Regulation of Power Sector in Singapore: Development and Current Practices

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Regulation of Power Sector in Singapore:

Development and Current Practices

Youngho Chang

School of Business

Singapore University of Social Sciences

13 December 2017

The 11th Capacity Building for

Officers of Electricity Regulatory Commissions

13 – 15 December 2017

Holiday Inn Orchard City Centre, Singapore

World at Night from Satellite

2

Agenda

• Descriptive statistics on electricity

• Why regulate the power sector

– Natural monopoly and social losses

– Social optimum in a natural monopoly market

– Rate of return regulation

• Models for restructuring the electricity sector

• Regulation of the power sector in Singapore

– Milestones, regulatory framework, industry structure and players

– Market power, measures and tests

– Vesting contracts

• Game-theoretic approach based on the Cournot Model

• Controlling market power and effectiveness

• Regulatory Sandbox

• Open Electricity Market

3

Electricity Consumption per Capita (kWh) in 2009

14000

12000

10000

8000

6000

4000

2000

0

Source: World Bank (2012) 4

Electricity Consumption per Capita

by Region in 2009 (kWh)

Region Consumption

Arab World 2,154.8

East Asia and Pacific 2,797.4

Euro Area 6,588.7

European Union 6,063.6

Latin America and Caribbean 1,901.2

Middle East and North Africa 2,445.2

North America 13,167.1

OECD 7.981.8

South Asia 516.9

Sub Saharan Africa 517.4

World 2,806.9

Source: World Bank (2012) 5

World Population Without Electricity

(Millions of People)

Rural Urban

S.

America 38 7

North

Africa-

Middle

East 30 17

Sub-

Sahara

Africa 438 109

S. Asia 580 126

S.E. Asia 182 41

Worldwide 1.3 billion continue to live without access to electricity.

Total 1,268 300 This is equivalent to 18% of the global population;

22% of those living in developing countries (IEA, 2014)

Source: World Energy Outlook 2006 (IEA) 6

Why Does Economics Concern

Power Supply?

• Motivations

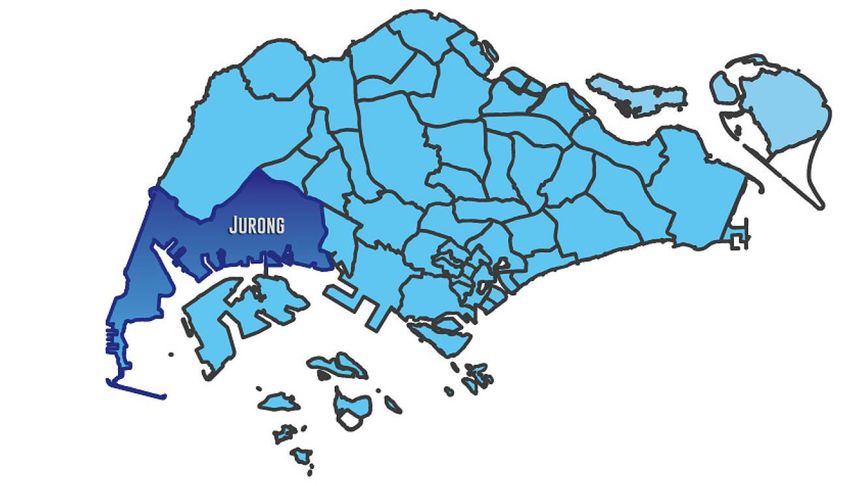

– Cost structure is rather unique

– Continuity requirement in power supply

– Efficiency

• Generation technologies and cost structures

– Long-Run Marginal Cost (LRMC)

• Fixed and variable costs

– Short-Run Marginal Cost (SRMC)

