Olympics (Long-Short): Global

Source: Factor Research 2021

F I N A N C I A L PL A N N I N GIt was not only the US government’s stimulus spending and global inoculation programmes that were

impacting equity prices in the first quarter. Early 2021 saw an unusual David-and-Goliath battle over

GameStop stock. The most popular explanation of events has been of that of “the populists (a phrase that

doesn’t really mean much anymore, beyond just “a collection of guys who are mad”) versus the Institutions”

essentially, a young group of stock picking enthusiasts, wanting to test the financial system to make sense

of whether it was all smoke and mirrors, set up by large financial intuitions for self-gain, or an efficient

capital market engine.

Large investment banks, believing the firm’s stock was all but finished had taken “short” positions, hoping

to profit from a fall in its price and eventual demise, common practice in modern day active management,

known as short selling. Unfortunately for them, a social media group had formed, unhappy at the “shorting”,

believing that the stock had real value in its fundamental business offering. They recruited a mass following

of likeminded buyers and using trading apps, drove the price of the stock upwards, causing it to increase

from $17.25 to $347.51 during January, an increase in price of 1914.5%. The motivation of the majority of

these investors then progressed into punishing hedge funds and testing the financial system as opposed

to a genuine belief that the firm was undervalued. However, some investors undoubtedly were able to take

advantage of the rapid increase in price and make a quick profit.

Figure 5 - GameStop Stock Price

Source: Nasdaq (2021)

The saga continued over the quarter, the stock’s price remained volatile and trading was suspended on

various platforms resulting in claims of foul play by investors who saw this as illegal intervention. The US

government and regulatory agencies took notice and launched a number on investigations. Where will it

end for GameStop? No one really knows, but fundamentally, the company appears hugely overvalued, with

social media led investors refusing to sell, claiming it is now not about the profits.

We all like an underdog story but investing is not about trying to turn a short-term profit; that is pure

speculation or as some may say, gambling. If you fancy a gamble, then sure, instead of putting your money

on “Number 4” at Cheltenham, buy GameStop, but be prepared to lose your entire bet. Unfortunately,

despite what you see in the movies, investing correctly is a slow and disciplined process best served by

investing in low cost, diversified index funds.

5

Washington Post (2021) F I N A N C I A L PL A N N I N GPortfolio Performance

6

Portfolio returns continue to build on the late momentum of last year. Returns over 1, 3, 5, and 7 years all

continue to remain in positive territory across both the Core and ESG models.

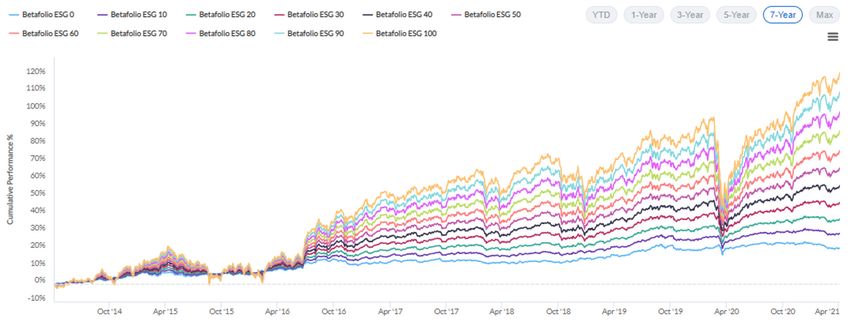

Figure 6 - Mathews Comfort Cumulative Gross Performance

Source: Betafolio (2021)

1-YEAR 3-YEAR 5-YEAR 7-YEAR

Mathews Comfort 0 0.7 7.6 14.8 29.4

Mathews Comfort 10 4.8 10.3 20.7 36.2

Mathews Comfort 20 9.0 12.9 26.5 42.9

Mathews Comfort 30 13.5 15.5 32.4 49.9

Mathews Comfort 0 18.4 18.1 38.7 57.4

Mathews Comfort 50 23.5 20.8 45.0 64.8

Mathews Comfort 60 28.9 23.4 51.5 72.5

Mathews Comfort 70 34.8 26.0 58.1 80.2

Mathews Comfort 80 41.0 28.7 65.0 88.5

Mathews Comfort 90 47.6 31.3 71.8 96.8

Mathews Comfort 100 54.7 34.1 79.4 105.6

Figure 7

Source: Betafolio (2021)

6

All data is up to last price – 5th April 2021. Past performance is no guarantee of future return. Data sourced from Morningstar API.

Careful consideration has been taken to ensure that the information is correct but it neither warrants, represents nor guarantees the

contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein.

