Pre-Budget Submission Budget 2019 - DUBLIN IS OUR BUSINESS - Dublin Chamber

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Pre-Budget Submission Budget 2019

DUBLIN IS OUR BUSINESS

Introduction

Budget 2019 comes

Dublin Chamber is the representative body for busi- at a pivotal moment.

nesses in the Greater Dublin Area (GDA), the engine of It will be the first since

the Irish economy and Ireland’s largest population hub.

Our cross-sectoral membership base comprises 1,300

the announcement of

firms across the capital city region, employing 300,000 the National Planning

people nationally. This gives Dublin Chamber a keen in- Framework (NPF) and the

sight into the needs of both businesses and their em-

ployees, informing a holistic vision of the commercial

accompanying National

environment in which economic competitiveness and Development Plan (NDP).

quality of life are complementary. We are committed It will also be the last

to helping businesses succeed in a successful Dublin.

Budget 2019 comes at a pivotal moment. It will be

before the UK exit from

the first since the announcement of the National Plan- the European Union.

ning Framework (NPF) and the accompanying National

Development Plan (NDP). It will also be the last before

the UK exit from the European Union. Budget 2019 will At the same time, Ireland is experiencing robust eco-

therefore be crucial to demonstrating Ireland’s serious- nomic growth, low unemployment, a buoyant labour

ness about business competitiveness vis-à-vis the UK market, and healthy consumer sentiment. In this con-

and its commitment to long-term planning and infra- text, the challenge is to formulate fiscal policy in such

structure investment. Government must send a loud a way as to insure Ireland against current and future

and clear signal in both respects. threats to the extent that is possible without overheat-

Ireland’s small open economy has continued to per- ing the economy.2 This requires a distinction between

form strongly despite rising international risks. expansionary measures that are strictly necessary

However, while the headline indicators are positive, to strengthen the fundamentals of the economy and

the underlying situation is more precarious. those that may be undertaken on a more short-term

With Government indebtedness equal to 260% of basis to improve Ireland’s relative competitive position.

General Government Revenue, Ireland remains acutely Additional fiscal expansion in 2019 should be under-

vulnerability to external shocks.1 The potential causes taken only to strengthen the productive capacity of

of these include Brexit, US tax reforms, EU pressure on the Irish economy, i.e. in the areas of infrastructure,

the Irish tax model, and global market downturns caus- Irish business productivity, and human capital. Target-

ing a sharp drop in Ireland’s corporate tax receipts from ed tax reliefs aimed at strengthening Ireland’s indige-

the multinational sector. Dublin Chamber believes that nous business base and increasing female labour force

Budget 2019 should be developed with these challeng- participation would be the most prudent use of fiscal

es in mind. space at this time.

1 Department of Finance (SPU 2018, April 2018), quoted by NTMA, www.ntma.ie/business-areas/funding-and-debt-management/debt-profile/debt-projections/

2 Early signs of overheating have already been reported by the OECD. OECD, Ireland Economic Forecast Summary, May 2018, www.oecd.org/eco/outlook/eco-

nomic-forecast-summary-ireland-oecd-economic-outlook.pdf

1 | Pre-Budget Submission Budget 2019

Dublin Chamber recommends

that the fiscal space should

be used to prepare Ireland

for the challenges ahead

by strengthening the

fundamentals of the economy

While Dublin Chamber highlights the growing diver-

gence in business tax competitiveness between Ire-

land and the UK, we argue that the business commu-

nity is more immediately concerned with the deeper

structural challenges facing Irish competitiveness. In-

ternal risk factors include the inadequacy of Ireland’s

economic infrastructure, the productivity gap between

Irish and multinational businesses, a pronounced reli-

ance upon tax receipts from a relatively narrow portion

of the economy, and a growing skills shortage. These

internal weaknesses leave Ireland’s highly globalised

economy vulnerable. Budget 2019 must take decisive

action to address them.

In this context, Dublin Chamber recommends that

the fiscal space should be used to prepare Ireland for

the challenges ahead by strengthening the fundamen-

tals of the economy. Government should:

• Invest in Ireland’s Infrastructure

• Grow Ireland’s Businesses

• Invest in Ireland’s Human Capital

Dublin Chamber has outlined four specific mea-

sures under each of these headings, detailed in sum-

mary overleaf. All measures have been costed where

appropriate and possible on the basis of official infor-

mation, while the overall package falls well within the

limits of fiscal space as outlined in the Summer Eco-

nomic Statement 2018.3 In developing this submission,

Dublin Chamber consulted with its membership base,

which includes firms of all sizes in a wide variety of sec-

tors. The recommendations were developed through

a series of surveys, workshops, briefings, one-on-one

meetings, and sessions of our Budget & Taxation Task-

force, and have been approved by the Chamber’s Policy

Council.

3 Department of Finance, Summer Economic Statement 2018,

June 2018, p. iii, https://www.finance.gov.ie/wp-content/up-

2 | Pre-Budget Submission Budget 2019 loads/2018/06/20180622-SES-2018.pdf#page=4

Summary of Recommendations

Invest in Ireland’s Infrastructure:

Measures to prioritise productive investment

Deliver the National Development Plan effectively Ring-fence unexpected receipts for investment in

and on schedule infrastructure

• Meet the fiscal commitments outlined in the • Use tax windfalls to accelerate delivery of priority

National Development Plan, requiring €7.3 billion infrastructure projects under the NDP or, where

in exchequer funding for public capital expenditure, this is not practicable in a given year, to increase

and clarify which projects will receive the increased the size of the Rainy Day Fund.

capital expenditure.

• Allow an informed debate on investment choices

by publishing a breakdown of capital spending by

county and Metropolitan Area; publicly ranking

infrastructure projects according to their cost-

benefit ratio; and publishing the cost-benefit

analyses for completed projects.

Prioritise projects in the Greater Dublin Area

Projects to relieve the growing pressure in the capital

city region must be prioritised for progress and

investment by the Exchequer in 2019. Dublin Chamber’s

priorities are:

• MetroLink

• DART Expansion Programme

• BusConnects

• Eastern & Midlands Region Water Supply Project

• Social & Affordable Housing Construction in Dublin

and other high-demand urban areas

Use the ‘Rainy Day Fund’ as an insurance policy for

the NDP

• Permit drawdown from the Rainy Day Fund if

economic growth dips below the level required to

fund delivery of the NDP (minimum 2% growth), to

ensure stable and steady delivery of the planned

infrastructure investments.

3 | Pre-Budget Submission Budget 2019

Grow Ireland’s Businesses:

Measures to encourage

entrepreneurship

& enterprise

Upgrade Entrepreneur Relief to surpass the UK.

• Raise the lifetime cap on qualifying gains for

Entrepreneur Relief from €1 million to €15 million

to send a strong signal that Ireland intends to

compete with the UK ahead of Brexit.