• Variable costs or avoidable costs

7Various Cost Structures of Firms TC = FC + VC(Q) 8

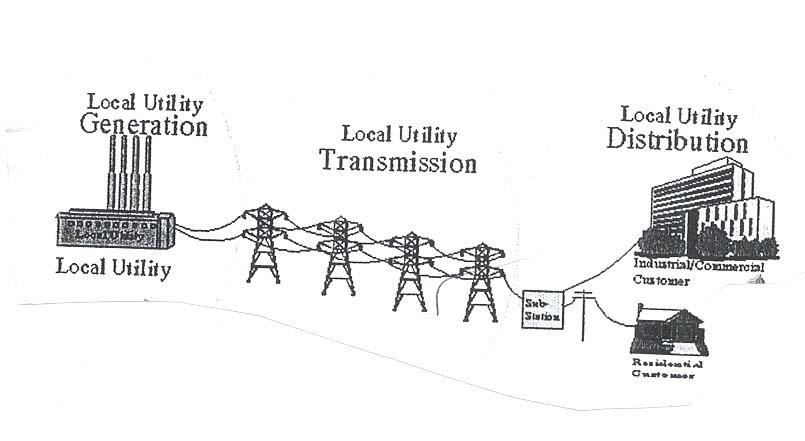

Electricity Generation, Transmission and

Distribution: A Schematic Diagram

9Inverse Demand and Cost Curves

in a Decreasing Cost Industry

10Monopoly Production, Price and Profit

Objective: Maximize Profits

P = 75 – 4Q

TC = 19Q – 0.25Q2

ATC = 19 – 0.25Q

MC = 19 – 0.5Q

TR = P*Q = 75Q – 4Q2

MR = 75 – 8Q

Profit (πm) = (Pm – ACm)*Qm

11Social Losses from Monopoly: Illustration

12Social Optimum in a Natural Monopoly Market

Objective: Maximize Social Welfare

Social Optimum: P(Q) – MC(Q) = 0

13Government Policy for a Natural Monopoly

• Rate of Return Regulation

– The utility is allowed to earn a normal rate of return on

their capital stock or their rate base (RB)

– The accounting equation

n

PQ

i 1

i i expenses s( RB )

where Pi the price of the i - th service class

Qi the quantity of the i - th service class

n the number of service classes

s the allowable of " fair" rate of return

RB the rate base of the regulated firm' s investment

14Merit Order by Marginal Running Cost

15Generating Costs

D'

D

16Structures of Electricity Market

• Under regulation

– Vertically integrated, mostly government owned,

natural monopoly

– Instruments for regulation

• Price and quantity

• Under deregulation

– Separation of industry by ownership

– Horizontally unbundled

• Full competition in generation and wholesale/retail

• Still monopoly in transmission and distribution (T&D)

• Motivations for unbundling?

17In a Deregulated Electricity Market

• Market becomes competitive

– Non-existence (or little abuse) of market power

– Easy entry and exit of players

– Efficiency of allocation and lower and/or stable prices

• Market functions properly

– Informed decisions

– Allocation of risk

– Transactions at minimal cost and lower production costs

• Market leads close to marginal-cost pricing

– Prices would be close to the marginal cost under workable

competition and a reasonably well-functioning market

environment

• What do we expect?

– Right and Stable Prices

– Competition and Reliability

18Models for the Electricity Sector

• Model 1

– No competition, vertically integrated, publicly or privately owned

• Model 2

– Model 1 but with competition in generation. A single buyer (a

distribution company) may buy from a number of different

producers

• Model 3

– Model 2 but with common or contract carriage of high voltage

transmission lines offered to all wholesale sellers and buyers

• Model 4

– Model 3 but retail customers also choose their suppliers in full

retail competition

194 Electricity Restructuring Models – Model 1

• Hunt and Shuttleworth (1996) – 4 models

• depend on competition at each stage

• Model 1: no competition - vertical

integration Local Distribution

•

20Electricity Restructuring Models – Model 2

• Model 2: competition generation

(gencos)

•

21Electricity Restructuring Models – Model 3

• Model 3: distribution companies (distcos)

