Quarterly Economic Bulletin - Volume 36 Q2 2017 - Association of Mortgage ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Quarterly Economic Bulletin Volume 36 Q2 2017

Executive Summary The UK’s economic fundamentals remain strong with inflation historically low, growth still in positive territory and a recovered pound, now impacted by electoral uncertainty Construction starts have picked up marginally – the new government must decide soon whether it plans to extend Help to Buy past 2020 to maintain confidence in new build Even if Brexit-fuelled uncertainty weighs on consumer spending and GDP in future, market expectations for medium term-interest rates remain low Consumer indebtedness is a growing concern and one the Bank of England must give full consideration to House price growth is likely to continue to stagnate this year and early next year The endemic lack of real income growth for the younger generation is becoming problematic, and if it persists, will likely pull house prices down over the medium to longer term despite the upward tug of net migration The switch from the Funding for Lending Scheme to the Term Funding Scheme puts the onus on lenders to increase net lending – it is this that has driven lenders to pay commissions on product transfer lending

AMI QUARTERLY ECONOMIC BULLETIN Volume 36 Q2 2017

Economic Overview

remains around 16 per cent below its peak

in November last year. The flipside of this

however, is that foreign investment into the UK

A

continues to look strong, with the Bank raising

lmost a year after the UK voted to its projection for business investment growth

leave the European Union, uncertainty in 2017 from earlier forecasts.

continues. The result of this month’s

general election will set the tone for how Wage growth is suffering however and has

Britain’s exit from the union is managed, and been exacerbated by rising inflation, which hit

could even throw yet more uncertainty into 2.6 per cent in April. Figures from the Office for

the mix should there be no clear majority and National Statistics revealed that earnings fell

therefore mandate to proceed. for the first time in three years in April, while

the Bank cut its forecast for average wage

This aside, the economic fundamentals growth in 2017 from 3 to 2 per cent. It expects

underpinning Britain’s stability remain real income growth to pick back up next year.

reasonably strong. In spite of slightly lower

growth than predicted in the first quarter – the All of this precludes what happens to market

second estimate of GDP was 0.2 per cent in the confidence as Brexit begins. The Bank of

first three months of the year – unemployment England has noted that ‘monetary policy cannot

is low, the pound had begun a recovery and, prevent either the necessary real adjustment

while rising, consumer price inflation remains as the UK moves towards its new international

at historically very low levels. Electoral trading arrangements or the weaker real

uncertainty has added new pressure to the income growth that is likely to accompany that

value of sterling as Theresa May is attacked adjustment over the next few years’.

from all sides by the range of opposition parties

emanating from all corners of the less than In other words, we may be in for a fairly rough

United Kingdom. ride between now and 2019 and even further

beyond.

Consumer spending is under pressure however,

perhaps in part a reflection of people opting It is now 10 years since the previous economic

to put off large purchases until the political cycle and the only certainty facing the UK is

outlook is clearer. Economists, notably Dr that its future is uncertain. AMI is of the belief

Andrew Sentence – a former Monetary Policy that the economy is likely to suffer over the

Committee member, have raised concerns next two or three years as Brexit negotiations

relating to rising household indebtedness. take place. But we do not think this will

Consumer spending has been driven in large cause significant damage to the housing and

part by cheap debt. Borrowing on credit mortgage markets, which remain governed by

cards and through personal loans has risen the significant imbalance between supply and

considerably; over the past five years, the UK demand. This in turn is also underpinned by low

has witnessed a £12billion surge in credit card interest rates making purchase and remortgage

borrowing alone. affordable for many.

The Bank of England is forecasting that the The potential for rising interest rates is also

recent slowdown in consumer spending will low, particularly given the view held by the

continue in the medium-term, driven by a Monetary Policy Committee last month

weaker pound. In spite of a general uptick when it confirmed that under ‘exceptional

in Sterling’s value since February, the pound circumstances the Committee must balance

AMI QUARTERLY ECONOMIC BULLETIN Volume 36 Q2 2017

any trade-off between the speed at which it

intends to return inflation sustainably to the

House Prices and

target [of 2 per cent] and the support that

monetary policy provides to jobs and activity’. Construction

Q

This seems as close as the Bank is willing to uarterly output in the construction

go to suggesting that very low interest rates industry grew for the fifth consecutive

are here to stay for the medium term at least. period, rising by 0.2 per cent in the

