Standard Life Private Equity Trust plc (SLPET) - Aberdeen Standard Investments

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

‘Title slide + image’

slide layout

January 2020

Standard Life Private

Equity Trust plc (SLPET)

Analyst & Shareholder presentation

This presentation is for one-on-one use with institutional investors and professional investors only and should not be distributed to or relied upon by retail clients.

1. Executive Summary 1

Standard Life Private Equity Trust plc

• A portfolio of high-conviction private equity managers, built from years of strong

High relationships and independent research

Conviction

• Over 60% of Net Asset Value (‘NAV’) to 14 core private equity managers1

• European mid-market focus, but with increasing international diversification

Disciplined • Active management with an over-commitment strategy, utilising co-investments

and the secondary market

• Current dividend yield of 3.6%2

Cash • £67.7m liquid resources3 + £100m unutilised credit facility

Generative

• Unique flat fee of 0.95% on NAV

• Deliver strong, long-term total returns for shareholders through capital gain and

Performance dividend yield

• Share price outperformed public equity markets over 1, 3, 5 and 10 years4

Notes: 1. As at 30 September 2019, Aberdeen Standard Investments. 2. Based on proposed full year dividend to 30 September 2019 and 30 September 2019 share price. 3. Includes cash and other liquid assets available for

investment. 4. Public equity markets indices refer to FTSE All Share (£), source: Thomson Reuters.

2 Past performance is no guide to future returns

2. Manager Overview

ASI Private Markets

Significant global presence offering extensive access to private markets opportunities

We have +400 professionals across 21 locations managing £64 billion across private markets.

This allows us to source opportunities for clients on a global scale and makes us one of the top ten private markets managers worldwide.1

Olso Helsinki

Stockholm

Edinburgh Copenhagen

London Amsterdam

Paris Frankfurt

Boston

New York Stamford Madrid Brussels Seoul Tokyo

Havana

Hong Kong

Bogota

Singapore

Private Equity

Infrastructure

Real Estate

Private Credit

Sydney

Natural Resources

Source: Aberdeen Standard Investments, as at 30 September 2019. 1: Willis Towers Watson Global Alternatives Survey 2017

4

Private equity capabilities

Experienced team providing access to best performance areas of private equity

Leveraging our large and connected team, networks and research capabilities

AUM: Professionals: Fund commitments: SLPET Manager:

> £12bn 41 1,000+ > 18 years

Capabilities: Ranging from early stage venture through growth and buy out capital

Office locations

Edinburgh

London

Boston Stamford

New York

As at 30 September 2019 Source: Aberdeen Standard Investments. AUM is calculated as NAV + Unfunded

5

SLPET Team and Senior Investment Resource

SLPET investment team and senior management team with an average industry experience of 20 years

SLPET Team

Alan Gauld, Patrick Knechtli, Mark Nicolson, Simon Tyszko, Ramone Moody,

Investment Director Head of Secondaries Head of Primaries Investment Manager Investment Analyst

Edinburgh Edinburgh Edinburgh Edinburgh Edinburgh

Senior Private Equity Team

Merrick McKay, Head of Private Equity Europe Kevin Carey, Senior Investment Director Mark Nicolson, Head of Primaries

Edinburgh/London London Edinburgh

Europe

Colin Burrow, Head of Co-investments Guy Eastman, Senior Investment Director Alistair Watson, Senior Investment Director

Edinburgh London Edinburgh

Patrick Knechtli, Head of Secondaries Cameron Graham, Senior Investment Director Sarah Farrell, Senior Investment Director

Edinburgh Edinburgh London

USA

Scott Reed, Co-Head of Private Equity USA John Dickie, Co-Head of Private Equity USA Eric Albertson, Senior Investment Director

Boston Boston Boston

Wider Investment Team SLPET Governance

• Global primary, secondaries and co-investment teams • Quarterly SLPET Board Meetings

• Provides broad market coverage and sourcing capability • SLPET Portfolio Management Committee

• Supported by Private Markets legal and back office teams • European Investment Committee process

• In-house Listed Private Equity expertise • Pipeline review and cash flow monitoring

Source: Aberdeen Standard Investments, as at 30 June 2019.