• own the distribution wires

• distcos and large buyers choose their

supplier

• competition in generation and wholesale

open access

wholesale market

224 Electricity Restructuring Models – Model 4

• Model 4: all customers choose suppliers

• full retail competition open access

•

23Model 4 is the Most Economically Efficient

• If there are

– A well-established electricity retailing system

– Mature market institutions

– Constant vigilance against market power

– Appropriate methods of dispatch

24Electricity Prices and Taxes, $/kWh, 2011

Chile U.K. New Norway Sweden U.S

Zealand

Price Price Price Price Price Price

(Tax) (Tax) (Tax) (Tax) (Tax) (Tax)

Industrial 0.18 0.12 0.06 0.04 0.08 0.07

(N/A) (0.00) (N/A) (0.01) (0.00) (N/A)

Households 0.25 0.19 0.18 0.10 0.18 0.12

(0.04) (0.01) (0.02) (0.03) (0.05) (N/A)

Observations:

25The Electricity Industry Milestones

1995 Corporatisation of PUB’s gas and electricity undertakings, Oct 1995

1998

Singapore Electricity Pool commenced operation, Apr 1998

1999

2000

Government decision on further deregulation, Mar 2000

2001 Energy Market Authority formed, Apr 2001

2002

2003 Commencement of National Electricity Market of Singapore, Jan 2003

Commencement of Phase 1 Retail Market Liberalisation, Jun 2003

Commencement of Phase 2 Retail Market Liberalisation, Dec 2003

2004

Vesting Contract & Interruptible Load scheme introduced, Jan 2004

2008

Completion of Temasek’s divestment of the 3 gencos, Dec 2008

2009

2010

2011

Contestability to all consumers (being studied)

26

Source: EMA (2012)The Electricity Industry Milestones (Cont’d)

• June 2011

– Electric Vehicle (EV) test-bed for the testability of EV prototypes and

technologies was launched

• October 2011

– The Singapore Energy Statistics report was launched

• March 2012

– An industry-led Power Manpower taskforce was formed

• May 2013

– The LNG terminal received its first commercial cargo and started

commercial operations

• October 2013

– A micro-grid incorporating solar photovoltaic technology was launched

– Demand response programme

• February 2014

– The official opening of the LNG Terminal

27The Electricity Industry Milestones (Cont’d)

• April 2015

– Electricity Futures Market

• October 2017

– Launch of Regulatory Sandbox (for energy sector innovations)

• April 2018

– Open Electricity Market in Jurong (Soft Launch)