Markets appear to trust that the Bank remains first quarter of 2017. Within these figures,

reluctant to raise rates, and measures of new housing completions were up significantly

financial market uncertainty are consequently in March, rising month-on-month by 3.8 per

low. Equity markets are also performing cent andSection up 5.4 per cent

1 Global economicon the year before.

and financial market developments

strongly, with the FTSE and S&P indices trading This is a positive picture but there are already

near all-time highs, fuelled by Sterling’s relative signs that output may be slowing back down.

weakness and the shunt this gives to larger Whether this is a temporary lull ahead of

corporate profitability. the14general election remains to be seen but In

Chart 1.5 Measures of financial market uncertainty are in its aftermath,

goods. Annual Government world export must focus on

price inflation excluding oil is

CHART: Measures of financial market uncertainty are low

low delivering the newto

estimated homeshave risen promised sharply byoverevery the past year, to 2.4%

Implied volatilities for US and euro-area equity prices party. 2017 Q1 (Table 1.B). That will push up UK import price

Differences from averages since 2002 (number of standard deviations) inflation (Section 4), as will the past fall in sterling.

2.5

CHART: Housing starts picked up sharply in 2016 H2 B

S&P 500 (VIX)(a) February Report Chart 2.7 Housing starts picked up sharply in 2016 H2

2.0 Housing starts(a) d

Euro Stoxx (V2X)(b)

1.1 The euroThousands areaper quarter (annualised) co

1.5 240

e

1.0 As the United Kingdom’s largest trading 200

partner, w

0.5

developments in the euro-area economy are important for sh

+ UK growth. Quarterly euro-area GDP growth 160 was stable m

a

0.0

– 0.5% in Q1 (Table 1.A). That was as expected in Februarym

0.5 (Table 1.C), and slightly higher than average 120 su

growth in rece

years. o

1.0

Inflation Report May 2017 80 T

1.5 e

2014 15 16 17 The recovery in euro-area growth in recent 40 years has narrotr

Source: Bank of England

Sources: Bloomberg and Bank calculations. the degree of slack in the economy. The unemployment ra re

0

2004 has 06 continued to fall12steadily 14 reaching 9.5% in March, arou

(a) VIX measure of 30-day implied volatility of the S&P 500 equity index.

08 10 16

(b) V2X measure of 30-day implied volatility of the Euro Stoxx equity index.

s CHART: Financial market prices imply that UK interest rates will stay

Chart A Financial market prices imply that UK interest Source: Bank

Sources: 2 ofpercentage

England

Department for Communitiespoints

and Local above

Governmentitsand Bank calculations. low (Chart 1.10). Im

2007–08

low for some time

rates

Chartwill

1.6stay

Thelow for some timepath for UK short-term

market-implied (a) NumberDespite

of permanent that,

dwellings four-quarter wage

in the United Kingdom started growth

by private remained

enterprises up to well belo

E

2016 UK real policy

interest ratesrate

hasand financial market estimates of expected

fallen The Conservatives

private its pastin England.

enterprises averagehave

Data are promised

rate 1.5%toinmeet

2016 Q2. Data for Q3 and Q4 have been grown in line with permanent dwelling starts by

at adjusted.

seasonally Q4. While weak productivi v

es have short-term real

International interestinterest

forward rates ten years

rates(a) ahead their 2015 commitment to deliver a million

growth (Chart 1.9) is likely to have weighed on wage growU

nomies. Per Per

centcent

7 2.0

homes bydegree the end of 2020

of spare have appears

capacity claimedtothey persist. a

al

Solid lines: May Report

6 willChart

deliver 2.8halfSurveys a million

point to morea pickupby the end growth

in export of th

Dashed lines: February Report Unitedof States

2022. Labour meanwhile is promising to build

Range model-based

estimates for UK 5 1.5 in 2017 p

icy

expected real interest

rates ten years ahead(a) 4 at least

UK exportsaDespite

million

and surveythe

new weakness

homesof and

indicators in euro-area

export boost

growth(a) the wage growth, core infla

b

3 1.0 provisionhas of risen

socialinhousing

recentPercentage

months

bothchanges toon1.2%

through in April (Table 1.B). Mu

local

a year earlier

t rates 20

The Average(a)

