Property Market Update - Kelvin Davidson Senior Property Economist March 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Property Market Update Kelvin Davidson Senior Property Economist March 2021

Outline for today Recent economic & property data – momentum still strong What will happen in 2021? The year of property politics

Outline for today Recent economic & property data – momentum still strong What will happen in 2021? The year of property politics

Housing has got very political

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 3

Government announcement could be a line in the sand

Much tougher for mortgaged investors, but new-builds still a clear option

▪ SIGNIFICANT: Investors can’t offset interest against income anymore to lower tax – immediate for new buyers, phased

over next four years for existing – changes sums by $’000s per year

▪ LESS IMPORTANT: Brightline Test extended, FHB income and price caps raised, extra supply measures (Kainga Ora funding,

infrastructure development)

▪ Bottom line:

– Interest deductibility change looks out of synch with other business investments

– But whether it’s right or wrong, there were no ‘carrots’ for other investments

– Suspect investors generally continue to buy and hold property – just less profitable, and/or go new-build

– But still an impact - long-time landlords (with more equity) may buy off newer investors

– A near term psychology/perception shift too; Government relentlessly chasing property

– Electoral cycle; National could well campaign on reversing these changes

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 4

Sales volumes have been solid, but a slowdown is looming

Sales high again in February, driven by Auckland

But low listings could be a restraint, and some sales rushed to beat LVR changes

NZ sales volumes Change in sales in three months to February

compared to year ago

Source: CoreLogic

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 6

Total listings lifting, but still low

New weekly flows started slowly in 2021

NZ stock of existing listings on the market NZ weekly flow of new for-sale listings

Source: CoreLogic

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 7

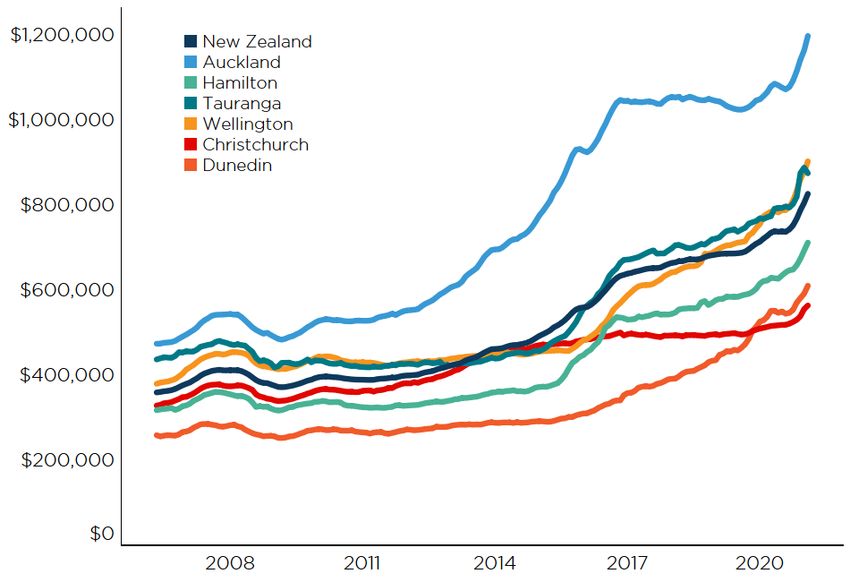

Property values have soared, on the back of tight supply/demand

Property values growing quickly again

15% rise in year to Feb - strong demand hitting up against low listings

Change in national average property values Average property values – main centres

