Russian economy and financial sector: beyond crisis but under sanctions. What to expect? Analytical Credit Rating Agency (ACRA) - Natalia ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

9 April 2018, Berlin

Russian economy and financial sector: beyond crisis but under

sanctions. What to expect?

Analytical Credit Rating Agency (ACRA)

Natalia Porokhova

Kirill Lukashuk

http://www.acra-ratings.com/

ACRA at a Glance

The Analytical Credit Rating Agency (Joint-Stock Company) was founded on November 20, 2015

Authorized capital of more than RUB 3 billion (more than USD 50mln)

27 shareholders – Russia’s largest companies and financial institutions – holding a 3.7% stake each

ACRA’s activities fully comply with the requirements of Federal Law N 222-FZ

August 25, 2016 ACRA became the first CRA included in the register of the Central Bank of Russia

ACRA’s clients are:

1. Financial institutions (banks, non-bank financial institutions, insurance companies)

2. Corporate entities

3. Regional and municipal authorities of the Russian Federation

National credit ratings scale includes ratings from AAA (RU) to D (RU)

Regular macroeconomic analysis and coverage of 20 sectors by designated analytical teams

1 http://www.acra-ratings.com/

Share of banks with ACRA ratings is more than 80%

Share of issuers with ACRA ratings on Russian bond market as at February 2, 2018*

80%

72%

49%

31%

Financial institutions Banks Regions Corporates

*By volume of issues Source: ACRA

2

http://www.acra-ratings.com/

ACRA Shareholders 3 http://www.acra-ratings.com/

Board of Directors (1)

ACRA’s Board of Directors and top management have

extensive global experience in the rating industry

KARL JOHANSSON – CHAIRMAN OF THE BOARD OF DIRECTORS (USA)

From 1995 to 2000, Mr. Johansson was a Managing Partner of Ernst & Young CIS, after that he was a Regional Partner for Eastern

Europe countries, including CIS (Vienna, Austria). From 2006 to 2014, he worked as Managing partner of Ernst & Young CIS in

Moscow. While in Russia, he was a coordinator of the Foreign Investment Advisory Council (FIAC) under the Government of the

Russian Federation.

THOMAS MISSONG – MEMBER OF THE BOARD OF DIRECTORS (AUSTRIA)

Has more than 16 years of experience in the field of financial markets, 10 of which in rating advisory activities. Since 2010, he

serves as the President of the European Association of Credit Rating Agencies EACRA (Paris, France). He is a Managing Director at

RATINGPLATFORM, a company providing research on rating agencies.

4 http://www.acra-ratings.com/

Board of Directors (2)

ANOUAR HASSOUNE – MEMBER OF THE BOARD OF DIRECTORS (LUXEMBURG)

Has more than 15 years of experience in the field of financial markets, including 12 years in international rating agencies, namely,

Moody's and Standard and Poor’s. From 2012 to 2015, he worked for The Bank of Tokyo-Mitsubishi UFJ as the head of research

and strategy for the Middle East and Africa. At present, he is a co-founder, co-owner and a Managing Director of West Africa

Rating Agency, as well as a Managing Partner of Euris Group.

EKATERINA TROFIMOVA – MEMBER OF THE BOARD OF DIRECTORS,

CHIEF EXECUTIVE OFFICER (RUSSIA)

From 2000 to 2011, Ms. Trofimova worked as a financial analyst, Director and Head of Russia and CIS Financial Institutions Rating

Group at Standard & Poor’s (Paris, France). In 2011 she joined Gazprombank and from 2012 to 2015 was a member of the Bank’s

Management Board and supervised the Rating Advisory Center.

VINCENT TRUGLIA – MEMBER OF THE BOARD OF DIRECTORS (USA)

Has more than 40 years of experience in the field of financial markets, including 15 years at Moody’s, 11 of which as a Managing

Director of the sovereign risk analytical team. As an independent consultant, he participated in strategy development for the non-

profit rating agency INCRA.

5 http://www.acra-ratings.com/

ACRA Key Principles

Good faith and high standards of rating • Qualified personnel with professional experience in the rating industry

activities • Code of Ethics and Professional Conduct is strictly adhered

Independence and prevention of conflicts • Transparent and diversified ownership structure

of interest • Internal controls identifying and eliminating any conflicts of interest

Timely disclosure of information on ACRA’s • Mandatory release of draft rating methodologies on ACRA’s website

activities • Annual publication of the transparency report of ACRA’s activities

• Strict compliance monitoring at all stages of rating process

Protection of confidential information

• Modern IT systems, data protection and rating process support

• All ACRA’s policies are publicly available on the official website

Transparency of rating methodologies and

the rating process • Market participants involvement in rating methodologies discussion.

6 http://www.acra-ratings.com/

ACRA Methodology Key Advantages

• Ensuring comparability of all assessments

• Accounting for Russian sectoral and regional specifics, as well as corporate governance peculiarities

• Ensuring transparency of assessment algorithms while retaining the ability to account for expert opinions

• Multiple-stage validation of all methodologies and rating models

• Accounting for forecast data in the course of creditworthiness assessment

• Employment of risk accumulation technology, i.e. pinpointing ‘anchor’ rating assessment factors

• Synergy between research departments and accounting for relevant expertise of contiguous business units in the course

of rating assessment (banking, regional and macroeconomics groups)

7 http://www.acra-ratings.com/

International and National Scales

International National

scale scale • The international rating scale compares creditworthiness of all

borrowers around the world

AAA AAA(RU) • The country ceiling caps an issuer’s rating at the sovereign level,

AA+ AA+(RU)

AA AA(RU) which results in strong rating compression in countries where the

AA- AA-(RU) sovereign rating is not the highest, i.e. borrowers of different

A+(RU)

A+

A(RU) quality are assigned the same ratings

A

A-(RU)

A- BBB+(RU) • The national rating scale compares creditworthiness of individual

BBB+ BBB(RU)

BBB BBB-(RU)

borrowers in a country with that of the national government

Country ceiling

BBB- BB+(RU)

BB+ BB(RU) • Regulators around the globe are switching to national scale

BB BB-(RU) ratings

BB- B+(RU)

B+ B(RU)

B B-(RU)

B- CCC(RU)

CC(RU)

CCC

C(RU)

CC SD(RU)

C D(RU)

SD http://www.acra-

D

ratings.ru/

8 http://www.acra-ratings.com/ACRA Methodological Toolbox: Design and Contents

Methodologies Principles

General approaches: Each and every ACRA methodology…

Key concepts of ACRA

Bonds ratings ….is developed by the methodology team in close cooperation with the analytical

General principles of forecasting team

ACRA Financial Stress Index …undergoes multiple validation and testing procedures

Financial institutions:

Banks and bank groups Testing samples:

Leasing companies

FI: 110 banks / 30 defaults / 3 years

Insurance companies

Microfinance organizations Corporates: 135 companies / 11 defaults / 4 years

Asset management companies Public finance: 85 regional governments / 5 years

Support assessment:

Government-related entities Validation and testing:

Group support and relationships

Foreign shareholder support G-spread and duration test

Public finance: Coefficient correlations test

Regional and municipal authorities

Prediction power assessment

Non-financial institutions: ACRA is fully equipped with methodologies for assigning ratings to a

Corporate rated entities wide range of rated entities and instruments within the financial,

Structured finance corporate or public sectors.