Federal funds rate(b) United Kingdom 2 councils of and thathousing associations.

rise is likely to have been To doerratic,this, however, reflectin C

BCC

a Labourthe Government would build 100,000

15

Bank Rate 1

+ 0.5

timing of the Easter holidays relative to 2016. Core T

flation 0

– + new social homesisaprojected

inflation year andto shelve

fall CBI theinTory

back May. 10 fl

ecline.

policy of Right to Buy. Both parties’ targets 5

ECB main refinancing rate 1

0.0 th

the

are unrealistic andconditions

impractical. Annual new remain

2

–

over UK real policy rate(b) Euro area

3 Financial in the euro area + supportive ofQ

ECB deposit rate 0.5 build dwelling growth. starts in 2016 by

As expected totalled 153,370. 0

e

pital 4 Exportsmarket

(b) contacts, – the European

During the same period, completions totalled 5

est rates

5 Central Bank (ECB) Markit/CIPSmade no changes to monetary policy re a

1993 95

2013

97

14

99 2001 03

15 16

05 07

17

09 11

18

13 15

19

17

20

1.0

140,660, a decrease of 1 per cent compared Agents e

ment and March and April meetings. As announced 10 in December 201

Source: Bank

Sources:

Sources: Bankof England

Bloomberg, Consensus Economics, HM Treasury, ONS and Bank calculations.

of England, Bloomberg, European Central Bank (ECB) and Federal Reserve. with 2015. d

reasing (a) End-month data to March 2017. The swathe shows estimates from four models. Three of the ECB EEF reduced its rate of asset purchases 15

from €80 billio

(a) the

Themodels

May 2017 and February

estimate 2017policy

the nominal curvesrate,

are estimated using instantaneous

and are adjusted forward overnight

for inflation expectations; T

index

one swapjointly

model rates in the fifteen

estimates working

nominal anddays

real to 3 Mayrates

interest and 25 January

using 2017 respectively.

RPI inflation. Nominal per month to €60 billion in April, and intends to continue

(b) interest

Upper bound of the

rates are target range.

zero-coupon ten-year forward rates derived from UK government bond 20 in

2007 these 09 purchases 11 until13 December 15 2017.17 The market-implied

prices. Inflation expectations estimates are for inflation five to ten years ahead from the

half-yearly Consensus survey, and are assumed constant in the intervening months. They are

n

but is of Chart 1.7 Equity prices have risen further globally

based on RPI inflation until 2005 and CPI inflation thereafter; prior to 2005, the estimates path

Sources: Bank for BCC,

of England, short-term interest

CBI, EEF, IHS Markit, ONS and Bankrates (Chart 1.6) and longer-te

calculations.

e

are adjusted by the difference between RPI and CPI inflation. Expected policy rates are

ttee International equity

derived by stripping out termprices (a)

premia estimated using the following four models: the government

(a) BCC measure bond

is the net percentage balanceyields (Chart

of manufacturing 1.4)companies

and service have fluctuated, howe d

benchmark model in Malik, S and Meldrum, A (2014), ‘Evaluating the robustness of UK term reporting that export orders and deliveries increased on the quarter; data are non seasonally

5 April, adjusted. CBI measure is the average of the net percentage balance of manufacturingthird of the 405,000 homes built since 2013 – 112,000 – have been bought by families

under Help to Buy. Arguably this is a higher proportion than we will see over the next

three years given that lenders have recovered their independent appetite to lend up to 95

per cent loan-to-value. However, the value the scheme offers is as a safety net for

AMI QUARTERLY ECONOMIC BULLETIN Volume 36 Q2 2017

builders deciding whether to deliver more or fewer new homes.

