State of Banking Industry & Implications for Commercial Real Estate

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

State of Banking Industry & Implications for

Commercial Real Estate

DORY A. WILEY, CPA, CVA, CFA

Managing Partner and Portfolio Manager

Mr. Wiley is a co-founder of Commerce Street Capital, LLC, and currently serves as President and

CEO. Mr. Wiley has 20 years of experience in the commercial banking, investment banking and

investment management, focused primarily on the financial services sector. He previously served

as President of SAMCO Capital Markets, Inc., which he joined in 1996. He also serves as Portfolio

Manager of Service Equity Partners, LP; Genesis Bank Fund, LP; and Commerce Street Income

Partners, LP. Additionally, Mr. Wiley:

• Previously served on the Board and Investment Committee of Independent Bankers Capital

Fund.

• Previously managed the Financial Institutions Group of Rauscher Pierce Refsnes (now RBC

Capital Markets).

• Is an appointed Trustee of the Teachers’ Retirement System of Texas, an $80 billion public

pension plan, and chairs the Alternative Assets Committee.

• Is a Certified Public Accountant, a Chartered Financial Analyst as well as a Certified Valuation

Accountant and holds multiple securities licenses.

• Received a BBA in Finance and Accounting from Texas Tech University and an MBA from

Southern Methodist University.

2

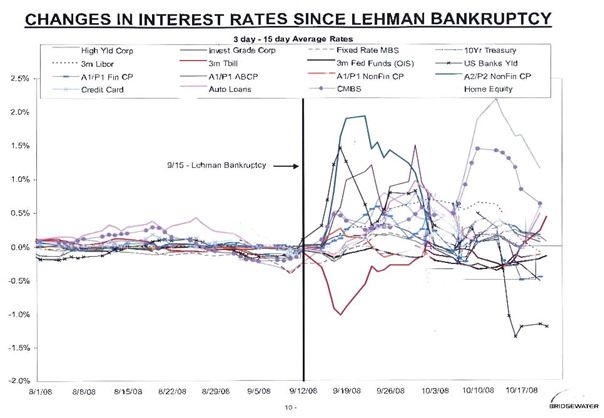

Lehman havoc

3

Customary Train Wreck Slide…

4

Consequences of Delevering

Defaults Decreasing Credit Supply Inability to Borrow

Lower Aggregate Demand Higher Cost of Capital

Lower Asset Prices Deflation

5

The large cap sector will suffer enormous additional losses

Credit cards, personal loans, auto loans, and to a certain extent, prime mortgages are

likely to produce

sizeable losses for larger financial institutions

These banks in the US and Europe have high exposure to bad assets with increased

leverage US Banks’ Level 3 Assets European Banks’

Europe’s (Multiple

bank of Market

leverage is currently Leverage

Cap)38x compared to 21x for the USRatios

5

4.6x

4.5 4.3x

4

3.5 3.3x

Citigroup

3

2.5

2

2.0x

1.5 1.2x

1 0.8x

0.5

0

Morgan Merrill Goldman JP Bank of

Stanley Citi Lynch Sachs Morgan America

Sources: Greed & Fear, 08 January 2009, 09 October 2008, European Central Bank November 2008

6Will TARP be enough?

7Bank and Thrift failures

Failures reached historic lows

1995 – 2007: 58 bank failures (annual failure rate of 0.042%)

2005 – 0 failures

2006 – 0 failures

2007 – 3 failures

2008 – 25 failures

2009 – 37 failures to date

Causes for Concern

Significant real estate exposure – primarily single family and construction

exposure in deteriorating markets

“Hot” funding, i.e. high levels of brokered deposits over core funding

Low tangible equity ratios

Similar Situation

1987 – 1991: 1,940 bank and thrift failures

Peaked in 1989 with 586 failures

Source: FDIC

8Sector analysis

Banking Market

8,400 Total Banks

(100) Largest Banks

(252) Problem Banks

8,000+ Non Problem Banks

Key Market Statistics

% of Total

Number Market

Banks with Positive Earnings 6,400 76.79%

Banks NPAs/Total Assets < 1% 4,279 51.34%

Banks with Real Estate Loans/Total Loans < 50% 1,190 14.28%

Banks with Capital > 8 % 4,951 59.41%

Source - Chart 1) FDIC as of February 2009; Chart 2) SNL as of 12/31/2008

9How does this market compare?