Introduce an Investor Relief to encourage investment

in Irish SMEs

• Introduce an Investor Relief along the UK model,

offering a lower 20% CGT rate on all investment in

unquoted trading companies where shares have

been held in excess of three years, with a lifetime

limit on qualifying gains of €10m.

Make the R&D tax credit work for SMEs

• Allow an upfront claim of the R&D tax credit cash

refund for SMEs, instead of the three year lagging

deferred cash-flow mechanism that currently

exists, and increase the R&D tax credit rate from

25% to 30% for SMEs.

Reduce income tax on dividends for entrepreneurs

to 30%

• Tax entrepreneurs at a lower rate of 30% on income

from share dividends to outmatch the UK offering

ahead of Brexit.

4 | Pre-Budget Submission Budget 2019

Invest in Ireland’s

Human Capital:

Measures to attract, retain,

and develop talent

Increase female labour market participation

• To ameliorate the childcare affordability problem,

double the maximum universal childcare subsidy for

children before the start of ECCE under the Affordable

Childcare Scheme from €80 per month to €160 per

month for a child in full-time care, with a commitment

to similar progressive increases in subsequent years.

• Consider improving the targeted subsidy element

of the Affordable Childcare Scheme to better reflect

the net income of the second earner in a family (not

just combined parental net income) with a view to

increasing labour force participation. More broadly,

and in the context of the proposals to reform income,

PRSI and USC, undertake a thorough examination of

how these taxes discourage ‘second earners’ from

returning to the workforce, with a commitment to

progressively removing labour force participation

barriers on the basis of the findings.

Allow SMEs to avail of the Special Assignee Relief

Programme (SARP) for new recruits

• Extend the Special Assignee Relief Programme to

new recruits for firms that are SMEs by the European

Commission definition.

Make the Key Employee Engagement Programme work

for SMEs

• Issue detailed guidance on valuations to provide

clarity for firms facing the compliance burden of

issuing share options at market value;

• The restriction of the value of share options granted

to any individual to 50% of the value of his/her annual

remuneration should be lifted.

• Allow qualifying individuals to make their services

available to other entities in a group, and reduce the

time required to work for a qualifying company to 30

hours per week.

Prevent taxation of employer-funded professional

subscriptions from taxation as BIK

• Amend Revenue guidance to make clear provision

for the exemption from Benefit-In-Kind taxation of

professional memberships that are commercially

necessary but not statutorily required.

5 | Pre-Budget Submission Budget 2019

Invest in Ireland’s Infrastructure

Ireland has a major public infrastructure deficit due to noted that urban Ireland particularly suffers as a

historic underinvestment, compounded by the fiscal result of shortcomings in transport infrastructure, and

impact of the economic crisis. Large-scale and long- warned the situation will be further aggravated by rising

term investment is now urgently required in Dublin’s economic activity and population growth.8 Dublin has

infrastructure stock in order to redress past neglect, been ranked as the 5th most traffic-congested city in

protect Irish competitiveness, and enhance the Europe,8 with public transport usage by commuters in

productive capacity of the Irish economy. From a broad the capital standing at just 22%.10 Using a very narrow

perspective, there is strong evidence of a positive definition of congestion, the NTA has estimated that

relationship between public investment, aggregate traffic congestion in the GDA now costs the national

demand, and potential growth; and Ireland has been economy at least €350 million per annum, rising to an

identified by the OECD as a country that would annual cost of €2 billion by 2033.11

particularly benefit from a change in Meanwhile, the social cost of inade-

fiscal priorities from current spending Table 1: Business feedback on quate infrastructural investment con-

internal challenges to Dublin

to capital investment.4 competitiveness7 tinues to mount.

Economic infrastructure consis- Government should allocate

tently ranks as the most important national resources in a manner that

7% 5

policy issue affecting Dublin busi- % respects and reflects where Irish

nesses, with almost half (48%) of people actually live in their greatest

recently surveyed firms choosing numbers. Investment should be

investment in infrastructure as their 22% focused on urban areas, which

top priority for Budget 2019. The in-

5

generally offer the greatest return

adequacy of Irish infrastructure is in- in terms of cost-benefit due to

ternationally perceived as the most 65% higher populations. The National

important barrier to doing business Competitiveness Council has argued

in Ireland according to the World Eco- that enhanced city performance

nomic Forum survey;6 and the busi- What is the biggest problem has positive spill-over effects on

ness community in Dublin concurs, facing Dublin’s competitiveness? the country as a whole. Prioritising

with inadequate infrastructure identi- Bad planning investment and initiatives to develop

fied as the biggest problem facing the Inadequate infrastructure the competitiveness of our cities is

city’s competiveness. Poor governance therefore the most effective use of

The European Commission has Ineffective promotion of Dublin Exchequer funds.12

4 International Monetary Fund, IMF Country Report No. 17/333, Ireland Technical Assessment Report: Public Investment Management Assessment, November 2017, p.7

5 Dublin Chamber Quarterly Business Risk Outlook Q2 2018

6 International Monetary Fund, IMF Country Report No. 17/333, Ireland Technical Assessment Report: Public Investment Management Assessment, November 2017, p.7

7 Dublin Chamber Quarterly Business Trends Survey Q4 2017

8 European Commission, 2017, ‘Country Report Ireland Including an In-Depth Review on the prevention and correction of macroeconomic imbalances’, p. 53

9 TomTom Traffic Index, Full Ranking, Europe – All Cities, https://www.tomtom.com/en_gb/trafficindex/list?citySize=ALL&continent=EU&country=ALL, accessed 23.07.2018

10 CSO, Census 2016, Profile 6 Commuting in Ireland, https://www.cso.ie/en/csolatestnews/presspages/2017/census2016profile6-commutinginireland/

11 Dept. of Transport calculation, Dáil Question No: 346, John Lahart TD. Ref No: 1857/17, Proof: 348, Answered by the Minister for Transport Tourism and Sport Shane

Ross. This is likely a conservative estimate. Back in 1997 the Dublin Transportation Office estimated the cost at £500 million, or c. €1.2 billion today adjusted for inflation.