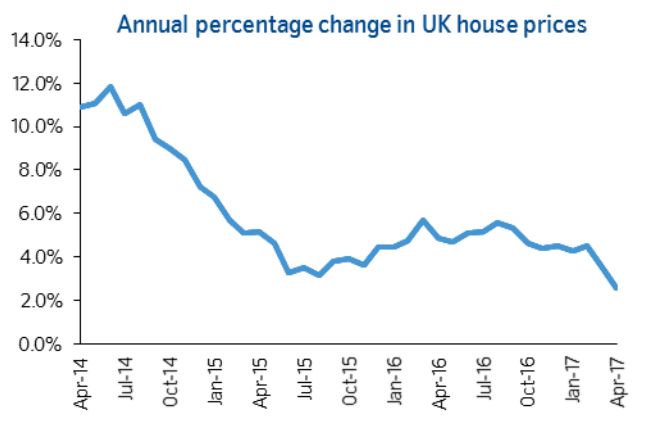

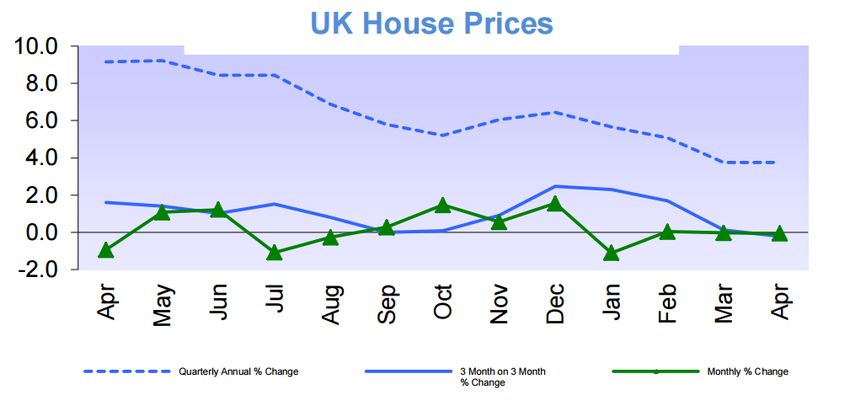

This is particularly important in light of recent data on house prices and activity in the

sales market. The latest numbers from the National Association of Estate Agents show the

number of house-hunters registered per estate agent branch fell to 381 in April. In March

there were 397 per branch, down from 425 in January and February. Supply also fell in

April. In March there were 39 properties available to buy per branch but in April this figure

dropped 8 per cent to 36 per branch. This is the lowest level seen since April 2016 when

agents had just 35 properties to market ahead of the referendum on leaving the European

Union.

CHART: Nationwide house price index CHART: Halifax house price index

CHART: Nationwide house price index

Source: Halifax

Source: Halifax

This may be a similar dip ahead of the general election, but given that this was announced

only recently, it is also possible that we are seeing the beginning of a wider slowdown in

the housing market. This is reflected in property prices. Both Halifax and Nationwide are

Source: Nationwide

Source: Nationwide now recording monthly falls in the average house price, with the Halifax index suggesting

that the average home is now £3,000 below its peak value, reached in December last year.

CHART: Halifax house price index London is suffering more than other areas in the country, but experience suggests that this

Delivering new homes to Britain is critical and branch. This is the lowest level seen

effect will ripple out more widely over the course of the year.

high targets are laudable but Governments since Aprilmonthly

consecutive 2016 when

fall in agents

April. RICS hadsuggests

data meanwhile just that

35buyer demand has

Mortgage lending is also subdued, with Bank of England approvals showing a third

must be practical on how they plan to achieve properties to market

indicates that mortgage approvalsahead

may remain oflacklustre

the referendum

now been stagnant or falling for five months, which chimes with the Bank’s data and

in the coming months. Buy-to-let

them. Part and parcel with this will be the Help onistreatment,

leaving the European having Union.

an effect onThis

propertymayvalues.be a

also significantly down on a year ago following the various changes to landlord tax

which is undoubtedly

to Buy equity loan scheme, which is currently similar

That said, dip

a fallahead

in propertyof the

prices general

is not likely to beelection,

severe and could but

serve to boost buyer

scheduled to close in 2020. Labour has said given that thisatwas announced only recently,

interest. It does however underline how important the Help to Buy scheme is in supporting

lenders’ confidence the higher end of the LTV scale.

it will extend this to 2027 if elected; it seems it is also Credit

Consumer possible that we are seeing the

sensible to consider an extension under a beginning

Following multipleof ahighwider slowdown

profile warnings in thedebt,

over rising consumer housing

the Financial Conduct

Authority has said it will review the sector. This covers credit cards, personal and

Conservative Government as well. market.

unsecured loans and car finance, the latter of which has ballooned in recent years with

the popularity of personal contract plans.