6

3. Why SLPET?

A differentiated offering

• A carefully selected range of private equity managers, built from • Consistent track record of selecting top performing managers

years of established relationships and proprietary research and funds

• One of the most concentrated listed private equity offerings, with • 75% / 66% of our investments fall within top or second

SLPET’s top 10 fund investments representing over 50% of quartile from a TVPI2 and IRR perspective, respectively3

portfolio NAV1

Over 60% portfolio NAV to

14 core managers… … which has led to superior returns

10% 13%

15%

21%

70%

50%

42%

35%

33% 31%

TVPI IRR

Top Second Third Fourth

Source: 1. Aberdeen Standard Investments, 53.9% portfolio NAV at 30 September 2019; excludes offerings which invest exclusively in affiliate or “in-house” funds 2. TVPI defined as Total value over paid in capital, representing

the return multiple of capital invested, net of management fees and carried interest; IRR defined as Internal rate of return 3. Source: Burgiss, data from 2007 – 2017 as at 30 June 2019. © owned by each of the

corporate entities named in the respective logos

8Core European mid-market focus

• We are committed to our European mid-market focus, with an • Highly selective exposure to differentiated US mid-market

attractive mix of pan-European and regional managers managers

• We selectively continue to evaluate top performing, hard-to-access

opportunities in the European lower mid-market and large cap /

global managers

Over 80% portfolio NAV to … with selective non-European exposure

European managers… that leverages ASI’s global platform

Large cap / global

US mid–market

Europe

US

US lower mid–market

Global

Notes: Figures at 30 September 2019. © owned by each of the corporate entities named in the respective logos. Companies selected for illustrative purposes only

to demonstrate Aberdeen Standard Investments’ investment management style and not as an indication of performance

9Leveraging the ASI private equity platform

Knowledge sharing is key to the platform

Secondary

• High quality deal flow

Idea Knowledge

Generation • Network Sharing

• GP relationships

• Manager selection

• Direct experience

• Active investor

Primary Co-investments

Reinforcing

Relationships

10Targeted deployment backing leading private equity managers

SLPET’s recent commitments demonstrate our selective

focus to the best performing managers…

2015 2016 2017 2018 2019

Secondary sale of

selected fund interests

… and active use of the secondary and co-investment market to

assist portfolio construction and cash utilisation

Notes: © owned by each of the corporate entities named in the respective logos. Companies selected for illustrative purposes only to demonstrate Aberdeen Standard Investments’ investment management style and not as an indication

of performance. Logo inside a dashed box represents a co-investment

11Disciplined investing

• Review a broad range of established private equity managers • “Best in class” in terms of geography, sector specialisation,

• Leveraging global presence to unlock opportunities investment strategy, value creation and deal sourcing

• Full due diligence process irrespective of track record and • Demonstrated the changing mix of our core manager group

relationship

Total primary pipeline >100 opportunities SLPET opportunities reviewed – 21 Commitments made in 2019 – 7

Core Manager Example Matching SLPET criteria

• Defensible – consistently strong performance

throughout the cycle

• Sourcing – Strong market position in the Nordic

mid-market

• Geographic focus – DACH and Nordic • Focus on operational change – Active owner

• Market segment – Mid-market

driving value creation through improving key

operational metrics

• Sector – Generalist • Experienced team – lessons learnt during the

global financial crisis

Notes: © owned by each of the corporate entities named in the respective logos. Companies selected for illustrative purposes only to demonstrate Aberdeen

Standard Investments’ investment management style and not as an indication of performance

12Sustainable dividend underpinned by robust long-term performance

• SLPET is committed to maintaining the current dividend of • Long-term outperformance against the FTSE All Share index

12.8 pence per share in real terms

• Dividends underpinned by strong realisations at the underlying

• 3.6% dividend yield ahead of peer group average of 2.1%1 portfolio and future expected realisations

SLPET share price and dividend yield

400 4.0%

350 3.5%

300 3.0%

250 2.5%

Pence

200 2.0%

150 1.5%

100 1.0%

50 0.5%

0 0.0%

Sep 2012 Sep 2013 Sep 2014 Sep 2015 Sep 2016 Sep 2017 Sep 2018 Sep 2019

Share price (price) Dividend yield (%)

Notes: Thomson Reuters Datastream. Dividend per share is based on proposed full year dividend to September 2019

Notes: 1. Based on proposed full year dividend to 30 September 2019 and 30 September 2019 share price.