9 http://www.acra-ratings.com/Commercial research

ACRA’s team comprises well-known economists and industry analysts who communicate with financial and real economy sector

companies as well as federal and regional authorities in practical contexts on a daily basis

Proprietary models and databases covering economies of countries and regions, budgets, and corporate finance

ACRA regularly publishes Russian economic outlook and industry forecasts as well as relevant topical research. These publications can

be found at: https://www.acra-ratings.ru/research

Macroeconomic and industry indicators forecast are in compliance with the proprietary methodology published on ACRA’s website

Fundamental research Industry forecasts Economic models

Assessing and forecasting effects on Forecasting industry indicators for: Excel models achieving client’s goals

the economy, regions, industries and • Issues to automate and visualize various

companies from changes in: • Credit quality economic scenarios

• Public policy (including fiscal and • Investment activities

tax, monetary, foreign economic

policy, etc.) For more details regarding this service

• Commodity and financial markets please contact Natalia Porokhova, Head of

• Ruble FX rate, prices, and interest Research and Forecasting Group,

rates natalia.porokhova@acra-ratings.ru

+7 495 139 04 90

10 http://www.acra-ratings.ru/Rating Model Validation

What we offer:

Calculation of quantitative efficiency metrics with respect to PD, LGD, EAD models of corporate borrowers, ALM models, IFRS9

provisioning models as well as marketing and collection models

For more information, please contact

Qualitative validation of models Olesya Shekholtseva, Project Manager

olesya.shekholtseva@acra-ratings.ru

Preparation of validation reports for potential submission to the Bank of Russia

+7 495 139 04 80 , ext. 127

Readiness assessment when preparing IRB models for submission to the Bank of Russia

Benefits for the client:

There would be no need for the client to create a separate division with highly-paid specialists who are underemployed most of the time

The client could avoid a conflict of interests that arises when validation and development are performed by the same division

Professional approach based on global best practices and experience in validating ACRA’s internal models and methodologies

ACRA’s specialists of Analytical Services Development Group are highly competent in validation of various model types (IRB, ICAAP,

IFRS9, ALM, etc.)

A opportunity to identify any bottlenecks in client’s models and determine areas for development

11 http://www.acra-ratings.ru/ACRA Trainings on Credit Analysis

Forthcoming trainings ACRA sees its mission in developing best practices

that provide the Russian financial market with basis

Fundamentals of credit analysis of regional and municipal authorities

for sustainable performance

(April 12-13)

Rating modelling fundamentals ACRA’s expertise is unique in terms of its

(April 23-24) competences and profound understanding of credit

risk

NEW! Forecasting in credit analysis. Course 1: macroeconomic and industry forecasting

fundamentals ACRA trainings are aimed at enhancing

(May 14-15) qualifications of financial market participants and

building up efficiency of managerial and investment

NEW! Change management hosted and presented by Ekaterina Trofimova, ACRA CEO

decision making

(May 21)

Fundamentals of credit analysis of insurance companies

(May 24-25)

Corporate credit analysis fundamentals

(May 29-30)

NEW! Advanced analysis of structured finance deals

(May 31 – June 1)

The art of presentation in credit analysis hosted and presented by Ekaterina Trofimova, ACRA CEO

(June 21-22)

Fundamentals of structured finance deals analysis For more information and enrollment,

(July 2-3) please contact

Fundamentals of asset management companies reliability analysis and credit analysis of non-

state pension funds

Artem Mayorov, Manager

(September 6-7) artem.mayorov@acra-ratings.ru

NEW! Forecasting in credit analysis. Course 2: practical aspects of economic modeling +7 495 139 04 80, ext. 147

(September 10-11)

Fundamentals of sovereign risk credit analysis

(Autumn, 2018)

12 http://www.acra-ratings.com/ACRA’s International activities

Cross-border projects:

Supranational methodology

Trade counterparties assessment

ACRA

International

International investors outreach: EAEU presence:

Insider’s view Central Banks dialog

Media events Analytical coverage

13 http://www.acra-ratings.com/Cooperation with a Chinese rating agency Golden Credit

On November 2 2017 ACRA signed the Memorandum of Understanding with a Chinese rating agency

Golden Credit Rating International (http://www.dfratings.com/)

Golden Credit rating agency

is among top five credit rating agencies in China

possesses a complete range of licenses required to

provide rating services

key shareholder is the state managing company China

Orient Asset Management established by the

Ministry of Finance of the PRC

Prospects for cooperation of ACRA and Golden Credit

o conduct joint analytical work For more information, please contact

o develop technological and informational cooperation Maria Mukhina, Operational director

o pursue mutual acknowledgement by Chinese and maria.mukhina@acra-ratings.ru

Russian investors and regulators +7 495 139 04 80, доб. 107

14 http://www.acra-ratings.ru/New economic environment: prospects for

development and key risks of Russian economy

Analytical Credit Rating Agency (ACRA)

http://www.acra-ratings.com/Russia: Absence of Usual Growth Conditions Offset by Impetus For Change

Key trends in Russian economy that can contribute to future economic growth and development:

1. Population ageing – constrains economic growth but gives additional stimuli for some industries.

2. Switching to low inflation mode – higher predictability for business and cheaper loans, but government and

businesses should seek new forms of flexibility.

3. Government expenditures decline – government role squeeze and inequality growth, more space for private activities

4. Turn to East – increase in share of Asian countries in exports, imports, FDI and external debt.

5. Sanctions – financial sanctions are absorbed, but sanctions against oil & gas companies will limit crude oil production

growth in 2020s.

Indicator 2015 2016 2017 2018 2019 2020 2021 2022

Real GDP (%, y-o-y) -2.5 -0.2 1.5 1.6 1.5 1.5 1.5 1.7

Inflation (%, Dec/Dec) 13.2 5.4 2.5 4.1 4.1 4 3.9 3.8

Urals oil price, USD/bbl 51.3 42.3 53.5 58 59.2 60.3 61.6 62.8

USD/RUB (12-month average) 61.3 67.2 58.3 58.3 58.8 59.7 60.5 60.2

Unemployment, % 5.6 5.5 5.2 5.2 5.3 5.4 5.4 5.4

References: ACRA macroeconomic forecast, Federal State

16 http://www.acra-ratings.com/

Statistics Service, Federal Treasury, Bank of RussiaLimitations for Further Extensive Growth of Russian Economy

Labor force Imports of goods

78 1,6

Imports of goods value index (2008=1)

77 1,4

Investment-oriented imports

76

1,2

75

1,0

74

0,8

73

0,6

72

0,4

71

0,2

70

69 0,0

2019

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2020

17 Source: Federal State Statistics Service, ACRA http://www.acra-ratings.com/Russia’s Potential Economic Growth is close to +1.5%

Total factor

productivity Working time

(a one-off)

-0.4

+0.3

+0.9 Labor force

Fixed capital

+1.5 +1.8

+0.8

Natural

resources

+0.2

18 Source: ACRA estimates http://www.acra-ratings.com/Economy is Close to it’s Potential GDP Growth Rate

12 11

Capacity underutilization (%, lhs)

10 10 Modest prospects of cyclical growth

Unemployment rate (%, rhs)

A relatively high level of labor, resources and

8 9 capacity utilization.

6 8 Low possibility of extensive expansion

Adverse demography: the employed

4 7 numbers to decline by 2-4% in 5 years

(accounting for offsetting effects of elderly

employment and expected migration).

2 6

Expensive investment-oriented imports

0 5 (due to RUB depreciation) is a source of

difficulties for capital-intensive industries.

-2 4

19 Source: Federal State Statistics Service, ACRA http://www.acra-ratings.com/Monetary policy approaching “neutral state” …

18

16

14

12 Bank of Russia deposit

rate (1 day) %

10

8 X

Projected level for SR rates ‘in equilibrium’

6 ?

4

Inflation target

2 Inflation, % Y-o-Y

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

20 Source: ACRA, Bank of Russia http://www.acra-ratings.com/… but the neutral rate itself could fall

CBR’s public method of neutral interest rate estimation

14 14

12 12

transition

10 10

Russia’s country risk

8 8

6 6

Global neutral rate

4 4

Target inflation (after monetary

2

policy transition) 2

0 0

2001-2003 2004-2006 2007-2009 2010-2014 2015-2017 2018 2019-2022*

21 Source: ACRA, Bank of Russia http://www.acra-ratings.ru/Inflation fell to historic lows, but its volatility may still be high

Inflation decomposition by factors and forecast for 2018-2021

Tariffs and

16% regulated prices

Monetary inflation

14% and expectations

Food market

conditions

12% Ruble Exchange rate

10% Inflation target

8%

6%

Inflation target is 4%. Monetary

policy has been tough since 2015.