The latest figures from the Bank of England show that while borrowing against our homes

Builders are responsible for delivering the This is reflected

is falling back, unsecuredin property

borrowing continuesprices. Both

to grow quickly. AprilHalifax

saw consumer credit

grow £1.5 billion, pushing the annual growth rate up from 10.2 per cent to 10.3 per cent.

new homes promised by politicians and they andThis Nationwide are now recording monthlycent in March to

was largely driven by an uptick in credit card lending from 8.9 per

9.7 in per cent in April, the strongest rate since March 2006. In April the Financial Policy

are motivated by profit margin. Help to Buy falls in the

Committee average

warned housein consumer

that this explosion price,debt with thefinancial stability at

is putting

risk. Not only is the risk of arrears on consumer credit higher than in the mortgage sector,

provides them with much needed certainty Halifax

these loans index

are also suggesting

being securitised andthat

sold onthe average

to other home

investors. Indeed,

headlines in the national press have begun drawing comparisons between sub-prime car

recent

at a time when there is little else that can be is now £3,000 below its peak value, reached in

loan contagion in the US and the credit crunch in 2007.

relied upon. The figures bear this out - almost December last year. London is suffering more

a third of the 405,000 homes built since 2013 than other areas in the country, but experience

– 112,000 – have been bought by families suggests that this effect will ripple out more

under Help to Buy. Arguably this is a higher widely over the course of the year.

proportion than we will see over the next

three years given that lenders have recovered Mortgage lending is also subdued, with Bank of

their independent appetite to lend up to 95 England approvals showing a third consecutive

per cent loan-to-value. However, the value the monthly fall in April. RICS data meanwhile

scheme offers is as a safety net for builders suggests that buyer demand has now been

deciding whether to deliver more or fewer new stagnant or falling for five months, which

homes. chimes with the Bank’s data and indicates that

mortgage approvals may remain lacklustre

This is particularly important in light of recent in the coming months. Buy-to-let is also

data on house prices and activity in the sales significantly down on a year ago following the

market. The latest numbers from the National various changes to landlord tax treatment,

Association of Estate Agents show the number which is undoubtedly having an effect on

of house-hunters registered per estate agent property values.

branch fell to 381 in April. In March there were

397 per branch, down from 425 in January and That said, a fall in property prices is not

February. likely to be severe and could serve to boost

buyer interest. It does however underline

Supply also fell in April. In March there were 39 how important the Help to Buy scheme is in

properties available to buy per branch but in supporting lenders’ confidence at the higher

April this figure dropped 8 per cent to 36 per end of the LTV scale.Table 2.C Household borrowing conditions have eased in recent

AMI QUARTERLY ECONOMIC BULLETIN

years Volume 36 Q2 2017

Average interest rates on household lending and other terms on credit card

lending

Monthly averages

Consumer Credit

Table 2.C Household borrowing conditions have eased in recent

TABLE: Household borrowing conditions

2005– have eased

2009– in recent

2013– years 2017

2016 2017

years

08 12 15 Q1 April

Average interest rates on household lending and other terms on credit card

F

lendingrates (per cent)(a)

Interest

ollowing multiple high profile warnings Two-year fixed-rate Monthly averages

over rising consumer debt, the Financial mortgage (75% LTV)

2005–

5.4

2009–

3.7 2.3

2013– 2016

1.7

2017

1.4

2017

1.4

Conduct Authority has said it will review Two-year fixed-rate

mortgage (90% LTV)

08

n.a.

12

6.0

15

4.1 2.6

Q1

2.5

April

2.5

the sector. This covers credit cards, personal Interestunsecured

£10,000 rates (per cent)

loan

(a)

7.8 9.0 5.3 4.1 3.7 3.7

and unsecured loans and car finance, the latter Two-year fixed-rate

£5,000 unsecured loan 10.0 12.7

mortgage (75% LTV) 5.4 3.7 2.39.7 1.79.2 1.49.3 1.4 9.5

of which has ballooned in recent years with the

Two-year fixed-rate

popularity of personal contract plans. Other terms

mortgage (90% LTV) n.a. 6.0 4.1 2.6 2.5 2.5

Average 0% balance transfer

£10,000

term unsecured

(months)(b) loan 7.8

8.2 9.0

12.4 5.3

19.6 4.1

25.7 3.7

29.6 3.7 n.a.