13 Past performance is no guide to future returns4. Performance Highlights

Overview of SLPET Performance

UK Listed Investment Trust

£710.1m

Net assets

High-conviction investor in leading private equity funds

+5.7%1 Long-term outperformance against listed markets

12 month share price

total return

Robust balance sheet with strong cash generation from the portfolio

+10.5%1 Enhanced dividend policy with an attractive yield of c. 3.6%

12 month NAV

total return

Unique flat rate fee of 0.95% on NAV

+8.9%

Since inception share price

annualised total return

+10.2%

Since inception NAV

annualised total return

Notes: 1. NAV and share price performance as at 30 September 2019. Total return includes re-invested dividends.

15 Past performance is no guide to future returnsSLPET Highlights for the 12 months to 30 September 2019

Net Asset Value per ordinary share

(“NAV”) NAV Share price

growth1 growth

461.8p (2018: 430.2p)

Net Assets +10.5% +5.7%

£710.1m (2018: £661.4m)

(2018: 13.5%) (2018: 5.8%)

Market cap 12 month total return

12 month total return

£541.2 million (2018: £531.2m)

Share price Proposed full year Management fee

352.0p (2018: 345.5p)

dividend

0.95% (2018: 0.95%)

12.8p (2018: 12.4p) of NAV

Yield 1.09% (2018: 1.10%)

23.8%2 (2018: 19.7%) Ongoing charged

Discount to net asset value 3.6%3 (2018: 3.6%) ratio

Notes: 1. Total return includes re-invested dividends. 2. As at 30 September 2019. 3. Based on proposed full year dividend to 30 September 2019.

16 Past performance is no guide to future returnsSLPET performance against peers

• Robust NAV performance versus peers across multiple time periods.

• With the exception of the 1 year time period, SLPET’s NAV performance (annualised NAV total return) has been strong in

comparison with peers

• In addition, SLPET offers a 3.6% dividend yield, which is above the peer group average1

NAV performance compared to peer group

20%

18%

16%

Annualised performance

14%

12%

10%

8%

6%

4%

2%

0%

1 year 3 years 5 years 10 years Since

inception

SLPET Pantheon ICG BMO HarbourVest

Source: ASI PE, Thomson Reuters Datastream

Notes: 1. Peer group includes BMO; ICG Enterprise; Harbourvest GPE; Pantheon International.

17 Past performance is no guide to future returnsRobust Balance Sheet

Strong balance sheet in line with peer group1 Prudent over commitment strategy

• Liquid resources of £67.7m (10.8% of portfolio NAV)2 • Outstanding commitments less liquid resources: 43% of

Fund NAV3 (long term target of 30-75%)

• £100m revolving credit facility available for short term

liquidity requirements • £450.2m outstanding commitments (of which £62.0m is

unlikely to be called)

Outstanding commitments

35% 500 76% 80%

450

450

70%

30%

400 388

369

60%

25% 350 326

47%

306

50%

As a % of NAV

300 43%

20%

£ million

246

250 228 40%

214

15% 31%

200 179

25% 30%

150 22% 23%

10% 150 126 129

18%

20%

14%

100

5% 14% 10%

50

1% 1%

0% 0 0%

Cash balance as % portfolio NAV Facility as % portfolio NAV Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep Sep

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Outstanding commitments Commitments in excess of liquid resources as a % of Fund NAV

SLPET ICG Enterprise BMO Harbourvest Pantheon

Notes: 1. Source: available annual reports and factsheets, data as at at 30 September 2019 2. Includes cash and other assets available for investment. 3. Over commitment ratio reduces to 40% following increased debt facility of

£100m agreed post-30 September 2019

Past performance is no guide to future returns

18Summary – a differentiated opportunity

The Standard Life Private Equity Trust provides exposure to:

• A diversified portfolio of leading private companies

• A carefully selected range of private equity managers, built from years of established relationships and

proprietary research

• Investments principally focused on European mid-market private companies

With the objective of delivering strong, long-term total returns for Shareholders through a

combination of capital growth and a progressive dividend.