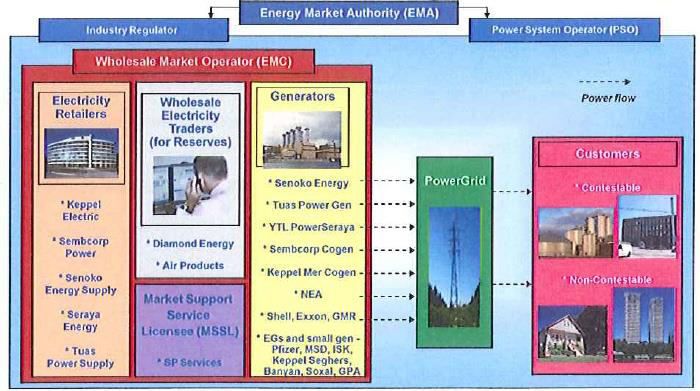

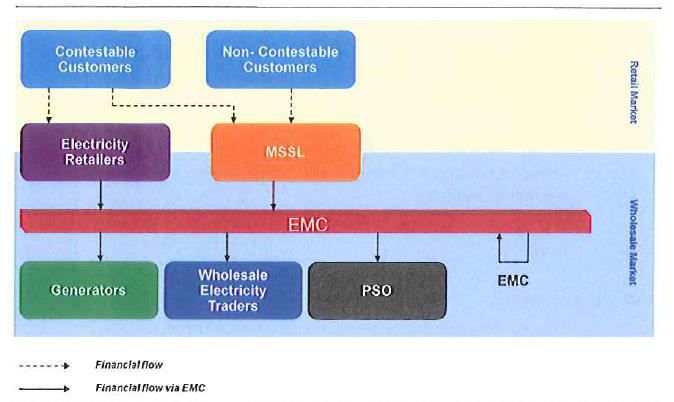

28Schematic Diagram of Market Structure

Energy Market Company

Market Operator

Wholesale Electricity Market

Electricity Spot

Market Retailers Consumer

Gencos* s

Spinning

Reserve Market

Market Support

System

Bilateral Contracts

* Generation Companies

29

Source: EMAPolicies and Regulations

• Goals

– To ensure a reliable supply of electricity to consumers

at competitive prices

• Reliability

• Reasonable (or competitive) price

• Action

– Forward-looking or proactive regulation

• New policies reflecting the latest environment of the industry

• Regular and timely update or change of regulation

• Example: vesting contracts

30Policies and Regulations: Scope

• Electricity Legislation and Regulations

• Codes of Practice

– Enforcement Actions

• Market Rules

• Performance Standards

• Exemption Orders

• Agreements

• Electricity Licences

• Electricity Licensed Workers/Installation Licences

• Policy Papers

• Vesting Contracts

31Electricity Legislation and Regulations

• The Energy Market Authority of Singapore Act (Chapter

92B)

• The Electricity Act (Chapter 89A)

32Regulatory Framework

EMA Act Electricity Act

EMA

Key Features

•Authorized activities

•Separation of contestable and non-

contestable sectors

•Powers to request for information Licences

•Preparation for emergencies and

security arrangements

•Licence fees

•Powers to audit

Licensees

Electricity Market Codes of Practice Performance

Rules • Transmission Code standards

• Metering Code

• Market Support

Services Code

• Regulated Supply

MSCP Services Code

RCP

(Market Surveillance and • Code of Conduct for

(Rules Change Panel)

Compliance Panel)

Retail Electricity

Licences

33

Source: EMA (2012)Electricity Industry Structure

Non-Contestable Sector Contestable Sector

34

Source: EMA (2012)Codes of Practice

• Five Codes of Practices

– Market Support Services Code

– Metering Code

– Code of Conduct for Retail Electricity Licensees

– Transmission Code

– Regulated Supply Service Code

• Two enforcement actions

– Red Dot Power Pte Ltd’s contravention

– PacificLight Energy Pte Ltd’s contravention

35Market Rules

• Energy Market Company (EMC), the market operator or

company, administers the Market Rules

• The Rules Change Panel (RCP) reviews all proposed

modifications to the Market Rules

36Performance Standards: SP PowerAssets Ltd.,

the Transmission Licensee

Service Service Indicator Service Performance

Dimension Standard Target (%)

Availability of Minimum advance notice for planned interruption of electricity 7 c.d 95

Supply supply

Reliability of Number of power failure incidents*caused by failure of, 0 100

Supply damage to, or operation of Licensee’s equipment or cables

Restoration of Time taken to restore electricity supply for each power failure 3 hours 100

Supply due to failure of, damage to, or operation of Licensee’s 2 hours 90

equipment or cables rated at 22kV or above

Quality of Supply Time taken to rectify voltage complaint or limit violation 2 c.d. 95

Time taken to correct a voltage complaint that requires 6 months 99

network reinforcement

Number of voltage dip incidents*due to failure of, damage to, 0 100

or operation of Licensee’s equipment or cables

Providing Supply Time taken to implement electrification scheme requiring new 10 weeks 90

substation after take-over of substation (up to 22kV)

Time taken to implement service connection requiring cable 6 weeks 90

installation work, after premises to be supplied with electricity

is ready to receive cable

Customer Contact Time taken to reply to a written complaint 7 w.d. 95

Metering Services Time taken to attend to meter problem at site upon notification 8 c.d. 95

Notes: * only incidents where the Licensee is determined by the Authority to be at fault will be counted

c.d. is calendar days; w.d. is working days 37Performance Standards: SP Services Ltd.

the Marker Support Services Licensee

Service Service Indicator Service Performance

Dimension Standard Target (%)

Providing Time taken to process application for electricity supply and reply to 14 c.d. 85