The latest figures from the Bank of England £5,000 unsecured loan

Average balance transfer

10.0 12.7 9.7 9.2 9.3 9.5

show that while borrowing against our homes fee (per cent)(b)

Other terms

2.4 3.0 3.1 2.7 2.7 n.a.

is falling back, unsecured borrowing continues Average 0% balance transfer

to grow quickly. April saw consumer credit

Sources: Moneyfacts(b)

Group and Bank calculations.

term (months) 8.2 12.4 19.6 25.7 29.6 n.a.

grow £1.5 billion, pushing the annual growth (a)Average

The Bank’s

financial

quotedtransfer

balance interest rate series are currently compiled using data from up to 19 UK monetary

fee (per institutions

cent)(b) (MFIs). Data are non 2.4seasonally

3.0adjusted. 3.1

Sterling-only

2.7end-month

2.7quoted rates.

n.a.

rate up from 10.2 per cent to 10.3 per cent. (b) The average 0% balance transfer term is the average of each lender’s maximum 0% balance transfer term

available. The average balance transfer fee applies to products with these terms. Longer transfer terms and

This was largely driven by an uptick in credit Source:

lowerBank

Sources: fees of England

imply

Moneyfacts easier

Groupcredit conditions.

and Bank Whole market data, excluding values of zero. End-month data.

calculations.

card lending from 8.9 per cent in March to 9.7 (a) The Bank’s quoted interest rate series are currently compiled using data from up to 19 UK monetary

CHART: Household

financial lending

institutions (MFIs). Datagrowth has slowed

are non seasonally slightly

adjusted. Sterling-only end-month quoted rates.

in per cent in April, the strongest rate since Chart 2.5 0%

(b) The average Household lending

balance transfer term growth

is the average has maximum

of each lender’s slowed0%slightly

balance transfer term

March 2006.

available. The average balance transfer fee applies to products with these terms. Longer transfer terms and

(a)

Household borrowing

lower fees imply easier credit conditions. Whole market data, excluding values of zero. End-month data.

Percentage changes on a year earlier

20

In April the Financial Policy Committee warned Chart 2.5 Household lending growth has slowed slightly

that this explosion in consumer debt is putting Household borrowing(a)

15

financial stability at risk. Not only is the risk of Secured lending to

Percentage changes on a year earlier

individuals 20

arrears on consumer credit higher than in the 10

mortgage sector, these loans are also being Consumer

credit

15

Secured lending to

securitised and sold on to other investors. individuals 5

Indeed, recent headlines in the national press 10 +

Consumer

have begun drawing comparisons between credit

0

5–

sub-prime car loan contagion in the US and the + 5

credit crunch in 2007. 0

– 10

Concern is mounting that the underwriting 2000 02 04 06 08 10 12 14 16 5

standards applied to consumer lending are (a) Monthly data. Sterling net lending by UK MFIs and other lenders. Consumer credit consists

of credit card lending and other unsecured lending (other loans and advances) and excludes

insufficient. This is particularly worrisome given

10

2000 loans.

student 02 04 06 08 10 12 14 16

the introduction of clear affordability rules on Source: Bankdata.

(a) Monthly of England

Sterling net lending by UK MFIs and other lenders. Consumer credit consists

mortgage lending in 2014 under the Mortgage Chart

of credit card lending and other unsecured lending (other loans and advances) and excludes

2.6

student loans.House price inflation has slowed but housing

Market Review and the subsequent inclusion market activity has been broadly stable

of consumer credit lending into the FCA’s House

Chartprices and mortgage

2.6 House approvalshas

price inflation forslowed

house purchase

but housing

regulatory remit in 2014. forms

market of activity

debt

Three-month overhas the

on three-month beenlong term

broadly may reflect

stable

both stricter affordability

annualised percentage change

30House prices and criteria

mortgage approvals from lenders 140

Thousands per month

for house purchase

It is clear that the affordability standards on mortgage borrowing and a decade of little

Three-month on three-month

Mortgage approvals

required of mortgage lenders are not being to2030no real wage growth.

annualised percentage change Thousands per month 120

for house purchase 140

(a)