Source: CoreLogic

18 July

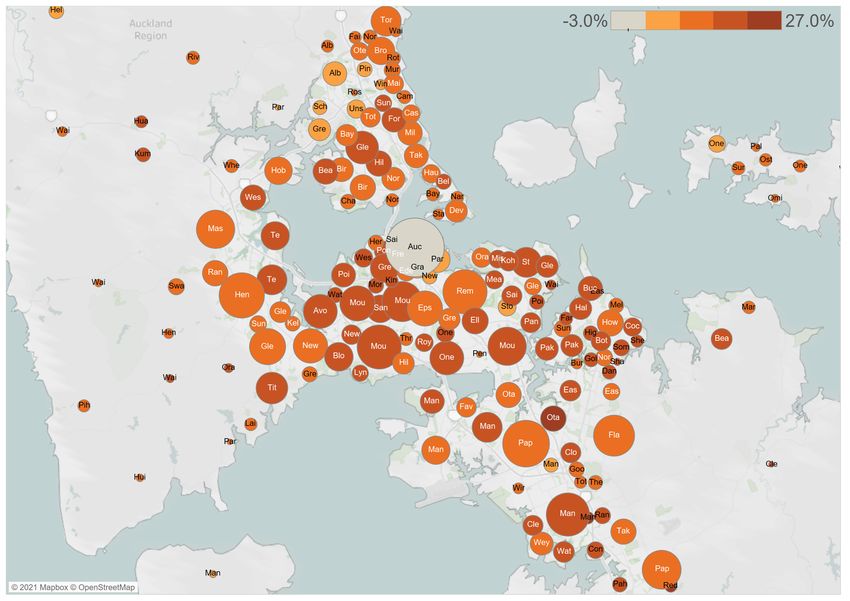

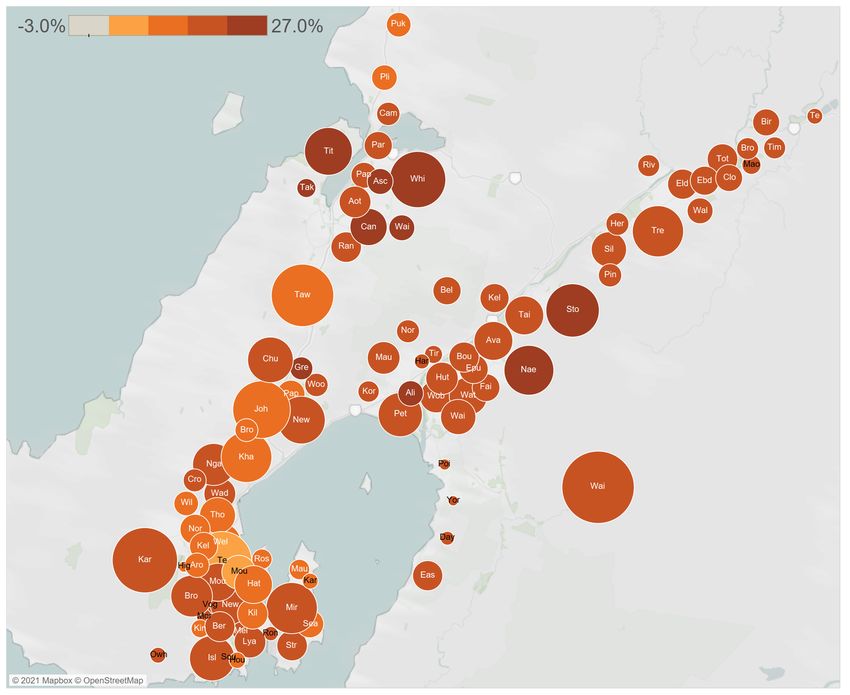

© 2019CoreLogic, Inc. All Rights Reserved. 9Broad-based upturn since lockdown

Suburb median value % change since March 2020

Auckland Wellington

18 July

© 2019CoreLogic, Inc. All Rights Reserved.

Source: CoreLogic 10Mortgaged investors active, but first home buyers waning?