Supply applicant

Lead time taken to inspect large electrical installation (supply capacity 7 w.d. 90

greater than 45kVA) and turn-on electricity supply upon request

Lead time taken to test small electrical installation (supply capacity less 10 c.d. 90

than or equal to 450kVA) and turn-on electricity supply upon request

Time taken to inspect pre-tested electrical installation and turn-on 3 w.d. 90

electricity supply upon request after opening of account

Waiting time at site for appointment to turn on or cut-off electricity supply 1.5 hours 90

Customer Time taken to reply to a written enquiry or complaint 7 w.d. 95

Contact

Queuing time at customer service counter (enquires and opening/closing 20 90

of accounts) minutes

Time taken by customer service officer to pick up telephone call 30 90

seconds

Metering Time taken to attend to meter disputes at site notification 8 w.d. 95

Service

Time taken to attend (make appointment, reply) to meter reading issues 5 w.d. 95

upon notification

Time interval between successive reading of billing meter(s) 2 monthly 95

Notes: c.d. is calendar days; w.d. is working days

38Exemption Orders

• The EMA may exempt any person or class of persons

from complying with the licensing requirement

39Agreements

• Agreements among various entities participating in the

Singapore electricity market

– Market Support Services Licensee (MSSL)-Market Participant

Agreement (a generation licensee/a contestable consumer)

– Power System Operator (PSO)-Market Participant Agreement

• PSO and each market participant under Market Rules

– Market Support Services Agreement (Retailer)

• MSSL (provider) and retailers (procurers)

– Market Support Services Agreement

• MSSL (provider) and demand response participants (procurers)

– Retailer Use of System Agreement

• The Transmission Licensee and an electricity retailer

– Generation Facility Operation Agreement

• Power System Operator (PSO) and a generation licensee

40Financial Flow between Market Players Source: EMC (2012) 41

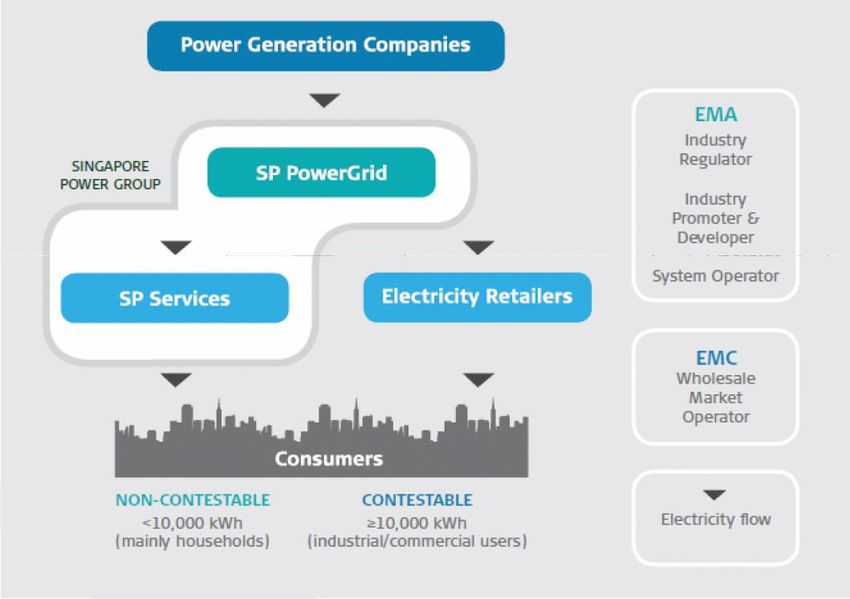

Electricity Licences

• Generation Companies

– One or more generating units of 10 MW or above each

• Retailers

– Retail electricity to contestable consumers

• Wholesalers

– One or more generating units of 1 MW or more each but less than 10 MW

• Market Support Services Licensee

– SP Services: Metering, managing metered data and facilitating access to a

wholesale electricity market, and supplying electricity to non-contestable

consumers

• Transmission Licensee/Transmission Agent Licensee

– SP PowerAssets Ltd: Managing the electricity transmission system

– SP PowerGrid Ltd: transmitting electricity

• Market Company

– Energy Market Company (EMC): Operating and administering Singapore’s

wholesale electricity market (NEMS)