12 Forfás, National Competitiveness Council, Our Cities: Drivers of National Competitiveness, April 2009, p. 7

6 | Pre-Budget Submission Budget 20191. Deliver the National Development Plan effectively and on schedule Ireland requires a long-term approach to infrastructure has improved the allocation of resources for projects, planning that accounts for future population the planning process is still inadequately linked to projections and supports the growth of city regions as decisions on funding. It also notes that there is room drivers of regional development.13 With this in mind, to improve the methodological rigor, sequencing, and Dublin Chamber welcomed the National Planning effectiveness of the project appraisal and selection Framework: Ireland 2040 Our Plan (NPF), Ireland’s processes.14 Parliamentary efforts to secure early new spatial development plan, and the accompanying clarity from Government about which specific projects National Development Plan 2018-2027 (NDP) for capital will receive extra funding from the increased capital investment. The NPF’s recognition of cities as the allocations in 2019, and how they will be prioritised, drivers of regional growth throughout Ireland was a have been unsuccessful.15 particularly welcome change from previous approaches The debate about capital investment priorities to spatial planning. The co-publication of the NDP should be informed by clear and up-to-date data on and NPF represented a positive step towards proper the relative costs and benefits of proposed projects. alignment of spatial and infrastructural development. In practice, however, there is a lack of transparency Budget 2019 will be the first since the launch of the both with respect to comparisons between regional two plans. It is crucial that Government demonstrates investment levels16 and comparisons between seriousness about its commitment to the infrastructure specific infrastructure projects. To introduce greater investments needed to support long-term planning and transparency to the decision-making process, Dublin intelligent urbanisation. The first test of Budget 2019 Chamber proposes that all infrastructure projects will be whether it meets the Government’s own fiscal under consideration be publicly ranked according to commitments as outlined in the NDP and allocates their cost-benefit ratio. This can be done in the form of additional capital funds in an effective manner. a simple list, without publicly revealing an estimate of However, serious concerns remain about delivery of cost in monetary terms. There would be no reason to the NDP and how projects will be prioritised in order withhold such information on grounds of commercial to make best use of public funds. The IMF has warned sensitivity; on the contrary, release of such data would that, while implementation of multi-year budgeting be clearly in the public interest. 13 Dublin Chamber, Submission on the Mid-Term Review of the Capital Investment Plan, April 2017 14 International Monetary Fund, IMF Country Report No. 17/333, Ireland Technical Assessment Report: Public Investment Management Assessment, November 2017, p.8 15 E.g. Dáil Éireann Debate Wednesday 11 July 2018, Question No. 490. Reference No. 31281/18. Deputy Barry Cowen. Answered by the Minister for Transport Tourism & Sport Shane Ross. Question in relation to use of the additional €316m for the Dept. Transport capital allocation in 2019. 16 National Income & Expenditure Table 25: Central & Local Government – Details of Gross Physical Capital Formation is no longer published, meaning that it is no longer possible to accurately compare the total level of capital formation in the GDA with that in other parts of Ireland. 7 | Pre-Budget Submission Budget 2019

Recommendations Budget 2019 must meet the Government’s fiscal Government must allow an informed debate on capital commitments as outlined in the National Development investment choices by: Plan. This will require €7.3 billion in exchequer funding • Publishing a breakdown of capital spending by for public capital expenditure, accounting for 3.5% of county and Metropolitan Area in its National projected Gross National Income.17 Income & Expenditure tables; The Government must clarify which projects it is • Ranking all infrastructure projects under consid- prioritising to receive the increased capital expenditure eration according to their cost-benefit ratio and under the National Development Plan over the 2019- making this data available to the public. 2022 period, with particular attention given to the €3.3 • Publishing the cost-benefit analyses prepared for billion in additional capital allocations to the Dept. of completed projects to encourage learning from Transport, Tourism & Sport over the same period.18 past experience. 17 Project Ireland 2040: National Development Plan 2018-2027, p. 19 18 Annex 1, Project Ireland 2040: National Development Plan 2018-2027, p. 104, 8 | Pre-Budget Submission Budget 2019

2. Prioritise projects in the Greater Dublin Area

Analysis by Dublin Chamber demonstrates that, Dublin received the second lowest level of capital

far from being a favoured location for Government investment per head from central government of

spending, the capital city receives significantly any county from 2009-2016. The combined four

less investment in its productive and social Dublin Local Authorities received less than half of

infrastructure than is required to support economic the national average over the period, and less than

competitiveness and quality of life. Despite the a third of the amount received by higher per capita

demographic pressures on its infrastructure, recipients, as illustrated in Table 2.

Table 2: Average Annual Capital Spending per capita 2009-201619

Kilkenny 718

Leitrim 633

Westmeath 596

Roscommon 557

Mayo 499

Kildare 492

Longford 484

Laois 478

Monaghan 472

Average 430

Tipperary 425

Clare 422

Kerry 419

Galway 404

Waterford 396

Limerick 386

Wexford 367

Donegal 350

Offaly 348

Cavan 345

Cork 343

Meath 317

Wicklow 280

Louth 270

Dublin 229

Carlow 203

€- 100 200 300 400 500 600 700 800

19 Includes 1) Income Received by Local Authorities for Capital Spending in Six Budget Service Categories including transport (37%), housing and urban regen-

eration programmes (34%) and general purpose grants (16%); 2) allocations from Transport Infrastructure Ireland for National Roads in each county. Does not

include: 1) One-Off Capital Spending on National Infrastructure Projects (such as Hospital Buildings and Primary Care Centres) that is difficult to geographically

localise and mainly takes the form of availability payments on PPPs.

19

Includes 1) Income Received by Local Authorities for Capital Spending in Six Budget Service Categories

9 | Pre-Budget Submission

including transportBudget 2019 and urban regeneration programmes (34%) and general purpose grants

(37%), housing

(16%); 2) allocations from Transport Infrastructure Ireland for National Roads in each county. Does not include:

1) One-Off Capital Spending on National Infrastructure Projects (such as Hospital Buildings a nd Primary CareTable 3: Capital Spending by Central Govt. in Local Authority 2009-2016 The underfunding of Dublin has been consistent Perhaps the most egregious example of underinvest- in recent years and it marks the continuation of a ment has been in the Housing category. Dublin is the broader pattern.20 Severe levels of underinvestment epicentre of the accommodation crisis; it has propor- have occurred in Dublin’s local infrastructure and tionally the highest social housing waiting lists in Ireland, capital maintenance. This includes the categories of and the highest number of households reliant upon Transport, Environment, Development Management, social housing supports such as Housing Assistance Education and Employment Services, Recreation and Payment or Rent Supplement. Yet despite having the General Purpose Grants. Dublin also received below- greatest needs, Dublin received below average capital average current funding for local services and below- investment in housing by the Central Government over average total spending by central government in the the 2009-2016 period, and less than half the amount 2009-2016 period. per capita received by the highest recipient county. 20 Edgar Morgenroth, The Regional Development Impacts of Transport Infrastructure, 2014, found that Dublin received the lowest level of capital investment in public infrastructure per head of any Irish region. Data collected in 2009: Dublin per capita capital investment €1041 vs. national average €1543 (i.e. two thirds of the national average). 10 | Pre-Budget Submission Budget 2019

This analysis is based only on Dublin’s resident account, it is clear that the abovementioned spending

population. It does not account for those living outside figures are merely a conservative representation of the

of Dublin who use its infrastructure every working day. inadequacy in funding for Ireland’s capital.