House prices

applied in the sale of personal and car loans, Mortgage approvals 120100

PCP and credit cards. If the philosophy that This is particularly

1020

House prices(a) acute for theforyounger

house purchase

and

sits behind the MMR rules on affordability has still

+

working generations whose incomes have100 80

010

taught the market anything, it must be that not+ been protected by the Government’s triple 80 60

–

credit scoring in isolation is an insufficient lock

10

0 on the state pension. The endemic lack of

measure of whether a consumer is able to real– income growth for the younger generation 60 40

afford to repay debt. is20becoming problematic, and if it persists, will40 20

10

likely pull house prices down over the medium

20

Increasing reliance on short-term, expensive to30longer

2004

term.

08 12 16 2004 08 12 16

20

0

30 0

Sources:2004

Bank of08

England,12

IHS Markit,

16 Nationwide

2004and Bank

08 calculations.

12 16

(a)Sources:

AverageBank

of the Halifax/Markit

of England, and Nationwide

IHS Markit, Nationwideand

house

Bankprice series.

calculations.

(a) Average of the Halifax/Markit and Nationwide house price series.be subject to revision, including those recently announced by current spending decisions; nonetheless they m

the ONS as partAMI QUARTERLY

of Blue Book 2017ECONOMIC spending

BULLETIN Volume

described below. 36 inQ2

the2017

long run, for example when pe

Over 2016, much of the fall in the aggregate sa

Chart A The household saving ratio has fallen driven by falls in non-labour income. In particu

Product Transfers

CHART: The household

Household saving

saving ratio (a) ratio has fallen

income earned on behalf of households by pen

Per cent

18 insurance companies fell sharply in Q4. By con

C

16 of labour

onsiderable noise hasandbeen

benefit

madeincome increased slightly

14 followinggenerally,

the decisionsoverbythe

multiple

past two decades, labour an

12 lenders to start paying

income procuration

has risen fees

relative to consumption, whil

Chart 3: Buyer Enquiries less Sales Instructions & House Prices on product transfers. This move is the right one

10 total household income to consumption has fa

50 80 6

in our view, but it is vital that in celebrating it

40 In other words, it is changes in non-labour inco

60 8

4 we do not give the incorrect impression that

Chart

40 3: Buyer Enquiries less Sales Instructions & House Prices

commission in driven

any waythe saving ratio lower over this period.

30

6 influences the advice

2050 80 6 2

1040

20 given to customers.

below, It has been suggested

forthcoming thatas part of Blue Bo

revisions

60 4

0 30

0

4 0 brokers withheld applications from certain

likely to mean that the saving ratio has fallen b

40

-10

20

-20 2

lenders in protest against

current their

data previous

suggest.

20 2

-20

10

-40

RICS New Buyer Enquiries less 0

-2 refusal to pay proc fees on transfers but this is

01963

categorically not the case.

73 83 93 2003 13

0

-30 -60 Seller Instructions (Adv. 5m, LHS) 0

-20 -4

-10

-40 -80 Nationwide

(a) Saving as a percentage of household post-tax income. house prices (% Forthcoming changes in Blue Book 2017

-40 3m/3m, RHS) -2

-20

-50 -100

Source:

-60 05 Bank

AMI is of the view

The that

ONSlenders

RICS New Buyer Enquiries less in fact chose

has announced -6 changes to the measu

-30 06 of07 England

08 09 10 11Seller 12 Instructions

13 14 (Adv.15 5m,

16 LHS)

17

-80

to begin payinghousehold

a fair reflection

Nationwide house prices (%

-4

incomeof the value

ahead of Blue Book 2017. Th

-40

Accounting for changes in the saving ratio created

3m/3m, RHS) by brokers on this business as a result

-50 CHART:

-100 Breakdown

Chart of consumer

5: Breakdown of credit

-6

Consumer Credit (% y/y) to have substantial implications for the aggreg

of an entirely different reason.