4%

The CBR key rate is above inflation by

2% 5%.

Inflation rate is still vulnerable to

0% potentials shocks. 2/3 of consumer

basket is subject to FX and food

-2% prices volatility, tax and tariff.

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

22 Source: ACRA estimates http://www.acra-ratings.com/Low Inflation Makes Costs rigid and State and Business Less Flexible during Crisis

Unemployment during the 2008-2009 crisis was lower in countries

with higher inflation

Fixing nominal wage under high

20% inflation means decrease in labor

Greece

costs. Russian business and state

18% Average inflation for 2003-2007 > 7,5% used to freeze nominal contracts in

The difference between the maximum unemployment levels for

Average inflation for 2003-2007 < 7,5%

16%

adverse environment.

Circle diameters are proportional to

Spain inflation

14%

The lower the inflation, the smaller

the benefit in real terms. The most

12% sensitive to low inflation mode will

Latvia

2009-2013 and 2008

be those industries focused on the

10%

Portugal

domestic market where the overall

8% inflation context affects prices the

most. Those industries are

6%

Italy Slovenia infrastructure monopolies (by virtue

4% Ukraine of regulation) and the services

United States

Canada Iran, Islamic Rep. Russian Federation sector.

2% South Africa Belarus

Australia

Indonesia Norway Chile

0% Germany Qatar

Kazakhstan

Azerbaijan

-2%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Source: ACRA estimates

Real GDP growth slowdown in 2009-2013 versus 2008

23 http://www.acra-ratings.com/Russian financial system has absorbed oil price volatility and sanctions

140 6

URALS

ACRA FSI monthly average, rhs

120 5

100

4

80

3

60

2

40

20 1

sanctions

0 0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

ACRA FSI measures stress in the financial system of Russia (more about methodology - on the website)

24 Source: ACRA estimates http://www.acra-ratings.com/Federal budget consolidation effectively started in 2017 …

25%

20%

non oil & gas deficit

15%

10%

5%

0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Non oil & gas revenues, % of GDP Oil & gas revenues, % of GDP Federal budget expenses, % of GDP

25 Source: Ministry of finance, ACRA estimates http://www.acra-ratings.com/… but it still has way to go, bringing more space to private activities

10%

5%

Aim: -0.7% GDP in 2020

0%

-1.5%

-8.0%

-5%

Non oil & gas federal budget balance, % of GDP

-10%

Federal budget balance, % of GDP

-15%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

26 Source: Ministry of finance, ACRA estimates http://www.acra-ratings.com/Brief history of Russian fiscal rules

2004-2007 2008 2013-2014 2017-…

Non-oil&gas deficit ≤ Structural deficit ≤ Primary structural

Main feature Structural deficit ≤ 0

4.7% of GDP 1% of GDP deficit ≤ 0

Non-oil&gas + oil&gas Non-oil&gas + oil&gas

Structural Non-oil&gas + oil&gas

(oil price ≤ arbitrary (oil price ≤ average since

part of - (≤ 40 $/barr., 2%-

fixed level, starting with 2008 or 3y moving

revenues indexed every year)

20$/barr.) average if it is lower)

Arbitrary chosen

Lack of expenditure

parameter (base oil

counter-cyclicality Abnormal period used

price) is too easy to

during recession may too determine “normal”

What we change procyclically

lead to the fiscal rule long-run features leads ?

have learned Lack of coordination

easing. It could become to unsustainability of the

with exchange rate

permanent instead of rule

policy may lead to

temporary

the Dutch disease

27 Source: ACRA http://www.acra-ratings.com/Fiscal rule’s hard connection to FX market interventions makes RUB more stable

Balancing interventions

85

Oil market Internal FX market 80 2018 2017

75

70

USDRUB

65

Other internal 60

Other global markets

markets

55

Ministry of finance buys amount of currency, which equals OG tax

revenues exceeding those at 40 $/barr. (assuming USDRUB is the

50

same as at the current oil price).

20 30 40 50 60 70 80

Elasticity of FX to oil price is not 0, because there are other external

Urals, $/barr. yearly average

factors of USDRUB having non-zero correlation with oil price.

28 Source: ACRA http://www.acra-ratings.com/Sector-Specific Investment Stimuli

Stimuli 2015-2016 2017-2018 2019-2021

Domestic market growth — Healthcare, Education, Insurance, IT

Export market growth Gas production and transportation, chemical industry, transport infrastructure

Agriculture, Food, + Textiles, Electrical appliances and electronics,

Import substitution Household chemicals, Tradable services, Construction materials,

Tourism Pharmaceuticals

Cost cutting (price competition) Retail, Logistics, Financial sector, IT

Maintenance CAPEX Infrastructure (electric power, heat power, roads), repair services

Data storage,

Liabilities to the government Power generation, Oil refining, Railcar industry

oil refining

29 Source: ACRA macroeconomic forecast, Bank of Russia

http://www.acra-ratings.com/Russian Government to Transfer Pension, Health Insurance to Business