A further 116,000 people commute into Dublin to work This anomaly is both socially inequitable and econom-

on a daily basis, and many more travel into the city for ically unsound. If sustained, it will exacerbate existing

education and public services.21 Moreover, the capital social problems and undermine Dublin’s international

city is the reception point for the overwhelming majority competitiveness as a city in which to live, work, invest,

of Ireland’s tourist population, with Dublin Airport and do business. Already, levels of life satisfaction are

receiving 82% of overseas visitors to the Republic lower in Irish cities than in rural areas, both among

of Ireland,22 and 68% of holidaymakers spending high-income and low-income groups.24 Other research

time in Dublin before travelling on to other parts of has found that the capital city has one of the lowest

the country.23 Taking these additional pressures into levels of self-reported life satisfaction in Ireland.25

Table 4: Total Housing Capital Investment per capita 2009-2016

21 Analysis of CSO Census 2016 data privately supplied to Dublin Chamber.

22 Dublin Airport, North Runway: Potential to connect, compete and grow, p.4, https://www.dublinairport.com/docs/default-source/North-Runway-Docs/po-

tential-to-connect-compete-and-growd6ad438b73386836b47fff0000600727.pdf?sfvrsn=0#page=4

23 Tourism Ireland, Facts& Figures 2016, p.4, https://www.tourismireland.com/TourismIreland/media/Tourism-Ireland/Press%20Releases/Press%20Releas-

es%202017/Facts-and-Figures-2016.pdf?ext=.pdf#page=4

24 Eurostat, Statistical Books, Urban Europe: Statistics on Towns, Cities & Suburbs 2016 Ed., p. 267

25 UCD Briefing Paper for Comhar, Clinch et al, Understanding & Measuring Quality of Life in Ireland: sustainability, happiness and well-being, p. 56

11 | Pre-Budget Submission Budget 2019Recommendations Projects to relieve the growing pressure in the capital city region must be prioritised for progress and invest- ment in 2019. Dublin Chamber’s priorities are: • MetroLink Dublin Chamber strongly supports the MetroLink proj- ect. We have long advocated an underground rail line to connect North County Dublin with the city centre, including a stop at Dublin Airport. This line should also serve the swelling commuter populations of North and South Dublin, including Sandyford and other high- growth areas. • DART Expansion Programme The DART Underground project will be crucial to the development of an integrated public transport system in Dublin. In the absence of developments on this, we recommend that other elements of the Expansion Pro- gramme, such as electrification, be progressed in 2019. • Bus Connects The NTA plan for new bus corridors and Bus Rapid Transit in the capital has the potential to be a valuable solution to mounting traffic congestion and should be prioritised for funding where further progress on the larger projects is not feasible. • Eastern & Midlands Region Water Supply Project Water systems in Dublin’s competitor cities typically operate at c. 80% capacity, while in Dublin this figure is approximately 98%. With Dublin expected to meet capacity constraints by 2025, and water outages al- ready a reality, construction of the Shannon pipeline is an urgent priority. • Social & Affordable Housing Construction Government must shift from the counter-productive policies of rental support and private home acquisition to the construction of new purpose-built social and affordable homes in high-density apartment develop- ments in the capital. This is needed to relieve pressure in the private market, address Dublin’s homelessness problem, and protect quality of life in the capital city. 12 | Pre-Budget Submission Budget 2019

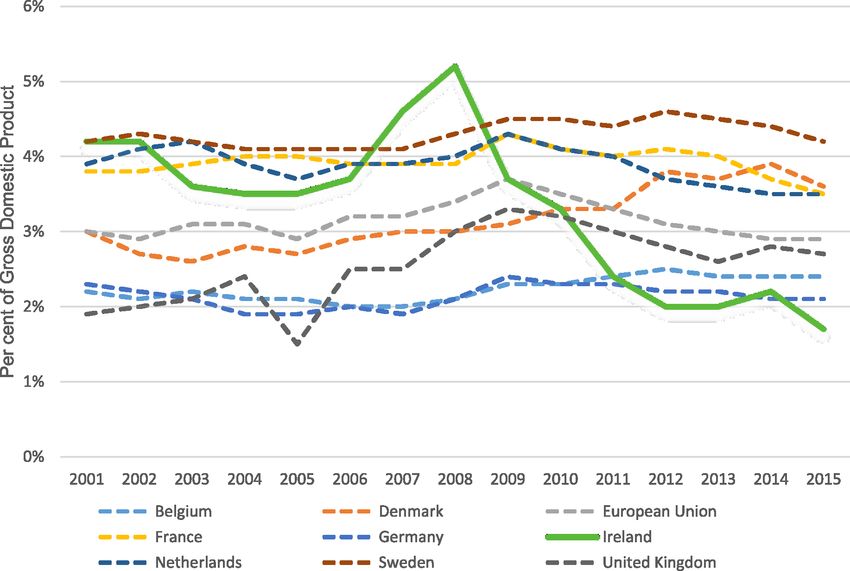

3. Use the ‘Rainy Day Fund’ as an

insurance policy for the NDP

Steady investment in Ireland’s productive infra- But the investment surge was short-lived, and cap-

structure will be crucial to economic success in the ital expenditure fell precipitously before these goals

coming years, but achieving this will require learn- were achieved; almost a decade later, it had failed to

ing from the lessons of the past. Ireland’s pattern of recover. This highly variable pattern contrasts with

capital investment in recent decades has been one the more stable pattern in Ireland’s European neigh-

of the most volatile in Western Europe. During the bours. Capital expenditure levels are now recovering,

boom years, Ireland raised its capital spend to com- but it is crucial that Ireland does not fall back into its

pensate for generations of underinvestment and to historical pattern of instability on account of an ex-

place itself on an even footing with competitors. ternal economic shock.

Table 5: General Government Gross Fixed Capital Formation, 2001 – 201526

26 Eurostat

13 | Pre-Budget Submission Budget 2019Dublin Chamber acknowledges the Rainy Day Fund Recommendation as a prudent means of strengthening Ireland’s fiscal To avoid a relapse into volatility, drawdown from the resilience. The initial tranche of €1.5 billion from the Rainy Day Fund should be legally permitted to ensure Ireland Strategic Investment Fund, combined with stable and steady delivery of the planned infrastructure annual €500 million contributions from 2019 to 2021, investments, if and when economic growth dips below will see the Fund reach €3 billion by 2021, providing a the level required to fund delivery of the National substantial resource for economic stabilisation. Development Plan (minimum 2% growth).27 27 4% over 2022-2027 period, based on 2% real and 2% inflation. Project Ireland 2040: National Development Plan, p. 19 14 | Pre-Budget Submission Budget 2019

4. Ring-fence unexpected receipts

for investment in infrastructure

Ireland’s infrastructure deficit is the biggest internal

challenge to both economic competitiveness and

Recommendation

quality of life. Addressing this should be the country’s • Tax windfalls, whether from the activities of

most pressing priority. Delay in delivery of key multinationals or other sources, should be used

infrastructural programmes will constrain economic to accelerate delivery of priority infrastructure

growth in the years ahead, ultimately undermining projects under the NDP or, where this is not

Ireland’s fiscal position. The EU Commission has practicable in a given year, to increase the size of

indicated that Irish fiscal sustainability is not at the Rainy Day Fund.

short-term risk, while medium and long-term risks

are based as much on competitiveness concerns

as on the level of Government debt.28 Therefore,

Government should take all opportunities to

accelerate infrastructure delivery where possible

under EU fiscal rules.