The majority of income for many households comes from

05 06 07 08 09 10 11 12 13 14 15 16 17

2.0 15 15 saving ratio.(1) Provisional estimates suggest th

wages, salaries or self-employment

Credit Cards income. Total labour

1.8

Chart 5: Breakdown of Consumer Credit

Personal loans (% y/y) ratio

The Funding for will be

Lending revised

Scheme up by 0.8 percentage point

brought

1.6 income, after taxes, currently accounts for a little over half of

2.0

1.4

10

15 1510 in during 2012between

operates 1997

on a fairly

and 2012 (Chart C). The size of

1.8 total household income asCredit Cards

measured by the ONS. straightforward asset for gilts swap between

1.2 Personal loans

1.6

1.0 5

10 105 lenders and the Bank of England. After several

1.4

0.8

1.2

Other people receive a substantial proportion of theirextensions

income of the funding

(1) For facility

more details, by the Bank,

see www.ons.gov.uk/economy/nationalaccou

articles/nationalaccountsarticles/impactofbluebook2017chang

0.6

1.0 from

05

lenders

government benefits or private pensions,5 0which togetherare now facing the liquidity drip being

financialaccounts1997to2012.

0.4

0.8 turned off after January 2018.

0.2

0.6 The scheme is gradually to be replaced with

0.0 -50 0 -5

0.4

06 07 08 09 10 11 12 13 14 15 16 17 the new Term Funding Scheme, introduced in

0.2

August last year, which allows banks to borrow

0.0 -5 -5

Source: Capital Economics

06 07 08 09 10 11 12 13 14 15 16 17 against their assets at very low rates from the

Chart 7: Unsecured Debt as % of Disposable Income

Bank of England. There is a catch with the new

22

20 CHART:

32

ChartUnsecured debt asDebt

7: Unsecured % of disposable income

as % of Disposable Income

32 scheme: unlike the FLS, the TFS puts the onus

18

1622 30 30

on lenders to increase net lending in order

1420

32 32

to benefit from the Bank of England’s cheap

1218

1016

28

30 30 28 borrowing rates.

8 14

6 12 26

28 28 26

4 10 The uptake figures are revealing. At the end

28

06

24

26 26 24 of 2016 just one lender – Aldermore – had

4

-2

2

-40 22

24 24 22 used the TFS while loans made by the Bank of

-6-2 England through the FLS rose to £60.8 billion

-8-4

-6

22

20

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

22 20

at the end of September. The latest figures

-8 20 20 show that uptake of the TFS is now rising – by

8 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

the last quarter of 2016, £20.6 billion was

e) Chart 9: Earnings & Inflation

borrowed by 21 lenders. In the first three

me)10 Source:

7 Capital Economics

Chart 9: Earnings &% Inflation 7

Average earnings (ex. bonuses, y/y of 3m. ave.) months of this year, it was up again, with a

9

10 67 CPI Inflation (% y/y of 3m. Ave.)

Average earnings (ex. bonuses, % y/y of 3m. ave.) Forecasts7 6 further £34.4 billion borrowed, bringing 28

8

9

78

56 CPI Inflation (% y/y of 3m. Ave.) Forecasts 6 5 lenders into the scheme with total borrowings

67 45 5 4 of £55.1bn.

56 34 4 3

45

23 3 2 Lenders must factor in this need to

34

12 2 1 demonstrate an increase in net lending in a

23

12 01 1 0

01 0 0

-1 -1

0 -1 07 08 09 10 11 12 13 14 15 16 17 18 19 20-1

07 08 09 10 11 12 13 14 15 16 17 18 19 20

Sources – Thomson Datastream, Bank of England, GfK, RICS

Sources – Thomson Datastream, Bank of England, GfK, RICSAMI QUARTERLY ECONOMIC BULLETIN Volume 36 Q2 2017

market where new lending remains subdued by pressure on competition. Lenders choosing

the uncertainty surrounding Brexit and ongoing to pay brokers a product transfer commission

affordability constraints for borrowers. is related to this changing landscape where

there is less incentive for brokers to actively

By AMI’s estimation, the product transfer woo existing borrowers away from their

market was anywhere between £80 billion lender’s retention deals to other more suitable

and £100 billion gross lending last year. In providers. It also fairly reflects the fact that

the context of a market that is £240 billion or where borrowers do choose to remain with

thereabouts, this section of lending is critical their existing lender, often they have discussed

if lenders are to grow net lending. They must this with their broker who has spent time

retain borrowers on their books as well as comparing retention deals with the wider

attract new customers, putting even more market to ensure it’s the best option.You can also read