Percentages may not total 100 due to rounding. Performance Periods: 1 Year: 05/04/2020-05/04/2021; - 3 Year: 05/04/2018-

05/04/2021, 5 Year: 05/04/2016-05/04/2021, 7 Year: 05/04/2014-05/04/2021. Additional performance periods may be accessed

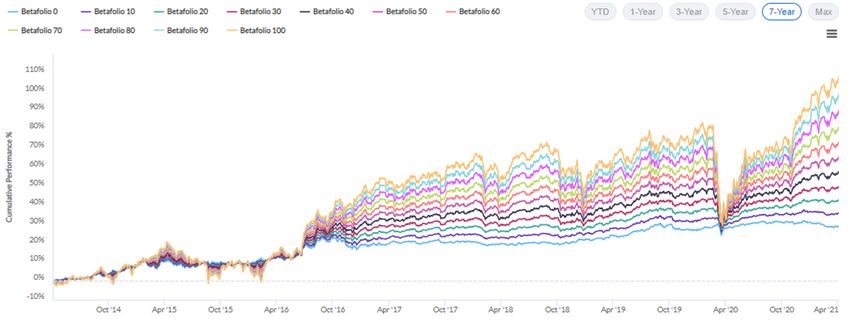

with the help of your adviser via the Betafolio Control Centre: https://app.betafolio.co.uk/ F I N A N C I A L PL A N N I N GPortfolio returns continue to build on the late momentum of last year. Returns over 1, 3, 5, and 7 years all

continue to remain in positive territory across both the Core and ESG models.

Figure 8 - Mathews Comfort ESG Cumulative Gross Performance

Source: Betafolio (2021)

1-YEAR 3-YEAR 5-YEAR 7-YEAR

Mathews Comfort ESG 0 0.1 7.0 11.2 21.0

Mathews Comfort ESG 10 4.0 10.8 18.1 29.3

Mathews Comfort ESG 20 8.0 14.1 24.8 37.3

Mathews Comfort ESG 30 12.1 17.9 32.2 46.5

Mathews Comfort ESG 0 16.7 21.7 39.8 55.9

Mathews Comfort ESG 50 21.2 25.5 47.7 65.7

Mathews Comfort ESG 60 26.0 29.2 55.6 75.3

Mathews Comfort ESG 70 31.2 33.3 64.2 86.2

Mathews Comfort ESG 80 36.2 36.8 72.4 96.9

Mathews Comfort ESG 90 41.7 40.5 81.0 107.7

Mathews Comfort ESG 100 46.5 43.6 89.1 118.2

Figure 9

Source: Betafolio (2021)

4

Closing value 24/12/2020 versus 29/12/2020. F I N A N C I A L PL A N N I N GClosing Words

This time last year the world was reeling from the realisation that the virus that had taken hold of our day

to day normality and posed a serious global health threat. Governments responded by introducing strict

lockdowns and the ensuing panic caused the fasted 30% drawdown of global equities in history.

The team here at Mathews Comfort will freely admit to being flabbergasted by the market’s reaction.

However, our data told us that large market shocks, although rare, had occurred for known reasons in

the past and that markets would recover. Indeed, we saw the subsequent fastest and largest advance in

equities markets in history during the second quarter of 2020.

A year on and equity markets are above their pre-shock levels. This recovery has been made possible by

the tenacity of some very clever scientists to whom we all owe a debt; developing vaccines in months as

opposed to years. In the UK at least, we appear to have the virus on the backfoot, and it looks increasingly

likely that life may soon return to some kind of normality. However, with France and Germany recently

announcing new lockdowns as they struggle to curb a third wave, it reminds us that the pandemic is far

from over.

Foremost, we wish everyone a safe return to normality and hope the performance of your portfolio during

the last year serves to reassure you of the robustness of its construction.

F I N A N C I A L PL A N N I N GBibliography

Corum, A. A., Malenko, A., & Malenko, N. (2021, February 18). Corporate Governance in the

Presence of Active and Passive Delegated Investment. European Corporate Governance Institute

– Finance Working Paper 695/2020.

International Monetary Fund. (2021). World Economic Outlook. Retrieved from:

https://www.imf.org/-/media/Files/Publications/WEO/2021/April/English/text.ashx

Rabener, N. (2021). Factor Olympics Q1 2021. Factor Research. Retrieved April 9, 2021:

https://insights.factorresearch.com/research-factor-olympics-q1-2021/

Washington Post. (2021, February 1). A Breakdown of the Gamestop Situation. Retrieved from:

https://www.washingtonpost.com/business/2021/02/01/understanding-gamestop-situation/

F I N A N C I A L PL A N N I N GYou can also read