In recent years, several categories of receipts

have generated more revenue than was expected

on the basis of initial estimates. Figures released by

the Department of Finance suggest that exchequer

returns for 2018 may be ahead of target, principally

due to buoyant receipts from tax on corporate

income. Cumulative corporation tax receipts by end-

June 2018 are 9.1% or €335 million ahead of target.29

Fiscal prudence demands that better-than-

expected revenues are not committed to the

expansion of current spending programmes, and

Dublin Chamber endorses the IMF’s recent warning

to avoid using temporary revenue gains to fund

permanent measures.30 Instead, they should be used

to enhance the productive capacity of the economy

through infrastructure investment.

28 European Commission DG ECFIN, Assessment of the 2018 Stability Programme for Ireland, 23 May 2018, p.16, https://ec.europa.eu/info/sites/info/files/econo-

my-finance/07_ie_sp_assessment_0.pdf#page=16

29 Department of Finance Fiscal Monitor (Incorporating the Exchequer Statement) June 2018, p.3, https://www.finance.gov.ie/wp-content/uploads/2018/07/

Fiscal_Monitor_2018_June-1.pdf#page=4

30 IMF, Ireland Staff Concluding Statement of the 2018 Article IV Mission, May 2018, https://www.imf.org/en/News/Articles/2018/05/14/ms051418-ireland-staff-

concluding-statement-of-the-2018-article-iv-mission

15 | Pre-Budget Submission Budget 2019Grow Ireland’s Businesses Budget 2019 will be the last before the UK withdrawal and the UK in order to provide a competitive context from the EU, a historic event that is likely to have major for our proposals on enterprise and entrepreneurship. implications for Ireland’s economic model. Brexit is It is clear that the UK is focused on assisting new not the only external threat that Ireland faces. As a British businesses to grow, thereby increasing both small open economy, Ireland is highly vulnerable to the employment and revenue-generating potential of fluctuations in the international market, or even to these firms. As illustrated in Table 6, Ireland’s business restructuring by a small number of multinational firms. environment now compares negatively with its nearest Meanwhile, US tax reforms have already blunted the neighbour in numerous respects. competitive edge of Ireland’s offering to FDI. Dublin Chamber acknowledges that Government While Ireland must withstand external political must balance social and economic needs when pressures on its corporation tax regime, and remain determining tax policy, and believes that this can attractive to international investors, it must also take be achieved whilst improving the entrepreneurial decisive action toavoid excessive reliance upon a environment. For example, the Chamber has long narrow number of highly mobile businesses.31 This advocated fairer and equal tax treatment for the self- will require the strengthening of Ireland’s indigenous employed, including raising the Earned Income Tax business base, both to increase the size of the overall Credit to the PAYE equivalent of €1,650, and removing economy and to increase the proportion of it accounted of the 3% USC surcharge on self-employed people for by Irish firms. Ireland must start to take a broader earning over €100,000. We would welcome progress view of industrial policy that places greater priority on towards these goals in Budget 2019, while consideration welcoming entrepreneurs and encouraging Irish SMEs should also be given to gradually increasing the entry to scale. point for the higher 40% income tax rate in order to The Government’s updated enterprise development ease pressure on average income earners. policy, Enterprise 2025 Renewed, acknowledges that While progress on all fronts is not be feasible in while some progress has been made towards updating one fiscal year, there is scope within the fiscal space Ireland’s tax regime in recent years, ‘we need to take as outlined in the summer economic statement account of our comparative position relative to the to send a strong signal that Ireland intends to offerings of our main competitors, and the reality that sharpen its competitive edge in an uncertain world. Irish enterprises are mobile too.’32 The need for such a Informed by comparative analysis and business comparison has never been more urgent than today. feedback, the following are Dublin Chamber’s priority With this in mind, Dublin Chamber has compared Ireland recommendations for 2019. 31 National Competitiveness Council, Competitiveness Bulletin 18-2: Economic Concentration 2018, http://www.competitiveness. ie/Publications/2018/Concentration-Bulletin.pdf 32 Enterprise 2025 Renewed: Building resilience in the face of global challenges, p. 13, https://dbei.gov.ie/en/Publications/Publica- tion-files/Enterprise-2025-Renewed.pdf#page=29 16 | Pre-Budget Submission Budget 2019

Table 6: Ireland-UK Business Competitiveness Table

Ireland UK / NI

(€1.1333 per £1 – 10/05/18 – www.ft.com)

(Budget 2018) (Budget Spring ‘18)

Investment in Critical Infrastructure

General Government Gross Capital Expenditure

2.00% 2.88%

as % of GNI (Current LCU) 2017

Income Tax

Salary at which rate changes to 40% 33 [€/£] €34,550 €52,528

Effective total tax rate on dividends at higher rate 52% 32.5%

Yes – 3% USC levy on

Different assessment for self-employed. income over No

€100,000

Yes – recent

Possible to defer income tax on share-options given to

introduction of KEEP Yes

specific key employees

for SMEs

Capital Gains Tax

Standard rate 33% 20%

10% on qualifying

Entrepreneur relief – CGT rate

assets up to €1m

Effective rate first ~€1m on exit after five years 10% 10%

Effective rate first ~€11m on exit after five years 31% 10%

Capital gains tax rate on disposal of shares in SMEs 33% 10%

Capital gains tax rate on Employment and Investment

33% 0%

Incentive Scheme qualifying investment or equivalent gains

Corporate Tax

Knowledge Development Box / Patent box income 6.25% 10%

Corporate Tax rate (UK’s by 2020) 12.50% 17%

R&D Tax Credit – upfront refunds for early stage/scaling

No Yes

companies

Capital gains tax business asset rollover relief No Yes

Value Added Tax

Standard Rate 23% 20%

Registration Threshold for SME providing services34 €37,500 €96,330

17 | Pre-Budget Submission Budget 20191. Upgrade Entrepreneur Relief to surpass the UK