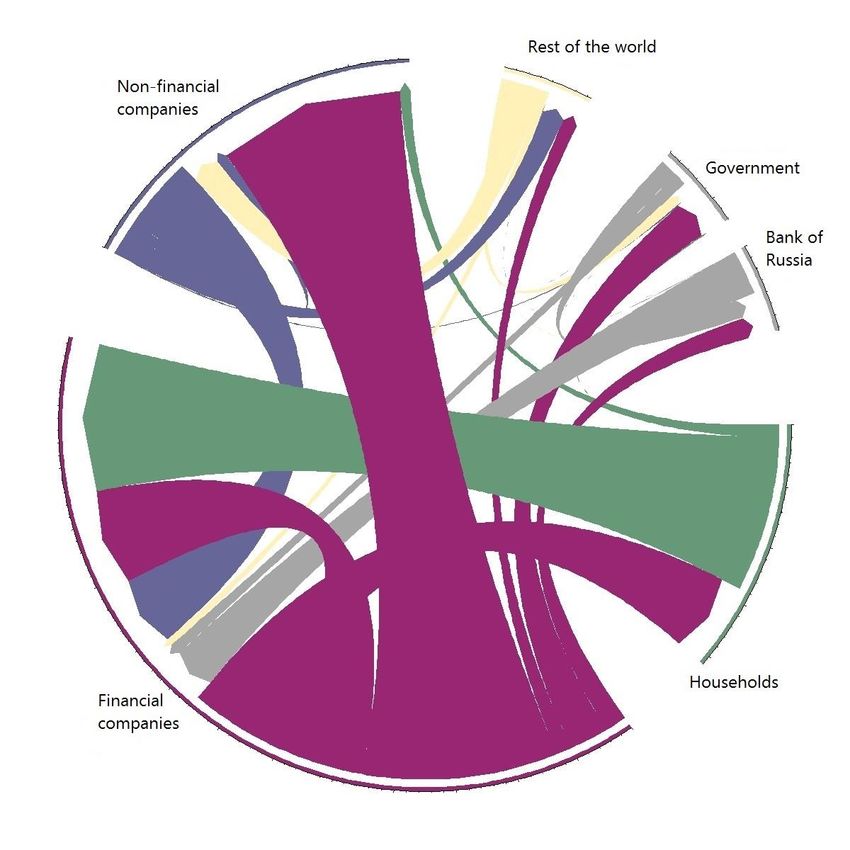

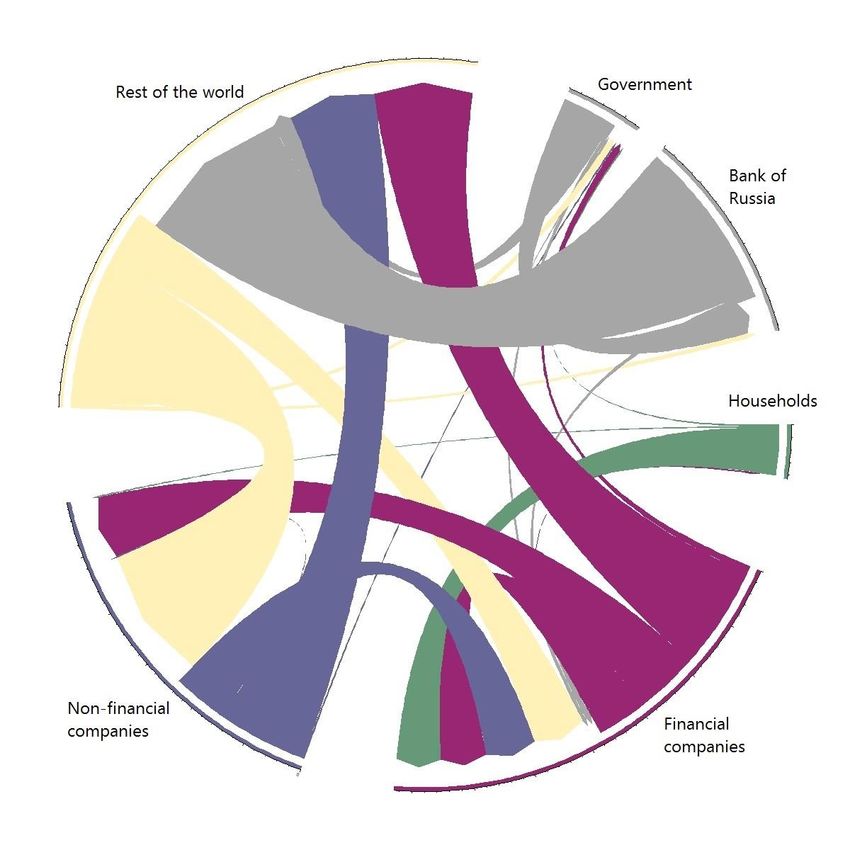

European Union Mutual debts “from who-to-whom”

Russia

as at 1 July 2017

• Debt relations in the form of loan, borrowing, deposit or debt security (stock, not flow).

• Arrows go from lenders to borrowers (from who-to-whom). Arrow thickness is proportionate to the share

Source: ACRA

of a sector’s debt in the aggregate debt of the economy.

30 http://www.acra-ratings.com/Top 7 Integrated O&G Players*: Debt is Not a CAPEX Limiting Factor

Russian Integrated O&G Leverage** CAPEX is peaking, EBITDA margin depressed by elevated taxes

2,5 80% 72,7% 73,8%

70,2%

2,08 2,08 67,1%

70% 63,0%

1,94

2,0

1,76 60%

1,60

50%

1,5

1,27 1,27

1,13 40%

1,09

26,6%

1,0 0,88 30% 24,2% 24,4%

22,0% 21,1%

20%

10,6% 12,1%

0,5 7,4%

10% 2,4%

-3,0%

0%

0,0 2013 2014 2015 2016 9M 2017 TTM

2013 2014 2015 2016 9M 2017 TTM -10%

Total Debt/EBITDA Net Debt/EBITDA CAPEX/EBITDA FCF/Sales EBITDA/Sales

• O&G players’ leverage remains at a comfortable level and does not affect their CAPEX programs.

• The 2014 debt increase in RUB terms was purely a result of the RUB devaluation.

• Sanctions had not caused changes in investment schedules.

* Gazprom, Rosneft, LUKOIL, Surgutneftegaz, Tatneft, Russneft, NOVATEK

** Leverage calculated without data for Surgutneftegaz

Source: ACRA estimates

31 http://www.acra-ratings.com/Sanctions Threaten to Constraint Russian Oil Production in 2020s

New large field commissioning, Russia’s oil production forecast, mln tons / year

aggregated peak production, mln tons / year

47 Bownfiels 2014-2015 Greenfields New Greenfields

44,6 576,5

570,6

570 561,7

547,5 547,6 547,0

32,65 4,7 51,4 61,7

540 534,1 14,8 40,2

24,3

9,4 21,8

24

29,2

510

31,5 31,5 31,2

29,8

13,25

525 521

480

504

491 490 488 485

0

450

2009-2010 2011-2013 2014-2015 2016-2017 2018-2019 2020-2021 2015 2016 2017 2018 2019 2020 2021

After the 2011–2013 hiatus, commissioning of new greenfields ensures growth potential through 2019-2020.

However, these greenfields are the last large conventional oil deposits in the Russian mainland. New incentives will be

required after 2020 for boosting production in both mature and new high production cost fields.

32 Source: ACRA estimates http://www.acra-ratings.com/New Greenfields: Rosneft and Gazpromneft to lead

New large fields commissioning timetable

Bashneft NOVATEK

Field Company Launch year Peak production, mt/y

3% 3%

Northern Chaivo Rosneft 2014-2015 1,6

Labaganskoye Rosneft 2014-2015 1,3 Surgutneftegaz

Srednebotuobinskoye Rosneft 2014-2015 5,0 4%

Imilor LUKOIL 2014-2015 5,0

Prirazlomnoye Gazprom neft 2014-2015 5,0

Novoport Gazprom neft 2014-2015 6,5

Trebs and Titov Bashneft & LUKOIL 2014-2015 4,8 LUKOIL

Yarudeyskoye NOVATEK 2014-2015 3,5 14%

Suzun Rosneft 2016 6,0

Naulskoye Rosneft 2016 2,5

Filanovskoye LUKOIL 2016 6,0

Pyakyakhinskoye LUKOIL 2016 3,5

South Talakan Surgutneftegaz 2016 1,5

Spielman Surgutneftegaz 2016 3,0

East Messoyakha Rosneft

Gazprom neft & Rosneft 2016 5,6

Yurubcheno-Tokhomskoye Rosneft 2017 5,0 Gazprom 58%

Russkoye Rosneft 2017 6,5 neft

Kondinskoe Rosneft 2017 5,0 18%

Taas-Yuriakh (phase 2) Rosneft 2018 5,5

Kuyumba Gazprom neft & Rosneft 2018 6,5

Tagul Rosneft 2018 5,0

Lodochnoye Rosneft 2019 2,0

Erginskoe Rosneft 2019 5,0

Sevostyanova, Sanarsky,

Rosneft 2021 10,0

Lisovsky

Chonsky Gazprom neft 2021 3,25 Source: ACRA estimates

33 http://www.acra-ratings.com/Russian Gas Exports turns to Asia

Russia’s natural gas production forecast, bcm / year Russia’s natural gas exports forecast, bcm / year

600 75% 310

290

500 476 471 470 464 457 13,8

451 70%

432 419 419 270 6,9

400 37

250 30

65% 22

22

300 284 230 15

245 261 15

221 220 235 15

210 217 60%

194 210

200 15

15

190 233 236 239

225 230

55% 218 210

100

170 192 196

0 50% 150

2013 2014 2015 2016 2017 2018 2019 2020 2021 2013 2014 2015 2016 2017 2018 2019 2020 2021

Gazprom

Pipeline exports (excl. China) LNG Exports Exports to China

Independent producers

Gazprom share in Russian gas production

After a record increase in gas production in 2017, the growth rate will slow down and the share growth of independent

producers will resume. Gas production in Russia will grow by 15% (+96 bcm) in 2021 compared to 2016.

The growth in exports after 2017 will mainly be ensured by the launch of LNG projects (Yamal LNG and Third Phase

Sakhalin-2), as well as the beginning of exports to China starting in 2020 via the Power of Siberia.

34 Source: ACRA estimates http://www.acra-ratings.com/Russian Power Industry: Incentives for Modernization

Power plants capacity in Russia

Renewables 1/2 of thermal power plants should

0% be phased out or modernized in

Nuclear the next decade

12%

Russian power market is among the

world largest liberalized electricity

Hydro market in the world.

20%

Russian government is designing new

incentives to raise $17 bln of

Thermal

investments in TPP modernization.

