THE DAILY BRIEF MARKETUPDATE WEDNESDAY,13JANUARY2021 GLOBAL MARKETS - CAPRICORN ASSET MANAGEMENT

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

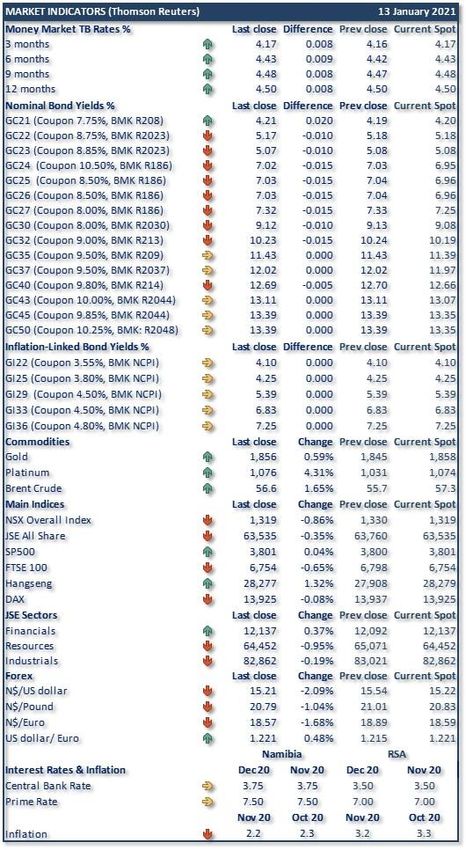

The Daily Brief Market Update Wednesday, 13 January 2021 Global Markets Stocks rose on Wednesday, tracking modest Wall Street gains, as expectations that a vaccine will eventually win the battle against the coronavirus fuelled recovery hopes, while tight supply expectations pushed oil prices to a one-year high. MSCI's broadest index of Asia-Pacific shares outside Japan rose 0.45%. Chinese shares rose 0.34% while South Korea's KOSPI gained 0.04%. Japan's Nikkei 225 rose 0.49%, but Australia's S&P/ASX 200 bucked the regional trend and slipped 0.12%. U.S. stock futures edged up 0.15%. Treasuries extended their rally in Asian trading, which pulled benchmark 10-year yields further away from the highest in almost a year and caused the yield curve to flatten slightly. Investors were betting that the incoming Biden administration would ramp up U.S. distribution of coronavirus vaccines, which would allow large parts of the U.S. economy to reopen, said Peter Essele, head of portfolio management at Commonwealth Financial Network in Boston. "The amount of pent-up demand is slowly being unwound and over the next year it is probably going to result in one the strongest growth in 20 years and markets are pricing that in," Essele said. "Right now, it's a

race between cases and the vaccine and the vaccine will ultimately win out and the curve will flatten out." On Wall Street, stocks fluctuated near unchanged for the session, not far from record highs. The Dow rose 0.19%, the S&P 500 gained 0.04% and the Nasdaq Composite added 0.28%. U.S. West Texas Intermediate (WTI) rose 0.81% to $53.64 a barrel, reaching the highest since February after a larger-than-expected decline in U.S. crude inventories. Brent crude rose 0.87% to $57.07. Oil prices were also supported after Saudi Arabia said it plans to cut output by an extra 1 million barrels per day in February and March. Some investors were monitoring developments in Washington after at least three Republicans said they would join Democrats in a vote expected Wednesday to impeach President Donald Trump over the attack on the U.S. Capitol. With seven days remaining in his term in office, Trump faces impeachment over accusations that he incited insurrection in a speech to his followers last week before hundreds of them stormed the Capitol, leaving five dead. Trump says his speech was appropriate. An impeachment trial could proceed even after Trump leaves office on Jan. 20, but analysts say they don't expect any further political turmoil in Washington to affect markets. "Markets since the election have been quite strong because uncertainty factor has been removed," Essele said. Yields on benchmark 10-year U.S. government debt fell to 1.1120% on Wednesday in Asia, down from an almost one-year high of 1.1870% reached in the previous session after a well-received auction of new 10-year notes. The yield curve, which had reached the steepest since May 2017 on expectations for big fiscal stimulus under a new Democratic administration, narrowed slightly to 96.6 basis points. The dollar nursed losses on Wednesday as a retreat in U.S. yields snuffed out its recent rebound. Against the yen, the greenback fell 0.18% to 103.58. The dollar also edged lower to $1.3679 against the British pound. Safe-haven spot gold added 0.28% to $1,860.51 an ounce. Domestic Markets The South African rand recovered on Tuesday, bouncing off a two-month low hit in the last session, as a recent rally in the dollar cooled. At 1510 GMT, the rand traded at 15.3975 versus the dollar, 0.85% firmer than its previous close. The currency has tumbled more than 5% since the beginning of 2021. Emerging market assets have been under pressure in the last week from continued dollar strength and U.S. higher yields, which are seen as negative. Sentiment also soured badly over a new peak in daily coronavirus infections and doubts over South Africa's vaccine supplies. "This afternoon, the rand has pierced the R15.40/USD level, ignoring the announced essential lack of change in South Africa's lockdown restrictions last night, and instead attempting to move stronger as global risk aversion wanes somewhat," Annabel Bishop of Investec said in a note. President Cyril Ramaphosa late on Monday said that the country had secured 20 million doses of COVID-19 vaccines, which would be delivered mainly in the first half of the year. South Africa has recorded more than 1.2 million COVID-19 cases and more than 33,000 deaths, the most on the African continent, but is yet to start its vaccination drive. Ramaphosa, however, said the cabinet had decided to maintain "level 3" lockdown restrictions, with relatively minor tweaks.

Stocks on the Johannesburg Stock Exchange (JSE) reversed some gains in the first fall since the

beginning of the year, as rising coronavirus cases and the continued lockdown hurt sentiment. The

benchmark FTSE/JSE all-share index dropped 0.35% to end the day at 63,535 points, while the

bluechip FTSE/JSE top 40 companies index ended down 0.38% to 58,493 points.

Government bonds firmed, with the yield on the 2030 instrument 2.5 basis points lower at 8.810%.

Corona Tracker

The number of new cases is distorted by cut-off times.

Source: Thomson ReutersMarket Overview

Notes to the table:

The money market rates are TB rates

“BMK” = Benchmark

“NCPI” = Namibian inflation rate

“Difference” = change in basis points

Current spot = value at the time of writing

NSX is a Bloomberg calculated Index

Important Note:

This is not a solicitation to trade and CAM will not necessarily trade at the yields and/or prices

quoted above. The information is sourced from the data vendor as indicated. The levels of and

changes in the yields need to be interpreted with caution due to the illiquid nature of the domestic

bond market.

Source: Bloomberg

For enquiries concerning the Daily Brief please contact us at

Daily.Brief@capricorn.com.na

Disclaimer

The information contained in this note is the property of Capricorn Asset Management (CAM). The

information contained herein has been obtained from sources which and persons whom the writer

believe to be reliable but is not guaranteed for accuracy, completeness or otherwise. Opinions and

estimates constitute the writer’s judgement as of the date of this material and are subject to change

without notice. This note is provided for informational purposes only and may not be reproduced in

any way without the explicit permission of CAM.You can also read