19Appendix 1: Private Equity Overview

Benefits of investing in Private Equity

Private Equity Value Creation Model

Proactive sourcing and Growing profits through Introducing leverage A transformed

acquisition of businesses increased revenue and to enhance returns business

improved efficiency

• Investing in Private Equity can generate high risk-adjusted returns

• Enables investors to access companies closed to listed-only investors

• Broader universe of opportunities – c. 5 times as many private companies versus listed

• Private equity is an investment style enabling alpha generation through

longer-term orientation

information advantage

less efficient markets

corporate governance / active ownership

better alignment of interests

control over exit

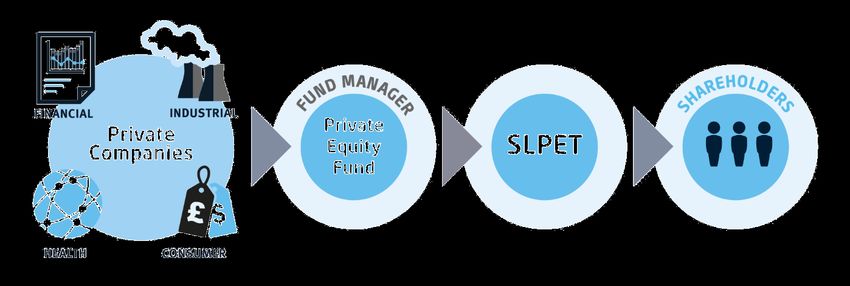

21Attractions of the SLPET model

Listed Private Equity Value Chain

• Liquid access to an illiquid asset class

• Long-term outperformance vs listed markets

• No private equity ‘J-curve’ via open-ended, evergreen structure

• No up front or exit fees associated with traditional private funds

• Historically SLPET has been a pure fund selector with no direct investments. New co-investment

programme leverages ASI’s existing platform to add diversification and reduce management fee expenses.

• Stable dividend yield and NAV growth

22Showcasing SLPET at work: Past and current portfolio companies © owned by each of the corporate entities named in the respective logos. Companies selected for illustrative purposes only to demonstrate Aberdeen Standard Investments’ investment management style and not as an indication of performance. 23

Private Equity market dynamics

Global private equity dry powder: buyout European buyout dry powder

$500bn

$200bn

$400bn $160bn

Dry Powder

$300bn $120bn

Dry Powder

$200bn $80bn

$40bn

$100bn

$0bn

$0bn 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 YTD Nov-

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 YTD Nov- 19

19

US Buyout Europe Buyout Asia/RoW Buyout Small (< $750m) Mid ($750m - $2.5bn) Large ($2.5bn - $5bn) Mega ($5bn+)

• Global private equity dry powder has reached record heights of • European buyout dry powder reached $184bn in November

$1.25tn as of November 2019, of which $728bn is targeted at 2019, slightly less than the dry powder in 2018 but well above

buyouts and $517bn at venture/growth. that available at the prior peak ($146bn in December 2009).

• The majority of buyout dry powder is targeted at the US, which • Despite the overall market trend, dry powder for funds less than

stands at $465bn for buyout funds. This is 120% above the post- $5bn in size has been relatively consistent since 2007, as the

crisis low point in 2012 and 55% above its previous peak in 2008. fund size expansion below $5bn and new entrants into the

European buyout dry powder is also at record levels, having market are offset by those GPs moving beyond $5bn in fund

reached $184bn at August 2019, however, expansion has been size.

slower than in the US and is currently at 75% above the post-crisis

low point in 2012 and 30% above its previous peak in 2008.