42Industry Structure and Players Source: EMC (2012) 43

Schematic Diagram of NEMS

with Financial Flows

44Electricity Licensed Workers/Installation Licences

• Electrical Worker Licence

– Electrician’s Licence

– Electrical Technician’s Licence

– Electrical Engineer’s Licence

• Electrical Installation Licence

– An electrical installation of approved load exceeding 45 kVA for

non-domestic purposes

• Cable Detection Worker Licence

– Cable detection work prior to the commencement of any earth

works

45Electricity Tariff

• Tariff revised quarterly to reflect cost of electricity

• Forward fuel prices for 2.5 month period to set tariff

• Regulated tariff only for Non-contestable Consumers

(households and small businesses, using less than

10MWh monthly)

Forward fuel price from Jan

SPS calculates and Electricity tariff set

to mid-Mar 2012 used in

announces tariff for 2Q 2012

computation of tariff

Jan Feb Mar Apr May Jun

Source: EMA (2012)

46Electricity Tariff Breakdown

Energy Costs Generation Companies

23.03 ¢/kWh

Network Costs

4.78 ¢/kWh

SP PowerAssets

SP Services

MSS Fee

0.22 ¢/kWh

Market Admin & PSO Power System Operator

Fee & Energy Market

0.05 ¢/kWh Company

Tariff for Jul to Sep 2012: 28.08 ¢/kWh

Source: EMA (2012) 47Targeted Assistance for Households

• GST Voucher - U-Save: a rebate to help lower- and

middle-income households with their utilities bills.

• Eligible households will receive their U-Save rebates

once every 6 months, in January and July

• Lump sum rebate encourages people to save electricity

Source: EMA (2012) 48Policy Papers

• Nine policy papers

– Handbook for Photovoltaic (PV) Systems (2011)

– Developments in the Singapore Electricity Transmission Network (2011)

– Policy on Self-Supply of Electricity (2008)

– Net Treatment of Embedded Generators (2006)

– Exemption of Embedded Generating Units in Operation Prior to 1 Jan

2003 from the Licensing Requirement (2006)

– Guidelines on Evaluation of Merger and Acquisition Proposals in the

Electricity Industry (2004)

– Briefings on the Procedure for Application for Electricity Supply in the

New Electricity Market Framework (2002)

– Application for Exemption form Compliance with Code of Practice

(2002)

– Policy on Direct supply of Electricity by Generating Sets to On-site

Loads (2002)

49Singapore Load Curve

Daily peak production

tends to occur during

the day,

Shoulder production

early in the morning and

later in the evening,

Off-peak during the night

Source: Energy Market Authority (EMA) Singapore

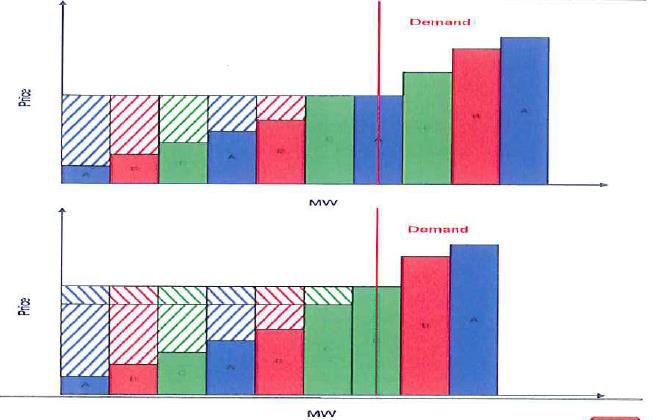

50Determination of Market Clearing Price

Price

($/MWh) Total demand

100

The market clears

at this point

80

60 Clearing price = $50/MWh

40

20

0

Quantity

Offers below the clearing Marginal Offers above the clearing (MW)

- 20 price are accepted unit price are not accepted

above

Company A Company B Company C

Source: EMA (2012)Physical and Economic Withholding

Source: EMC (2012)