10“Even worse than the Great Depression?”

The S&P has fallen 56.4% in 513 days which means it will need a 17% recovery to match the Great

Depression

The Great Depression lasted 997 days so we are half way through this bear market!

Hopefully new leadership can reverse the trend but stocks are down 28.4% since the election

Source: SmartMoney Even worse than the Great Depression”, March 6, 2009

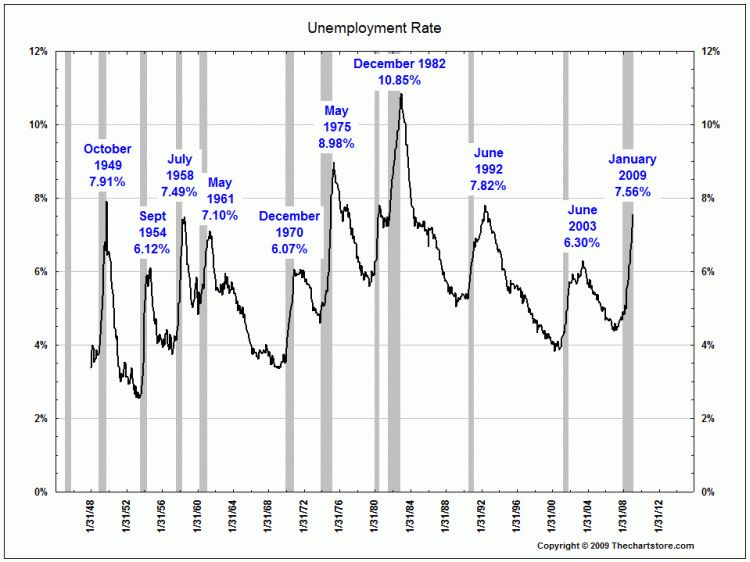

11Unemployment by recession

12Wealth destruction

Real Estate losses have spread into other sectors such as equities, pension, and mutual funds

Estimates show 20% of US wealth had been destroyed by the end of 2008 Q4

Household wealth has already incurred half the percentage loss as the Great Depression

At 2008 year end, US wealth destruction was believed to be approximately $13 trillion

Source: Merrill Lynch,8 January 2008; Economicdata 2008

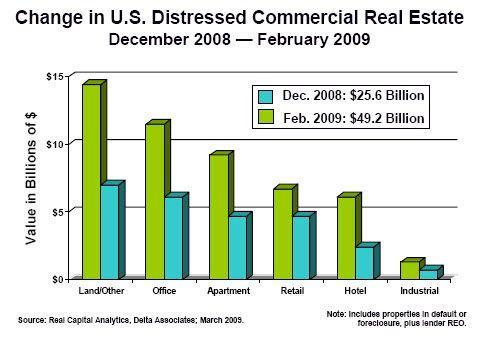

13Commercial real estate could cause further pain

More than 35% of banks have CRE portfolios that exceed 300% of risk-based capital, according to SNL's call report

data.

Commercial real estate can be a liability but it has a more manageable downside. However, unlike consumer loans

such as credit cards, commercial loans usually have notable collateral attached to them, which limits loss levels.

Charge-offs went from 1.77% of average loans to 2.65% mainly due to commercial financial and commercial

agricultural real estate.

More concerning is the demand for commercial real estate has taken a plunge in the 1st quarter. Originations for

hotel properties was down 88%, retail properties fell 76%, and office properties were down 66% according to

Mortgage Bankers Association.

Unemployment is currently at 8.9% and many economists think it will approach 10% which would increase

foreclosing rates which are already 32.25% higher in April than the year before.