Source: Preqin, data as at 30 November 2019

24Private Equity market dynamics

European deal value and volume European deal value

€60bn 600 100%

90%

€50bn 500

80%

70%

€40bn 400

60%

50%

Volume

€30bn 300

Value

Value

40%

€20bn 200 30%

20%

€10bn 100

10%

0%

€0bn 0 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1

H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 2012 2013 2014 2015 2016 2017 2018 2019

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

< €100m €100m - €1bn €1bn+ Buyout Volume < €100m €100m - €1bn €1bn+

• European buyout activity has increased overall following the 2009 • Activity increasingly dominated by large cap deals

trough, growing in value and volume by 19% and 11% CAGR • Over 50% value in deals over €1bn in value (measured

respectively through to 2018. by company’s Enterprise Value)

• 2018 activity was particularly active, with total transaction value • 30% within SLPET’s sweet spot of mid-sized transactions

surpassing all previous periods post-crisis.

• Activity in the large/mega buyout space has been more subdued

since the peak in the 2005-2007 period; however, this segment

showed a spike in activity in H1 2018, driving full-year values.

Source: Preqin, data as at 30 November 2019. For illustrative purposes only.

25SLPET discount and secondary market trading

• During 2019 SLPET’s discount ranged from 9.2% to its • High quality private equity funds continue to trade at, or a

current level of 23.5%1 premium to NAV

• 1-year average moving average discount of 20.0% • Slight dip in marketing pricing from 97% at December 2018

to 95% at June 2019

• Clear spread between SLPET pricing and that of the

secondary private equity market, despite the SLPET

secondary portfolio being of high quality

Share price premium / (discount) to NAV Secondary pricing as a percentage of NAV

15% 120%

110%

10%

100%

5%

Share price premium / (discount)

90%

Pricing as a percentage of NAV

0%

80%

-5% 70%

-10% 60%

50%

-15%

40%

-20%

30%

-25%

20%

-30% 10%

-35% 0%

Jan 2019 Apr 2019 Jul 2019 Oct 2019 Jan 2020 Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec Dec

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

SLPET Pantheon ICG BMO HarbourVest % of NAV (SLPET) % of NAV (Secondaries)

Source: Thomson Reuters Datastream

Source: SL Capital, Thomson Reuters Datastream, Greenhill Secondary Market Update & Outlook

Notes: Data as at 31 December 2019. Source: Aberdeen Standard Investments, Thomson Reuters Datastream.

26 Past performance is no guide to future returnsAppendix 2: SLPET Portfolio

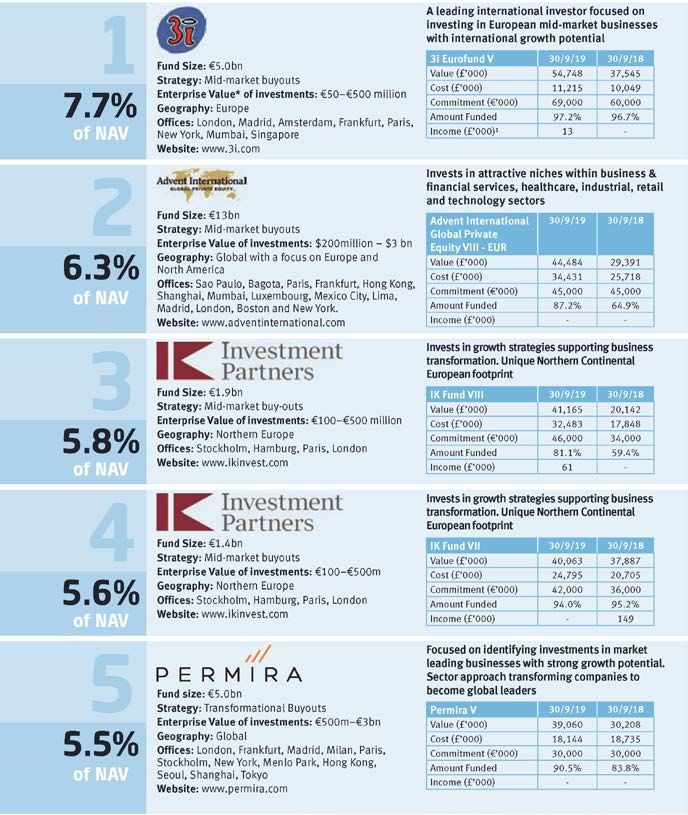

SLPET Portfolio Largest 10 private equity funds – 53.9% Total Fund NAV Notes: Aberdeen Standard Investments, 30 September 2019. © owned by each of the corporate entities named in the respective logos. Companies selected for illustrative purposes only to demonstrate Aberdeen Standard Investments’ investment management style and not as an indication of performance 28