52Market Power and Measures

53Lerner Index

• The relative mark-up over marginal cost

– The difference between price and marginal cost as a

fraction of the price

– A ratio of price less marginal cost of supply to price

– Price-cost margin

• Zero (0): no market power

• One (1): infinite market power

• It measures a firm’s ability to maintain prices

above competitive level at its profit-maximizing

level of output

54Test Results of Market Power: An Example

Measures Values and Remarks

CS4 96%

CS8 Close to 100%

HHI 0.2662

SMA Negative for all gencos

RSI Larger than 1 for all gencos

Lerner Index 0.188 – 0.250

Source: Compiled from Chang (2007) Energy Policy, 35: 403 – 412

55Three Game-theoretic Models

• Cournot model

– Each firm chooses quantity to maximize profits given

the other firms output

• Duopoly

• Stackelberg model

– One firm is a leader in the market setting the quantity

knowing how the other firm will react

• Bertrand model

– The two firms set price instead of quantity

– The Bertrand solution is the same as the competitive

solution

56Perfect Competition Solution

57Cournot Game without Contracts

58Cournot Game with Contracts

59Vesting Contracts

• A contractual agreement between generation

companies and SP Services Ltd (MSSL)

– To sell a specifies amount of electricity (the vesting

contract level) at a specified price (the vesting

contract price)

– The vesting price is set by taking account both the

long-run marginal cost of the most efficient generation

technology that account for at least 25% of the total

electricity demand in Singapore

– The EMA reviews the vesting parameters every two

years or when necessary

60Definition of Net Generation Capacity

• Net Capacity = N x [G-C-R-(A+S+F+O) x G]

– N: Number of Units

– G: Gross Unit Capacity

– C: Cogeneration Use

– A: Auxiliary Usage Rate

– R: Reserve

– S: Scheduled Outage

– F: Forced Outage

– O:Other De-Rating

61Market Power in NEMS

• Various price levels in 2004 and 2005

– The Generation Weighted Average (GWA)

Pool Price

• The price observed in the wholesale market,

presumed a perfectly competitive solution

– Average Market SRMC

• The average price of all generators offered at their

SRMC, presumed a perfectly competitive market

– VC Strike Price

• LRMC of the next efficient new generator

62Evidence of Market Power 1

• Vesting Contract (VC) strike price (LRMC) is

close to the Generation Weighted Average

(GWA) pool price

Price ($/MWh) 2004 2005

VC Strike Price 96.95 110.94

GWA Pool Price 81.48 108.72

Average Market SRMC N/A 85.07

63Evidence of Market Power 2

• The 2004 prices were lower compared to the VC

Strike price (quarterly basis);

• The 2005 prices were much closer to the VC

Strike price

Price 2004 2005

($/MWh)

1 2 3 4 1 2 3 4

VC Strike 94.24 96.25 95.73 101.56 101.2 96.35 117.38 128.39

Price 9

GWA 68.86 82.78 82.06 92.11 85.84 107.90 116.22 124.42

Market

Price

64Evidence of Market Power 3

• Average Market SRMC is far lower than actual

market price in 2005

Price ($/MWh) Load Block GWA

Peak Shoulder Off-Peak

Average Market 84.37 84.68 86.43 85.07

SRMC

Actual Market Price 111.46 110.73 103.99 108.72

65Vesting Contract Level (%):

Suggested, Scheduled and Actual

2004 2005 2006 2007 2008 2009 2010 2011 2012

Suggested 54 55 62 46

Scheduled 65 50 50 50 50 40 40 40 40

Actual 65 65 65 65*/55 55 55 55 60 55

Suggested: PA Consulting or EMA Consultant

Scheduled: establish prior to 2004

Actual: EMA’s decision by every two-year review

*: For the first two quarters of 2007 (Jan – Jun 07)

66Vesting Contract Level (updates)

Period Vesting Contract Level (%)