68%

Renewable energy support may not be

extended in 2020s. Renewables lose

competition to cheap conventional

resources (gas).

Source: ACRA estimates

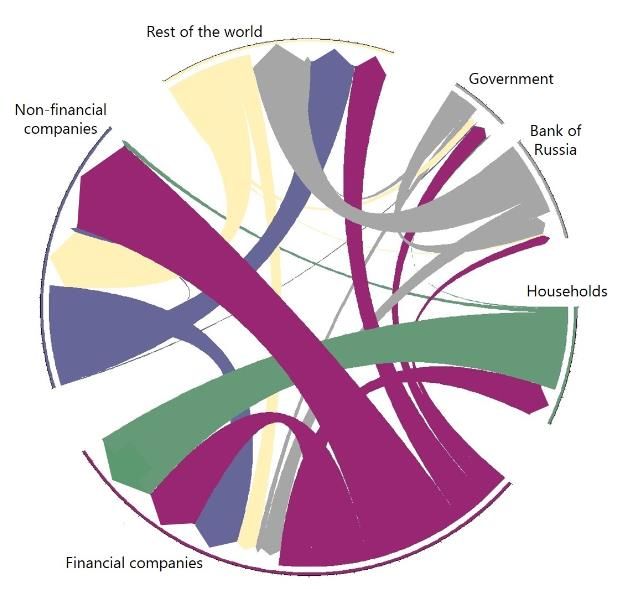

35 http://www.acra-ratings.com/Share of Debt Vulnerable to Sanctions Dropped to 13%

Estimated maximum share of debt assets and liabilities

susceptible to stricter financial sanctions The estimated maximum share of debts

25% due from residents and susceptible to

forced repayment is 13.2%. In the

NFCs Government + worst-case scenario, the liquidity

Bank of Russia constraints may affect 22.4% of debt

20%

assets.

Share of liabilities

15% Sector For non-financial companies (NFCs), the

average role of the rest of the world is

important in terms of both share (46%

10% for assets and 35% for liabilities) and

amount

Financial companies

5% But non-financials are more resilient to

01.01.2014

stricter refinancing conditions, as about

01.07.2017

40% of scheduled repayments fall on

0%

the intragroup debt, which is easy to

0% 10% 20% 30% 40% 50% 60% refinance.

Share of assets

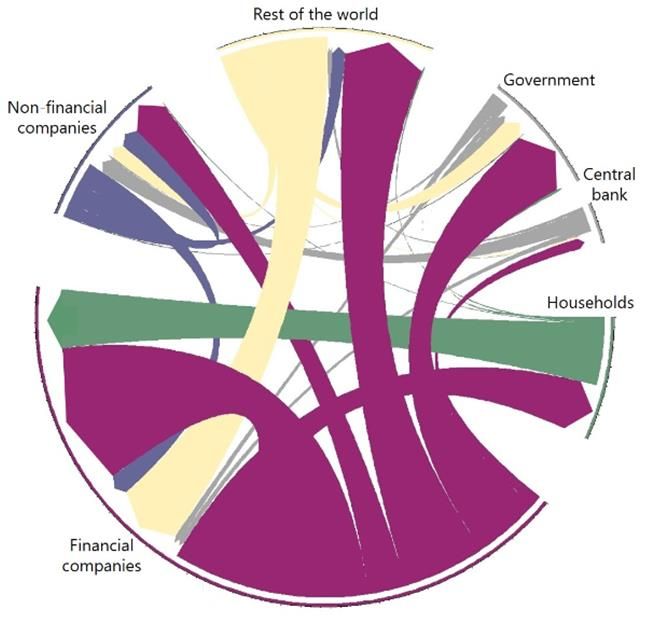

36 Source: ACRA estimates http://www.acra-ratings.com/Internal loans are more than a half of foreign currency debt

Mutual debts “from who-to-whom”

RUB as at 1 July 2017

Other currencies

• Debt relations in the form of loan, borrowing, deposit or debt security (stock, not flow).

• Arrows go from lenders to borrowers (from who-to-whom). Arrow thickness is proportionate to the share

Source: ACRA

of a sector’s debt in the aggregate debt of the economy.

37 http://www.acra-ratings.com/Credit quality has persistent sectoral component

Share of foreign

Bank credit overdue, all currencies currency loans

is higher than Credit risk Industries

Historic NPL

the economy levels

average

Overdue 1. Credit risk is • Utilities

14%

level up Construction materials

way below • Transport infrastructure < 1,9%

Trade average • Telecommunications

12%

Agriculture • Oil & Gas and Chemicals

2. Credit risk is

• Metals 1,9% - 4,6%

below average

10% • Power generation

Food

Services • Defense sector

01.03.2018

8% Construction • Machinery

Wood (1.03.2018 - 19.6% !) • Mining

• Transportation

Machinery 3. Credit risk level • Retail trade

Mining (non-energy) 4,6% - 5,7%

6% is neutral • Agribusiness

Private loans • Packaged food and

Metals beverages

Paper

• Healthcare

4% • IT & Media

Transport and

Chemistry

Other communication

Transport • Real estate

Energy 4. Credit risk is

2% machinery

Processing of raw

Overdue above average

•

•

Paper and forest products

Oilfield services

5,7% – 6,2%

materials Mining (energy) level down

0% 5. Credit risk is • Infrastructure construction

0% 2% 4% 6% 8% 10% 12% way above • Residential construction >6,2%

average • Wholesale trade

01.03.2017

38 Source: ACRA, Bank of Russia http://www.acra-ratings.com/Credit quality pricing in Russia

% 16

Effective YTM of corporate bonds

14

12

10

8

6

4

2

higher than AA-(RU) higher than BBB(RU) higher than B-(RU)

0

01.2016

03.2016

04.2016

05.2016

06.2016

07.2016

08.2016

09.2016

11.2016

12.2016

01.2017

02.2017

03.2017

04.2017

05.2017

06.2017

07.2017

08.2017

09.2017

10.2017

11.2017

12.2017

01.2018

02.2016

10.2016

39 Source: Cbonds http://www.acra-ratings.ru/Russia’s specific economic risks for 2018

Growth lower than Inflation lower than

Sanctions

expected aimed

Sharp growth of

Banking assets

quality, low NIM ? protectionist

measures in global

trade

Non-obvious links

between traditional

OPEC+ agreement US financial markets

markets and

cryptocurrencies etc.

40 Source: ACRA http://www.acra-ratings.com/Russian Financials At A Crossroads

Analytical Credit Rating Agency (ACRA)

Kirill Lukashuk

Senior Director, Head of financial institutions ratings

http://www.acra-ratings.com/Ratings & analytical coverage

Banks & Leasing

Insurers

Funds & AMs

42 http://www.acra-ratings.com/ACRA’s ratings cover 80% of Russian banking system

State-owned banks and FI Private banks Foreign-owned banks

Sberbank AAA(RU) / Stable JSC “ALFA-BANK” AA(RU) / Stable AO Toyota Bank AAA(RU) / Stable

Bank GPB (JSC) AA(RU) / Positive

Vnesheconombank AAA(RU) / Stable Bank RRDB (JSC) AA-(RU) / Stable COMMERZBANK (EURASIJA)

AAA(RU) / Stable

AO

JSC "AHML" AAA(RU) / Stable BANK "ROSSIYA" A+(RU) / Stable Natixis Bank JSC AAA(RU) / Stable

PJSC Sovcombank A(RU) / Stable Credit Agricole CIB AO AAA(RU) / Stable

Bank “National Clearing AAA(RU) / Stable Tinkoff Bank A(RU) / Stable

ING BANK (EURASIA) JSC AAA(RU) / Stable

Centre” (JSC)

JSC Russian Agricultural AA(RU) / Stable CREDIT BANK OF MOSCOW A(RU) / Stable

AO Citibank AAA(RU) / Stable

Bank

RNCB A(RU) / Stable The joint-stock Bank A-(RU) / Stable

JSC Nordea Bank AAA(RU) / Stable

«ROSEVROBANK»