SLPET Portfolio Largest 10 underlying companies – 16.7% Total Fund NAV Notes: Aberdeen Standard Investments, 30 September 2019. © owned by each of the corporate entities named in the respective logos. The figures shown above are based on gross valuations, before carry provision. In the exceptional case of Action the Manager has estimated Action's as a % of NAV, net of carry provision. 29

SLPET Portfolio Geographic location of underlying investments Notes: Aberdeen Standard Investments, 30 September 2019 30

SLPET Portfolio Sector exposure and holding period of underlying investments Notes: Aberdeen Standard Investments, 30 September 2019 31

Portfolio valuation multiples – top 50 investments

Enterprise value/EBITDA Multiple of enterprise value / EBITDA

10

• The top 50 private companies that represent 50% of the net

asset value at 30 September 2019 (being the most recent 8 7

data) had a median EV / EBITDA multiple of 13.1x. 6

6 5 5 5 5

Count

• Those valued at a multiple of greater than 15x are generally 4 4 4

private companies that have strategic value. These 4

businesses are growing strongly in highly rated sub-sectors 2

(e.g. software, medical technology). Higher valued 2 1

companies include Action and Teamviewer 0

0

< 8x 8x - 9x 9x - 10x 10x - 11x 11x - 12x 12x - 13x 13x - 14x 14x - 15x 15x - 16x 16x - 17x 17x - 18x > 18x

EV / EBITDA Multiple

Current Investments Exited Investments - Not Listed Exited Investments - Listed

Net debt/EBITDA Top 50 underlying portfolio companies as at 30 June 2019

In the case of 2 investments, it has not been possible to calculate meaningful multiples due to the nature of the underlying businesses.

• Median Net Debt / EBITDA in the portfolio at 4.8x was

Multiple of net debt / EBITDA

consistent with the prior period. The private equity 18 16

managers in the portfolio are generally prudent in relation to 16

14

the capital structures of their underlying companies.

12 10

• Whilst leverage can be relatively high (>5x EBITDA),

Count

10

optically high multiples often relate to highly cash 8 6

generative businesses. 6

5 5

4

4

• Both metrics are in line with the private equity market for 2

2

similar sized deals and vintages.

0

< 2x 2x - 3x 3x - 4x 4x - 5x 5x - 6x 6x - 7x > 7x

Net Debt / EBITDA Multiple

Current Investments Exited Investments - Not Listed Exited Investments - Listed

Top 50 underlying portfolio companies as at 30 June 2019.

In the case of 2 investments, it has not been possible to calculate meaningful multiples due to the nature of the underlying businesses.

Notes: Aberdeen Standard Investments, 30 June 2019

32Underlying portfolio – growth rates

LTM sales and EBITDA growth

• The underlying portfolio has exhibited strong average revenue and EBITDA growth of over 10% from 2017 – 2019.

LTM Sales and EBITDA growth

20% 20%

18% 18%

LTM Sales and EBITDA growth (%)

16%

16% 16%

14% 14%

12% 12%

12% 11% 12%

10%

10% 11% 10%

8%

8% 8%

6% 6%

4% 4%

2% 2%

0% 0%

Jun 2016 Jun 2017 Jun 2018 Jun 2019

LTM sales growth LTM EBITDA growth

Data sourced from average growth rates across portfolio companies at underlying private equity funds