Commercial real estate losses under the stress test will hurt larger regional banks such as: Fifth Third Bancorp

(13.9%), Regions Financial Corp (13.7%), KeyCorp (12.5%), PNC Financial Services Group Inc.(11.2%) and U.S.

Bancorp (10.2%).

Source: SNL Financial, LP, “CRE shoe has yet to drop — and may not”, Kevin Dobbs May 14,2009

14Banks, lenders, asset managers taking losses

Selected Bank Writedowns/Losses - $501 billion

Writedowns & Losses and Capital Raised

Writedowns Capital Writedowns Capital

Firm & Losses Raised Firm & Losses Raised

Citigroup 55.1 49.1 E*Trade 3.6 2.4

Merrill Lynch 51.8 29.9 Nomura Holdings 3.3 1.1

UBS 44.2 28.3 Natixis 3.3 6.7

HSBC 27.4 3.9 Bear Stearns 3.2 -

Wachovia 22.5 11.0 HSH Nordbank 2.8 1.9

Bank of America 21.2 20.7 Landesbank Sachsen 2.6 -

IKB Deutsche 15.3 12.6 UniCredit 2.6 -

Royal Bank of Scotland 14.9 24.3 Commerzbank 2.4 -

Washington Mutual 14.8 12.1 ABN Amro 2.3 -

Morgan Stanley 14.4 5.6 DZ Bank 2.0 -

JPMorgan Chase 14.3 7.9 Bank of China 2.0 -

Deutsche Bank 10.8 3.2 Fifth Third 1.9 2.6

Credit Suisse 10.5 2.7 Rabobank 1.7 -

Wells Fargo 10.0 4.1 Bank Hapoalim 1.7 2.4

Barclays 9.1 18.6 Mitsubishi UFJ 1.6 1.5

Lehman Brothers 8.2 13.9 Royal Bank of Canada 1.5 -

Credit Agricole 8.0 8.9 Marshall & Ilsley 1.4 -

Fortis 7.4 7.2 Alliance & Leicester 1.4 -

HBOS 7.1 7.6 U.S. Bancorp 1.3 -

Societe Generale 6.8 9.8 Dexia 1.2 -

Bayerische Landesbank 6.4 - Caisse d'Eparagne 1.2 -

Canadian Imperial 6.3 2.8 Keycorp 1.2 1.7

Mizuho Financial Group 5.9 - Sovereign Bancorp 1.0 1.9

ING Group 5.8 4.8 Hypo Real Estate 1.0 -

National City 5.4 8.9 Gulf International 1.0 1.0

Lloyds TSB 5.0 4.9 Sumitomo Mitsui 0.9 4.9

IndyMac 4.9 - Sumitomo Trust 0.7 1.0

WestLB 4.7 7.5 DBS Group 0.2 1.1

Dresdner 4.1 - Other European Banks 7.2 2.3

BNP Paribas 4.0 - Other Asian Banks 4.6 7.8

LB Baden-Wuerttemberg 3.8 - Other U.S. Banks 2.9 1.9

Goldman Sachs 3.8 0.6 Other Canadian Banks 1.8 -

Total 501.1 352.9

Source: Bloomberg, 9/4/08

15Insights and Outlooks

Incoming President Ronald Reagan stated in his 1981 inaugural address that “In

this present crisis, government is not the solution to our problem; government is

the problem.” The mood today couldn’t be more different.

Outlook

Reducing any deflation is the main concern of policymaker’s monetary goals

A real concern of prevalent wage decline

Recovery of equity and credit markets tends to occur in the middle of recessions, not the end

Risk asset prices are likely to have discounted much of the economic damage

If deflation occurs, a dollar of debt that is unpaid becomes a bigger dollar

Source: J.P. Morgan Asset Management, Ins and Outs January 5 2009

16How deep is the hole?

17Fed’s “More Adverse” Stress Test Case Assumptions

Loan Type Loss Rate %

First lien mortgages 8.5

Closed-end junior lien mortgages 25.0

Home equity lines of credit (HELOC) 11.0

Commercial and industrial loans 8.0

Construction and land development loans 18.0

Multifamily loans 11.0

Commercial real estate loans (nonfarm, nonres) 9.0

Credit card loans 20.0

Other consumer loans 12.0

Other loans 10.0

Source: Federal Reserve’s overview of stress test results

18Fed CRE stress tests

The Federal Reserve warns that 19 leading US Banks could face $53 billion in CRE losses.