«Bank Otkritie Financial BBB-(RU) / Under revision «Bank «Saint-Petersburg» PJSC A-(RU) / Stable

AO UniCredit Bank AAA(RU) / Stable

Corporation» (PJSC) (positive)

BANK “ROSSIYSKY CAPITAL” BBB+(RU) / Positive Sviaz-Bank BBB+(RU) / Negative

AO Raiffeisenbank AAA(RU) / Stable

(PJSC)

LOCKO-Bank BBB+(RU) / Stable DeltaCredit Bank JSC AAA(RU) / Stable

SDM-Bank PJSC BBB+(RU) / Stable

PJSC ROSBANK AAA(RU) / Stable

Expobank LLC BBB+(RU) / Stable Limited Liability Company

AAA(RU) / Stable

Rusfinance Bank

MCIB Bank LLC BBB(RU) / Stable

JSC «RN Bank» AA(RU) / Stable

CB "Renaissance Credit" (LLC) BBB-(RU) / Stable

Credit Europe Bank Ltd. BBB(RU) / Stable

«AVANGARD» JSB BB+(RU) / Stable

CB "Kuban Credit" Ltd BB+(RU) / Stable

LLC CBED «THE BANK OF KAZAN» BB-(RU) / Stable

43 http://www.acra-ratings.com/Ratings & analytical coverage

Banks & Leasing

Insurers

Funds & AMs

44 http://www.acra-ratings.com/Fragile inputs….

Post-recessionary economic environment suggests growth opportunities to Russian banks…

GDP growth, albeit sluggish (1.5%-2%), will likely continue in 2018

Rebounding private sector consumption will support mortgage/auto/unsecured retail lending

Trade, housing construction and infrastructure sectors will also require new lending

Therefore, banking assets will gradually grow

…But significant problem loans, increasing regulatory pressures and “new normal” in interest rates

prevail

Problem loan levels are at highest levels since 2010 and underprovisioned

ACRA views inflation at around 4% beyond 2017 meaning lower interest rates, shrinking NIM and contained net

income levels in the long term

The CBR insists on higher provisioning charges, introduces additional regulation and continues “to heal” the banking

system

45 http://www.acra-ratings.com/…..major strategic threats

NIM pressure Asset quality Competition

• We expect interest rates • Slowly recovering • Constantly increasing

and inflation to be operational environment power of state-owned and

historically low in next 18- with limited growth state-related banks

36 months potential • Low demand from

• On the back of rates trend • Significant share of corporates due to poor

and ALM structure, we problem loans (15%) performing economy and

assume NIM to drop up to • Low provision coverage strategic uncertainties

100bp (55% system-wide) • Tangible risks of troubled

• Only small number of • Material shift in CBR’s banks privatization

banks are well prepared tolerance towards delaying (5-7 years vs 3 as

and started to actively impairment recognition publicly stated)

invest in fee-related

strategy/products 2-3

years ago

46 http://www.acra-ratings.com/Overall Banking Assets Will Increase

Dynamics of Russian Bank Assets

100% 103% 99%

96% 93% 93% 95%

81%

41% 40% 42% 44%

38% 36% 38%

32%

14% 15% 13% 13% 14% 14% 15% 16%

2013 2014 2015 2016 2017F 2018F 2019F 2020F

Bank assets / GDP Corporate lending / GDP Retail lending / GDP

Despite some recovery in 2017, growth in the banking system assets will be subdued – at around 5%

In 2018–2020, growth in assets will be 5-6% on average, which will support anticipated nominal GDP growth (around 5%

on average)

Nevertheless, the CBR’s tight monetary policy and low-inflationary environment will constrain growth in the banking

assets

47 http://www.acra-ratings.com/Competition dynamics

State-owned banks, market share State-owned banks in TOP-10 banks

75% 95%

70% 90%

70% 90%

65% 63% 85%

82% 82%

61% 81%

60%

60% 80%

55% 75%

2014 2015 2016 2017 2014 2015 2016 2017

2014 2015 2016 2017 2014 2015 2016 2017

The government’s stake in the entire banking system has risen. The above figure has become the highest

among all industries in the Russian market (the government owns 66% of the oil&gas sector).

Competition between government-owned banks for funding sources and borrowers would intensify ever

more, and the reliability factor would become secondary for the competition.

48 http://www.acra-ratings.ru/Competition: State plays the Game

The government’s stake in the entire banking system has risen to 70% by early 2018 vs 63% as at early

2017.

In the TOP 5 there are no private banks, in the TOP 10 there are three (including one foreign sub)

Risks of delaying privatization of failed players and coming of new ones

Active development of the industry-linked state owned banks (Rosselkhozbank, Roskap, PSB, RNCB)

Risks:

• Imperfect management of investments

• Regulatory forbearance

• “directed lending” practices, development of politically important sectors

• State-to-state market model (state corporates - state banks)

• Increased amount of contingent liabilities of the budget and the Bank of Russia in terms of

banking sector support

49 http://www.acra-ratings.ru/Problem Loans Are at a Highest Level Since 2010

12-15%

12

9,5 9,8 Problem loans (ACRA)

10 9,5

8,2 8,3

8 NPL90+ (ACRA)

6,6 6,7 6,7 6,7 6,9

6,2 6 6

5,7

6 Impaired loans (CBR)

4,8 4,5 4,7

4,2

3,8 5,7

4 1+ overdue loans (CBR)

2,5

2

01.01.2009 01.01.2010 01.01.2011 01.01.2012 01.01.2013 01.01.2014 01.01.2015 01.01.2016 01.01.2017 01.07.2017

Problem loan levels in Russian banking system are at around 12–15%

The share of problem loans at the banks’ balance sheets has been growing since 2013

Officially recognized problem loans are highest for the last ten years

Major risks are related to restructured loans and borrowers with weak creditworthiness

50 http://www.acra-ratings.ru/Rated Banks Snapshot

50%

Problem loans vs NPL90+

44%

45%

39%

40%

35% 30%

30%

30%

24%

25% 22%

20%

20% 18% 17%

15% 15% 14%

15% 13%

11% 10% 9%

10% 15% 8%

13% 11% 4%4%

5% 10% 3% 2%1%

8% 8% 8% 8% 7%

0% 5% 6% 6% 4% 4%

2% 2% 4% 4% 2%1% 3% 1%

1% 2% 2% 0%

There are banks (still with a license from CBR), more than a quarter of the assets of which are problem/impaired

The gap between NPLs and problem loans increases with growth problem loans share

Information about the real impairment level in most cases, do not exist in the audited IFRS (Otkritie, B&N – EY)

51 http://www.acra-ratings.ru/Problem loans coverage is not sufficient

Coverage of bad loans by provisions Poor provision coverage of bad loans is

the key risk of creditworthiness decline

A little over half of the bad loans are

provisioned (51.7%)

An one-off recognition of all problem

loans full impairment will lead to a

decrease of capital adequacy levels to

regulatory thresholds

More conservative position of the Bank of

Russia regarding bad loans provisioning

ratio will represent a challenge for credit

institutions in the next 12-18 months

In specific cases it might have an adverse

effect on credit ratings and their outlook

52 http://www.acra-ratings.com/Asset quality indicators: state and private on par

State-owned Privately-owned Subsidiaries of

banks banks foreign banks

Problem loans 11,1% 15,6% 9,5%

NPL90+ 5,5% 6% 6,2%

High-risk industries lending

107,3% 102,8% 30,5%

(% of Tier-1 capital)

Related-party lending

30,7% 27% 1,1%

(% of Tier-1 capital)

Non-core assets

17,8% 10% 0%

(% of Tier-1 capital)

Top-10 borrowers concentration

148,3% 158,6% 174,4%

(% of capital)

53 http://www.acra-ratings.ru/Increasing Risk Appetite Will Contain Capital Adequacy Growth