Entrepreneur Relief from Capital Gains Tax provides for The Department of Finance has acknowledged that

disposals of qualifying business assets by entrepreneurs ‘retention [of the relief] is important in the context of

to be charged at a lower 10% CGT rate up to a lifetime possible Brexit impacts and other issues than may arise

limit on chargeable gains.33 To qualify, among other as the UK exits the EU.34 Moreover, the Programme

conditions, an individual must own at least 5% of for Government promises ‘We will reduce the rate of

the business and have spent a certain proportion Capital Gains Tax for new start-ups to 10% from 2017

of their time working in the business as a director or (held for five years and subject to a €10 million cap on

employee for three out of the previous five years, prior gains).’35

to disposal. The aim is to encourage entrepreneurs to The cost of bringing Ireland’s lifetime limit up to the

found, operate, and dispose of businesses in the State, nominal UK equivalent of €10 million, as promised in

and to build a reputation for Ireland as a country that the Programme for Government, has been estimated

welcomes and rewards enterprise. Dublin Chamber at €54 million using the non-dynamic costing model

made the case for the revised Entrepreneur’s Relief in employed by the Department of Finance. However, a

2015, and welcomed its introduction in Budget 2016. further increase in the limit to €15 million would incur an

However, Ireland’s offering to entrepreneurs remains added annual cost to the exchequer of just €2 million,

starkly uncompetitive in relation to the UK’s, which according to the same model, while positioning Ireland

includes a lifetime cap of £10m (c. €11.2m in current at a very clear competitive advantage against the UK.36

market prices) on qualifying gains for Entrepreneur

Relief. This compares with a modest €1m cap in Ireland.

A larger limit is required to encourage greater ambition

Recommendation

and scaling by entrepreneurs; and Ireland should send • Raise the lifetime cap on qualifying gains for

a strong signal that it intends to compete with the UK Entrepreneur Relief from €1 million to €15 million

ahead of Brexit. Consideration could also be given to to send a strong signal that Ireland intends to

given to amending the 5% share requirement to refer compete with the UK ahead of Brexit. Cost: €56

to the point of investment, ensuring that entrepreneurs million.

who retain their initial investment are not penalised as

subsequent external investment is received.

33 Qualifying business assets include those in most productive businesses, excluding businesses involving land dealing or holding investments.

34 It has previously been argued that Ireland’s less generous scheme is compensated for by the existence of Retirement Relief, which can be claimed to values

ranging from €500,000 to €3 million. However, this ignores the reality of successful serial entrepreneurship today, which often takes place well before retirement

age. Moreover, the combined value of the current reliefs is still substantially lower than the UK equivalent. Department of Finance Tax Strategy Group – TSG

17/11, Capital & Savings Taxes, 25 July 2017, p.5.

35 Programme for a Partnership Government, p.38.

36 Department of Finance Tax Strategy Group – TSG 18/10, Capital & Savings Taxes, 10 July 2018, p.11, https://www.finance.gov.ie/wp-content/up-

loads/2018/07/TSG-18-10-Capital-and-Savings-Taxes-PL.pdf#page=11. Dublin Chamber notes the limitations of non-dynamic costing, and the fact that previous

reductions in Capital Gains Tax have had a stimulatory effect on economic activity, ultimately increasing revenue generation.

18 | Pre-Budget Submission Budget 20192. Introduce an Investor Relief to

encourage investment in Irish SMEs

Growing Ireland’s indigenous business base will The Irish CGT regime effectively incentivises

require greater investment by SMEs. While the passive investment in larger foreign firms over

Government’s enterprise policy commits to ‘ensuring investment in higher risk Irish SMEs. This runs

a competitive funding environment that provides contrary to the national interest, which clearly lies

a range of options to support our enterprises from in building up a greater indigenous business base

start-up to growth’, in reality, the flat-rate CGT so as to avoid over-reliance on a small number of

regime undermines efforts to promote investment in highly mobile multinationals. With a similar concern

SMEs.37 There is no incentive to choose investment in mind, the UK introduced an ‘Investors’ relief’ from

in a home-grown start-up over investment in a CGT. It offers a lower CGT rate of 10% on lifetime

longer-established multinational. The ESRI recently gains of up to £10 million from disposals of shares in

identified a significant investment gap in the Irish an unlisted trading company or the holding company

SME sector in a joint study with the Dept. Finance, of a trading group.39

calculating that the gap amounts to just over €1

billion for 2016 alone.38

Application of a flat 33% CGT rate on all capital

gains, irrespective of the level of risk taken and the

contribution to the Irish economy of the underlying

Recommendations

investment, is clearly inequitable. Investors pay the • Introduce an Investor Relief along the UK model,

same CGT on passive investments in large blue chip offering a lower 20% CGT rate on all investment

foreign companies as they would on higher-risk Irish in unquoted trading companies where shares

companies. People providing angel investment, have been held in excess of three years.40 While

people providing their services as employees, and lower than the British rate of 10%, it would be an

shareholders who do not meet the 5% threshold important first step to encourage investment in

to avail of Section 597AA (Entrepreneur Relief) indigenous business.

are therefore unfavourably treated. Moreover, the • To keep the scheme open to small-scale

distinction between large quoted companies, with investors, there should be no minimum

a liquid market for the sale of shares, and unquoted percentage shareholding in order to qualify.

firms, with a much less liquid market for the sale of • Establish a lifetime limit on qualifying gains at the

shares, is not reflected in the taxation regime. nominal UK equivalent of €10m.

37 Dept. Business Enterprise & Innovation, Enterprise 2025 Background Report, p. xv

38 “The magnitude of this “investment gap” is economically meaningful and is estimated to be just over 30% (in 2016) relative to SMEs actual investment.” ESRI,

Measuring the Investment Gap & its Financing Requirements for Irish SMEs, 8 March 2018, https://www.finance.gov.ie/wp-content/uploads/2018/03/180308-

Measuring-the-Investment-Gap-and-its-Financing-Requirements-for-Irish-SMEs.pdf

39 HM Revenue & Customs internal manual, Capital Gains Manual, CG63500P, https://www.gov.uk/hmrc-internal-manuals/capital-gains-manual/cg63500p

40 The Dept. Finance has reported that it is unable to calculate the cost of introducing a version of the UK scheme in Ireland as tax returns do not identify the

amount of chargeable gains associated with unquoted shares. Dáil Éireann Debate Thursday 5 July 2018, Question No. 86, Reference No. 29776/18. Deputy

Pearse Doherty. Answered by the Minister for Finance Paschal Donohoe.