Due to the risk premium and the cost of debt going up paired with the amount of leverage going down

some forecasts predict CRE causing another 20% decline in addition to the 30% already experienced.

The Federal Reserve has calculated an adverse stress test that would cause those 19 banks to lose 9% of

their $600 billion CRE portfolio.

CRE that has been hit hard already include: shopping malls, apartments, office buildings, and industrial

parks.

Source: Financial Times, May 9, 2009

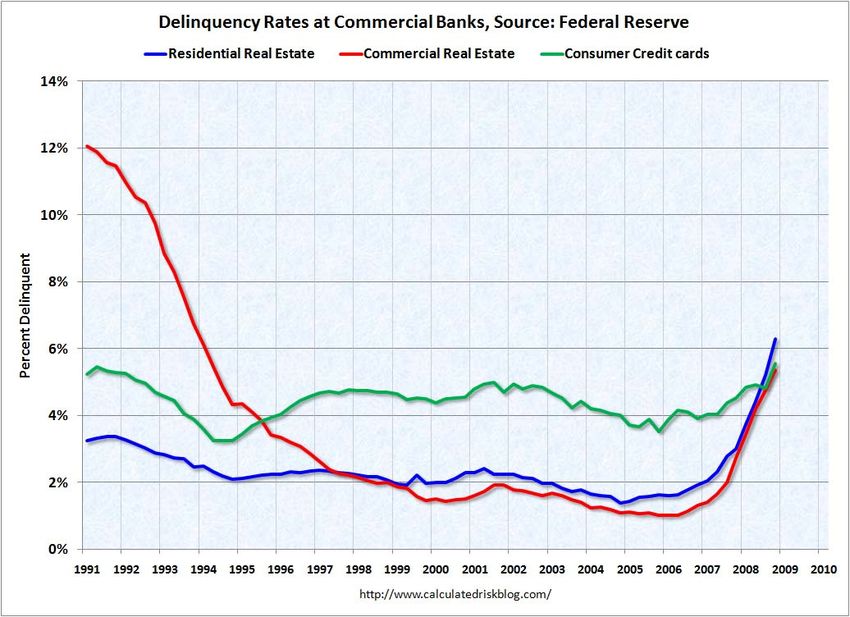

19Will CRE delinquency return to historic levels?

20Disturbing trend

21CMBS REITs Liquidity Crunch

With no capital from credit and equity markets, CMBS investors are focused on deleveraging and

managing credit in existing portfolios, and we see “Going Concern” warnings in quarterly reports of some

CMBS REITs.

However, pricing rallied significantly in April and May, primarily in AAA-rated tranches, but with some

increases in subordinated tranches.

The Federal Reserve’s Term Asset-Backed Securities Loan Facility (TALF) was recently expanded to

include newly-issued CMBS, and then further expanded to include qualified senior tranches of legacy

CMBS.

The FED said, “The extension of eligible TALF collateral to include legacy CMBS is intended to promote

price discovery and liquidity for legacy CMBS. The resulting improvement in legacy CMBS markets should

facilitate the issuance of newly issued CMBS, thereby helping borrowers finance new purchases of

commercial properties or refinance existing commercial mortgages on better terms.

Government intervention should ideally be a short-term solution, but should help to encourage private

investors to come back to the market.

Source: SNL

22The Texas market

23Loan composition changes in 1st Quarter 2009

Source: Seeking Alpha

242009 Forecast

Recession will enter trough

Continued rise in unemployment

Deleveraging occurs through shrinking assets and growing equity

Price discovery of financial assets

Mortgage market will begin to clear at lower prices

Increase in industry consolidation

Continued government intervention

A return to more normalized valuation

Sources: Keefe, Bruyette & Woods

25You can also read