15% 6,5

13,9%

13,7%

14%

13,3%

6

Problem loan levels will stabilize over the

13%

12,4% 5,5 next 12-18 months, largely thanks to

11,8% 11,7% 11,6%

increasing new lending and improving

12% 11,5% 5

11,6%

11,0%

credit quality of corporate borrowers in

11% 11,4% 4,5 some sectors of economy

10,1%

In case of more aggressive approach to

10% 4

9,20%

9% 3,5 risk appetite, capital adequacy will

stagnate vs. its current level of 11.5%

8% 3

7%

3,2 3,2 3,8 3,6 4,6 4,2 5,3 4,8 6,0 5,3

2,5 Under more “aggressive” scenario, loss

2016 2017 2018 2019 2020

absorption buffer will advance to RUB 5.3

Absorbtion capacity, trln trillion in nominal terms; however, it will

Absorbtion capacity - aggressive scenario, trln

still sustain impairment of assets by 5.9%

Tier-1 (IFRS), %

Tier-1 (IFRS) - aggressive scenario, %

maximum

Н1.2 (CBR), %

54 http://www.acra-ratings.com/NIM Is Recovering, But Will Not Exceed Pre-Crisis Levels

6%

5,6%

5,4%

Significant market volatility in 2014 with further

6% 5,3% decline in loans interest rates outpacing deposits

4,9%

5,0% resulted in weak NIM in 2015

5%

4,6%

4,5% 4,5% NIM growth in 2016 reflected both stabilization of

5%

4,2% loan/deposit interest rates and rebalancing of

interest-earning assets towards higher-income

4% 3,8% instruments

3,6%

4% 3,4%

3,3% 3,3% NIM stabilization (4.5%) is expected in 2017.

3%

Sberbank will continue to outstrip other banks

In 2018, NIM will likely decline to levels posted in

3%

2016

2012 2013 2014 2015 2016 2017 2018 (F)

NIM (IFRS) NIM (IFRS, without Sberbank)

55 http://www.acra-ratings.com/New Normal: Low Inflation, Low Interest Rates, Subdued NIM

20% 17%

Inflation is at historically lowest levels

15% 12,9%

10%

(around 2.5% in October 2017). ACRA

10% 8% 7,25% long-term scenario envisages around 4%,

11,4% 11%

5,5% which is the CBR’s target

5%

6,5%

5,4%

3,2%

4,6% Key rate will be heading towards 7% over

0%

next 12-18 months

2013 2014 2015 2016 2017 (F) 2018 (F)

Inflation CBR Key Rate

20% 18,3%

Retail Deposit Rate (Net Income Will Not Return To The Past

2,0% Following financial crisis, Russian banking

1,7% system net income declined to almost zero

1,5% in 2014-15

1,5%

1,3% 1,2%

Recovery in 2016 was achieved largely

1,0% 1,0% 1,0%

1,0% thanks to Sberbank, while the rest of the

banking system was only marginally

0,5% 0,5% 0,5% profitable

0,5% 0,4%

0,2% Net income will not return to the past. We

0,0% expect rather low profitability metrics with

0,0%

ROA of around 1% in total and around

2012 2013 2014 2015 2016 2017 2018 (F)

0.5% excluding Sberbank

-0,5% -0,4%

Going forward, Russian banks will face

increasing competition for non-interest

-1,0% income sources. Adjustments in operating

ROA ROA without Sberbank expenses will also matter

57 http://www.acra-ratings.com/Regulatory Innovations

Proportional regulatory regime to be introduced since 2018. Small banks are heavily impacted.

The Central Bank will introduce two types of banking licenses:

General license (minimum capital requirement is RUB1 bln). Such banks will have to comply with heightened capital

requirements, Basel III implementation and full-fledged CBR’s supervision.

Basic license (minimum capital requirement is RUB300 mln). Banks with a basic licenses are largely for SME lending in

regions; banned from operations with foreign counterparties (excepting nostro accounts). The CBR exercises simplified

supervision approach.

New legislation on financial rehabilitation of failed banks. The CBR introduces two important financial tools:

“Bail-in” mechanism

The CBR’s Banking Sector Consolidation Fund being responsible for support of troubled banks. The Fund will absorb

toxic assets and recapitalize failed banks (transformation from lending mechanism to equity financing)

ACRA views both instruments positively, albeit their effectiveness to be tested

58 http://www.acra-ratings.com/New mechanism of financial rehabilitation in Russia

Two important financial tools of the CBR

Appropriation Buyout of receivables,

Decision of shares and other

of funds (₽) assets, issuing loans,

BD of CBR

to FBSC allocating deposits

Fund of Banking

“Bail-in”

Sector Consolidation

mechanism (FBSC)

ACRA views both instruments

Shares, loan receivables, other assets

Bank

positively, albeit their of

effectiveness to be tested BSCF Asset Bank

Russia

(CBR) Shares, loan

management

main risks receivables, other company

higher assets (100% subsidiary

further

motivation of

increasing of of CBR)

depositors to

statutory share

allocate funds in

in Russian

state-owned

banking sector

banks After financial rehabilitation shares and assets can be

sold by CBR at public auction

Decrease of competition at the sector New

owner

59 Source: ACRA, Bank of RussiaOtkritie & B&N Bank cases Key implications for investors: size does not matter junior creditors face material risks audited statements is only a well-drawn picture bank goes to default when regulator wants it is not enough to be overliquid to survive 60 http://www.acra-ratings.ru/

Russian leasing market could break the record of 2012-2013

New business volume* dynamics

900 65% 850 70%

770 783 60%

800 741 742

680 50%

700

36% 40%

600 545

30%

500

15% 20%

400

4% 2% 10%

300

0%

200 -13%

-10%

-20%

100 -20%

0 -30%

2011 2012 2013 2014 2015 2016 2017

New leasing volume, RUB bln Growth rate, %

Key market drivers

vehicle lease (+30% of growth in new leasing volume)

aircraft lease (+40%)

rolling stock lease (+70%) Source: ACRA estimates

*volume of new equipment granted by lessors

61 http://www.acra-ratings.ru/Leasing market reform (2018-2021) What’s new for leasing companies: new status for leasing companies – non-credit financial institutions leasing could not be combined with other financial activities capital requirements (min 20 and 50 mln RUB since 2021, depends on lessor’s assets volume) move to IFRS market regulation through self-regulatory organizations new industry standards 62 http://www.acra-ratings.ru/

Ratings & analytical coverage

Banks & Leasing

Insurers

Funds & AMs

63 http://www.acra-ratings.com/Insurance market growth rates to outpace GDP in the medium term

Low penetration of insurance services in Russia will provide

GDP, Insurance market growth rates for high growth rates in the sector

25%

22%

21% Annual market growth expected at 11% within the 2017-

20%

2021 horizon

15%

15% Population aging and monetary policy to support rapid

11% 12%

growth of life insurance. In 2016, the segment posted a

10%

8%

9%

8% phenomenal growth of 66% y-o-y, with the main contributor

7% 7%

being investment life insurance fostered in turn by banks’

5% 4%

active involvement in insurance policy sales and by lower

2%

deposit interest rates

0%

2012 2013 2014 2015 2016 2017-2021

Insurance market, total Non Life GDP nominal Car sales growth to push motor premiums up

64 http://www.acra-ratings.ru/OMTPL and investment insurance risks threaten growth stability

At the same time, the insurance market is facing Life Segment

increasing systemic risks that may undermine expected 250

216

growth rates

200

In the short term, the most pronounced risks are

150

connected with the OMTPL crisis. This segment has so far 130

109

failed to curb the loss-making trend for insurers. 100 85

In the next two to three years, the sector might confront 53

50

the risk of policyholders growing disappointed by

investment life insurance. This may well run the booming 0

2012 2013 2014 2015 2016

life insurance segment into a real shock, should Life total premium, RUR bln.

investment insurance policies bring about weak returns.