19 | Pre-Budget Submission Budget 20193. Make the R&D tax credit work for SMEs Business Research & Development in Ireland remains Development tax credit is almost twice as common dominated by larger, foreign-owned MNCs, with only among large firms as among SMEs, and is almost four 1% of small firms engaged in R&D.41 This year, the OECD times more common among foreign firms as among Economic Survey has again highlighted the existence firms founded in Ireland.44 of a two-speed economy in Ireland, confirming that Many SMEs, and most start-ups, face cash flow the productivity gap between the indigenous and issues which make the 3-year deferred claim model multinational sectors is actually widening rather than unattractive or impractical. Allowing an upfront narrowing.42 To address the growing productivity gap payment would make the R&D tax credit a more between the indigenous and multinational sectors, realistic option for early stage firms with lower cash Government must take steps to improve the low levels resources. In the competitive context of Brexit, it is of innovation among Irish SMEs. also worth noting the regime in the UK, where there is The Research & Development Tax Credit is one of the a special R&D Relief available to SMEs with extremely principal schemes the Government uses to encourage attractive conditions, including a super deduction of R&D among businesses. As currently designed, 130% of qualifying costs for SMEs.45 however, it is failing to drive R&D among indigenous businesses on the scale that Ireland requires. The European Commission has advised that the emphasis Recommendations in Ireland’s R&D strategies for business should be to build up research and innovation capability within Irish • Allow an upfront claim of the R&D tax credit cash SMEs, and has recommended that the R&D tax credit refund for SMEs, instead of the three year lagging scheme must be targeted at SMEs specifically.43 deferred cash-flow mechanism that currently Feedback from Dublin Chamber members indicates exists. As this purely a cash-flow measure, it is that there is a low take-up of the R&D tax credit outside would be cost-neutral over a three-year period, the multinational sector at present. It is particularly with minimal exchequer impact. low among firms founded in Ireland and among firms • Increase the R&D tax credit rate from 25% to 30% that are SMEs by the European Commission definition. for SMEs, to compare better with the UK’s SME The same study indicates that use of the Research & R&D Relief. Cost: €30 million.46 41 European Commission Research & Innovation Observatory Country Report 2017: Ireland, pp.24-26 42 OECD Economic Survey of Ireland 2018, https://www.oecd.org/eco/surveys/economic-survey-ireland.html 43 European Commission Research & Innovation Observatory Country Report 2017: Ireland, p.26 44 Dublin Chamber Business Risk Outlook Survey Q2 2018 45 HM Revenue & Customs internal manual, Corporate Intangibles Research & Development Manual, CIRD90000, https://www.gov.uk/hmrc-internal-manuals/ corporate-intangibles-research-and-development-manual/cird90000 46 Dáil Éireann Debate Thursday 5 July 2018, Question No. 87, Reference No. 29777/18. Answered by the Minister for Finance Paschal Donohoe. The overall cost of the R&D tax credit reached €553 million in 2014. Dept. Finance, Economic Evaluation of the R&D Tax Credit, October 2016., p. 6, https://igees.gov.ie/wp-con- tent/uploads/2014/01/R-and-D-Credit-Evaluation-2016.pdf#page=6 20 | Pre-Budget Submission Budget 2019

4. Reduce income tax on dividends

for entrepreneurs to 30%

To succeed in developing prospering indigenous be the only option that is encouraged. In many cases

businesses on a large scale, it is critically important the scaling of Irish SMEs may be of greater long-term

that Ireland provides a supportive environment value to the Irish economy.

for entrepreneurship throughout the life-cycle of The Government’s updated enterprise policy

a business, rather than merely during the start- includes a commitment to ‘strengthen the

up phase. Promotion of a start-up culture must competitiveness of Ireland’s tax regime to support

be combined with effective long-term rewards for start-ups, small and medium enterprises (SMEs)

entrepreneurs who choose to stay on and scale scaling.’48 However, Ireland’s competitive position is

their businesses rather than accept the allurement clearly wanting at present. In the UK, the effective

of a short-term reward by selling the firm. Ireland’s total tax rate on share dividends at the higher rate

present tax regime lacks this holistic and long-term is 32.5% compared with 52% in Ireland, a stark

approach. differential in the context of the Brexit.

Under the current system of incentives, divestment

is the only means by which entrepreneurs can

extract large-scale value from their firm in a manner

that is not subject to the full rate of income tax, as Recommendation

Entrepreneur Relief only applies to CGT on the value

of shares. Recent changes introduced by the Finance • Tax entrepreneurs at a lower rate of 30% on

Act 2017 have further increased the difficulty.47 income from share dividends to outmatch the UK

The result is an ‘inefficient incentive’ that drives offering ahead of Brexit.49 The qualifying criteria

successful businesspeople to ‘sell up’ rather that for this lower rate would be the same as those

stay on and grow their business further. While that apply to individuals and firms with respect

divestment is an appropriate and desirable outcome to Entrepreneurs Relief from Capital Gains Tax.

for serial entrepreneurs, for example, it should not

47 Finance Act 2017 introduced the new Section 135(3A), TCA 1997, as an anti-avoidance mechanism. In practice it serves to convert many genuine transactions

from distributions that are subject to CGT into distributions subject to income tax. E.g. management buyouts are a traditional mechanism to allow key stakehold-

ers to exit or retire from their businesses. But making these transactions subject to income tax undermines their attractiveness; it pushes businesses towards

sales to third parties or liquidation if a CGT exit is to be achieved.

48 Enterprise 2025 Renewed: Building resilience in the face of global challenges, p. ix, https://dbei.gov.ie/en/Publications/Publication-files/Enterprise-2025-Re-

newed.pdf#page=13

49 Revenue has tentatively estimated the total cost of a 30% income tax rate on dividend income from Irish resident companies (replacing all income tax, PRSI,

and USC currently collected) applied universally at €95 million. Restriction of the scheme to qualifying entrepreneurs would limit the cost to a fraction of this

figure. Dáil Éireann Debate Thursday 5 July 2018, Question No. 85, Reference No. 29775/18. Answered by the Minister for Finance Paschal Donohoe.

21 | Pre-Budget Submission Budget 2019Invest in Ireland’s Human Capital

Ireland’s people are its greatest resource. A large Table 7: GDA Businesses Experiencing

and skilled labour force will be crucial to facilitating Skills Shortages Q2 2018

business growth and maintaining international Are you currently looking for employees

competitiveness in the coming years. However, with a with a certain skillset, but having difficulty?

buoyant labour market approaching full employment,

and high accommodation costs in the GDA, the cost

and availability of skilled labour is a growing concern

for businesses. Whereas almost half (47%) of Dublin 37%

Chamber members were affected by skills shortages in (NO)

63%

Q4 2016, this proportion has risen to almost two thirds

(YES)

(63%) in Q2 2018.50 The range of affected sectors and

business functions presently includes financial services,

ICT, engineering, construction, tourism and hospitality,

international trading, and sales and marketing.

This challenge of access to skilled labour will continue

to mount in the context of strong economic growth.

The tightening supply of labour is already placing

upward pressure on wage costs, and making it diffi-

cult for SMEs to compete with larger firms for skilled

employees. As the OECD has recently noted, high Irish

labour costs threaten to slow business growth and

undermine economic competitiveness through infla-

tion.51 To maintain Ireland’s attractiveness as a location

for FDI and to support indigenous business growth,

Dublin Chamber recommends that the Government

take measures to attract, retain, and develop talent in

the Irish labour force.