2013 1H 55

2013 2H 50

2014 40

2015 1H 30

2015 2H 25

2016 20

67Market Share (%) and CS4: Updates

68CS4: 2005 - 2013

69HHI: Updates

70Total Capacity and SMA: Updates

71RSI: Updates

72Monthly USEP 2004 – 2012

Monthly USEP from 2004-2012

300

250

200

150

SGD

100

50

0

73USEP in 2008

USEP

(S$/MWh)

1200

1000

800

600

400

200

0

-200

74USEP in 2009

Half hour USEP in 2009

5000

4000

3000

2000

1000

0

01.Jän.09 01.Feb.09 01.Mär.09 01.Apr.09 01.Mai.09 01.Jun.09 01.Jul.09 01.Aug.09 01.Sep.09 01.Okt.09 01.Nov.09 01.Dez.09

-1000

75Lerner Index with LRMC

76Lerner Index with SRMC

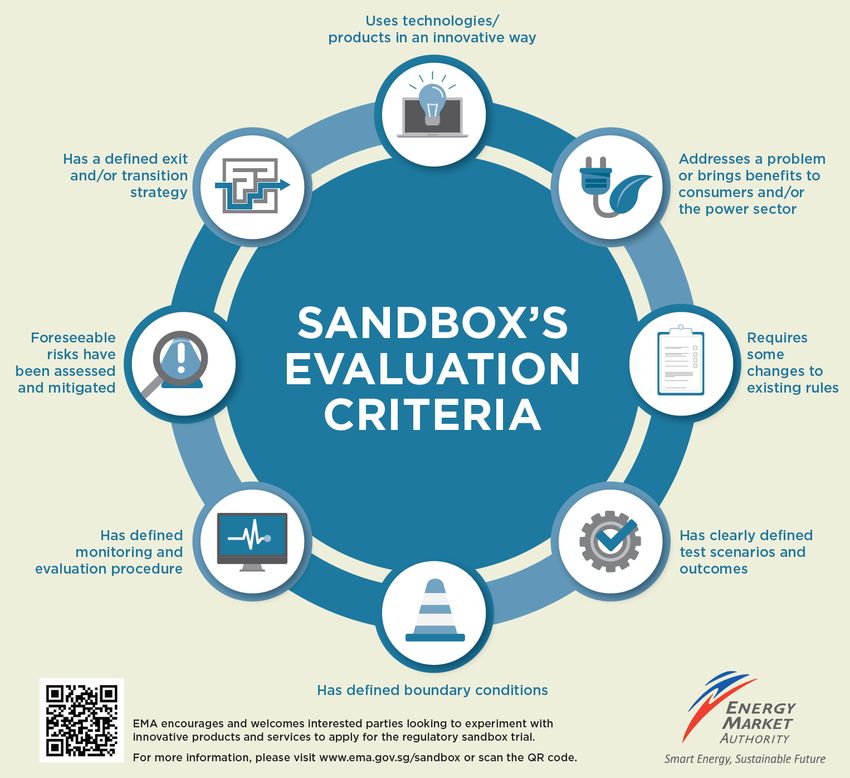

77Regulatory Sandbox Framework

• To provide a ‘safe space’ in which interested parties can

experiment with innovative solutions without being

subjected to the prevailing regulatory requirements

• Safeguards will be introduced during the experiment to

minimize risks to consumers and industry

– The duration of the trial or the maximum number of consumers

78Regulatory Sandbox Regulation: Illustration

79Soft Launch of Open Electricity Market

• A pilot program

• It starts April 2018

• A total of 108,000 household and 9,500 business

accounts in Jurong will have the option of buying

electricity from a retailer of their choice or SP Group (the

current MSSL)

– Currently businesses with an average monthly electricity

consumption of at least 2,000 kWh have the option of buying

electricity from a retailer of their choice or SP Group

• The Energy Market Authority (EMA), the regulator, will

extend the option to the rest of consumers in Singapore

(about 1.3 million accounts) in the second half of 2018

80Map of Soft Launch in Jurong

81Thank you for your attention!

If you have any question or comment,

please contact me at

yhcahgn@suss.edu.sg

82You can also read