THE DAILY BRIEF MARKETUPDATE MONDAY,08MARCH2021 GLOBAL MARKETS - CAPRICORN ASSET MANAGEMENT

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Daily Brief Market Update Monday, 08 March 2021 Global Markets Share markets turned mixed on Monday as the U.S. Senate passage of a $1.9 trillion stimulus bill augured well for faster global economic growth, but also put fresh pressure on Treasuries and tech stocks with lofty valuations. The upbeat economic news continued as China's exports surged 155% in February compared with a year earlier when much of the economy shut down to fight the coronavirus. "With the Senate's passage, we expect growth momentum to accelerate and forecast global GDP growth will surge to a 7.5% annualised rate in the middle quarters of the year," said JPMorgan economists in a note. "Every $1 trillion of fiscal stimulus adds around $4-$5 to EPS, implying 6-7% upside for the remainder of the year." However, analysts also expected a sharp acceleration in inflation, stoked in part by the latest spike in oil prices, which was pushing up bond yields and stretching equity valuations, particularly in the high tech space. That saw Nasdaq futures reverse early gains to slip 1.0%, dragging S&P 500 futures down 0.2%. MSCI's broadest index of Asia-Pacific shares outside Japan followed with a fall of 0.5%, while

Chinese blue chips shed 0.9%. Japan's Nikkei clung to a gain of 0.2%, while EUROSTOXX 50 futures were still up 0.8% and FTSE futures 0.9%. Equity investors had taken heart from U.S. data showing nonfarm payrolls surged by 379,000 jobs last month, while the jobless rate dipped to 6.2% in a positive sign for incomes, spending and corporate earnings. U.S. Treasury Secretary Janet Yellen tried to counter inflation concerns by noting the true unemployment rate was nearer 10% and there was still plenty of slack in the labour market. Yet yields on U.S. 10-year Treasuries still hit a one-year high of 1.625% in the wake of the data and stood at 1.59% on Monday. Yields increased a hefty 16 basis points for the week, while German yields actually dipped 4 basis points. The European Central Bank meets on Thursday amid talk it will protest the recent rise in euro zone yields and perhaps mull ways to restrain further increases. The diverging trajectory on yields boosted the dollar on the euro, which fell away to a three-month low of $1.1892, and was last pinned at $1.1904. BofA analyst Athanasios Vamvakidis argued the potent mix of U.S. stimulus, faster reopening and greater consumer firepower was a clear positive for the dollar. "Including the current proposed stimulus package and further upside from a second- half infrastructure bill, total U.S. fiscal support is six times greater than the EU recovery fund," he said. "The Fed is also supportive with U.S. money supply growing two times faster than the Eurozone." The dollar index duly shot up to levels not seen since late November and was last at 92.057, well above its recent trough of 89.677. It also gained on the low-yielding yen, reaching a nine-month top of 108.63, and was last changing hands at 108.41. The jump in yields has weighed on gold, which offers no fixed return, and left it at $1,705 an ounce and just above a nine-month low. Oil prices were up the highest levels in more than a year after Yemen's Houthi forces fired drones and missiles at the heart of Saudi Arabia's oil industry on Sunday, raising concerns about production. Prices had already been supported by a decision by OPEC and its allies not to increase supply in April. Brent climbed $1.44 a barrel to $70.80, while U.S. crude rose $1.36 to $67.45 per barrel.

Domestic Markets

South Africa's rand was set for a weekly loss of more than 2% against the dollar on Friday, as higher

bond-market borrowing costs and a rising dollar sapped risk appetite. Stocks ended higher, led by

petrochemical firm Sasol's 14% surge.

At 1725 GMT the rand was 0.13% weaker at 15.3350 against the dollar, trimming losses after hitting

a near eight-week low of 15.4100 earlier in the session. The currency was on track to post losses of

2.2% since Monday.

The currency rallied to a 2021 peak of 14.3950 last week on fiscal consolidation plans laid out by

South Africa's finance minister, but it has struggled to gain further as soaring U.S. bond yields sapped

enthusiasm for risk currencies worldwide.

The latest bout of volatility was sparked when U.S. Federal Reserve Chairman Jerome Powell on

Thursday showed little alarm about the rise in yields.