Notes: Aberdeen Standard Investments, 30 June 2019

33Appendix 3: Costs

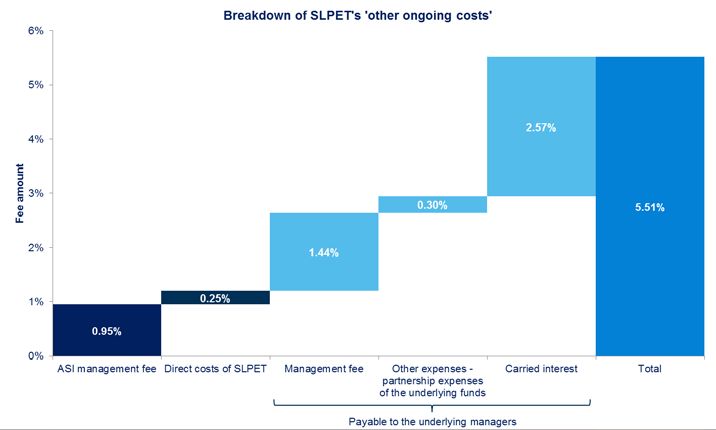

SLPET costs compared to peers

• Current NAV is net of ongoing costs

• Fees and carry already priced into secondary transactions

• Most significant element is underlying carried interest – only

payable when underlying funds generate strong

performance

Fund of Funds Direct

Costs SLPET ICG BMO Pantheon HarbourVest HgCapital

Entry costs 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

One-off costs

Exit costs 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Portfolio transaction costs 0.03% 0.13% 0.06% 0.05% 0.00% 0.20%

Ongoing costs

Other ongoing costs 5.51% 3.22% 3.36% 3.89% 1.89% 2.10%

Performance fees 0.00% 0.00% 0.53% 0.00% 0.00% 0.00%

Incidental costs

Carried interests 0.00% 2.68% 0.00% 0.00% 0.80% 2.00%

Total 5.54% 6.03% 3.95% 3.94% 2.69% 4.30%

Notes: As at 1 January 2019 for SLPET, source: Aberdeen Standard Investments. Peer group data as at 1 January 2018, source: Key Information Document (KID)

35Appendix 4: Current Shareholders 36

Current Shareholder Constituents

• Large investor base of over 150 shareholders. Largest shareholder is Phoenix Group, with c. 56% shareholding1

• Remaining investor base is diverse with a mixture of asset managers (Blackrock, L&G) and smaller retail investors via

platforms (Hargreaves Lansdown, FundsDirect)

No. of shares at

No. Name % of shares 30-Nov-19

(m)

1 Phoenix Group Holdings 56.37% 86,661,475

2 Quilter Cheviot Investment Management 5.97% 9,179,047

3 Oxfordshire CC PF 3.03% 4,658,684

4 Hargreaves Lansdown, stockbrokers (EO) 2.63% 4,037,044

5 Charles Stanley 2.45% 3,769,014

6 Interactive Investor (EO) 2.41% 3,708,150

7 Smith & Williamson Wealth Management 1.75% 2,691,529

8 Scottish Enterprise PF 1.74% 2,670,482

9 Legal & General Investment Management 1.55% 2,376,585

10 LGT Capital Partners 1.50% 2,303,617

11 AJ Bell, stockbrokers (EO) 1.05% 1,613,776

12 BlackRock 0.93% 1,430,108

13 EFG Harris Allday, stockbrokers 0.81% 1,241,885

14 Transact (EO) 0.77% 1,189,672

15 Rathbones 0.76% 1,160,813

16 Red Rocks Capital 0.74% 1,135,999

17 Mr David Currie 0.73% 1,116,696

18 Brewin Dolphin, stockbrokers 0.71% 1,085,435

19 Alliance Trust Savings 0.69% 1,068,201

20 Credit Suisse Private Banking 0.68% 1,040,000

Total 87.25%

Notes: Aberdeen Standard Investments, 30 November 2019

37Appendix 5: Discrete performance

Discrete performance

Annual total return (annualised) 1 year 3 years 5 years 10 years Since Inception

SLPET NAV +10.5% +13.2% +15.2% +12.7% +10.2%

SLPET Share Price +5.7% +13.8% +12.6% +14.6% +8.9%

FTSE All Share Index +2.7% +6.8% +6.8% +8.3% +5.6%

Discrete Performance 30 Sep 19 30 Sep 18 30 Sep 17 30 Sep 16 30 Sep 15

SLPET NAV +10.5% +13.8% +15.3% +25.0% +12.1%

SLPET Share Price +5.7% +5.8% +31.9% +28.0% -4.0%

FTSE All Share Index +2.7% +5.9% +11.9% +16.8% -2.3%

Notes: Net performance data as at 30 September 2019. Discrete performance shown as 12 month periods to 30 September 2019. Source: Aberdeen Standard Investments, Thomson Reuters Datastream.