50 Dublin Chamber Quarterly Business Trends Survey Q4 2016; Dublin Chamber Business Risk Outlook Q2 2018

51 OECD, Ireland Economic Forecast Summary, May 2018, https://www.oecd.org/eco/outlook/economic-forecast-summary-ireland-oecd-economic-outlook.pdf

22 | Pre-Budget Submission Budget 20191. Increase female labour market participation

While inward migration will continue to play a valuable other Northern European economies. It contrasts with

role in meeting business needs, population growth a differential of 2.7 percentage points in Sweden, 2.9

in the Greater Dublin Area carries its own challenges percentage points in Finland, 5.7 in Denmark, 6.7 in

in terms of managing overstretched infrastructure France, 7.7 in Germany, and 8.4 in Belgium, for example.53

and the inadequate housing stock. However, there is According to the latest figures, the differential in the

considerable untapped potential in the Irish labour force labour force participation rate between men and

that can be utilised without unnecessarily increasing women at all ages represents 254,500 women who are

pressure on the availability of accommodation through out of the labour force in Ireland.54

excess demographic growth. The room to expand There is clear evidence that Ireland’s gap in female

female labour force participation has been widely labour market participation is largely due to the burden

noted.52 of childrearing falling principally upon women in a

The female employment rate in Ireland is 10.4 context of high childcare costs.55 As Table 8 illustrates,

percentage points lower than the male rate. This the female rate of labour force participation diverges

gender gap is considerably higher than that in most sharply from the male rate around childbearing age

Table 8: Ireland: Labour Force participation rate by age group, 201656

52 E.g. ESRI Quarterly Economic Commentary Summer 2018, pp. 51-55, https://www.esri.ie/pubs/QEC2018SUM.pdf#page=62

53 CSO, Women and Men in Ireland 2016, Employment, Table 2.2, EU: Employment Rate 2016, https://www.cso.ie/en/releasesandpublications/ep/p-wamii/

womenandmeninireland2016/employment/

54 CSO, Labour Force Survey Q1 2018, Table 7 & Table 8, https://www.cso.ie/en/releasesandpublications/er/lfs/labourforcesurveyquarter12018/

55 Indecon Report on Support for Childcare for Working Families & Employment Implications, Nov 2013, pp.ii-iii

56 CSO, Women and Men in Ireland 2016, Employment, https://www.cso.ie/en/releasesandpublications/ep/p-wamii/womenandmeninireland2016/employment/

23 | Pre-Budget Submission Budget 2019and fails to catch up until retirement. The result is that to work by a second earner following withdrawal from

amongst people of typical childrearing age, there are the labour force on account of parenthood, taking

135,000 fewer women in the labour force than men.57 full account of childcare costs. Business feedback

Statistical evidence for the impact of childcare suggests that, as presently structured, the labour

affordability on the labour market is strongly supported taxation system (USC, PRSI and income tax) is serving

by business community feedback. Three quarters to discourage highly skilled people from returning to

(75%) of Dublin Chamber members now report that the workforce.

the cost of childcare has a material impact on their There are many variables affecting such situations,

business, affecting the cost and/or availability of and this topic requires comprehensive study at an

staff. Meanwhile, almost one in five Dublin Chamber official level. However, an initial exploratory analysis

members have specifically identified easing female by Dublin Chamber suggests that an individual who

labour market participation as the solution to helping withdraws from the labour force to give birth and/

them access the skills they require.58 or care for an infant may only add marginally to net

With this in mind, Dublin Chamber endorses family income by returning to work. It is clear that the

recent IMF advice that ‘attention should be given to attractiveness of returning to work, even at higher

providing affordable childcare, reducing high second- salary levels generally expected by skilled employees,

earner marginal tax rates, and eliminating gender pay is weakened by the structure of the tax system and the

gaps.’59 Dublin Chamber supports the commitment low level of childcare support currently available.

to ‘introduction of a robust model for subsidised This is confirmed by stark findings from the

high quality childcare’,60 and we welcome the Single European Commission. Ireland has the second highest

Affordable Childcare Scheme introduced by the participation tax rate (PTR) in the EU for potential

Department of Children & Youth Affairs last year as a female entrants to the labour force when out-of-pocket

first step. According to initial calculations, for 2018, childcare costs are taken into account.62 With a PTR of

the additional budget requirement for the Affordable 94% in such situations, Ireland is second only to the

Childcare Scheme (over and above the 2017 budget) UK in its penalisation of second earners with children.63

will be €44m.61 Dublin Chamber recommends a more

significant expansion of fiscal support for the new

Single Affordable Childcare Scheme in order to expedite

progress towards greater affordability.

Recommendations

There is no one solution to the childcare affordability • To ameliorate the childcare affordability problem

issue, however, and the Government must take a in 2019, double the maximum universal childcare

broader approach. Specifically, it must examine the subsidy under the Affordable Childcare Scheme

impact of the taxation system on the decision to return from €80 per month to €160 per month for a child

in full-time care before the start of ECCE, with

a commitment to commensurate progressive

increases in subsequent years. Cost: €19m64

57 Comparison of men and women aged 25-59, CSO, Labour Force Survey Q1

2018, Table 7, https://www.cso.ie/en/releasesandpublications/er/lfs/labour- • Consider improving the targeted subsidy element

forcesurveyquarter12018/ of the Affordable Childcare Scheme to better

58 Dublin Chamber Business Risk Outlook Q2 2018

59 IMF, Ireland Staff Concluding Statement of the 2018 Article IV Mission, reflect the net income of the second earner in a

May 2018 family (not just combined parental net income)

60 Programme for a Partnership Government

61 Department of Children & Youth Affairs, Policy Paper on the Development with a view to increasing labour force participation.

of a new Single Affordable Childcare Scheme, October 2016, p. 71 More broadly, and in the context of the proposals

62 The participation tax rate (PTR) is a means of measuring the level of

incentive or disincentive for labour market entry that is inherent in the tax and to reform income, PRSI and USC, undertake

benefit system. a thorough examination of how these taxes

63 European Commission, DG Justice, Secondary earners and fiscal policies

in Europe (Rastrigina & Verashchagina), 2015, p. 54, https://ec.europa.eu/ discourage ‘second earners’ from returning to the

info/sites/info/files/150511_secondary_earners_en.pdf#page=54 workforce, with a commitment to progressively

64 Department of Children & Youth Affairs calculation based on the forecast

cost of providing the universal childcare subsidy (CCSU) for the 2017/18 removing labour force participation barriers on the

programme year. July 2018. basis of the findings.

24 | Pre-Budget Submission Budget 2019You can also read