"Emerging market currencies have felt the pinch globally as the U.S. Dollar reminded currency

markets of its power as the world's reserve currency," said DailyFX analyst Warren

Venketas. Powell's speech on Thursday failed to put concerns over rising yields at ease which could

lead to the detriment of the rand in the short to medium-term, Venketas added.

South African government bonds have also been hit. The yield on the benchmark 2030 government

issue added 18 basis to 9.320%, its highest level since October.

In the stock market, the Top-40 index closed 0.87% higher at 62,788, while the broader all-share was

up 0.78% at 68,271. Shares in Sasol were boosted by oil prices, which jumped more than 3% after

OPEC and its allies agreed not to increase supply in April as they await a more substantial recovery in

demand.

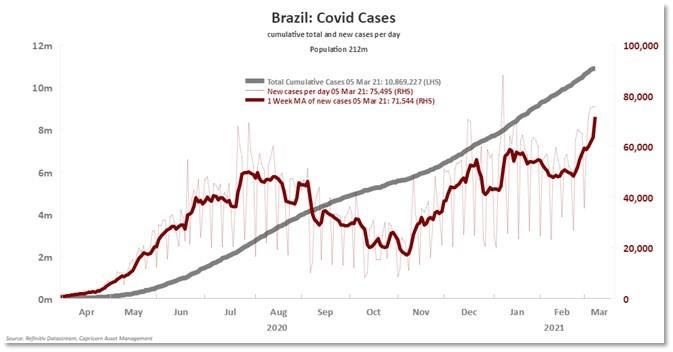

Corona Tracker

The number of new cases is distorted by cut-off times.

Source: Thomson Reuters

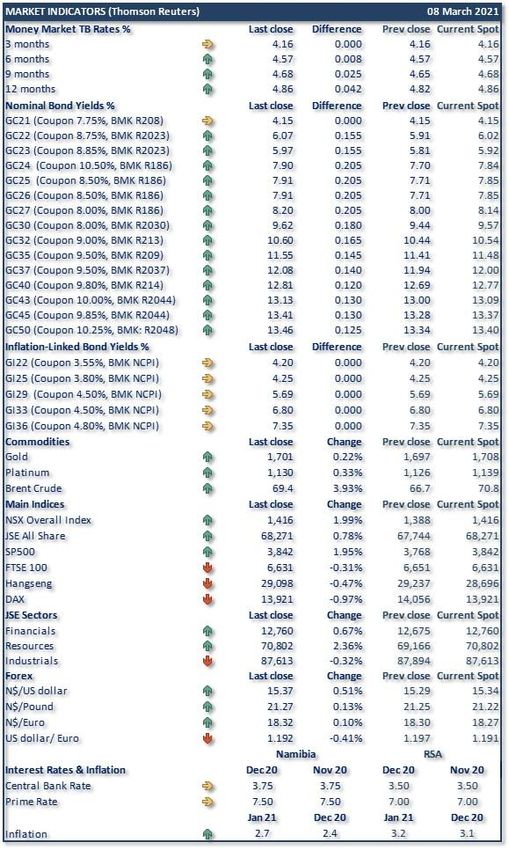

Market Overview

Notes to the table:

The money market rates are TB rates

“BMK” = Benchmark

“NCPI” = Namibian inflation rate

“Difference” = change in basis points

Current spot = value at the time of writing

NSX is a Bloomberg calculated Index

Important Note:

This is not a solicitation to trade and CAM will not necessarily trade at the yields and/or prices

quoted above. The information is sourced from the data vendor as indicated. The levels of and

changes in the yields need to be interpreted with caution due to the illiquid nature of the domestic

bond market.

Source: Bloomberg

For enquiries concerning the Daily Brief please contact us at

Daily.Brief@capricorn.com.na

Disclaimer

The information contained in this note is the property of Capricorn Asset Management (CAM). The

information contained herein has been obtained from sources which and persons whom the writer

believe to be reliable but is not guaranteed for accuracy, completeness or otherwise. Opinions and

estimates constitute the writer’s judgement as of the date of this material and are subject to change

without notice. This note is provided for informational purposes only and may not be reproduced in

any way without the explicit permission of CAM.You can also read