39 Past performance is no guide to future returnsImportant information The value of investments, and the income from them, can go down as well as up and investors may get back less than the amount invested. Past performance is not a guide to future results. An investment in this Company is subject to market, currency, over- commitment and liquidity risks. Investors should review the relevant Key Information Document (KID) prior to making an investment decision. These can be obtained free of charge from www.slpet.co.uk or by writing to SL Capital Partners LLP, 1 George Street, Edinburgh, Scotland, United Kingdom, EH2 2LL The information in this document is confidential and may not be reproduced or redistributed in whole or in part without the prior written consent of Standard Life Investments (Private Capital) Limited (“SL Capital”). Recipients of this document acknowledge that unauthorised disclosure of the information in this document may give rise to significant loss to SL Capital and/or its affiliates and civil liability for the discloser. Nothing in this document constitutes a direct or indirect offering or placement by SL Capital (or by any other person) of interests, units or shares in any alternative investment fund or in any other fund, entity or undertaking. Any such offering or placement would only be made where, among other conditions, all required regulatory consents, authorisations and approvals to such offering or placement have been obtained. There is no guarantee that any such offering or placement will be made. No future decision to invest in any fund which may be established to participate in the investment opportunity contemplated in this document should be made other than on the basis of the constitutional documents of such fund. While the information set out in this document has been prepared in good faith, no representation or warranty is given, and no responsibility is accepted, by SL Capital or its affiliates (or by any of their respective officers, employees or agents) in relation to its accuracy or completeness and any such liability is expressly disclaimed. All opinions and estimates in this document are those of SL Capital, and constitute SL Capital’s best judgement as of the date of this document (or, if different, as of the date indicated in this document). The information is only as current as the date of this document (or, if different, the date indicated), and may be superseded by subsequent market events or for other reasons. Statements concerning market trends are based on current market conditions, which may fluctuate. References to future returns are not promises or even estimates of actual returns that may be achieved, and should not be relied upon. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation. In addition, any forecasts are based upon subjective estimates and assumptions about circumstances and events that may not yet have taken place or may never do so. Any investment in any fund which may be established would be speculative, would involve significant risk and would only be suitable for sophisticated investors who have sufficient experience and knowledge to make their own evaluation of the merits and risks of an investment in such fund. In particular, the investment objective of any such fund may not be achieved and an investment in any such fund would only be suitable for investors who are able to bear a substantial loss of investment and for whom the illiquid nature of the investment is suitable. If a fund is established to participate in the investment opportunity contemplated in this document, a more detailed explanation of the material risks associated with an investment in such fund will be set out in an investor disclosure document issued by SL Capital. Prospective investors in any such fund should ensure that they read that document and understand the nature of the investment and the extent of their exposure to risk in making an investment in such fund. Prospective investors will be required to determine for themselves the suitability of an investment in any fund which may be established in light of their own circumstances and seek such professional advice as they may require. Prospective investors must not treat the content of this document or any subsequent communications from SL Capital or any of its affiliates as advice relating to legal, taxation, accounting, regulatory, investment or other matters. No person has been authorised to give any information or make any representations not contained in this document and, if given or made, such information or representations may not be relied upon as having been made or given with the authority of SL Capital. No responsibility is accepted by SL Capital or any of its affiliates or by any other person in respect of any such information or representations. Aberdeen Asset Managers Limited, registered in Scotland (SC108419) at 10 Queen’s Terrace, Aberdeen, AB10 1XL. Standard Life Investments Limited registered in Scotland (SC123321) at 1 George Street, Edinburgh EH2 2LL. Both companies are authorised and regulated in the UK by the Financial Conduct Authority. Calls may be monitored and/or recorded to protect both you and us and help with our training. © 2019 Standard Life Aberdeen, images reproduced under licence D/H GB-270619-92397-2 40

You can also read