65 http://www.acra-ratings.ru/Insurance sector’s RoE is among the highest in the Russian economy

Insurers’ return on equity (RoE) before tax was 24% in 2016

27,7

and 28% in 2015, while the economy average was 13% and

24,1

11%.

19,8

High sector returns are supported by growth in life insurance

15,9 and high effective interest rates that generate income from

14,4

investments. Net loss ratio in the non-life segment declined

11,2 10,9

down to 53% from 61% in 2014–2015

On average, major insurers are more profitable than minor

3,3

companies. This boosts M&A transactions, as companies

strive to increase business efficiency by way of consolidation

2013 2014 2015 2016

Insurance sector ROE, % Banking sector ROE, % ACRA expects insurers’ RoE to decline in the upcoming years,

but RoE is expected to be high enough, for the sector to

remain appealing to investors.

66 http://www.acra-ratings.ru/Ratings & analytical coverage

Banks & Leasing

Insurers

Funds & AMs

67 http://www.acra-ratings.com/Asset management companies

The Russian market of collective investments

6 5,71

5,09

5

4,28

4 3,49

3

2,41

2,10

2 1,49

1,05 0,92 0,98 0,89 0,92 0,92 1,04

1 0,76 0,77

0

2014 2015 2016 2017, 2q

Total market NSPF' pension savings NSPF' pension reserves Closed-end mutual investment funds

General trend is the market growth. The growth basis – NSPF’ pension savings

The market volume of closed-end mutual investments funds and NSPF’ pension reserves – stagnation at 1 trillion and

800-900 billion rubles respectively

ACRA sees some potential in open-ended mutual investment funds and individual asset management because of

lower interest rates on banks deposits

Other assets of Russian collective investments market have barely changed in 2 years

68 http://www.acra-ratings.ru/Non-state pension funds (1)

40

Private pension provision participants overall decrease in

34,4

the number

29,8

30 Distrust in Russian Federation’ pension system due to

26,3

frequent legislative changes and weak financial literacy

22,1

Often the low quality of private pension provision assets

20

The use of “administrative leverage”, forcing a person to

engage in private pension provision

10 The insured persons has a trend to increase the number

6,4 5,8 5,3 5,6

The transfer of insured persons funds from Pension Fund of

Russia to NSPF because of the transition from accumulative

0

2014 2015 2016 2017, 2q pension component to individual pension capital

Insured persons number (pens. savings)

Private pension provision participants number (pens. reserves)

Units: millions of people

69 http://www.acra-ratings.ru/Non-state pension funds (2)

The overall growth of the Russian pension system: from 3.9 6

trillion rubles in 2014 to 5.4 trillion rubles in second quarter

5

1,2

of 2017 1,1

1,0

4

The NSPF’ pension savings growth rate is ahead of the same 0,9

of Pension fund of Russia (PFR): an average of 8.6% in NSPF 3

1,7

2,1 2,4

revised -0.6% in PFR 1,1

2

In 2016 there was a significant moment for entire Russian

1 1,9 2,1 2,0 1,8

pension industry – the total volume of NSPF’ pension savings

ahead the PFR’ pensions savings 0

2014 2015 2016 2017, 2q

The NSPF’ pension reserves grow steadily by an average of NSPF' pension reserves

NSPF' pension savings

2.3% in the quarter Pension Fund of Russia's pension savings

Units: trillions of rubles

70 http://www.acra-ratings.ru/Contact Details

Russian website: www.acra-ratings.ru

English website: www.acra-ratings.com

АКРА Рейтинговое агентство

General Contacts: On Cooperation Issues:

info@acra-ratings.ru Managing Director for Business Development

+7 495 139 04 80 Alexey Bogomolov

75, Sadovnicheskaya emb., alexey.bogomolov@acra-ratings.ru

Moscow, 115035, Russia +7 495 139 04 99

Regulatory Affairs & Compliance: Credit Ratings Methodology:

Manager Senior Director

Anastasia Morgunova Kirill Lukashuk

anastasia.morgunova@acra-ratings.ru kirill.lukashuk@acra-ratings.ru

+7 495 139 04 80, ext. 151 +7 495 139 04 82

71 http://www.acra-ratings.com/Disclaimer (С) 2018 Analytical Credit Rating Agency (Joint-Stock Company), ACRA (JSC) 75, Sadovnicheskaya embankment, Moscow, Russia www.acra-ratings.com The Analytical Credit Rating Agency (ACRA) was founded in 2015, with its 27 shareholders representing major Russian corporate and financial institutions and its authorized capital exceeding RUB 3 bln. ACRA’s main objective is to provide the Russian financial market with high-quality rating products. Methodologies and internal documents of ACRA are developed in compliance with the Russian legislation and with regard to global rating industry best practices. The provided information, including, without limitation, credit and non-credit ratings, rating assessment factors, detailed credit analysis results, methodologies, models, forecasts, analytical reviews and materials, as well as other information placed on the ACRA website (further referred to as Information), coupled with the ACRA website software and other applications, are intended for information purposes only. Information must not be modified, reproduced or distributed by any means, in any way or form, either in whole, or in part, in marketing materials, as part of public relations events, in news bulletins, in commercial materials or reports without a prior written consent from, and reference to, ACRA. Any use of Information in violation of these requirements or the law is prohibited. ACRA credit ratings reflect ACRA’s opinion about the ability of a rated entity to meet its financial obligations or about the credit risk of individual financial obligations and instruments of a rated entity at the time of publication of the relevant Information. Non-credit ratings reflect ACRA’s opinion about certain non-credit risks assumed by interested parties interacting with a rated entity. The assigned credit and non-credit ratings reflect all material information pertaining to a rated entity and known by ACRA (including the information received from third parties), the quality and reliability of which ACRA considers appropriate. ACRA shall not be responsible for the accuracy of information provided by clients or relevant third parties. ACRA does not audit or otherwise verify the provided data and shall not be held responsible for their accuracy and completeness. ACRA conducts rating analysis of information provided by customers using its own methodologies, with the texts thereof available on ACRA’s website – www.acra- ratings.com/criteria. The only source that reflects the latest Information, including the one about credit and non-credit ratings assigned by ACRA, is ACRA’s official website – www.acra-ratings.com. Information is provided on an "as is" basis. Information shall be considered by users exclusively as ACRA’s statement of opinion and must not be regarded as advice, recommendation or suggestion to buy, hold or sell securities or other financial instruments of any kind, nor shall it be viewed as an offer or advertisement. Neither ACRA, nor its employees and persons affiliated with ACRA (further referred to as the ACRA Parties) provide any direct or implied guarantee expressed in any form or by any means regarding the accuracy, timeliness, completeness or applicability of Information for making investment and other decisions. ACRA does not act as a fiduciary, auditor, investment or financial advisor. Information must be regarded solely as one of the factors affecting an investment decision or any other business decision made by any person who uses ACRA’s information. It is essential that each of such persons conduct their own research and evaluation of a financial market participant, as well as an issuer and its debt obligations that may be regarded as an object of purchase, sale or possession. Users of Information shall make decisions on their own, involving their own independent advisors, if they deem it necessary. ACRA Parties shall not be responsible for any action taken by users based on Information provided by ACRA. ACRA Parties shall under no circumstances be responsible for any direct, indirect or consequential damages or losses resulting from interpretations, conclusions, recommendations and other actions taken by third parties and directly or indirectly connected with such information. Information provided by ACRA is valid only as of the date of preparation and publication of materials and may be amended by ACRA in the future. ACRA shall not be obliged to update, modify or supplement Information or inform anyone about such actions, unless the latter was recorded separately in a written agreement or is required by the legislation of the Russian Federation. ACRA does not provide advisory services. ACRA may provide additional services, if this does not create a conflict of interest with rating activities. ACRA and its employees take all reasonable measures to protect all confidential and/or material non-public information in their possession from fraud, theft, unlawful use or inadvertent disclosure. ACRA provides protection of confidential information obtained in the course of its business activities as required by the legislation of the Russian Federation. 72 http://www.acra-ratings.com/

You can also read