Investors & FHBs not selling anything, movers sitting tight = listings issues

Buyer Classification Buyer Classification

New Zealand Auckland

Source: CoreLogic

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 11Strong contributor is of course low interest rates

Investors ‘searching for yield’ – LVR removal played a role too (but no more)

Lending to investors Breakdown of existing mortgage debt

50%

1,600 18% 46%

45%

1,400 16%

Investor $ flows >70% LVR (LHS)

40% Owner occupiers

High LVR investors % of total lending (RHS) 14%

1,200

35% Investors

12%

1,000

30%

10%

800 25%

8%

600 19%

20%

6% 16%

400 15%

4%

10%

200 10%

2% 5%

5% 3%

0 0%

Jan 2019 Jul 2019 Jan 2020 Jul 2020 Jan 2021 0%

Floating Fixed < 1 year Fixed > 1 year

Source: RBNZ

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 12Still many areas where housing ‘need’ has outpaced stock change

Hence we need high levels of dwelling consents to continue

Required extra housing minus stock change 2015-20

Source: CoreLogic

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 13It’s got political quickly

Some of the economic ‘headwinds’ are losing intensity

Unemployment rate fell from 5.3% to 4.9% in Q4 2020

NZ Activity Index and GDP Stocks and flows of mortgage

payment deferrals ($m)

10%

Annual % change 25,000 Weekly new applications

5% Total stock

20,000 Deferral exits

0%

15,000

-5%

NZ Activity Index (advanced 2 months) 10,000

-10% GDP

5,000

-15%

0

-20%

-5,000

-25%

Mar 2020 May 2020 Jul 2020 Sep 2020 Nov 2020 Jan 2021

2012 2014 2016 2018 2020

Source: RBNZ

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 15But the ownership ‘divide’ has got political quickly ….

‘Comfortable’ for existing owners, very hard for those saving a deposit

NZ: value to income ratio and NZ: years to save a deposit and rent to

mortgage payment affordability income ratio

8 70% 10 35%

9

7 60%

8 30%

6

50% 7

5 6 25%

40%

4 5

30% 4 20%

3

Value to income ratio (LHS) 3 Years to save a deposit (LHS)

20%

2 Value to income average Deposit years average

2 Rent to income ratio (RHS) 15%

Share of income required for repayments (RHS) More affordable 10%

1 1 Rent to income average

Repayments average More affordable

0 0% 0 10%

2004 2006 2008 2010 2012 2014 2016 2018 2020 2004 2006 2008 2010 2012 2014 2016 2018 2020

Source: CoreLogic

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 16…. hence the rules are tightening for investors

Interest-only loan restrictions could be next cab off the rank (May)

Interest only lending as % of Source: RBNZ % of new lending at debt to income ratio

stocks and flows greater than 5

50%

50%

45%

45% 42%

39% 40%

40%

35%

35%

30%

30%

25% First home buyers

25% 22%

20% Other owner occupiers

20%

15%

15% 13%

10%

10%

5%

5%

0%

0%

Jun 2017 Dec 2017 Jun 2018 Dec 2018 Jun 2019 Dec 2019 Jun 2020

Owner-occupier stock Owner-occupier flow Investor stock Investor flow

• Government emphasis is on equity – either to satisfy LVR requirements and/or reduce your interest

payments (so that deductibility is less of an issue anyway)

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 17Could rents rise? Maybe ….

But some tenants doing it hard, and income is still an anchor

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 18Near-term: ‘more of the same’ Second half of year: slowdown

2021 is already the ‘year of

property politics’

▪ Near-term momentum still upwards (tight

listings, low mortgage rates), but bear in mind

‘lost summer’ of tourism

Annual sales volumes (incl. forecast)

160,000 ▪ Some sales have been ‘brought forward’ - and

140,000

listings could restrain activity too

120,000

▪ So, with LVRs now also back in place, and

100,000

potential psychology effects of Government

80,000

measures, second half of the year may be

60,000

slower for sales, and price growth to cool too

40,000

20,000 ▪ Affordability is also a problem, and I-O lending

0 limits probably on the way

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

▪ ‘Real’ effects of Government measures (esp.

Source: CoreLogic interest deductibility) a slower-burner – might

change buyer mix, rather than drop prices

18 July

© 2019CoreLogic, Inc. All Rights Reserved. 20Let’s discuss Kelvin Davidson Senior Property Economist Kelvin.davidson@corelogic.co.nz @KDavidson_CL

You can also read